Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

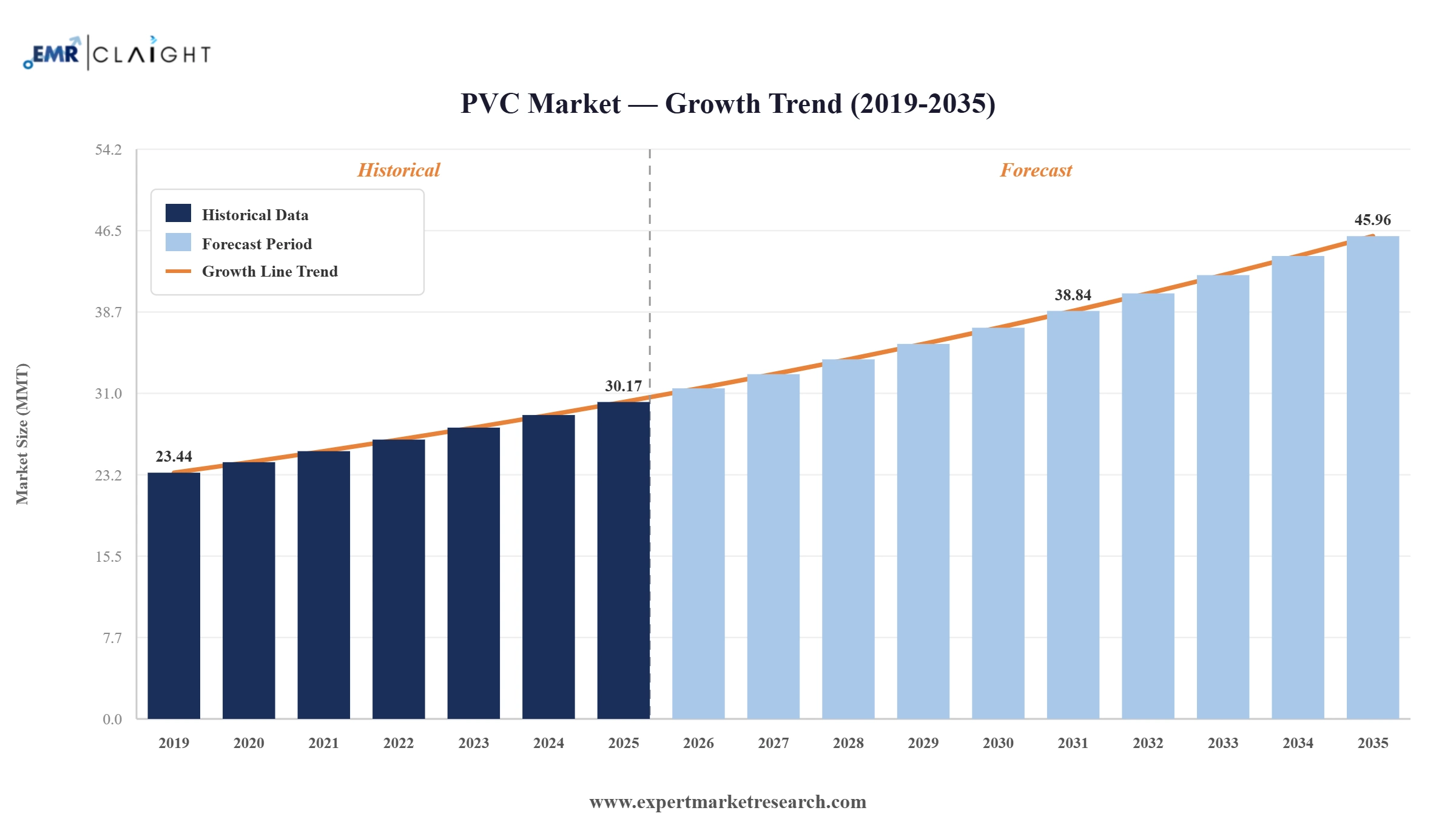

The global PVC market reached a volume of 30.17 MMT in 2025 and is projected to expand at a CAGR of around 4.30% during the forecast period of 2026-2035. Growing infrastructure construction, the calcium-based stabiliser transition under lead phase-out, electrical grid expansion driving wire and cable demand, and growing healthcare and packaging end use are fuelling growth. The market is expected to reach 45.96 MMT by 2035.

