Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

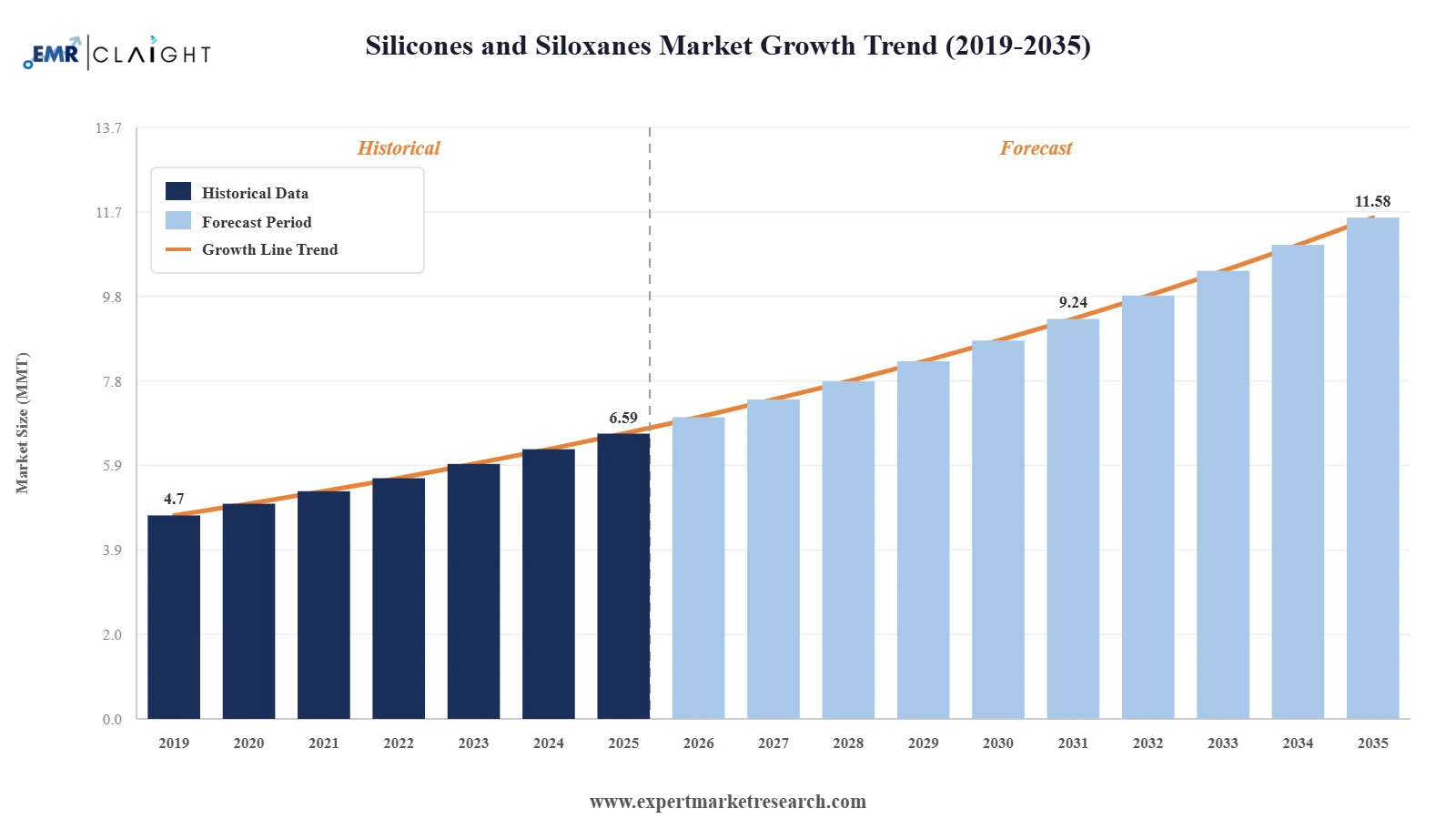

The silicones and siloxanes market attained a volume of 6.59 MMT in 2025 and is projected to expand at a CAGR of 5.80% through 2035. The market is further expected to achieve a volume of 11.58 MMT by 2035. Rising adoption of electric vehicles is accelerating demand for heat-resistant silicones. This has enabled suppliers to secure long-term contracts by developing battery-grade materials with improved insulation, safety performance, and extended operational lifespans globally.

Growing demand from medical devices is significantly driving growth in the market, as implantable components require biocompatible, sterilization-stable silicones. Another factor is construction refurbishment, where long-lasting silicone sealants reduce lifecycle costs. These uses favor suppliers investing in formulation consistency, regulatory testing, and application-specific technical support rather than volume-led commodity expansion, boosting the overall silicones and siloxanes market value.

Companies are focusing on reducing volatile siloxane emissions while maintaining thermal stability. For example, in January 2024, Wacker Chemie AG expanded its specialty silicone elastomer portfolio in Europe with a new low-cyclic siloxane grade targeting electronics and medical molding applications. This move came as Europe, Middle East, and Africa (EMEA) alone procured USD 675.1 millions of electronic system design products and services in Q3 2025, increasing demand for high-purity silicone materials used in encapsulation, sealing, and thermal management. Such developments in the silicones and siloxanes market show how leading manufacturers are prioritizing performance compliance over commodity volumes, positioning silicones as critical inputs in regulated and precision-driven industries.

