Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

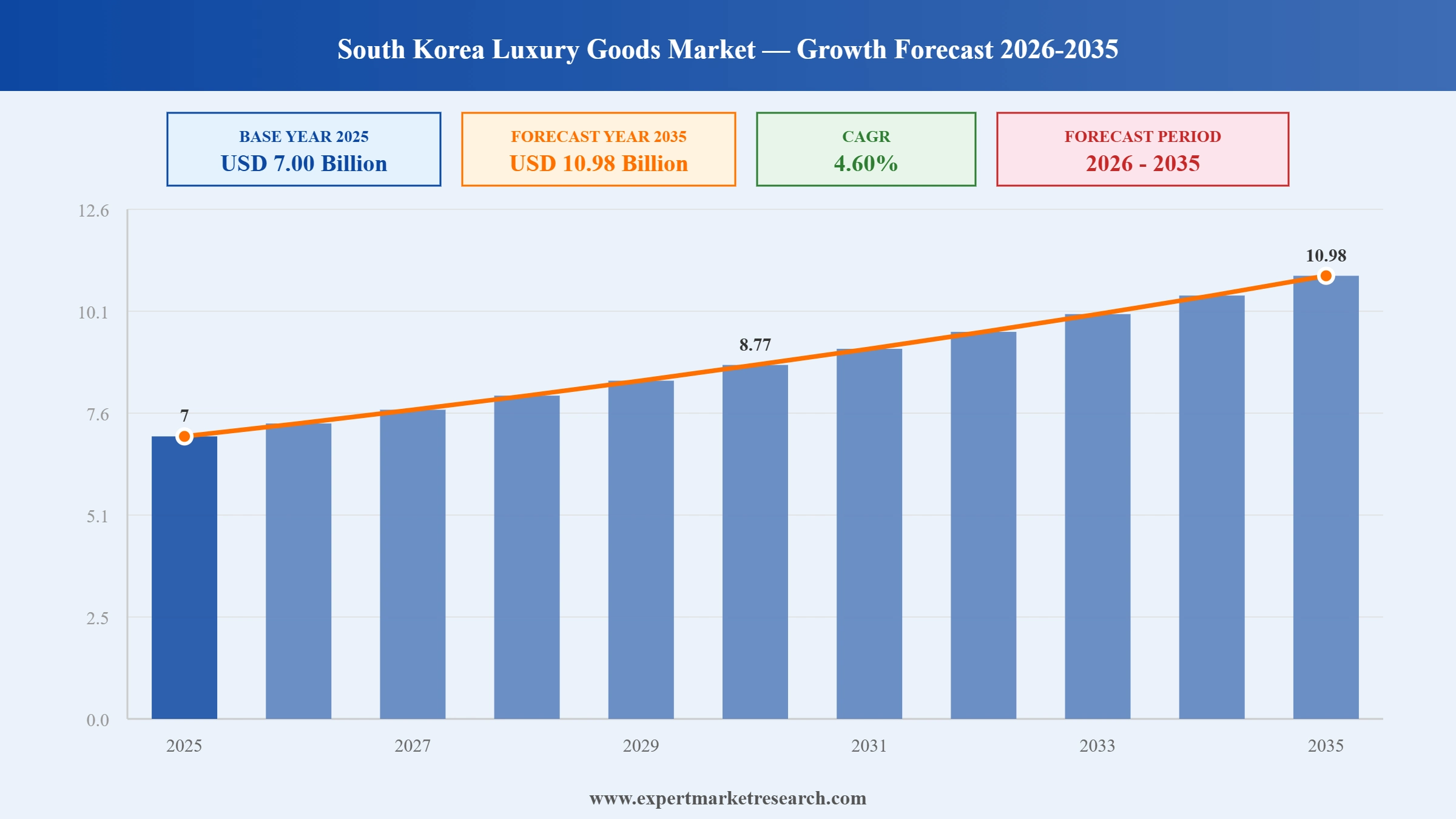

The South Korea luxury goods market reached a value of USD 7.00 Billion at 2025 and is projected to expand at a CAGR of around 4.60% during the forecast period of 2026-2035. With rising per capita luxury expenditure among millennial and Gen Z consumers, growing K-pop and celebrity-driven aspirational demand, expanding digital and offline luxury retail infrastructure in Seoul, and surging tourist spending from Chinese and Japanese visitors, the market is expected to reach USD 10.98 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

South Korea's luxury goods market is being propelled by a convergence of cultural, demographic, and structural forces. Ultra-premium international houses are deepening their retail commitments in Seoul, while domestic department stores record sustained double-digit growth in watches and jewellery. The market reflects a clear barbell structure: top-tier luxury brands accelerate while mid-tier labels face consumer preference shifts toward either ultra-luxury or authenticated resale.

