Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

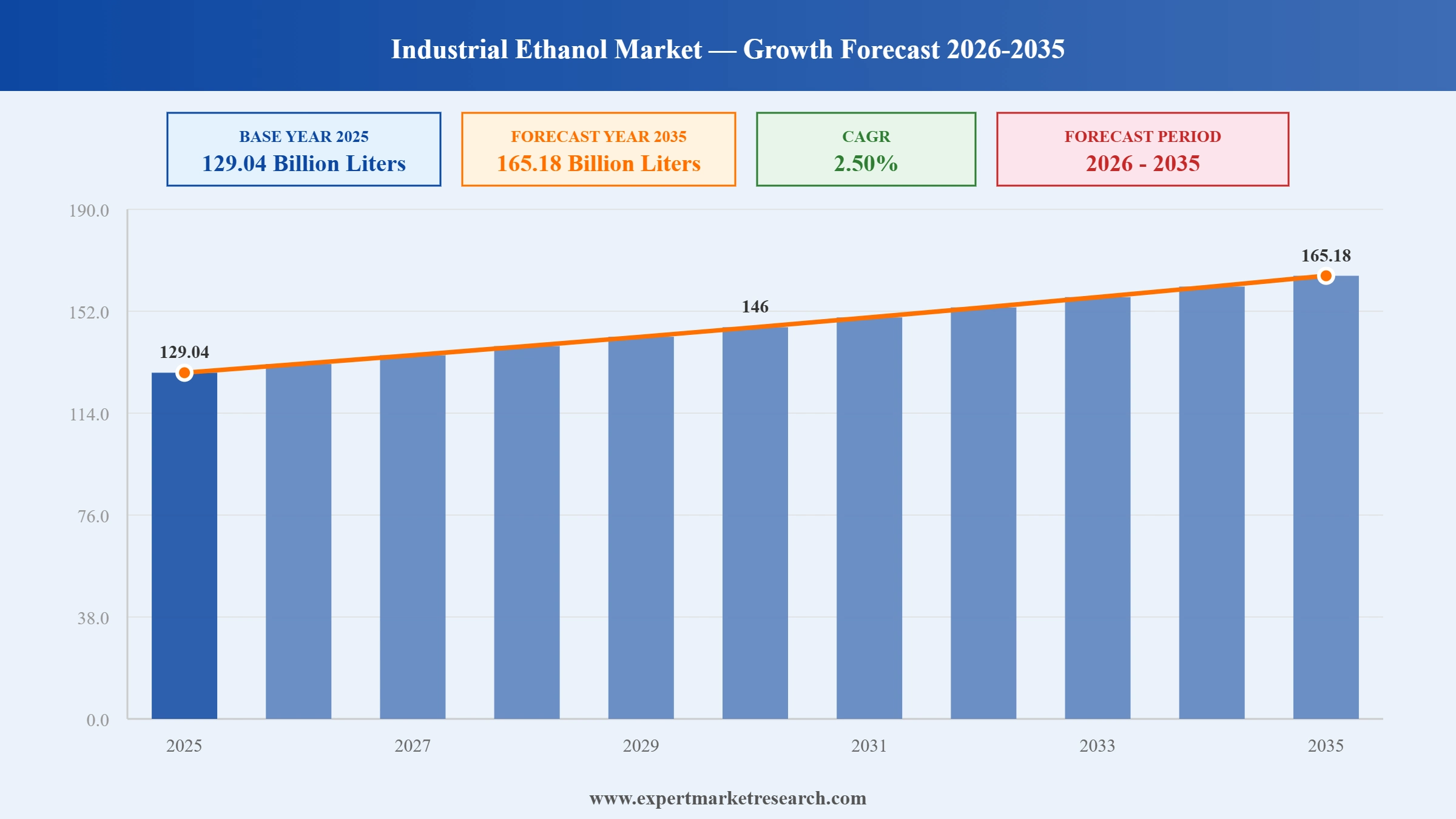

The Global Industrial Ethanol Market reached a volume of 129.04 Billion Liters at 2025 and is projected to expand at a CAGR of around 2.50% during the forecast period of 2026-2035. With expanding chemical intermediate demand for acetic acid and acrylates, growing pharmaceutical and personal care applications, accelerating substitution of synthetic with bio-based ethanol, and significant feedstock and policy support across Brazil, the United States, and India, the market is expected to reach 165.18 Billion Liters by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Global Industrial Ethanol market growth is being shaped by the structural shift from synthetic to bio-based ethanol, integrated bio-circular value chains, sugarcane-corn dual feedstock strategies in Brazil, and policy-driven capacity expansion in India.

