Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

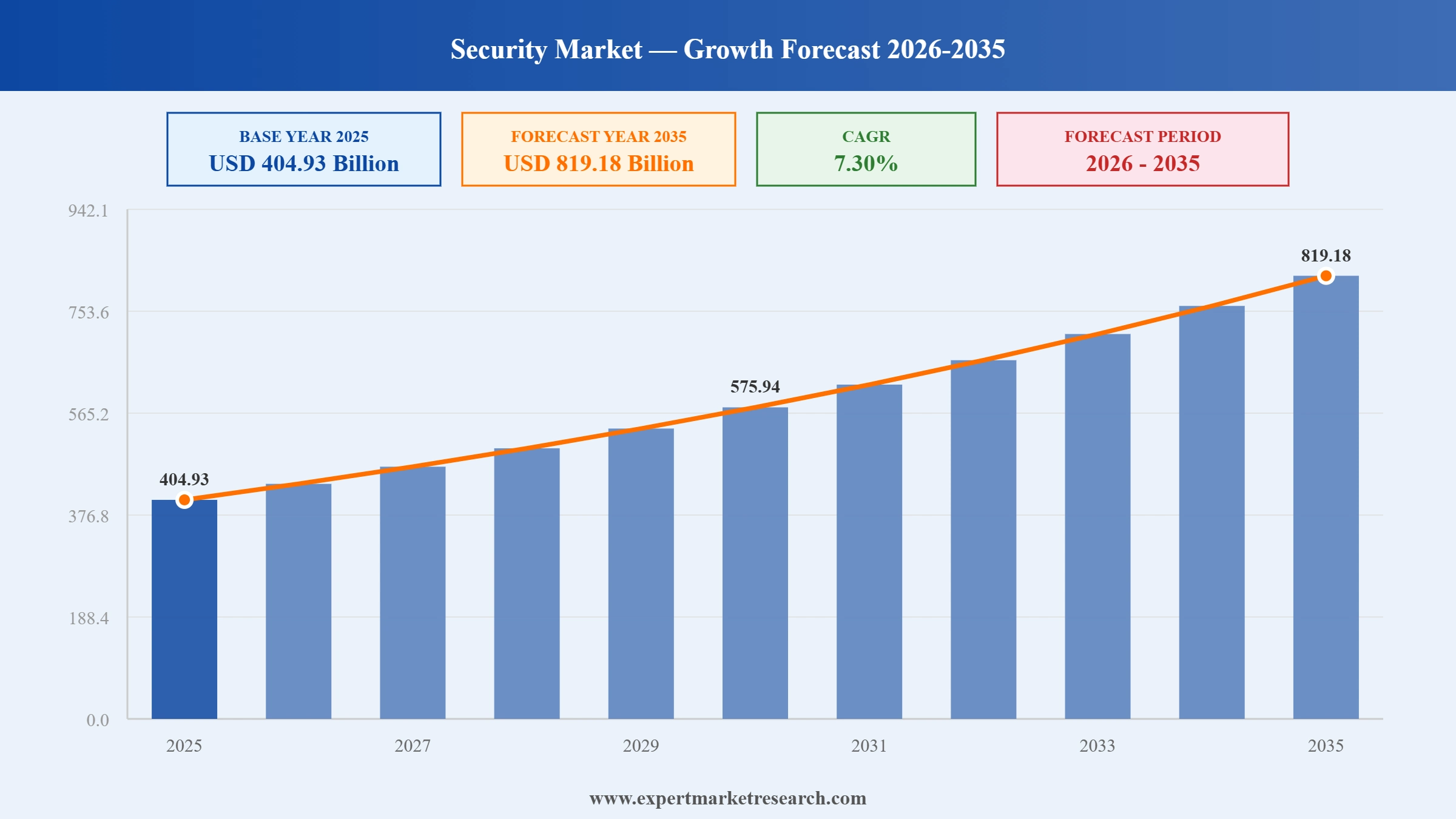

The global security market attained a value of USD 404.93 Billion in 2025 and is projected to expand at a CAGR of 7.30% through 2035. The market is further expected to achieve USD 819.18 Billion by 2035. With an increase in ransomware complexity and digitalization of critical infrastructure, there is an increase in enterprises investing in artificial intelligence-based security platforms, identity protection, and unified threat management systems around the world.

