Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

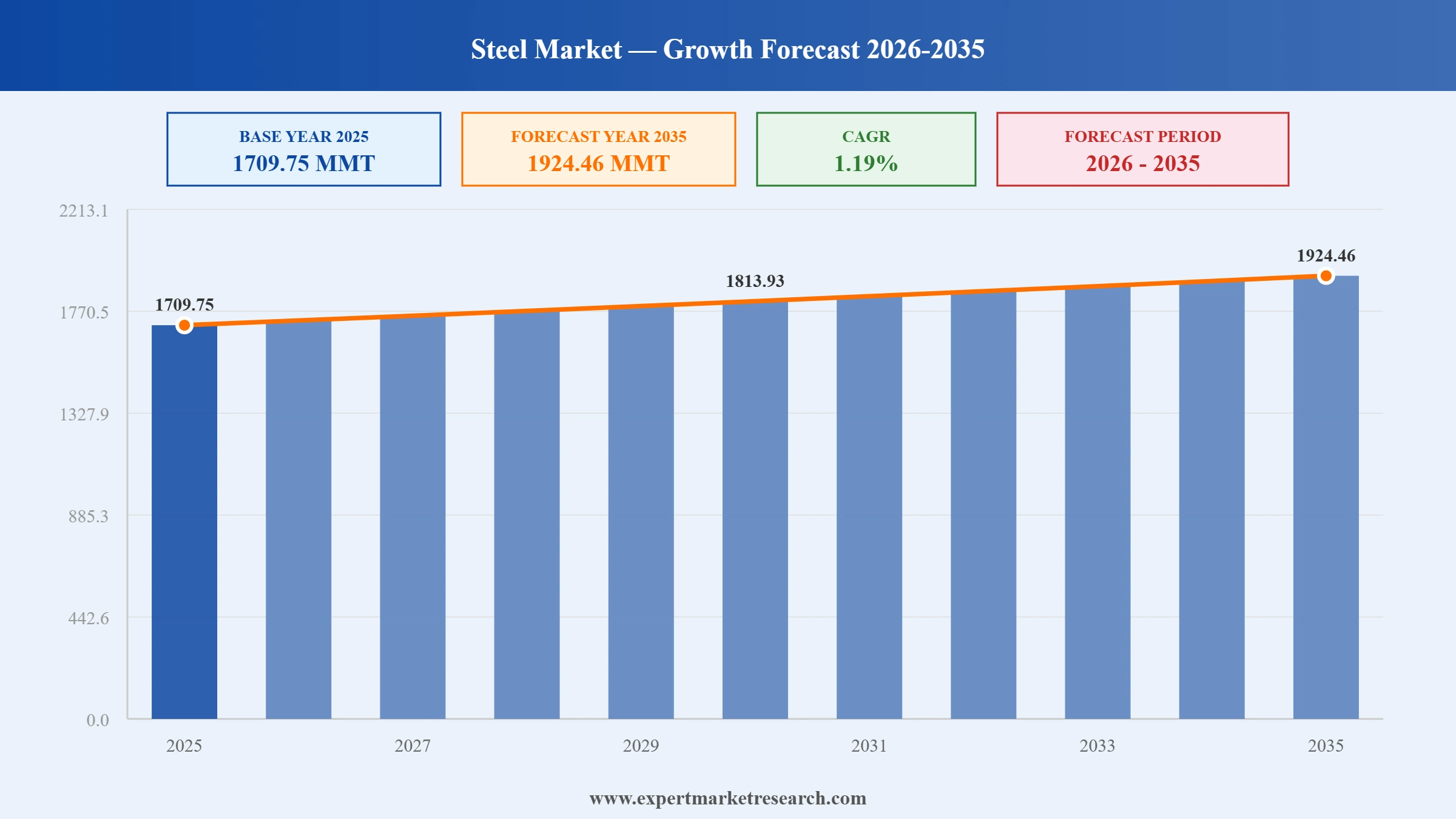

The global steel market reached a volume of 1709.75 MMT in 2025 and is projected to expand at a CAGR of 1.19% through 2035. The market is further expected to achieve a volume of 1924.46 MMT by 2035. The increased investment in infrastructure of renewable energy plants, electric cars, and industrial reshoring programs continue to drive the need for more advanced types of steel, prompting manufacturers to increase their production of specialized products.