Cargill announced plans to build a corn-based ethanol plant adjacent to its existing sugarcane operations in Brazil, broadening feedstock flexibility and reinforcing the company's position in the country's expanding ethanol economy. The project complements the February 2025 SJC Bioenergia acquisition and reflects Cargill's strategy of integrating sugarcane and corn ethanol assets to optimise utilisation across the harvest cycle. Brazil's diversified ethanol mix is increasingly relevant for industrial users in personal care, pharmaceuticals, and beverages, alongside its dominant role in road-fuel blending.

Archer Daniels Midland and Mitsubishi Corporation signed a non-binding memorandum of understanding to establish a strategic alliance exploring collaboration across the agriculture and biofuels value chain, including industrial ethanol applications. The partnership leverages ADM's portfolio of eighteen ethanol plants and approximately 1.8 billion gallons per year of bioethanol capacity, alongside Mitsubishi's global trading and infrastructure network. The MOU is intended to deepen access to Asian markets, expand low-carbon supply chains for fuels and chemicals, and reinforce ADM's position in industrial ethanol amid rising demand for sustainable feedstocks across Japan and Southeast Asia.

Cargill signed a sale and purchase agreement to acquire the remaining fifty percent stake in SJC Bioenergia, taking full ownership of the integrated sugar, ethanol, corn oil, and high-protein animal feed producer based in Goiás, Brazil. The company, now operating as Cargill Bioenergia, runs two agro-industrial units in Quirinópolis and Cachoeira Dourada and adds substantial sugarcane and corn-based ethanol capacity to Cargill's renewable energy platform. The acquisition follows more than 6.8 billion reais of recent Brazil investments and underlines the strategic importance of bio-ethanol within Cargill's global agriculture and renewable energy portfolio.

INEOS shut its synthetic ethanol plant at Grangemouth in Scotland, the United Kingdom's last remaining synthetic ethanol facility, removing approximately 180,000 tonnes per year of ethylene-based industrial ethanol capacity from European supply. INEOS cited unsustainable economics under high energy and carbon costs. The closure accelerates the structural shift in industrial ethanol from synthetic to bio-based feedstocks, particularly across the European Union, where regulatory and customer preferences increasingly favour fermentation-derived ethanol from sustainable sugar and grain sources. The decision reshapes regional supply balances for personal care and pharmaceutical buyers.

CropEnergies AG progressed with construction and commissioning of Europe's first integrated renewable ethyl acetate facility at the Zeitz Chemical and Industrial Park in Germany, with total investment between EUR 120 million and EUR 130 million. The plant is designed to produce 50,000 tonnes per year of ethyl acetate from sustainable industrial ethanol while generating renewable hydrogen as a co-product. Combined with biogenic carbon dioxide from CropEnergies' fermentation process, the facility supports power-to-X downstream routes and electro-fuels, embedding industrial ethanol within Europe's emerging bio-circular chemical economy.

Industrial ethanol production is shifting decisively from synthetic ethylene-based routes to fermentation-based bio-ethanol, driven by carbon pricing, customer sustainability mandates, and renewable feedstock availability. The shift is reshaping European supply chains and pricing dynamics for personal care, pharmaceuticals, and chemical intermediate buyers. In January 2025, INEOS closed its synthetic ethanol facility in Grangemouth, Scotland, the United Kingdom's last remaining synthetic ethanol plant with 180,000 tonnes per year of capacity, reinforcing the structural transition toward bio-based industrial ethanol and accelerating Industrial Ethanol market growth in fermentation-derived supply chains.

Producers are integrating industrial ethanol assets with downstream bio-circular chemicals, embedding ethanol within renewable hydrogen, biogenic carbon dioxide, and power-to-X value chains. The strategy raises margins, anchors customer demand, and aligns with EU Green Deal policy direction. In 2025, CropEnergies AG progressed commissioning of Europe's first integrated renewable ethyl acetate plant at Zeitz, Germany, designed to convert sustainable ethanol into 50,000 tonnes per year of ethyl acetate while generating renewable hydrogen and capturing biogenic carbon dioxide for downstream e-fuel applications.

