Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

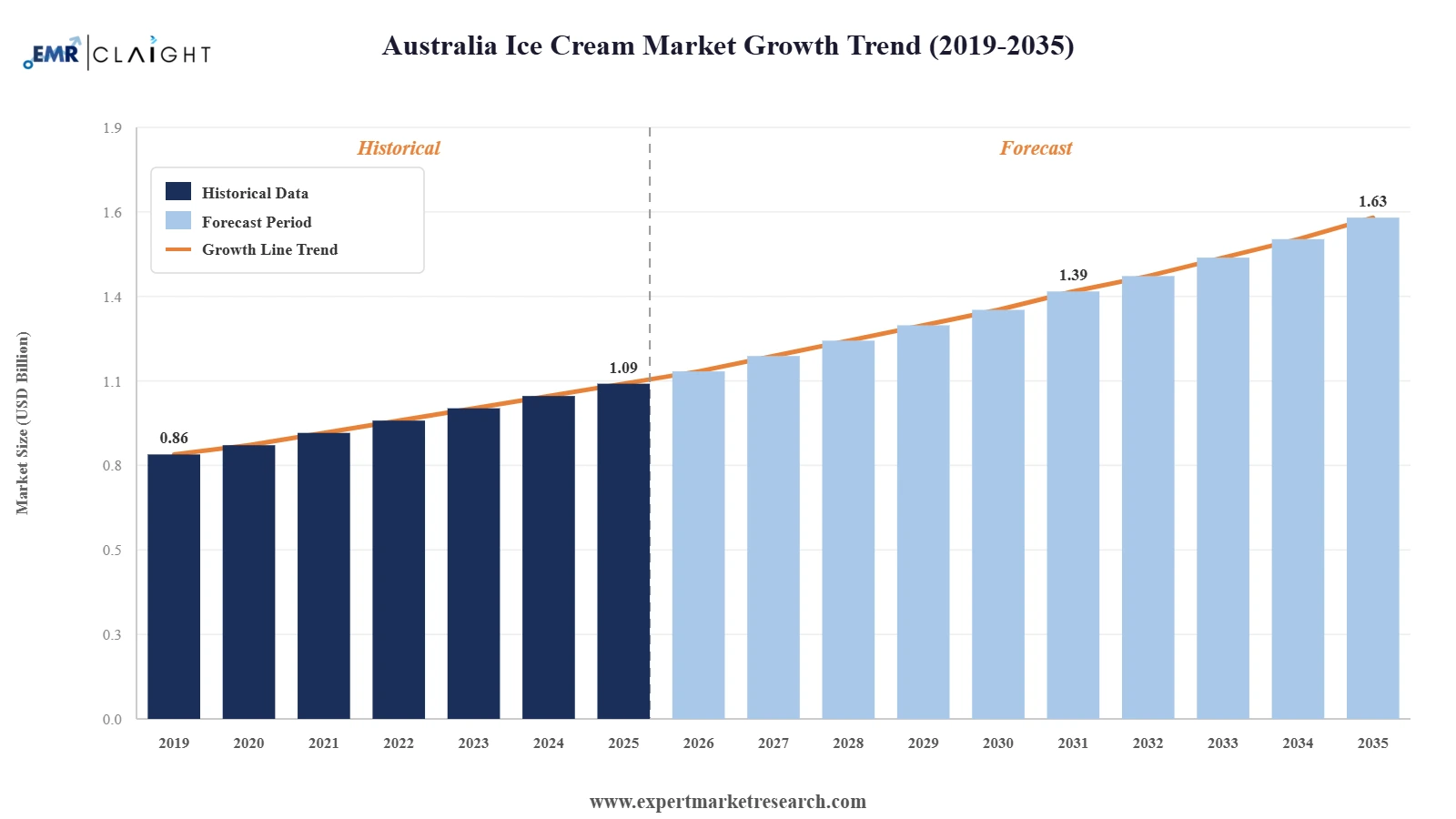

The Australia ice cream market attained a value of USD 1.09 Billion in 2025 and is projected to expand at a CAGR of 4.10% through 2035. The market is further expected to achieve USD 1.63 Billion by 2035. Growing café and dessert bar menus using scoopable and mochi style ice cream formats are boosting demand.

The market is reshaping around fast flavor rotation and lifestyle led ranges that stretch well past the summer peak. In November 2025, Bulla unveiled a new range of ice cream products, adding five launches across its Murray St Ice Creamery and Splits lines, supported by new coconut and oat bases that hold smoother texture at lower fat. This Australia ice cream market trend translates into rising dairy alternative interest in the country. Retailers also support these launches with expanded freezer space and clearer shelf cues that help shoppers spot special diets faster.

