Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

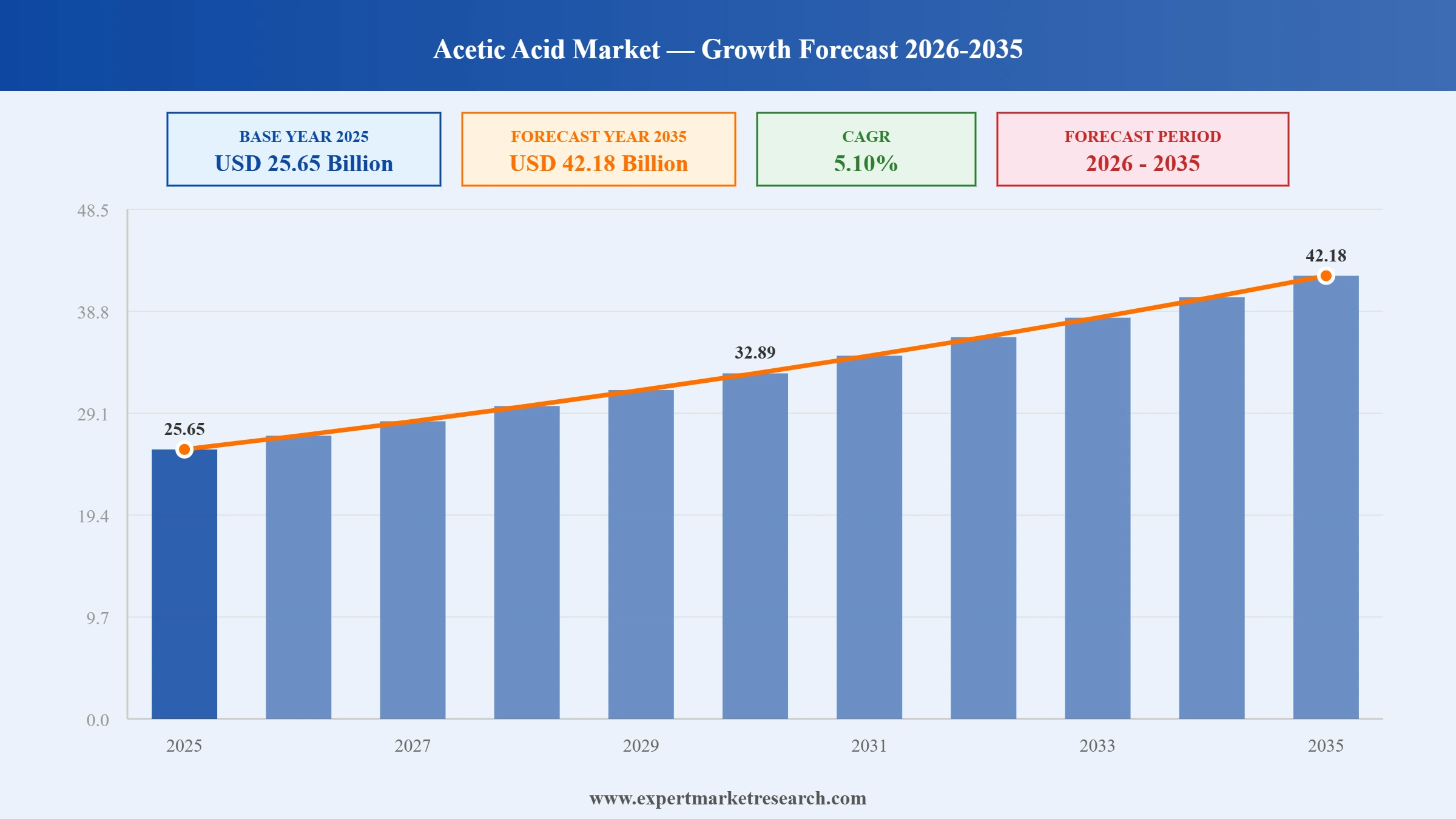

The Global Acetic Acid Market was valued at USD 25.65 Billion in 2025 and is set to grow at a CAGR of around 5.10% through 2026-2035. Capacity expansion investment in North America and Asia, alongside emerging bio-based production routes, is keeping growth momentum intact. The market is on track to reach USD 42.18 Billion by 2035. Expanding downstream demand for vinyl acetate monomer, growing use in purified terephthalic acid production, and rising pharmaceutical and food preservation applications are driving the global acetic acid market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global acetic acid market is in a period of structural adjustment. Trade flow realignments, bio-based production gaining commercial momentum, and active acetyl chain restructuring are reshaping how this market is supplied and priced. VAM and PTA remain the demand anchors, but sustainability-linked capital is increasingly redirected toward lower-carbon production routes.