According to Plumbing & Mechanical, Charlotte Pipe implemented a 10% price increase on PVC and CPVC pipe effective March 26, 2026, with wider PHCP-PVF pricing adjustments rolling through mid-April. The double-digit hikes reflect persistent inflationary pressures on resins, signaling firmer pricing dynamics across the North American PVC value chain heading into the spring construction season.

According to Plastics News, North American suspension PVC prices rose in March 2026 alongside polypropylene and polystyrene, as supply constraints, higher feedstock costs, and stronger export demand tightened domestic markets. The upward movement marks a notable reversal from the prolonged price weakness seen during 2025, suggesting producer discipline and reduced inventory could underpin firmer PVC pricing through the second quarter.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Global PVC Market Report Summary | Description | Value |

| Base Year | MMT | 2025 |

| Historical Period | MMT | 2019-2025 |

| Forecast Period | MMT | 2026-2035 |

| Market Size 2025 | MMT | 30.17 |

| Market Size 2035 | MMT | 45.96 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 4.30% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 5.0% |

| CAGR 2026-2035 - Market by Country | India | 5.7% |

| CAGR 2026-2035 - Market by Country | China | 4.7% |

| CAGR 2026-2035 - Market by Product Type | Chlorinated PVC | 4.9% |

| CAGR 2026-2035 - Market by End Use | Building and Construction | 5.1% |

| Market Share by Country 2025 | UK | 3.7% |

The global PVC market is converging capacity investment, sustainability transitions, and construction demand recovery. Major producers are committing to large-scale feedstock integration in North America while advancing recycled and low-VOC product portfolios in Europe.

Shintech Inc., the US subsidiary of Shin-Etsu Chemical, announced a USD 3.4 billion investment on March 5, in the year 2026 to expand its Louisiana footprint with the new ethylene, chlorine, and PVC facilities, targeted for completion by 2030. The investment is one of the largest capital commitments in the global PVC market, positioning the Shintech forthe North American demand recovery as Chinese excess capacity eases.

Westlake Corporation had completed the acquisition of ACI in January of 2026. They had been strengthening their exposure to the high-voltage wire and cable market. The deal complements Westlake's PVC resin and compound capabilities for electrical infrastructure driven by grid modernisation and data centre construction.

INEOS Group had upgraded its European PVC plants in July 2025 to produce high-performance, low-VOC PVC resins for the sustainable building materials. The upgrade positions INEOS for growing European demand for compliant PVC in profiles, flooring, and construction under tightening EU emissions regulations.

Orbia launched its Vinyl in Motion PVC recycling initiative in May 2025, aimed at repurposing post-consumer PVC into pipes, flooring, and building products. The programme supports circular economy targets while lowering resin acquisition costs across the Americas and Europe.