In January 2026, LVMH confirmed plans to expand Louis Vuitton and Dior flagship stores in Seoul's Cheongdam district, with Dior's renovation potentially beginning as early as 2027 and including a permanent restaurant. Bulgari is also considering its first standalone Korean flagship, while a Tiffany flagship store is scheduled to open in Cheongdam-dong in 2027, reinforcing LVMH's long-term commitment to the South Korea luxury goods market.

In December 2025, Hyundai Department Store launched its dedicated Chaumet boutique in Pangyo, expanding the French high jewellery brand's footprint beyond Seoul's central luxury corridors. The opening catered to the affluent suburban consumer base and reflected growing demand for exclusive watch and jewellery retail experiences across the South Korea luxury goods market.

In June 2025, Vacheron Constantin opened a flagship store in Seoul, targeting South Korea's expanding premium watch consumer base. The launch aligned with a surge in department store watch and jewellery sales, with Lotte, Shinsegae, and Hyundai all recording year-on-year growth of 35 to 38 percent in the category during Q3 2025.

In March 2024, Cartier Korea announced a historic sales milestone of approximately USD 1.1 billion for the fiscal year ending that month. The surge was partly attributed to an 8.4% uptick in marriages in South Korea and a sustained 16-month streak of growth in wedding-related luxury gifting, confirming jewellery and watches as the fastest-growing product categories within the market.

Watches and jewellery have become the standout growth segment within the South Korea luxury goods market, buoyed by rising marriage rates and gold price appreciation of over 80 percent year-on-year to KRW 245,000 per gram by February 2026. LVMH Watch and Jewelry Korea reported a 32.8% sales increase, while Bulgari Korea grew 23.3% to KRW 419.1 billion, cementing hard luxury as both a store of value and a fashion statement.

The South Korea luxury goods market growth trajectory is increasingly bifurcated. Ultra-luxury brands such as Hermes, which posted 20.9% growth reaching KRW 964.2 billion in 2024, and Chanel, which recorded 8.2% growth to KRW 1.84 trillion, continue to outperform. Mid-tier brands like Fendi and Ferragamo, however, reported declines of 20% and 12.7% respectively, as consumers trade up or turn to authenticated resale channels.

Tourist inflows from China and Japan, combined with the depreciation of the Korean won, have added a meaningful layer to luxury sales in the South Korea luxury goods industry. Tourist spending climbed roughly one-third to a record KRW 9.26 trillion in 2024, as international visitors found luxury goods in Seoul competitively priced relative to their home markets, further lifting total luxury sales volumes.

Celebrity endorsements and K-pop idol partnerships remain core demand drivers in the South Korea luxury goods market. Brands partner with Korean stars to reach younger consumers across social media, generating viral visibility that translates into in-store and online sales. The broad cultural export of K-drama and K-pop lifestyles has made Korean luxury consumption a globally watched trend, attracting international brands to deepen their Seoul commitments.

Online luxury resale is reshaping how younger South Korean consumers engage with premium goods. Korea's secondhand luxury market is projected to exceed KRW 50 trillion in 2026 from KRW 43 trillion in 2025, per the Seoul Economic Daily. KREAM, an authenticated resale platform, has expanded into luxury handbags and watches, drawing MZ generation consumers who seek sustainability, value, and investment-grade luxury purchases within the South Korea luxury goods market.

