Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

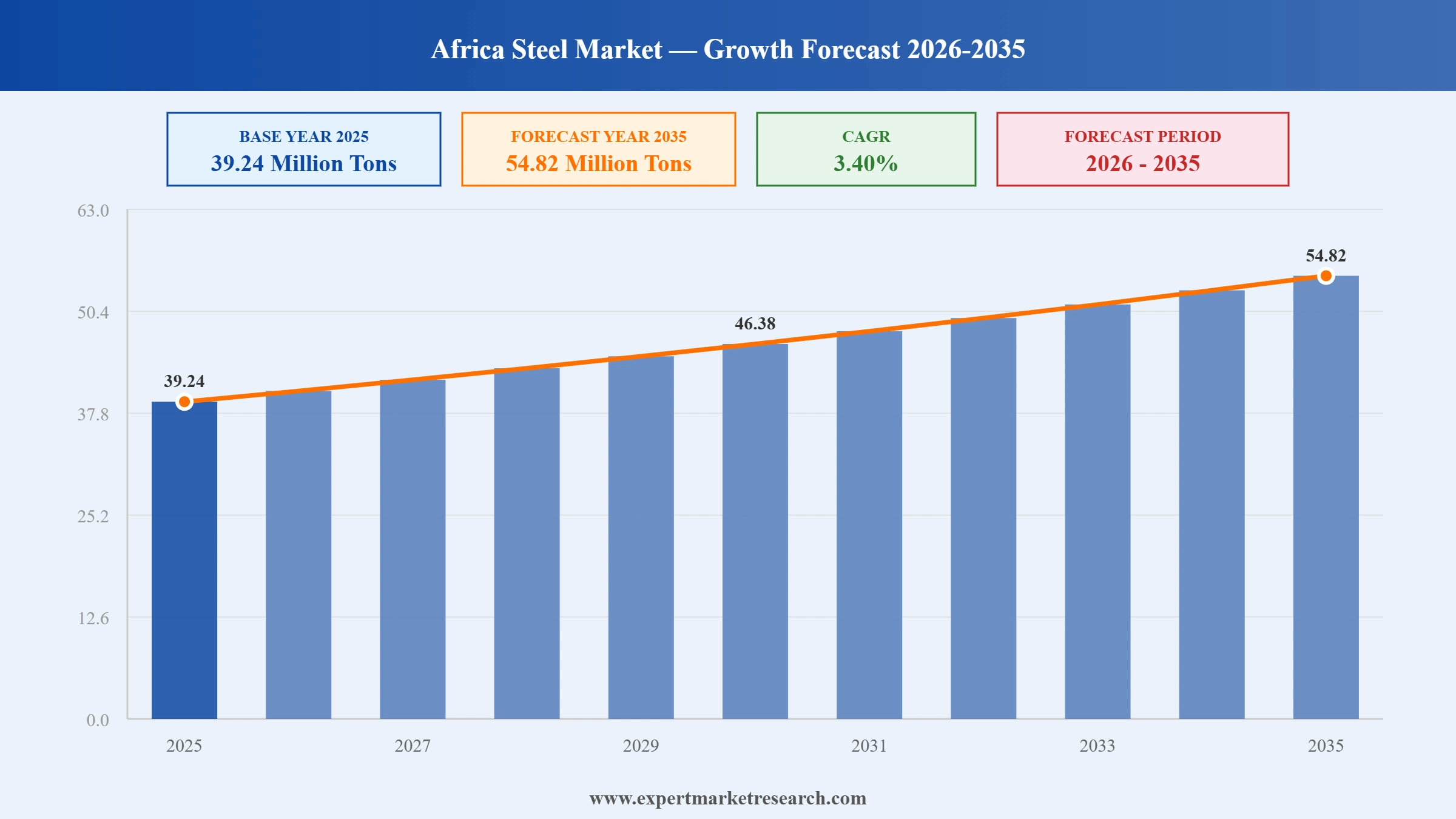

The Africa steel market reached a volume of 39.24 Million Tons at 2025 and is projected to expand at a CAGR of around 3.40% during the forecast period of 2026-2035. Lifted by accelerating infrastructure spending, large-scale construction projects across South Africa, Egypt, and Nigeria, rising automotive assembly, and growing investments in renewable energy and low-carbon steelmaking, the market is expected to reach 54.82 Million Tons by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Africa's steel industry is in the middle of a structural reset. Trade safeguard reviews, mega-scale Chinese and Japanese capital commitments, regional production partnerships, and a deliberate push toward low-carbon technologies are all converging at once. The past 18 months have delivered more decisive moves than the previous five years combined, and the direction is clear: more local production, less import dependence, and a steady shift toward sustainable steelmaking.

