Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

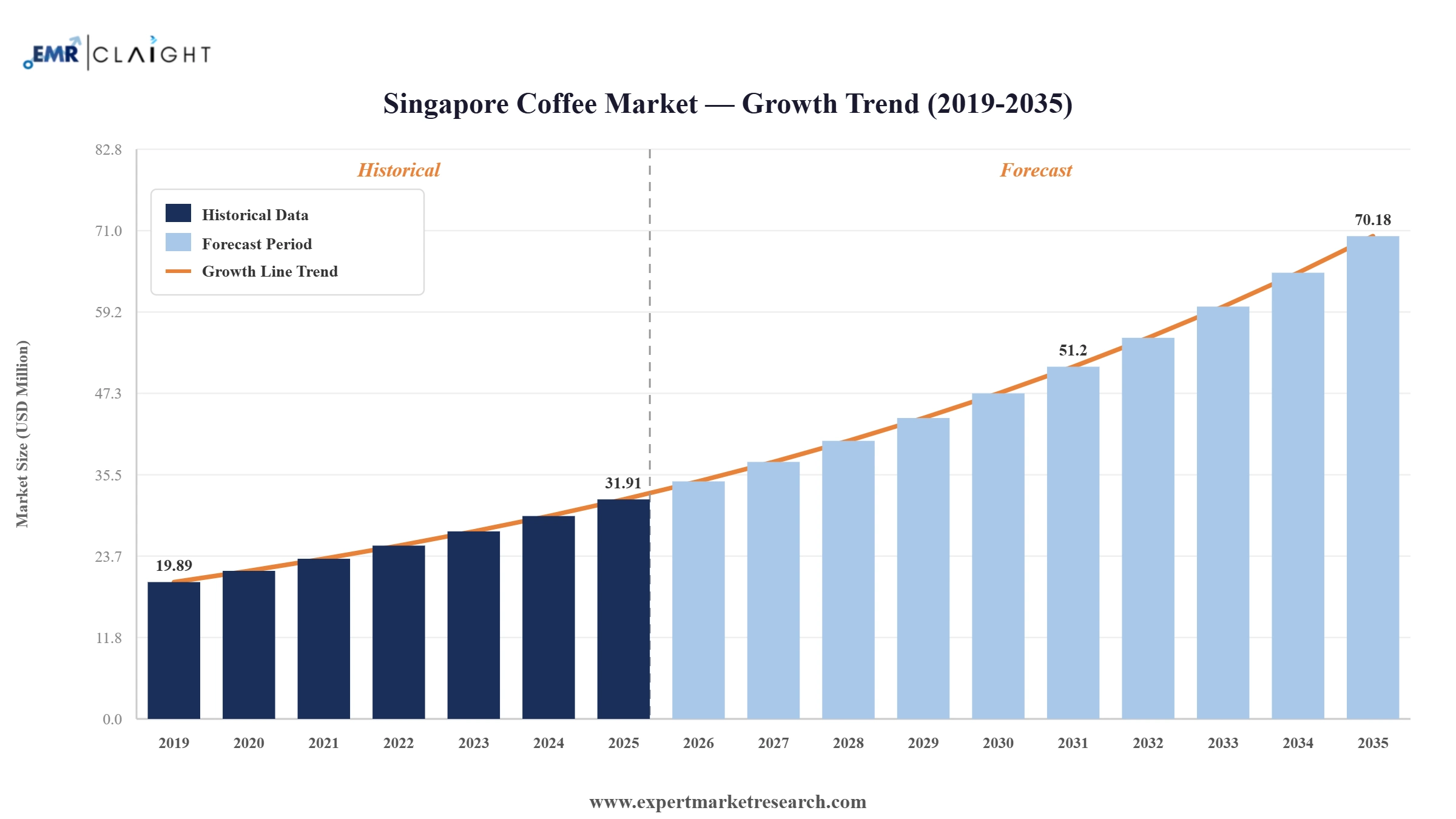

The Singapore coffee market reached a value of USD 31.91 Million in 2025 and is projected to expand at a CAGR of around 8.20% during the forecast period of 2026-2035. Singapore's vibrant café culture, strong consumer demand for premium and specialty coffee, the growing kopitiam coffee ecosystem, expanding HoReCa sector, and the rapid adoption of coffee pods and capsules are driving Singapore coffee market growth. The market is expected to reach USD 70.18 Million by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Singapore coffee market is driven by Singapore's vibrant café culture, the growing popularity of specialty and artisanal coffee, expanding international coffee chain presence, the strong kopitiam traditional coffee heritage, and growing consumer demand for premium, sustainable, and single-origin coffee experiences among Singapore's cosmopolitan population.