The market is increasingly shaped by downstream specializations. Automotive OEMs are specifying advanced silicone fluids for EV battery protection and lightweight sealing. Construction suppliers are shifting toward long-life silicone sealants that reduce maintenance cycles. For example, companies like Hempaguard NB are offering silicone hull coating performance to the newbuilding stage, without the need for pre-or post-delivery dry docking since June 2025. Meanwhile, personal care manufacturers are reformulating with volatile-free siloxanes to meet tightening regulatory scrutiny, accelerating the overall demand in the silicones and siloxanes market. Premium grades command stronger margins as customers value durability, safety, and formulation consistency over pricing flexibility.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Global Silicones and Siloxanes Market Report Summary | Description | Value |

| Base Year | MMT | 2025 |

| Historical Period | MMT | 2019-2025 |

| Forecast Period | MMT | 2026-2035 |

| Market Size 2025 | MMT | 6.59 |

| Market Size 2035 | MMT | 11.58 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 5.80% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 6.8% |

| CAGR 2026-2035 - Market by Country | India | 9.1% |

| CAGR 2026-2035 - Market by Country | UK | 7.5% |

| CAGR 2026-2035 - Market by Type | Resins | 5.8% |

| CAGR 2026-2035 - Market by Application | Home and Personal Care | 6.0% |

| Market Share by Country 2025 | Germany | 4.8% |

WACKER and SICO Performance Material launched a new application development center for organofunctional silanes in Jining, China. Such developments strengthen application-driven silane innovation, showing how companies can invest in co-located R&D to accelerate customized silicone formulations, thereby boosting the overall silicones and siloxanes market growth.

Elkem ASA launched SILBIONE LSR Select EC 70, an advanced medical-grade liquid silicone rubber. Competitors can leverage this silicones and siloxanes market trend and invest in cleanroom production, biocompatibility testing, and long-term supply partnerships.

Evonik Coating Additives launched TEGO Foamex 8051, the newest product in its TEGO Foamex series of defoamers. These developments signal growth in silicone-based additives for performance coatings, creating opportunities for suppliers to expand siloxane-derived additives that improve surface quality and process efficiency across industrial formulations.

Shin-Etsu Chemical Co., Ltd. created innovative silicone products for personal care uses as part of its silicon chemistry-focused solutions. Hence, silicone producers can also develop low-volatility, regulation-ready siloxanes that preserve sensory performance while meeting tightening global compliance standards.

Electrification is reshaping demand patterns across the silicones and siloxanes market. EV manufacturers increasingly rely on high-performance silicone elastomers for battery insulation, fire resistance, and thermal gap filling. Silicone suppliers are responding with battery-grade materials designed to withstand higher voltages and thermal cycling. Companies like Dow and Wacker are prioritizing flame-retardant and low-outgassing silicone formulations. For example, in August 2025, WACKER unveiled fire-resistant silicone rubber to enhance EV battery safety, offering cost-effective insulation through extrusion.

Stricter healthcare regulations are pushing the demand for medical-grade silicones and siloxanes. This has increased the adoption of platinum-cured silicones in implants, tubing, and wearable devices. In response, major producers are expanding cleanroom manufacturing and traceability systems. Low extractables and consistent molecular weight control have become critical for device manufacturers targeting FDA and EU MDR approvals, widening the silicones and siloxanes market scope. For example, Zhermack offers two silicones called ZA SFX 0020 and ZA SFX 10 WT 10, which have passed biocompatibility tests in October 2023.

Construction-related silicones are benefiting from evolving building codes emphasizing durability and energy efficiency. Silicone sealants and façade coatings offer UV resistance, elasticity, and long service life, making them suitable for extreme climates. Manufacturers are launching neutral-cure and low-VOC silicone sealants to align with green building certifications. For instance, in March 2023 Dow announced the expansion of its silicone sealant products to offer photovoltaic (PV) module assembly materials, accelerating the overall silicones and siloxanes market value. Suppliers targeting construction firms and developers can thus focus on application-specific systems rather than generic sealants, improving margins and repeat procurement.

Personal care regulations are reshaping siloxane demand. Authorities in Europe and parts of North America are restricting cyclic siloxanes like D4 and D5, compelling reformulation across cosmetics and haircare products. In response, silicone producers are launching alternative siloxane fluids with lower volatility and improved biodegradation profiles. For example, Dow Personal Care debuted its first silicone elastomer blends with an extended portfolio for color cosmetics, skin care, and hair care, at the New York Society of Cosmetics Chemists (NYSCC) Suppliers’ Day, in the United States, in June 2025. Large FMCG companies are locking in supply partnerships with silicone producers that offer formulation support. This silicones and siloxanes market trend is shifting competition toward specialty fluids and application expertise rather than commodity silicone oils.

