Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

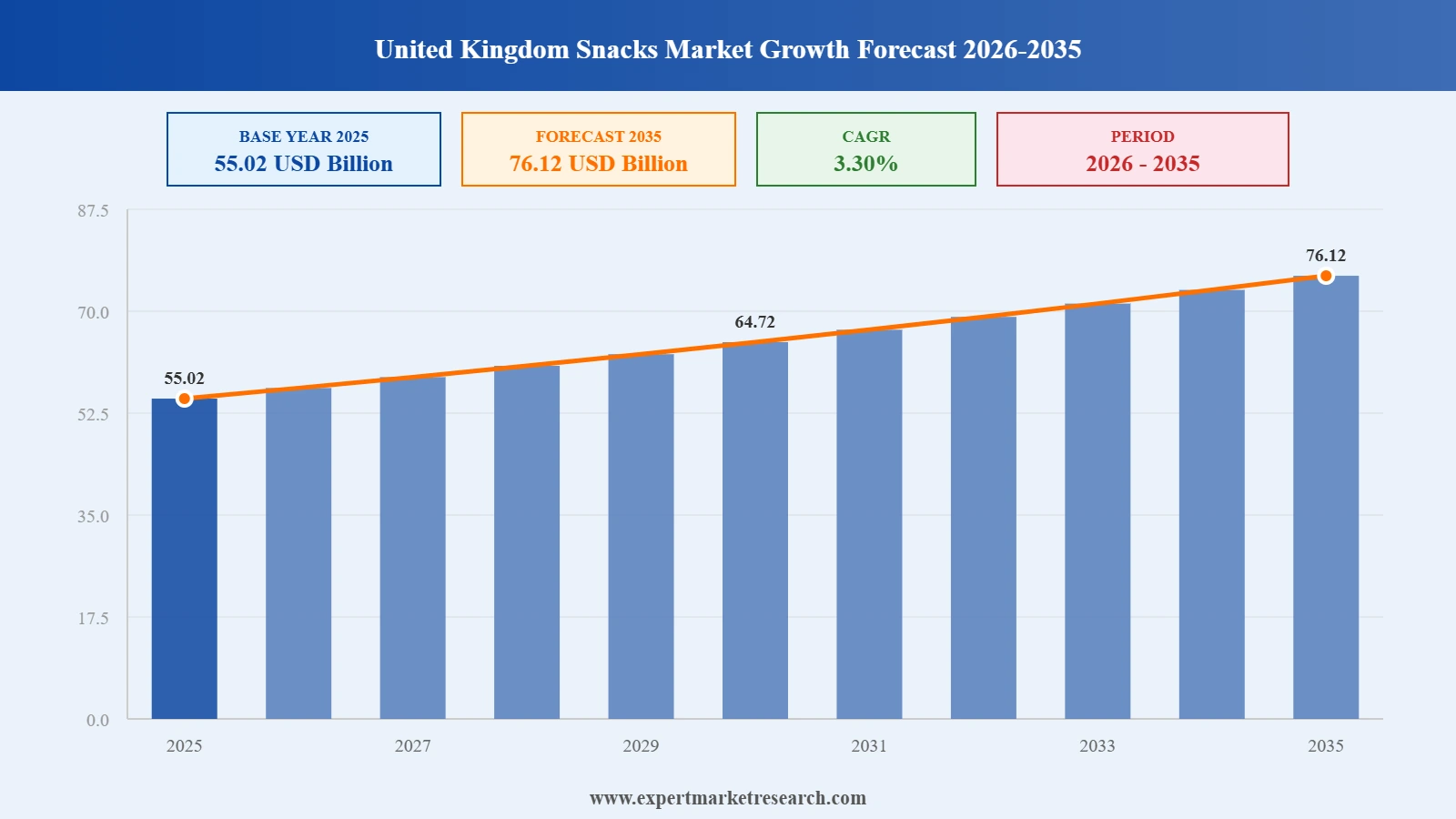

The United Kingdom Snacks Market reached a value of USD 55.02 Billion at 2025 and is projected to expand at a CAGR of around 3.30% during the forecast period of 2026-2035 to reach USD 76.12 Billion by 2035. With England's dominant position anchored by rising disposable incomes and strong appetite for both savoury and premium snacking options, growing consumer demand for clean-label and plant-based snack formats is reshaping the product innovation landscape, accelerating online retail channel adoption driven by grocery delivery platform expansion, and strategic international brand consolidation through M&A activity is intensifying UK market competition.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| United Kingdom Snacks Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 55.02 |