In July 2025, South Africa notified the WTO's Committee on Safeguards that it had opened an investigation into specific flat-rolled iron and non-alloy steel imports. The probe is set to reshape import dynamics, local pricing, and competitive positioning across the Africa steel market, particularly for flat steel categories where domestic producers have lost share to lower-cost Asian imports.

In May 2025, Zimbabwe Iron and Steel Company (Zisco) and Dinson Iron & Steel Company signed a strategic partnership to coordinate steel production in Zimbabwe. The deal aims to lift output, generate jobs, and revive the country's long-dormant steel industry by combining each party's manufacturing strengths and complementary product focus.

In September 2024, South Africa's Industrial Development Corporation and China's Hebei Iron & Steel Group signed a memorandum of understanding to jointly develop a major steel plant valued at USD 4.5 billion. Planned in two phases, the project is positioned to lift local production, drive competition, lower prices, and support meaningful job creation across the South African steel ecosystem.

In April 2024, the Libyan Iron and Steel Company and Italy's Danieli signed a memorandum of understanding to build a direct reduction plant inside LISCO's existing facilities. The plant is designed to produce 2 million tons per year of sponge iron and hot briquetted iron, materially shifting the supply dynamics of the North African steel market.

African governments are actively supporting domestic steel production to cut import dependence and accelerate industrialisation. Nigeria's revival push for the Ajaokuta Steel Plant and the development of the Stellar Steel Plant in Ogun State, alongside South Africa's R812 billion infrastructure programme, are creating multi-year demand pipelines that anchor private investment decisions across the Africa steel industry.

Innovation is changing how steel gets made on the continent. Electric arc furnace adoption and low-carbon initiatives like XCarb are enabling more energy-efficient, sustainable production. The XCarb innovation fund committed over USD 150 million globally in October 2022 to support decarbonisation technologies, including a stake in Boston Metal's molten oxide electrolysis route, signals where the Africa steel market trends are heading.

The continent's construction sector is the dominant steel consumer, particularly across South Africa, Nigeria, Egypt, and Kenya. Flagship projects such as Egypt's New Administrative Capital, Kenya's LAPSSET corridor, and large-scale urban housing programmes are pulling significant volumes of rebar, structural steel, and long steel products, and public-private partnerships are accelerating delivery cycles.

South Africa remains the continent's automotive hub, attracting global OEMs for local assembly and regional export. Rising vehicle production and component manufacturing are increasing demand for high-strength and coated steel, while EV adoption is driving uptake of advanced alloy grades. Morocco and Egypt are also expanding their automotive supply chains, broadening the addressable specialty steel base.

Egypt's steel sector is scaling at speed. Beshay Steel's 1.5 million square metre Egyptian footprint exemplifies the country's industrial diversification push, with active investments across flat steel, HR and CR coils, and galvanised lines. The capacity is positioned to serve both domestic infrastructure and the growing appliance, machinery, and automotive export segments out of Egypt.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The report by Expert Market Research titled "Africa Steel Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

