Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

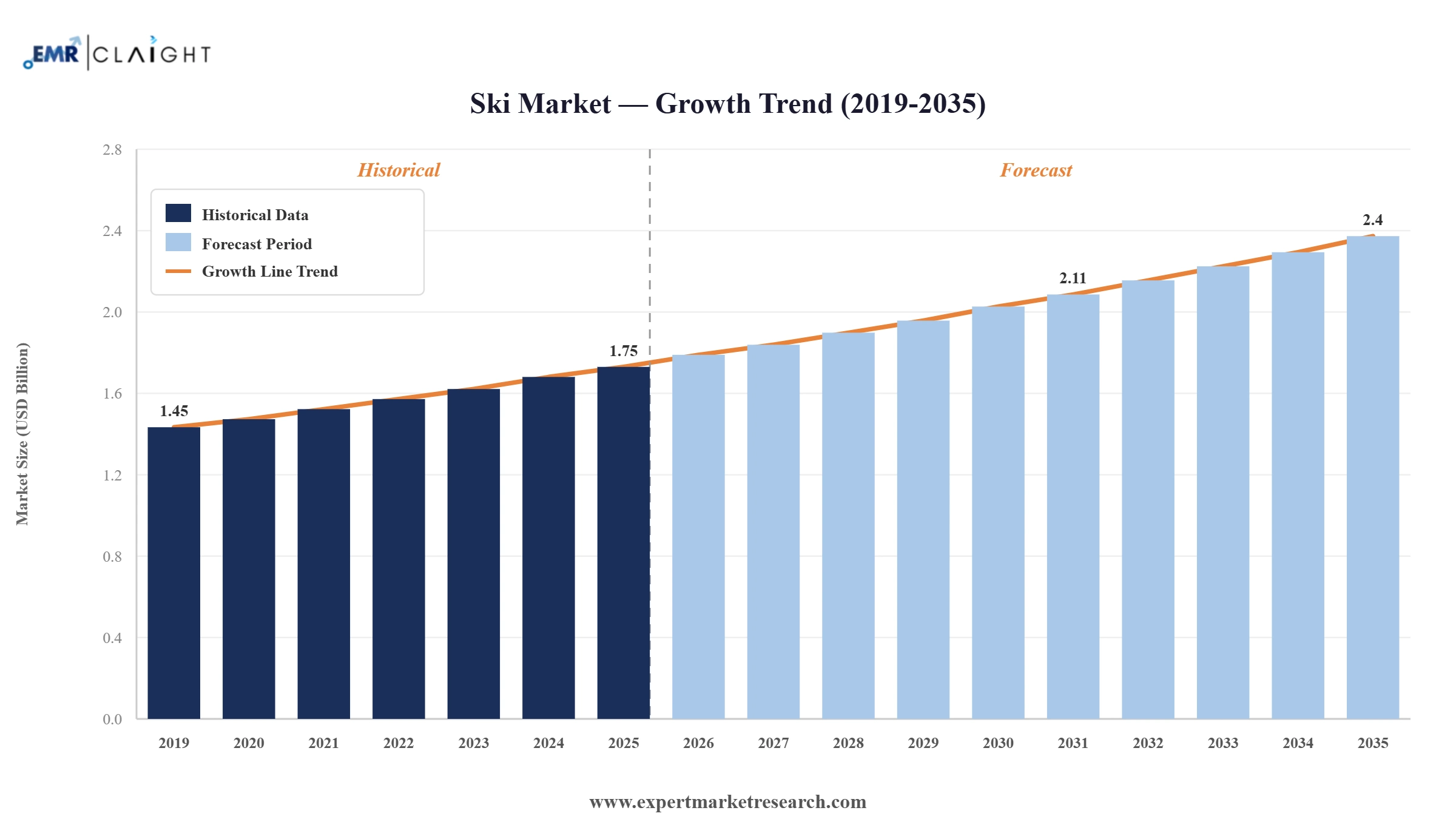

The global ski market reached a value of USD 1.75 Billion at 2025 and is projected to expand at a CAGR of around 3.20% during the forecast period of 2026-2035. With the expanding participation in winter sports globally following the legacy of the 2022 Beijing Winter Olympics, the continuous advancement of lightweight and high-performance ski equipment materials, the rapid growth of indoor ski infrastructure in non-traditional markets across the Middle East and Southeast Asia, and rising disposable income and aspirational winter tourism activity in Asia Pacific and Latin America, the market is expected to reach USD 2.40 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global ski market is being reshaped by the intersection of technological product innovation, geographic expansion into non-traditional ski markets, and growing aspiration-driven participation from emerging market consumers. Established European and North American brands are investing in lighter materials, smarter designs, and sustainable manufacturing, while Asia Pacific's rapid infrastructure investment is fundamentally broadening the market's consumer base. These combined dynamics are driving both volume and value growth across product and distribution segments through the forecast period.