| Market Size 2035 | USD Billion | 76.12 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 3.30% |

| CAGR 2026-2035 - Market by Region | England | 10.2% |

| CAGR 2026-2035 - Market by Region | Scotland | 3.5% |

| CAGR 2026-2035 - Market by Type | Fruit Snacks | 3.8% |

| CAGR 2026-2035 - Market by Distribution Channel | Online Channels | 13.7% |

| 2025 Market Share by Region | England | 78.4% |

The United Kingdom Snacks Market is being shaped by a distinct set of evolving dynamics: England's accelerating regional demand growth, the ongoing shift toward clean-label and better-for-you snacking driven by health-conscious British consumers, rising consumer appetite for bold and novel flavour innovations including swicy and umami profiles, and the strategic response of global snack conglomerates to UK regulatory and market pressures. Together, these trends are expected to sustain healthy and sustained market expansion through 2035.

In December 2025, Mars Incorporated completed its USD 35.9 billion acquisition of Kellanova, adding iconic snack brands including Pringles, Pop-Tarts, and Cheez-It to its UK portfolio alongside its existing Snickers, Twix, M&Ms, and Kind confectionery and snack bar brands. The combined Mars Snacking entity now operates across more than 145 markets globally, including the United Kingdom, with a portfolio of 9 billion-dollar brands. The acquisition significantly strengthens Mars's competitive position in the UK snacks market relative to PepsiCo (Walkers) and Mondelez International, and creates new cross-brand innovation and promotional opportunities for UK retail partners.

In December 2025, PepsiCo's UK operations launched a new range of baked snacks lower in fat and calories, targeting the growing segment of British consumers who prioritize health and nutritional transparency without compromising on flavour. The product development initiative reflects PepsiCo's response to the sustained demand for healthier snacking alternatives across the UK market and aligns with the company's global commitment to building out its better-for-you snack portfolio alongside its core Walkers, Lay's, and Doritos brands. The launch was distributed across UK supermarkets and convenience retail channels, with targeted digital marketing to health-conscious consumer demographics.

In November 2025, Nestle's UK operations announced a strategic partnership with a leading plant-based ingredient supplier to develop and expand its range of healthy snacks incorporating plant-derived protein and fibre sources. The partnership is intended to bolster Nestle's position in the rapidly growing UK plant-based snacking segment, where consumer demand for products aligned with reduced meat consumption and sustainable sourcing continues to strengthen. The collaboration is expected to yield new snack product launches across the UK retail market during 2026, spanning both confectionery-adjacent and savoury snack formats.

In August 2024, Mars Incorporated and Kellanova announced a definitive agreement under which Mars agreed to acquire Kellanova for USD 83.50 per share in cash, a total consideration of USD 35.9 billion. For the UK market, the deal has significant implications as Kellanova's Pringles brand, manufactured in Belgium and widely distributed across UK retail, would join Mars's existing UK snacking presence. The combination was projected to create intensified competition with PepsiCo's Walkers and Mondelez International across UK salty, sweet, and mixed snacking segments, accelerating promotional and innovation cycles across British supermarkets and convenience retail.

In 2024, major snack manufacturers operating in the United Kingdom accelerated investments in premium and clean-label product development, responding to rising British consumer demand for snacks with shorter ingredient lists, natural flavourings, and transparent sourcing credentials. This trend is particularly pronounced among younger UK consumers, who are increasingly scrutinizing ingredient labels and brand sustainability practices as part of their purchase decisions. Private label manufacturers are also expanding their digital presence and premium snacking ranges across Tesco, Sainsbury's, and ASDA, as supermarket own-brand snacks command growing consumer trust and shelf space in the competitive UK retail landscape.