Two potent catalysts are driving the overall security market growth. The first is the increasing number of regulations being put in place by governments on cybersecurity for essential industries, and enterprises are upgrading their security infrastructure to comply with these regulations and ensure continuous monitoring. Secondly, enterprises are increasingly using artificial intelligence-based security operations centers to detect and prioritize threats and minimize the workload of analysts through orchestration. This is spurring security technology providers to offer subscription-based security services and acquisitions.

Artificial Intelligence-based threat intelligence, autonomy in surveillance systems, and cloud security systems are redefining the global security market due to evolving threats of cyber and physical nature. For example, in March 2026, Google finalized its acquisition of Wiz in order to strengthen its portfolio of cloud security solutions with multi-cloud security and advanced threat and risk detection capabilities based on AI technology. This move highlights the shift of priority among hyperscale technology providers from individual security products to integrated security ecosystems.

The growth of the security market is further fueled by investments in digital transformation projects, regulatory compliance, and infrastructure protection. Security providers are increasingly offering integrated solutions combining cybersecurity and physical security technologies along with identity verification and predictive analysis. Key players are building partnerships with cloud providers, semiconductor producers, and industrial automation companies to develop scalable architectures of security systems for manufacturing, healthcare, financial, transport, and governmental sectors. In June 2026, Canada and Germany strengthened semiconductor partnership, enhancing resilient supply chains, innovation, research collaboration, and AI-driven industrial competitiveness.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Global Security Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 404.93 |

| Market Size 2035 | USD Billion | 819.18 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 7.30% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 8.4% |

| CAGR 2026-2035 - Market by Country | India | 9.7% |

| CAGR 2026-2035 - Market by Country | China | 8.1% |

| CAGR 2026-2035 - Market by Service | Managed Security Services | 8.0% |

| CAGR 2026-2035 - Market by Application | Government | 8.3% |

| Market Share by Country 2025 | India | 3.8% |

AI Security Platform from F5 was introduced, offering AI application security, governance, runtime security, and visibility within hybrid environments. Therefore, market players can create AI governance, runtime security, and shadow AI detection tools, as enterprises are rapidly increasing the use of generative AI.

SGS unveiled Compass, a data-driven platform for assessing risks of suppliers, compliance management, traceability, and sustainability of global supply chains. Other companies in the security market can also implement AI-based compliance analytics, supplier cybersecurity, and global supply chain risk management platforms.

Keenfinity released Radionix, their specific line of intrusion systems, providing smarter perimeter security and intrusion detection systems for industrial and commercial security purposes. Organizations can upgrade their smart intrusion detection system, integrated access control, and AI-powered perimeter monitoring range for critical infrastructure projects, accelerating demand in the security market.

Made-in-India 50 Series CCTV cameras with intelligent video analytics, enterprise-level cybersecurity, and integration were launched by Honeywell. Organizations can purchase locally manufactured smart surveillance systems with enhanced cybersecurity functionalities for smart cities and critical infrastructure projects.

The market is undergoing an evolution in the face of artificial intelligence (AI) as organizations are able to quickly identify, investigate, and neutralize threats faster using new security technologies. Generative AI technology is being deployed by security vendors to help SOCs prioritize alerts, analyze malware, and respond to incidents, accelerating the security market value. In October 2025, Microsoft rolled out an AI-powered security platform, unifying threat detection, automated response, and enterprise-wide cyber resilience against evolving attacks. At the same time, CISA continues advocating its Secure by Design approach, urging software developers to build greater security controls at the development phase.

