Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

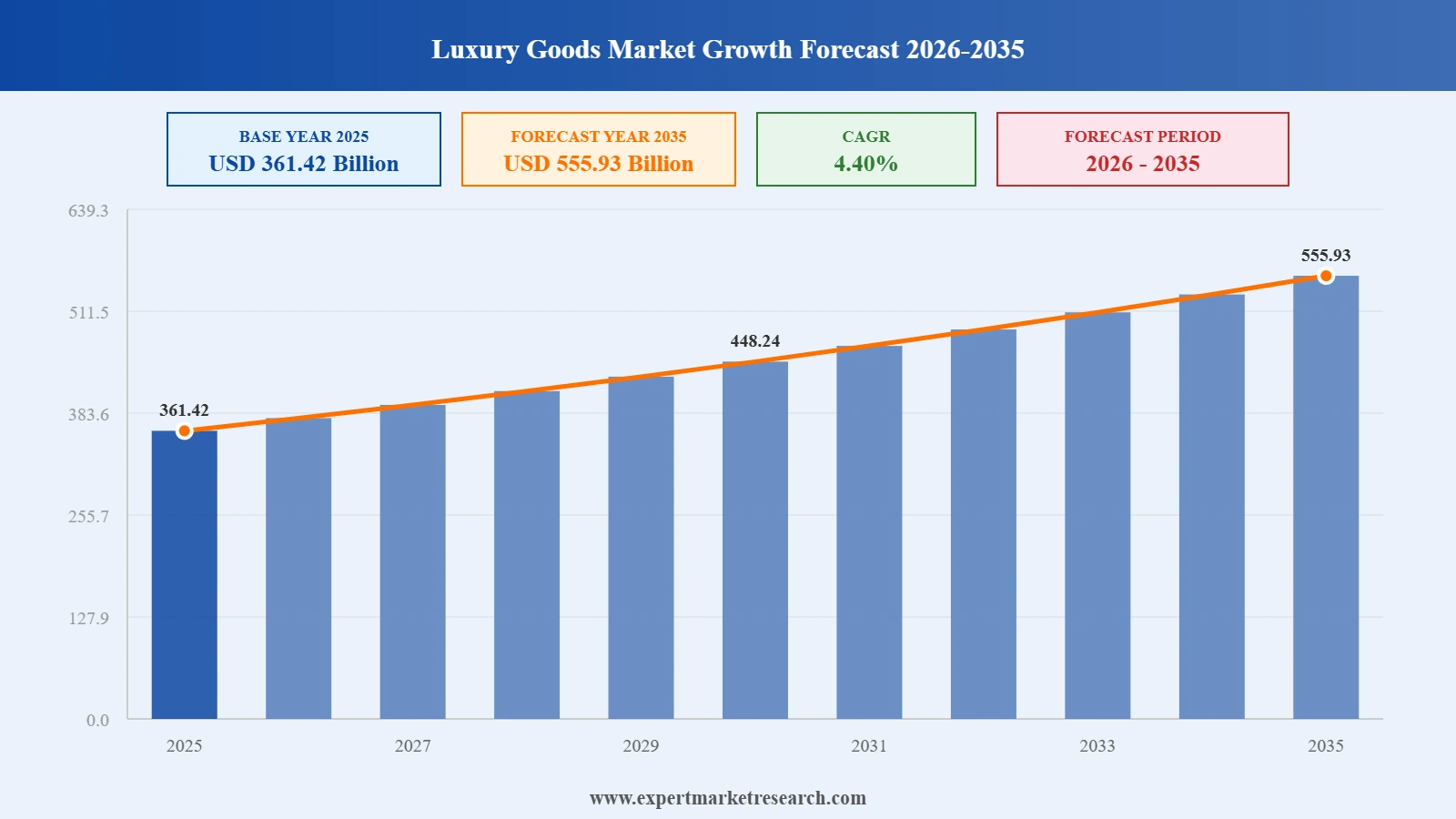

The global luxury goods market reached a value of USD 361.42 Billion at 2025 and is projected to expand at a CAGR of around 4.40% during the forecast period of 2026-2035 and expected to reach USD 555.93 Billion by 2035. With rising global HNWI population expanding the addressable buyer base, accelerating adoption of digital commerce and omnichannel brand experiences, strong aspirational demand from millennials and Generation Z driving generational renewal, and strategic brand entry into high-growth markets including India and Southeast Asia.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global luxury goods market is navigating a complex transition shaped by generational demand shifts, digital channel maturation, and strategic geographic expansion into new high-growth markets. Conglomerates including LVMH and Kering continue to lead through diversified brand portfolios and operational resilience, while independent heritage houses like Hermès defend their exclusive positioning through supply chain mastery and controlled scarcity. Sustainability credentials, digital product passports, and AI-driven personalisation are emerging as competitive differentiators beyond traditional craftsmanship and heritage narratives.

