Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

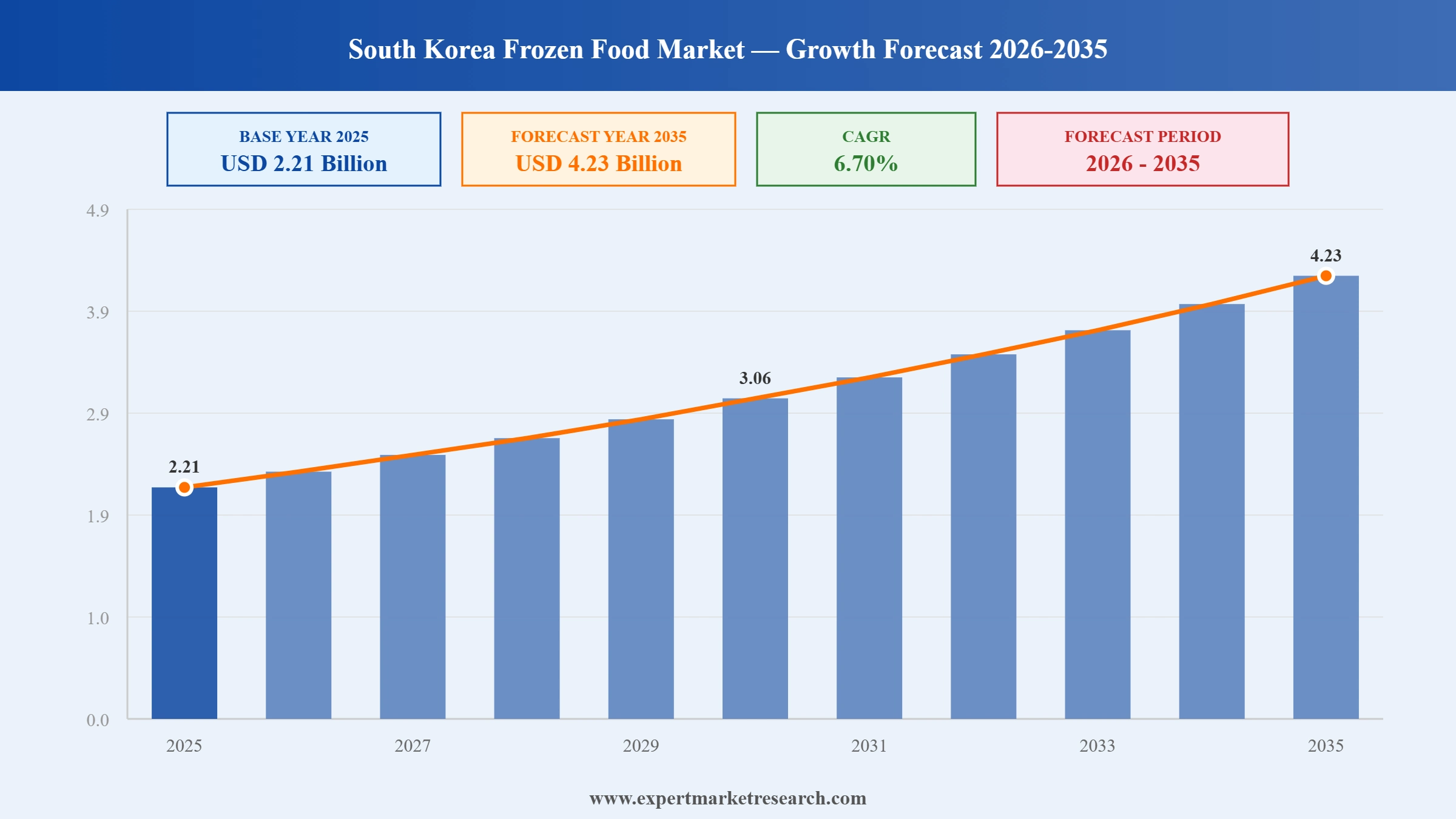

The South Korea frozen food market reached a value of USD 2.21 Billion at 2025 and is projected to expand at a CAGR of around 6.70% during the forecast period of 2026-2035. With the rapid rise of single-person households driving convenience food demand, growing consumer acceptance of frozen Korean cuisine including dumplings and gimbap, expanding modern retail and online delivery infrastructure, and the strong global popularity of K-food lifting domestic frozen food production and innovation, the market is expected to reach USD 4.23 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The South Korea frozen food market is undergoing significant structural transformation, driven by sustained growth in convenience food culture, surging global demand for Korean frozen products, and increasing investment in production technology and market consolidation. These dynamics are reshaping both the domestic market and the competitive strategies of South Korean food companies.