Local and global producers now target smaller batch production and faster sensory trials. Many brands trial seasonal fruit blends, low sugar formats, and premium inclusions. In September 2024, Frozen foods brand Frosty Fruits launched a reduced-sugar version of its best-selling flavor. The new Frosty Fruits Tropical 50-per-cent Less Sugar is made from real fruit juice and contains no artificial sweeteners, colors, or flavors, accelerating the Australia ice cream market value.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Uber Eats revealed the unique Sydney debut of SMiZE & DREAM, an innovative international ice cream brand created by Tyra Banks. SMiZE & DREAM offers artisanal, flavor-rich ice cream, with a unique hidden treat tucked away at the bottom of each container. This Australia ice cream market development highlights rising demand for premium, story-driven ice cream brands delivered on-demand, opening opportunities for local makers to scale artisanal formats through digital-only channels.

Kinder revealed the introduction of Kinder Chocolate Ice Cream in Australia. Kinder’s entry in the market shows how nostalgia-led confectionery brands can unlock family tubs and novelty sticks, encouraging Australian players to build dessert mashups that boost impulse purchases.

The Australian brand Peters Ice Cream teamed up with Cadbury and Oreo to introduce two 'movie snack choices', namely Cadbury Choc Tops and Oreo Cookie Tops. These co-branded treats point to strong novelty momentum and flavor licensing, motivating producers to create eye-catching inclusions that boost profit margin across snackable formats.

Chinese ice cream and tea brand Mixue launched its initial Australian outlet in Sydney's World Square shopping center. This Australia ice cream market development signals growing competition from global ice cream chains, pushing domestic brands to sharpen pricing, texture quality, and café-linked menus, especially in high-traffic urban hubs.

Plant-based ice cream is becoming a bigger growth engine as households look for dairy alternatives that actually taste close to classic dairy. Brands like Bulla and Pana Organic keep adding oat, coconut, and almond bases. Retailers have carved out dedicated freezer sections for vegan SKUs, making discovery easier. In August 2023, plant-based ice cream brand Over the Moo debuted a bite-sized ice cream range, offering a vegan take on the well-known choc ice format. Food Standards Australia New Zealand continues to reinforce allergen labeling clarity, and that gives confidence to cafés and catering sites that want safe, inclusive menus, driving the Australia ice cream market growth. The overlap between dairy-free, premium flavor, and lower sugar options is widening, creating space for new textures and fruit-forward profiles.

Premium positioning is thriving as brands invest in product inclusions that hold clean structure in transport and service. Messina keeps releasing limited runs tied to its patisserie roots, and Bulla pushes richer notes in seasonal tubs. In March 2025, Neil Perry joined forces with skincare and make-up brand La Mer to host the first-ever La Mer Crèmery, a retro-inspired ice cream parlor popping up for one weekend only in Guilfoyle Park, in Sydney’s Double Bay, accelerating the overall demand in the Australia ice cream market. Chefs in hotel and resort kitchens look for scoopable formats that retain shape on warm plates.

Dairy processors focus more on farm provenance, low-food-mile milk, and pasture-based supply. State programs supporting regional dairy resilience, including grants for processing upgrades, are improving consistency and capacity. Consumers respond well to tubs showing regional milk origins, which boosts trust and makes price less of a barrier. In July 2025, Golden North inaugurated a new facility in Murray Bridge to boost production and expand its dairy offerings. Local sourcing also resonates with export-ready suppliers that position the country as a clean, reliable dairy hub, propelling the Australia ice cream market scope. Brands pair traceable milk streams with modern flavors, combining authenticity and novelty.

New handheld sticks, protein-leaning mini formats, and mochi shells align well with consumer demand for portion control and novelty. For example, in October 2024, Magnum launched its first bite-sized Bon Bons, joining Ben & Jerry's and Yasso in leveraging micro-formats. Retailers back these product lines with secondary placements near self-checkout during warmer months, creating new Australia ice cream market opportunities. Airline and stadium caterers also test handheld SKUs for easier service and reduced mess.

Limited editions now run across shorter cycles, backed by social sampling and click-through tracking. Loyalty data from major retailers like Woolworths and Coles helps refine freezer sets as per local demand, aligning with diverse tastes, broadening the Australia ice cream market scope. In July 2025, Wall’s partnered with Minecraft, the world’s bestselling game, to launch a limited-edition ice cream aimed at gaming enthusiasts. Meal delivery apps offer add-on ice cream, bringing fresh demand curves in cooler months. Brands treating digital platforms as core to assortment planning can strategize quicker than those who depend on traditional seasonal calendars.

The EMR’s report titled “Australia Ice Cream Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