Skis Rossignol SAS introduced a new premium carbon-reinforced ski line in March 2025, targeting advanced and expert recreational skiers seeking enhanced energy transfer and reduced vibration. The launch expands Rossignol's high-performance product tier and strengthens its competitive position in the premium segment of the ski market across European and North American resort retail channels.

Amer Sports Corporation extended the Salomon alpine ski range into expanded Asian retail distribution in November 2024, capitalising on accelerating ski participation growth in China and South Korea. The initiative includes dedicated product lines designed for beginner to intermediate skiers, aligned with the demographic profile of Asia Pacific's rapidly growing first-time ski consumer base.

Fischer Sports GmbH unveiled a multi-year sustainable manufacturing initiative in July 2024, targeting a significant reduction in production waste and introducing bio-based resin components across its alpine ski lines. The programme signals the brand's commitment to environmentally responsible production and positions Fischer at the forefront of sustainability within the competitive global ski equipment industry.

Black Diamond Equipment, Ltd introduced an expanded ski touring boot collection in February 2024, addressing growing consumer interest in backcountry and off-piste skiing globally. The range targets the fast-growing ski touring segment with a focus on uphill efficiency and downhill performance, broadening Black Diamond's product coverage within the global ski boots and accessories category.

China's significant investment in ski resort infrastructure following the 2022 Beijing Winter Olympics is sustaining robust Asia Pacific ski market growth. Resorts in Zhangjiakou and Chongli have continued to expand lift capacity and beginner slopes through 2024, converting the Olympic legacy into long-term retail demand for ski equipment at all price points.

Advances in carbon fibre and bio-composite materials are elevating ski market performance standards across product categories. Rossignol and Fischer both introduced lighter-weight ski constructions in 2024, reducing equipment weight while maintaining structural rigidity, improving the appeal of high-performance skiing for a wider range of recreational consumers globally.

The expansion of indoor ski facilities across the Middle East and Southeast Asia is creating sustainable year-round demand for ski equipment in non-alpine geographies. Ski Dubai and ski Egypt have continued to generate consistent equipment retail and rental volumes through 2024, demonstrating how indoor venues convert warm-climate consumers into active ski market participants.

Ski touring and backcountry skiing are among the fastest-growing sub-categories in the ski market, driven by growing consumer preference for mountain access beyond groomed pistes. Brands including Black Diamond and Fischer have significantly expanded their ski touring product ranges in 2024, capturing demand from experienced skiers seeking versatility and off-resort adventure experiences.

Environmental responsibility is becoming a meaningful competitive differentiator in the global ski industry. Fischer Sports' 2024 sustainability programme and Rossignol's use of partially recycled base materials reflect a broader industry movement toward reducing the carbon footprint of ski equipment production, responding to growing consumer and regulatory pressure for sustainable outdoor sports goods manufacturing.

The report of Expert Market Research's titled "Ski Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

