Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

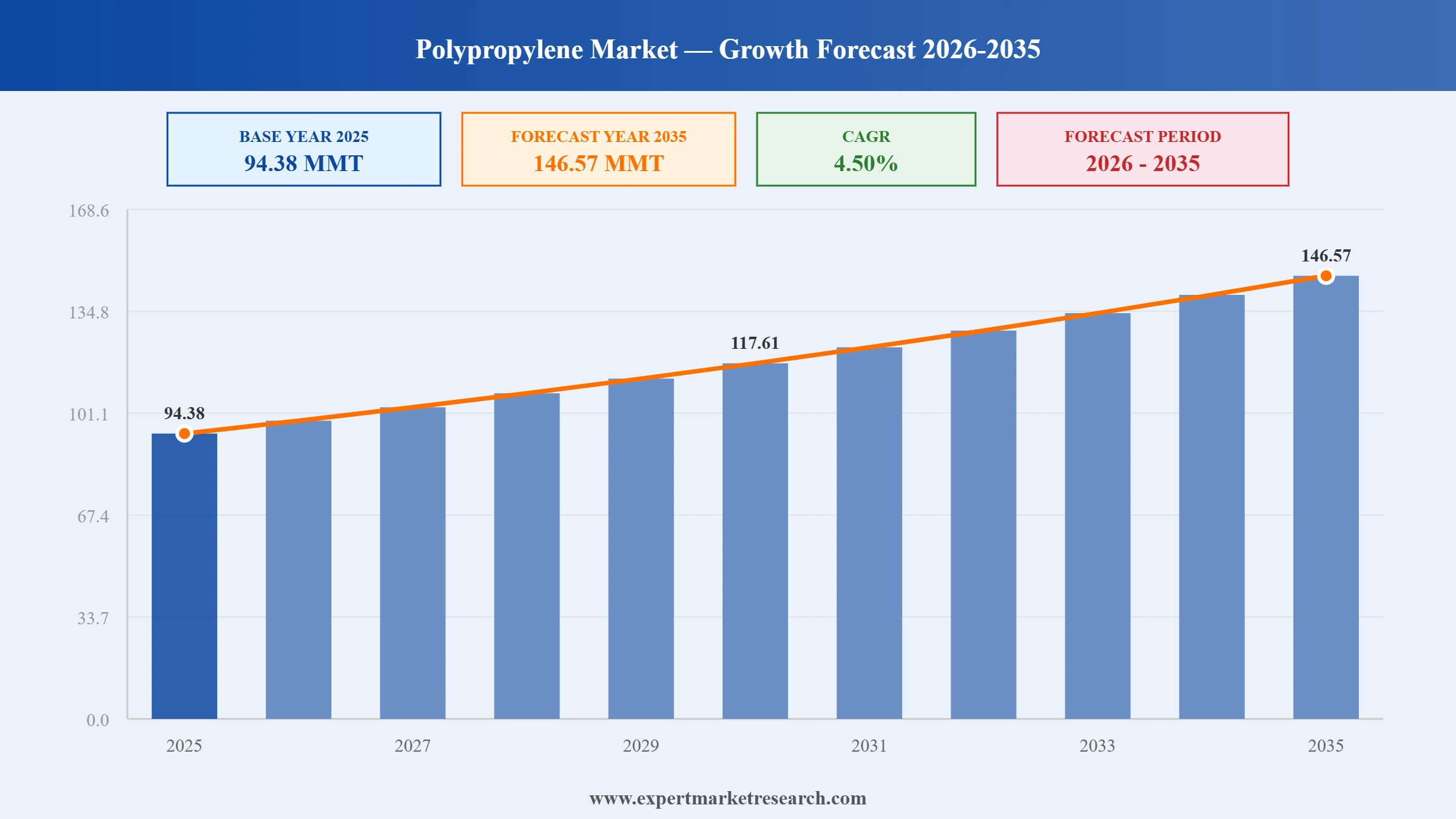

The Global Polypropylene Market reached a volume of 94.38 MMT at 2025 and is projected to expand at a CAGR of around 4.50% during the forecast period of 2026-2035. With expanding packaging consumption, accelerating automotive lightweighting, growing medical-grade demand, and rising adoption of mechanically and chemically recycled polypropylene, the market is expected to reach 146.57 MMT by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Global Polypropylene market growth is being shaped by accelerating circularity investments, capacity migration to Asia and the Middle East, premiumisation toward HMS and medical-grade resins, and tighter regulation around plastic packaging.