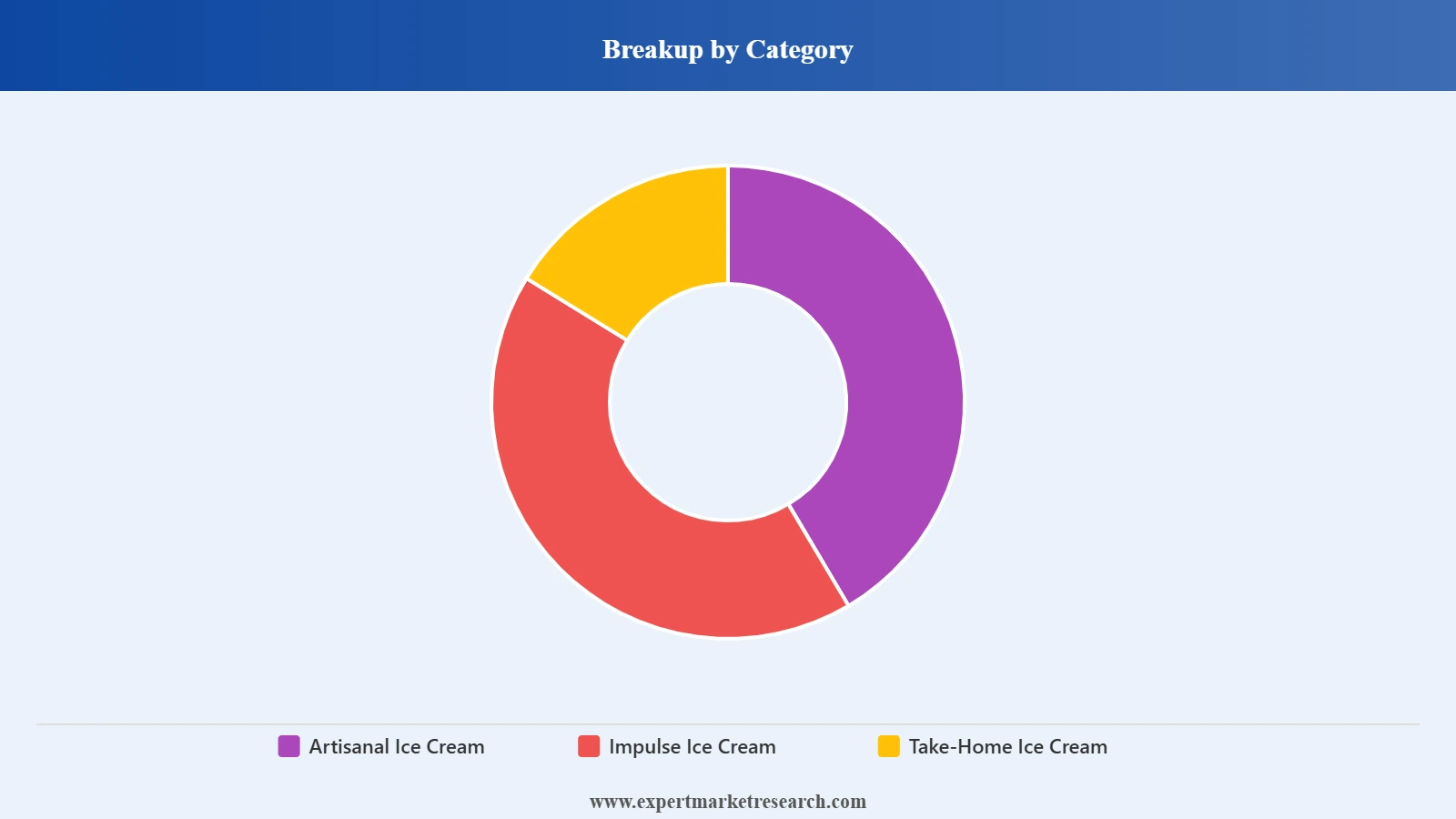

Market Breakup by Category

Key Insight: Take-home tubs capture substantial share of the Australia ice cream market because families want everyday value and broad flavor choice. Impulse ice creams thrive on portability and hot-weather spikes tied to tourism and events. Artisanal formats strengthen their market share by promising richer textures. Vanilla remains a safe path to repeat purchase, while chocolate attracts indulgence seekers and fruit flavors to support lighter tastes.

Market Breakup by Flavour

Key Insight: Vanilla remains the leading flavour choice in the Australia ice cream market due to its broad consumer appeal and compatibility with diverse toppings and dessert formats. Chocolate continues to attract indulgence-focused consumers seeking rich and premium taste experiences. Fruit flavours benefit from growing demand for refreshing and lighter options, particularly during warmer seasons. The Others segment supports market diversification through innovative, seasonal, and specialty flavours that appeal to consumers looking for unique taste experiences.

