Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

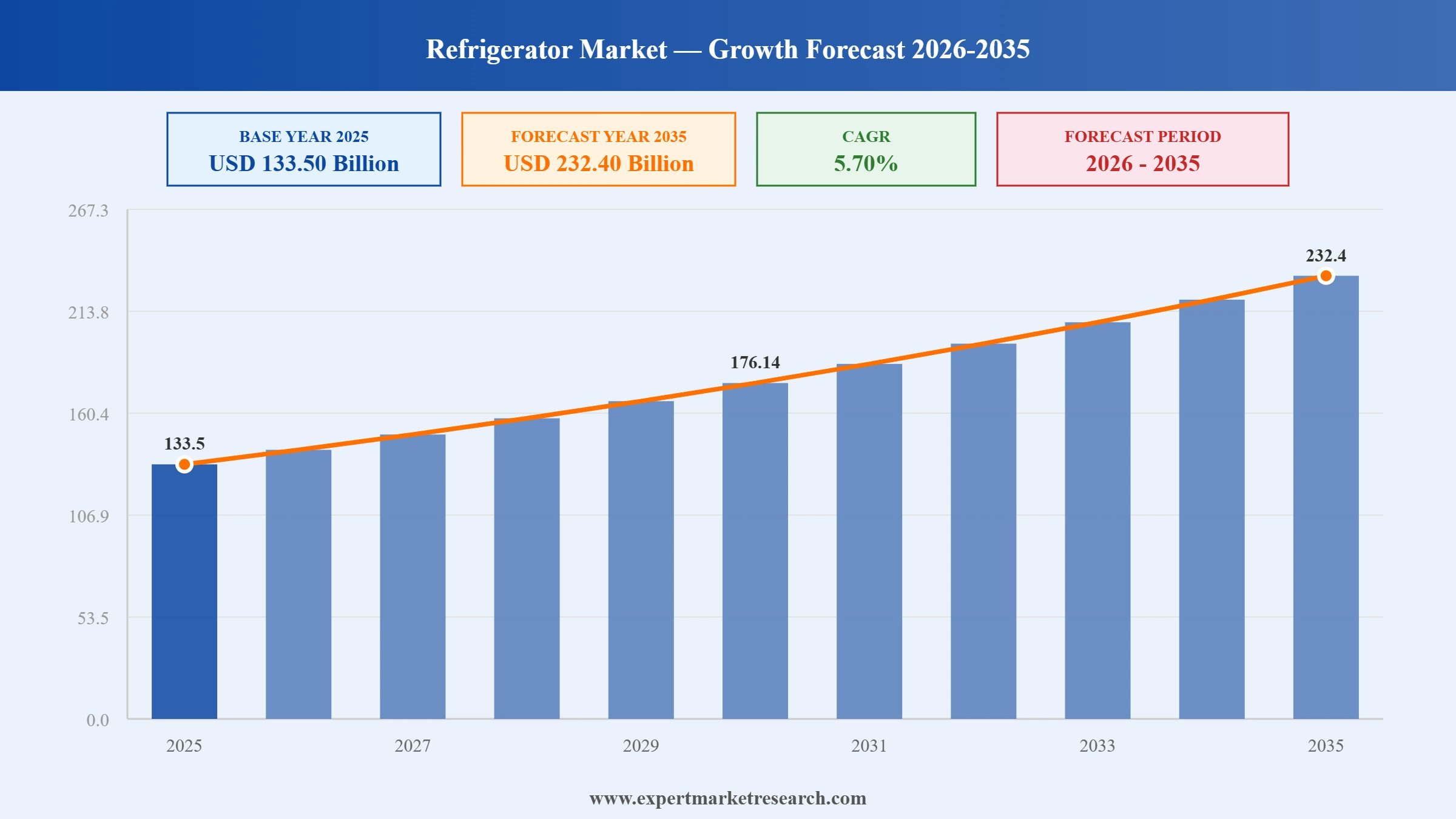

The global refrigerator market attained a value of USD 133.50 Billion in 2025 and is projected to expand at a CAGR of 5.70% through 2035. The market is further expected to achieve USD 232.40 Billion by 2035. Increased popularity of smart kitchens, coupled with more stringent energy efficiency standards and greater emphasis on food preservation technologies, is driving manufacturers to hasten their pace of development of AI-equipped refrigeration products and premium offerings.

The global refrigerator market is experiencing massive growth with leading companies focusing on making smart improvements in cooling, optimizing energy utilization, and developing their appliance ecosystems further. For instance, in April 2026, Samsung Electronics introduced an upgrade to its Bespoke AI refrigerator range by equipping them with on-device artificial intelligence capabilities such as identifying foods, suggesting how to store the foods, and connecting to home automation platforms. Such a move demonstrates a trend among major companies toward software-based products rather than those featuring unique hardware. In addition, Samsung announced that its ecosystem of SmartThings-connected appliances had over 390 million registered users in 2024, thus emphasizing the rising significance of such platforms in the market.

Competitiveness in the global refrigerator market is largely determined by premiumization, sustainability, and innovations in component manufacturing. Companies such as LG Electronics, Haier Smart Home, Whirlpool Corporation, and Panasonic are utilizing more innovative inverter compressors, artificial intelligence for energy management, and natural refrigerants. Furthermore, companies are working to develop modular storage designs and intelligent cooling systems to minimize food waste. For example, in May 2025, Godrej introduced AI-powered Eon Velvet refrigerators featuring intelligent cooling, energy optimization, premium design, and enhanced consumer convenience.