SCG Chemicals and PTT Global Chemical signed a strategic memorandum in April 2026 to explore a joint venture combining olefins and polyolefins assets in Thailand. The integration is expected to strengthen Southeast Asian petrochemical positions with downstream implications for acetic acid derivative and vinyl value chains.

Celanese reported Acetyl Chain net sales of USD 1.0 billion in Q1 2026, a 10% sequential increase on volume and pricing improvements in China. Late-quarter trade flow disruptions redirected demand toward its Clear Lake, Texas facility and integrated Western Hemisphere supply network.

INEOS continued integration activities in January 2026 following its acquisition of Eastman's Texas City petrochemical assets, including a major acetic acid production facility. The move consolidated INEOS' North American acetyl chain position and strengthened its control over feedstock management and derivative supply in the Western Hemisphere.

Kemvera announced pilot reactor commissioning in January 2026 and plans for a 50,000 MTPA commercial-scale bio-based acetic acid facility in the United States. The progress reflects growing producer and buyer interest in low-carbon acetic acid alternatives as sustainability mandates tighten across regulated markets.

Vinyl Acetate Monomer holds the largest share of acetic acid end-use consumption globally. Polyvinyl acetate-based adhesives, emulsion polymers for paints and coatings, and textile finishes all depend on VAM as a key input. The construction sector's reliable demand for adhesives and surface coatings provides a stable consumption floor that is relatively insulated from short-term economic volatility.

China controls approximately 55% of global acetic acid production capacity through domestic methanol carbonylation plants operating at a scale no other region can replicate on cost terms. Sinopec, Jiangsu Sopo, and Chang Chun Group sustain this structural advantage. Asian exports into Europe and North America remain limited by freight costs, benefiting integrated Western Hemisphere producers.

Bio-based acetic acid is transitioning from pilot scale toward early commercial production. Biomass fermentation routes are attracting investment from sustainability-focused chemical buyers and European regulatory-driven demand. The segment remains a small fraction of total capacity, but investment acceleration through 2025 and 2026 points to a more meaningful role by the end of the forecast period.

Purified Terephthalic Acid is acetic acid's second-largest and fastest-growing application. PTA production for polyester fiber and PET resin grows in step with Asia's textile and packaging industries, keeping acetic acid demand anchored to the broader polyester value chain trajectory across China, India, and Southeast Asia.

North America and Western Europe are benefiting from a structural trade flow shift. With Asian acetic acid exports into these regions remaining at historically low levels due to freight costs and geopolitical complexity, Celanese's Clear Lake plant and other regional producers are capturing Western Hemisphere demand with an advantaged cost position. This dynamic is reshaping procurement and pricing relationships across the Atlantic acetyl market.

The report of Expert Market Research's titled "Global Acetic Acid Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