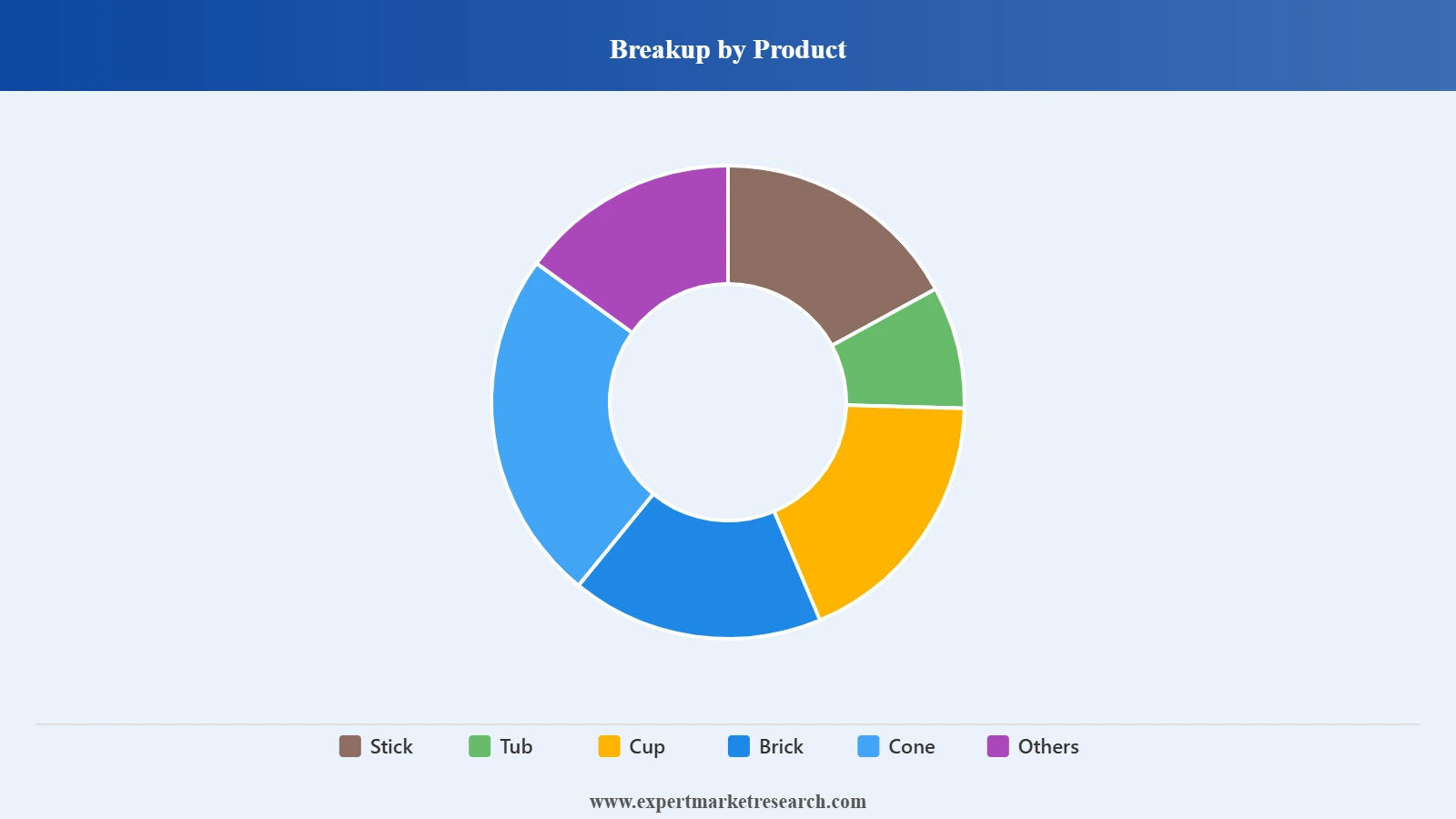

Market Breakup by Product

Key Insight: Tubs anchor majority of the demand in the Australia ice cream market through meal-time versatility and dense flavor variety, while sticks gain major momentum owing snacking demand and single-serve convenience. Cups provide grab-and-go simplicity for schools, offices, and cafés. Cones lean on nostalgic draw and strong display appeal, while bricks support portion slicing for home bakers and foodservice plating.