Modernization through technological advancement, sustainability through investments towards reduced carbon emissions, and innovation in terms of improved materials continue to define the development trajectory of the global steel market. One of the latest major developments was the move by ArcelorMittal that revised its decarbonization strategy, targeting 10% carbon-intensity reduction by 2030 while maintaining net-zero ambitions, in April 2026. It is worth noting that the move is triggered by an increased demand from the industry for lower carbon emission steels. Based on data from the World Steel Association, global crude steel production surpassed the 1.85 billion ton mark in 2025.

The use of high-end and specialty-grade steel in order to boost the profit margin and improve customer satisfaction is among the key strategies adopted by steel market players. Automotive companies are now interested in high-strength steels that allow vehicles to become lighter while still maintaining their strength. On the other hand, various energy infrastructure projects are becoming potential markets for the provision of corrosion-resistant and highly durable steel materials. The other trend involves the integration of digital production technology and AI-enabled quality control software solutions within factories. In February 2026, India approved major steel sector investments and policy initiatives to enhance sustainable domestic steel production.

On the other hand, there are two separate growth factors motivating the increased demand in the steel market. Governments worldwide are investing in the development of transportation corridors, industrial zones, bridges, and infrastructure related to power transmission, thereby creating demand for large quantities of steel products. Secondly, manufacturers are engaging in localized production in the wake of recent geopolitical turmoil in the market, which leads to new production facilities for steel products.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Global Steel Market Report Summary | Description | Value |

| Base Year | MMT | 2025 |

| Historical Period | MMT | 2019-2025 |

| Forecast Period | MMT | 2026-2035 |

| Market Size 2025 | MMT | 1709.75 |

| Market Size 2035 | MMT | 1924.46 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 1.19% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 2.41% |

| CAGR 2026-2035 - Market by Country | India | 2.89% |

| CAGR 2026-2035 - Market by Country | China | 2.40% |

| CAGR 2026-2035 - Market by Product | Flat Steel | 2.46% |

| CAGR 2026-2035 - Market by Application | Domestic Appliances | 2.72% |

| Market Share by Country 2025 | China | 49.50% |

AM/NS India developed patented Zagnelis Protect coated steel, improving corrosion protection, localization, and modern auto production processes. Steel manufacturers can purchase specialized coated steel for cars as an alternative to importing foreign products due to increasing demand for EVs and automobiles.

Indian and United Kingdom governments settled on steel trade issues, ensuring that their FTA is implemented from July 15, 2026, while protecting most of India’s steel exports. Exporters can benefit from the trade agreement to increase sales abroad, accelerating the steel market growth.

The partnership between Primetals Technologies and WISCO resulted in the installation of six-strand casting technology for production of defect-free rail steel. Steel manufacturers have an opportunity to embrace modern casting technologies in order to enhance product quality and minimize waste, among other benefits.

JSW Steel initiated the construction of a new Odisha plant to increase production capacity in response to increased demand for its products. Organizations therefore have an opportunity to grow through investments in greenfield capacity addition, boosting development in the steel market.

Steel decarbonization is one of the biggest growth driving factors within the global steel market. The growing emphasis on sustainable industries means that companies within the sector are investing heavily in technologies aimed at reducing emissions. Companies are now increasingly setting up electric arc furnace operations, green iron-making operations, and carbon capturing facilities. The Carbon Border Adjustment Mechanism of the European Union aims to reduce emissions intensity in the industry. On the other hand, in June 2026, Maharashtra sought six iron ore mines for Gadchiroli, accelerating plans for a INR 3 lakh crore green steel hub in India.