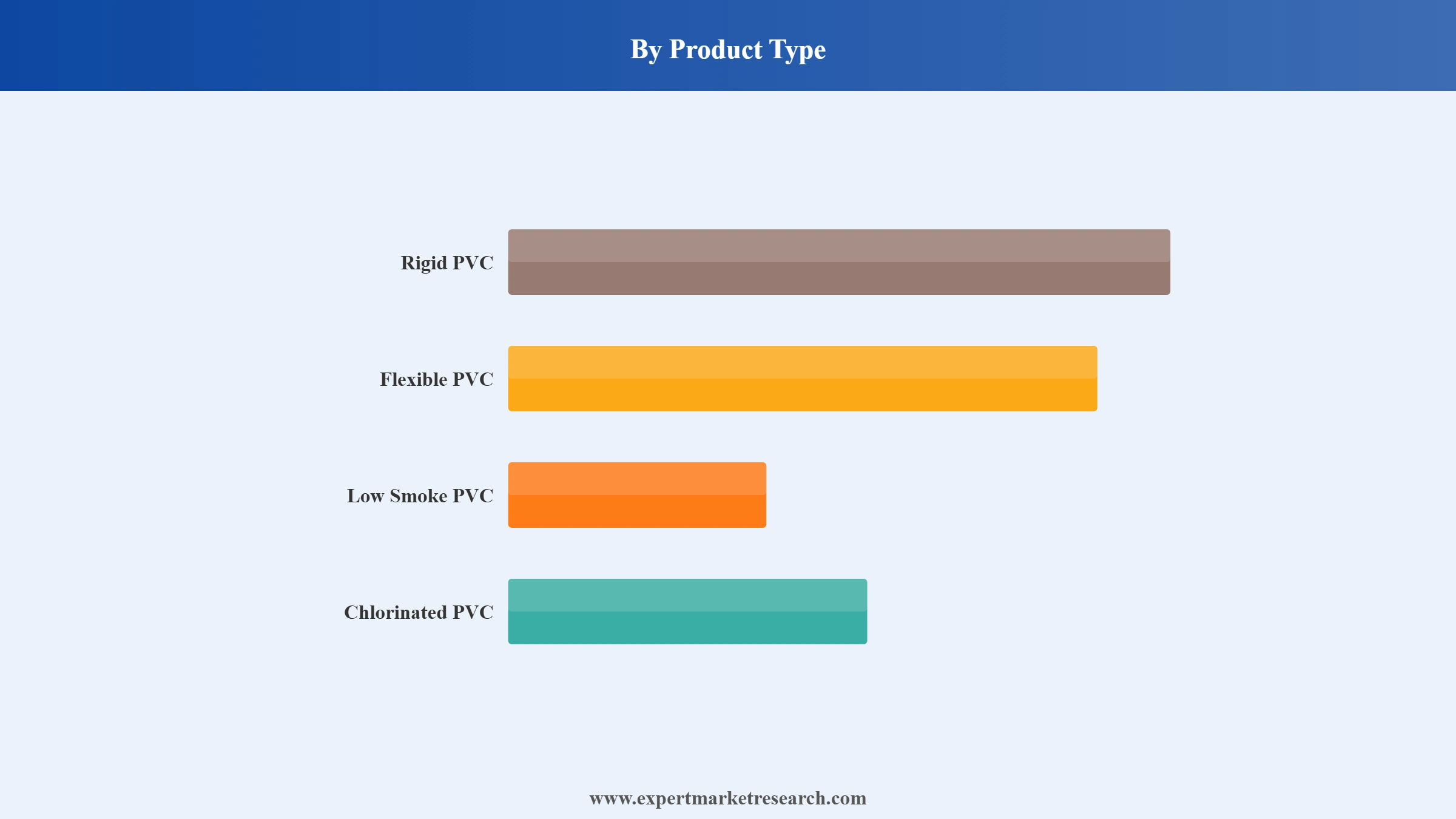

Rigid PVC is the dominant product type in the global PVC market, anchored by pipes, profiles, flooring, and construction components. Construction contributes over 50% of total PVC demand globally, with rigid formulations serving the majority of this volume across infrastructure and residential building.