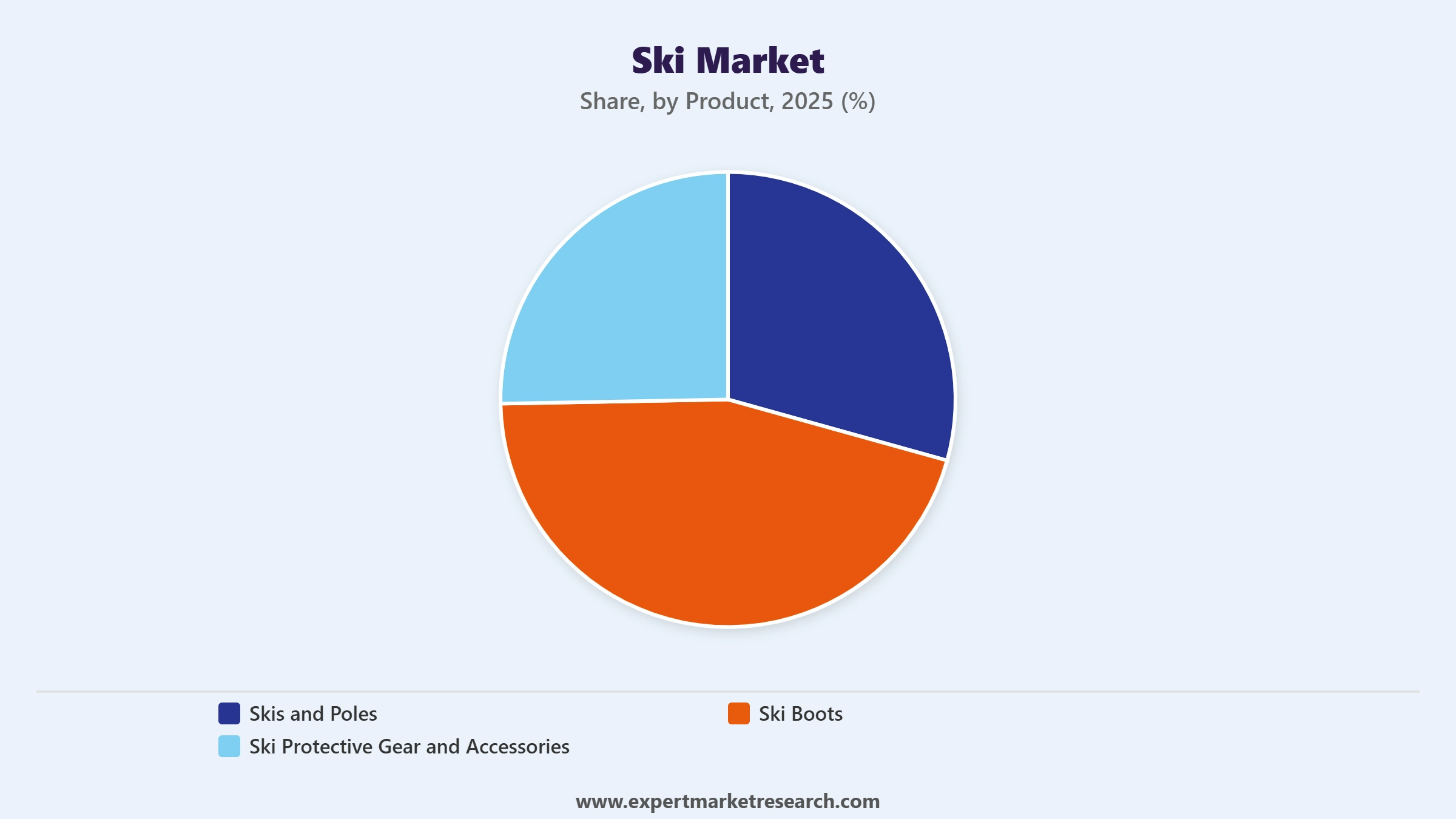

Market Breakup by Product

Key Insight: Skis and poles represent the dominant product category in the ski market, accounting for the largest revenue share across both recreational and professional segments. Continuous innovation in carbon fibre, titanium reinforcement, and rocker profile technology has sustained premium price points and strong consumer replacement cycles. Ski boots are the second-largest product category, providing significant revenue per unit due to the critical importance of precise fit. Ski protective gear and accessories, including helmets, goggles, and gloves, represent a high-growth segment supported by increasing safety regulation at resorts and growing consumer awareness of protective equipment standards.