Large-scale infrastructure projects are driving significant demand for steel products across the globe. Governments are committing significant budgets to projects aimed at building transportation networks, developing urban centers, constructing energy projects, and establishing industrial hubs. Examples include the continued investment in United States. infrastructure programs under the Infrastructure Investment and Jobs Act, which calls for significant investment in bridges, railway lines, port facilities, and energy infrastructure. On the other hand, India is working on its National Infrastructure Pipeline, which involves various construction projects across multiple sectors, boosting the steel market expansion. In June 2026, MMRDA successfully launched a 252-metric-tonne steel span for Metro Line 2B above Central Railway tracks, showcasing advanced engineering execution.

The growing popularity of automotive applications is driving the development of new high-strength steel grades. Their application aims at improving vehicle safety, cutting weight, and boosting energy efficiency. High-strength steel grades are especially popular in the manufacturing of electric vehicles due to their lightness, which helps extend the driving range from the battery pack. The list of automotive steel grades offered by companies like ArcelorMittal and POSCO is expanding rapidly in response to the demand in the steel market. In March 2026, Tata Steel Nederland and Volkswagen advanced ultra-high-strength steel development, improving vehicle safety, corrosion resistance, and manufacturing energy efficiency.

The development of digital steelmaking is being driven by the implementation of AI, predictive maintenance, automation, and real-time monitoring systems, reshaping the entire steel market dynamics. Major steel producers are implementing smart manufacturing systems to boost production rates, save energy, and produce better-quality products. For instance, Tata Steel is investing in analytics and digital twin technology to increase production efficiency. Governments of several countries are implementing industrial modernization programs to support the adoption of Industry 4.0. Aligning with this trend, in June 2026, TechESteel introduced a digital platform offering transparent pricing, secure settlements, supplier verification, and financing solutions.

There are many emerging business opportunities being created due to the fast installation of renewable energy infrastructure, which provides new opportunities for steel market players that are providing their products for wind power, solar energy, and grid modernization. Steel for offshore wind farms needs corrosion-resistant material suitable for such harsh conditions, and according to policies on energy transition in Europe, China, and North America, there is increasing demand for renewable energy generation. Hence, companies are making specialized energy steels resistant to corrosion and long-lasting in use. In June 2026, Avaada planned 10.5 GW renewable additions, targeting 17.7 GW capacity within two years through secured projects.

The Expert Market Research's report titled “Global Steel Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