Two key demand triggers are positively impacting the refrigerator market dynamics. The first one relates to higher urbanization and increased disposable incomes driving greater demand for premium multi-door and smart refrigerators that feature connectivity and smart food management solutions. The other demand trigger relates to energy consumption regulation trends, which are pushing consumers to replace their old refrigerators with energy-efficient variants.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Haier launched the Horizon fridge with state-of-the-art freshness preservation, superior looks, and improved storage. Other firms could manufacture fridges with similar features in order to attract urban customers looking for food preservation, leveraging such developments in the refrigerator market.

Haier launched a high-end side-by-side fridge with a BPA-free water dispenser. Other firms can also incorporate such health-centric and high-capacity storage innovations into their refrigerators.

Samsung brought out new single-door refrigerators with energy efficiency technologies, superior cooling capabilities, and enhanced designs. Such advancements encourage other brands to focus on value-sensitive consumers by providing inexpensive and energy-saving refrigerators with excellent cooling capabilities.

Panasonic introduced a new range of Made-in-India refrigerators with bottom freezers, making it easy to access them and making life more convenient for users. Other firms can therefore develop ergonomic refrigerator designs, thereby accelerating the refrigerator market value.

The growing importance of artificial intelligence is creating a competitive advantage for players in the international refrigerator market by helping them extract recurring value from the devices, rather than just selling them. The major companies are equipping premium refrigerators with food recognition and inventory tracking functions, along with the ability to adjust the cooling process according to predicted consumption rates. The latest model line from Samsung, which represents its Bespoke AI series, features the ability to recognize and track various foods inside the device. Refrigerators are presently being marketed as the central units within smart homes owing to Samsung's SmartThings platform. On the other hand, in January 2026, GE Profile launched a smart refrigerator featuring barcode scanning, AI meal planning, inventory tracking, and food waste reduction capabilities.

With energy-efficient rules becoming stricter, refrigerator market players are being driven to adopt more advanced compressor technologies and develop intelligent energy management systems. Companies such as LG Electronics, Whirlpool Corporation, and Panasonic are working towards developing inverter compressors to conserve electricity during operation without affecting its cooling capacity. The United States' Department of Energy maintains certain appliance efficiency standards aimed at encouraging manufacturers to sell appliances with a reduced energy footprint. In Europe, the Ecodesign framework initiative encourages the adoption of energy-saving refrigeration equipment. Aligning with such regulations, September 2025, Liebherr launched new Class A fridge-freezers, delivering lower energy consumption, sustainability benefits, and premium food preservation performance.

Environmental compliance emerges as one of the key growth factors in the refrigerator market due to the shift towards low global warming potential refrigerants. Environmental compliance is gaining importance due to increased use of hydrocarbons like R600a in refrigerants to adhere to global climate change policies. Under the Kigali Amendment to the Montreal Protocol, nations are continuously being motivated to cut down hydrofluorocarbon use, impacting decisions related to refrigerant technology adoption. Companies such as Haier and Panasonic are developing environmental compliance product offerings. Similarly, in February 2026, Enex Technologies highlighted ammonia, CO₂, propane, and water-based refrigeration solutions, advancing sustainable cooling and energy-efficient HVAC innovations.

The trend of premiumization continues to be one of the important refrigerator market trends as manufacturers focus on premium consumers by offering value-added products. Manufacturers are emphasizing customization options, such as flexible storage sections and customizable units. The development of Samsung Bespoke and LG Electronics InstaView line-up of refrigerators reflects the growing interest of companies in offering premium product offerings. This trend is getting stronger owing to the rise in urban disposable income levels. In February 2024, GE Appliances introduced quad-door refrigerators featuring convertible storage, AutoFill pitchers, smart connectivity, and flexible cooling zones.

Leading fridge makers are enhancing their regional manufacturing capabilities to increase supply chain robustness and respond to regional refrigerator market needs. Manufacturers such as Haier, LG Electronics, and Whirlpool Corporation are launching enhanced manufacturing facilities that include features like automation, digitalization, and smart factories. Governments are also providing support for these ventures through various industrial development and domestic manufacturing incentives. In this regard, India’s incentive schemes aimed at electronics and appliance manufacturing are driving regional capacity enhancements among leading global appliance brands. Through these endeavors, manufacturers can cut down on logistical expenses, enhance accessibility, foster innovations, and cater to changing consumer demands in their target regions. For example, in July 2024, Sharp partnered with Elaraby to build a refrigerator plant in Egypt, expanding production capacity and regional exports.