Borouge and Borealis unveiled Recleo, a new global brand consolidating mechanically recycled polyolefin grades, including post-consumer and post-industrial recycled polypropylene compounds, into a single, cost-effective portfolio. Recleo is positioned for use in mobility, building and construction, appliances, infrastructure, and consumer products. The launch represents one of the largest concerted moves by joint-venture polyolefin producers to scale recycled polypropylene at industrial volume, helping brand owners meet upcoming European and Middle East regulatory targets for recycled content in plastic packaging and durable applications.

ExxonMobil commissioned a second advanced recycling unit at its Baytown, Texas facility, doubling its capacity to convert plastic waste, including used polypropylene and polyethylene, into circular feedstocks. The site has now processed more than 100 million pounds of plastic waste through Exxtend technology. ExxonMobil also confirmed plans for a third and fourth Baytown unit and a first unit in Beaumont, raising regional capacity toward 500 million pounds per year. The expansion supports the company's global goal of reaching one billion pounds per year of advanced recycling capacity by 2027.

Borealis announced an investment exceeding EUR 100 million in a new High Melt Strength Polypropylene production line at its Burghausen site in Germany, with start-up scheduled for the second half of 2026. The new line will produce Daploy HMS PP, a grade engineered for foamability, lightweighting, and mechanical strength suitable for monomaterial recyclable solutions across packaging, automotive, building and construction, and consumer goods. The move underscores European producers' pivot toward differentiated, sustainability-aligned polypropylene grades that command premium margins amid intense Asian capacity competition.

LyondellBasell sanctioned a new metathesis unit at its Channelview Complex near Houston, designed to convert ethylene into approximately 400 thousand metric tons per year of propylene to feed downstream polypropylene and propylene oxide production. Construction is set to begin in the third quarter of 2025 with start-up planned for late 2028, with the project employing 750 workers at peak construction. The investment strengthens LyondellBasell's feedstock self-sufficiency, supports growing North American polypropylene demand, and reduces exposure to merchant propylene volatility across the Gulf Coast cluster.

Sinopec completed phase-two construction of the Zhejiang Ningbo Petrochemical Industrial Base at Zhenhai, with cumulative investment of about CNY 41.6 billion, lifting refining capacity above 50 million tonnes per year and adding sizeable polypropylene output. Sinopec Guangxi Petrochemical separately started up a 400,000 tonne per year polypropylene unit in Qinzhou, capable of producing homopolymer, ethylene random copolymer, impact copolymer, and butene-containing grades. The launches underline China's accelerated polypropylene capacity build-out, which added more than five million tonnes per year of nameplate capacity in 2024.

Major polypropylene producers are scaling chemical and mechanical recycling to meet brand-owner mandates and EU and Middle East regulations on recycled content. Investments target proprietary technologies, certified circular grades, and compounding lines that consume post-consumer polypropylene streams. The trend reflects a structural shift from linear to circular polymer chains and is influencing capital allocation across North America and Europe. In May 2025, ExxonMobil doubled its Baytown advanced recycling capacity by commissioning a second unit, supporting the global Polypropylene market growth and positioning Exxtend technology as a credible circular feedstock route.

Producers are unifying recycled polypropylene and polyethylene portfolios under specialised brands to simplify customer adoption and signal scale. The strategy lowers barriers for converters and brand owners by pooling post-consumer and post-industrial grades under common quality and sustainability standards. In December 2025, Borouge and Borealis launched Recleo, a global brand consolidating mechanically recycled polyolefins, including PCR and PIR polypropylene compounds, for mobility, packaging, infrastructure, and consumer products. The launch demonstrates how integrated joint ventures intend to capture premium margins from sustainability-led demand.