Perimeter-based security architectures are being replaced with Zero Trust frameworks that constantly authenticate every user, device, and application. An increasing number of remote workers and hybrid cloud environments are fueling demand for identity-based security architectures, widening the security market scope. In April 2024, Cisco launched HyperShield, AI-native, distributed security architecture that secures apps, networks, and workloads on hybrid infrastructures. The Zero Trust Strategy of the United States federal government keeps pushing agencies towards modernization and adoption of such security architectures.

Security market players are focusing on innovations through acquisitions, which help to enhance cloud-native security features. Google's acquisition of Wiz marked a significant industry milestone, enabling the company to strengthen its multi-cloud security portfolio by integrating advanced vulnerability management and risk visibility capabilities. With businesses moving into the clouds of AWS, Microsoft Azure, and Google Cloud, there is a growing need for cloud security platforms. Aligning with such a trend, in June 2026, Endava partnered with Wiz to deliver integrated cloud security, strengthening secure enterprise AI adoption across complex multi-cloud environments.

The security market observes a rise in investments in critical infrastructure protection from governments to defend against cybersecurity threats. Several companies are offering integrated platforms, which include video surveillance systems, AI analytics, access control, and cybersecurity monitoring for critical infrastructures. Industrial cybersecurity providers are creating dedicated solutions for OT environments for monitoring industrial control systems. For example, in June 2026, Honeywell expanded its OT cybersecurity suite with AI-powered threat detection, strengthening critical infrastructure resilience, and industrial cyber defense.

Intelligent physical security can be realized using biometrics, face recognition technology, AI-enabled video analytics, and unified access control systems, reshaping the security market trends and dynamics. The use of physical and cyber security operations in organizations is being adopted in order to achieve better visibility and reduce the risks associated with unauthorized access. In August 2025, HID Global rolled out additional biometric and mobile credential capabilities to support digital identity management within the enterprises. Governments are also advocating digital identity initiatives and authentication standards for public services and critical infrastructures.