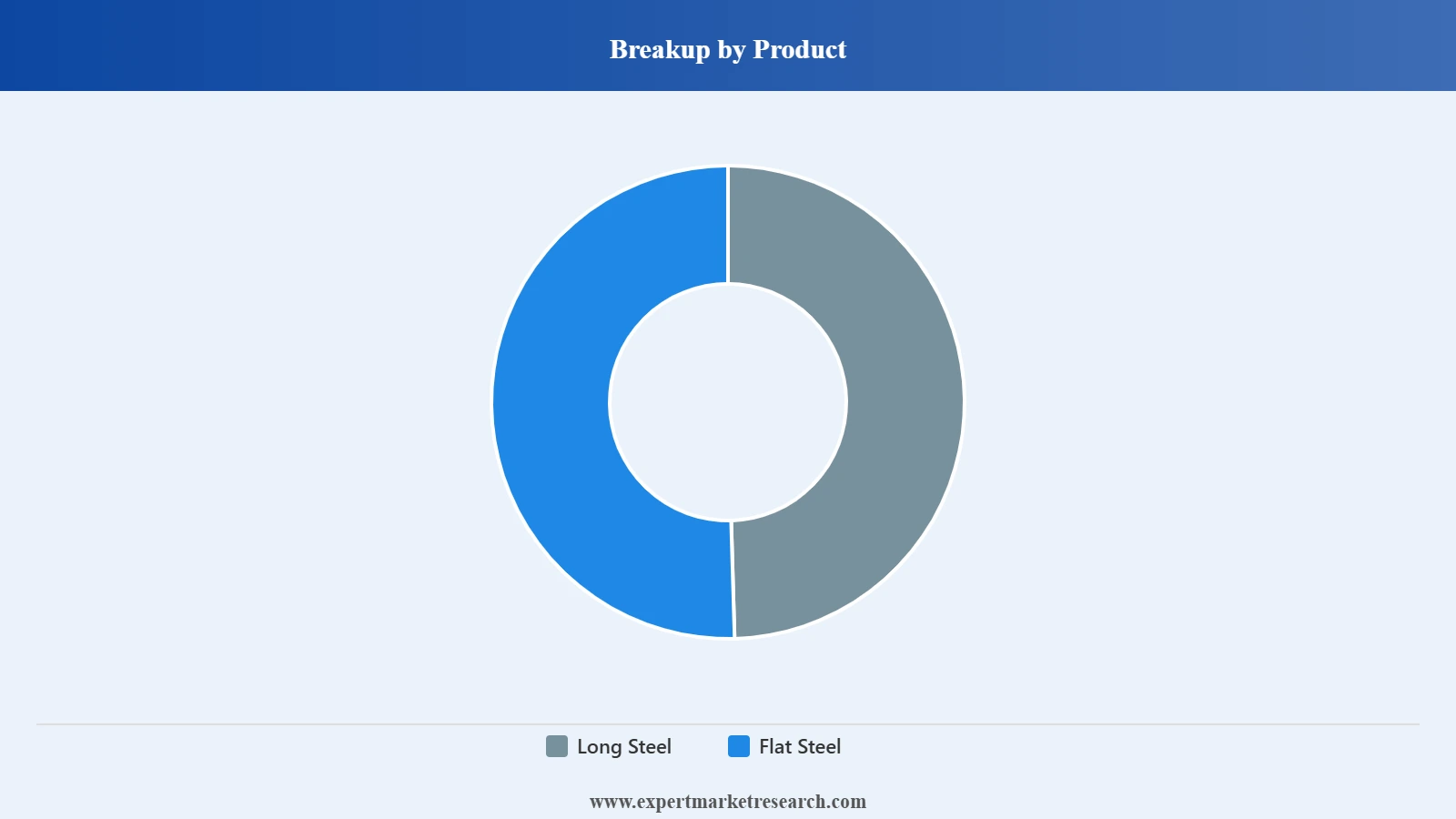

Market Breakup by Product

Key Insight: Long steel currently dominates the Africa steel market by volume, with rebars, wire rods, and structural sections supporting the bulk of construction, manufacturing, and automotive demand. The category benefits directly from large infrastructure pipelines and local procurement rules that favour domestic rolling mills. Flat steel, including HR and CR coils, colour coated sheet, and welded pipes, is scaling faster than long steel on the back of automotive, appliance, and machinery investments across Egypt and Morocco. Government infrastructure budgets, urbanisation, renewable energy projects, and AfCFTA-led trade liberalisation are all combining to widen both the supply base and demand envelope of the Africa steel industry.