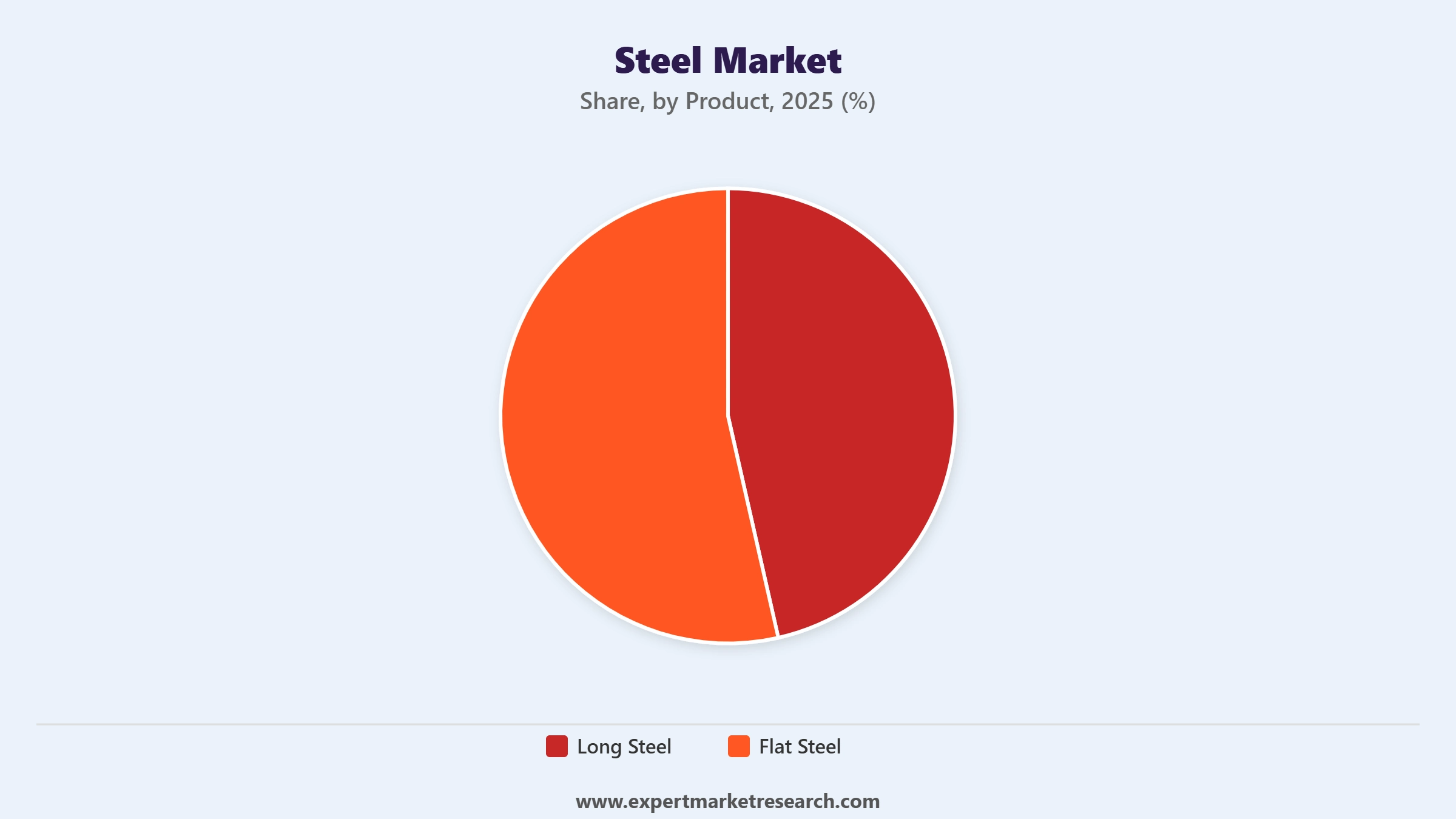

Market Breakup by Product

Key Insight: The steel market exhibits unique dynamics of growth in both categories of products. Flat steel continues to hold its dominant position due to its application in automotive production, industrial machinery manufacturing, packaging purposes, and engineering products where surface quality is important. However, long steel is seeing higher growth rates due to rapid developments in infrastructure, urbanization, renewable energy, and other projects in which such products can be used. Flat steel companies tend to concentrate more on improving their product quality and developing advanced technologies. In October 2025, Jindal India launched a USD 169 million steel facility, increasing capacity 60% and expanding coated products.