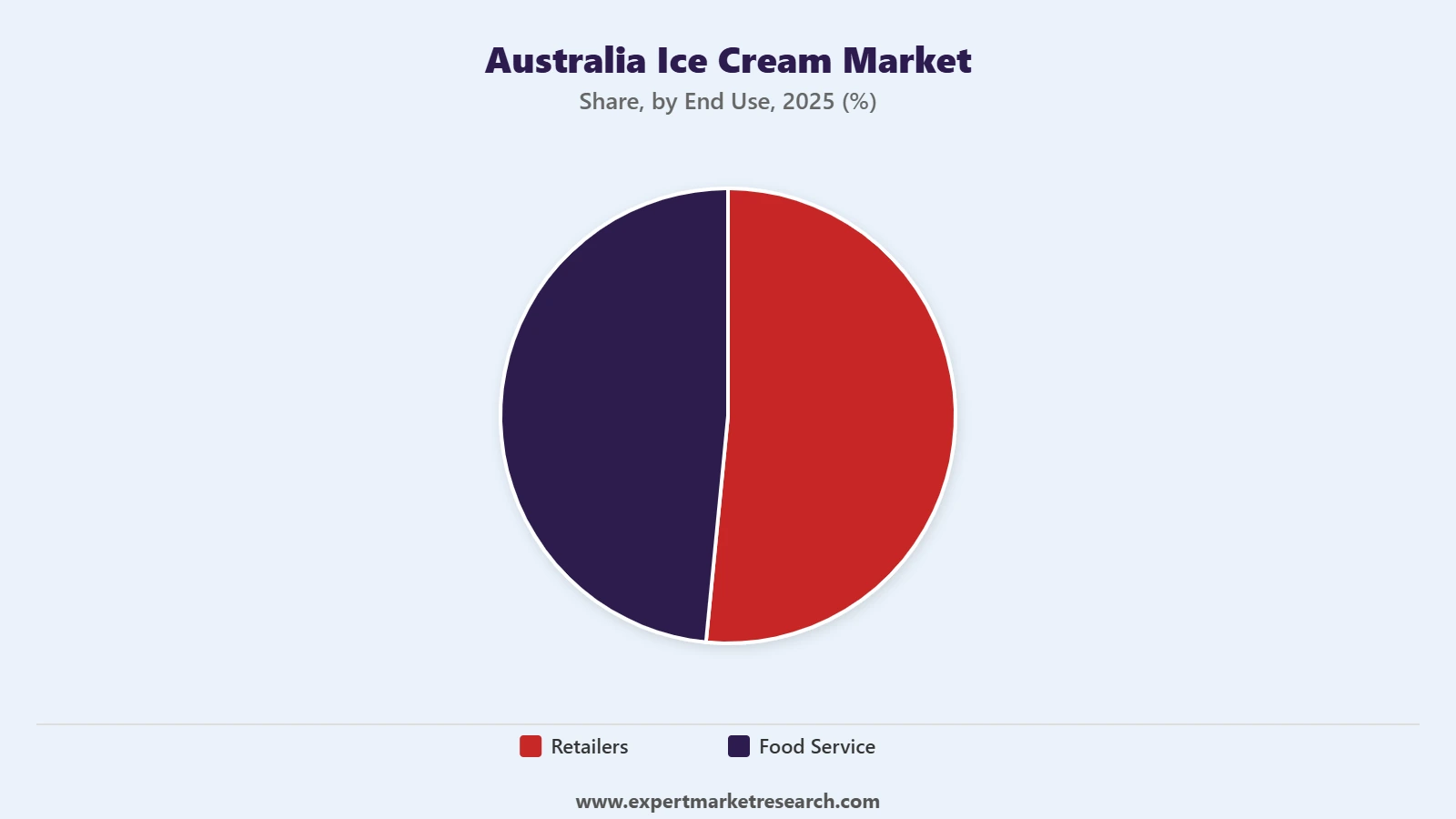

Market Breakup by End Use

Key Insight: Retail continues to dominate the market, driven by broad assortment and repeat household purchases. Foodservice channels boost revenue growth through plated desserts, novelty shells, and reliable scooping specifications. Retail success hinges on freezer space, clear navigation, and value tiers, while foodservice leans on performance, flavor differentiation, and back-of-house ease, boosting Australia ice cream market penetration. Makers balance both end use categories with tailored pack sizes and texture profiles, strengthening visibility and placement.