The Expert Market Research's report titled “Global Refrigerator Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

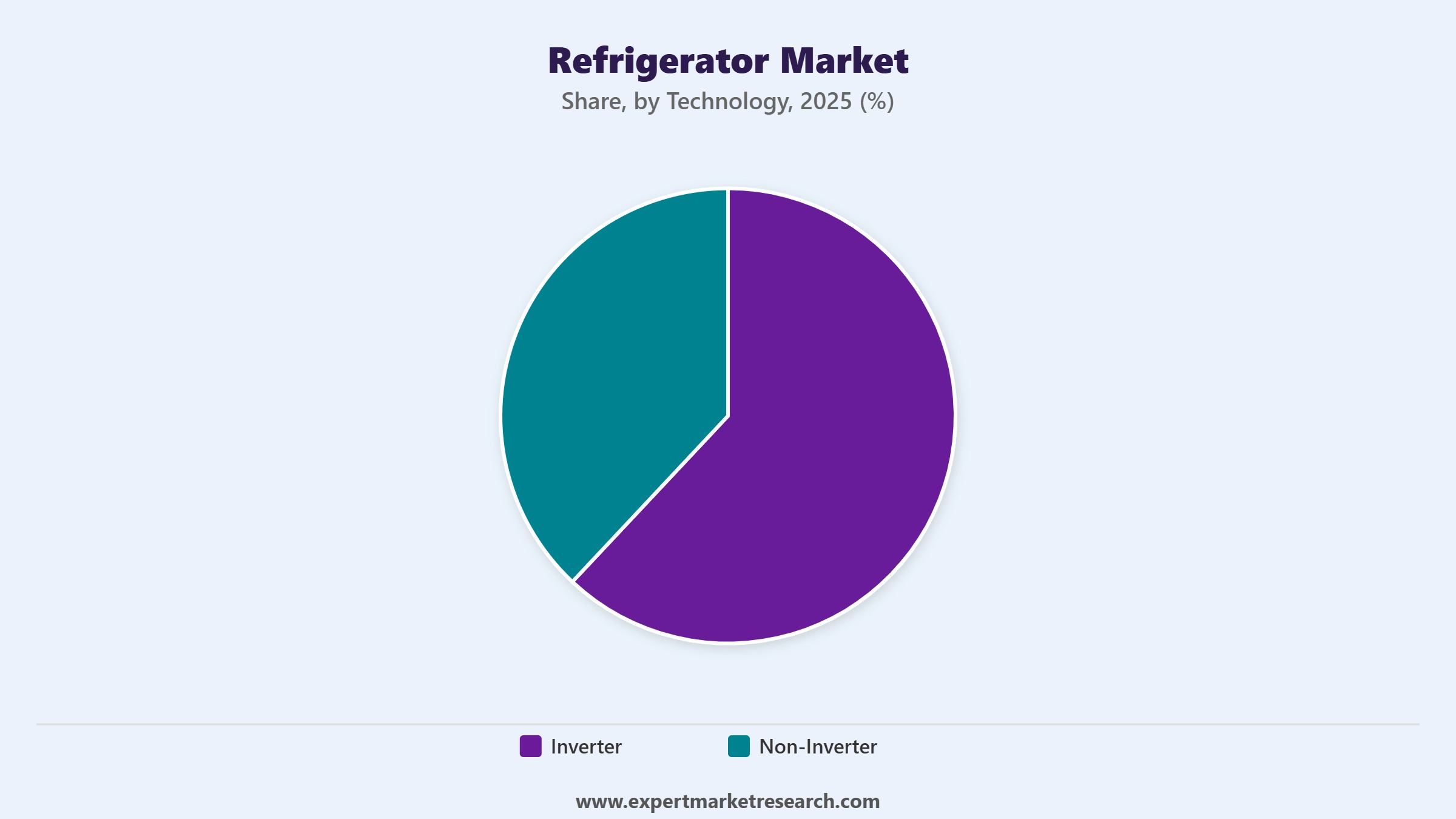

Breakup by Technology

Key Insight: Technology segmentation in the refrigerator market exhibits the harmony between innovations aimed at increasing efficiency and demands based on affordability concerns. The leading trend in the industry is related to the use of inverter technology, as it enables lowering energy expenditure, increasing consistency, and implementing the strategy of positioning premium products. However, non-inverters are also gaining popularity among those who prefer more affordable ways of maintaining the freshness of food items. Companies keep both types of technology within their product portfolios to cater to different purchase preferences in both developed and developing countries.