Governments are encouraging localized chemical manufacturing to reduce import dependency and logistics risk. National industrial strategies in China, India, and the Middle East support domestic silicone production through incentives and infrastructure investment. As a result, silicone producers are expanding regional plants and debottlenecking existing facilities. This improves delivery reliability for downstream users in electronics, construction, and healthcare, opening up new silicones and siloxanes market opportunities. Companies are directing this focus on regional capacity to respond faster to custom orders and demand fluctuations. For example, in January 2026, Trelleborg Group expanded its LSR tooling expertise with the acquisition of Nexus Elastomer Molds GmbH.

The EMR’s report titled “Global Silicones and Siloxanes Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

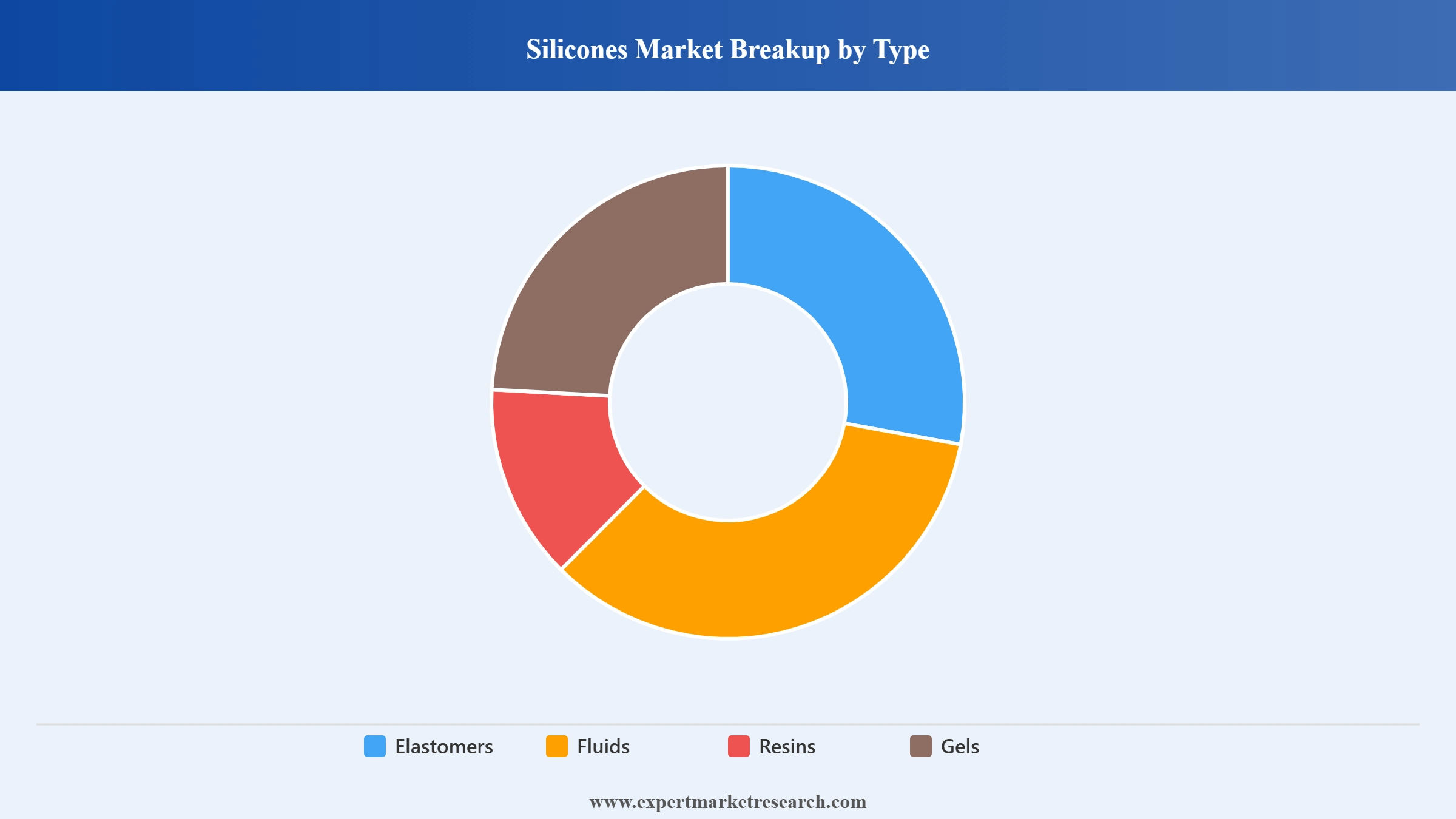

Silicones Market Breakup by Type

Key Insight: Elastomers lead the market due to durability and regulatory trust, while fluids grow through reformulation needs. Resins support coatings and adhesion systems requiring rigidity and gels serve niche damping and protection uses. In January 2025, SIO New Material (SIOResin) announced the launch of SIOResin SIO-517, a room temperature curing high-temperature resistant silicone resin. Each segment considered in the silicones and siloxanes market report, responds to different performance expectations. Suppliers manage portfolios carefully to avoid overlap.

