Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

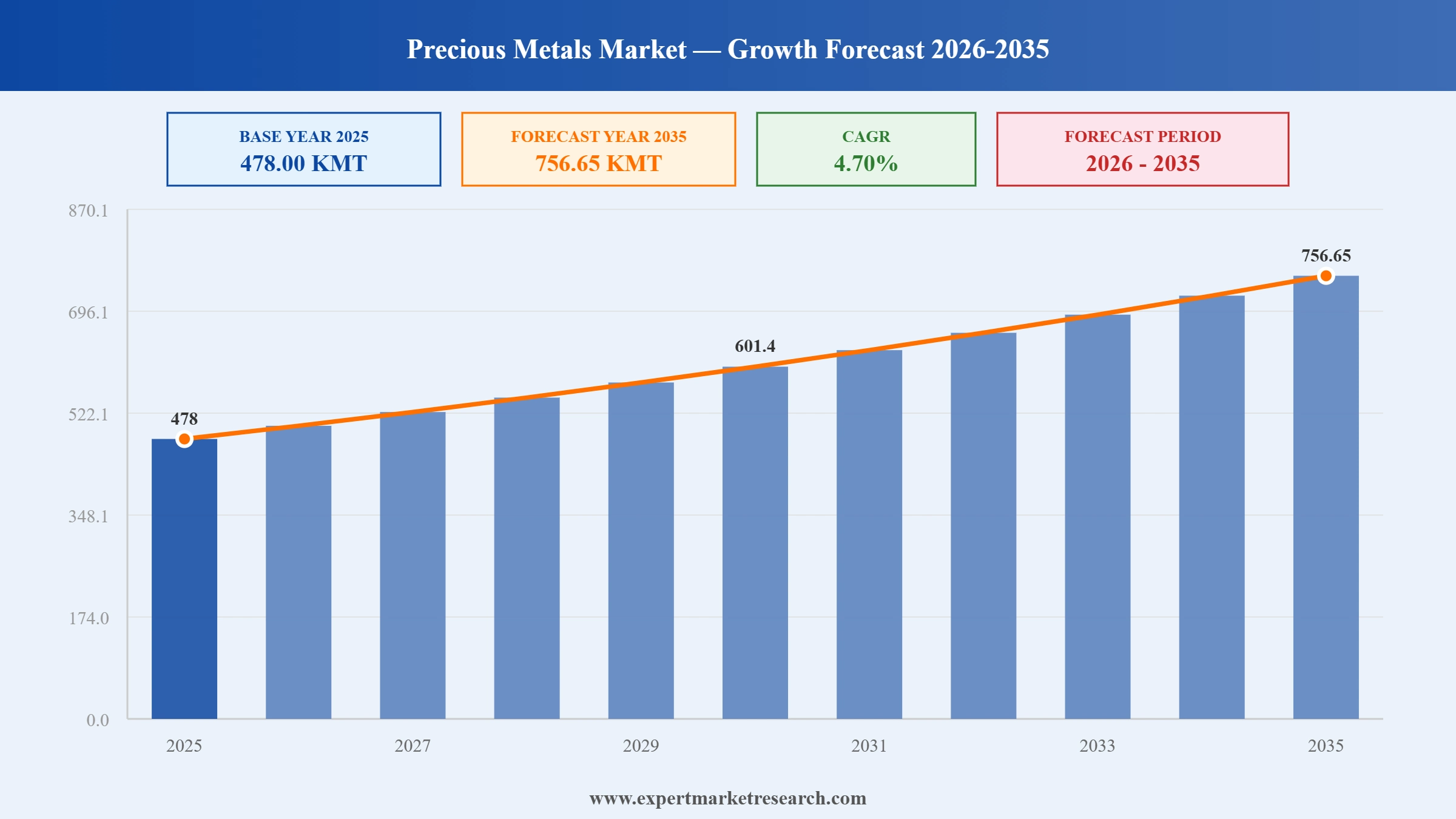

The global precious metals market reached a volume of 478.00 KMT at 2025 and is projected to grow to 756.65 KMT by 2035, expanding at a CAGR of around 4.70% between 2026 and 2035. Precious metals gold, silver, and the platinum group metals (PGMs) of platinum, palladium, and rhodium are rare, naturally occurring metallic elements prized for their scarcity, durability, conductivity, and enduring role as both industrial inputs and stores of value. The market sits at the intersection of three demand engines that rarely move in unison: investment and safe-haven buying, jewelry and adornment, and a fast-expanding base of industrial and high-technology applications spanning electronics, automotive catalysts, solar photovoltaics, hydrogen fuel cells, and medical devices.

The global precious metals market encompasses the extraction, refining, trading, and industrial and investment application of four primary metals: gold, silver, platinum, and palladium. These metals share defining characteristics: exceptional rarity relative to base metals, resistance to corrosion and oxidation, high economic value per unit weight, and a combination of physical, electrical, and catalytic properties that make them indispensable across a wide range of industrial applications. They are measured and traded in troy ounces (31.1 grams per troy ounce) at the commodity level, though market research aggregations sometimes express volumes in metric tonnes or kilo metric tonnes (KMT).