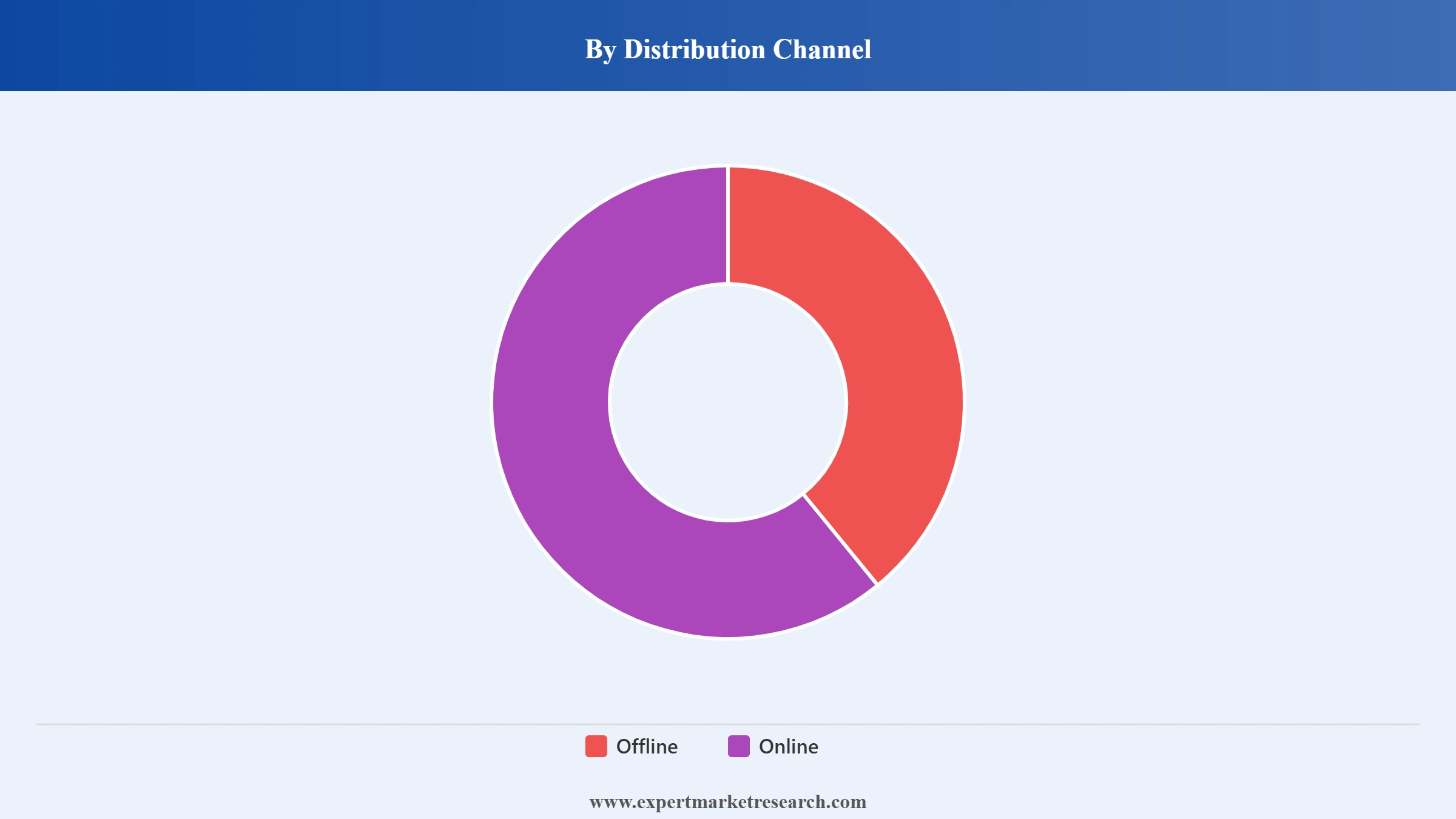

Market Breakup by Distribution Channel

Key Insight: Offline retail holds the dominant share of ski market distribution, reflecting the product-specific need for expert fitting, boot customisation services, and equipment testing that physical retail and resort-based shops provide. Speciality ski stores and resort rental operations are critical touchpoints where consumers make high-consideration purchases for boots and skis. Online channels are growing at a faster rate, driven by the availability of detailed product specifications, consumer review ecosystems, and competitive pricing from direct-to-consumer and speciality e-commerce platforms. Seasonal purchasing behaviour and the growing confidence of experienced skiers buying online are steadily increasing the digital channel's share of total ski market revenue.