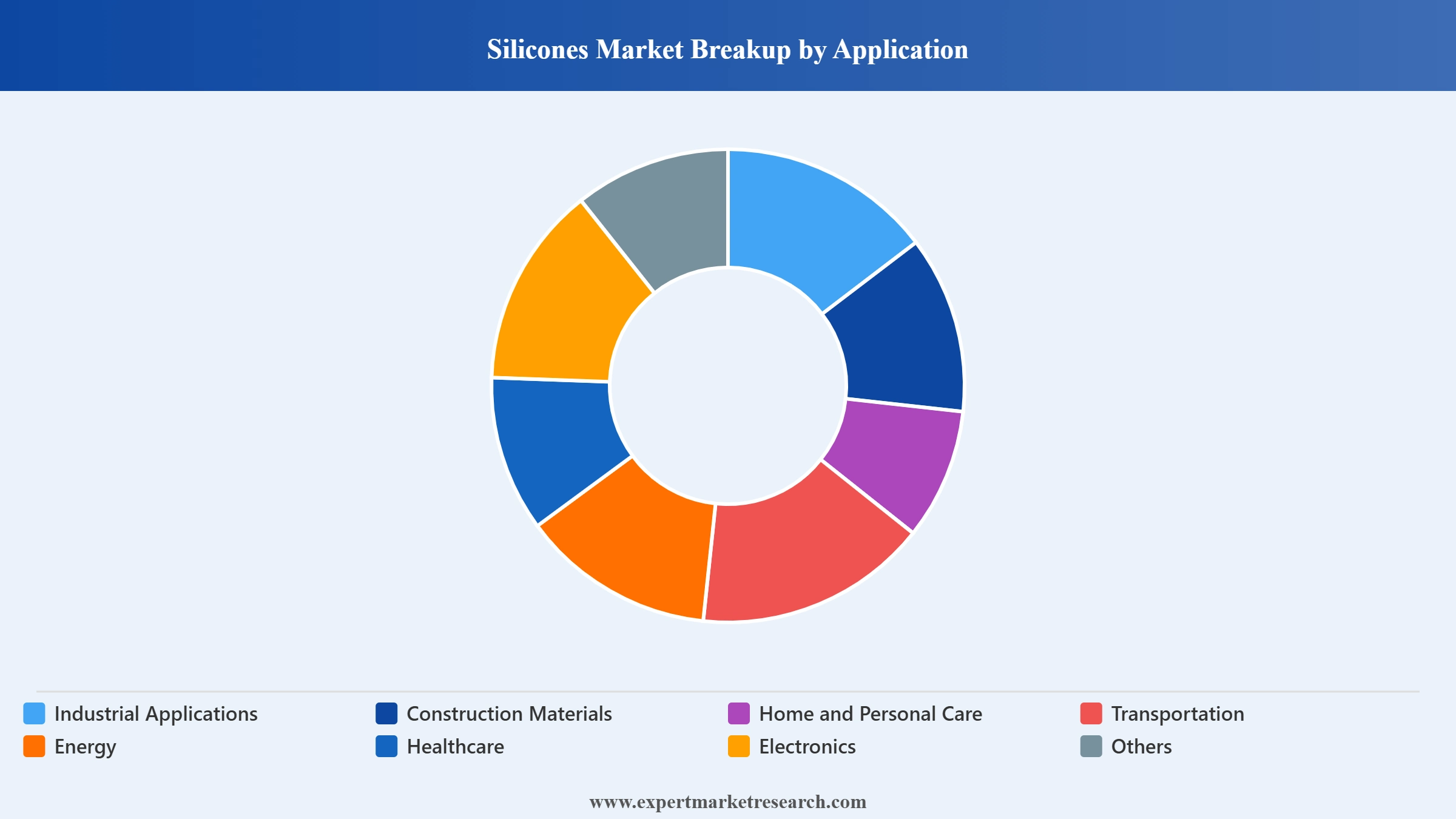

Silicones Market Breakup by Application

Key Insight: Currently, industrial applications lead silicone consumption due to large volumes and consistent performance requirements. Healthcare demand is expanding its share in the silicones and siloxanes market revenue as regulations mandate higher material purity and safety. Construction relies on durability and weather resistance; on the other hand transportation prioritizes fire safety and vibration control. Energy systems require thermal stability, and electronics depend on precision and purity.