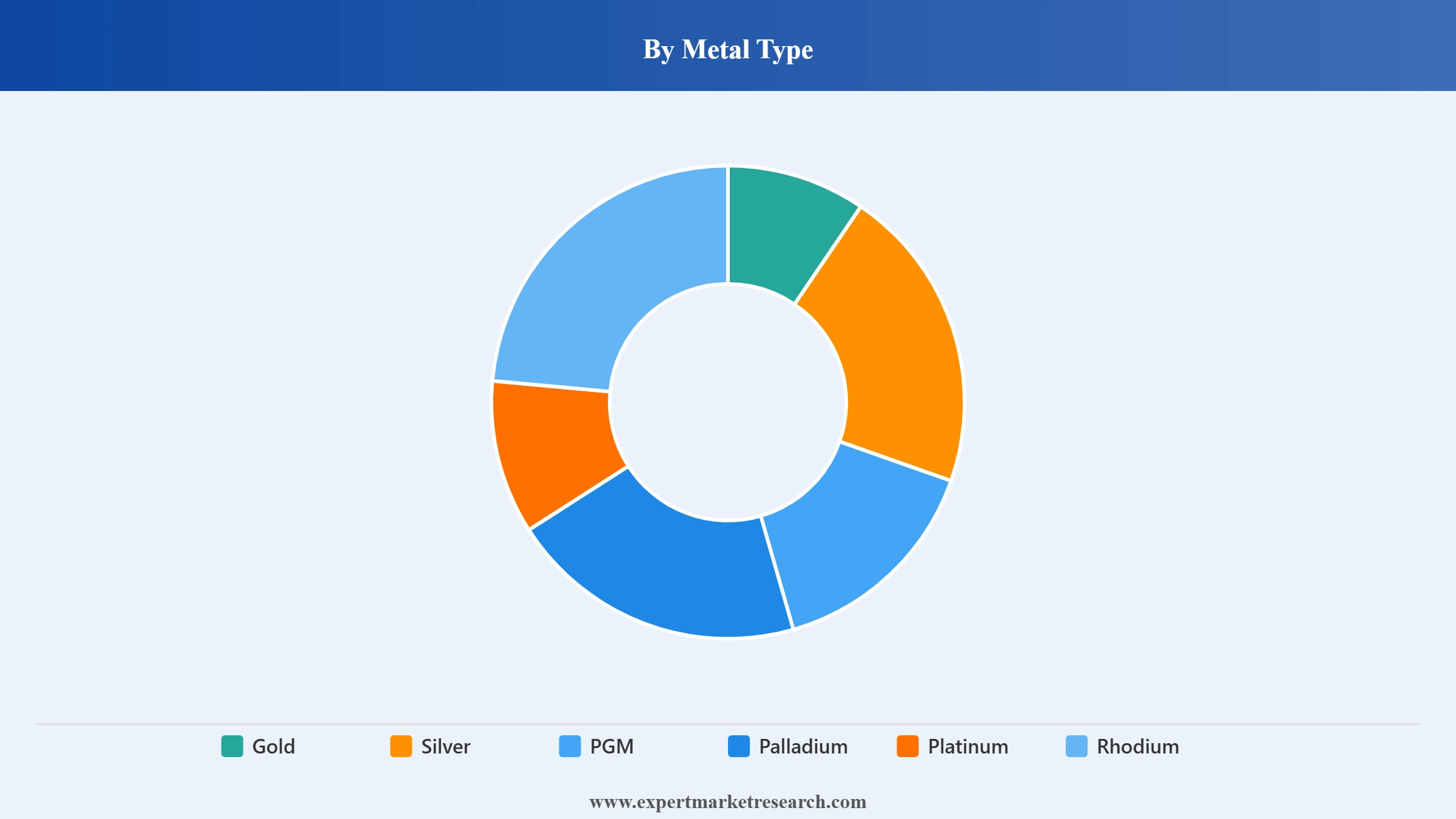

The market is structurally segmented both by metal type and by application. Gold dominates by value, accounting for approximately 71-83% of global precious metals market revenues depending on price levels and methodology. Silver is the highest-volume metal by weight and the fastest-growing by projected CAGR, driven by its dual role as both an investment metal and an increasingly critical industrial input for the green energy transition. Platinum and palladium, collectively part of the platinum group metals (PGMs), serve primarily industrial purposes, most critically as catalysts in automotive exhaust after-treatment systems, with growing emerging demand in hydrogen fuel cell technology.