CJ CheilJedang launched the frozen food industry's first fully automated gimbap production line at its Jincheon campus in March 2026. The 18-month proprietary development effort automates every manufacturing stage from rice loading to finished roll slicing and tray-packing.

UCK Partners initiated the sale of Umji Food Co. in September 2025, a Korean frozen dumpling and fried rice OEM valued at up to KRW 300 billion. Umji supplies Costco globally and has secured frozen product contracts with Sam's Club.

Pulmuone became the first Korean company to launch frozen gimbap in China in December 2024, distributing tuna kimbap at Sam's Club stores across the country. Plans to ship 620,000 units annually reflected surging international demand for Korean frozen food products.

Sajo Daerim Corp. launched its frozen kimbap brand in June 2024, entering South Korea's competitive frozen food market. The tuna and vegetable kimbap products had shipped 36 tons to the US before launch, with monthly exports of 72,000 rolls planned.

South Korea's growing single-person household culture is a key driver of the South Korea frozen food market growth, with over 7.8 million solo households estimated in South Korea as of 2024, choosing convenient, portion-controlled frozen meals for daily food needs.

Frozen gimbap has emerged as a transformative product category in the South Korea frozen food market. CJ CheilJedang's Bibigo frozen gimbap recorded cumulative global sales exceeding 6 million units by mid-2025, highlighting the product's strong domestic and international consumer demand.