The United Kingdom Snacks Market is experiencing the downstream effects of a global wave of M&A consolidation, as major snack conglomerates build broader, more competitive multi-category portfolios aimed at strengthening their positions in premium retail environments such as UK supermarkets and convenience chains. In December 2025, Mars Incorporated completed its USD 35.9 billion acquisition of Kellanova, combining Mars's UK confectionery presence with Kellanova's salty and sweet snack brands including Pringles and Pop-Tarts. The consolidated Mars Snacking entity is expected to increase competitive pressure on PepsiCo's Walkers and Mondelez International across UK savoury, confectionery, and snack bar categories.

British consumers are placing increasing emphasis on transparency, natural ingredients, and health credentials when selecting snack products, driving brands to reformulate existing products and launch new clean-label ranges across bakery, confectionery, and savoury snacking formats. The United Kingdom Snacks Market growth is being reinforced by this premiumization trend, as consumers demonstrate willingness to pay higher prices for snacks that align with their nutritional and ethical values. This trend is particularly influential in England's urban markets, where health-conscious demographics and high retail sophistication create ideal conditions for clean-label premium snack adoption. Major private label manufacturers and established brands alike are competing for this growing consumer segment through reformulation, ingredient transparency initiatives, and sustainability-focused packaging.

Leading global snacks brands operating in the UK are actively launching healthier snack product lines in response to persistent British consumer demand for reduced-calorie, reduced-fat, and nutritionally enriched snacking options. This trend is shaping both product development roadmaps and retail shelf space allocation, with supermarkets including Tesco and Sainsbury's dedicating growing shelf space to better-for-you snack formats. In December 2025, PepsiCo UK launched a new range of lower-fat, lower-calorie baked snacks aimed at health-conscious British consumers, demonstrating the company's commitment to building out its healthier alternatives portfolio in the UK market alongside its core Walkers and Doritos brands.

The UK snacks market is experiencing meaningful growth in plant-based and functional snack formats, driven by increasing numbers of British consumers identifying as flexitarian or reducing their meat and animal-product consumption. Manufacturers are investing in plant-based protein, fibre-enriched, and functional ingredient integration to capture this growing demand pool, developing snack products that offer both nutritional benefits and familiar flavour profiles. In November 2025, Nestle UK announced a strategic partnership with a leading plant-based ingredient supplier to develop an expanded range of plant-derived healthy snacks, positioning itself to capture growing consumer interest in products that combine sustainability credentials with accessible taste and convenience.

The Expert Market Research's report titled “United Kingdom Snacks Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