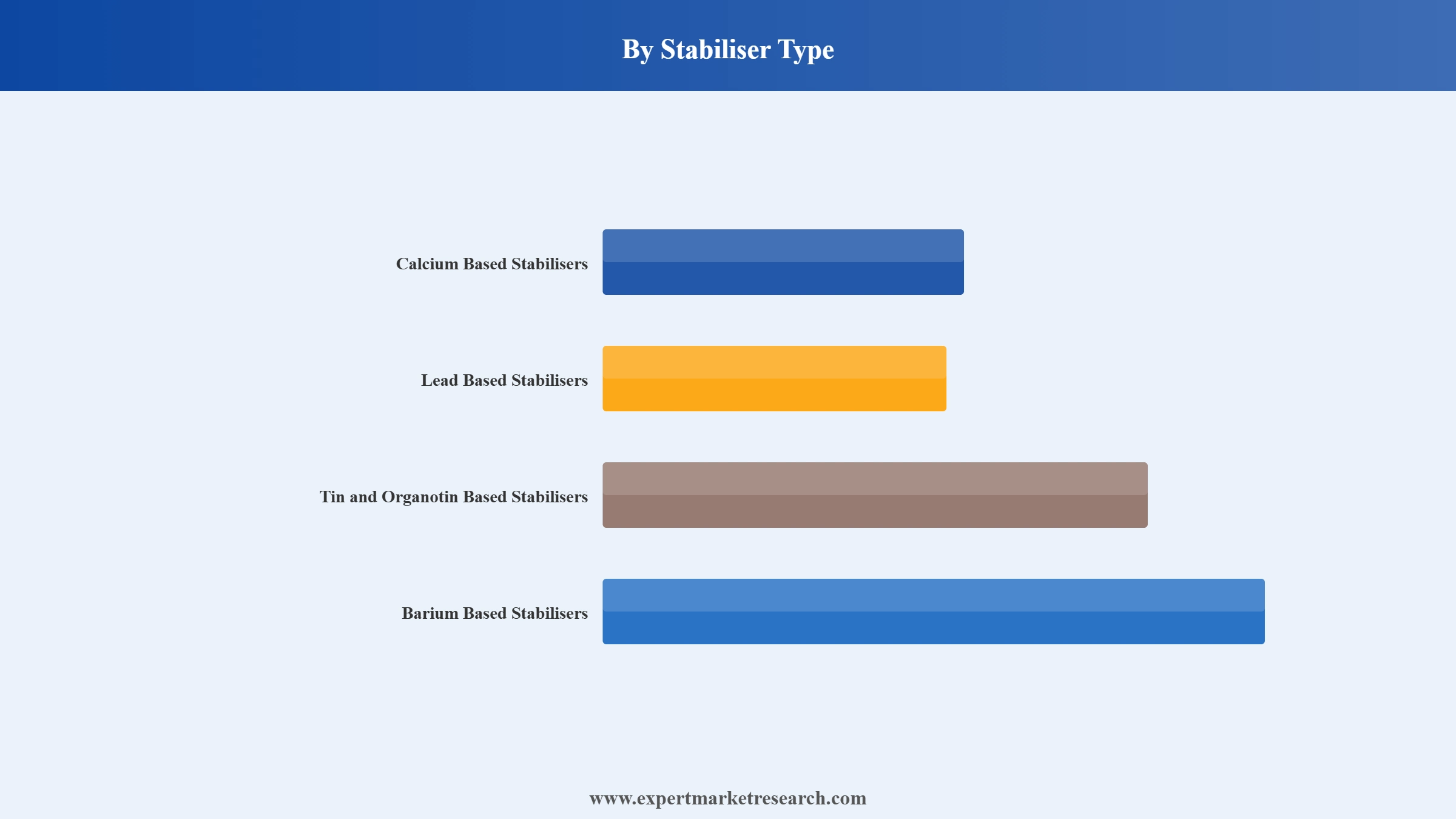

Calcium-based Ca-Zn stabilisers are the fastest-growing stabiliser category, benefiting from lead phase-outs across Europe, North America, and progressively Asia. Ca-Zn systems offer non-toxic performance meeting REACH and RoHS requirements while maintaining processing efficiency across rigid and flexible PVC applications.