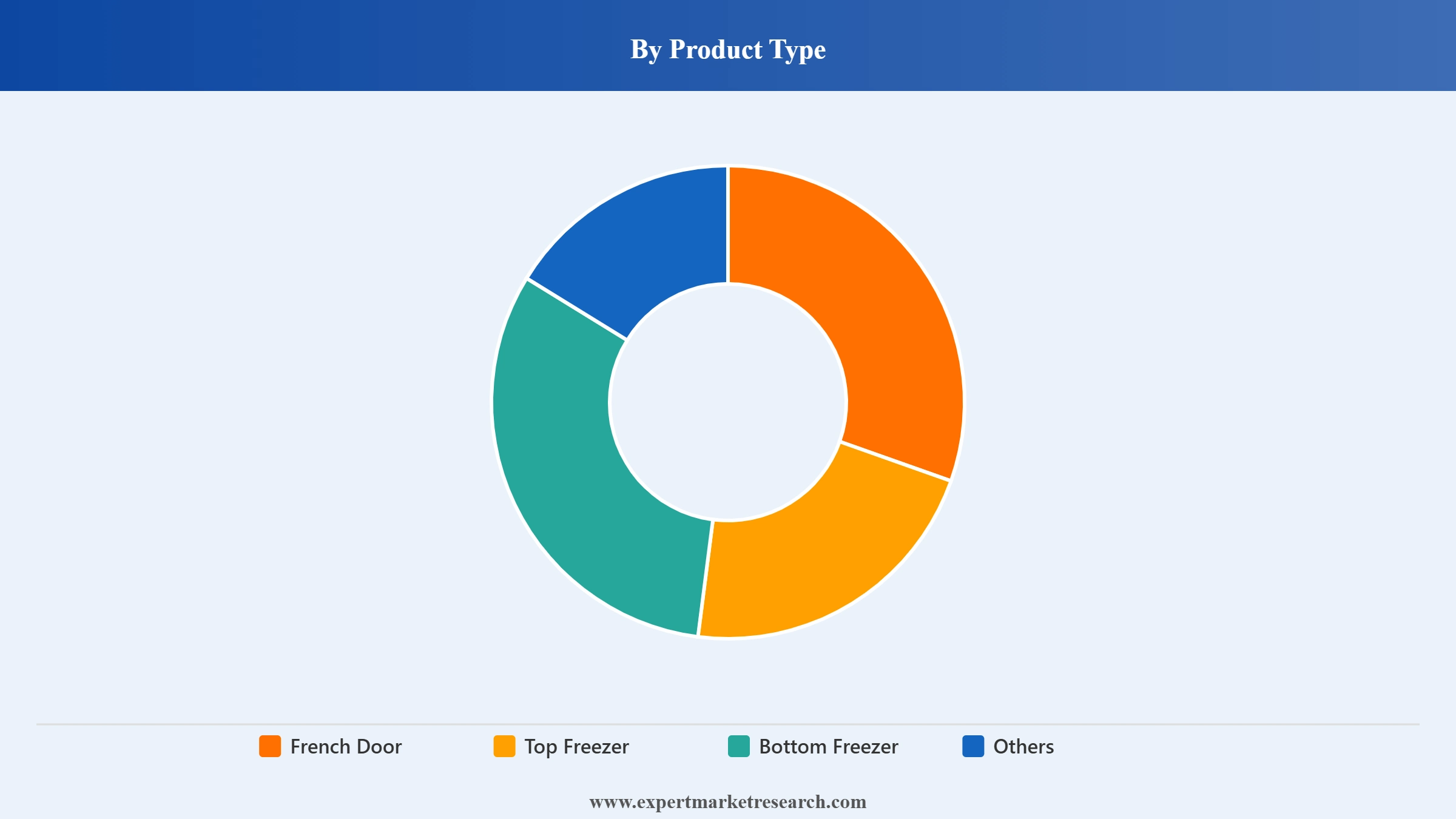

Breakup by Product Type

Key Insight: Product-type segmentation shows how different consumers have different concerns when it comes to refrigerator types. Top-freezer refrigerators are gaining popularity since they offer value for money, dependability, and easy accessibility of products, boosting the refrigerator market value. The popularity of French door refrigerators is on the rise because premium customers appreciate their increased capacities and functionality. Bottom-freezer refrigerators cater to customers looking for ergonomics. There are various refrigerator designs that meet certain requirements of consumers in regard to specific spaces. Manufacturers try to offer more choices in different product segments to satisfy the needs of diverse customers.