“Global Security Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

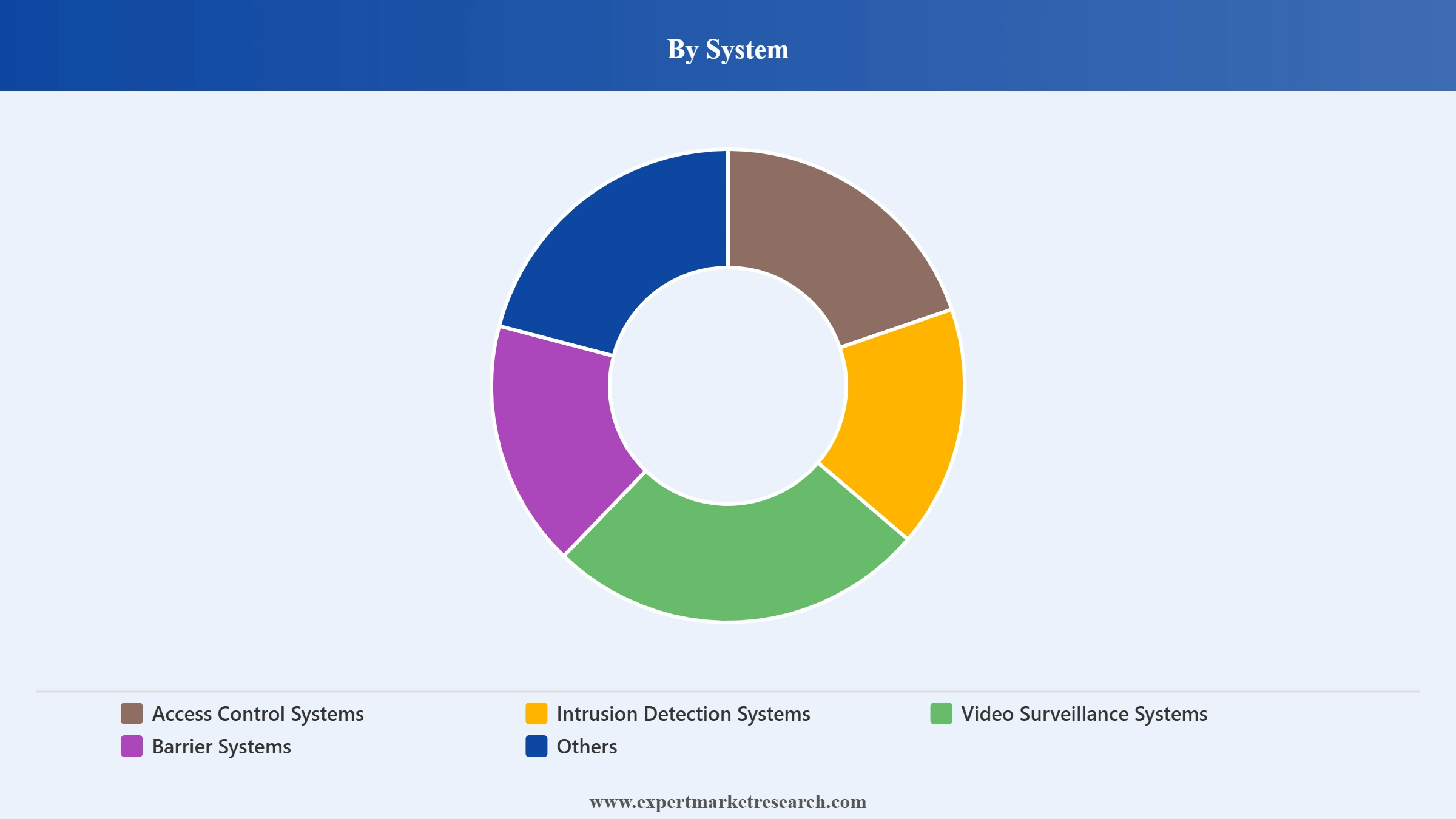

Market Breakup by System

Key Insight: Video surveillance systems dominate the security market due to their ability to offer constant surveillance, intelligence, and artificial intelligence-powered threat detection in complex environments. Access control systems are expanding their market share due to the rising trend of identity-based security becoming an integral part of enterprise risk management practices. The intrusion detection systems are becoming important for identifying threats in critical infrastructures, while the barrier systems continue being used to provide perimeter protection in transportation, utilities, and industrial facilities. Other security systems cater to specific needs.