Polypropylene producers in North America are reinforcing propylene feedstock self-sufficiency to mitigate volatility from cracker turnarounds and propane market swings. The trend favours integrated metathesis, propane dehydrogenation, and on-purpose propylene assets close to ethylene crackers. In March 2025, LyondellBasell approved a new 400,000 tonne per year metathesis unit at its Channelview, Texas complex, scheduled for start-up in late 2028, anchoring future polypropylene production growth in the United States. The decision signals continued willingness to commit multi-year capital despite cyclical margin pressure.

Massive Chinese polypropylene capacity additions are tilting global trade flows, lengthening Asian supply, and pressuring producers in Europe and the Americas to focus on differentiated and circular grades. Integrated Chinese refiners are commissioning new world-scale units capable of producing the full polypropylene grade slate. In January 2025, Sinopec completed phase-two construction of its Zhenhai-anchored Zhejiang Ningbo Petrochemical Industrial Base, while Guangxi Petrochemical started up a 400,000 tonne per year polypropylene unit in Qinzhou capable of producing homopolymer, random, impact, and butene grades.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global polypropylene market report highlights segmentation by polymer type, process, application, and end-use, with detailed categorisation into sub-segments. It examines regional and country levels, focusing on volume and revenue growth. Industry trends indicate emerging shifts, influencing the market’s structure and dynamics across various segments. Companies are using these insights to adapt and capitalise on the changing demand across different region and applications.