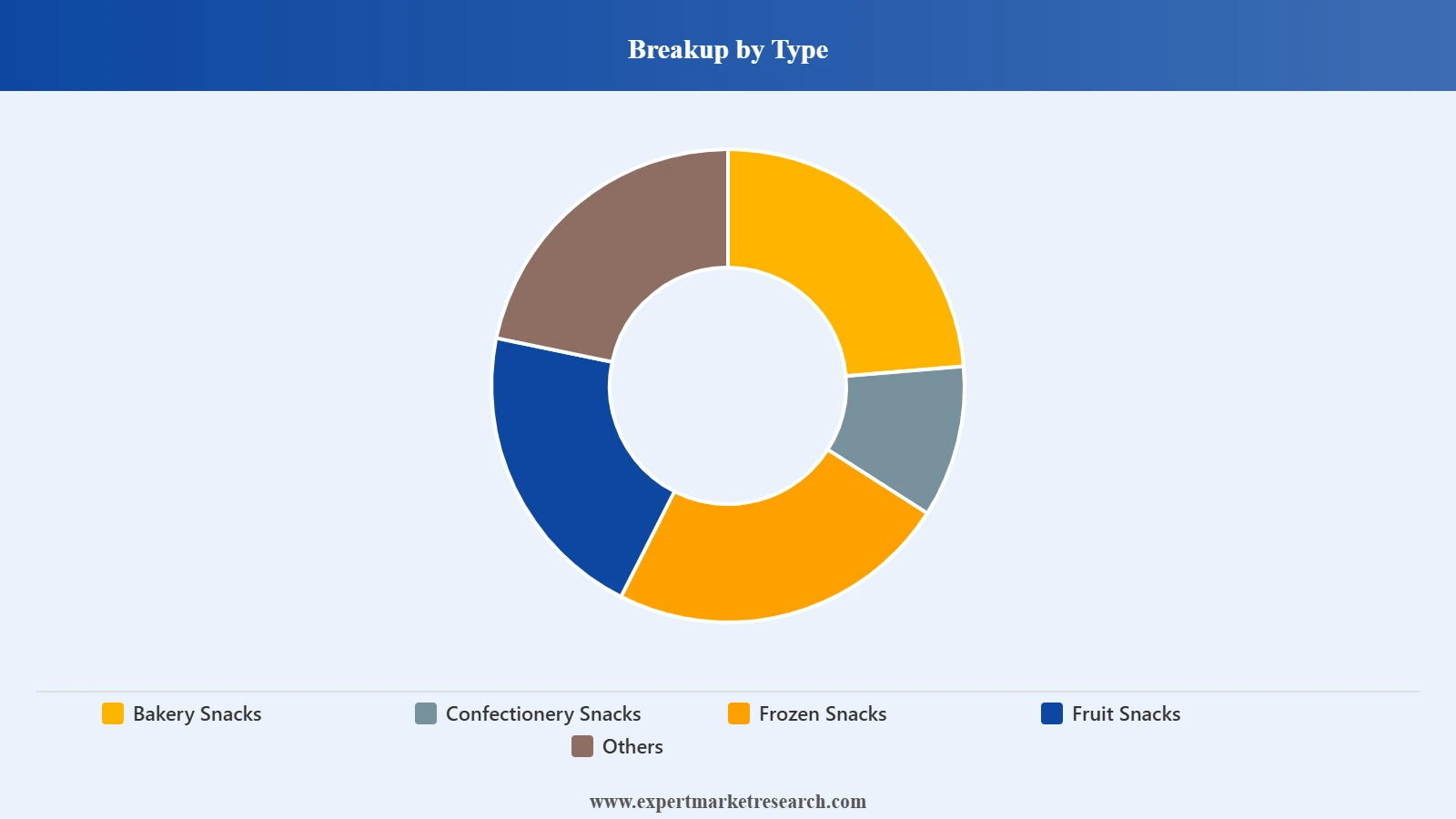

Market Breakup by Type

Key Insight: Confectionery Snacks represent the largest type segment in the UK snacks market, encompassing chocolate bars, candy, and sweet confectionery formats that are deeply embedded in British snacking culture. Brands including Cadbury (Mondelez), Maltesers and Twix (Mars), and Rowntrees and KitKat (Nestle) dominate this segment, benefiting from near-universal brand recognition and consistent gifting and impulse purchase demand. Bakery Snacks, covering biscuits, crackers, and cereal bars, represent the second most significant type segment, with the biscuit category in particular holding a uniquely prominent position in British food culture. Frozen Snacks are a growing category as UK consumers increasingly adopt convenient meal-adjacent snacking formats that require minimal preparation. Fruit Snacks serve health-oriented consumers seeking naturally derived sweet alternatives. The Others category encompasses savoury crisps and nuts, popcorn, and emerging categories including legume-based crisps and rice cakes.