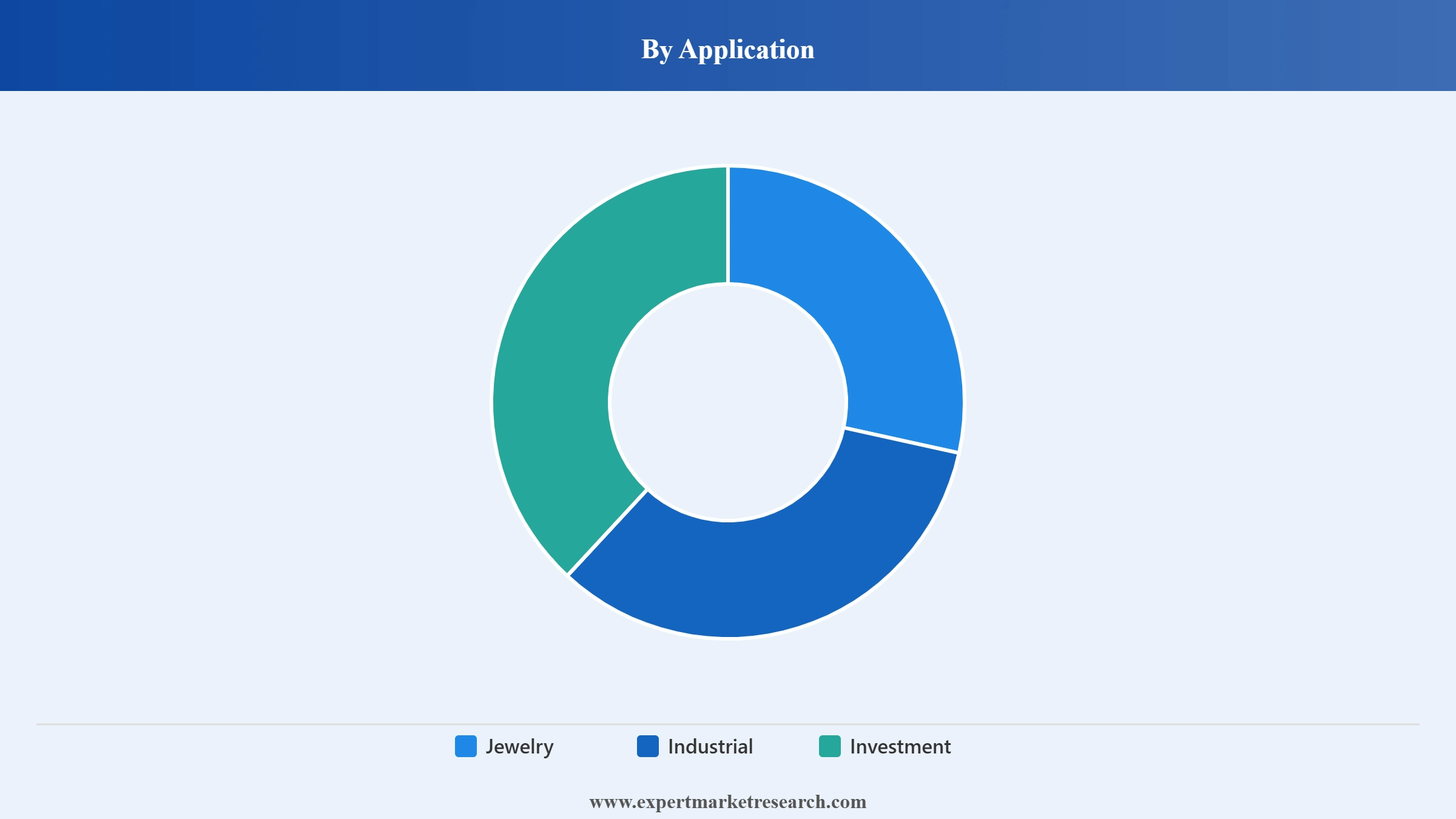

By application, jewelry accounts for the largest share at approximately 36.9% of the 2026 market, followed by investment demand and a rapidly expanding industrial segment that collectively represent over 46% of the 2025 market value. The industrial segment is the fastest-growing by application, driven by the green energy transition, electronics expansion, and automotive emission control requirements.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Geopolitical Uncertainty and Safe-Haven Investment Demand

Geopolitical tension is the most directly responsive driver of gold and silver investment demand, and 2025 illustrated this dynamic with exceptional clarity. Ongoing conflicts in Eastern Europe and the Middle East, U.S. trade policy volatility, concerns about the durability of international economic institutions, and heightened strategic competition between major powers all contributed to sustained investor flight toward the safety, liquidity, and wealth preservation attributes of gold and silver. When uncertainty rises at this magnitude, gold historically benefits from both institutional allocation and retail demand, and 2025 was consistent with this pattern at record intensity.