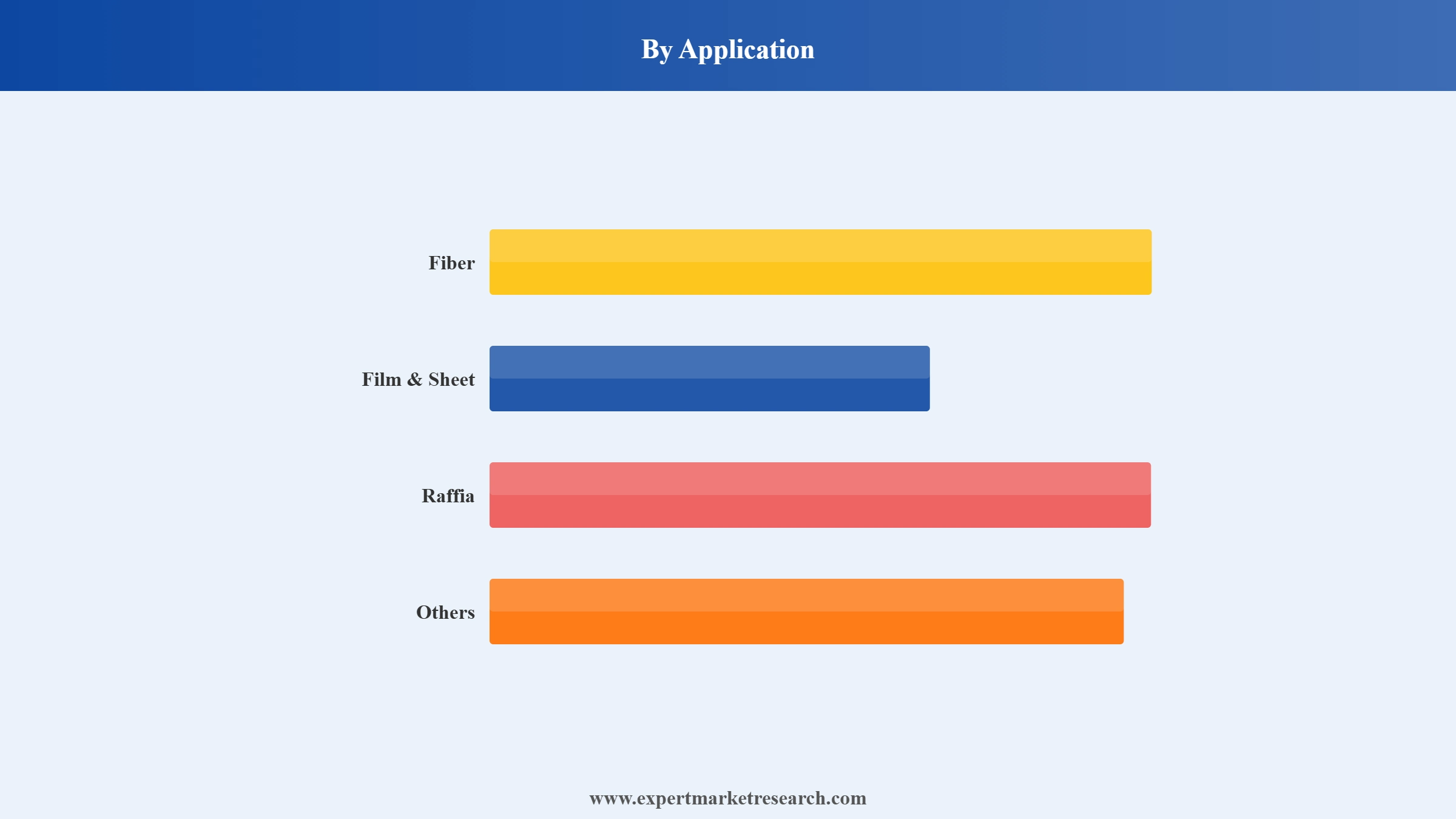

Market Breakup by Application

Key Insight: Film and sheet, fibre, and raffia are the primary application categories for polypropylene volumes. Film and sheet applications dominate due to extensive use in flexible food packaging, hygiene products, and consumer goods, where polypropylene's clarity, barrier properties, and lightweight benefits drive substitution against alternative polymers. Fibre is heavily consumed in nonwovens for hygiene, medical, and automotive interiors, while raffia underpins woven sacks and flexible intermediate bulk containers in agriculture and industrial packaging. Producers including LyondellBasell, Sinopec, and Reliance Industries are tailoring grade development around higher-clarity films, biaxially oriented polypropylene structures, and recycled feedstock blends to meet evolving brand-owner specifications.