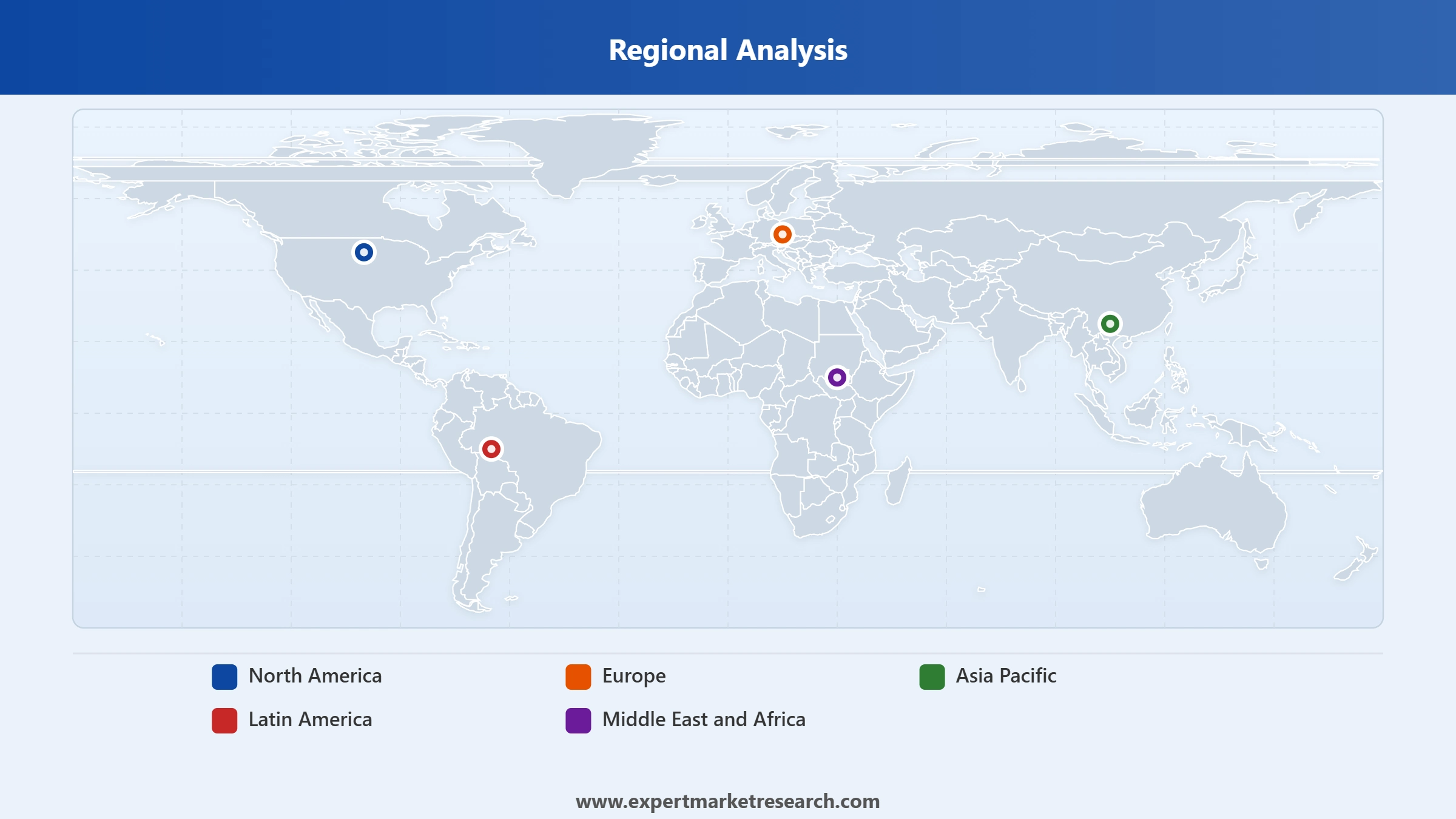

Market Breakup by Region

Key Insight: Europe holds the dominant regional share of the ski market, anchored by the Alps region spanning France, Austria, Switzerland, and Italy, which collectively represent the world's most visited ski destination cluster. The region's deeply established ski culture, high per-capita equipment spend, and the headquarters presence of major brands including Rossignol, Fischer, and Atomic sustain consistent demand. North America is the second-largest market, driven by the United States and Canada's mature resort infrastructure. Asia Pacific is the fastest-growing region, powered by China's post-Olympic ski infrastructure build-out and rising participation in Japan, South Korea, and Australia. Latin America and the Middle East and Africa represent early-stage but growing markets supported by indoor ski venues and expanding high-altitude resort development.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Product, skis and poles dominate the market due to their position as the core equipment category and continuous premium product innovation driving strong replacement demand

Skis and poles account for the largest share of the ski market by product, underpinned by their status as the fundamental equipment purchase for every alpine and touring skier. High replacement frequency among performance-focused recreational skiers, combined with strong aspirational demand for premium all-mountain and race-oriented models from brands such as Rossignol, Fischer, and Atomic, sustains consistent revenue generation across this segment. The diversification of ski types, including carving, powder, touring, and park variants, expands the category's addressable market by targeting distinct skiing styles and consumer segments.