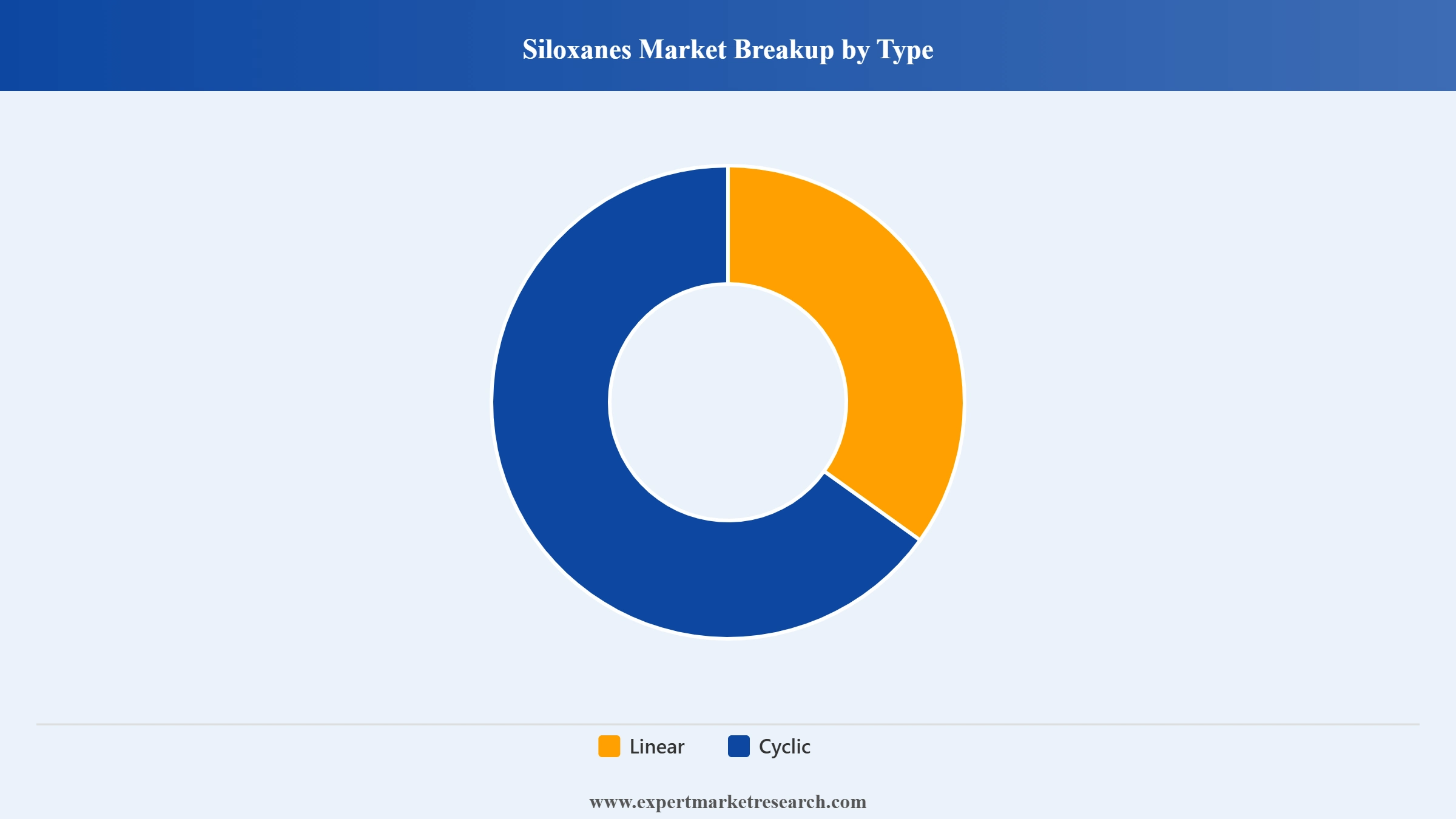

Siloxanes Market Breakup by Type

Key Insight: Linear siloxanes represent the key driving factor boosting the overall silicones and siloxanes demand due to stable behavior and process reliability. Cyclic siloxanes support efficiency-driven polymerization and specialty synthesis. Material consistency remains critical for downstream quality, hence, suppliers must balance compliance requirements with performance efficiency. Strategic positioning determines long-term viability in regulated markets.