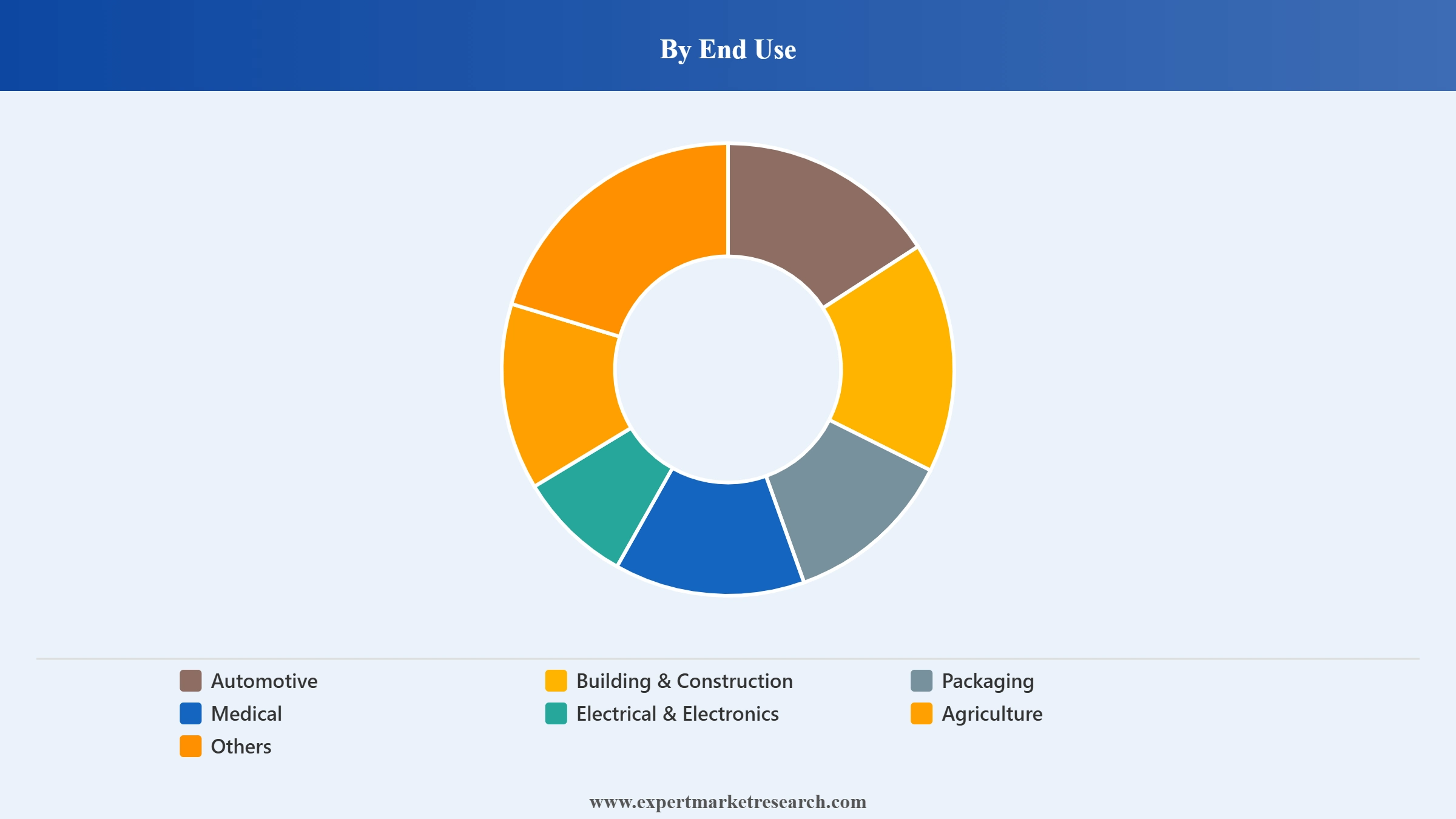

Market Breakup by End Use

Key Insight: Packaging is the largest end-use segment, accounting for the bulk of polypropylene demand thanks to its role in food containers, films, caps, closures, and flexible pouches. The segment benefits from e-commerce expansion, monomaterial recyclability mandates, and substitution against polystyrene and polyethylene terephthalate. Automotive is a high-value end use where polypropylene compounds enable lightweighting in bumpers, dashboards, door panels, and battery housings for electric vehicles, supported by Borealis's Daplen and Recleo grades. Healthcare adoption is rising for syringes, vials, and diagnostic devices, while building and construction draws on pipes, geotextiles, and insulation systems.