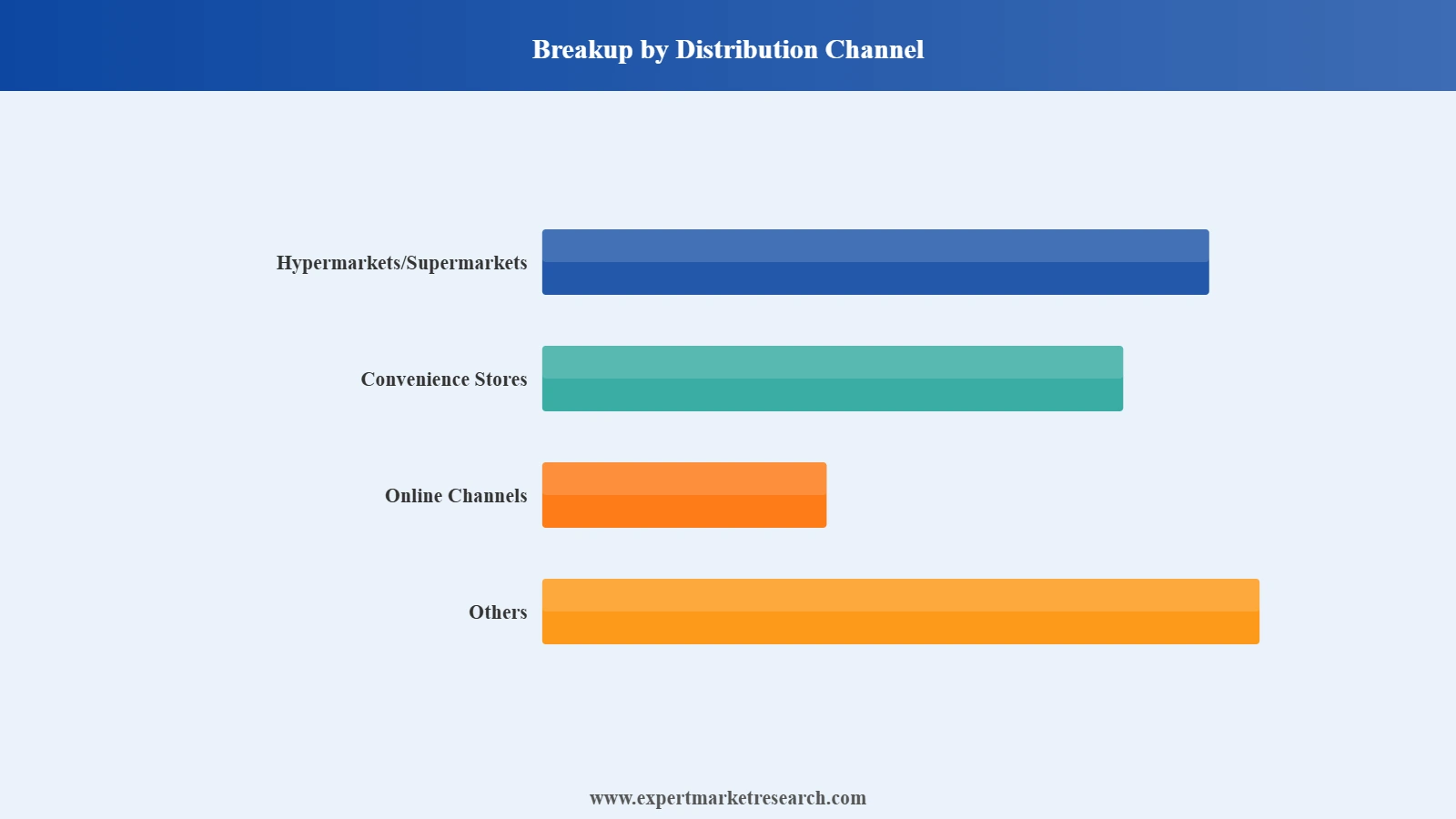

Market Breakup by Distribution Channel

Key Insight: Hypermarkets and Supermarkets dominate the UK snacks distribution landscape, accounting for the majority of snacking revenue through major grocery chains including Tesco, Sainsbury's, ASDA, and Morrisons, as well as discount grocers including Aldi and Lidl that have significantly expanded their snack ranges in recent years. Convenience Stores, anchored by chains including Spar, Co-op, and independent newsagents, serve as critical distribution points for impulse-format, single-serve, and on-the-go snack purchases, particularly in urban areas across England. Online Channels are the fastest-growing distribution segment in the UK snacks market, driven by the rapid expansion of grocery delivery services including Deliveroo Grocery, Ocado, and Amazon Fresh, as well as direct-to-consumer snack subscription boxes that target health-oriented and premium consumer segments. The Others category covers food service outlets, petrol station forecourts, and vending channels that contribute consistent snack volumes across the UK.