Brazilian ethanol producers are integrating sugarcane and corn-based ethanol assets to smooth seasonal supply, optimise asset utilisation, and improve margin resilience. Dual-feedstock platforms are particularly valuable for industrial ethanol buyers in personal care, pharmaceuticals, and beverages who require year-round supply at consistent quality. In February 2025, Cargill agreed to take full control of SJC Bioenergia, now Cargill Bioenergia, which operates two integrated sugarcane and corn ethanol units in Goiás, deepening Cargill's footprint in Brazil's hybrid feedstock model and strengthening industrial ethanol supply across Latin America.

India achieved its 20 percent ethanol blending target ahead of schedule in 2025 and is now expanding ethanol production capacity beyond fuel applications, supporting industrial uses in pharmaceuticals, personal care, and chemical intermediates. The expansion is supported by long-term offtake agreements, GST relief, and surplus rice allocations from the Food Corporation of India. In 2025, India's ethanol production capacity rose to about 1,623 crore litres, anchored by both grain-based and sugar-based pathways and creating new supply for industrial ethanol buyers in domestic and export markets.

The Expert Market Research's report titled “Global Industrial Ethanol Market Report and Forecast 2026-2035” provides a detailed analysis of the market based on the following segments:

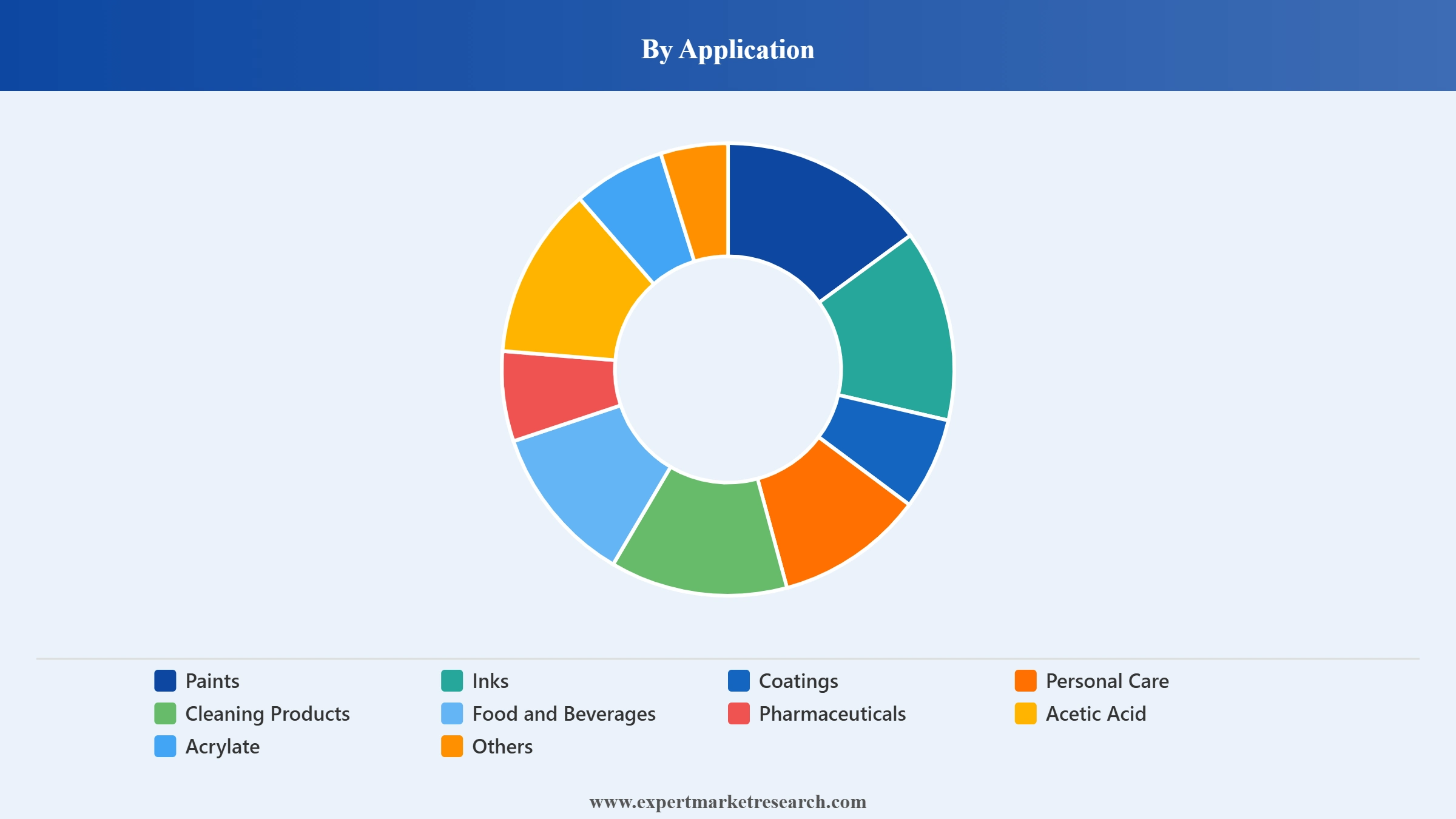

Market by Application

Key Insight: Acetic Acid is among the largest application segments for industrial ethanol, given its central role as a chemical intermediate for paints, inks, coatings, polymers, and textiles, with rising demand in China, India, and South Korea anchoring growth. Pharmaceuticals are another major application, where high-grade ethanol acts as a solvent, excipient, and sanitiser feedstock, supported by global pharmaceutical manufacturing growth. Personal care and cleaning products represent fast-growing applications, particularly in emerging markets, while CropEnergies's renewable ethyl acetate plant at Zeitz illustrates how industrial ethanol is being embedded into broader bio-circular chemical value chains across Europe.