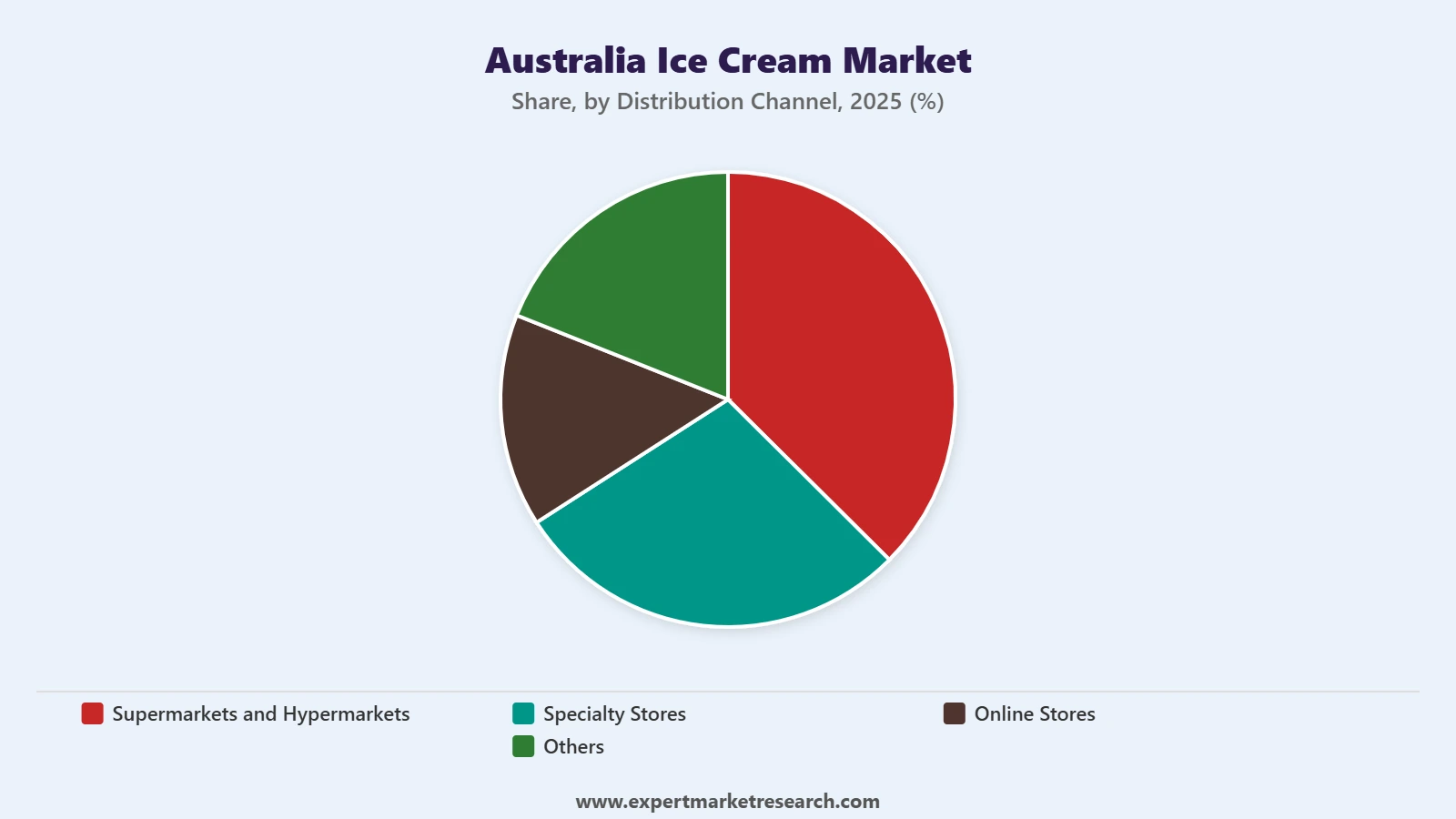

Market Breakup by Distribution Channel

Key Insight: Supermarkets and hypermarkets shape category norms through assortment scale and visibility, while specialty stores pitch premium stories and artisanal churn. Online channels widen the reach to remote buyers and supports flavor exploration. “Others,” including convenience outlets and foodservice wholesalers, handle on-the-go and bulk needs.