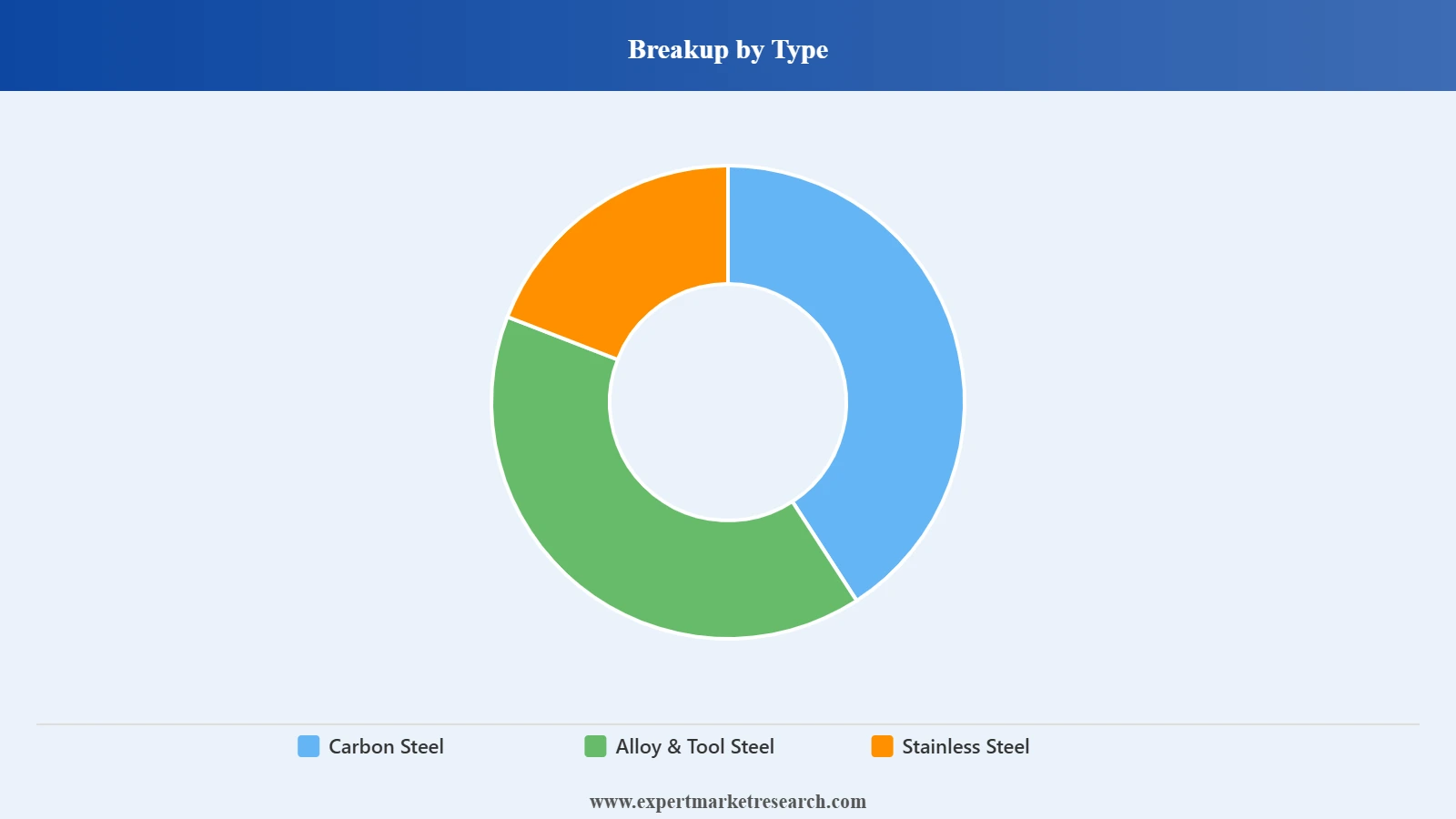

Market Breakup by Type

Key Insight: Carbon steel leads the Africa steel market by both volume and revenue, thanks to its breadth of application across construction, pipelines, and general industrial use, and its cost advantage over specialty grades. Alloy and tool steel sit in a smaller but rapidly expanding bucket tied to automotive, energy, and industrial machinery applications. Stainless steel is the fastest-growing type by share, supported by demand from food processing, pharmaceutical, EV, and renewable energy applications across South Africa, Egypt, and Morocco. Local production capacity for specialty grades remains thin, which keeps imports relevant but also signals an opportunity for new entrants and technology partnerships.