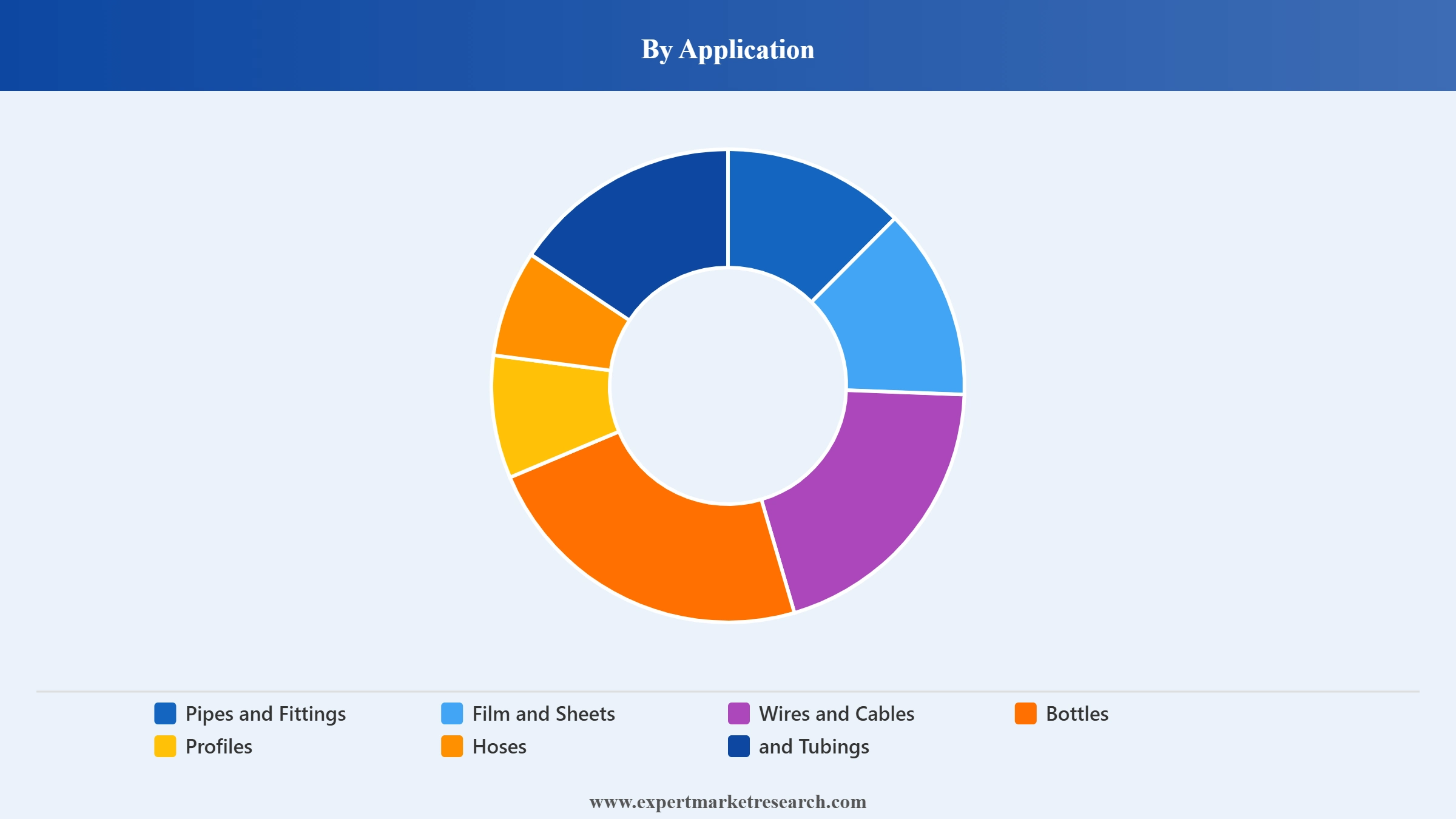

Pipes and fittings commands the dominant application share at over 45% of total global PVC consumption. Infrastructure investment across water supply, sewerage, and agriculture in Asia Pacific and the Middle East sustains large and growing pipe volumes.

Building and construction accounts for over 50% of total PVC demand, sustained by residential construction in Asia and the Middle East, commercial building in North America, and renovation programs in Europe across pipes, profiles, and flooring.