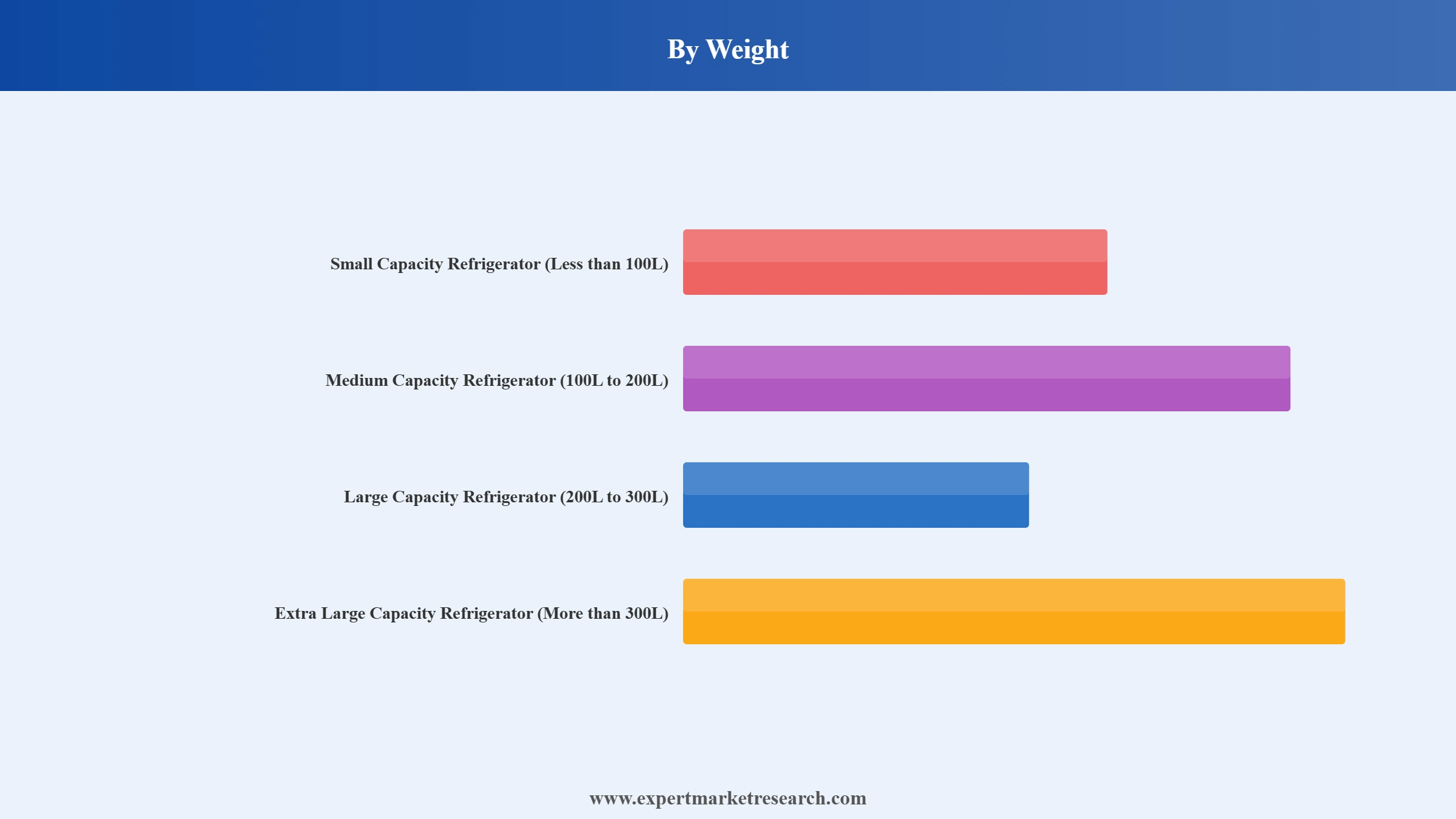

Breakup by Weight

Key Insight: High capacity refrigerators enjoy their position of leadership in the refrigerator market since they represent the best balance among the three aspects including storage space, affordability, and utility in domestic settings. The segment of extra large capacity refrigerators is experiencing fast growth due to the increasing demand for convenient features, versatility, and technological advancement from premium customers. The medium segment of capacity provides the solution to smaller family units and apartment dwellers, while small-capacity refrigerators are designed to suit individuals and second refrigerators in homes.