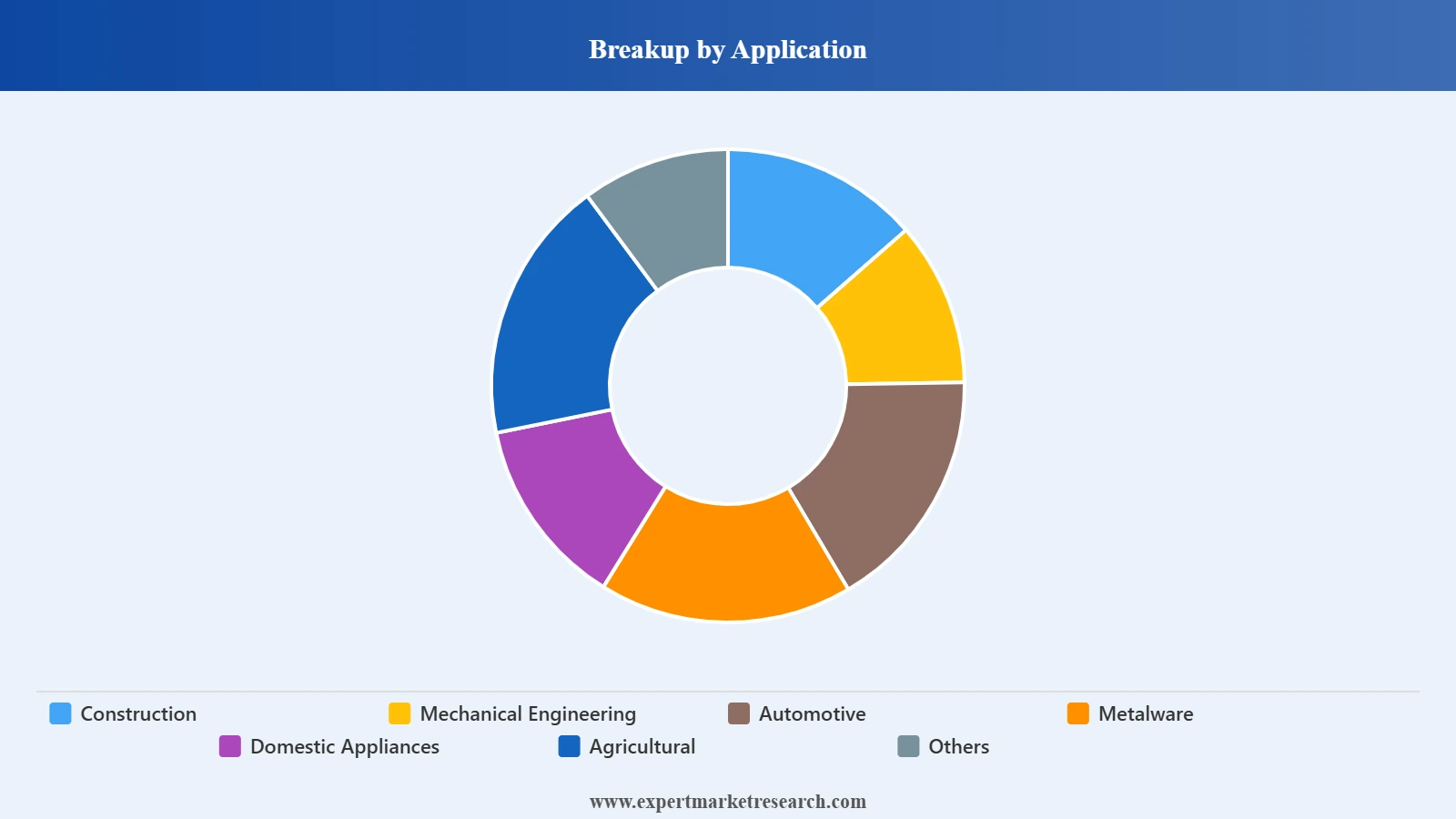

Market Breakup by Application

Key Insight: Construction captures the largest share of the Africa steel market, lifted by sustained infrastructure spending, residential housing rollouts, and continental mega-projects. Automotive and mechanical engineering are the fastest-growing application clusters, particularly across South Africa, Morocco, and Egypt where global OEMs continue to expand local assembly footprints. Metalware, domestic appliances, and agricultural applications add meaningful breadth, supported by the rise of regional manufacturing and rural mechanisation programmes. Combined, these application segments give the Africa steel industry a more diversified demand profile than at any point in its recent history.