Central Bank Reserve Diversification Away from the U.S. Dollar

Sovereign central banks have become structural buyers of gold in a manner that represents a qualitative shift in global reserve management strategy. Central bank gold purchases since 2022 have run at more than double the 2015–2019 average, with 863 tonnes purchased in 2025 alone. Emerging market central banks in China, India, Poland, Turkey, and across the Middle East and Central Asia are systematically increasing their gold reserve allocations as a strategy to reduce dependence on U.S. dollar-denominated assets, a trend that analysts refer to as "de-dollarization." This is not cyclical safe-haven purchasing driven by a specific crisis event; it represents a deliberate multi-year reserve diversification policy that provides a persistent floor under gold demand regardless of short-term price levels.

Green Energy Transition Creating Multi-Decade Industrial Demand for Silver and PGMs

The transition to renewable energy and zero-emission transportation is generating structural long-term industrial demand for silver, platinum, and palladium that represents a significant new demand vector over and above their traditional applications. Silver is indispensable in solar photovoltaic manufacturing and high-performance electronics. Solar panels are projected to consume over 230 million ounces of silver annually by 2026, making the solar sector silver's single largest industrial demand driver. Platinum and palladium serve as essential catalysts in hydrogen fuel cells and electrolyzers technologies central to the green hydrogen production ambitions of multiple major economies. As global decarbonization commitments translate into large-scale infrastructure investment, the structural demand for these metals in clean energy applications will compound over decades.

Jewelry Demand: Cultural Traditions and Rising Middle-Class Consumption

Jewelry is the largest single application category for precious metals, accounting for approximately 36.9% of global market revenues in 2026. Gold jewelry demand is anchored by deep cultural traditions in China and India, the world's two largest gold jewelry markets, where gold ornaments are integral to wedding ceremonies, religious festivals, and generational wealth transfer practices. The combination of rising middle-class incomes, urbanization, and the expansion of organized jewelry retail across these markets creates a durable structural growth floor for gold jewelry demand even when gold prices are elevated. Silver jewelry, prized for its accessibility at lower price points than gold, is growing particularly strongly in younger consumer demographics across Asia, Europe, and Latin America.

Electronics and Semiconductor Manufacturing Driving Silver and Gold Demand

The relentless growth of the global electronics industry generates persistent industrial demand for gold and silver. Gold is used in semiconductor wire bonding, connector plating, and precision electronic contacts where its combination of corrosion resistance, conductivity, and malleability is unmatched. Silver's conductivity, the highest of any metal, makes it essential in high-performance electrical contacts, printed circuit boards, conductive inks for flexible electronics, and RFID antennas. The expansion of 5G network infrastructure, the proliferation of connected devices, and the growth of high-performance computing applications are all silver-intensive demand vectors. The electronics sector alone consumes approximately 240 million ounces of silver annually, with 8–12% growth projected through 2026.

Monetary Policy, Inflation Hedging, and ETF Investment Flows

Precious metals, particularly gold and silver, serve as established inflation hedges and monetary policy risk managers in institutional and retail investment portfolios. Federal Reserve monetary easing interest rate reductions that lower the opportunity cost of holding non-yielding assets like gold and silver, is a direct driver of investment demand. Gold-backed exchange-traded funds (ETFs) saw significant inflow growth in 2025 as institutional investors increased their precious metals allocations in response to elevated inflation uncertainty, currency debasement concerns, and portfolio diversification requirements. When real interest rates are low or negative, gold and silver investment demand is structurally elevated, creating a persistent demand pillar that complements jewelry and industrial demand.

The precious metals market is governed by a balance of structural demand drivers, cyclical investment flows, supply-side constraints and emerging technological opportunities. The dynamics below summarise the forces most likely to shape value and volume through 2035.

A defining trend is the convergence of precious metals with the clean-energy transition. Silver consumption in photovoltaic cells has become a structural pillar of demand, while platinum and iridium are increasingly specified for hydrogen electrolysers and fuel cells. In parallel, the market is professionalising around sustainability: leading miners and refiners are investing in lower-carbon extraction, water and energy efficiency, and certified responsible-sourcing chains to satisfy environmental, social and governance (ESG) mandates. Digital access is another notable trend tokenised and exchange-traded vehicles are broadening retail participation in gold and silver alongside a steady rise in secondary supply from recycling, which now materially supplements primary mine output for gold and PGMs.

Several reinforcing drivers underpin growth. Safe-haven investment demand expands during inflationary and geopolitically unsettled periods, with central banks adding to gold reserves to diversify away from single-currency exposure. Rising disposable incomes and enduring cultural significance sustain jewelry demand across Asia and the Middle East. Industrial pull is intensifying as electronics miniaturisation, electric mobility, renewable-energy infrastructure and medical technology each raise consumption of silver, gold and PGMs. Finally, the metals’ role as a hedge against currency depreciation keeps them embedded in diversified portfolios, lending the market a demand floor that few commodity classes enjoy.