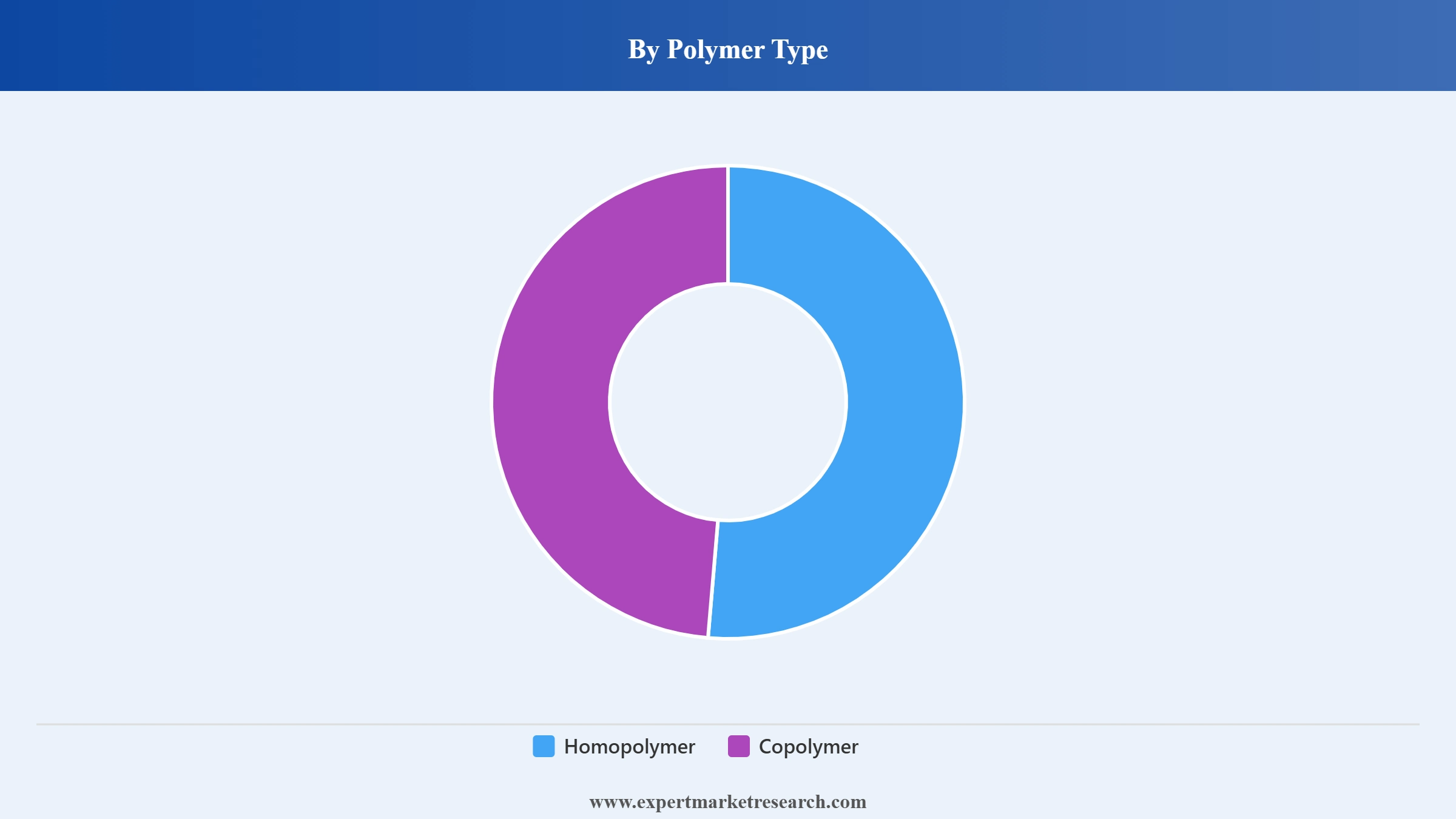

Market Breakup by Polymer Type

Key Insight: Homopolymer polypropylene holds the largest share, anchored by its dominance in raffia, fibre, films, rigid packaging, and general-purpose injection moulded parts where stiffness and clarity matter most. Copolymer grades, including random and impact copolymers, command premium positions in automotive, appliance, healthcare, and high-impact rigid packaging, where toughness, low-temperature performance, and clarity are critical. Sinopec's Guangxi Petrochemical 400,000 tonne per year unit started in 2025 is notable for being able to produce the full slate of homopolymer, random, impact, and butene-containing copolymers, illustrating producers' increasing focus on multi-grade flexibility within single trains.

Market Breakup by Process

Key Insight: Injection moulding is the dominant process route for polypropylene, supporting automotive parts, caps and closures, household goods, and consumer durables. Extrusion moulding is critical for films, sheets, fibres, pipes, and BOPP applications, while blow moulding underpins bottles, containers, and industrial parts. Process innovation, including thinner-wall injection moulding, advanced extrusion of monomaterial structures, and improved gas-phase polymerisation, is reducing material intensity and improving recyclability. Borealis's Daploy HMS PP, supported by a EUR 100 million Burghausen investment in 2025, targets foam extrusion applications where high melt strength enables lightweight monomaterial structures suited to packaging and automotive.