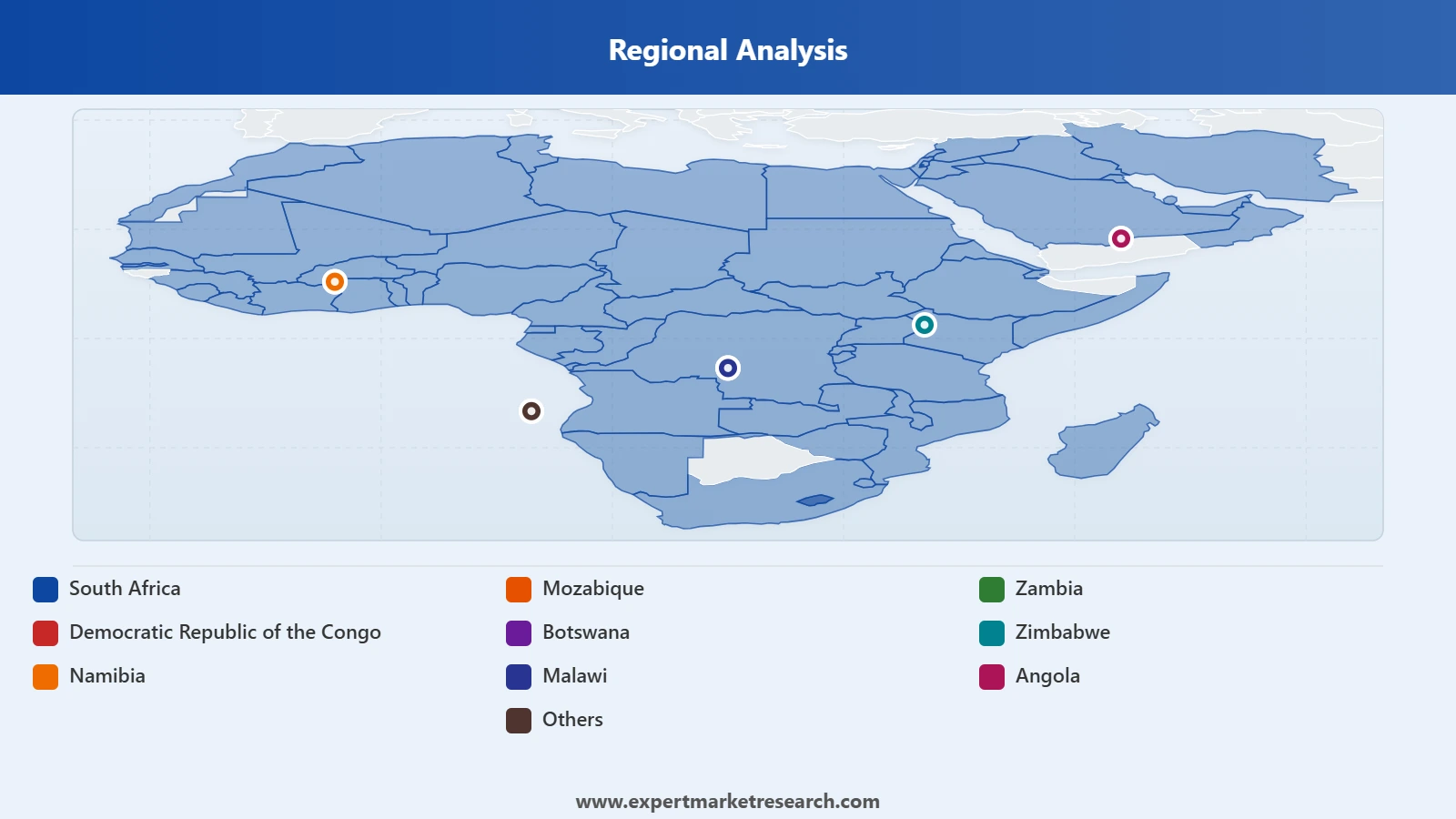

Market Breakup by Region

Key Insight: South Africa remains the largest producer and consumer of steel on the continent, supported by its mature manufacturing base, deep value chain, and aggressive infrastructure spending. Nigeria, Egypt, and Morocco are positioning as fast-growing regional hubs, each leveraging policy support, international partnerships, and local capacity buildouts. Mozambique, Zambia, DRC, Botswana, Zimbabwe, Namibia, Angola, and Malawi together represent a meaningful long-tail demand base, particularly around mining-linked construction and infrastructure spending. Country-level diversity is one of the defining characteristics of the Africa steel market and creates parallel opportunities for both regional producers and global suppliers.

By Product, Long Steel dominates the market due to large-scale infrastructure and housing demand across the continent

Long steel products, including rebars, wire rods, and structural sections, hold the dominant share of the Africa steel market by volume. Demand is concentrated around infrastructure mega-projects, transportation networks, energy grid expansion, and the housing programmes that anchor government spending across South Africa, Nigeria, and Egypt. Local procurement policies favour domestic rolling mills, and the category benefits from a relatively shorter value chain that keeps producers cost-competitive against imports. Affordable housing initiatives and ongoing urban infrastructure investment ensure long steel will remain a structural anchor of the African steel industry for the foreseeable future.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Flat steel, including HR and CR coils, colour-coated sheet, and welded pipes, is the fastest-growing product category. Investments in automotive, appliance, and machinery production across Egypt, Morocco, and South Africa are driving most of the growth, and AfCFTA-enabled trade is accelerating both production upgrades and export diversification. Rising middle-class consumption is amplifying demand for galvanised and pre-painted flat steel used in white goods, light commercial vehicles, and construction cladding.