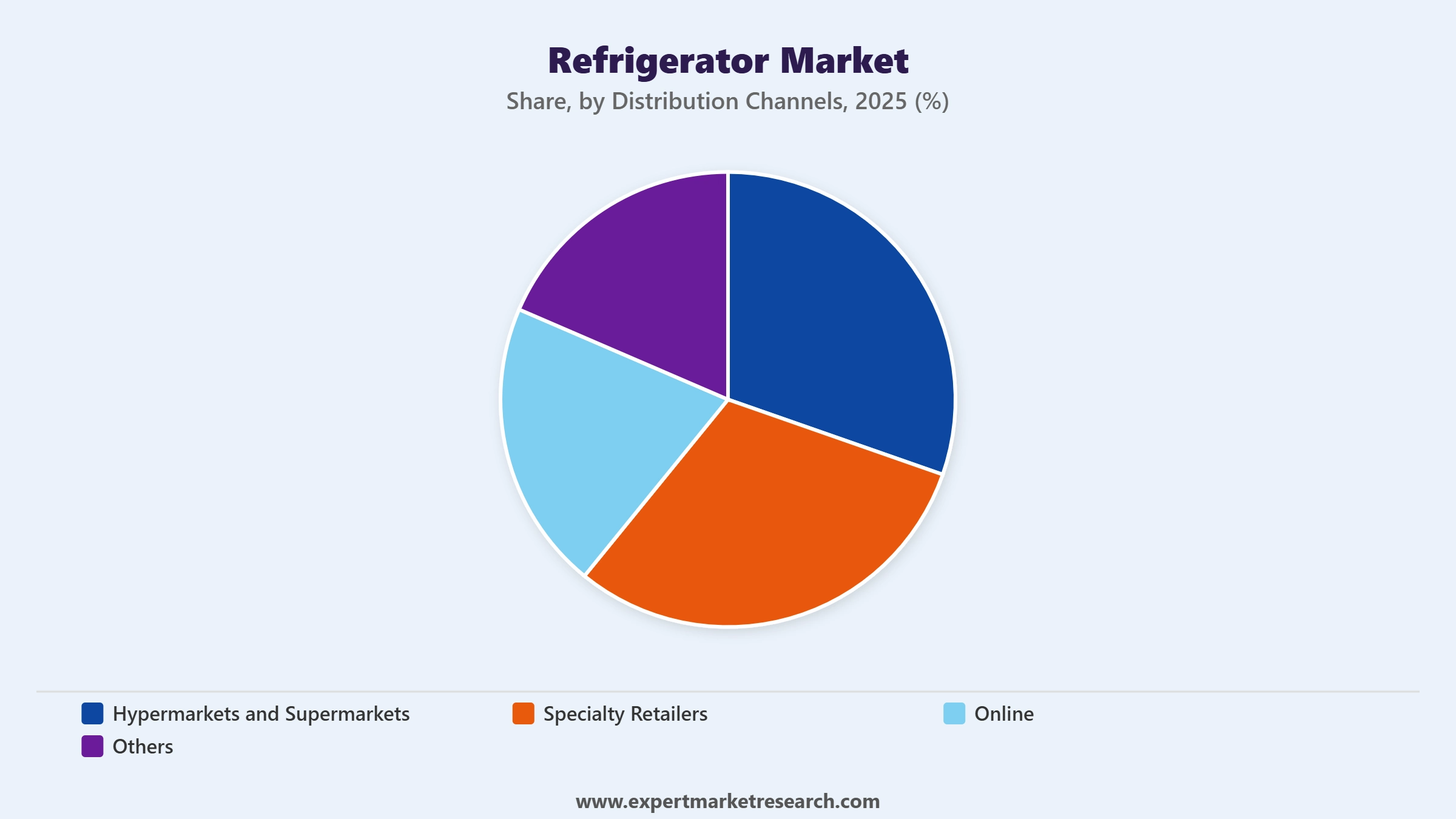

Breakup by Distribution Channels

Key Insight: The refrigerator market observes changes in the dynamics of distribution channels considering the efforts being made by manufacturers for omnichannel expansion. The lead is held by specialty stores because of their personalization in dealing with customers, expertise in selling products, and ability to sell appliances at a high level of quality. There is fast growth in online channels on account of the convenience that comes from purchasing products online and greater product availability. Hypermarkets and supermarkets are important channels of distributing entry level and mid-range refrigerators since they offer product availability and competitive prices.

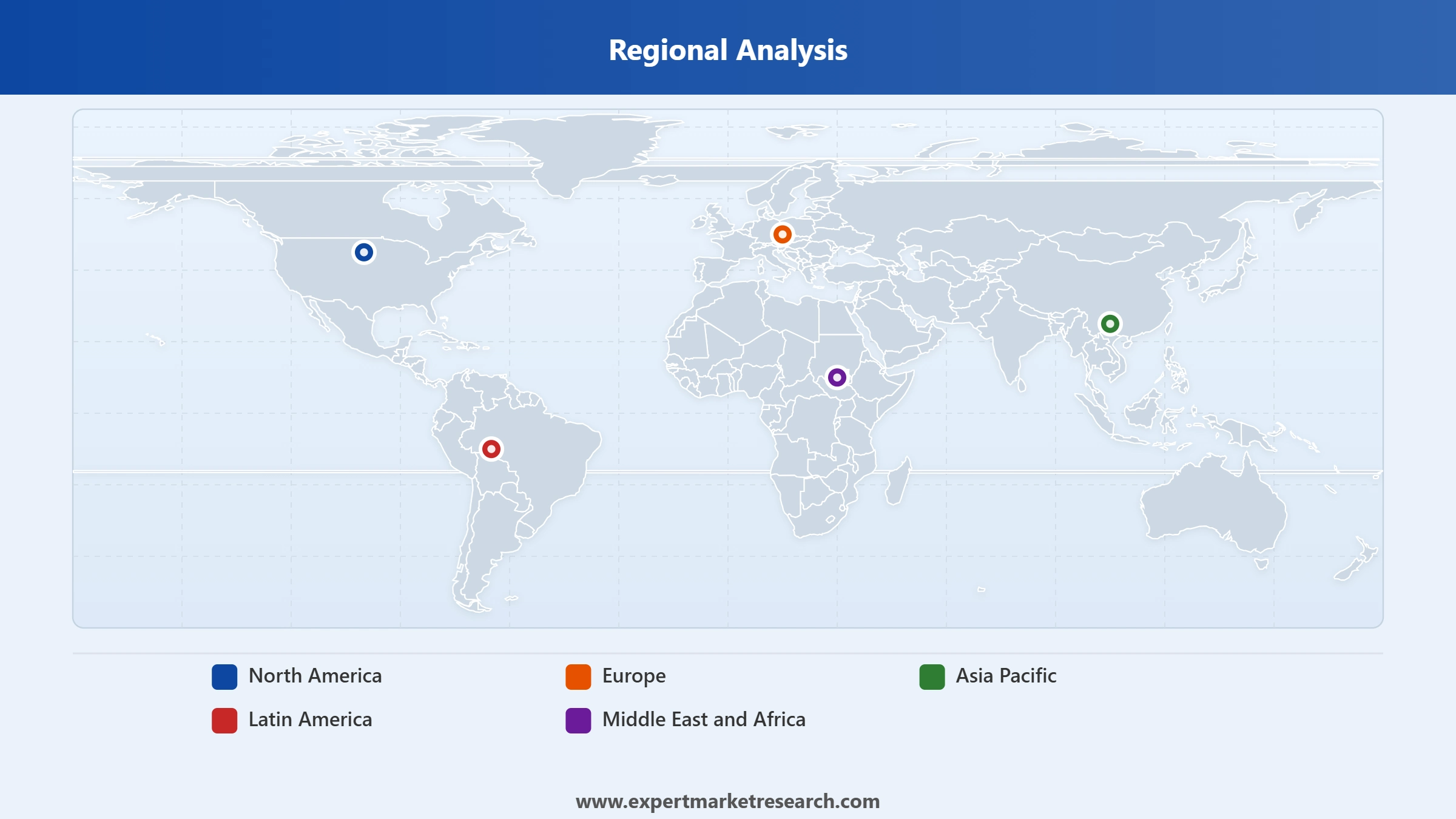

Breakup by Region

Key Insight: Performance in different regions depends on the strength of manufacturing, consumer buying behavior, and infrastructure. In terms of performance, the Asia Pacific region dominates the refrigerator market owing to its capacity for large-scale manufacturing operations, increased urban population, and the prevalence of appliance purchase. The market further observes a remarkable growth in the performance of the Middle East and Africa owing to improved standards of living and increased use of household appliances. North America benefits from high-end appliances and smart homes, while Europe prioritizes energy-efficient appliances. Latin America keeps creating opportunities by virtue of urbanization and increased appliance usage.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Inverter refrigerators account for the largest share of the market due to superior energy optimization