The Expert Market Research’s report titled “South Korea Luxury Goods Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

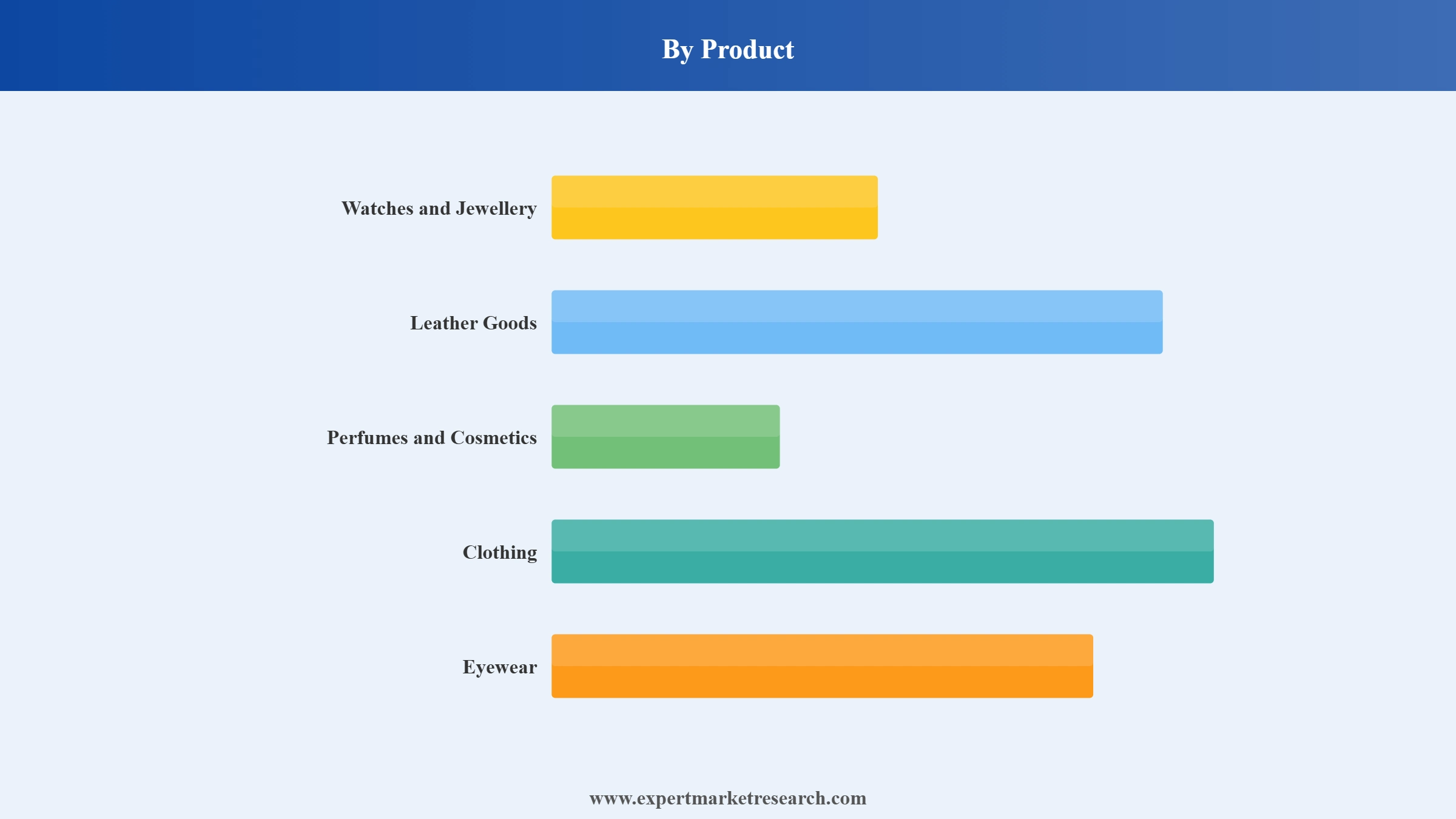

Market Breakup by Product

Key Insight: Clothing holds the dominant product share within the South Korea luxury goods market, accounting for 40.25% in 2025, driven by seasonal flagship collections and the influence of celebrity and K-pop collaborations. Watches and jewellery represent the fastest-growing category at a CAGR of around 6.45% through the forecast period, supported by surging marriage rates, rising gold prices, and a growing culture of hard luxury as both status and investment. Leather goods, perfumes, and eyewear contribute steadily to overall market expansion.