Luckin Coffee established 81 self-operated outlets in Singapore as of March 2026, reinforcing its position as a key affordable premium coffee chain in Singapore's competitive coffee market. Singapore serves as Luckin Coffee's first international market for self-operated store operations, with the chain leveraging lessons from Singapore to improve partner operations and local market insights for further international expansion. Singapore's chained specialist coffee and tea shops market is forecast to grow at a CAGR of approximately 9% from 2026 to 2030.

ZUS Coffee, a Malaysia-based coffee chain founded in 2019 that operates approximately 550 outlets in Malaysia, entered Singapore in December 2024 with its first international market store at Changi Airport's Terminal 4. Singapore became ZUS Coffee's second international market after the Philippines, where it opened 46 stores in September 2023. ZUS Coffee aims to join leading global coffee brands including Starbucks, The Coffee Bean & Tea Leaf, and Paris Baguette in Singapore's competitive coffee chain market.

Oriental Kopi, a Malaysia-based coffee chain, established a collaboration with Paradise Group, a Singapore-based food and beverage company, in May 2024 to establish its presence in Singapore's growing coffee chain market. The collaboration reflects the growing trend of Southeast Asian regional coffee chains entering Singapore's competitive coffee market. Singapore's brand shares for Luckin Coffee jumped from 2% to 10% between 2023 and 2025, reflecting strong consumer appetite for affordable specialty coffee alternatives.

Singapore's specialty coffee adoption continued to accelerate in early 2024, with a growing ecosystem of local roasters including Perk Coffee Pte Ltd. offering single-origin profiles and Southeast Asian flavor-inspired blends. Singapore's highly tech-savvy and affluent consumer base, combined with the growing influence of third-wave coffee culture, is driving demand for single-origin, artisanal, and sustainably sourced coffee products. Ground coffee pods are emerging as a standout segment, bridging specialty quality with convenience for time-pressed professionals.