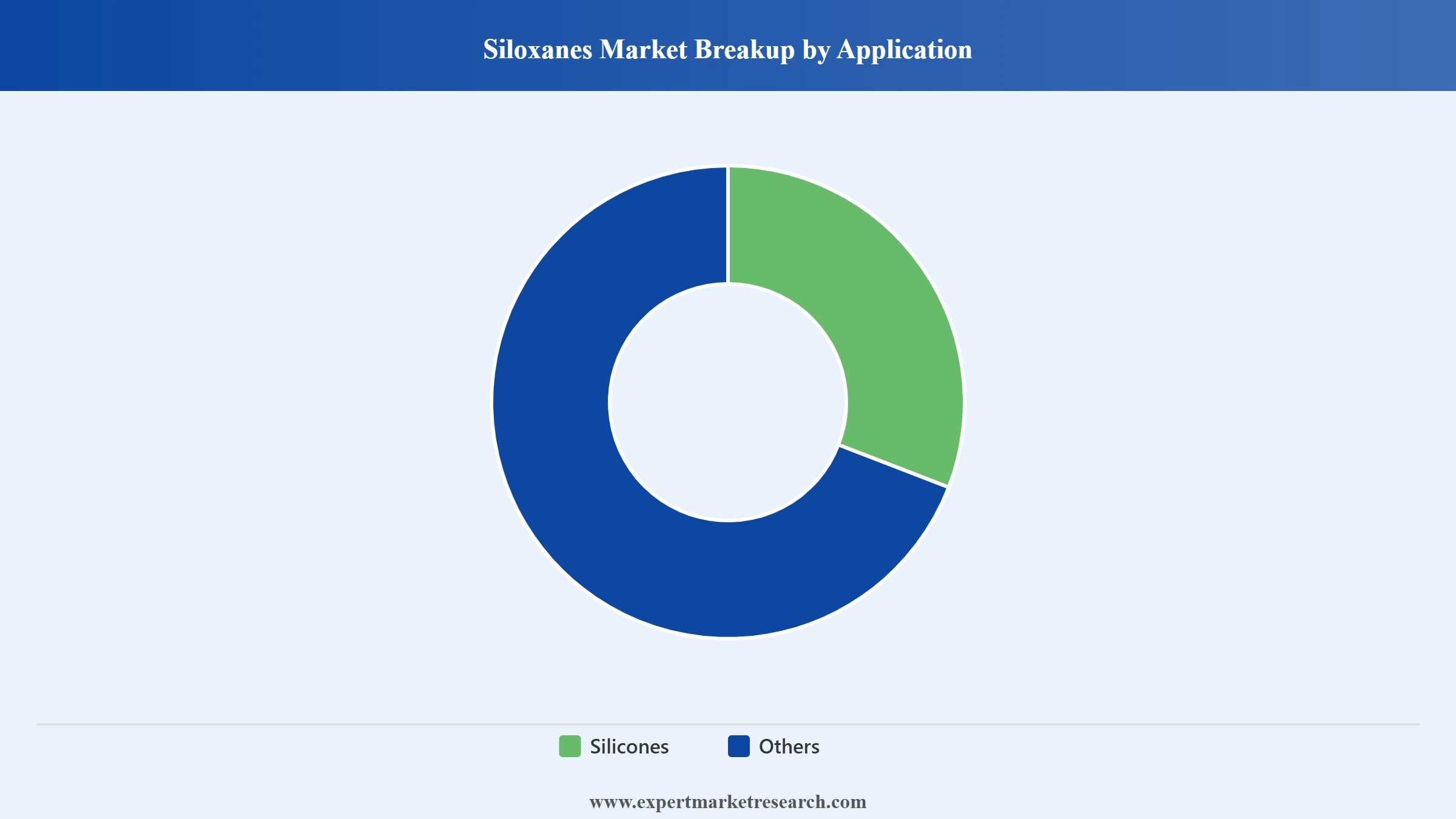

Siloxanes Market Breakup by Application

Key Insight: While silicone production dominates the majority of the consumption. Other applications are growing through specialty chemical use. Siloxanes are used in coatings, lubricants, and surface treatments. Companies like Evonik are launching siloxane-based defoamer for WB inks & overprint varnishes. Growth in the silicones and siloxanes market also comes from industrial performance needs. Producers tailor siloxanes for specific reactions in this category as customization matters more than scale.