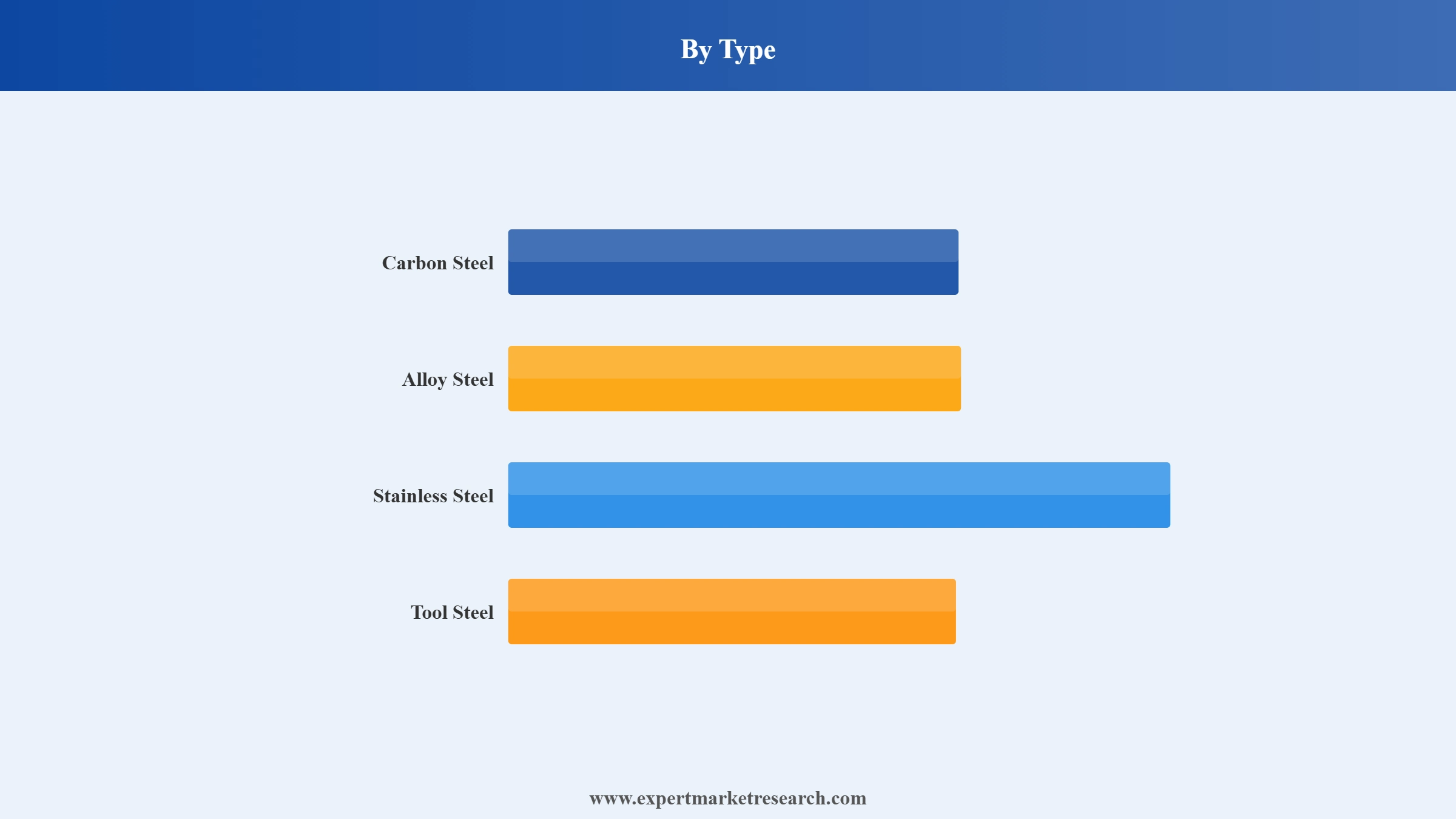

Market Breakup by Type

Key Insight: Every kind of steel fulfills a specific purpose within the steel market. The usage of carbon steel can be attributed to its cost-effectiveness and strength, making it ideal for large-scale construction and manufacturing purposes. In cases where extra strength and wear resistance are required, alloy steel plays a significant role. Stainless steel is gradually becoming popular since industries increasingly focus on rust resistance and durability of the equipment used. Tool steel is also useful within the industry in precision manufacturing and machining processes. In April 2026, Jindal Stainless expanded into retail and construction segments, strengthening downstream presence and customer reach.