Ski boots represent a high-value product segment within the ski market, where consumers prioritise precision fit, energy transfer efficiency, and thermal performance. Boot technology investment by brands including Apex Ski Boots and established players such as Salomon and Tecnica continues to drive replacement cycles among experienced skiers. Ski protective gear and accessories are the fastest-growing product category, fuelled by mandatory helmet policies introduced at major resorts across Europe and North America in recent years, which have significantly expanded the addressable market for safety-oriented ski equipment beyond casual consumer choice.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Distribution Channel, offline retail accounts for the dominant share of the market due to the high-consideration nature of ski equipment purchases and the critical importance of expert fitting services

Offline channels hold the dominant distribution share in the ski market, driven by the inherently tactile and expertise-dependent nature of ski equipment purchase decisions. Ski boots, in particular, require professional fitting and shell modification services that physical retail and resort shop environments uniquely provide. Speciality ski retailers located in alpine resort towns operate as year-round consumer touchpoints and serve as experiential brand showrooms for leading manufacturers. Resort-based rental services also feed offline equipment sales, as first-time and developing skiers transitioning from rental to owned equipment typically do so through in-store consultation with trained retail staff.

Online channels are the fastest-growing distribution mode in the ski market, benefiting from the growing confidence of experienced skiers purchasing replacement skis and accessories without physical fitting. Direct-to-consumer platforms operated by Rossignol, Fischer, and Helly Hansen have expanded their digital retail capabilities significantly in recent years. The online channel is particularly effective for ski clothing, protective accessories, and poles, where size standardisation reduces the fitting complexity that constrains boot and ski purchases. Seasonal sale periods and bundle promotions through digital channels are attracting value-conscious consumers who previously relied exclusively on physical retail for ski equipment purchases.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Europe dominates the market due to the highest concentration of alpine ski infrastructure, deeply embedded ski culture, and headquarters presence of major global ski equipment brands

Europe holds the largest regional share of the ski market, anchored by the Alps region which encompasses the world's most visited and commercially developed ski destination cluster across France, Austria, Switzerland, and Italy. France's Les Trois Vallees and Austria's Ski Arlberg collectively attract tens of millions of skier visits annually, creating sustained and predictable demand for ski equipment retail and rental across all product categories. The headquarters presence of Skis Rossignol SAS in France and Fischer Sports GmbH in Austria creates a tight brand-market alignment that reinforces European consumer loyalty to domestically produced premium ski equipment.

Asia Pacific is the fastest-growing regional market in global skiing, with China at the forefront of expansion. Government-led investment in winter sports following the 2022 Beijing Winter Olympics has resulted in over 800 ski resorts operating across China, with major facilities in Zhangjiakou, Chongli, and Harbin continuing to expand through 2024. Amer Sports and Rossignol both announced dedicated Asia Pacific distribution expansion initiatives in 2024, recognising the region's growing contribution to ski market growth. Japan and South Korea add further depth to the Asia Pacific ski market with well-established resort ecosystems and strong domestic demand for high-performance ski equipment across both alpine and touring disciplines.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The ski market is moderately consolidated, with a small group of European and North American brands accounting for the majority of premium equipment revenue. Skis Rossignol SAS, Fischer Sports GmbH, and the Amer Sports portfolio (which includes Salomon and Atomic) dominate the alpine ski segment through continuous product innovation, strong resort retail relationships, and athlete endorsement programmes. Black Diamond Equipment occupies a leading position in the ski touring and backcountry segment, which has emerged as one of the market's highest-growth product niches.

