Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The global rigid plastic packaging market was valued at USD 221.07 Billion in 2025. The industry is expected to grow at a CAGR of 4.10% during the forecast period of 2026-2035, the market attaining a valuation of USD 330.40 Billion by 2035.

Compound Annual Growth Rate

4.1%

Value in USD Billion

2026-2035

| Global Rigid Plastic Packaging Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 221.07 |

| Market Size 2035 | USD Billion | 330.40 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 4.10% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 4.8% |

| CAGR 2026-2035 - Market by Country | India | 5.4% |

| CAGR 2026-2035 - Market by Country | China | 4.5% |

| CAGR 2026-2035 - Market by Material | Polyethylene Terephthalate (PET) | 4.7% |

| CAGR 2026-2035 - Market by End-User Industry | Food & Beverage | 4.6% |

| Market Share by Country 2025 | Japan | 4.2% |

Rigid plastic packaging refers to packaging that is typically made from plastic and is designed to be rigid so as to better protect items contained within the packaging. It utilises materials including polyethylene terephthalate, polypropylene, and high density polyethylene for packaging of containers and bottles, among others. Rigid plastic packaging is stronger, sturdier, and heavier than its counterparts and is often used for wrapping delicate products requiring enhanced protection. The significant benefits of this packaging include cost efficiency and longevity.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The EMR’s report titled “Rigid Plastic Packaging Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

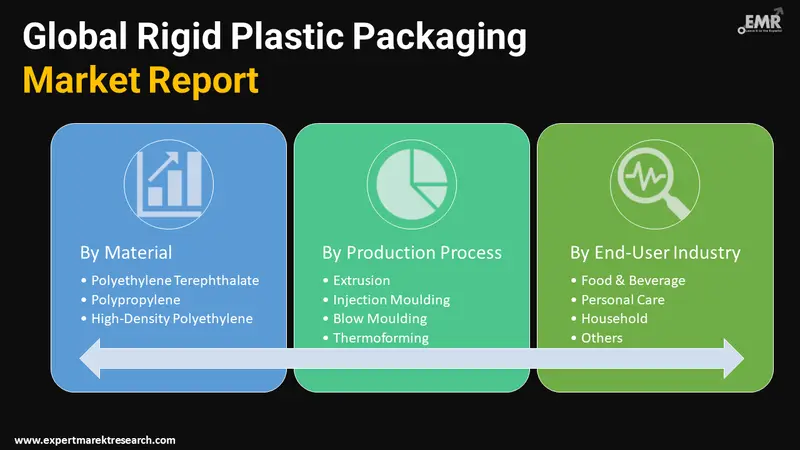

Breakup by Material

Breakup by Production Process

Breakup by End-User Industry

Breakup by Region

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The food and beverage end-user industry is anticipated to witness significant growth in the rigid plastic packaging market over the forecast period owing to increasing demand for containers, jars, and bottles by the food and beverage industry. Growing population levels, rising urbanisation, and increasing demands for packaged food and beverages is propelling the growth of the market for rigid plastic packaging. Moreover, busy work schedules and hectic lifestyles are increasing the utilisation of plastic containers for storing food and beverages. Rising environmental concerns are increasing the demands for long lasting packaging solutions further aiding the growth of the market for rigid packaging solutions as they are sturdy and last for longer durations of time.

| CAGR 2026-2035 - Market by | Country |

| India | 5.4% |

| China | 4.5% |

| USA | 3.7% |

| Germany | 3.4% |

| Australia | 3.2% |

| Canada | XX% |

| UK | XX% |

| France | XX% |

| Italy | 2.9% |

| Japan | XX% |

| Saudi Arabia | XX% |

| Brazil | XX% |

| Mexico | XX% |

The Asia Pacific region is expected to account for a significant portion of the market share for rigid plastic packaging by region over the forecast period owing to rapid urbanisation and industrialisation. The expansion of economic activities and economies in the region is expected to boost the growth of the rigid packaging market in countries such as India and China. Other factors propelling the growth of the market in the Asia Pacific include rising disposable incomes, growing manufacturing activities, and increasing levels of consumption. Meanwhile, in the Middle East and Africa, the Saudi Arabia rigid plastic packaging market is anticipated to witness growth over the forecast period due to growing personal care and food industries in the country.

ALPLA is a packaging and container manufacturing company that was established in 1955 and is based in Vorarlberg, Austria. Their specialities include injection moulding, bottles, injection blow moulding, closures, and caps. ALPLA is one of the leading companies in the packaging solutions sector and are renowned for producing high quality plastic packaging.

Amcor plc is a packaging and container manufacturing company that was founded in 1864 and is headquartered in Zurich, Switzerland. They produce rigid containers, flexible packaging, and speciality cartons for pharmaceuticals, home and personal care, and food and beverages, among others. Amcor is focused on making packaging that is lightweight, reusable, and recyclable and made from large amounts of recycled content.

Amcor plc is a packaging and container manufacturing company that was founded in 1864 and is headquartered in Zurich, Switzerland. They produce rigid containers, flexible packaging, and speciality cartons for pharmaceuticals, home and personal care, and food and beverages, among others. Amcor is focused on making packaging that is lightweight, reusable, and recyclable and made from large amounts of recycled content.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other market players include DS Smith plc, Klöckner Pentaplast, Plastipak Holdings, INC., Pactiv Evergreen Inc., Sealed Air, Silgan Holdings Inc., Sonoco Products Company, Graham Packaging Company, Consolidated Container Company, and Reynolds Group Ltd., among others.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market attained a value of nearly USD 221.07 Billion.

The market is assessed to grow at a CAGR of 4.10% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach about USD 330.40 Billion by 2035.

The major market drivers include rising demand from the food and beverage industry, growth of food chains, and increasing demand for environment friendly packaging solutions.

The key trends fuelling the growth of the market include increasing utilisation by the healthcare industry, growing popularity of e-commerce, and rising consumption of consumer goods.

Rigid plastic is derived from thicker and denser materials and provides increased protection against heat and other environmental and non-environmental factors.

The major regions in the market are North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa.

The various end-user industries for rigid plastic packaging include food and beverage, personal care, household, and healthcare, among others.

The significant production processes for rigid plastic packaging in the market include extrusion, injection moulding, blow moulding, and thermoforming.

The key players in the global rigid plastic packaging market are ALPLA, Amcor plc, Berry Global, Inc, DS Smith plc, Klöckner Pentaplast, Plastipak Holdings, INC., Pactiv Evergreen Inc., Sealed Air, Silgan Holdings Inc., Sonoco Products Company, Graham Packaging Company, Consolidated Container Company, and Reynolds Group Ltd., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Material |

|

| Breakup by Production Process |

|

| Breakup by End-User Industry |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.