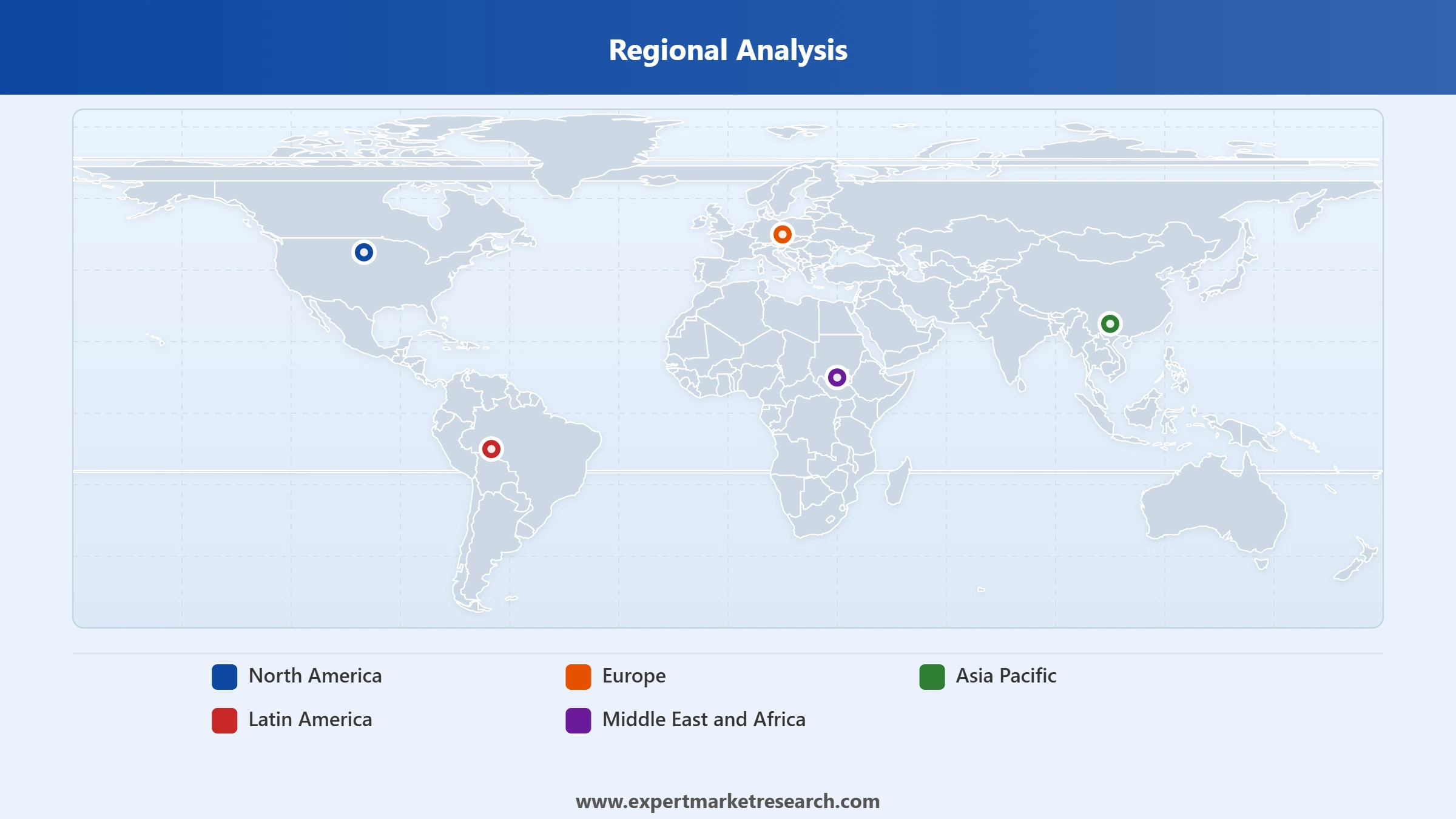

Market Breakup by Region

Key Insight: Asia Pacific leads the global market through manufacturing scale and downstream demand concentration. Europe emphasizes compliance, sustainability, and regulatory alignment. North America prioritizes innovation and high-performance applications. The Middle East is expanding capacity to support industrial diversification. Latin America is developing selectively, driven by localized demand. Regional silicones and siloxanes market dynamics vary widely in maturity and regulation.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By silicone type, elastomers hold the largest market share due to durability and multi-industry adoption

Silicone elastomers lead the market because they deliver mechanical stability across demanding environments. Industrial manufacturers rely on elastomers for sealing, gasketing, and insulation where heat, pressure, and chemical exposure are constant. Automotive and electronics players favor elastomers due to flexibility retention over long operating cycles. Medical device producers also depend on elastomers for implantable and wearable components. Such nuanced industrial use cases drive producers to refine platinum-cured and low-extractable grades to meet compliance needs. For example, in May 2025, Dow enriched its beauty care portfolio with bio-based and silicone ingredients and introduced carbon-neutral silicone elastomers at New York SCC.

Silicone fluids are also gaining major momentum in the silicones and siloxanes market due to reformulation pressure across personal care, lubricants, and thermal management systems. Cosmetic brands are shifting toward modified silicone fluids with controlled volatility and improved spread-ability. Electronics manufacturers use fluids for heat transfer and dielectric protection. So, producers are developing specialty fluids that balance performance with regulatory acceptance.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Industrial applications account for the largest share of the market due to performance-driven and regulated usage requirements

Industrial applications dominate silicone consumption because performance failure carries high operational risk. Manufacturers use silicones for insulation, sealing, lubrication, and protection in harsh environments. Chemical plants, machinery producers, and electronics assemblers rely on stable performance under temperature stress. Silicone suppliers target this segment with application-specific grades rather than general-purpose products. For example, in November 2025, WEVO-CHEMIE GmbH introduced WEVOSIL 23010 and WEVOSIL 23030, two new liquid silicone rubbers (LSRs) specially developed for silicone textile coatings and sealing applications (CIPG/FIPG).

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The healthcare category, driven by regulatory-driven material upgrades, is also expanding its share in the silicones and siloxanes market scope. Medical devices require biocompatible and sterilization-stable silicones. Producers are expanding medical-grade portfolios to support implants, tubing, and wearable diagnostics. Healthcare OEMs demand traceability and documentation. Silicone suppliers are investing in cleanroom production and validation processes. For instance, Gerresheimer offers complete, silicone-oil- and PFAS-free syringe systems made from glass and cyclic olefin polymer (COP) for the pharma, biotech and cosmetics industries, since April 2025.

Linear siloxanes secure the largest share of the market due to stability and downstream compatibility

Linear siloxanes lead the overall silicones and siloxanes industry growth because they offer predictable molecular behavior and formulation flexibility. They are widely used as intermediates in silicone production. Linear structures provide stability across temperature ranges. Manufacturers prefer them for controlled reactions and consistent output while suppliers focus on purity and consistency to meet downstream quality standards. Demand in this category remains steady as they anchor silicone value chains.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Cyclic siloxanes are growing through specialty use despite regulatory pressure. Producers are refining low-emission cyclic grades for controlled applications. Growth comes from closed-loop systems and industrial processing rather than consumer exposure. Companies invest in emission control and recovery systems to comply with regulatory thresholds while enabling efficient polymerization routes. For instance, in July 2025, Elkem ASA announced the launch of innovative cosmetic formulations with low-cyclic silicone ingredients.