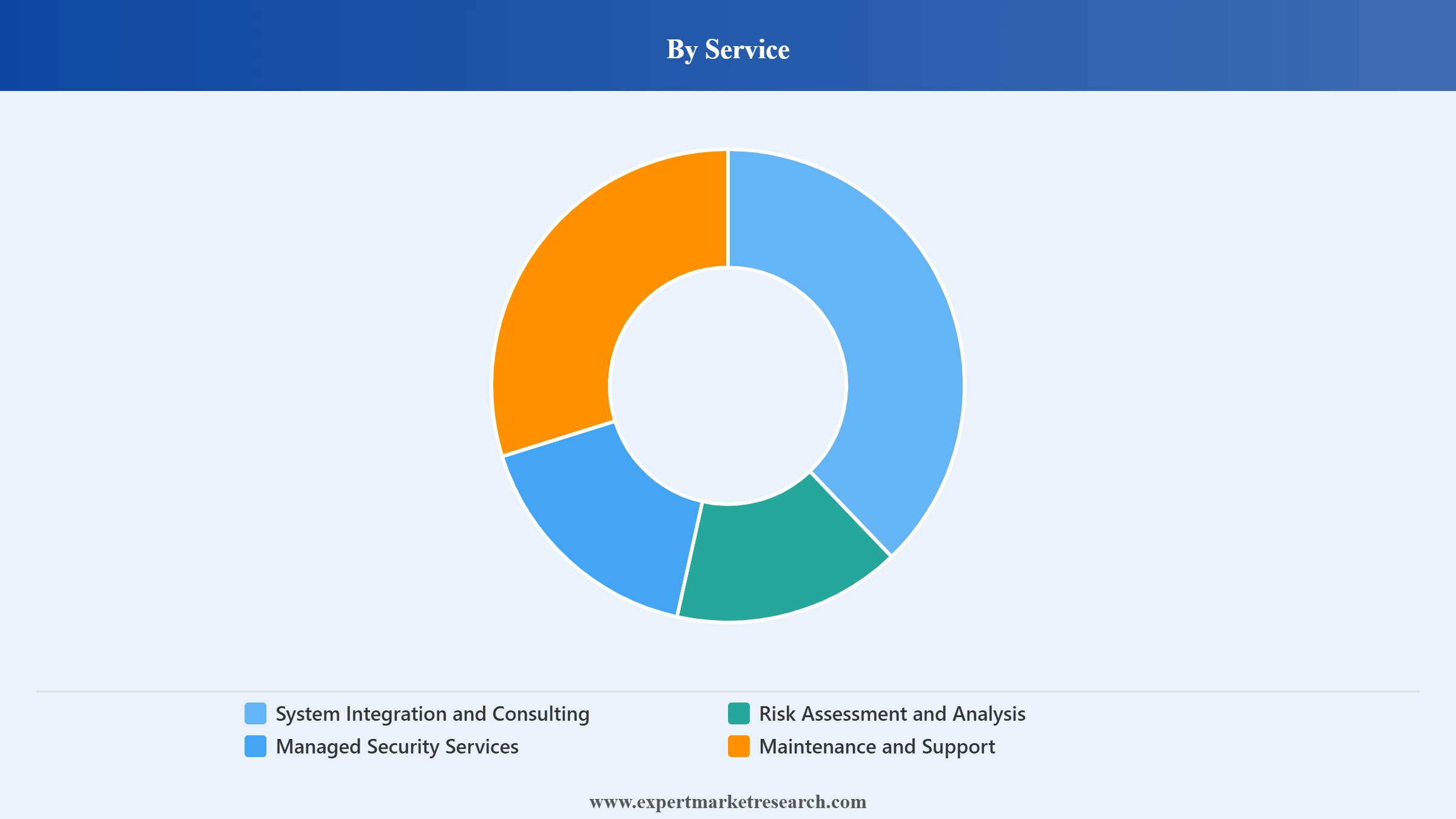

Market Breakup by Service

Key Insight: The current demand for security services is moving towards the concept of security management through the lifecycle. This security market trend is led by managed security services, which provides consistent security solutions, operational skills, and scalable security operations. Risk assessment and analysis expand their share as businesses develop more strategic approaches to their digital transformation initiatives. System integration and consulting services continue playing a critical role in integrating different security systems into one environment. In June 2026, Hitachi and Google Cloud expanded their alliance, advancing physical AI deployment and strengthening enterprise cybersecurity against AI-driven threats. The category of maintenance and support services helps in keeping the consistency of systems and infrastructure.