Market Breakup by Region

Key Insight: Asia Pacific is the dominant region in the global polypropylene market, supported by China's massive capacity additions, India's downstream growth led by Reliance Industries, and steady consumption across ASEAN converters. North America benefits from competitive feedstock and integrated assets such as LyondellBasell's Channelview complex, while Europe focuses on differentiated and circular grades through Borealis, INEOS, and TotalEnergies. The Middle East and Africa region is positioned as a major export base, with SABIC and Borouge expanding polyolefin capacity. Latin America's growth is anchored by Braskem's integrated petrochemical platforms in Brazil and Mexico.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Market by End Use: Packaging is the dominant end-use sub-segment, accounting for over half of polypropylene consumption thanks to flexible films, rigid containers, caps, closures, and hygiene applications. Packaging dominance is reinforced by e-commerce growth, monomaterial sustainability targets, and the migration of brand owners toward all-polypropylene structures that simplify recycling. Investments such as Borealis's Daploy HMS PP line in Burghausen, announced with EUR 100 million in capital, illustrate how producers are aligning capacity with packaging-led demand. Automotive ranks as the second-largest segment, with polypropylene compounds central to lightweighting strategies for both internal combustion engine and electric vehicle platforms.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Market by Polymer Type: Homopolymer polypropylene leads the polymer type segmentation by a wide margin, used extensively in fibres, raffia, films, and general-purpose injection moulded parts. Its dominance reflects strong global demand for woven sacks, hygiene nonwovens, BOPP films, and consumer durables. Copolymer grades are growing faster owing to demand for impact-resistant automotive parts, premium appliance components, and clarified containers. Sinopec's 2025 start-up of a Guangxi unit capable of producing the full homopolymer and copolymer slate, alongside Borealis's automotive Daplen launches in 2025, demonstrates how producers are scaling both volume and product breadth across polymer types.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific: Asia Pacific is the dominant region in the global polypropylene market, anchored by China, India, Japan, South Korea, and ASEAN. China alone has commissioned multiple world-scale units, including Sinopec's Zhenhai phase-two completion in January 2025 and Guangxi Petrochemical's 400,000 tonne per year polypropylene start-up. Reliance Industries continues to expand its integrated petrochemical platform at Jamnagar with an USD 8.7 billion crude-to-chemicals scheme expected to be commissioned by 2027. Demand drivers include packaging for fast-moving consumer goods, automotive lightweighting, infrastructure expansion, and growing healthcare needs. Local converters are also adopting recycled and bio-based polypropylene as governments tighten plastic regulations across India, Japan, and Southeast Asia.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America: North America is the second-largest regional market, supported by competitive feedstock, integrated assets, and a strong polymer-converter base. LyondellBasell's March 2025 sanction of a 400,000 tonne per year metathesis propylene unit at its Channelview Complex near Houston signals continued investment in feedstock self-sufficiency for polypropylene. ExxonMobil's expansion of advanced recycling at Baytown, doubled in May 2025, reinforces the region's leadership in chemical recycling for polypropylene streams. Major end-use drivers include packaging, automotive, healthcare, and building and construction. Producers are increasingly focused on differentiated grades, including high-clarity, high-melt-strength, and recycled-content polypropylene, to defend share against Asian imports and align with corporate sustainability commitments.

The global polypropylene market is moderately consolidated, with the top tier comprising integrated petrochemical majors that own propylene feedstocks, polymerisation technology, and global compounding networks. LyondellBasell, Sinopec, PetroChina, ExxonMobil, SABIC, Reliance Industries, Borealis, INEOS, and Formosa Plastics dominate global capacity, while Braskem, TotalEnergies, BASF, LG Chem, and DuPont hold strong regional or differentiated positions.

Competitive priorities now centre on circular polypropylene, premium grades such as HMS and medical resins, automotive compound innovation, and feedstock optimisation. Producers are investing in advanced and mechanical recycling, certified renewable polypropylene, and joint ventures to access growing Asian and Middle Eastern demand while differentiating against rapidly expanding Chinese capacity. Strategic partnerships and consolidation around recycled polyolefin brands such as Recleo are reshaping how producers approach customer offerings.