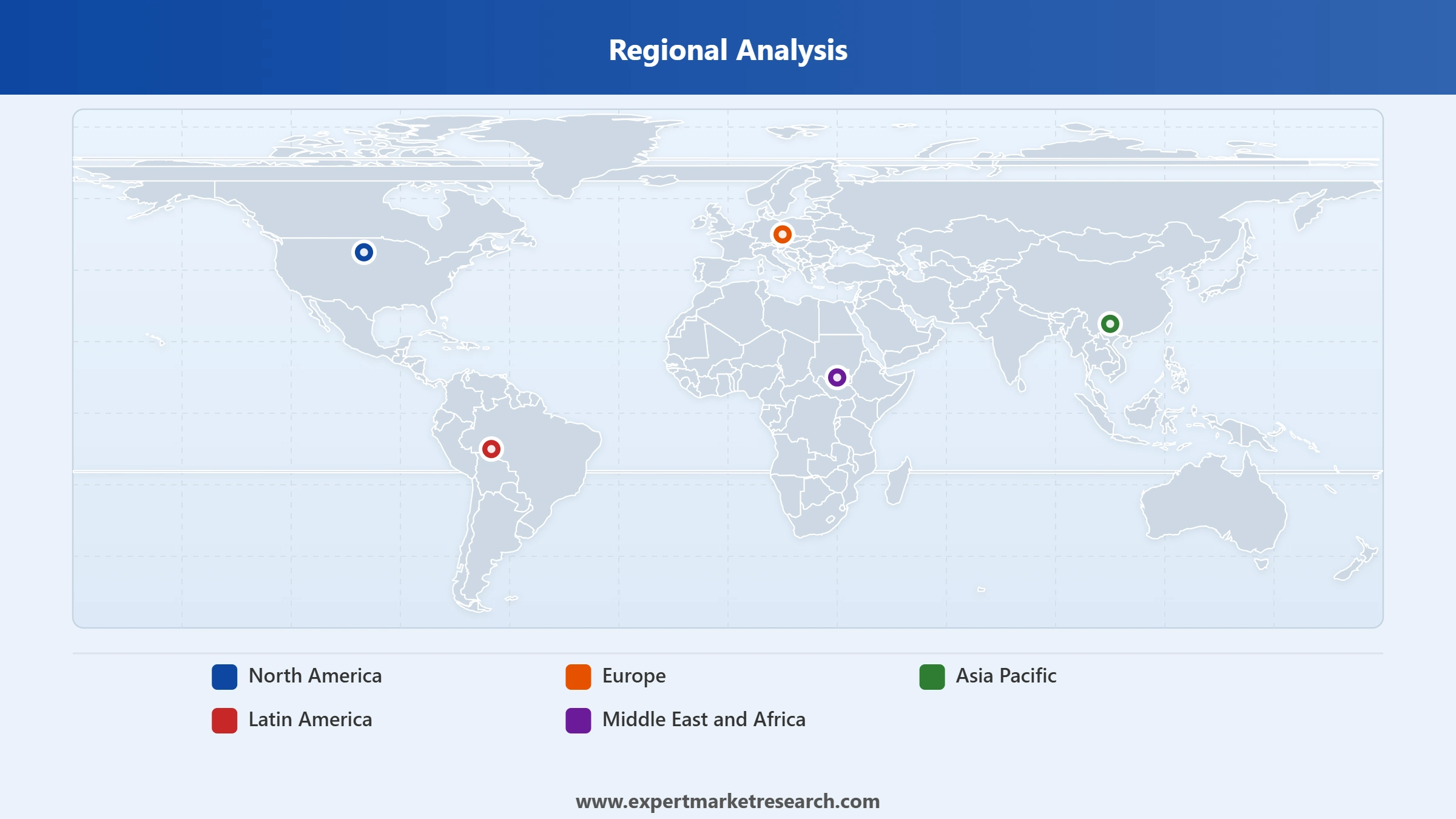

Market Breakdown by Region

Key Insight: North America is a major regional market, anchored by the United States' large bioethanol industry led by Archer Daniels Midland and Cargill, with eighteen operational ADM ethanol facilities and approximately 1.8 billion gallons per year of capacity. Latin America is significant, particularly Brazil, where sugarcane and corn-based ethanol production is expanding through Cargill Bioenergia and other integrated producers. Asia Pacific is the fastest-growing region, driven by India's E20 ethanol expansion and rising industrial demand in China. Europe is undergoing a structural shift toward bio-based ethanol, illustrated by CropEnergies's renewable ethyl acetate facility and INEOS's exit from synthetic ethanol production at Grangemouth.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Market by Application: Acetic Acid is the dominant application sub-segment, accounting for a substantial share of industrial ethanol consumption, particularly in Asia where downstream demand from paints, inks, coatings, and polymer producers is large and growing. The dominance is reinforced by the integration of acetic acid into adhesives, esters, and textiles supply chains. Pharmaceuticals are another high-share application, with industrial ethanol used as a solvent and excipient in formulation manufacturing. CropEnergies's 2025 commissioning of a renewable ethyl acetate plant in Zeitz, Germany illustrates how producers are extending the value chain by capturing downstream chemical intermediates with high carbon-credit and sustainability premiums.