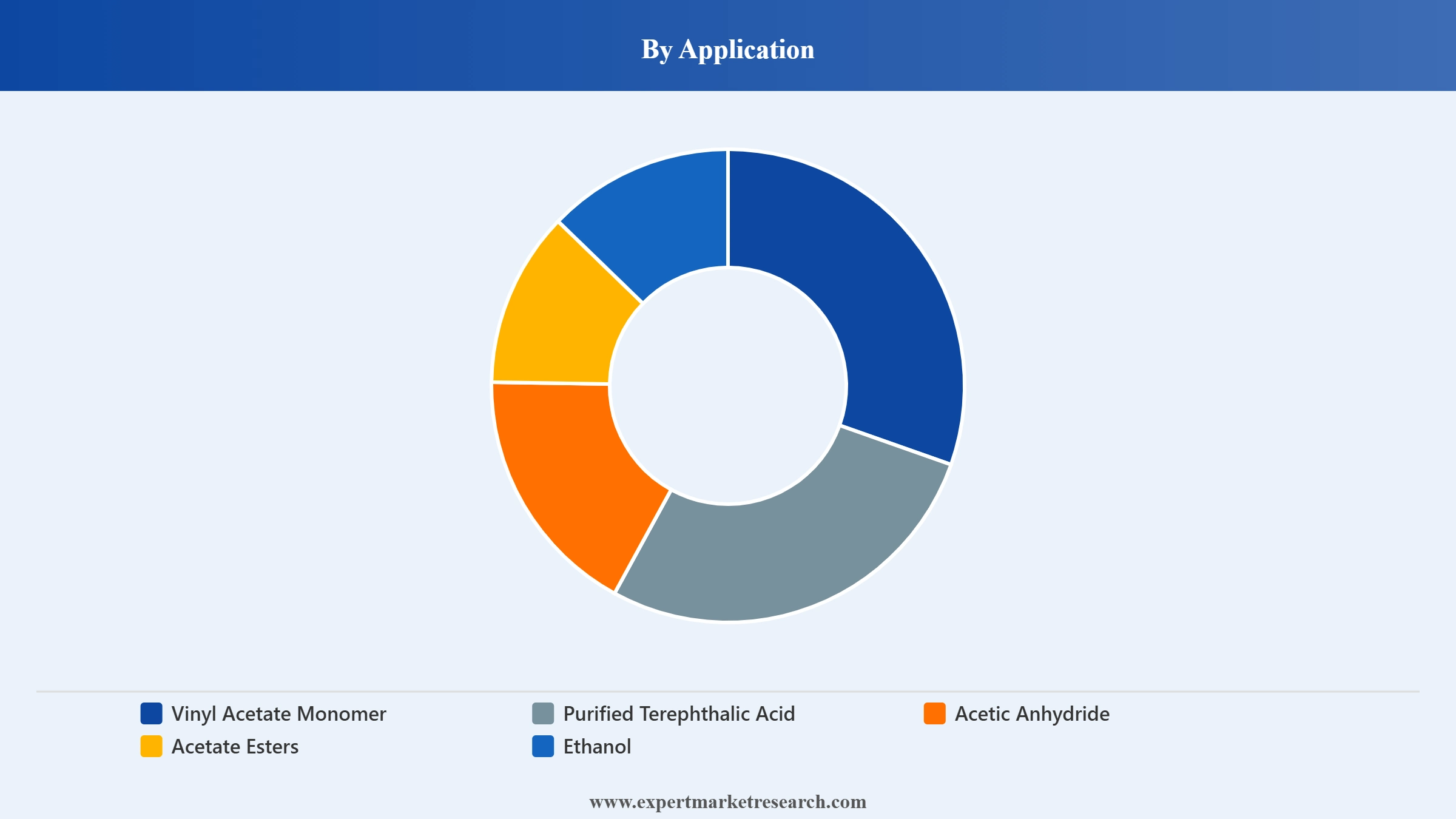

Market Breakup by Application

Key Insight: VAM dominates application-level demand, feeding into polyvinyl acetate for adhesives, paints, and coatings tied to construction and packaging cycles. PTA is the fastest-growing application, driven by polyester fiber and PET resin demand in Asia's textile and packaging sectors.