In April 2026, Kering announced a strategic partnership with ICCF, acquiring a minority stake to combine complementary strengths across the luxury industry. The collaboration signals Kering's strategy of deepening its multi-brand ecosystem through selective strategic investments, reinforcing its position alongside LVMH as one of the two dominant conglomerates shaping the global luxury goods market.

In June 2025, Hermès launched a new line of luxury leather goods incorporating recycled materials and innovative sustainable production techniques. The range demonstrated Hermès's commitment to evolving its artisan heritage toward responsible luxury, positioning sustainability as a core brand attribute rather than a compromise on the quality that defines the global luxury goods market.

In May 2025, Prada announced the acquisition of a boutique jewellery brand to accelerate its expansion into the high-jewellery segment and diversify its product portfolio beyond leather goods and apparel. The move reflects the growing strategic priority of watches and jewellery as the highest-margin and fastest-growing product type in the global luxury goods market.

In April 2025, Rolex launched new GMT-Master II, Oyster Perpetual, and other models born from its philosophy of perpetual movement and horological mastery. The launches reinforced Rolex's position as the world's most recognised luxury watch brand and sustained secondary market desirability, supporting the premium pricing architecture that defines watches in the global luxury goods market.

Approximately 60% of luxury purchases are now influenced by online experiences, and digital channels are expected to account for over 15% of total global luxury goods market revenue in 2026. Luxury brands including Chanel, Louis Vuitton, and Hermès have invested in immersive e-boutiques, virtual try-on, and AI-driven personalisation to maintain exclusivity while extending digital accessibility.

Millennials and Generation Z are the leading consumer growth cohorts in the global luxury goods market, collectively driving demand for brand authenticity, sustainability credentials, and digital engagement. These demographics favour heritage narrative and limited-edition exclusivity, sustaining strong secondary market activity on platforms like StockX and Vestiaire Collective alongside primary brand purchases.

Louis Vuitton, Dior, Cartier, and Chanel all accelerated their India expansion strategies in 2025 and 2026, opening flagship boutiques in Delhi, Mumbai, and Bengaluru. India's rapidly growing HNWI population and young, brand-conscious affluent consumer base are positioning the country as the next structurally significant demand engine for the global luxury goods market after China.

The EU's Corporate Sustainability Reporting Directive and upcoming digital product passports are compelling luxury brands to document supply chain provenance, material sourcing, and carbon footprint. Brands that embed sustainability into their luxury narrative including Hermès with its recycled leather lines are converting regulatory compliance into brand equity within the global luxury goods market.

Watches and jewellery represent the largest segment by revenue in the global luxury goods market, with Rolex, Patek Philippe, and Cartier timepieces increasingly purchased as investment-grade assets. Collector markets and auction platforms are sustaining premium secondary pricing, and entry of financial investors into high-jewellery funds reflects the asset-class normalisation of luxury goods.

The report by Expert Market Research's titled "Global Luxury Goods Market Report and Forecast 2026-2035", offers a detailed analysis of the market based on the following segments:

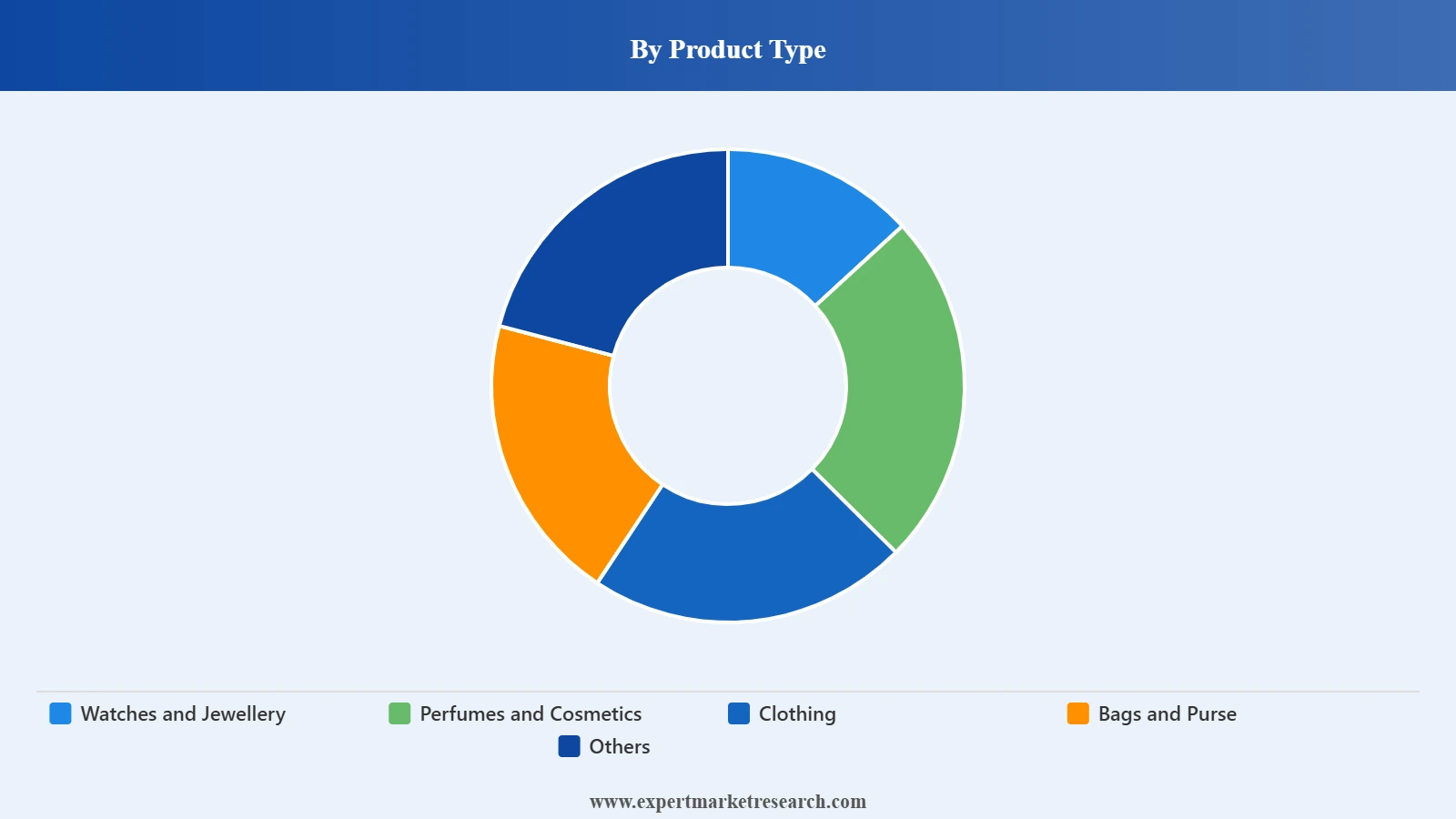

Market Breakup by Product Type

Key Insight: Watches and jewellery command the largest revenue share in the global luxury goods market, valued at approximately USD 165 billion in 2026, underpinned by the dual role of luxury timepieces as both lifestyle items and investment assets. Bags and purses from heritage houses including Louis Vuitton, Chanel, and Hermès are the most recognisable luxury status symbols globally. Perfumes and cosmetics provide broader accessibility entry points into luxury brands. Clothing anchors the seasonal fashion cycle that drives editorial attention and retail traffic for conglomerates.