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Latin America: Latin America, led by Brazil, is the dominant region in industrial ethanol production, anchored by competitive sugarcane economics, large integrated mills, and expanding hybrid sugarcane-corn platforms. Cargill's February 2025 full acquisition of SJC Bioenergia, now Cargill Bioenergia, is a clear demonstration of how multinational agribusiness players are deepening their Brazilian ethanol footprints. Cargill's August 2025 plan to build a corn ethanol plant adjacent to existing sugarcane operations further emphasises feedstock flexibility. Demand drivers include both fuel and industrial applications, with surplus production increasingly available for export markets in personal care, pharmaceuticals, and chemical intermediate use cases across North America, Europe, and Asia.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific: Asia Pacific is the fastest-growing region for industrial ethanol, driven by India's rapid capacity build-out for fuel blending and downstream industrial applications. India achieved its E20 fuel blending target ahead of schedule in 2025 and continues to expand capacity beyond 1,623 crore litres. China is a major industrial ethanol consumer, particularly for acetic acid and chemical intermediates, while Japan and Southeast Asia are emerging buyers of bio-based ethanol for personal care and pharmaceuticals. Long-term offtake agreements signed by Indian public-sector oil marketing companies, GST relief, and surplus rice allocations from the Food Corporation of India underpin a stable demand and supply environment supportive of industrial ethanol producers regionally.