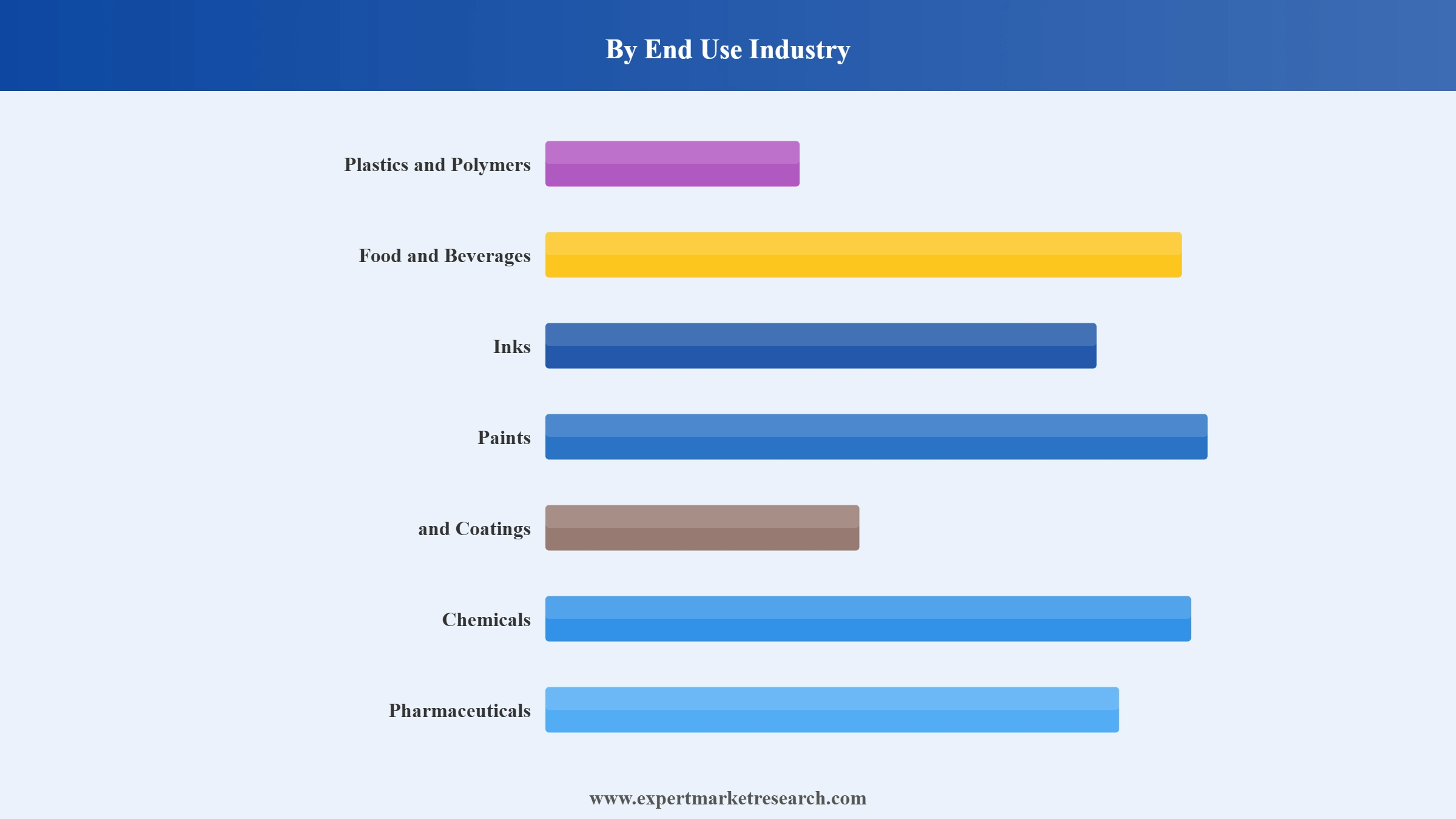

Market Breakup by End Use Industry

Key Insight: Plastics and Polymers absorbs the largest end-use share through PTA-derived polyester and VAM-derived polymer demand in packaging, textiles, and construction. Pharmaceuticals is a smaller but stable channel through acetic anhydride consumption in aspirin and other active pharmaceutical ingredient synthesis.