By application, silicone production dominates siloxane consumption due to integrated value chains

Silicone production consumes the majority of siloxanes as essential intermediates. Integrated producers convert siloxanes internally to control quality and cost. Vertical integration improves margins and reduces exposure to volatility. Producers focus on process efficiency and yield optimization. This segment favors large manufacturers with chemical integration capabilities. Investment efforts are mainly directed towards reactor efficiency and waste reduction. Companies like Elkem ASA are initiating strategic reviews of their silicones division as part of their efforts to streamline operations and reallocate resources.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific secures a substantial share of the market due to manufacturing scale and downstream demand concentration

Asia Pacific dominates the silicones and siloxanes market due to manufacturing concentration and demand diversity. Electronics, automotive, and construction industries drive consumption. For example, Azimuth AI & Cyient Semiconductors announced the launch of ARKA GKT-1, India's first-gen IP powered silicon chip for edge AI & smart energy in November 2025. Producers also benefit from integrated supply chains and government-backed industrialization.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Middle East and Africa is emerging as the fastest-growing silicones and siloxanes market due to industrial diversification efforts. Governments are encouraging local chemical manufacturing to reduce import dependence. Demand is rising across construction, energy, and healthcare applications. Infrastructure investments are supporting steady consumption growth. Producers see the region as a strategic expansion hub as local production improves supply reliability. Ongoing capacity development is strengthening long-term demand visibility across multiple end-use industries.

Leading silicones and siloxanes market players are shifting focus from volume expansion toward specialty grades for electronics, healthcare, and electric vehicles. Investment is flowing into low-cyclic, high-purity, and flame-resistant formulations that meet tightening regulations. Opportunities are emerging through long-term supply agreements with OEMs seeking material consistency. Players are also localizing production to reduce logistics risk and meet government-backed industrial policies. Digital process control and closed-loop manufacturing are becoming cost advantages.

Silicones and siloxanes companies that integrate upstream siloxanes with downstream silicone products gain margin stability. The market rewards suppliers that combine regulatory readiness, formulation expertise, and reliable delivery. Competitive differentiation now depends less on scale alone and more on technical collaboration with customers during product development cycles. This shift favors firms investing early in compliance testing, customer labs, and co-development platforms globally to secure future-focused contracts across industries across the world.

Dow Chemical Company, established in 1897 and headquartered in Michigan, United States, serves the silicones market through advanced materials focused on electronics, mobility, and construction. Dow supplies silicone elastomers, fluids, and sealants designed for thermal management and safety. The company invests heavily in low-outgassing and flame-retardant technologies for EVs and data centers.

Wacker Chemie AG, founded in 1914 and headquartered in Munich, Germany, is a major supplier of specialty silicones and siloxanes. The company focuses on high-purity elastomers and medical-grade silicones. Wacker supports electronics and healthcare manufacturers requiring strict regulatory compliance. Recent investments emphasize low-cyclic siloxanes and closed-loop production. Wacker caters to customers through technical centers and localized plants.

Founded in 2012 and based in Bengaluru, India, Momentive Performance Materials Inc. specializes in advanced silicones for industrial and electronics uses. Momentive focuses on specialty elastomers, resins, and fluids. The company targets aerospace, EVs, and semiconductor packaging. Momentive invests in formulation science and application testing. It serves customers needing tailored performance rather than commodity volumes.

Shin-Etsu Chemical Co., Ltd., founded in 1926 and headquartered in Tokyo, Japan, is a leading global silicone producer. The company supplies silicones and siloxanes for electronics, construction, and healthcare. Shin-Etsu emphasizes vertical integration and process efficiency. Its materials support semiconductor manufacturing and medical devices.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other key players in the market include Elkem Silicones, among others.

Unlock the latest insights with our silicones and siloxanes market trends 2026 report. Discover regional growth patterns, consumer preferences, and key industry players. Stay ahead of competition with trusted data and expert analysis. Download your free sample report today and drive informed decisions in the market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate volume of 6.59 MMT.

The market is projected to grow at a CAGR of 5.80% between 2026 and 2035.

By 2035, the global silicones and siloxanes market is estimated to reach 11.58 MMT.

Manufacturers are expanding specialty grades, investing in low-cyclic chemistries, localizing production, strengthening OEM collaborations, upgrading process efficiency, and securing long-term contracts while aligning portfolios with regulatory, sustainability, and customer requirements.

The key trends guiding the market are the use of siloxanes and silicones in the food industry, the versatility of silicones, and the surging use of liquid silicone as a lubricant and waterproof sealant in window fittings and bathrooms.

The major regions in the market are North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa.

The major types of silicones in the market are elastomers, fluids, resins, and gels, while the major siloxanes types are linear and cyclic.

The various applications of siloxanes are silicones, among others, whereas silicones find applications in industrial applications, construction materials, home and personal care, transportation, energy, healthcare, and electronics, among others.

The key players in the market include Dow Chemical Company, Wacker Chemie AG, Momentive Performance Materials Inc., Shin-Etsu Chemical Co., Ltd., and Elkem Silicones, among others.

Companies face regulatory pressure on siloxanes, raw material volatility, high energy costs, long qualification cycles, capital-intensive expansions, and rising customer expectations for supply reliability and compliance across global markets.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Silicones Market Breakup by Type |

|

| Silicones Market Breakup by Application |

|

| Siloxanes Market Breakup by Type |

|

| Siloxanes Market Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.