The market faces meaningful headwinds. Price volatility driven by macro sentiment, currency swings and speculative positioning complicates planning for industrial buyers and can destabilise margins across the chain. High capital intensity and long permitting and development timelines constrain the responsiveness of new mine supply, while the geographic concentration of PGM production exposes the market to geopolitical and logistical disruption. Technological substitution is a structural risk: thrifting and material substitution in electronics and catalysis, and the shift toward battery-electric vehicles that require no autocatalyst, can erode demand in specific applications. Regulatory and environmental compliance costs add further pressure, particularly for smaller producers and refiners.

The clearest opportunity lies in the energy transition, where silver and PGMs are positioned as enabling materials for solar, hydrogen and grid-scale electrification. Recycling and urban mining represent a fast-growing, lower-footprint supply stream that also strengthens ESG credentials and supply security. Emerging-market wealth creation across South-East Asia, the GCC and parts of Africa and Latin America expands the jewelry and investment base. Product and channel innovation, from fractional digital ownership to new ETF structures and bank-backed savings products, opens precious metals to a wider, younger investor cohort. Companies that integrate refining, build circular-economy capacity and certify responsible sourcing are best placed to capture disproportionate value.

The market is segmented by type into gold, silver and platinum group metals, and by application into industrial, jewelry, investment and other uses. Each segment is governed by a distinct demand logic, and their combination is what gives the sector its diversified, resilient growth profile.

Market Breakup by Metal Type

Key Insight: By value, gold is the cornerstone of the precious metals market. Its demand spans central-bank reserves, exchange-traded funds, bar-and-coin investment and an extensive global jewelry trade, making it the principal store-of-value asset within the sector and the segment most sensitive to monetary policy and currency movements. Silver, while lower in unit value, is the volume leader and the most industrially exposed of the major metals: photovoltaics, electrical contacts, electronics, brazing alloys and medical applications now account for a substantial share of its consumption, layering structural industrial growth on top of its traditional investment and ornamental roles. This dual character makes silver both a beneficiary of the energy transition and a participant in precious-metals investment cycles.

Market Breakup by Application

Key Insight: The jewelry application remains the largest single consumer of precious metals by volume, anchored by deep cultural demand in India, China and the Middle East and supported by rising disposable incomes and evolving fashion preferences. The investment application bullion, coins, ETFs and digital products is the most cyclical but also the most powerful counter-weight, expanding sharply during periods of economic stress and lending the market its safe-haven character. Industrial applications are the fastest-structurally-growing segment, propelled by electronics, automotive catalysis, solar energy, hydrogen technologies and medical devices; this is where the energy transition is converting precious metals into strategic materials. The “others” category captures uses such as dentistry, chemical process catalysis and specialised electronics, rounding out a demand base that spans finance, fashion and high technology.