The inverter refrigerator market comprises the largest share of the global refrigerator market owing to the adoption of energy-efficient cooling solutions among other factors. Such cooling solutions control compressor speeds depending on cooling needs. This technology is more efficient and ensures temperature stability within the refrigerator. Key firms involved include LG Electronics, Samsung Electronics, Haier, and Panasonic which produce a wide range of their products with inverter cooling technology. There is increasing consumer interest in appliances that can minimize energy costs as well as ensure quiet operation and durability. In December 2024, Samsung introduced AI Hybrid Cooling refrigerators, combining AI algorithms and hybrid cooling for energy efficiency, freshness, and storage.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The segment for non-inverter variants is also gaining momentum in the refrigerator market especially in cost-conscious markets where energy savings are not a major consideration. Non-inverter refrigerators are characterized by smaller size and lower prices making them ideal for first-time users. Other advantages associated with these refrigerators include reduced maintenance expenses and initial investment costs relative to sophisticated inverter models. Some of the emerging regional players are expanding distribution and manufacturing capacity within these areas. Electrification of households as well as rising numbers of middle-class individuals are expected to stabilize demand in this segment over the long term.

Top freezer refrigerators lead demand growth through affordability and practicality

Top freezer refrigerators continue to sustain its dominance in the refrigerator market because of wide consumer acceptability, effective space usage, and favorable pricing. Top freezer models continue evolving through improvements in space management, energy efficiency, and modern interior designs. In addition, top freezers gain more popularity among mid-level income earners who desire affordable quality refrigeration units. Appliance firms keep expanding their top freezer refrigerators portfolio because this model provides cost-effective production while meeting the needs of consumers. In June 2025, Equator introduced the RF 142 S refrigerator featuring energy-efficient operation, flexible shelving, modern compressor technology, and enhanced food preservation performance.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The French door refrigerator is becoming increasingly popular in the market. This product category enjoys increased popularity because of premiumization trends as well as increased development of appliances ecosystems. Consumers find this refrigerator attractive because of its large storage capacity, flexible compartment configurations, and connectivity options. Companies like Samsung, LG Electronics, and Whirlpool Corporation are offering advanced French door refrigerators with features such as artificial intelligence and advanced food preservation technologies. The rising demand for high-end kitchen appliances contributes to this trend in the refrigerator market. In May 2026, LG launched French Door refrigerators and AI-powered appliances, enhancing premium smart-home convenience.

Large capacity refrigerators secure the largest share of the market demand through family-oriented storage requirements

Large capacity refrigerators with capacity between 200L and 300L continue to dominate the refrigerator market as these models cater to storage demands of medium sized households. These are gaining massive traction among manufacturing companies as they are affordable and serve the functional purpose well. Large capacity refrigerators offer flexibility in terms of design and configuration. These refrigerators can be found with inverter technology, adaptability in terms of cooling technology and flexible shelves. Increased urbanization and changing demands for food storage are expected to continue to drive demand in this segment.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The extra large capacity segment is witnessing growth in the refrigerator market driven by increased need for storage space among premium consumers along with smart features and improved cooling technology. Extra large refrigerators are being designed to include AI control, conversion capabilities and improved preservation technology. Changing lifestyle preferences such as large kitchens and preference for buying in bulk volumes are adding further impetus to growth in this segment. Innovative multi door configuration and customizable designs would help companies gain an edge in differentiation. For example, in May 2025, Bosch introduced high-capacity top freezer refrigerators featuring advanced freshness technologies, flexible storage, and energy-efficient performance.

By distribution channel, specialty retailers capture a substantial share of the market through product expertise and services

Specialty retailers play a crucial role in accelerating the refrigerator market penetration because they can offer demo services, technical support, and installation assistance. Such outlets are usually preferred by customers in the case of purchasing high-value goods that need proper assessment before buying. It is easier for the manufacturers to create an attractive showroom that would demonstrate all the best features, connectivity options, and customization of the appliances. Good after-sales services further solidify the position of specialty retailers. In the case of premium refrigerators, consumers usually appreciate consultations with experts and engaging services offered by such retailers. In March 2026, Thomson launched its refrigerator range in India, targeting category expansion through affordable, feature-rich cooling solutions and broader consumer appliance offerings.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Online sales are growing at the fastest rate because digital marketing and commerce make the purchase experience for consumers easier, allowing comparisons of products, flexible payment schemes, and easy home deliveries. Appliance makers are more interested in cooperation with digital providers and in creating new models of direct consumer sales, boosting the refrigerator market expansion. Consumers have access to more products available in one place, get clear information on pricing policies, and enjoy the process of purchasing. The development of advanced visualization technology and virtual tours helps to gain consumer confidence in online appliance purchases.