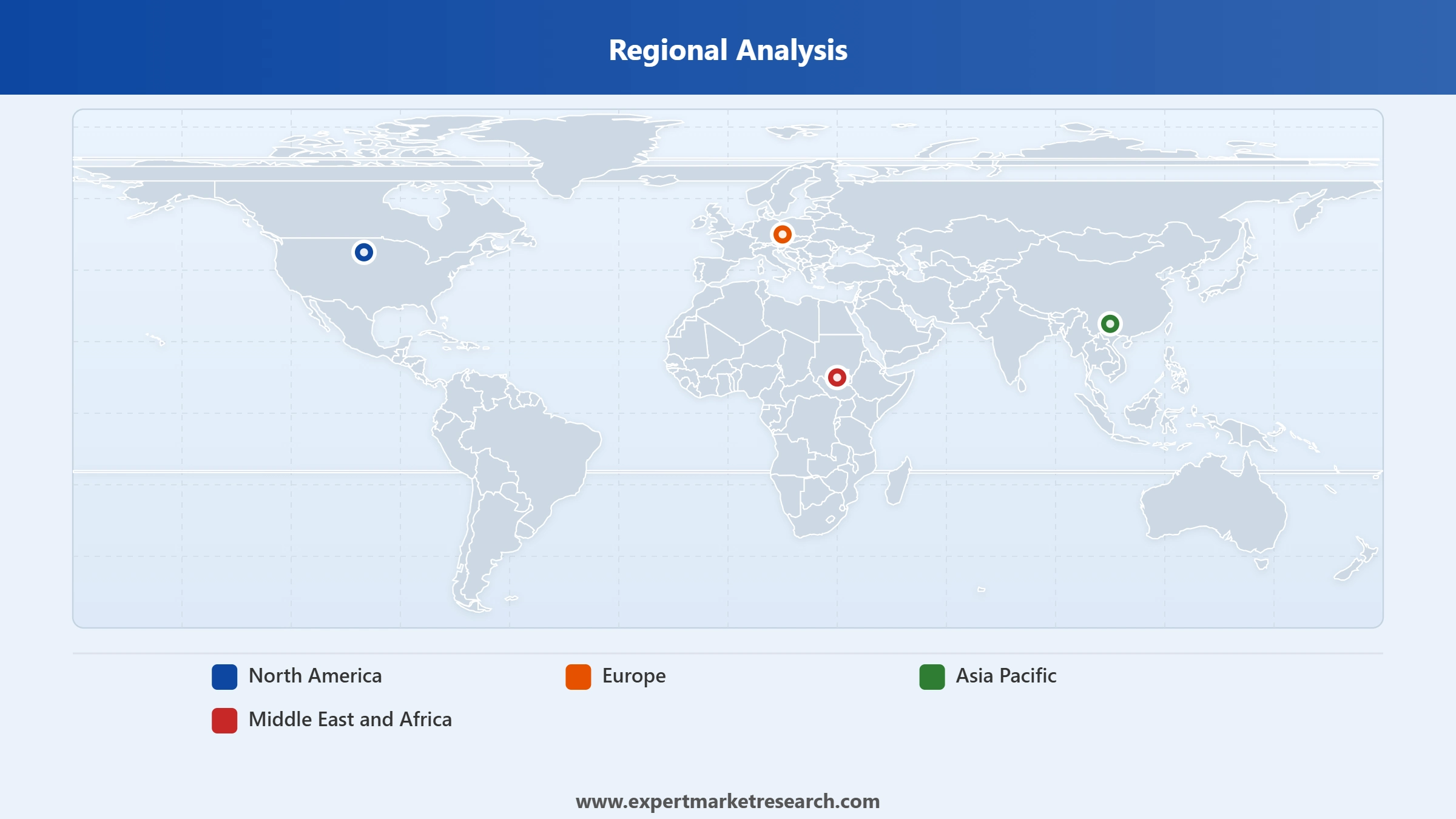

Market Breakup by Region

Key Insight: China dominates both production and consumption, accounting for roughly 55% of global capacity through its methanol carbonylation plants. North America holds a strategically important position through Celanese's Clear Lake facility, one of the most cost-competitive single-site acetyls operations outside Asia.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Application, Vinyl Acetate Monomer dominates the market due to its critical role as a polymer precursor across adhesives, coatings, and construction material applications

VAM accounts for the largest share of global acetic acid consumption by application. The downstream products it generates, primarily polyvinyl acetate and vinyl acetate ethylene copolymers, go into a broad and structurally stable set of industries: construction adhesives, emulsion paints, textile finishes, and packaging coatings. According to data from Mordor Intelligence, VAM led with approximately 27.97% of the acetic acid market share in 2024, and that leadership position is expected to hold through the forecast period.

PTA records the fastest application-level growth, driven by polyester and PET resin capacity additions across China, India, and Southeast Asia. Acetic anhydride serves a stable pharmaceutical demand base, while acetate esters feed printing inks, industrial solvents, and specialty coatings.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By End Use Industry, Plastics and Polymers holds the dominant share due to large-volume consumption in polyester fiber, PET resin, and polymer manufacturing

Plastics and Polymers leads the end-use hierarchy, driven by PTA-derived polyester and VAM-derived polymer demand in packaging, textiles, and building materials. The structural growth of Asia's polymer industries ensures acetic acid consumption in this segment grows in step with the broader value chain.

Inks, Paints, and Coatings is a meaningful secondary end-use tied to VAM consumption for emulsion paint binders and adhesive formulations. Pharmaceuticals provides a stable, premium channel through acetic anhydride in active pharmaceutical ingredient synthesis, and food and beverages uses acetic acid as a preservative and acidulant.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

China dominates the global acetic acid market due to its large-scale methanol carbonylation production capacity and extensive downstream chemical manufacturing base

China commands the global acetic acid market on both the supply and demand side. Methanol carbonylation plants operated by Sinopec, Jiangsu Sopo, and others represent approximately 55% of global production capacity, while domestic PTA, VAM, and acetate ester manufacturing absorbs a dominant share of that output. Government support through investment incentives and infrastructure policy reinforces China's structural advantage through the forecast period.