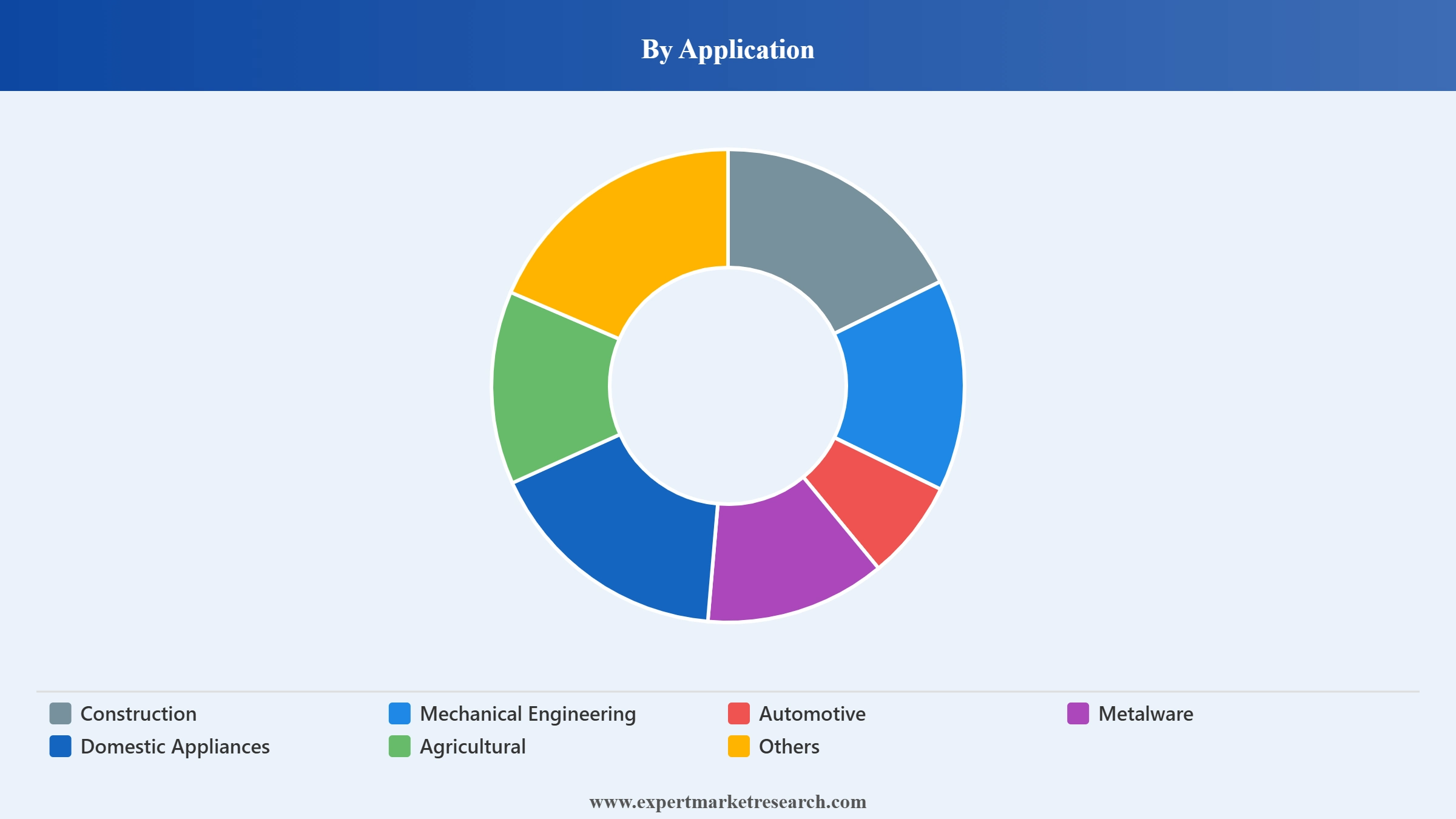

Market Breakup by Application

Key Insight: Demand in the steel market is influenced by the varied demands of industries. Construction and building activities are the biggest consumers because of continued infrastructure development projects. Mechanical engineers use steel in making machines that must be durable in their operations. Automotive industries are evolving with innovations in vehicle production and usage of light-weight materials. Metalware industries are benefiting from the availability of durable and easily producible metal. Agricultural machinery producers are finding it beneficial to use durable metals in their activities.