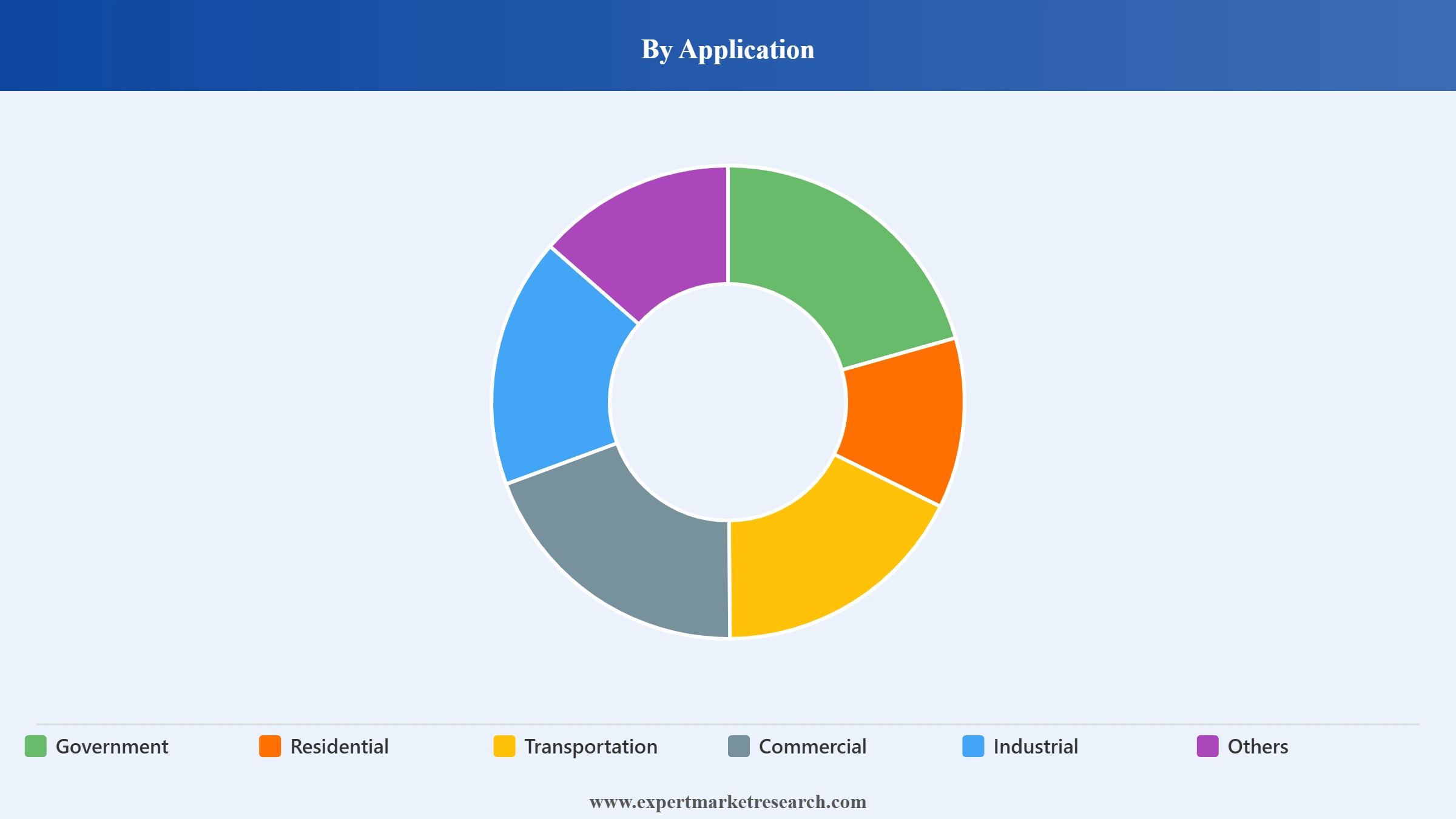

Market Breakup by Application

Key Insight: The need for application varies in relation to risk levels associated with operations. Businesses lead the security market growth as a result of consistent investment in security system modernization. Industrial facilities are one of the fastest adopters of security applications due to increased needs for cybersecurity and physical security as a result of connectivity in these facilities. The government agencies around the world are also adding to the market value considering the responsibilities related to national security. Transportation agencies focus on surveillance and perimeter security in addition to passenger security. Others cater for specific operational environments.

Market Breakup by Region

Key Insight: Regional growth trends are characterized by the diversity in the level of digital maturity and infrastructure modernization. North America is positioned at the forefront of the global security market owing to its consistent innovation, adoption by enterprises, and cybersecurity investments. Growth in Asia Pacific is fueled by the increasing pace of digital transformation, industrial expansion, and development of smart infrastructure projects. Europe boasts the advantages of the regulation-led modernization of security and strong focus on critical infrastructure security. Latin America keeps on integrating security technologies into its business and public safety applications. The Middle East and Africa witness increasing investments in large-scale infrastructure security and smart city security projects.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Video surveillance systems continue to dominate the market due to AI-enabled real-time monitoring adoption

The segment that represents the greatest share of the global security market belongs to video surveillance systems as organizations increasingly install artificial intelligence-enabled cameras, video cloud management systems, and advanced video analytics in their commercial, industrial, transportation, and public infrastructure facilities. Businesses are switching from old-style CCTV systems to intelligent surveillance systems that can recognize faces, behavior patterns, license plates, and make predictions. In June 2026, Alarm Detection Systems launched SEEKER, combining AI analytics with live operator intervention for proactive real-time threat detection.