North America holds a strategically differentiated position. Asian exports into the region remain at historically low levels due to freight costs, giving North American producers a more protected competitive environment. Europe benefits from similar dynamics. The Middle East and Africa, South East Asia, and North East Asia are all growing consumption markets driven by polymer, textile, and pharmaceutical industry expansion.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global acetic acid market is dominated by a small number of large, integrated chemical companies with methanol carbonylation plants across multiple geographies. Celanese and INEOS hold particularly strong Western Hemisphere positions, while Chinese producers dominate Asian supply. Feedstock access, scale economics, and proximity to downstream customers define the competitive landscape.

Founded in 1918 and headquartered in Dallas, Texas, Celanese Corporation is the world's largest integrated acetic acid producer. Its Clear Lake, Texas facility is one of the most cost-competitive single-site acetyls plants globally. In Q1 2026, Celanese reported Acetyl Chain net sales of USD 1.0 billion, a 10% sequential increase driven by volume and pricing improvements primarily in China.

Founded in 1976 and headquartered in Riyadh, Saudi Arabia, SABIC is one of the world's largest petrochemical companies, with operations across basic chemicals, polymers, and specialty products. Its integrated Saudi Arabian complex provides feedstock access advantages for acetic acid and derivative production, supporting supply across the Middle East, Africa, and Asia.

Founded in 1920 and headquartered in Kingsport, Tennessee, Eastman Chemical Company is a global specialty chemical producer with a strong acetyls heritage. Following its Texas City asset sale to INEOS, Eastman is refocusing on higher-margin specialty materials, while its acetyls technology remains a significant intellectual property asset licensed to producers globally.

Founded in 1897 and headquartered in Midland, Michigan, Dow is one of the world's largest diversified chemical companies, with a strong presence across plastics, coatings, and industrial intermediates. Dow downstream VAM and acetate-derived polymer consumption positions it as both a major customer and an active participant in the broader acetyl chemicals market.

Other key players in the market are Gujarat Narmada Valley Fertilizers and Chemicals Limited, British Petroleum, LyondellBasell Industries Holdings B.V., HELM AG, Indian Oil Corporation Ltd., Jiangsu Sopo, Chang Chun Group, Daicel Corporation, Mitsubishi Chemical Corporation, SEKAB, INEOS Group Holdings S.A., Global Chemical Resources, Altiras Chemicals LLC, Saudi Basic Industries Corporation, Anant Pharmaceuticals Pvt. Ltd., and others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Our full report for 2026-2035 provides the production data, derivative demand analysis, price trends, and competitive intelligence to navigate the global acetic acid market with confidence. Reach out to our team to access the complete report or request a customised version.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 25.65 Billion.

The market is experiencing steady growth, driven by increasing demand in textiles, pharmaceuticals, and packaging industries, garnering a 5.10% CAGR through 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 42.18 Billion by 2035.

Rising demand for intermediates like acetic acid in pharmaceuticals, plastics, and adhesives is the major market driver.

The key acetic acid market trends include increasing acceptance of bio-based acetic acid, technological advancements, improvements in production capacities, and growing demand for plastics and textiles.

The major regional markets for acetic acid, according to the report, are China, North America, Western/Eastern Europe, North East Asia, South East Asia and the Middle East and Africa.

The different applications of acetic acid in the market are vinyl acetate monomer (VAM), purified terephthalic acid (PTA), anhydride, ethyl acetate, and butyl acetate.

The various end use industries in the market for acetic acid are plastics and polymers, food and beverages, inks, paints, and coatings, chemicals, and pharmaceuticals, among others.

The major players in the market, according to the report are SABIC, Eastman Chemical Company, Gujarat Narmada Valley Fertilizers & Chemicals Limited, Dow, British Petroleum, LyondellBasell Industries Holdings B.V., HELM AG ,Indian Oil Corporation Ltd., Celanese Corporation, Jiangsu Sopo, Chang Chun Group, Daicel Corporation, Mitsubishi Chemical Corporation., Svensk Etanolkemi AB (SEKAB), INEOS Group Holdings S.A, Global Chemical Resources, Altiras Chemicals LLC, Saudi Basic Industries Corporation, and Anant Pharmaceuticals Pvt. Ltd., among others.

The vinyl acetate monomer (VAM) segment holds the largest market share due to its extensive use in adhesives, paints, and coatings.

Growth in pharmaceuticals, textiles, plastics, and food preservation, along with sustainability initiatives, is driving the market.

Asia Pacific held the highest market share due to strong demand from China and India in textiles, packaging, and pharmaceuticals.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Application |

|

| Breakup by End Use Industry |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.