Founded in 2007 through the merger of Lyondell Chemical Company and Basell Polyolefins, LyondellBasell is headquartered in Rotterdam and Houston. It is among the world's largest producers of polypropylene, operating proprietary Spheripol and Spherizone technologies and a global compounding footprint. Capabilities span homopolymers, copolymers, recycled and bio-based polypropylene through its Circulen portfolio, with notable strengths in automotive, packaging, and infrastructure applications.

Founded in 1998 and headquartered in Beijing, Sinopec is China's largest integrated oil and petrochemical group. It operates extensive polypropylene capacity across Maoming, Zhenhai, Guangxi, and other complexes, serving China's massive packaging, automotive, and infrastructure converters. Sinopec's 2025 completion of the Zhenhai phase-two expansion and the start-up of the Guangxi 400,000 tonne per year unit reinforce its leadership in scale, integration, and grade breadth across the homopolymer and copolymer slate.

Founded in 1973 and headquartered in Mumbai, Reliance Industries Limited is India's largest private sector company and one of the top global polypropylene producers, with capacity exceeding three million tonnes per year. Its integrated Jamnagar refining-petrochemicals complex anchors domestic supply across films, fibres, and automotive grades. Reliance's planned crude-to-chemicals expansion, valued at around USD 8.7 billion and slated for 2027 completion, will further deepen its propylene and polypropylene integration in India.

Founded in 1976 and headquartered in Riyadh, SABIC is one of the world's largest diversified chemicals companies, with significant polypropylene capacity at home and through joint ventures. Its capabilities span homopolymer and copolymer grades, certified circular polypropylene, and bio-based grades. SABIC's strengths lie in deep cost-advantaged feedstock integration, automotive and healthcare compound development, and partnerships with brand owners on certified recycled and renewable polypropylene for packaging and consumer applications.

Other key players in the market are Borealis AG, BASF SE, INEOS Group, LG Chem, DuPont, PetroChina Company Limited, Braskem S.A., Exxon Mobil Corporation, Formosa Plastics Corporation, TotalEnergies SE, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Discover the latest insights on the Global Polypropylene Market 2026 with our comprehensive report. Stay ahead of the curve with valuable data on capacity expansions, recycled and bio-based grade adoption, and high-growth end-use segments. Whether you are commissioning new capacity, sourcing recycled feedstock, or evaluating downstream investments, this report gives you the clarity you need. Download your free sample now and discover the key opportunities in the thriving Global Polypropylene industry.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market attained a volume of 94.38 MMT in 2025.

The market is estimated to grow at a CAGR of 4.50% during 2026-2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach a volume of 146.57 MMT by 2035.

The key drivers include the expanding packaging sector, increasing application of polypropylene in the automotive and healthcare sectors, and the increasing recycling of polypropylene due to rise in sustainability concerns.

The key regional markets for polypropylene are North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa.

The key applications include injection moulding, fibre, film, blow moulding, extrusion coating, and other extrusion, among others.

The market's end user includes Automotive, Building & Construction, Packaging, Medical, Electrical & Electronics, Agriculture, and other sectors.

The key players in the polypropylene market include LyondellBasell Industries Holdings B.V., China Petrochemical Corporation, PetroChina Company Limited, Braskem S.A., Exxon Mobil Corporation, Formosa Plastics Corporation, Reliance Industries Limited, TotalEnergies SE, SABIC, Borealis AG, BASF SE, INEOS Group, LG Chem, and DuPont, among others.

The Asia Pacific region led the polypropylene market, driven by increasing demand from the automotive and packaging sectors, particularly in countries like India, China, and Japan.

The market growth is being driven by the increasing use of polypropylene in fibres, raffia, and film & sheet, alongside the growing trend of applying polypropylene in the automotive sector to produce lightweight vehicles for better fuel efficiency.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Application |

|

| Breakup by End Use |

|

| Breakup by Polymer Type |

|

| Breakup by Process |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.