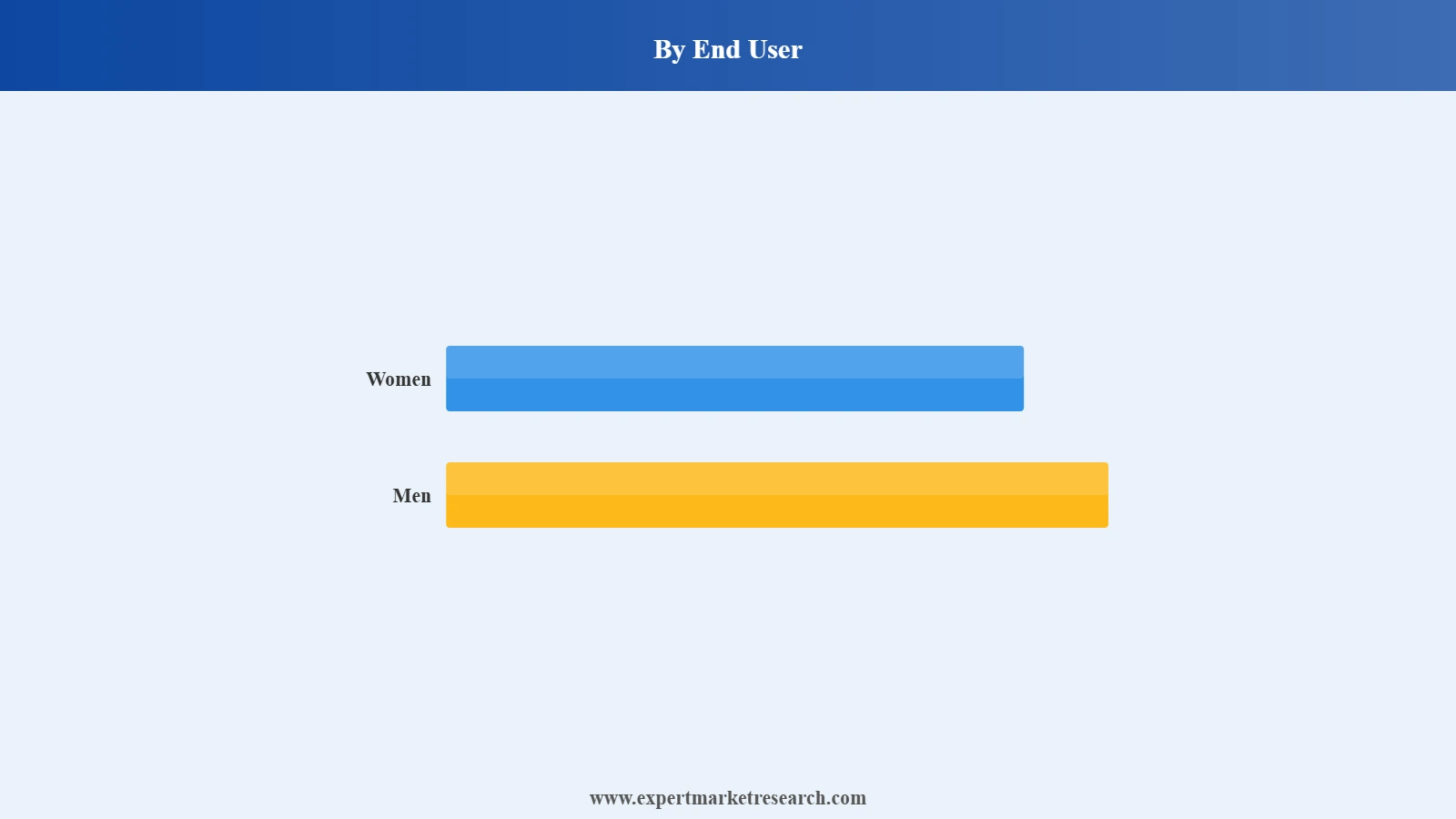

Market Breakup by End User

Key Insight: Women account for approximately 55% of global luxury goods revenues, driven by their broader product participation spanning handbags, cosmetics, jewellery, apparel, and fragrances. Brands including Chanel, Dior, and Hermès have historically centred their brand identity on female luxury consumers. The male segment is a fast-growing opportunity, driven by rising men's wear demand, luxury watch collecting culture, and growing interest in leather goods and grooming-adjacent luxury categories.