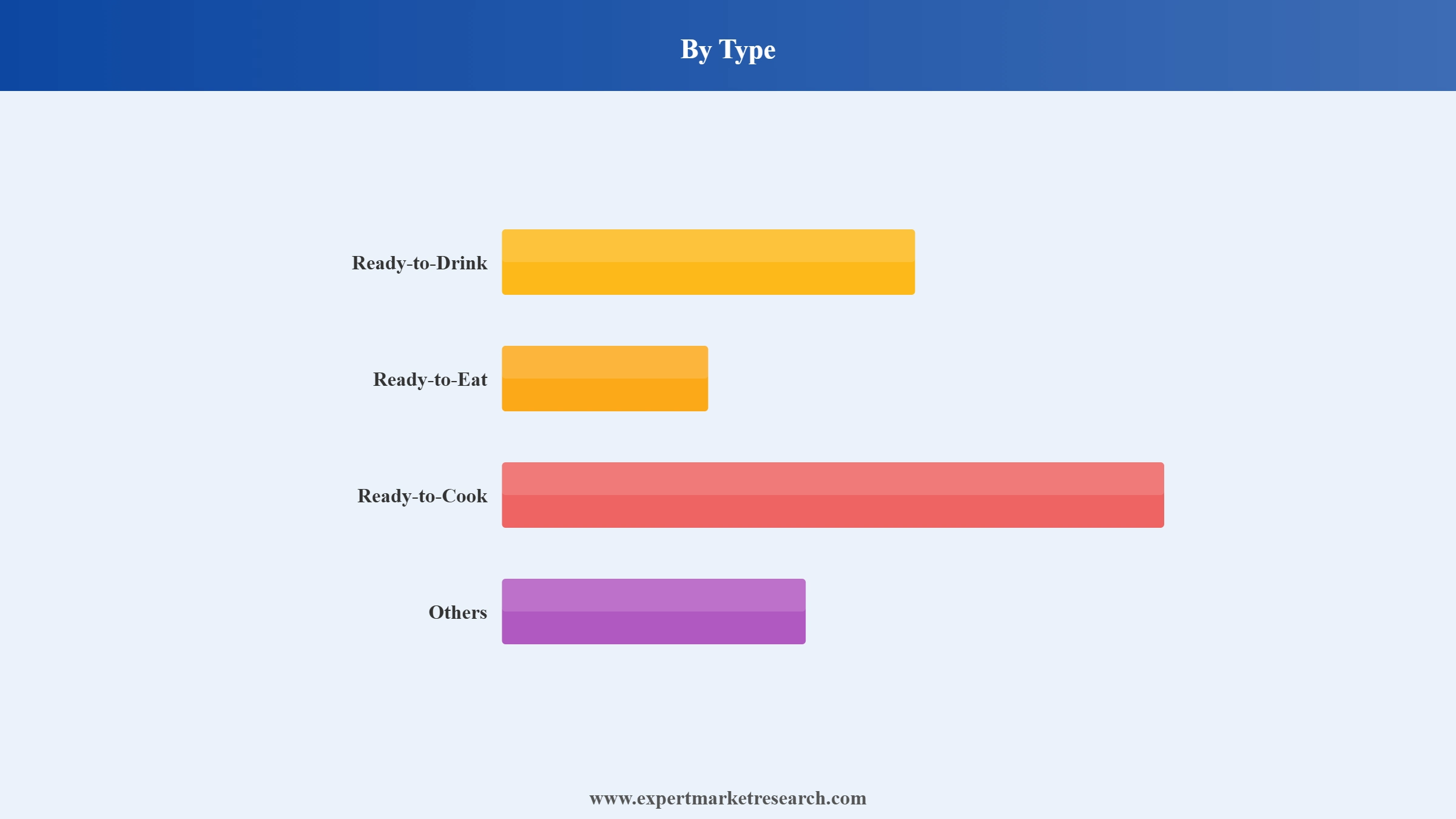

Ready-to-Eat products are the dominant type in the South Korea frozen food market, driven by growing demand for microwavable meals and time-saving food solutions among South Korea's dual-income households, working-age millennial consumers, and large student population in major urban centres.

Supermarkets and hypermarkets are the dominant distribution channel for frozen food in South Korea, offering extensive refrigerated aisles for dumplings, kimbap, and ready meals. Major Korean retailers including Emart, Lotte Mart, and Homeplus drive the bulk of frozen food sales.

Online channels are the fastest-growing distribution mode in the South Korea frozen food market. E-commerce platforms including Coupang and Market Kurly now enable same-day frozen delivery, transforming how South Korean urban consumers purchase frozen dumplings, kimbap, and ready-meal products daily.

The Expert Market Research's report titled “South Korea Frozen Food Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Type

Key Insight: Ready-to-Eat products hold the dominant share of the South Korea frozen food market by type, driven by the strong preference among busy urban consumers, students, and single-person households for meals requiring only microwave reheating. The rise of home meal replacement culture post-pandemic has significantly expanded the Ready-to-Eat segment, with frozen rice dishes, dumplings, kimbap, and portion-controlled meal solutions occupying prominent shelf space across modern retail and convenience channels. Ready-to-Cook is the second most significant type, growing steadily as Korean consumers seek premium cooking experiences at home. Ready-to-Drink represents an emerging segment, offering frozen beverage solutions across convenience store and vending channels.