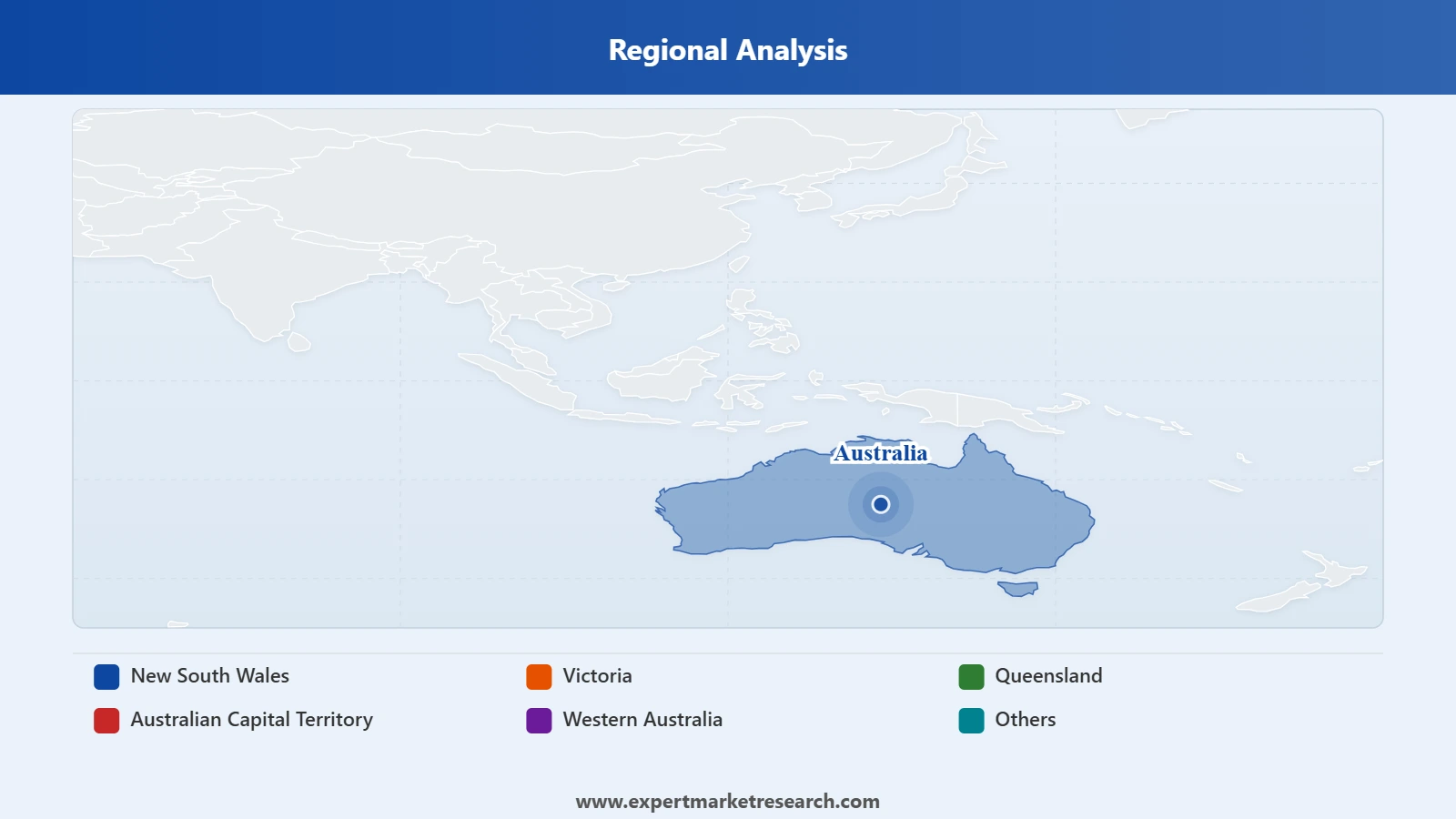

Market Breakup by Region

Key Insight: New South Wales drives the market with strong retail depth and tourism pull. Victoria and Queensland add scale through metro density and outdoor leisure culture. Australian Capital Territory grows at the fastest pace owing to surging premium and wellness trends. The Western Australia ice cream market and other regions strengthen demand through café, beach, and event settings. While dense metros push innovation, regional hubs lean on reliability and value. This regional landscape supports continual flavor refresh, stronger cold-chain execution, and broader menu usage.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Take-home ice cream category currently captures the largest share due to family-size value

Take-home ice cream leads the Australia ice cream industry because households want flexible packs that fit everyday occasions. Producers push one-liter and two-liter tubs with richer inclusions, lactose-free mixes, and seasonal flavors that feel premium. Local makers focus on smoother melt, better refreeze tolerance, and sturdy tubs that travel well for low wastage. Foodservice wholesalers also stock larger tubs for cafés and dessert bars. In February 2025, Bulla partnered with Hershey's to launch two new one-liter ice cream tub flavors, which were made available at Coles.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Artisanal ice cream is gaining major momentum in the Australia ice cream market dynamics because shoppers and cafés want deeper flavor notes, cleaner ingredient lists, and tighter control on overrun. Boutique creameries and premium brands release short-run batches using local fruit, single-origin chocolate, and inclusions like honeycomb shards or patisserie crumbs. These SKUs get strong demand in specialty stores, farmers markets, and hospitality venues that pitch experience over price. In October 2025, Woolworths launched nostalgic birthday favorite flavors including Mud Cake, Lamington, and Pavlova ice cream varieties, each retailing for AUD 6.50 per one-liter tub. Artisanal suppliers also focus on egg-based custards, silkier churn, and chef collaborations, lifting sensory impact.

By product, tubs register the largest share of the market due to format flexibility

Tubs dominate the market because they offer portion control and kitchen versatility. Families scoop multiple serves from a single pack, while cafés and dessert bars plate from wide lids that simplify speed and yield. Brand owners load tubs with layered sauces, larger inclusions, and plant-based bases that need space to show their value. Tubs retain ice cream quality intact even during transportation, shielding texture and shape, which reduces risk in longer supply chains.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Sticks observe major growth in the Australia ice cream market because they align with snacking, portability, and portion control requirements. Producers experiment with crisp coatings, mochi-style layers, protein enrichments, and vibrant inclusions that drive visual appeal. Retailers place sticks during warm months near checkouts and in multipacks for home freezers. In July 2024, Australian dairy co-operative Norco unveiled its newest ice cream range, Cape Byron, which features chunky inclusions on an ice cream stick. Foodservice sites choose sticks for fast service during events, travel, and entertainment settings.

By end use, retailers accounted for a significant share of the market revenue thanks to broad freezer penetration

Retailers currently dominate the market because supermarkets, convenience outlets, and specialty grocers manage wide freezer sets that catch routine traffic. Their scale supports deeper flavor rotation, larger tub sizes, indulgent sticks, and plant-based lines. Retailers also coordinate with suppliers on packaging refreshes and display efficiency, improving engagement. Premium and artisanal ranges benefit from storytelling on pack, while private labels push tighter product value with clean-label claims.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Foodservice businesses also contribute to the Australia ice cream market revenue, because cafés, dessert bars, hotels, and restaurants expand menus with plated scoops, mochi shells, affogato builds, and premium stick pairings. Suppliers tailor tub specifications, inclusions, and overrun to support consistent plating. In February 2025, Lee Kum Kee and Gelato Messina collaborated to create two gelato flavors using Lee Kum Kee's sauces and condiments. Travel, event, and leisure venues use single-serve novelties for speed and reduced waste.

By distribution channel, supermarkets and hypermarkets secure the largest share via strong freezer networks

Supermarkets and hypermarkets dominate the distribution channel since they hold the most extensive freezer runs, capturing planned and impulse trips. They depend on data to refine flavor mix, pushing limited runs beside everyday classics. Fridge adjacency to bakery and fruit displays spurs pairing ideas. Supermarkets anchor family tubs, plant-based novelties, and multipack sticks while ensuring cold-chain stability. Promotional calendars and loyalty rewards help lift trial and repeat. Their deep logistics capability and national presence make them the essential gateway for brands scaling production.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

As per the Australia ice cream market report, online channels grow at an accelerated pace as households and foodservice buyers rely on delivery to restock freezers without store time. Retailers and pure-play platforms expand cold chain capacity and flexible slots. Specialty creameries use direct-to-consumer sites for drops and sample bundles, building flavor discovery. Digital listings highlight allergens, format type, and plant-based cues, helping shoppers compare quickly.