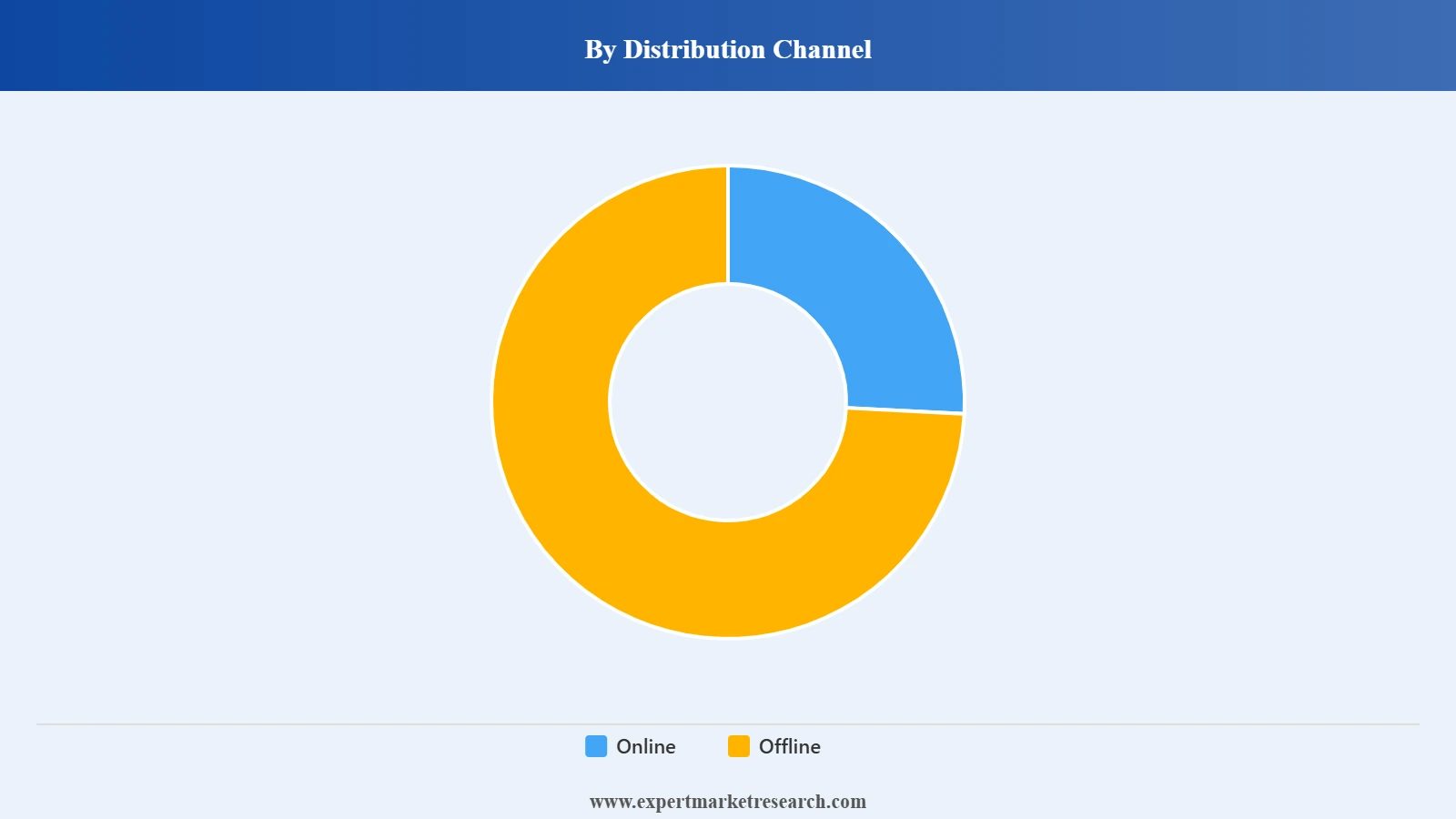

Market Breakup by Distribution Channel

Key Insight: Offline channels including mono-brand boutiques, department stores, and airports hold the dominant share of the global luxury goods market, as in-store brand experience, personal styling service, and tactile product engagement remain central to the luxury purchasing ritual. Online is the fastest-growing channel, with digital boutiques and luxury e-commerce platforms expected to account for over 15% of revenues in 2026. Brands are integrating virtual consultations and personalised digital gifting to extend luxury experiences into digital environments.