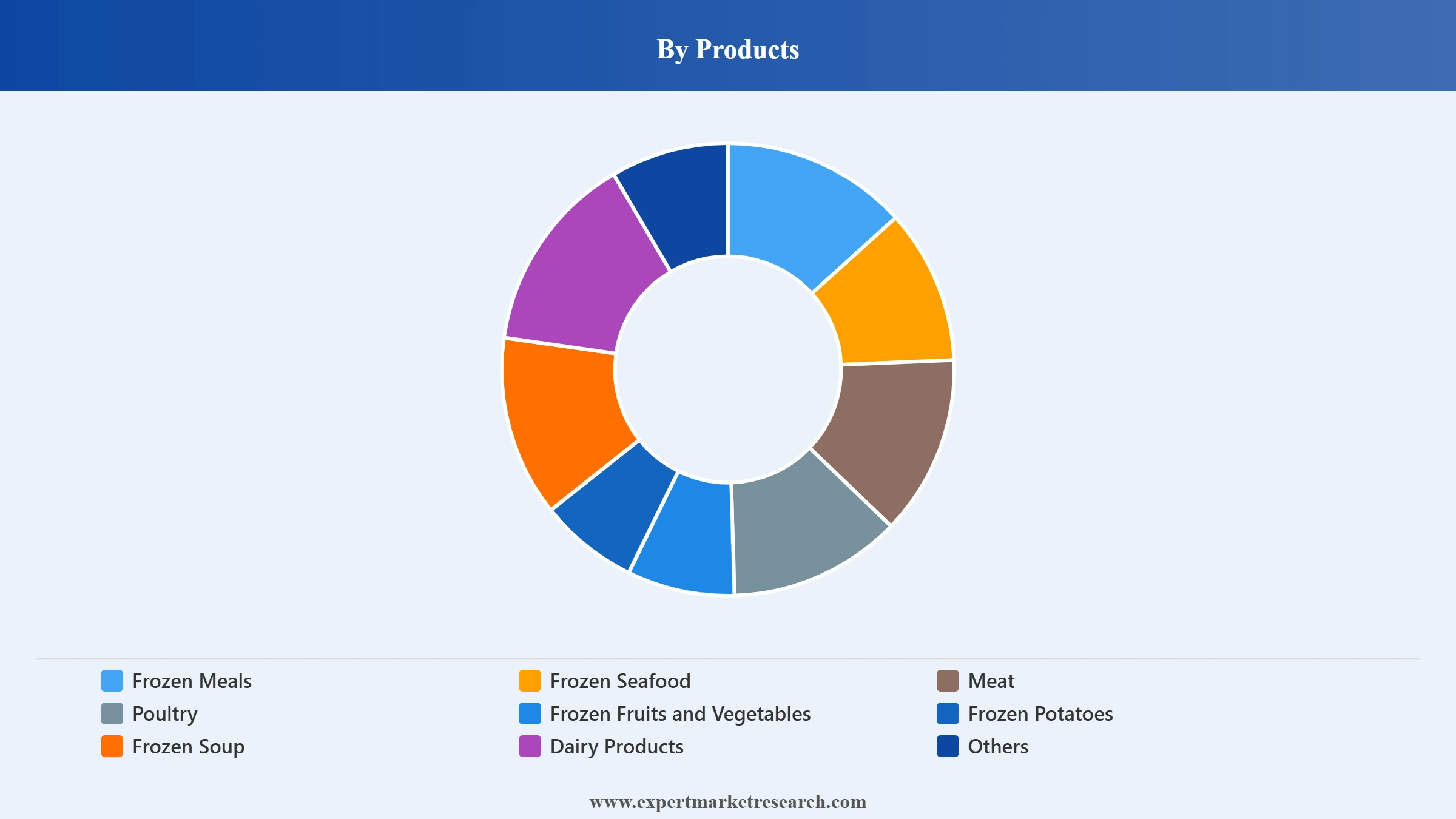

Market Breakup by Product

Key Insight: Frozen Meals hold the dominant share of South Korea's frozen food market by products, driven by the sustained popularity of frozen dumplings, frozen fried rice, frozen bibimbap, and frozen noodle dishes among consumers seeking fast, nutritious meal solutions. South Korea's domestic production of frozen meals reached KRW 3.45 trillion in 2022, reflecting strong category leadership. Frozen Seafood, Meat, and Poultry is the second largest product category, supported by strong Korean culinary traditions around seafood and meat-based dishes. Frozen Fruits and Vegetables are growing in line with rising health consciousness, while Frozen Soup and Dairy Products serve niche demand segments including single-serve instant soups and frozen desserts.