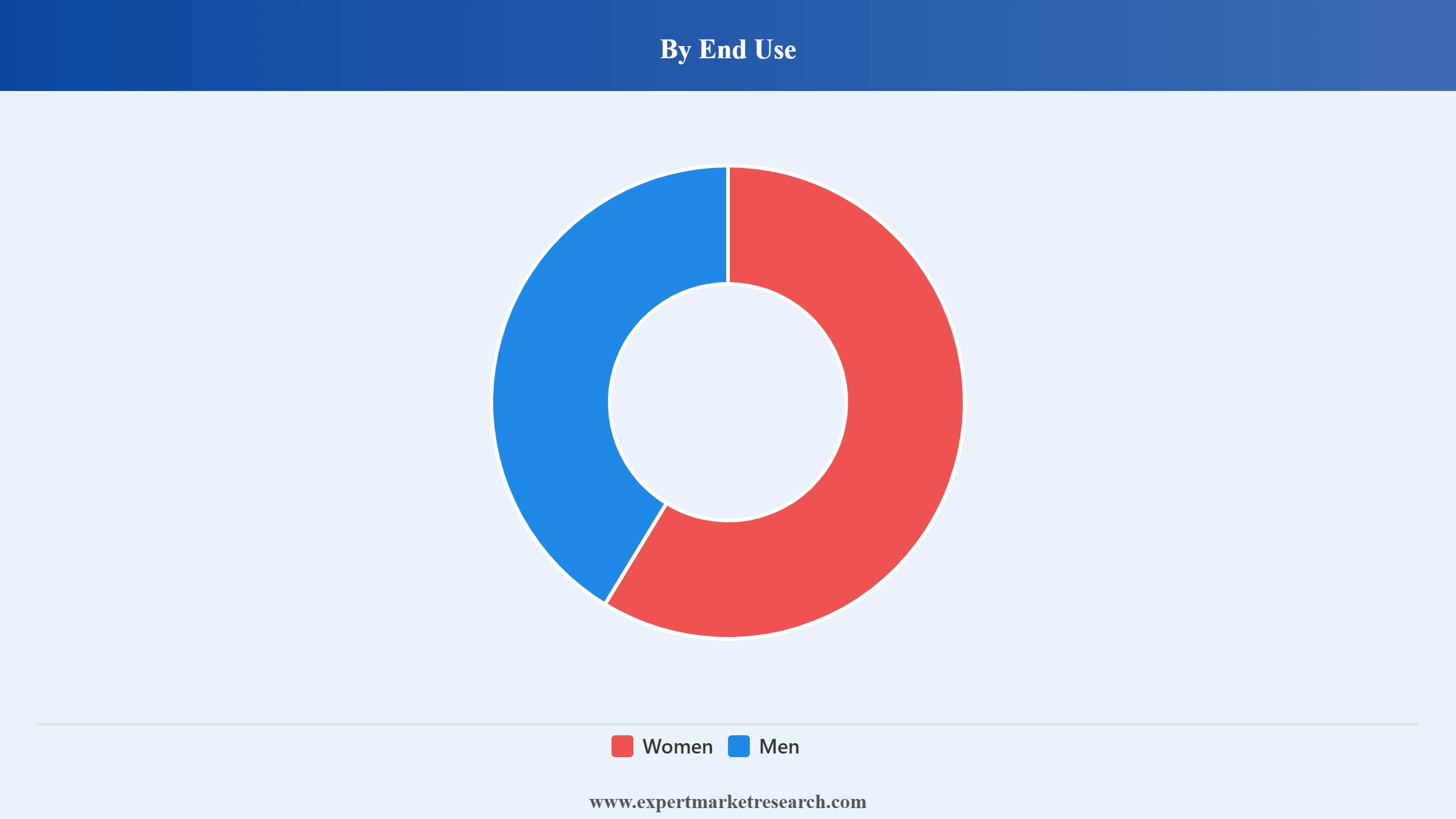

Market Breakup by End Use

Key Insight: Women remain the primary end use segment within the South Korea luxury goods market, driven by high engagement with clothing, leather handbags, cosmetics, and jewellery. The male luxury segment is expanding meaningfully, underpinned by growing acceptance of male grooming, premium menswear, and luxury watch ownership among younger professional men. Brands including Dior and Louis Vuitton have developed targeted menswear and accessories lines specifically for the Korean market, broadening the male consumer base and narrowing the gender consumption gap in luxury.