Market Breakup by Region

Key Insight: Regional trends of growth reflect diverse demand influences within the steel market. The largest steel consumer is the Asia Pacific, where demand for steel results from massive manufacturing activities, industrial development, and infrastructure work. In North America, the demand reflects manufacturing updates, along with initiatives for local production of steel. In Europe, there are demands for advanced steel products, environmental considerations, and industrial use. The Latin American market is characterized by demands associated with building activities, mining investments, and industrial expansion. Rapid growth is happening in the Middle East and Africa region.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By product, flat steel registers the largest share of the market due to manufacturing versatility

Flat steel makes up for the highest steel market share as it finds wide application in the automotive, machinery, ships, packaging, and construction sectors. It is preferred by manufactures due to its potential for precision engineering and product development as well as fabrication. Manufacturers of steel are developing high strength and coated products in order to accommodate changes in industry demand. The demand for flat steel is expected to rise from auto manufacturers due to increased demand for high-strength materials that increase safety and allow for electric car production. In June 2026, LME and SHFE announced the agreement to launch a cash-settled steel futures contract, expanding global market access.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Long steel is becoming the most rapidly growing segment because of increased investment in the construction of transportation infrastructure, commercial buildings, industrial buildings, and renewable energy facilities. Rebars, wire rods, and structural sections are experiencing increased demand from engineering companies. Governments of various countries focus on urbanization and development, which increases demand in the long steel market. Manufacturers develop larger capacity and new high-strength varieties to facilitate the construction of large-scale projects requiring long steel.

By type, carbon steel dominates the market due to affordability advantages

The carbon steel segment holds the largest share in the steel market due to factors such as its affordability, strength, and wide range of usage in construction, manufacturing, transport, and industry. This type of steel strikes the perfect balance of efficiency and cost effectiveness, which makes it the preferred choice for use in structural framework, equipment parts, pipeline construction, and fabrication. Industrial producers of steel are striving to enhance their efficiency and production processes for the purpose of satisfying demands of industrial buyers. Steel's popularity within emerging and developed countries guarantees consistent demand from several end-user segments. In June 2025, Tata Steel scheduled construction of its United Kingdom low-carbon steel plant from July 2025, targeting operations by 2027.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Growth in the stainless steel market is the most rapid among all types of steel due to increased demand from industries such as food processing, medicine, energy, transport, and advanced manufacturing. Due to the characteristics that stainless steel possesses including resistance to corrosion, durability, and so on, the need for this metal continues to grow as it proves to be highly suitable for applications in challenging environments. Specialized grades of stainless steel are currently being produced for specific needs within clean energy, industrial production, and consumer segments.

Construction applications lead demand growth through infrastructure development projects

Construction boasts the largest application share in the steel market since steel is one of the essential materials for the construction of commercial buildings, residential projects, industrial structures, bridges, and infrastructure development. The versatility of steel, its strength, and durability continue to be useful in handling more complicated construction projects. Governments and private firms are focusing on the development of modern infrastructure facilities, which is expected to fuel the growth of the market in this domain. Companies are developing new grades of steel, which enhance bearing capacities but help streamline the entire process of construction.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The automotive sector emerges as the fastest-growing application segment owing to the increased production of electric cars, trucks, railways, and transportation systems. There is a growing need among automobile companies to develop light-weight high-strength steel products, which can be used in automobiles without affecting their safety features. Several firms are also developing steel products in collaboration with automobile companies to suit future transportation needs. In August 2024, ArcelorMittal Europe introduced low-carbon steel deliveries using HVO and electric trucks, reducing transport emissions by 90%.

Asia Pacific secures the leading share of the market through industrial capacity expansion

The Asia Pacific region dominates the market for steel globally because of its huge manufacturing activities, vast investments made in infrastructure, and construction works. Industrial and construction projects in nations like China, India, Japan, and South Korea are contributing significantly towards the growth of steel demand. Steel manufacturers in the region are using state-of-the-art manufacturing technology and making investments in special grade steels. The presence of a lot of automotive, electronics, machinery, and construction companies only increases the region's dominance as far as steel products are concerned. In April 2026, Gerdau introduced a low-emission steel portfolio, supporting decarbonization goals across automotive and construction sectors.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Middle East and Africa steel market is growing at the fastest pace as the overall infrastructure is undergoing a diversification process, and governments are taking active steps to improve their industrial and energy sectors. Economic transformation plans involving manufacturing zones, logistics centers, renewable energy, and urbanization programs are resulting in increased demand for structural and specialized steel products. The production capacity of regional companies is on an expansion path; at the same time, these businesses are also attracting foreign investments.