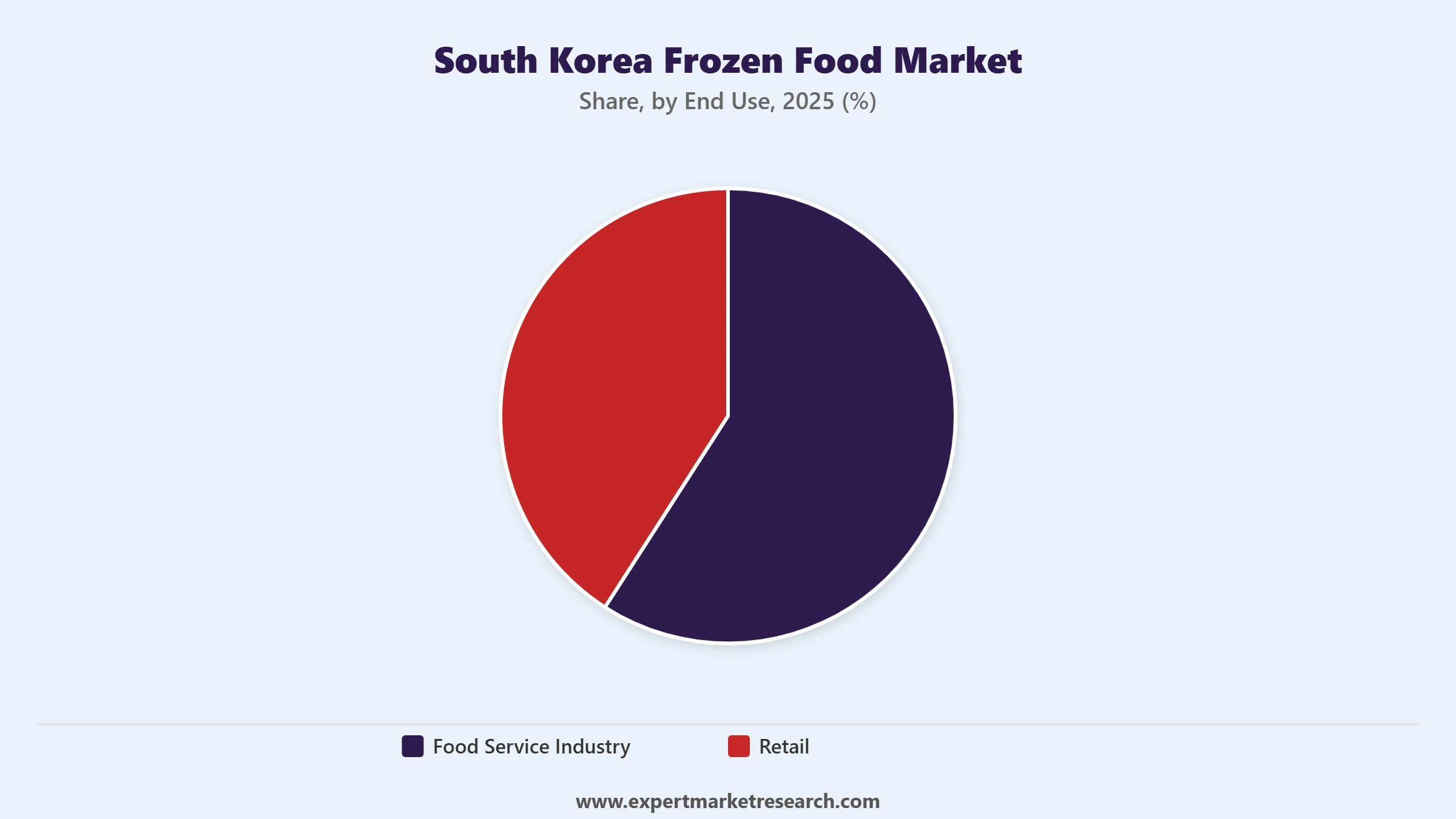

Market Breakup by End Use

Key Insight: The Food Service Industry is the dominant end use segment in the South Korea frozen food market, supported by the large and diverse food service sector including restaurants, cafes, convenience store prepared food sections, school cafeterias, and corporate catering. South Korean food service operators increasingly source frozen dumpling, seafood, and rice products from established suppliers including CJ CheilJedang and Nongshim to ensure consistent quality and supply. The Retail segment is the fastest-growing end use channel, driven by expanding modern grocery retail, the growth of e-commerce grocery platforms such as Coupang and Market Kurly, and South Korean consumers' increasing openness to purchasing frozen food products for home preparation.