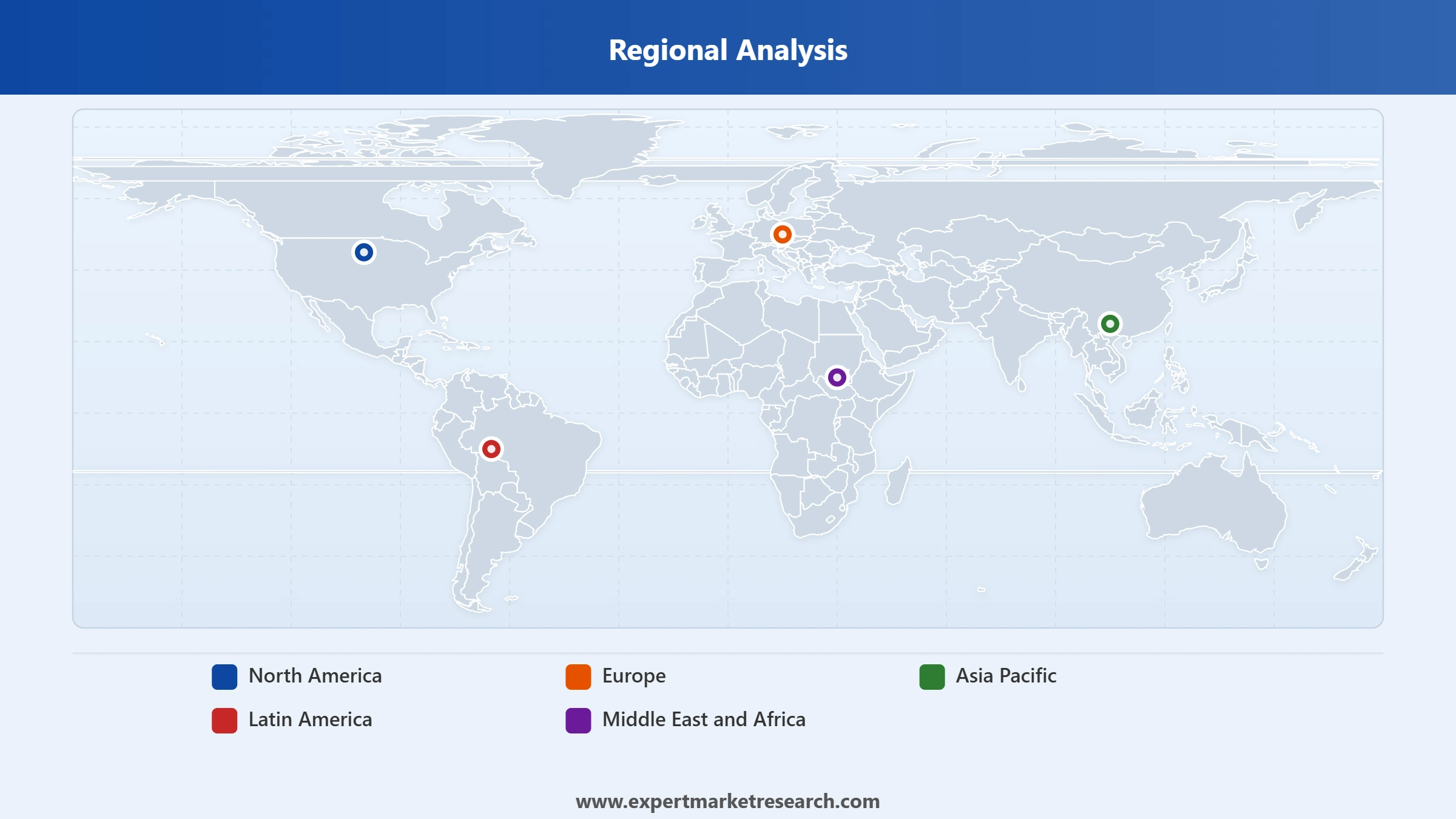

Asia Pacific accounts for over 65% of total global PVC consumption, with China contributing approximately 45% of global demand. The region's construction and manufacturing base sustains production investment and volume growth, while Chinese export pricing remains the primary external variable shaping global PVC price trends.

The "Global PVC Market Report and Forecast 2026-2035" by Expert Market Research offers a detailed analysis of the market based on the following segments:

Market Breakup by Product Type

Key Insight: Rigid PVC dominates through construction, infrastructure, and packaging. Low Smoke PVC is gaining ground in electrical applications under tightening fire-safety codes. Chlorinated PVC serves high-temperature plumbing and industrial piping, growing with commercial construction.

Market Breakup by Stabiliser Type

Key Insight: Lead-based stabilisers retain share where phase-out is not yet mandated. Ca-Zn stabilisers are the fastest-growing type, driven by REACH compliance and expanding non-toxic formulation demand across all major PVC end-use sectors.

Market Breakup by Application

Key Insight: Pipes and fittings commands the dominant application share through infrastructure and irrigation investment. Wires and cables is the fastest-growing segment through grid expansion and data centre construction. Film and sheets serve flexible packaging and medical applications.