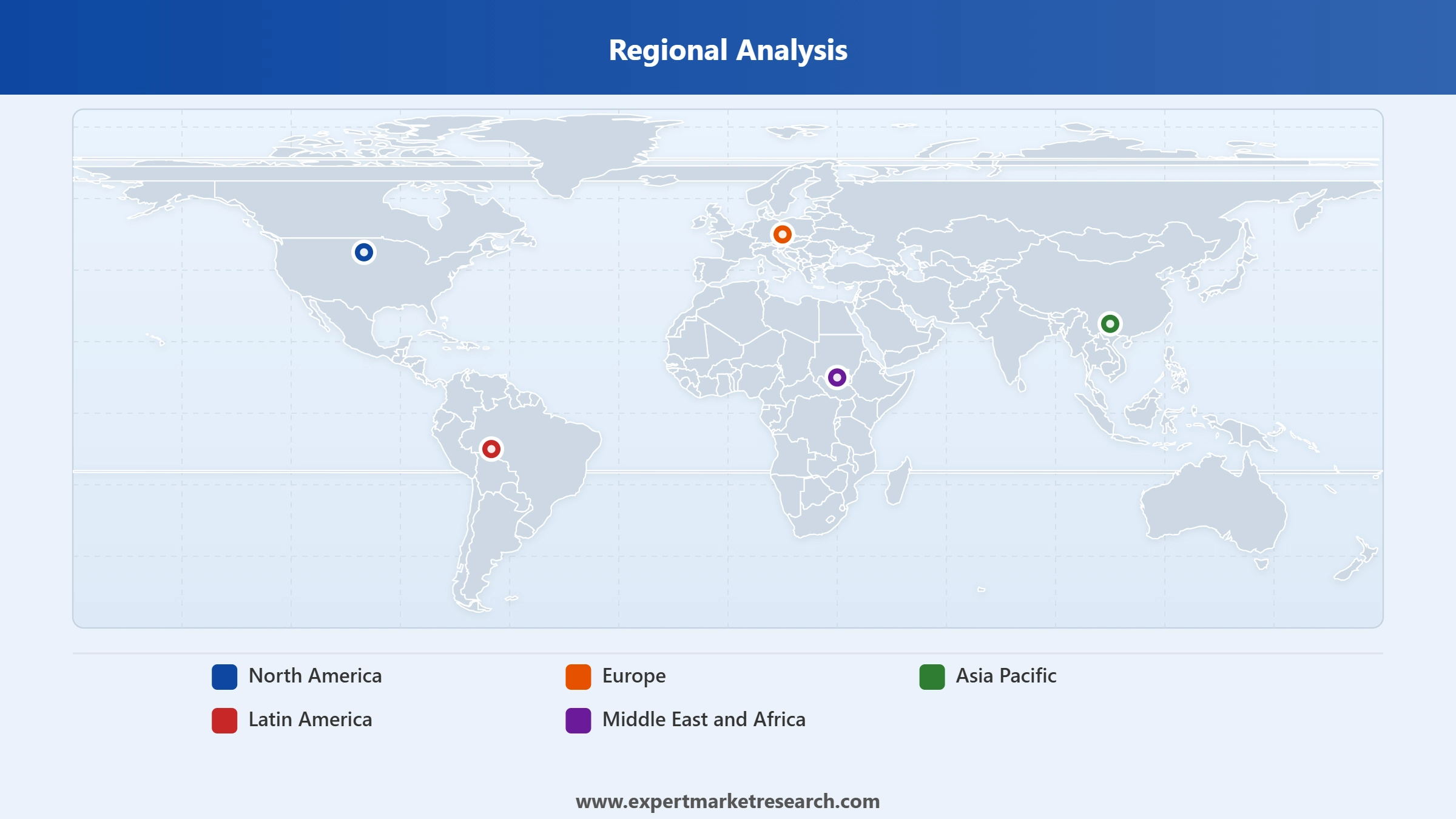

Market Breakup by Region

Key Insight: Asia Pacific holds the largest share of the global precious metals market both as a major producer, with China being a leading gold producer and Australia a significant gold exporter, and as the world's dominant precious metals consumer through jewellery demand from India and China. Middle East And Africa is the second most significant region, encompassing South Africa's historically dominant platinum and gold mining industry along with significant gold production across Ghana, Tanzania, and Mali. North America hosts several of the world's largest gold mining companies including Barrick Mining and Newmont Corporation.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Metal Type, gold accounts for the dominant share of the market due to its universal role as a financial reserve asset, jewellery material, and industrial component with no viable substitute in critical applications.

Gold commands approximately 50% of the global precious metals market by value, underpinned by central bank reserve holding programmes that collectively represent the largest institutional gold demand segment globally. The sustained gold purchasing by central banks in China, India, Turkey, and other emerging market economies reflects a structural shift toward gold as a reserve diversification tool. Barrick Mining's extensive portfolio of Tier One gold mines across five continents and Newmont Corporation's diversified global gold production base collectively represents the two largest gold mining enterprises in the global precious metals market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Silver occupies the second-largest metal position in the global precious metals market, uniquely positioned at the intersection of investment demand and industrial consumption. The rapid expansion of global solar photovoltaic installation capacity, driven by climate policy commitments and falling solar module costs, is creating structural long-term industrial silver demand growth that is partially decoupled from economic cycles. Gold Fields Limited and Kinross Gold Corporation, while primarily gold producers, operate in geological provinces where silver co-production generates meaningful additional revenue contributions alongside core gold output.

By Application, jewellery accounts for the dominant share of the market due to the deep cultural significance of gold and platinum jewellery in major consumption markets including India, China, and the Middle East.

Jewellery accounts for approximately 40% of global precious metals market demand by value, with gold jewellery consumption in India alone representing one of the world's single largest demand drivers. Indian gold jewellery demand is tied to the approximately 10 million annual wedding ceremonies where gold ornaments are culturally obligatory gifts, creating consistent structural demand regardless of gold price levels. The Middle East and Africa region's jewellery market, anchored by Gulf Cooperation Council consumers' strong preference for 22-karat gold ornaments, further sustains global jewellery demand in the global precious metals market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Industrial applications represent the fastest-growing demand segment in the global precious metals market, with silver's expanding solar photovoltaic use and platinum group metals' automotive and hydrogen fuel cell applications driving growth above the overall market rate. Freeport-McMoran and Anglo-American Plc operate major PGM and copper production operations that generate platinum, palladium, and rhodium as co-products from base metals mining, positioning them as important PGM suppliers alongside dedicated platinum group metals producers including Northam Platinum Holdings in South Africa.

Demand is distributed across five major regions, each with a distinct blend of jewelry, investment and industrial consumption. Asia-Pacific leads global volume, while North America and Europe contribute mature investment and industrial demand, and the Middle East & Africa and Latin America offer both consumption growth and critical supply.