Market Breakup by Distribution Channels

Key Insight: Offline retail channels hold the largest share of the South Korea luxury goods market, anchored by flagship mono-brand stores, high-traffic department stores including Lotte, Shinsegae, and Hyundai, and duty-free zones in Seoul and Incheon that attract both domestic shoppers and tourists. Online is growing fastest, supported by authenticated resale platforms like KREAM, brand-operated e-commerce, and social commerce via Kakao and Naver. Virtual try-on technology and AI-enabled personalization are accelerating digital luxury conversion, particularly among millennials and Gen Z consumers.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By product, clothing accounts for the dominant share of the market due to K-pop endorsements and seasonal collections

Clothing commands the largest product share within the South Korea luxury goods market because the country's fashion-conscious consumer base responds strongly to seasonal collections, celebrity endorsements, and the global visibility of K-pop idol styling. Major houses including Chanel, Louis Vuitton, and Dior design capsule collections targeting Korean market tastes, generating sustained high-volume purchases particularly among affluent millennials and professional consumers in Seoul and other major cities.

Despite clothing's dominance, watches and jewellery represent the most dynamic growth story. Department stores across Korea recorded 35 to 38 percent year-on-year gains in this category in Q3 2025, supported by rising marriage rates and gold appreciation. Cartier Korea's USD 1.1 billion revenue milestone for fiscal year 2024 and Vacheron Constantin's Seoul flagship opening in June 2025 confirm this segment's sustained commercial momentum within the South Korea luxury goods industry.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By end use, women account for the dominant share of the market due to high demand for clothing, handbags, and jewellery

Women constitute the larger end use segment, driven by historically higher engagement with luxury clothing, leather handbags, cosmetics, and fine jewellery in South Korea. The country's strong beauty and fashion culture, combined with K-pop and K-drama influence, sustains female consumer interest in premium international brands. Chanel Korea's 8.2% sales growth to KRW 1.84 trillion in 2024 is partly attributable to female consumers' affinity for the brand's seasonal clothing and accessories collections.

Men represent a growing end use segment, with younger Korean males increasingly viewing luxury watches, premium menswear, and designer accessories as status markers and investment assets. Brands have responded by expanding Korean menswear ranges and dedicating more floor space to male-targeted collections. Gold prices surging 80% year-on-year to KRW 245,000 per gram by February 2026 have also elevated male interest in luxury watches as tangible stores of value within the South Korea luxury goods market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By distribution channels, offline channels account for the dominant share of the market due to flagship store experience and department store footprint

Offline retail is the primary channel within the South Korea luxury goods market because mono-brand flagship stores, luxury department store concessions, and duty-free zones collectively provide the experiential, touch-and-feel engagement that reinforces luxury brand prestige. Department store groups Lotte, Shinsegae, and Hyundai reported combined luxury sales growth across watches, jewellery, and apparel that consistently outperformed other retail categories in 2024 and 2025, confirming offline's structural role as the commercial anchor of the market.

Online is growing at the fastest pace, propelled by KREAM's authenticated resale marketplace, brand digital flagships, and the growing comfort of Korean consumers with high-value online transactions. Korea's secondhand luxury market is set to reach KRW 50 trillion in 2026, per the Seoul Economic Daily, as MZ generation consumers drive trade in authenticated pre-owned luxury goods. LVMH's planned Bulgari and Tiffany flagship openings in 2027 will further stimulate omnichannel engagement across offline and digital touchpoints within the South Korea luxury goods market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The South Korea luxury goods market is dominated by European luxury conglomerates, with LVMH, Kering, and Richemont collectively accounting for the largest share of branded luxury sales. These global powerhouses benefit from strong brand heritage, Seoul flagship stores, and deep celebrity partnership strategies tailored to Korean consumer sensibilities. The competitive environment is fragmented across product verticals, with no single player dominating across clothing, watches, leather goods, and cosmetics simultaneously.