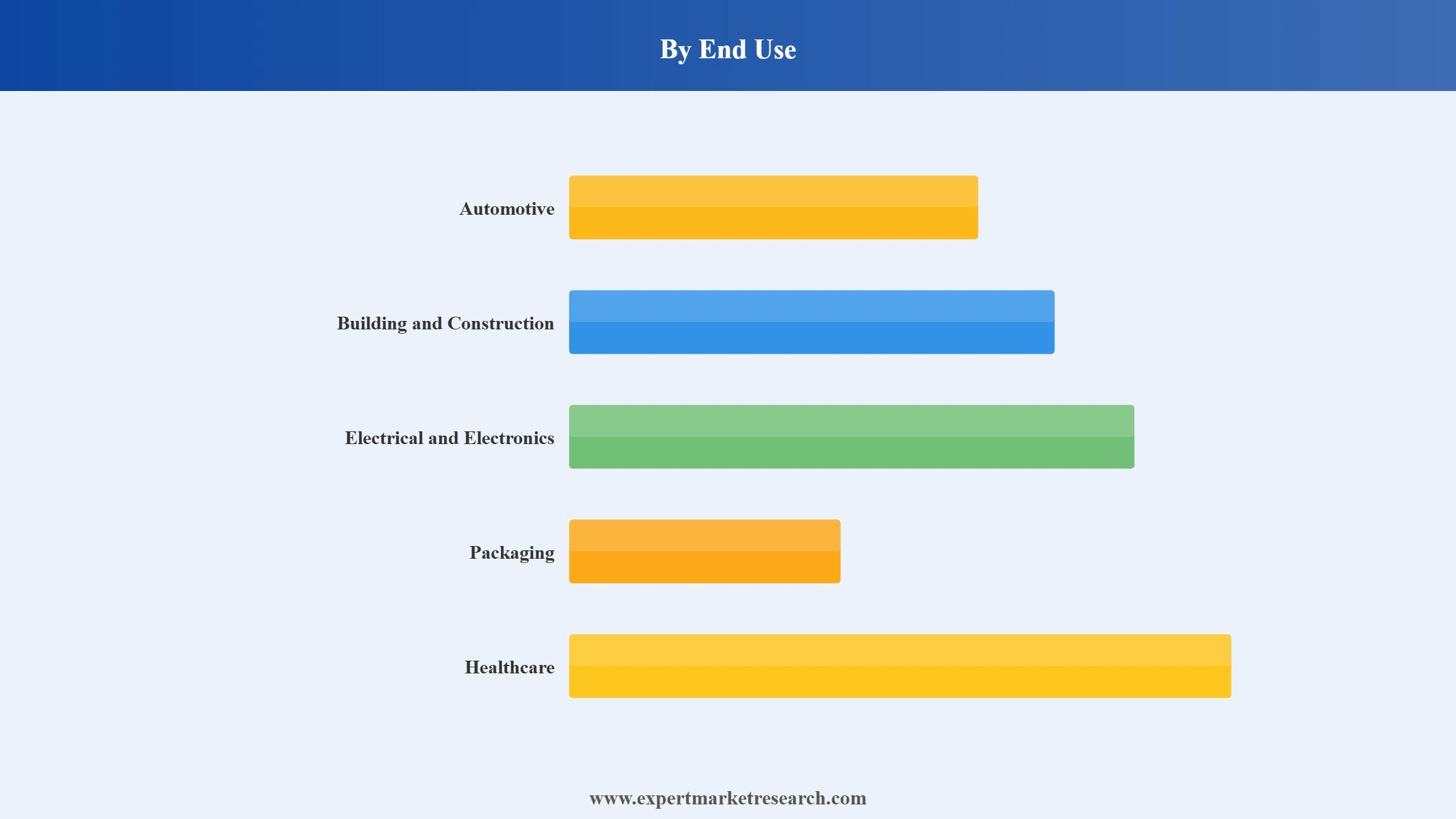

Market Breakup by End Use

Key Insight: Building and construction dominates at over 50% of global PVC consumption. Electrical and electronics is fast-growing through power infrastructure modernisation and EV charging expansion. Healthcare is a stable, premium-margin segment through medical tubing and blood bag applications.

Market Breakup by Region

Key Insight: Asia Pacific dominates with over 65% of global PVC consumption, anchored by China and India's construction sectors. Europe is advancing Ca-Zn adoption and recycled PVC integration under EU circular economy mandates. North America is seeing major fresh capacity investment through Shintech's USD 3.4 billion Louisiana expansion.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Product Type, Rigid PVC dominates the global PVC market due to its critical role in construction, infrastructure pipes, and building profiles globally

Rigid PVC commands the largest share through durability, corrosion resistance, and cost-effectiveness in construction pipe, profiles, flooring, and roofing. China and India are the highest-volume consumers through large-scale pipe and building material demand.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Stabiliser Type, Lead Based Stabilisers currently hold significant global share but Calcium Based Ca-Zn systems are the fastest-growing category

Lead-based stabilisers retain share where phase-out is not yet implemented, particularly in Asia Pacific and Middle East and Africa. Calcium-based Ca-Zn systems are rapidly capturing share as brand owners globally mandate non-toxic PVC inputs.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Application, Pipes and Fittings account for the dominant share due to large infrastructure and agricultural water network investment globally

Pipes and fittings consume the largest share of global PVC through water supply, sewerage, irrigation, and utility infrastructure. In India alone, pipes represent approximately 73% of PVC consumption, with government-funded programs sustaining non-discretionary demand.