Competitiveness in the global industry is shifting towards the production of green steel, high-end materials, digital manufacturing practices, and sustainable supply chains. Leading steel market players are making massive investments in electric arc furnace technology, hydrogen-based steel manufacturing processes, smart manufacturing capabilities, and premium steels to set themselves apart from other companies focusing more on sheer volumes. One particular opportunity worth considering relates to the provision of specialized steel to make electric vehicles, offshore wind farms, power transmission facilities, and advanced manufacturing systems.

Firms are making attempts at forming strategic alliances with automotive firms, contractors in the construction business, and companies in the renewable energy industry to ensure steady orders in the coming years. New possibilities are associated with industrial reshoring operations, infrastructure upgrades, and greater demand for eco-friendly materials. Moreover, steel companies are focusing on developments in the area of utilizing AI technologies for implementing quality control mechanisms, predictive maintenance software platforms, and creating digital twins of steel facilities.

ArcelorMittal was established in 2006, with its headquarters located in Luxembourg. It specializes in the manufacture of high-end automotive steel, low-carbon steel, and the deployment of smart manufacturing technologies. By making significant investments in hydrogen-based steel production and electric arc furnace technologies, the company aims to cater to the demands of industrial clients for sustainable steel products to be used in transportation, construction, and renewable energy sectors.

Ansteel Group Corporation Limited was founded in 1916 with headquarters in Anshan, China. The company caters to various industries such as infrastructure, shipbuilding, automobile manufacturing, and energy. Ansteel Group's initiatives include expanding production capacity for high-end steel and the adoption of intelligent manufacturing technologies.

Nippon Steel Company was established in the year 1934, with its headquarters located in Tokyo, Japan. It offers superior steel products in various industries such as automotive, engineering, and energy. This company is focusing on improving the use of advanced materials technologies and carbon reduction programs as well as providing next generation steel solutions.

HBIS Group was founded in 2008 in Shijiazhuang, China. It offers an extensive range of steel products to various clients in the construction, automotive, appliances, and industrial segments. It is actively working on various green manufacturing projects, digital manufacturing, and new specialty steels.

Other key players in the market include Jiangsu Shagang Group, POSCO Holdings Inc., JFE Steel Corporation, Tata Steel Limited, Hyundai Steel Co., Ltd., and China Baowu Steel Group Corporation, among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock the latest insights with our steel market trends 2026 report. Discover regional growth patterns, consumer preferences, and key industry players. Stay ahead of competition with trusted data and expert analysis. Download your free sample report today and drive informed decisions in the market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the global steel market attained a volume of approximately 1709.75 MMT.

The market is projected to grow at a CAGR of 1.19% between 2026 and 2035.

The steel market size is estimated to reach 1924.46 MMT in 2035.

The key driving factors of the market growth are the increasing infrastructure investments and expanding sectors including automotive and construction.

The key trends aiding the market include technological developments such as Industry 4.0, digitalisation, automation, and additive manufacturing in steel production and the growing demand for light weighted steel in automotive sector.

The different types of steel include carbon steel, alloy steel, stainless steel, and tool steel.

Based on application, the market is segmented into building and construction, mechanical engineering, automotive and transportation, metalware, domestic appliances, agricultural, heavy industry, consumer goods, and others.

The competitive landscape consists of ArcelorMittal S.A., Ansteel Group Corporation Limited, Nippon Steel Corporation, HBIS Group Co., Ltd., Jiangsu Shagang Group, POSCO Holding Inc., JFE Steel Corporation, Tata Steel Limited, Hyundai Steel Co., Ltd, China Baowu Steel Group Corporation, Baosteel Group, Emirates Steel, NUCOR, Outokumpu, and Thyssenkrupp, among others.

Based on type, the leading segment considered in the market report is flat steel.

The market is broken down into North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa.

The leading segment considered in the market report is carbon steel, by the product analysis.

Based on application, the leading segment of the global steel market is building and construction.

The key regions considered in the market report are Australia, Canada, Colombia, Africa, and Chile.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product |

|

| Breakup by Type |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Trade Data Analysis |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.