Domestic luxury house Minjukim has carved a distinct position in the designer clothing segment, appealing to younger aspirational consumers and K-pop styling demand. International mono-brands like Rolex and Chanel operate with exceptional pricing power, while multi-brand department store environments foster category-level competition. The strategic priorities of major players increasingly center on flagship store experience, digital engagement, and authentic celebrity partnerships to sustain relevance with South Korea's informed and discerning luxury consumer base.

The world's largest luxury conglomerate, founded in 1987 and headquartered in Paris, France. LVMH operates Louis Vuitton, Dior, Bulgari, Tiffany, and over 75 other premium houses in South Korea, with Cheongdam flagship expansions planned for Louis Vuitton and Dior from 2027. The group's combined South Korean revenues for Louis Vuitton and Dior reflect consistent high-single-digit annual growth, supported by tourism demand and strong domestic consumption.

Founded in 1963 and headquartered in Paris, France, Kering operates Gucci, Saint Laurent, Bottega Veneta, and Balenciaga in South Korea. The group leverages K-pop celebrity partnerships and social media-led campaigns to maintain brand relevance among millennial and Gen Z luxury consumers. Gucci remains one of the most recognised international luxury brands among Korean shoppers, supported by a dedicated flagship presence in Seoul's premium shopping corridors.

Founded in 1988 and headquartered in Geneva, Switzerland, Richemont operates Cartier, Van Cleef and Arpels, IWC, and Panerai in South Korea. Cartier Korea achieved a historic USD 1.1 billion sales milestone for fiscal year ending March 2024, capitalizing on South Korea's rising marriage rates and strong bridal jewellery demand. Richemont's watches and jewellery portfolio directly benefits from South Korea's fastest-growing luxury product category.

Founded in 1910 and headquartered in Paris, France, Chanel is one of the most commercially powerful mono-brands in South Korea. Chanel Korea reported KRW 1.84 trillion in sales in 2024, representing 8.2% year-on-year growth. The brand's clothing, handbags, and fragrance collections consistently generate significant consumer demand, with long-standing flagship stores in Cheongdam-dong and department store concessions reinforcing its dominance in the South Korea luxury goods market.

Other key players in the market are The Swatch Group Ltd, ROLEX SA, Minjukim, Guccio Gucci S.p.A., Prada S.p.A, and others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Gain the intelligence you need on the South Korea luxury goods market with our comprehensive report. Explore how K-pop influence, surging watch and jewellery demand, ultra-premium brand polarisation, and a booming authenticated resale segment are redefining the landscape. Whether you manage a flagship brand, operate in luxury retail, invest in consumer discretionary, or seek market entry intelligence, this report gives you the clarity to act with confidence. Download your free sample today and discover the key opportunities across luxury goods in South Korea.

United Kingdom Luxury Goods Market

Latin America Luxury Goods Market

United States Luxury Goods Market

Asia Pacific Luxury Goods Market

Philippines Luxury Goods Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the South Korea luxury goods market reached an approximate value of USD 7.00 Billion.

The market is projected to grow at a CAGR of 4.60% between 2026 and 2035.

Key strategies driving the market include localising campaigns with K-influencers, integrating AR tools in stores, launching eco-luxury capsules, partnering with K-culture platforms, and embedding personalisation tech to deepen consumer ties across online and offline.

Digitalisation and sustainability emergence, along with consumer awareness and innovation in the fashion industry are the leading trends.

The dominant type of luxury products in the industry are watches and jewelry, leather goods, perfumes and cosmetics, clothing, and eyewear, among others.

The leading distribution channels in the luxury market are online and offline retail channels.

The key players in the South Korea luxury industry are LVMH Moët Hennessy, Compagnie Financière Richemont SA, The Swatch Group Ltd, ROLEX SA, Kering Group, Minjukim, Guccio Gucci S.p.A., Chanel, Prada S.p.A, among others.

The key challenges are import tariffs, changing tax norms on resale, influencer fatigue, and consumer scepticism over authenticity and ethical sourcing in the face of greenwashing.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product |

|

| Breakup by End Use |

|

| Breakup by Distribution Channels |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.