The fastest growing segment of the global security market is represented by access control systems with companies focusing on identity authentication, biometric access control, mobile credentials, and zero-trust security policies. Companies integrate digital and physical identities by deploying hybrid access management systems via cloud technology to manage distributed and hybrid business locations. There is continued demand in the healthcare, financial, manufacturing, education, and government industries where access control is becoming an important part of enterprise security architecture. In May 2026, Cognizant launched Secure AI Services, enabling enterprises to securely govern, protect, and scale agentic AI systems responsibly.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Managed security services dominate the market owing to rising outsourced cybersecurity operations

Managed security services are largely contributing to the security market revenue, as businesses become more dependent on outsourcing services related to continuous threat monitoring, incident response, vulnerability management, and compliance. The increasing shortage of cybersecurity professionals and expansion of IT infrastructure motivate companies to switch to subscription-based security models providing 24/7 support. Providers are actively developing their capabilities for AI-based Security Operation Centers, managed detection and response, and cloud security. For example, in June 2026, Check Point expanded its MSP platform with AI security, unified bundles simplifying secure AI adoption.

The segment of risk assessment and analysis is also expanding its share in the security market as businesses start conducting proactive risk assessments prior to deploying new digital infrastructure, cloud services, automation systems, and interconnected devices. Enterprises need to conduct comprehensive risk assessments to analyze risks from operational, cyber, regulatory, and physical perspectives in one framework. Consulting firms and security vendors are developing their assessment tools using AI-powered analytics, digital twins, and predictive modeling. For example, in June 2026, FlowForma launched FlowAssure, an evidence-first AI platform automating vendor risk assessments, accelerating reviews, and improving auditability.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Commercial applications account for the largest share of the market through enterprise-wide integrated security infrastructure investments

Commercial applications are contributing to the security market value as corporations make more investments into intelligent surveillance, access management, cyber security integration, and building security automation. Commercial enterprises, including corporate offices, banks, retail outlets, hotels, healthcare companies, and universities, need robust security ecosystems that will ensure the protection of employees, clients, physical and IT assets simultaneously. Manufacturers are developing integrated platforms that involve video analytics, identity management, and real-time monitoring, allowing commercial companies to operate effectively in compliance with the new regulations and corporate governance policies. For example, in June 2026, India-based HIVE launched an AI platform delivering verified, evidence-based clinical decision support for healthcare professionals.

As per the security market report, there is a rapid growth of industrial applications as manufacturing, utility, logistics, and energy sectors enhance the security of operational technology systems against cyberattacks and physical threats. Smart factories, interconnected production lines, and industry 4.0 initiatives require the development of security solutions for industrial control systems and critical equipment. Vendors are developing special platforms that combine OT cybersecurity, AI surveillance, predictive monitoring, and access management. This helps to increase resilience of industrial operations by avoiding interruptions and downtime. In June 2026, Data Theorem launched the first closed-loop AI security platform, automating exploit detection, remediation, and runtime application protection.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America accounts for the leading market position through technology innovation and cybersecurity leadership

North America holds the position of the biggest regional security market on account of enterprise digitalization, high cybersecurity implementation rate, robust investments into the security of critical infrastructure, as well as the presence of top global security technology firms. Enterprises operating in financial, healthcare, governmental, manufacturing, and tech industries continue upgrading their security infrastructures using artificial intelligence, cloud technologies, and comprehensive identity management.