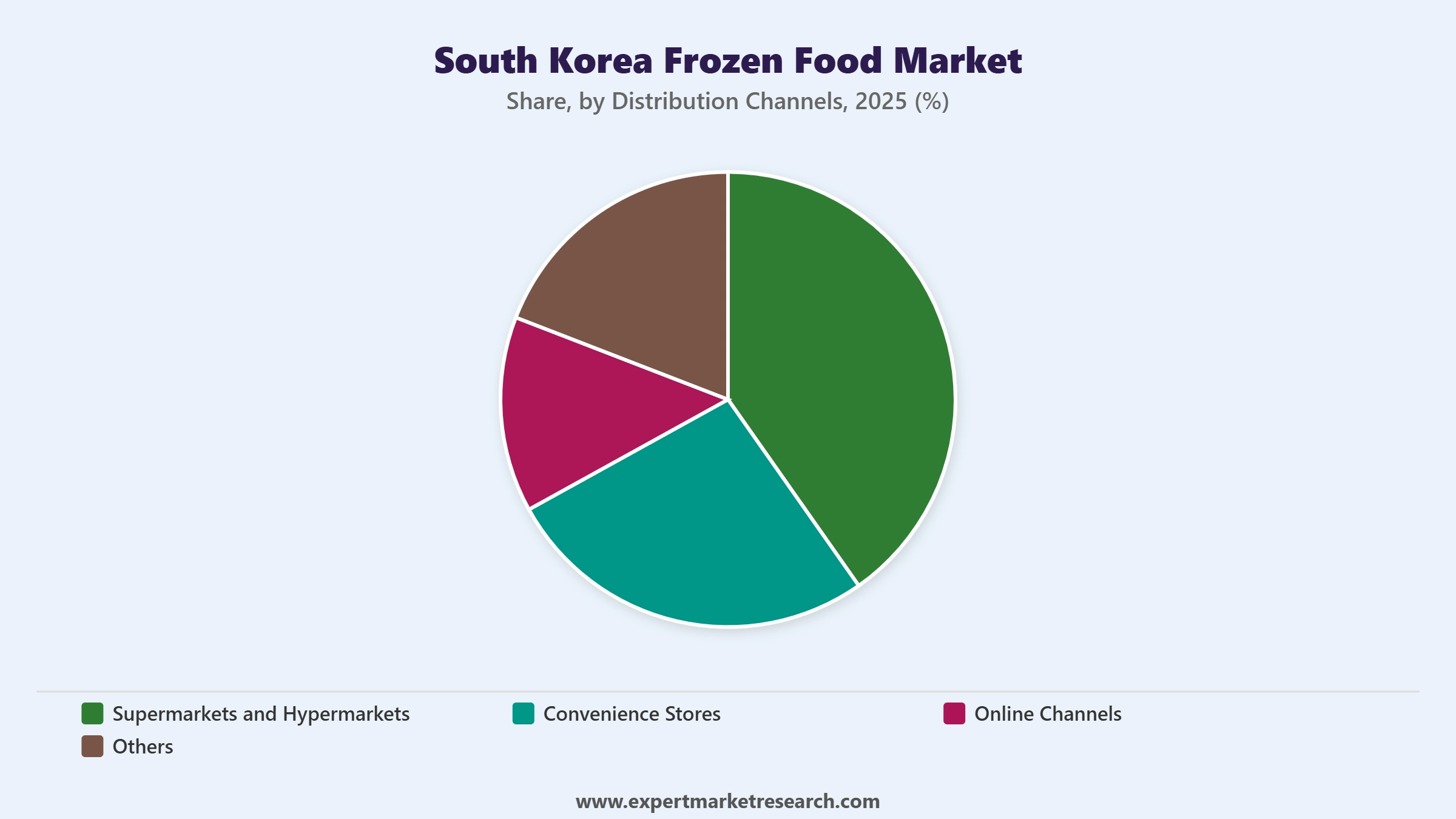

Market Breakup by Distribution Channel

Key Insight: Supermarkets and hypermarkets are the dominant distribution channel in the South Korea frozen food market, providing extensive frozen food sections with wide brand variety and premium refrigerated storage at major retail destinations. South Korean chains including Emart, Lotte Mart, Homeplus, and Costco Korea maintain large frozen food aisles catering to weekly household shopping patterns. Convenience Stores such as GS25, CU, and 7-Eleven Korea have become increasingly significant, offering grab-and-go frozen meal solutions for students and urban workers. Online Channels are the fastest-growing distribution channel, with same-day grocery delivery platforms rapidly capturing frozen food market share as South Korean consumers embrace digital grocery purchasing.

By Type, Ready-to-Eat dominates the market due to high urban consumer demand for microwavable, time-saving meal solutions

Ready-to-Eat products dominate the South Korea frozen food market by type, accounting for the largest revenue share driven by the country's high urbanisation rate, growing solo and dual-income household demographics, and deeply embedded convenience food culture. Microwavable frozen dumplings, frozen bibimbap, frozen fried rice, and ready-to-heat rice bowls are staple items in South Korean households, particularly among young urban professionals and students. CJ CheilJedang's Bibigo brand and Nongshim's product lines are the dominant contributors to this segment's strength in both retail and food service channels. South Korea's domestic frozen food production exceeded KRW 3.45 trillion in 2022, with Ready-to-Eat formats leading production volumes.