The competitive environment is increasingly shaped by sustainability positioning, geographic expansion into Asia Pacific, and product category diversification into touring and protective gear. Brands investing in lightweight material technology and eco-friendly manufacturing are gaining differentiation in premium consumer segments across Europe and North America. Smaller specialist brands including Icelantic LLC and Apex Ski Boots compete through niche product excellence, targeting experienced skiers willing to pay a premium for category-specific performance. The growing role of direct-to-consumer digital channels is gradually shifting competitive dynamics, enabling both established and emerging brands to engage consumers without traditional distribution intermediaries.

Founded in 1924 and headquartered in Ried im Innkreis, Austria, Fischer Sports GmbH is one of the world's leading ski manufacturers, producing alpine, Nordic, and ski touring equipment. The company operates its own research and development centre and manufacturing facilities in Austria and Ukraine, supplying premium ski products to recreational and professional markets globally. Fischer is known for its technical precision, consistent innovation in ski construction, and long-standing partnerships with national ski teams and World Cup racing programmes across Europe and North America.

Founded in 1957 and headquartered in Salt Lake City, Utah, United States, Black Diamond Equipment, Ltd is a leading manufacturer of skiing, climbing, and mountain sports equipment. The company specialises in ski poles, ski touring boots, and backcountry skiing gear, holding a strong position in the fast-growing ski touring and off-piste segments. Black Diamond's product development is anchored in the outdoor athlete community, and its technical innovation in lightweight alpine touring equipment has earned it strong brand loyalty among backcountry and freeride skiing consumers globally.

Founded in 1950 and headquartered in Helsinki, Finland, Amer Sports Corporation is one of the world's largest sporting goods companies, managing a portfolio of premium brands that includes Salomon, Atomic, Arc'teryx, and Wilson. In the ski segment, Salomon and Atomic are among the most commercially significant alpine ski brands globally, competing across recreational, racing, and freestyle categories. Amer Sports' scale, multi-brand strategy, and global distribution infrastructure give it unmatched market reach across all major ski regions, from the European Alps to North America and Asia Pacific.

Founded in 1907 and headquartered in Saint-Jean-de-Moirans, France, Skis Rossignol SAS is one of the oldest and most recognised ski manufacturers in the world. The company produces a full range of alpine skis, ski boots, bindings, poles, and ski apparel under the Rossignol and Dynastar brand names. Rossignol has a strong competitive presence in the European market and maintains global reach through an extensive resort retail distribution network. The brand's deep roots in French Alpine culture and its sustained investment in World Cup racing programmes reinforce its premium positioning across both professional and recreational ski segments.

Other key players in the market are United States Ski Pole Company, Fatcan Ski Poles, Apex Ski Boots, Icelantic LLC, Demon United, Helly Hansen AS, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Stay ahead in the ski market 2026 with our comprehensive research report. From product innovation trends and regional growth dynamics to distribution channel evolution and competitive brand strategies, this report gives you the intelligence to make well-informed decisions. Whether you are expanding a ski equipment line, evaluating market entry into Asia Pacific, or assessing your competitive positioning in established European and North American resort markets, download your free sample today and unlock the key opportunities shaping the future of global skiing.

Japan Ski Market

Italy Ski Market

Canada Ski Market

Europe Ski Market

Ski Manufacturing Supply Chain And Component Sourcing

Ski Resort Infrastructure And Rental Systems

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

At 2025, the market reached an approximate value of USD 1.75 Billion.

The market is projected to grow at a CAGR of 3.20% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach USD 2.40 Billion by 2035.

The major drivers of the ski market include the growing numbers of initiatives to increase skiing participation, increasing number of people pursuing skiing as a recreational activity, and introduction of new products and technologies for skiing safety.

The increasing customer preference for snow-related activities and tourism activities and surging number of ski resorts are the key trends propelling the growth of the market.

By product into skis and poles, ski boots, and ski protective gear and accessories; by distribution channel into offline and online; and by region across North America, Europe, Asia Pacific, Latin America, and Middle East and Africa with country-level data for 17 individual markets.

The primary distribution channels in the market are offline and online.

The key players include Fischer Sports GmbH, Black Diamond Equipment, Ltd, Amer Sports Corporation, Skis Rossignol SAS, United States Ski Pole Company, Fatcan Ski Poles, Apex Ski Boots, Icelantic LLC, Demon United, Helly Hansen AS, and Others.

Powder skis, freestyle skis, snowblades, carving skis, racing skis, freeride skis, and big mountain skis are some of the different types of skis.

The average skier replaces their skis every 8 years.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.