New South Wales secures the leading position in the market due to diverse consumption patterns

New South Wales leads the Australia ice cream market owing to dense metro populations, tourism flows, and diverse eating habits that support wide freezer sets. Retailers lean on premium tubs, limited editions, and strong novelty runs. Foodservice operators experiment with plated scoops and mochi shells, aided by frequent menu refresh cycles. Distributors offer deep coverage that protects temperature integrity, which is crucial for quality.

Australian Capital Territory is quickly expanding its share in the Australia ice cream market owing to premium ready desserts and café culture align with artisanal and plant-based positioning. Higher wellness engagement supports lower sugar, lactose-free, and oat-based tubs. Foodservice channels in government and corporate hubs favor clean scooping performance and reliable hold. Specialty grocers and dessert bars test bold flavors, encouraging rotation.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The market is shifting toward formats that combine novelty, nutrition, and storytelling. Australia ice cream companies focus on richer inclusions, plant-based bases, and faster flavor rotation that helps stores refresh freezers without major resets. Players explore AI-assisted planning to align micro-clusters of flavor demand with store-level product mixes, reducing waste and improving margins. There is also momentum in handheld and mochi shell novelties, supported by better coating technology that protects texture through long transport routes.

Foodservice partners want scoopable tubs that resist ice crystals and plate clean under heat lamps, opening room for reformulation and stabilizer upgrades. Packaging redesign is another focus area, with lighter lids, QR-linked allergen guides, and lower-plastic tubs gaining traction. Australia ice cream market players that balance cost discipline with indulgence and differentiated flavor stories are positioned to grow faster in the coming years.

Australasian Food Group Pty Limited, established in 2000 and headquartered in Victoria, Australia, builds momentum through the Peters brand portfolio, pairing mainstream tubs with indulgent sticks and cones. The company works closely with supermarkets to broaden year-round presence. It serves foodservice clients with reliable scooping formats that handle temperature fluctuations in commercial kitchens.

Golden North Ice Cream, established in 1923 and headquartered in Laura, South Australia, focuses on clean-label recipes and a nut-free production environment. Its regional sourcing strategy and slow churn approach appeal to premium shoppers. The company supplies tubs and novelty lines to retailers across southern states and works with foodservice partners that want dependable dairy texture.

General Mills Inc., founded in 1928 and headquartered in Minnesota, United States, extends its global expertise into Australia through the Häagen-Dazs brand and distribution partners. The company leans on rich inclusions and globally recognized recipes, supplying premium tubs and multipacks, impacting the Australia ice cream market value. It targets specialty retail and upscale hospitality venues, where strong flavor identity commands repeat purchase. Consistent messaging around craftsmanship and texture gives the brand a clear space in the premium tier.

Unilever Australia Limited, established in 1890 and headquartered in Sydney, Australia, leverages its large footprint with brands like Streets, Cornetto, and Magnum. The business covers mass retail, convenience, and foodservice channels with broad novelty and tub offerings. Unilever balances classic favorites with limited editions and sustainability initiatives, including lighter packaging and updated cold chain efficiency.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other key players in the market include Regal Cream Products Pty Ltd., Invidia Foods, and Supatreats Australia Pty. Ltd., among others.

Unlock the latest insights with our Australia ice cream market trends 2026 report. Discover regional growth patterns, consumer preferences, and key industry players. Stay ahead of competition with trusted data and expert analysis. Download your free sample report today and drive informed decisions in the market.

United Kingdom Ice Cream Market

North America Ice Cream Market

Latin America Ice Cream Market

Australia Private Label Frozen Dessert Strategy

Australia Premium Dessert Cafes And QSR Innovation

Australia Cold Chain Logistics For Frozen FMCG

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 1.09 Billion.

The market is projected to grow at a CAGR of 4.10% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach USD 1.63 Billion by 2035.

Expanding premium novelties, strengthening plant-based lines, enhancing scoop stability, investing in digital flavor testing, and refining packaging sustainability, are some of the key strategies driving the market forward.

Key trends aiding the market expansion are the emphasis on sustainability to attract environmentally conscious consumers, and the adaptation to changing consumer preferences by leveraging digital channels for marketing and distribution.

Regions considered in the market are New South Wales, Victoria, Queensland, Western Australia, and Australian Capital Territory, among others.

Based on product, the market segmentations include stick, tub, cup, brick, and cone.

Artisanal ice cream, impulse ice cream, and take-home ice creams are considered in the report.

The key players in the market include Australasian Food Group Pty Limited, Golden North Ice Cream, General Mills Inc., Unilever Australia Limited, Regal Cream Products Pty Ltd., Invidia Foods, and Supatreats Australia Pty. Ltd., among others.

Companies face rising input costs, complex cold-chain demands, intense freezer competition, and pressure to balance indulgence with cleaner labels, while managing seasonal swings and rapid flavor rotation cycles.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Category |

|

| Breakup by Flavour |

|

| Breakup by Product |

|

| Breakup by End Use |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.