Ready-to-Cook is the second most significant type in South Korea's frozen food industry, catering to consumers who prefer a home-cooking experience with the convenience of pre-portioned, pre-seasoned frozen ingredients. Products including raw frozen seafood, marinated frozen meats, and pre-prepared frozen meal kit components serve this segment. Premiumisation is an emerging trend within Ready-to-Cook, with South Korean consumers increasingly seeking high-quality ingredients in frozen formats. Dr. Chung's Food Co., Ltd. and SPC GFS are among the companies serving this growing segment, alongside CJ CheilJedang's plant-based and premium frozen product lines.

By Products, Frozen Meals account for the dominant share of the market due to strong consumer preference for convenient, ready-to-heat Korean cuisine

Frozen Meals are the dominant product category in the South Korea frozen food market, driven by the strong demand for convenient, portion-controlled Korean cuisine including dumplings, fried rice, and bibimbap. CJ CheilJedang's Bibigo brand holds strong market positions across frozen dumpling and kimbap categories, while the domestic OEM sector represented by companies such as Umji Food Co. supplies frozen dumplings and fried rice to major food retailers globally, with UCK Partners valuing Umji at up to KRW 300 billion in its September 2025 divestment process. South Korea's frozen meal production capacity continues to expand.

Frozen Seafood, Meat, and Poultry is the second most significant product category in South Korea's frozen food industry, supported by strong Korean culinary traditions around tuna, squid, shrimp, pork, and chicken in both home cooking and food service settings. Sajo Daerim Corp.'s expansion into frozen kimbap featuring tuna products in June 2024 exemplifies how traditional seafood companies are extending into frozen meal formats. Frozen Fruits and Vegetables are a growing category, driven by health-conscious consumer trends and increased adoption of frozen vegetable side dishes such as spinach, corn, and broccoli for home cooking convenience.

By End Use, Food Service Industry accounts for the dominant share of the market due to large volumes of frozen ingredient procurement across restaurant and institutional channels

The Food Service Industry holds the dominant share of the South Korea frozen food market by end use, with restaurants, cafeterias, convenience store prepared food sections, school canteens, and hotel kitchens consuming significant volumes of frozen dumplings, seafood, and processed meat products. South Korea's food service sector relies heavily on consistent-quality frozen ingredients sourced from leading producers including CJ CheilJedang, Daesang, and Nongshim. The sector's purchasing volumes are supported by South Korea's extremely active restaurant culture, a globally high eat-out frequency, and the widespread presence of convenience stores offering freshly prepared frozen food items.

The Retail segment is the fastest-growing end use channel in South Korea's frozen food industry, driven by expanding modern grocery retail footprints, the rapid penetration of online grocery delivery platforms, and South Korean consumers' increasing openness to purchasing premium frozen food for home consumption. South Korean e-commerce grocery platforms including Coupang, Market Kurly, and SSG.com offer same-day delivery of frozen dumplings, gimbap, and meal kits, significantly lowering the friction for impulse frozen food purchases. The retail segment is expected to narrow the gap with food service as digital grocery infrastructure matures.

By Distribution Channels, Supermarkets and Hypermarkets account for the dominant share of the market due to wide frozen product variety and high household shopping frequency

Supermarkets and hypermarkets are the dominant distribution channel in South Korea's frozen food market, providing consumers with the widest selection of branded and private-label frozen food products in well-maintained refrigerated sections. Major South Korean retail chains including Emart, Lotte Mart, Homeplus, and Costco Korea maintain large-format frozen food aisles that drive weekly household frozen food purchasing across all product categories. The modern retail channel's structured shelf space, promotional activities, and loyalty programmes support high brand visibility and repeat purchasing for leading frozen food brands from CJ CheilJedang and Nongshim.

Convenience Stores are a distinctive and growing distribution channel in South Korea's frozen food industry, with GS25, CU, and 7-Eleven Korea collectively operating tens of thousands of locations that serve busy urban consumers seeking fast, affordable frozen meal solutions. The dense network of South Korean convenience stores enables rapid product distribution for single-serve frozen dumplings, rice balls, and soup products. Online Channels are the fastest-growing distribution mode, with platforms including Coupang and Market Kurly enabling same-day frozen food delivery. CJ CheilJedang and other producers are actively strengthening their digital channel presence to capture the rapidly growing online frozen food consumer segment.