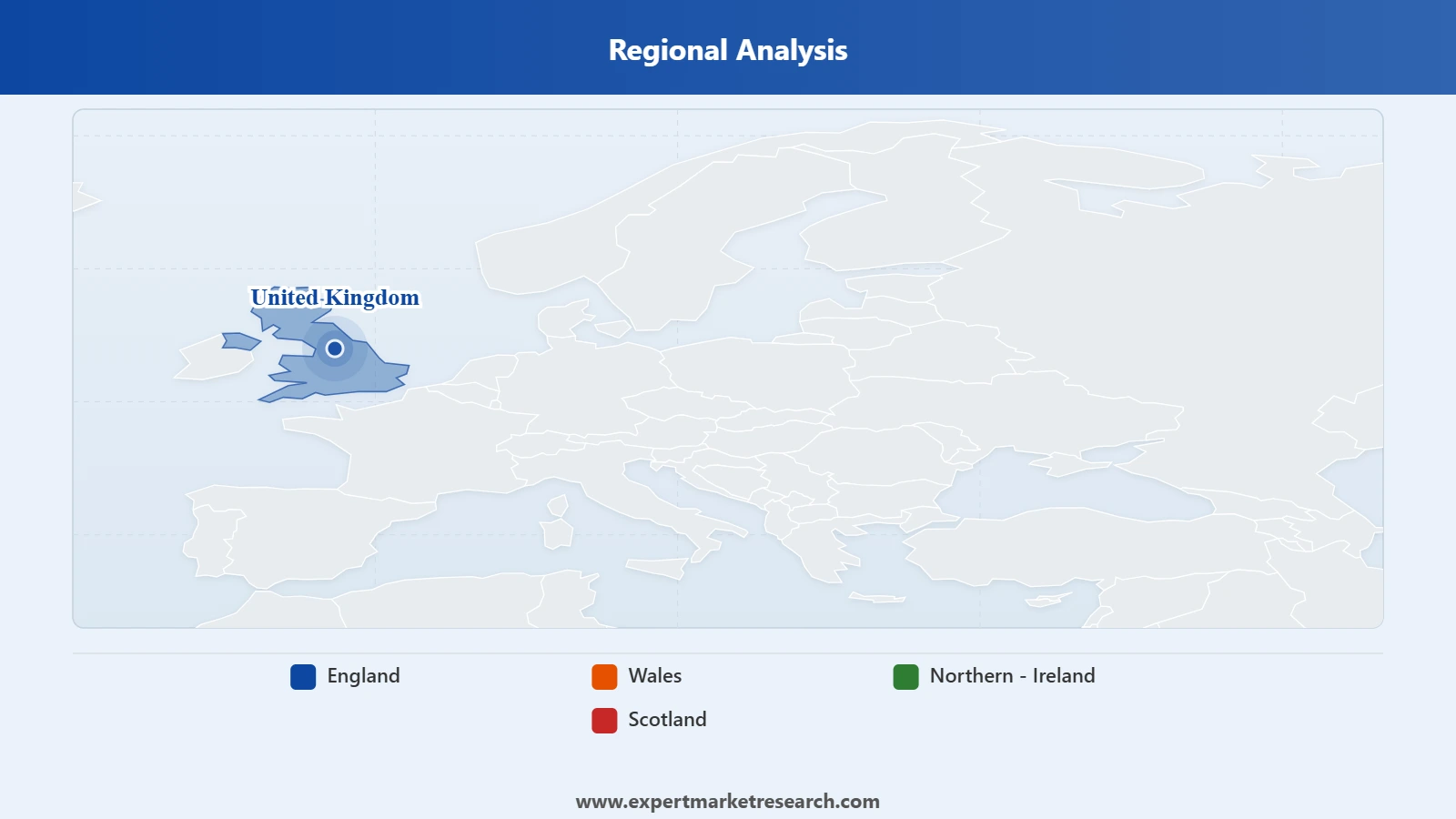

Market Breakup by Region

Key Insight: England dominates the UK snacks market, accounting for approximately 78% of total market revenue, driven by its large population base, high urban density, and concentration of major retail chains and distribution infrastructure. England is also the fastest-growing UK region, projected to expand at a CAGR of 10.2% over the forecast period, anchored by rising consumer disposable incomes, particularly in London and the South East, and increasing appetite for premium, savoury, and innovative snack formats. Scotland represents the second-largest regional market, with strong demand for both traditional confectionery formats and newer health-oriented snack options driven by a health-aware urban consumer base in Edinburgh and Glasgow. Wales and Northern Ireland are smaller but stable regional markets that benefit from the same distribution networks and brand availability as their larger counterparts, with both regions showing growing interest in clean-label and locally produced snack brands.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Type

Within the type segmentation, Confectionery Snacks hold the dominant share of the UK snacks market revenue, reflecting Britain's deep cultural affinity for chocolate and confectionery as everyday indulgence and gifting products. The dominance of Mondelez International's Cadbury brand, alongside Mars's strong confectionery portfolio and Nestle's KitKat, Rowntrees, and Aero brands, ensures consistent high-volume confectionery snack sales across all UK retail formats. Bakery Snacks, including the biscuit category where McVitie's (Pladis) and Cadbury hold leading positions, represent the second-largest revenue contributor, with premium and natural biscuit ranges growing at an accelerated rate.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Distribution Channel

Within the distribution channel segmentation, Hypermarkets and Supermarkets command the dominant share of UK snacks revenue, consistent with the central role of weekly grocery shopping at major retail chains in British household provisioning. The online channel is gaining meaningful share, particularly in premium and specialist snack categories where discovery and subscription models drive consumer engagement. Convenience store channels maintain strong performance in impulse-format, single-serve, and on-the-go snack categories, particularly in high-footfall urban locations across England where commuting and lunchtime snacking patterns generate consistent daily demand.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