Asia Pacific leads market expansion through manufacturing capabilities and consistent demand

Asia Pacific leads the global refrigerator industry growth owing to its strong manufacturing environment, rising urban population, and increased usage of home appliances. This region houses major players such as Haier, LG Electronics, Samsung Electronics, Panasonic, and other large-scale manufacturers. Increasing population of middle class families, high rate of housing activities, and rising need for replacement contribute to the expansion of the market. Corporations are establishing local manufacturing facilities and R&D centers in this region. Together, all these features reinforce the presence of Asia Pacific as the leading producer and consumer market for refrigerators.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Middle East and Africa region emerges as the fastest growing market for refrigerators owing to increased urbanization and electrification levels, along with investment in infrastructure. There is an increase in the demand for household appliances in this market which encourages manufacturers to expand their presence and make more products available. Increased network of retail outlets and consumers' higher purchasing ability are some of the other driving factors of this regional refrigerator market. Corporations are launching efficient and locally suited models of refrigerators in order to cater to the regional demand. For example, in May 2025, LG introduced the MoodUP refrigerator featuring customizable LED panels, smart connectivity, and personalized kitchen aesthetics for UAE consumers.

Increasing competition is becoming more evident as the industry moves past standard cooling capacities towards advanced and sustainable appliance ecosystem developments. Leading refrigerator market players are increasingly investing in artificial intelligence-based food detection, smart cooling systems, home networking, as well as use of eco-friendly refrigerants. The industry also witnesses growth in regional manufacturing plants and digitized factories aimed at improving product launch speed and resilience in the supply chain.

Some of the refrigerator companies are also finding new opportunities in the rise of smart kitchens, increased premium refrigerators sales, energy-efficient regulations, and higher replacement rates. Furthermore, software platforms for predictive maintenance and customized storage are being used to build customer engagement. The collaboration between companies and technology vendors to improve refrigerator offerings is also gaining prominence.

LG Electronics is an international electronics company founded in 1958 and operating from the headquarters in Seoul, South Korea. It provides services in the refrigerator market by using efficient inverter compressor technology, artificial intelligence cooling technology, and high-end InstaView products. Currently, LG is working on developing connected appliance ecosystems utilizing ThinQ technology along with food preservation, energy efficiency, and smart diagnostics. The company keeps introducing new premium refrigerators suitable for smart kitchen environments.

Haier Group was founded in 1980 and operates from the headquarters in Qingdao, China. It caters to the refrigerator industry with a wide range of products from affordable to premium segments. The company focuses on innovation driven by customer demands, modular refrigeration, and energy-efficient cooling technology. With its global brands of household appliances, Haier fulfills diverse demands of consumers in both developed and emerging markets..

Founded in the year 1911, headquartered in Michigan, United States, Whirlpool Corporation prioritizes innovation, adaptable storage solutions, and energy efficient cooling technologies. The organization produces refrigerators with adaptive compartment design, sophisticated fresh technology, and easy-to-use interface. Whirlpool Corporation keeps improving its product differentiation through user-centric innovations as well as adding premium appliances to satisfy the growing needs of households in food storage and convenience.

Founded in 1969, headquarters in Suwon, South Korea, Samsung Electronics is involved in refrigerator business through Bespoke AI refrigerators, SmartThings platform, and innovative food management systems. The company is working on AI Vision Inside technology that will be able to recognize the type of food in the fridge and manage the inventory more efficiently.

Other key players in the market include Hitachi Ltd., Electrolux AB, Panasonic Corporation, BSH Home Appliances Corporation, Miele & Cie. KG, Arçelik A.Ş, Toshiba Corporation, Midea Group, Honeywell International Inc., Godrej & Boyce Manufacturing Company Limited, and Sharp Electronics Corporation, among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock the latest insights with our refrigerator market trends 2026 report. Discover regional growth patterns, consumer preferences, and key industry players. Stay ahead of competition with trusted data and expert analysis. Download your free sample report today and drive informed decisions in the market.

United States Refrigerator Market

North America Refrigerator Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The global market size for refrigerators reached a value of more than USD 133.50 Billion in 2025.

The market is expected to reach a value of USD 232.40 Billion by 2035.

The market is expected to grow at a CAGR of 5.70% between 2026 and 2035.

The major market drivers are longer durations between grocery shopping trips, smarter features, and versatile storage options.

Major trends of the market include technological advancements, and glass doors.

The major regional markets are North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa.

Key players for the global refrigerator market are LG Electronics Inc., Haier Group, Whirlpool Corporation, Samsung Electronics Co., Ltd., Hitachi Ltd., Electrolux AB, Panasonic Corporation, BSH Home Appliances Corporation, Miele & Cie. KG, Arçelik A.S, Toshiba Corporation, Midea Group, Honeywell International Inc, Godrej & Boyce Manufacturing Company Limited, and Sharp Electronics Corporation, among others.

A refrigerator, commonly known as a fridge, is an common home appliance used to store and preserve food items that are perishable.

The market is segmented based on product type, technology, weight, distribution channel and region.

Tetrafluoroethane gas is commonly used in refrigerators.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Technology |

|

| Breakup by Product Type |

|

| Breakup by Weight |

|

| Breakup by Distribution Channels |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Trade Data Analysis |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.