Asia-Pacific Precious Metals Market Analysis

Asia-Pacific is the dominant precious metals market, driven by the scale of jewelry consumption and investment demand in China and India and by the region’s expansive electronics and solar manufacturing base. China leads across the full spectrum jewelry, investment and industrial use supported by its position as both a major producer and the world’s largest manufacturing hub, which sustains high consumption of silver and PGMs in electronics and automotive production. India’s deep cultural affinity for gold, together with rising incomes and a fast-growing investment culture, makes it a structural growth engine, while South-East Asia adds an emerging-market layer of jewelry and investment demand.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America Precious Metals Market Analysis

North America is a mature, investment-led market underpinned by sophisticated financial markets, widespread ETF adoption and strong safe-haven demand for gold and silver. The United States is the region’s largest single market, combining robust investment activity with substantial industrial consumption across electronics, aerospace and the automotive sector. Demand for PGMs and silver is reinforced by the region’s adoption of electric vehicles and renewable-energy infrastructure, and by a favourable regulatory environment and advanced mining and refining capacity that support steady, technology-aligned growth.

Europe Precious Metals Market Analysis

Europe blends mature investment demand with a heavy industrial draw, particularly for platinum and palladium used in automotive catalytic converters. Germany’s large automotive manufacturing base anchors PGM consumption, while the region’s refiners and recyclers are increasingly central to a circular precious-metals value chain. Geopolitical developments have reshaped historical supply relationships, prompting diversification of sourcing and accelerated investment in recycling and responsible-sourcing infrastructure. The result is a region where industrial and investment demand together deliver steady performance and where ESG-aligned value-chain integration is a defining competitive theme.

Middle East & Africa Precious Metals Market Analysis

The Middle East & Africa region combines strong jewelry and investment demand especially across the GCC, where gold holds deep cultural and store-of-value significance with a critical role in global supply. Africa is a cornerstone of world PGM and gold production, giving the region strategic importance on the supply side even as Gulf markets drive consumption. Rising tourism, wealth accumulation and the development of regional bullion trading hubs are expanding the market, while investment in local refining and value addition is gradually deepening the region’s position in the precious-metals chain.

Latin America Precious Metals Market Analysis

Latin America is primarily a supply-side powerhouse, hosting major silver and gold production across Mexico, Peru and the broader Andean belt, while also developing growing domestic jewelry and investment demand. The region’s mineral endowment makes it pivotal to global silver supply in particular, linking its fortunes to industrial and solar demand worldwide. Expanding investment in mining infrastructure, alongside rising regional incomes, supports a dual narrative of resource production and gradually maturing local consumption.

The global precious metals market's mining segment is moderately concentrated among a group of large multinational producers, with Barrick Mining Corporation and Newmont Corporation collectively representing the world's two largest gold mining enterprises. The competitive landscape is shaped by the distinct geographic concentration of different metal types: gold production is geographically diversified across five continents, while platinum group metal production is heavily concentrated in South Africa's Bushveld Igneous Complex and Russia's Norilsk mining region. Major companies compete on production cost efficiency, reserve quality, project development pipeline, and capital allocation discipline.

Founded in 1917 and headquartered in London, United Kingdom, Anglo American Plc is a globally diversified mining company with significant precious metals operations including platinum group metals through its Anglo American Platinum subsidiary, one of the world's largest primary PGM producers operating mines in the Bushveld Igneous Complex of South Africa. Anglo American's PGM operations produce platinum, palladium, and rhodium as primary products alongside gold co-production. The company's strategic review processes and portfolio optimisation efforts have made it a focal point of mining sector corporate activity in the global precious metals market in recent years.

Founded in 1921 and headquartered in Denver, Colorado, Newmont Corporation is the world's largest gold mining company by production volume, operating gold and silver mines across nine countries including the United States, Australia, Canada, Peru, Ghana, and Mexico. Newmont's emphasis on technological innovation and sustainability in its mining operations, including the deployment of autonomous haul trucks and renewable energy integration at mine sites, positions it as an industry benchmark for responsible precious metals production. The company's extensive global reserve base and consistent dividend policy make it a preferred investment vehicle for exposure to the global precious metals market.

Founded in 1994 and headquartered in Johannesburg, South Africa, Northam Platinum Holdings Limited is a leading independent platinum group metals producer operating the Booysendal and Zondereinde mines in South Africa's Bushveld Igneous Complex, which collectively produce platinum, palladium, rhodium, and ruthenium. The company has pursued an aggressive organic growth strategy through the mechanised expansion of its Booysendal North and South operations. Northam Platinum's significant ownership stake in Royal Bafokeng Platinum adds further production capacity exposure in the global precious metals market's critical PGM supply segment.

Founded in 1983 and headquartered in Toronto, Canada, Barrick Mining Corporation (rebranded from Barrick Gold Corporation in May 2025) is a leading global gold and copper mining company with six Tier One gold mines and operations spanning 18 countries. In February 2026, Barrick announced plans for an IPO of NewCo to maximise value from its Nevada Gold Mines joint venture and Pueblo Viejo assets. In September 2025, Barrick agreed to sell its Hemlo mine for up to USD 1.09 billion as part of its non-core asset divestiture programme generating approximately USD 2.6 billion in 2025, shaping competitive positioning in the global precious metals market.