England is the overwhelmingly dominant UK snacks market, contributing approximately 78% of total national snacks revenue and recording the strongest regional growth trajectory at a CAGR of 10.2% over the forecast period. The combination of England's large and economically diverse population, the concentration of UK snack retail headquarters and distribution networks, and rising consumer spending power across key markets including London, Manchester, Birmingham, and Bristol collectively underpin this dominance. Savory snacking is particularly strong in England, where Walkers crisps, Pringles, and private label crisp ranges command consistent weekly household purchase volumes. The online snacks retail segment is also most developed in England, where grocery delivery infrastructure and consumer digital adoption are most advanced, creating rapid growth opportunities for both established and challenger snack brands.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Scotland is the second-largest UK snacks regional market, with a health-conscious urban consumer base in Edinburgh and Glasgow showing growing preference for premium, artisan, and natural snack products alongside traditional confectionery formats. Convenience stores and petrol station forecourts serve as critical snack distribution channels in Scotland's rural areas, where supermarket access is more limited. Wales and Northern Ireland represent smaller but stable snacks markets, with distribution concentrated through major supermarket chains including Tesco and Lidl and strong consumer demand for both confectionery and bakery snack formats. Both regions are showing early-stage growth in plant-based and clean-label snacks as consumer health awareness increases, supported by the same UK-wide product launches by major brands including Nestle, PepsiCo, and Mondelez.

The United Kingdom Snacks Market is dominated by a small number of global food conglomerates whose brands command the majority of retail shelf space and consumer loyalty across all UK snack categories. PepsiCo's Walkers brand is the most recognized crisps brand in the UK, while Mondelez International's Cadbury range holds the leading position in confectionery snacking. The completion of the Mars-Kellanova acquisition in December 2025 adds a significant new multi-category competitive force, with Pringles joining Mars's existing chocolate and confectionery brands to create a broader UK snacking portfolio.