By Type, Carbon Steel captures the dominant share due to versatility and cost efficiency across applications

Carbon steel dominates the Africa steel market by type. Its cost efficiency and broad applicability across construction, pipelines, and general industrial use make it the workhorse grade for almost every major demand driver on the continent. Structural beams, reinforcements, and foundational frameworks all rely heavily on carbon steel, and the category gets a steady demand floor from government-backed urban and transport infrastructure investment that shows no signs of slowing.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Stainless steel and alloy steel together form the fastest-growing type cluster, lifted by demand from automotive, food processing, pharmaceuticals, and renewable energy applications. High-strength and corrosion-resistant grades are increasingly required, and partnerships with international producers and technology transfers are gradually improving local manufacturing capability. The shift toward EV production in North and South Africa, combined with renewable energy buildouts, supports a structurally higher trajectory for specialty steels across the Africa steel industry.

By Application, Construction holds the dominant share, anchored by infrastructure mega-projects and housing programmes

Construction drives the overall steel demand profile of the Africa steel market. Urban expansion, residential housing rollouts, and mega-projects such as Egypt's New Administrative Capital, Kenya's LAPSSET corridor, and Nigeria's transport infrastructure programme are the most visible drivers, but the everyday pipeline of commercial buildings, bridges, and public works adds an equally important steady stream of demand. Public-private partnerships and international funding from the AfDB, World Bank, and Chinese policy banks are accelerating project delivery, and local content policies favour domestic production, reinforcing the case for long steel and flat steel demand simultaneously.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Automotive and manufacturing represent the fastest-growing application clusters across the Africa steel market. Vehicle assembly in South Africa, Morocco, and Egypt, combined with appliance production in North and East Africa, is pulling demand for alloy, high-strength, and stainless grades. EV adoption, automotive lightweighting, and high-specification steels are reshaping the application mix, and SMEs in the metalware and domestic appliance categories are scaling export potential under AfCFTA-led regional integration.

South Africa dominates the market due to a mature production base, deep value chain, and robust infrastructure programmes

South Africa leads the Africa steel market by both production volume and consumption share. The country generated around 4.063 million tons of crude steel between January and October 2024 alone, anchored by a mature industrial base, a deep network of suppliers, and consistent government infrastructure spending channelled through the National Treasury's multi-year public works programme. The September 2024 USD 4.5 billion MoU between the Industrial Development Corporation and Hebei Iron & Steel Group signalled the scale of foreign capital flowing into the local production base. South African producers are also at the forefront of EAF adoption and low-carbon steelmaking initiatives, which is positioning the country as the most ESG-compliant production hub on the continent.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Nigeria is the fastest-growing steel market in Africa, lifted by a sustained push to revive long-dormant production assets and build new ones. The operationalisation of the Ajaokuta Steel Plant, combined with the USD 400 million Stellar Steel Plant project in Ogun State that targets over 3,500 jobs, is reshaping Nigeria's steel supply landscape. Domestic raw material availability, supportive government policies, and a deep infrastructure project pipeline are all converging to lift consumption. Import reduction initiatives further strengthen the case for local production, and Nigeria is expected to close the gap with South Africa as a continental production hub over the forecast period.

The Africa steel market is highly competitive and is shaped by the parallel presence of global steel giants and emerging local producers, each chasing opportunities across construction, automotive, and renewable energy demand. Producers are increasingly focused on technological innovation, sustainable production methods, and strategic partnerships that can match the continent's growing infrastructure appetite. Electric arc furnace technology and low-carbon production methods are helping firms cut operational costs and shrink environmental footprints simultaneously.

Investments in local rolling mills, downstream processing capacity, and specialty steel grades for automotive and energy use are giving the leading Africa steel market players room to differentiate beyond price competition. Urbanisation, large-scale infrastructure programmes, and renewable energy rollouts represent the most material growth opportunities for both domestic and international participants. The African Continental Free Trade Area (AfCFTA) framework adds another dimension, allowing producers to optimise logistics, scale regional exports, and offer tailored solutions for both local and international buyers across the steel value chain.