Market Breakup by Region

Key Insight: Europe holds approximately 52% of global luxury goods revenues in 2025, anchored by its unrivalled concentration of heritage luxury houses including LVMH, Kering, Hermès, Richemont, Chanel, and Prada. Asia Pacific is the fastest-growing region, with Chinese consumers accounting for approximately 22 to 24% of global luxury purchases by nationality and India emerging as the next high-growth frontier. North America leads in per-capita luxury spending, and the Middle East is a high-growth market supported by Gulf wealth and luxury tourism.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By product type, watches and jewellery dominate the market due to investment-grade asset appeal and strong heritage brand positioning

Watches and jewellery hold the largest product share in the global luxury goods market, valued at approximately USD 165 billion in 2026, driven by the dual role of luxury timepieces as lifestyle items and investment-grade assets. Rolex, Patek Philippe, and Cartier command strong secondary market premiums, sustaining primary retail pricing and brand desirability across generations. The jewellery sub-category benefits from rising demand for high-jewellery from aspiring affluent consumers in Asia and the Middle East.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Bags and purses are the highest-profile product category for luxury conglomerates by media coverage and brand recognition, with Chanel's classic flap, Hermes's Birkin, and Louis Vuitton's Neverfull among the most coveted items globally. In May 2025, Prada acquired a boutique jewellery brand specifically to access the high-jewellery adjacency of this trend. Perfumes and cosmetics provide volume and accessibility that sustain brand engagement among aspirational consumers who cannot yet afford core luxury categories.

By end user, women account for the dominant share of the market due to broader product category participation and higher brand engagement

Women generate the larger share of revenue in the global luxury goods market, with higher participation across handbags, cosmetics, jewellery, apparel, and fragrances creating a broader spending footprint per consumer than the male segment. Leading brands including Chanel, Dior, and Hermès have built their identity, editorial presence, and flagship product lines around female consumers. Increasing financial independence among women in developing economies is expanding the female luxury buyer base into new geographies.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The male luxury consumer segment is growing as men's fashion, luxury watch collecting, and leather goods become culturally normalised markers of aspiration. In April 2025, Rolex's new GMT-Master II and Oyster Perpetual launches reinforced the brand's appeal to male collectors globally. Men's wear and luxury grooming categories are attracting increasing brand investment from houses including Giorgio Armani and Ralph Lauren, broadening the male consumer base in the global luxury goods market.

By distribution channel, offline retail accounts for the dominant share of the market due to brand experience immersion and product authenticity assurance

Offline channels command the dominant share of the global luxury goods market, as mono-brand boutiques, department store concessions, and airport duty-free retail deliver the in-person brand experience that defines luxury purchasing. Physical stores enable personalised styling consultations, exclusive product previews, and the tactile quality assessment that justifies premium pricing. Heritage brands including Hermès maintain deliberate physical retail scarcity to preserve brand exclusivity.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Online is the fastest-growing channel, forecast to account for over 15% of revenues in 2026, driven by digital boutiques, personalised e-commerce experiences, and luxury resale platforms. In 2025, Gucci announced a strategic partnership with a leading technology platform to co-create an immersive luxury retail experience and digital ecosystem, reflecting how heritage brands are investing to capture the digitally native Gen Z luxury consumer within the global luxury goods market.

Europe dominates the market due to unrivalled concentration of heritage luxury conglomerates and high tourist-driven luxury spending

Europe commands approximately 52% of global luxury goods revenues in 2025, anchored by France and Italy's extraordinary density of heritage luxury houses. LVMH, Kering, Richemont, Chanel, Hermès, Prada, and Valentino all operate from European headquarters, and the continent's luxury tourism ecosystem generates additional demand from international shoppers. France alone accounts for approximately 20% of the global luxury market, with Paris serving as the world's pre-eminent luxury retail and fashion destination.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific is the fastest-growing region, projected to expand at a CAGR of approximately 5.4% through the forecast period, significantly above the global average. China's consumer base remains the dominant growth driver, while India is emerging as the next high-growth frontier with LVMH, Dior, Cartier, and Chanel all accelerating India expansion in 2025 and 2026. Japan and South Korea sustain high per-capita luxury spending, and Southeast Asian markets are becoming more active as regional HNWI populations grow in the global luxury goods market.

The global luxury goods market is highly concentrated at the conglomerate level, with LVMH, Kering, and Richemont collectively controlling a significant share of global luxury revenues across fashion, leather goods, watches, jewellery, cosmetics, and spirits. Independent heritage houses including Chanel, Hermès, and Rolex compete through scarcity, brand autonomy, and operational mastery rather than conglomerate scale.

Competition increasingly turns on brand equity defence, generational consumer transition management, sustainability narrative, and digital channel development. The luxury market's moderate growth trajectory through 2035 means share shifts are more consequential than absolute market expansion, making portfolio management, creative direction quality, and geographic market entry timing the decisive competitive variables in the global luxury goods market.