The global industrial ethanol market is moderately consolidated at the producer tier, with multinational agribusiness and chemical players competing alongside large national operators. Archer Daniels Midland, Cargill, Tereos, COFCO, and CropEnergies are leading bio-based producers, while INEOS Group has historically anchored synthetic ethanol supply in Europe before exiting the segment in 2025.

Competitive priorities now centre on bio-based feedstocks, integrated bio-circular value chains, and capacity expansion in low-cost regions such as Brazil and India. Producers are investing in renewable hydrogen, biogenic carbon dioxide, and ethyl acetate downstream routes to capture sustainability premiums and align with policy directives in the European Union, the United States, and Asia. Strategic acquisitions, exemplified by Cargill Bioenergia, and capacity rationalisation, exemplified by INEOS at Grangemouth, are reshaping the global industrial ethanol supply landscape.

Founded in 1902 and headquartered in Chicago, Illinois, Archer Daniels Midland is one of the world's largest agricultural processing companies. Its industrial ethanol portfolio is anchored by approximately eighteen ethanol facilities and about 1.8 billion gallons per year of bioethanol capacity. ADM's strengths include scale, deep US grain-supply integration, an expanding range of low-carbon ethanol products, and growing global reach via the March 2025 strategic memorandum of understanding with Mitsubishi Corporation across agriculture and biofuels.

Founded in 1865 and headquartered in Wayzata, Minnesota, Cargill is one of the world's largest privately held agribusiness and food companies. Its industrial ethanol footprint expanded significantly in 2025 with the acquisition of full ownership of SJC Bioenergia in Brazil, now Cargill Bioenergia, and a planned corn ethanol plant adjacent to existing sugarcane assets. Capabilities span sugarcane and corn ethanol, integrated milling, animal nutrition, renewable energy, and biofuels supply across the Americas, Europe, and Asia.

Founded in 2006 as a subsidiary of Südzucker AG and headquartered in Mannheim, Germany, CropEnergies AG is one of Europe's leading bioethanol producers. The company operates plants in Germany, Belgium, the United Kingdom (Ensus), and France. CropEnergies has expanded into bio-circular chemicals with its Zeitz renewable ethyl acetate plant, supported by EUR 120 to 130 million in investment, and produces sustainable industrial ethanol for personal care, pharmaceuticals, beverages, and chemical intermediate applications across Europe.

Founded in 1998 and headquartered in London, INEOS is a multinational chemicals group that historically operated significant industrial ethanol capacity in Europe, including the Grangemouth synthetic ethanol plant. The company exited synthetic ethanol production at Grangemouth in January 2025, citing unsustainable economics under high energy and carbon costs. INEOS continues to participate in the broader industrial chemicals value chain, including downstream solvents, intermediates, and specialty applications relevant to industrial ethanol's customer base.

Other key players in the market are Tereos Participations, Unicol Limited, Alcool Ferreira SA, COFCO, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Discover the latest insights on the Global Industrial Ethanol Market 2026 with our comprehensive report. Stay ahead of the curve with valuable data on bio-based capacity expansion, downstream chemical integration, and high-growth regions. Whether you are a producer planning capacity additions, a chemical buyer evaluating sustainable feedstocks, or an investor assessing M&A opportunities, this report gives you the clarity you need. Download your free sample now and discover the key opportunities in the thriving Global Industrial Ethanol industry.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the global industrial ethanol market attained a volume of almost 129.04 Billion Liters.

The market is projected to grow at a CAGR of 2.50% between 2026 and 2035.

The major drivers of the market are rising disposable incomes, increasing population, increasing hygiene awareness, rising demand from the developing regions, and growing technological advancements.

The key trends guiding the growth of the market include the growing consumer awareness about the usage of antibacterial products and increasing demand from the paints, inks, and coatings sector.

The major regions in the market are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific, with Asia Pacific accounting for the largest share in the market.

Paints, inks, and coatings, personal care, cleaning products, food and beverage, pharmaceuticals, acetic acid, and acrylate, among others, are the major applications of industrial ethanol in the market.

The major players in the market are Archer Daniels Midland Company, Cargill, Incorporated, Tereos Participations, Unicol Limited, CropEnergies AG, Alcool Ferreira SA, COFCO, and INEOS Group Holdings S.A, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.