Wires and cables is the fastest-growing application through grid modernisation, EV charging, and data centre construction. Film and sheets serve food and pharmaceutical flexible packaging; profiles anchor the European window and door market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By End Use, Building and Construction accounts for the dominant share due to PVC's pervasive use across pipes and construction components globally

Building and construction is the largest end-use at over 50% of global PVC output, driven by residential construction in Asia Pacific, infrastructure in the Middle East, and renovation in Europe. PVC's cost, versatility, and weathering resistance make it dominant across multiple construction components.

Electrical and electronics is the second-fastest end use through power grid investment and digital infrastructure expansion. Healthcare is a smaller but high-value segment through blood bags, IV tubing, and surgical drains.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific dominates the global PVC market due to China's dominant production capacity, India's rapidly growing construction sector, and the region's large industrial manufacturing base

Asia Pacific commands over 65% of global PVC consumption, with China accounting for approximately 45% of world demand. India is the fastest-growing national market through infrastructure programs, with per capita consumption of just 2.4 kg per annum. Asia Pacific is growing at 5.00% CAGR through the forecast period.

Europe is advancing Ca-Zn adoption and recycled PVC integration under EU REACH. North America is seeing major capacity investment from Shintech's USD 3.4 billion Louisiana expansion. Latin America and the Middle East and Africa are growing markets through infrastructure investment and construction activity.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global PVC market is moderately concentrated, with the top five producers controlling approximately 43% of global capacity. Competitive dynamics are shaped by feedstock integration, geographic reach, and the ability to navigate between commodity and specialty grades for construction, electrical, and healthcare applications.

Sustainability is a growing competitive differentiator. Orbia's Vinyl in Motion recycling programme and INEOS's low-VOC upgrades represent positioning strategies separating premium producers from commodity suppliers as sustainability requirements tighten.

Founded in 1926 and headquartered in Tokyo, Japan, Shin-Etsu Chemical is the world's largest PVC producer with total capacity exceeding 4 million tons per year and Shintech as its dominant North American subsidiary. In March 2026, Shintech announced a USD 3.4 billion Louisiana expansion with new ethylene, chlorine, and PVC facilities targeted for completion by 2030.

Founded in 1986 and headquartered in Houston, Texas, Westlake Corporation is an integrated global producer of PVC resin, chlorovinyls, compounds, and downstream pipe products. In January 2026, Westlake acquired ACI for high-voltage wire and cable capabilities, and in late 2025 optimised its North American chlorovinyls footprint by closing non-competitive facilities.

Founded in 1998 and headquartered in Rolle, Switzerland, INEOS is one of the world's largest chemical companies and a major European PVC producer through its Inovyn subsidiary. In July 2025, INEOS upgraded its European plants for high-performance, low-VOC PVC resins for sustainable building materials under tightening EU emissions requirements.

Founded in 1953 and headquartered in Bogota, Colombia, Orbia is a global diversified company and major PVC producer across the Americas and Europe. In May 2025, Orbia launched its Vinyl in Motion PVC recycling initiative to repurpose post-consumer PVC into pipes and building products, positioning itself as a sustainability leader in the market.

Other key players in the market are Formosa Plastics Corp., LG Corp. (LG Chem Ltd.), Occidental Petroleum Corp., Saudi Basic Industries Corporation SJSC, Xinjiang Zhongtai Chemical Co. Ltd., KEM ONE SAS, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Our full report for 2026-2035 delivers the volume data, stabiliser technology analysis, application demand intelligence, and competitive benchmarking to navigate the global PVC market with confidence. Reach out to access the complete report or request a customised version.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market reached nearly 30.17 MMT in 2025.

The market is projected to grow at a CAGR of 4.30% between 2026 and 2035.

The market is assessed to witness healthy growth in the forecast period to reach around 45.96 MMT in 2035.

The different types of products rigid PVC, flexible PVC, low smoke PVC, and chlorinated PVC, among others.

The different applications of PVC include pipes and fittings, film and sheets, wires and cables, bottles, and profiles, hoses, and tubings, among others.

The different regions covered in the market report are North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa.

The key market players are INEOS AG, Westlake Corp., Formosa Plastics Corp., LG Corp. (LG Chem Ltd.), Occidental Petroleum Corp., Saudi Basic Industries Corporation SJSC, Orbia Advance Corporation SAB de CV, Shin-Etsu Chemical Co. Ltd., Xinjiang Zhongtai Chemical Co. Ltd., and KEM ONE SAS, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Stabiliser Type |

|

| Breakup by Application |

|

| Breakup by End Use |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.