Established in 1968 and headquartered in Pohang, South Korea, POSCO is a global steel leader serving the Africa steel market with advanced steel solutions. The company focuses on high-strength and specialty grades for construction, automotive, and renewable energy applications. POSCO supports regional infrastructure projects through local partnerships and sustainable production practices, and continues to expand its product portfolio to address the evolving industrial demand profile across the continent.

Founded in 1970 and based in Spain, Acerinox is a leading stainless steel producer serving Africa's industrial, construction, and energy sectors. The company combines innovative production technologies, corrosion-resistant steel grades, and flexible supply chain solutions to address regional demand. Through strategic distribution networks and partnerships, Acerinox covers the growing need for durable steel products across automotive, infrastructure, and appliance manufacturing in the African steel market.

Established in 2012 and headquartered in Tokyo, Japan, Nippon Steel supplies high-quality flat and long steel products to Africa's construction, mechanical engineering, and automotive sectors. The company leverages advanced manufacturing know-how, sustainable steelmaking processes, and technology transfer programmes to lift local capacity. Its tailored solutions address regional infrastructure and industrial requirements while reinforcing environmentally responsible production practices across the value chain.

Founded in 1914 and based in Helsinki, Finland, Outokumpu specialises in stainless and high-performance steels serving Africa's automotive, industrial, and energy sectors. By offering corrosion-resistant and recyclable steel grades, Outokumpu supports sustainable construction and industrial projects across the continent. The company continues to invest in regional partnerships and innovation-driven R&D to address evolving market demand and improve both operational efficiency and environmental performance.

Other key players in the Africa steel market include African Industries Group, Egyptian Steel Group, El Marakby Steel, The Libyan Iron and Steel Company, Dinson Iron & Steel Company (Private) Limited, Best Angola Metal, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Get the latest perspective on the Africa steel market with our 2026 report. Track the rise of low-carbon steelmaking, the foreign capital pouring into local capacity, and the segment-level shifts reshaping demand across construction, automotive, and energy. Whether you are a steel producer planning a regional expansion, an EPC contractor sizing rebar requirements, or an investor weighing exposure to African industrialisation, the report delivers the clarity you need. Download your free sample now and explore the opportunities reshaping the thriving Africa steel industry.

Australia Steel Market

Stainless Steel Market

Electrical Steel Market

Saudi Arabia Structural Steel Market

Asia Pacific Stainless Steel Market

Upto 15% Off

USD

$3499 $3149

$5599 $5039

$6999 $5949

$8459 $7190

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the Africa steel market reached an approximate volume of 39.24 Million Tons.

The market is projected to grow at a CAGR of 3.40% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach 54.82 Million Tons by 2035.

Stakeholders are investing in local manufacturing, implementing low-carbon technologies, expanding specialized steel portfolios, forming regional partnerships, enhancing supply chains, and leveraging trade agreements to capture Africa’s growing steel demand.

Key trends aiding market expansion include the increased attention to locally produced steel, expansion of steel manufacturers in the region, and development of steel alloys for improved properties.

Countries considered in the market are South Africa, Mozabique, Zambia, Democratic Republic of the Congo, Botswana, Zimbabwe, Namibia, Malawi, Angola, among others.

Steel is an alloy of iron and carbon which offers properties like tensile strength, yield strength, malleability, and toughness.

The different types of steel in the market are carbon steel, alloy & tool steel and stainless steel.

The various application of steel in the market are construction, mechanical engineering, automotive, metalware, domestic appliances and agricultural, among others.

The key players in the market include POSCO Co., Ltd., Acerinox S.A., Nippon Steel Corporation, Outokumpu Oyj, African Industries Group, Egyptian Steel Group, El Marakby Steel, The Libyan Iron and Steel Company, Dinson Iron & Steel Company (Private) Limited, and Best Angola Metal, among others.

High raw material costs, infrastructure constraints, energy inefficiencies, and regulatory hurdles, coupled with intense competition and fluctuating global steel prices, are the main challenges facing Africa steel market participants.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product |

|

| Breakup by Type |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 3,499

USD 3,149

tax inclusive*

Single User License

One User

USD 5,599

USD 5,039

tax inclusive*

Five User License

Five User

USD 6,999

USD 5,949

tax inclusive*

Corporate License

Unlimited Users

USD 8,459

USD 7,190

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.