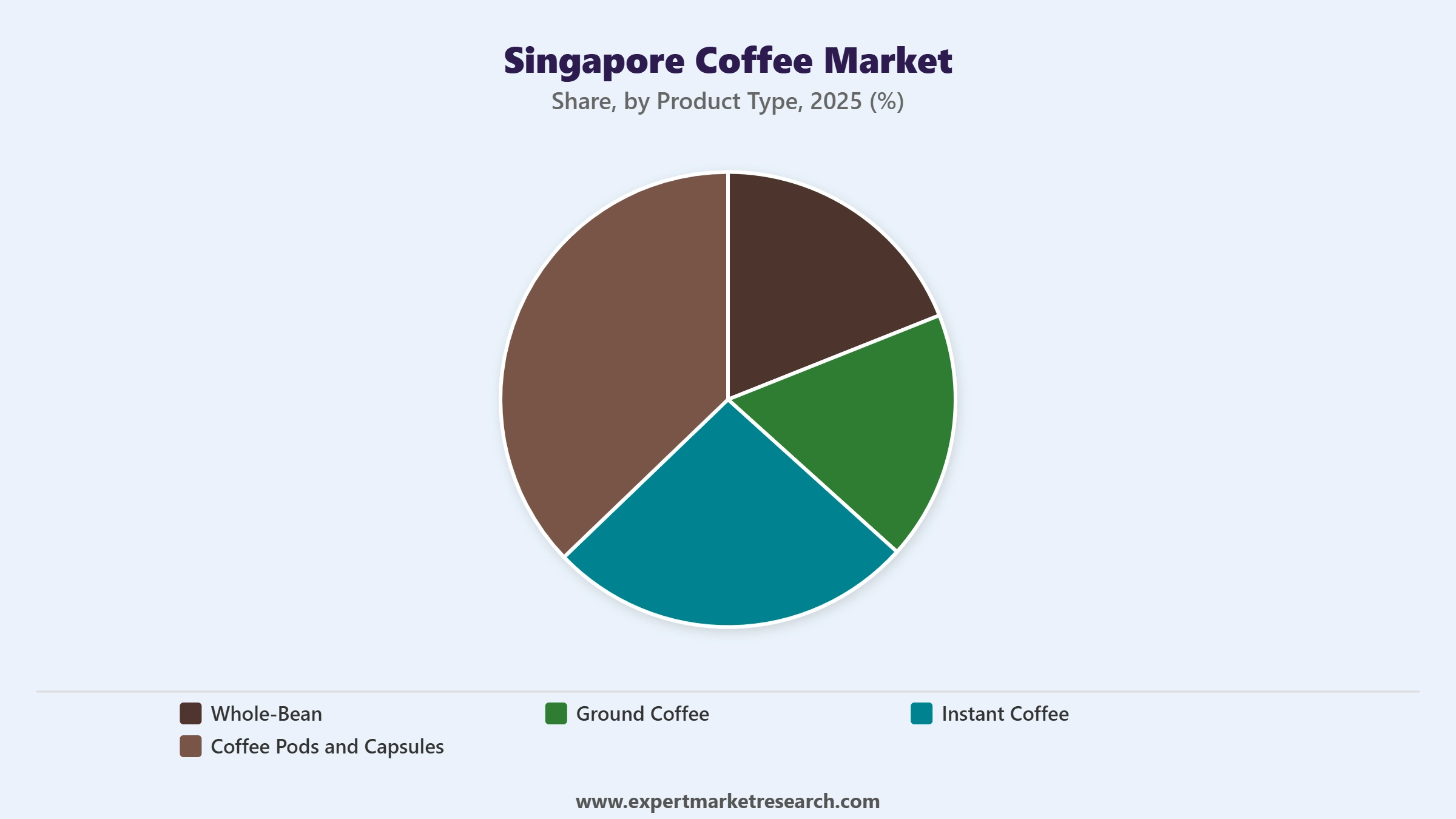

Ground Coffee is the dominant Singapore coffee market product type, driven by the essential role of ground coffee in Singapore's growing specialty café sector, established kopitiam coffee culture, and the demand for freshly brewed coffee experiences. Singapore's specialty café scene serves approximately 1,000 customers per day in the Central Province on average. Ground coffee growth is supported by the expanding third-wave café culture among Singapore's millennials and Gen Z consumers.

Instant Coffee is a significant Singapore coffee market product type, driven by its convenience, affordability, and ease of preparation among Singapore's busy professional and student population. Instant coffee from brands including Nescafe (Nestle), Old Town White Coffee, and Kopiko is widely consumed across household and office settings. Instant coffee is expected to gain a growing Singapore coffee market share through innovations in premium instant formats catering to quality-conscious consumers.