Privately held and headquartered in Paris, Chanel Limited is one of the world's most valuable independent luxury houses, renowned for its classic flap handbag, No. 5 fragrance, and haute couture heritage. Chanel's independence from public markets allows disciplined investment in brand equity and product scarcity. Its entry into India's luxury market and sustained digital investment position it for continued growth in the global luxury goods market.

Founded in 1963 and headquartered in Paris, Kering is a global luxury conglomerate housing Gucci, Saint Laurent, Bottega Veneta, Balenciaga, Alexander McQueen, Brioni, and Pomellato. In April 2026, Kering announced a strategic partnership and minority stake acquisition in ICCF to combine complementary luxury industry strengths. Gucci's brand evolution and Kering's sustainability leadership programme are key strategic pillars in the global luxury goods market.

Founded in 1905 and headquartered in Geneva, Switzerland, Rolex is the world's most recognised luxury watch brand. In April 2025, Rolex launched its new GMT-Master II, Oyster Perpetual, and companion models, maintaining the perpetual calendar of new releases that sustains collector demand and secondary market premiums. Rolex's status as both a luxury lifestyle symbol and an investment-grade asset anchors the watches and jewellery segment leadership in the global luxury goods market.

Founded in 1837 and headquartered in Paris, Hermès International is one of the world's most prestigious independent luxury houses, built on supply-chain mastery, artisan craftsmanship, and deliberate scarcity. In June 2025, Hermès launched a new luxury leather goods line incorporating recycled materials, demonstrating its evolution toward sustainable luxury. Its Birkin and Kelly bags command the highest secondary market premiums in the global luxury goods market.

Other key players in the market are Giorgio Armani S.p.A., Ralph Lauren Corporation, Compagnie Financiere Richemont SA, Prada SpA, VALENTINO S.p.A., Tiffany and Co., Estee Lauder Companies Inc., Cartier International AG, Capri Holdings Limited, LVMH Moet Hennessy Louis Vuitton SE, Burberry Group plc, L'Oreal Group, Shiseido Company Limited, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Access comprehensive intelligence on the global luxury goods market with our latest forecast report. Whether you are a luxury house, conglomerate investor, retail operator, digital platform, or market entry strategist, our report provides the data and clarity to navigate brand positioning, geographic expansion, and consumer segment transitions. Download your free sample today and explore the key growth opportunities in luxury goods.

United Kingdom Luxury Goods Market

United States Luxury Goods Market

South Korea Luxury Goods Market

Philippines Luxury Goods Market

Australia Luxury Goods Market

Luxury Product Diversification and Engagement Insights

Luxury Digital and E Commerce Growth Insights

Luxury Travel Experiential Lifestyle Growth Insights

Upto 15% Off

USD

$2999 $2699

$4399 $3959

$5599 $4759

$6659 $5660

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market value for 2025 is estimated to be nearly USD 361.42 Billion.

The market is expected to grow at a CAGR of 4.40% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach USD 555.93 Billion by 2035.

The increasing wealth of the population is a key factor contributing to the market's growth.

Key trends aiding market expansion include the growing e-commerce sector, which is likely to propel the sales of luxury products along with rising advancements in technology and adoption of omnichannel strategies by market players.

Regions considered in the market are North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa.

Watches and jewellery, perfumes and cosmetics, clothing, and bags/purse, among others are the major products in the market.

Offline and online are the major distribution channels of the product.

Women and men are the different end users in the market.

Key players in the market are LVMH Moet Hennessy Louis Vuitton SE, Chanel Limited, Hermès International S.A., Cartier International AG, Rolex SA, Estée Lauder Companies Inc., Tiffany & Co., Giorgio Armani S.p.A, VALENTINO S.p.A., Ralph Lauren Corporation, Kering SA, Compagnie Financière Richemont SA, Prada SpA, Capri Holdings Limited, Burberry Group plc, L’Oréal Group (France), and Shiseido Company, Limited (Japan), among others.

The clothing category is anticipated to dominate the market in terms of product type.

The Asia Pacific region held the largest share of the market.

The rise of technology-integrated and environmentally friendly products is anticipated to boost product adoption.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by End User |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,999

USD 2,699

tax inclusive*

Single User License

One User

USD 4,399

USD 3,959

tax inclusive*

Five User License

Five User

USD 5,599

USD 4,759

tax inclusive*

Corporate License

Unlimited Users

USD 6,659

USD 5,660

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.