The Asia Pacific security market records the fastest growth on account of smart city initiatives, industrial automation, digitalization of public services, and cloud adoption in the region. Manufacturing capacity, urbanization processes, and development of critical infrastructure bring significant opportunities for the use of integrated security technologies. Enterprises operating in Asia Pacific actively invest in intelligent surveillance systems, biometric solutions, cybersecurity platforms, and managed security services in order to ensure security of fast-growing digital ecosystems. In July 2026, ESDS launched Swaraj Cloud, India's sovereign AI-autonomous cloud platform ensuring secure, compliant, Indian-hosted enterprise infrastructure.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Competitiveness is escalating in the global market as security companies are integrating physical security, perimeter protection, AI-based surveillance, and intelligent access control systems to build security ecosystems. Cloud-based monitoring systems, predictive analytics, autonomous intrusion detection, and cyber security integrations are key investment opportunities that vendors are making to stand out in the market. Collaborations and partnerships with smart cities planners, industrial infrastructure owners, transportation organizations, and defense entities are bringing new business opportunities for vendors.

Leading security market players are also considering the modularity of security systems that can be customized for commercial, industrial, and government projects. Rising demands for critical infrastructure protection are leading vendors to create interoperable security systems that integrate barriers, sensors, surveillance cameras, and command centers via one platform. Furthermore, vendors are expanding their geographical footprint by building their distribution networks and localized manufacturing. Continuous investment in AI automation, edge computing, and integrated security management systems is expected to continue to be the core competitive advantage in the coming years.

Ameristar Perimeter Security was founded in 1982 and operates from Oklahoma, United States. It offers its services in high-security perimeter fencing and barriers. Its core services include the manufacture of high-security perimeter fencing, gates, and integrated barriers, with special emphasis on long-life anti-climb barriers and rapid deployment barriers.

ATG Access Ltd. was founded in 1989 and is based in the United Kingdom. The company manufactures products that mitigate hostile vehicle threats such as bollards, road blockers, and integrated access control solutions. Its key areas of service include airport terminals, government buildings, commercial developments, and public sites.

Barrier1 Systems, LLC was founded in 2006, and its headquarters are located in North Carolina, United States. The company produces vehicle barriers, security gates, bollards, wedge barriers, and custom-made perimeter security systems. Barrier1 Systems emphasizes providing engineered security solutions for military bases, transportation systems, data centers, and industrial facilities through fast installations and project-specific customization.

CIAS Elettronica Srl was founded in 1974, and its headquarters are located in Milan, Italy. The company specializes in developing perimeter intrusion detection systems that use microwave barriers, fiber optics, fence protection, and smart detection systems. CIAS Elettronica Srl provides highly accurate security monitoring with low false alarm rates for critical infrastructures, airports, prisons, and power plants.

Other key players in the market include Delta Scientific Corporation, Hangzhou Hikvision Digital Technology Co., Ltd., Zhejiang Dahua Technology Co. Ltd., ASSA ABLOY AB, Motorola Solutions, Inc., and Axis Communications AB, among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Discover the latest insights on the Global Security Market 2026 with our comprehensive report. Stay ahead of the curve with valuable data on system innovations, integrator demand, and top growth regions. Whether you are launching a new surveillance line or expanding into managed security services, this report gives you the clarity you need. Download your free sample now and discover the key opportunities in the thriving Global Security industry.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the global security market value was USD 404.93 Billion.

The market is expected to grow at a CAGR of 7.30% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach USD 819.18 Billion by 2035.

The major drivers include increase in cyber attacks, development of industrial sector, and CCTV adoption in prominent economies globally.

The key trends include the growth in smart city projects along with smart home adoption.

The major regions in the market are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific.

The systems of security available are access control systems, intrusion detection systems, video surveillance systems, and barrier systems, amongst others.

Major applications include government, residential, transportation, commercial, industrial, and others.

By service, the market is categorised into system integration and consulting, risk assessment and analysis, managed security services, and maintenance and support.

The major players in the market include ATG Access Limited, Barrier1 Systems, LLC, Cias Elettronica Srlare, Perimeter Protection Germany GmbH, Delta Scientific Corporation, Hangzhou Hikvision Digital Technology Co., Ltd., Zhejiang Dahua Technology Co. Ltd., ASSA ABLOY AB, and Motorola Solutions, Inc.

The different types of security include equipment and services.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by System |

|

| Breakup by Service |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.