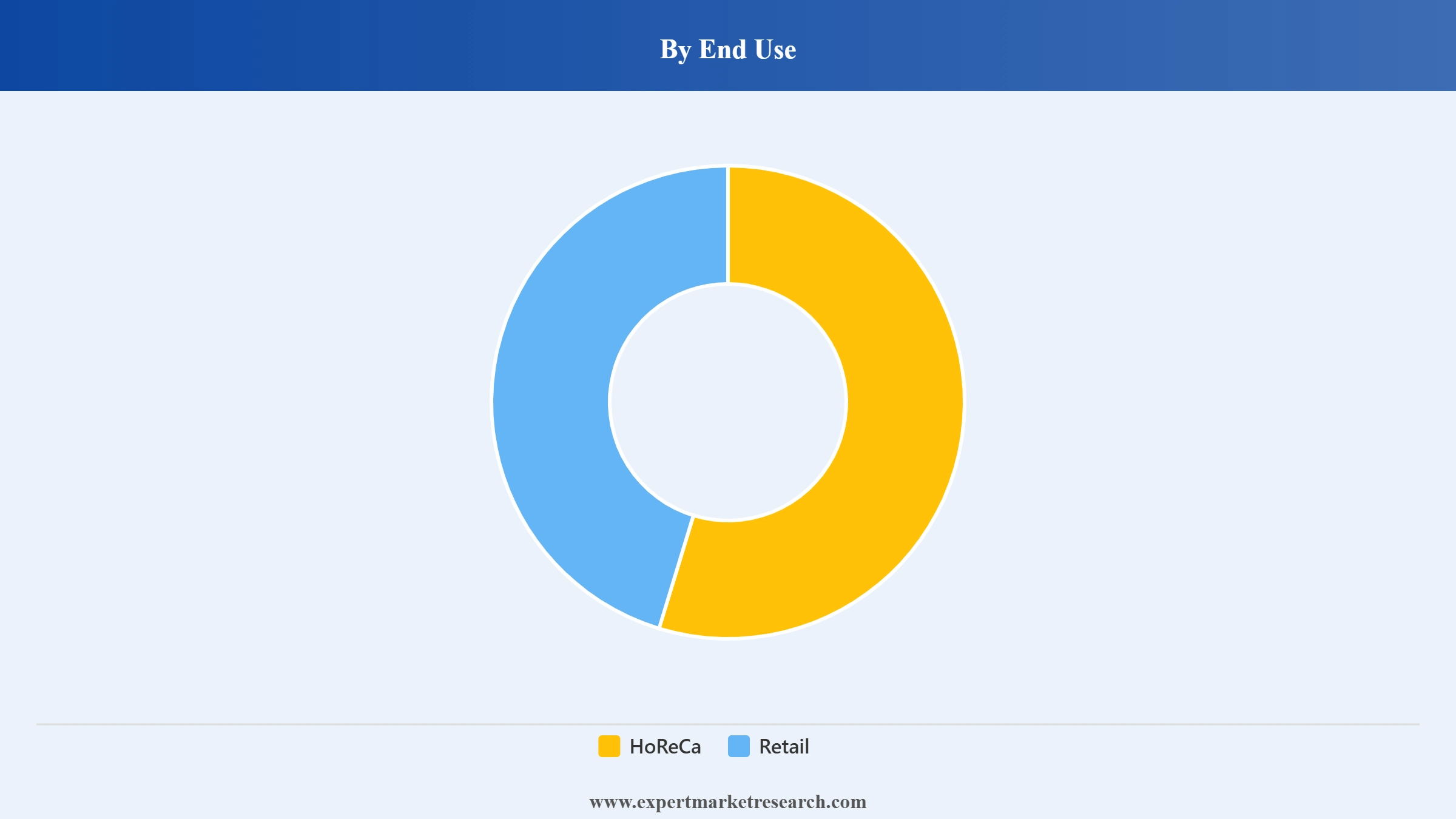

HoReCa is the dominant Singapore coffee market end use, driven by the dominant role of Singapore's large and thriving hotel, restaurant, and café foodservice sector. Cafes in the Central Province of Singapore average around 1,000 customers per day. Singapore's position as Southeast Asia's leading hospitality and meetings, incentives, conferencing, and exhibitions (MICE) hub drives significant HoReCa coffee consumption across hotels, conventions, and premium restaurants.

Recent Development Description 4: Retail is a significant Singapore coffee market end use, driven by the growing consumer preference for home brewing, the availability of premium retail coffee options across Singapore's supermarkets and specialty stores, and the rapid adoption of coffee pods and capsules. Retail coffee purchasing through NTUC FairPrice, Cold Storage, and online platforms is growing as Singapore consumers invest in premium home coffee brewing equipment and premium ground coffee and pod formats.