The South Korea frozen food market is highly competitive and dominated by large Korean food conglomerates with diversified product portfolios, extensive manufacturing infrastructure, and strong domestic and international distribution networks. CJ CheilJedang, through its Bibigo brand, holds the leading position in the frozen dumpling, frozen gimbap, and ready-meal segments. Market participants compete on product innovation, quality, convenience features, and pricing, with increasing focus on health-conscious and plant-based frozen food formats. Private equity activity is also reshaping the sector, with mid-sized frozen food OEM companies attracting significant investor interest.

Global K-food demand is creating a new competitive dynamic as South Korean frozen food producers invest in both domestic automation and overseas manufacturing capacity to serve export markets. Companies are racing to establish production scale, with CJ CheilJedang's automated gimbap line in Jincheon representing a major competitive investment in March 2026. Smaller specialist producers such as Sajo Daerim are entering premium segments like frozen kimbap, intensifying competition across product categories and distribution channels.

CJ CheilJedang Corp., founded in 1953 and headquartered in Seoul, South Korea, is the country's largest food company and the leading player in the South Korea frozen food market through its Bibigo brand. It produces frozen dumplings, gimbap, fried rice, and ready meals, exporting to over 70 countries.

Nongshim Co., Ltd., founded in 1965 and headquartered in Seoul, South Korea, is a major Korean food and beverage company primarily known for its instant noodle and snack products. Nongshim participates in the South Korea frozen food market through its range of frozen Korean cuisine and ready-meal offerings.

Dr. Chung's Food Co., Ltd. is a South Korean food company specialising in Korean traditional rice cakes, frozen foods, and ready-to-eat products. The company produces a wide range of frozen Korean food items including dumplings, rice cakes, and HMR offerings for the domestic retail and food service markets.

SPC GFS CO. LTD is the food service distribution subsidiary of South Korea's SPC Group, a major food conglomerate operating Paris Baguette, Baskin-Robbins Korea, and Dunkin' Korea. SPC GFS supplies frozen food products, baked goods, and food ingredients across South Korea's food service and retail channels.

Other key players in the market are Daesang Corporation, Taejong FD Co., Ltd., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock comprehensive intelligence on the South Korea frozen food market with Expert Market Research's detailed 2026 report. Explore in-depth analysis of frozen meal segment dynamics, product innovation across dumplings, gimbap, and ready-to-eat formats, distribution channel performance, and competitive positioning of leading companies including CJ CheilJedang, Nongshim, and Dr. Chung's Food. Whether you are a food manufacturer, retail chain, private equity investor, or market entry planner, this report delivers the clarity you need to capture high-growth opportunities in South Korea's thriving frozen food sector. Download your free sample today.

South Africa Frozen Foods Market

Colombia Frozen Food Market

Frozen Food Market

South Korea Frozen Plant-Based and Meat Analog Products

South Korea Frozen Seafood Innovation

South Korea Frozen Ready Meals Market Insights

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 2.21 Billion.

The market is projected to grow at a CAGR of 6.70% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach USD 4.23 Billion by 2035.

Key strategies driving the market include product diversification with health-focused and plant-based options, technological innovations in freezing and packaging, expanding export markets, collaborations for new flavors, and sustainability initiatives. Brands also leverage digital marketing and convenience to attract busy, health-conscious consumers.

Busy lifestyles, awareness as well as acceptance of frozen foods and concern regarding healthy diet and fitness are the major trends.

The dominant type of frozen food in the industry are Frozen Meals, Frozen Seafood, Meat, and Poultry, Frozen Fruits and Vegetables, Frozen Potatoes, Frozen Soup, and Dairy Products, among others.

The distribution channel segment is led by supermarkets/hypermarkets, convenience stores, and online stores, among others.

The key players in the market report include CJ CheilJedang Corp., Nongshim Co.,Ltd., Dr.Chung’s Food Co.,Ltd, SPC GFS CO. LTD, Daesang Corporation, Taejong FD Co., Ltd. and others.

The ready-to-eat (RTE) segment dominates the market due to the increasing demand for convenience among South Korea’s busy urban population.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Products |

|

| Breakup by End Use |

|

| Breakup by Distribution Channels |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.