Competition in the UK snacks market is increasingly influenced by regulatory dynamics, particularly the UK Government's High Fat, Sugar, and Salt (HFSS) restrictions on product placement and promotions in large retailers, which have prompted manufacturers to invest in reformulated and better-for-you product ranges. Smaller and challenger brands are carving out growing niches in premium, organic, and plant-based snacking, leveraging online channels and health-focused retail partnerships to build consumer awareness and trial outside the traditional supermarket snack aisle.

Founded in 1965 and headquartered in Purchase, New York, PepsiCo operates the Walkers brand, the UK's most iconic crisps and snacks label, through its Frito-Lay international division. Walkers commands dominant shelf space across UK supermarkets and convenience stores and is sold in numerous formats including classic crisps, baked varieties, Wotsits, and Quavers. PepsiCo's UK strategy includes expanding its portfolio of baked and lower-fat snack options to address growing consumer health consciousness while sustaining high-volume sales of its core flavored crisps range.

Founded in 2012 as a Kraft Foods spin-off and headquartered in Chicago, Illinois, Mondelez International is one of the most significant snack companies in the UK through its Cadbury chocolate brand, as well as biscuit brands including Oreo, Ritz, Belvita, and Mikado. Cadbury holds an unparalleled position in British consumer loyalty, particularly in confectionery and chocolate snacking, with Dairy Milk and Roses being consistent top-selling UK snack products. Mondelez continues to invest in premium chocolate and biscuit innovation in the UK while also responding to regulatory pressures through HFSS-compliant product reformulations.

Founded in 1906 as Kellogg Company and rebranded as Kellanova in 2023 following the separation of its cereal business, Kellanova was headquartered in Chicago, Illinois, and operated key UK snack brands including Pringles (produced at its Belgian facility and widely distributed in UK retail), Pop-Tarts, Cheez-It, and RXBAR prior to its December 2025 acquisition by Mars Incorporated. Under Mars Snacking, these brands will continue to be developed for the UK market, with Pringles in particular maintaining its position as one of the leading premium crisp and snack brands across British supermarkets and convenience channels.

Founded in 1856 and headquartered in Golden Valley, Minnesota, General Mills operates in the UK snacks market through brands including Nature Valley granola bars, Fibre One, Old El Paso snacking formats, and Larabar, serving the growing health-oriented UK consumer segment seeking nutritious, natural, and convenient snacking options. Nature Valley is particularly well-distributed across UK supermarkets and convenience stores as a leading cereal bar brand, benefiting from strong consumer associations with wholesome ingredients and an active outdoor lifestyle. General Mills' UK strategy emphasizes natural ingredient formulations and HFSS-aware product development to maintain retail placement and consumer relevance.

Other key players in the market are Nestle S.A., Grupo Bimbo S.A.B. de C.V., The J.M. Smucker Company, Tyson Foods Inc., Mars Incorporated Inc., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Looking to build or grow your presence in the United Kingdom's dynamic snacks market? Our 2026-2035 report delivers comprehensive market sizing, category-level forecasts, regional growth dynamics across England, Scotland, Wales, and Northern Ireland, and in-depth competitive intelligence on leading players from PepsiCo's Walkers to Mars Snacking and Mondelez International's Cadbury. Whether you are a snacks manufacturer, UK retailer, private label developer, or investor, this report provides the data-driven foundation for confident strategic decisions. Download your free sample today and uncover the key opportunities driving the UK snacks market forward through 2035.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 55.02 Billion.

The market is projected to grow at a CAGR of 3.30% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 76.12 Billion by 2035.

The different types of snacks in the market are bakery snacks, confectionery snacks, frozen snacks, and fruit snacks, among others.

The major regions covered in the market report are England, Wales, Northern – Ireland, and Scotland.

The different distribution channels in the market are hypermarkets/supermarkets, convenience stores, and online channels, among others.

The key market players are Pepsico, Inc., Mondelez International Inc., Kellanova, General Mills, Inc., Nestle S.A., Grupo Bimbo S.A.B. de C.V., The J.M. Smucker Company, Tyson Foods, Inc., and Mars Incorporated, Inc., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.