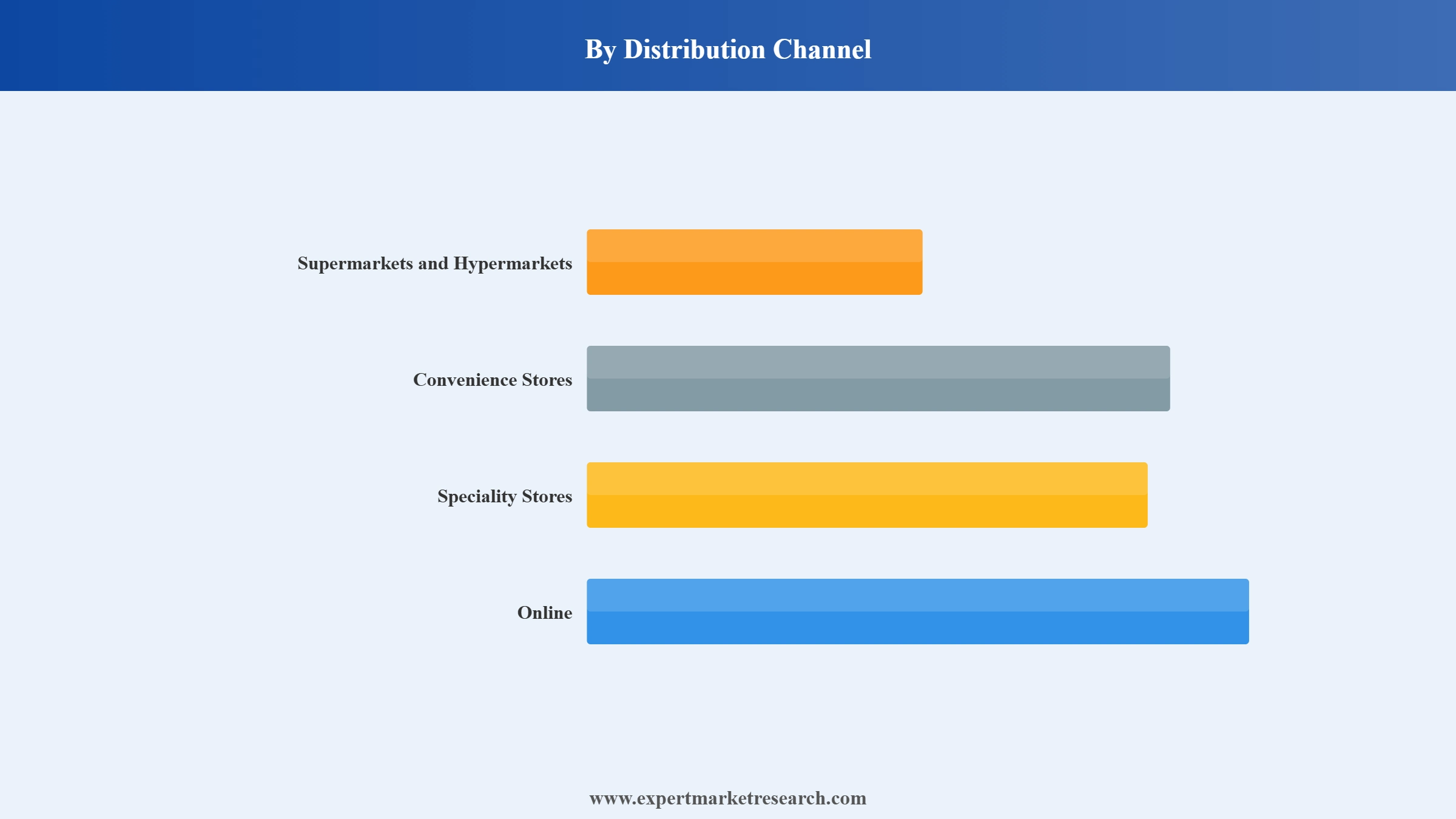

Supermarkets and Hypermarkets are the dominant Singapore coffee market distribution channel, driven by the dominant role of NTUC FairPrice, Cold Storage, Giant, and Sheng Siong as Singapore's primary grocery retailers. These retailers stock a wide range of ground coffee, instant coffee, coffee pods, and whole-bean coffee products from Nestle, Lavazza, Starbucks, and local Singapore brands. Specialty Stores and Online channels are growing through premium and e-commerce coffee adoption.

The "Singapore Coffee Market Report and Forecast 2026-2035" by Expert Market Research offers analysis across the following segments:

Market Breakup by Product Type

Key Insight: Ground Coffee is the dominant Singapore coffee market product type through the specialty café and kopitiam culture. Coffee Pods and Capsules is the fastest-growing type through the growing home coffee brewing convenience trend.

Market Breakup by End Use

Key Insight: HoReCa is the dominant Singapore coffee market end use through the large and growing hotel, restaurant, and café sector. Retail is significant through supermarket and online coffee purchasing.