Other key players in the market are Southern Copper Corporation, Newcrest Mining Limited, Kinross Gold Corporation, Polyus, Gold Fields Limited, Freeport-McMoRan, AngloGold Ashanti, and Randgold and Exploration Company Limited, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

May 2026 - Equinox Gold and Orla Mining agreed a transformative USD 18.5 billion all-stock merger. The two producers announced a combination designed to create a leading North American gold company, consolidating complementary asset bases and unlocking operational and cost synergies. The deal exemplifies the broader wave of consolidation sweeping the gold-mining sector, as producers scale up to capture historically high gold prices, strengthen their reserve and production profiles, and improve access to capital. By building larger, more diversified portfolios anchored in stable mining jurisdictions, the merged entity is positioned to deliver greater free cash flow and resilience through commodity-price cycles.

April 2026 - Trafigura entered Ghana's gold sector with a landmark offtake-and-financing package. On 9 April 2026, global commodity trader Trafigura signed an offtake agreement with Ghanaian-owned Heath Goldfields to purchase 700,000 ounces of gold doré from the Bogoso–Prestea mine in Ghana's Western Region, while extending a USD 65 million debt-financing facility to restart the mine's oxide-ore operations after a two-year hiatus. Valued at roughly USD 2.3 billion at prevailing gold prices, the agreement marked Trafigura's first transaction in West Africa's largest gold producer and a significant step in the expansion of its dedicated precious-metals trading desk. The structure pairing a long-term purchase commitment with upfront capital underscores how trading houses are increasingly using resource-backed financing to secure future supply, de-risk dormant assets and deepen their footprint across African gold production.

April 2026 - Wheaton Precious Metals closed a USD 4.3 billion silver stream on the Antamina mine in Peru. Effective 1 April 2026, Wheaton acquired BHP's 33.75% share of payable silver from the world-class Antamina mine, doubling its total exposure there to 67.5% and cementing one of the cornerstone assets in its streaming portfolio. The transaction is expected to add approximately 6.0 million ounces of attributable silver per year over its first five years, materially boosting Wheaton's production and cash-flow profile. The deal illustrates the growing strategic importance of streaming and royalty models in financing precious-metals supply, offering investors leverage to silver prices and exploration upside while carrying a lower operating-risk profile than conventional mining.

April 2026 - Wheaton Precious Metals expanded into Australia with a USD 275 million gold-and-silver stream on the Jervois Project. Wheaton's first streaming transaction in Australia one of the world's premier mining jurisdictions, covers a portion of the gold and silver produced at the fully permitted Jervois project and is expected to add 92,000 ounces of gold and 9.2 million ounces of silver to the company's attributable reserves over a projected ten-year mine life, with first production anticipated in the second half of 2027. The move reflects a deliberate strategy of deploying capital into long-life, low-cost assets in stable jurisdictions to sustain diversified, multi-decade production growth.

December 2025 - Trafigura backed Sierra Leone's first commercial-scale gold mine. Ahead of its later Ghana entry, Trafigura joined a lending group supporting the development of Sierra Leone's first large-scale commercial gold operation through a structured debt-financing arrangement. The transaction marked an early milestone in the trading house's broader move into precious metals as bullion prices surged, and demonstrated how commodity traders are deploying substantial cash reserves to secure supply relationships and unlock financing for emerging African gold projects.

Explore the full scope of intelligence on the global precious metals industry from 2026 with our comprehensive market report. Gain insights on production dynamics, investment demand trends, industrial applications growth, corporate strategy developments, and regional market shifts defining the precious metals landscape. Whether you are a mining company, metal trader, industrial user, jewellery manufacturer, or investor, this report delivers the strategic intelligence needed. Download your free sample today and discover the key opportunities in the global precious metals industry through 2035.

Upto 15% Off

USD

$3999 $3599

$2499 $2249

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market reached a volume of 478.00 KMT in 2025.

The market is projected to grow at a CAGR of 4.70% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach a volume of 756.65 KMT by 2035.

The key types are gold, silver, pgm, platinum, palladium, and rhodium.

The key regional markets for precious metals are North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa.

The factors driving the growth of the market are the rising demand for precious metals in jewellery, the increasing use of platinum and palladium in the automotive sector, and the emerging demand for lightweight vehicles.

The key trends of the market include the increasing adoption of gold and silver as investments, rising technological advancements, and the expansion of the semiconductor manufacturing sector.

The key players in the market include Anglo American Plc, Southern Copper Corporation, Newmont Corporation, Northam Platinum Holdings Limited, Newcrest Mining Limited, and Kinross Gold Corporation, Polyus, Gold Fields Limited, Freeport-McMoRan, Barrick Gold, Gold Fields Limited, AnglogoldAshanti, and Randgold & Exploration Company Limited, among others.

Based on metal segment, gold held the largest revenue share owing to high price and application in jewelry and investment.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Metal Type |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.