Market Breakup by Distribution Channel

Key Insight: Supermarkets and Hypermarkets is the dominant Singapore coffee market distribution channel through major grocery retailers. Online is the fastest-growing channel through e-commerce coffee adoption.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Product Type, Ground Coffee is the dominant product type in the Singapore coffee market

Ground Coffee commands the largest Singapore coffee market share by product type, driven by its dominant role in Singapore's specialty cafés, kopitiams, and premium home brewing market. Coffee Pods and Capsules is the fastest-growing type through growing consumer demand for premium, convenient, and consistent single-serve coffee formats. Instant Coffee is a significant type through affordability and convenience. Whole-Bean serves the premium specialty coffee and barista market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By End Use, HoReCa is the dominant end use in the Singapore coffee market

HoReCa commands the largest Singapore coffee market share by end use, driven by Singapore's large hotel, restaurant, café, and kopitiam foodservice sector. Retail is a significant end use through supermarket coffee, home brewing, and specialty store purchases. The growing home brewing trend, driven by coffee pod adoption and premium ground coffee, is expanding the Retail end use segment.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Distribution Channel, Supermarkets and Hypermarkets is the dominant channel in the Singapore coffee market

Supermarkets and Hypermarkets commands the largest Singapore coffee market share by distribution channel through major grocery retailers including NTUC FairPrice, Cold Storage, Giant, and Sheng Siong. Convenience Stores serve ready-to-drink and impulse coffee purchases across Singapore's 7-Eleven and Cheers networks. Speciality Stores and Online are growing through premium and e-commerce coffee adoption.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Singapore coffee market is competitive, with global coffee chains, multinational FMCG companies, and local Singapore coffee brands competing through product quality, premium positioning, café experience, digital loyalty programmes, and distribution reach.

Nestle S.A. is a Switzerland-based global FMCG company with a dominant Singapore coffee market presence through its Nescafe instant coffee, Nespresso coffee pods, and Starbucks retail coffee licensing brands. Nestle serves Singapore's retail coffee segment with its Nescafe Classic, Nescafe Gold Blend, and Nespresso capsule product ranges. Nestle's Nescafe brand is one of the most widely consumed instant coffee brands across Singapore's household and office coffee segments.

Starbucks Corp. is a US-based global coffee chain with a dominant Singapore coffee market presence through its premium café chain operations. Starbucks operates an extensive Singapore café network and serves Singapore consumers with its signature espresso beverages, cold brew, frappuccino, and premium whole-bean and ground coffee retail products. Starbucks globally reported its first same-store sales growth in two years, with a 4% increase in North America in 2025, reflecting the impact of CEO Brian Niccol's turnaround strategy.

Inspire Brands Inc. is a US-based multi-brand restaurant company with a significant Singapore coffee market presence through its Dunkin' brand. Dunkin' (owned by Inspire Brands) serves Singapore consumers with affordable coffee beverages, espresso drinks, and packaged retail coffee products. Inspire Brands operates across multiple food and beverage brands globally, with Dunkin' serving Singapore's growing demand for accessible and value-priced coffee beverages.

LUIGI LAVAZZA S.p.A is an Italy-based premium coffee company with a significant Singapore coffee market presence through its premium ground coffee, coffee pods, and espresso blend product portfolio. Lavazza serves Singapore's growing premium retail and HoReCa coffee segments with its Qualita Oro, Gran Selezione, and Lavazza espresso capsule ranges. The company's premium Italian coffee heritage and product quality position it as a key premium coffee brand in Singapore's competitive coffee market.

Other key players include Perk Coffee Pte Ltd., among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Our full report for 2026-2035 delivers the market data, competitive intelligence, and strategic analysis to capture Singapore's growing coffee market.

Singapore Coffee Subscription Market Insights

Singapore RTD Coffee Beverage Market Trends

Singapore Coffee Supply Chain And Sourcing Trends

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market is estimated to grow at a CAGR of 8.20% between 2026 and 2035.

The market is being driven due to surge in coffee consumption, the rising popularity of instant coffee, and the growing establishment of coffee shops.

The key trends aiding the market include technological advancements and the emergence of smart coffee machines, strategic initiatives by market players, and the incorporation of sustainable and ethical practices in coffee production.

Based on product type, market segmentations include whole-bean, ground coffee, instant coffee, and coffee pods and capsules, among others.

Different end uses are HoReCa and retail.

The major players in the market are Nestle S.A., Starbucks Corp.¸Inspire Brands Inc., LUIGI LAVAZZA S.p.A, and Perk Coffee Pte Ltd., among others.

In 2025, the market attained a value of nearly USD 31.91 Million.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach about USD 70.18 Million by 2035.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by End Use |

|

| Breakup by Distribution Channel |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.