Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

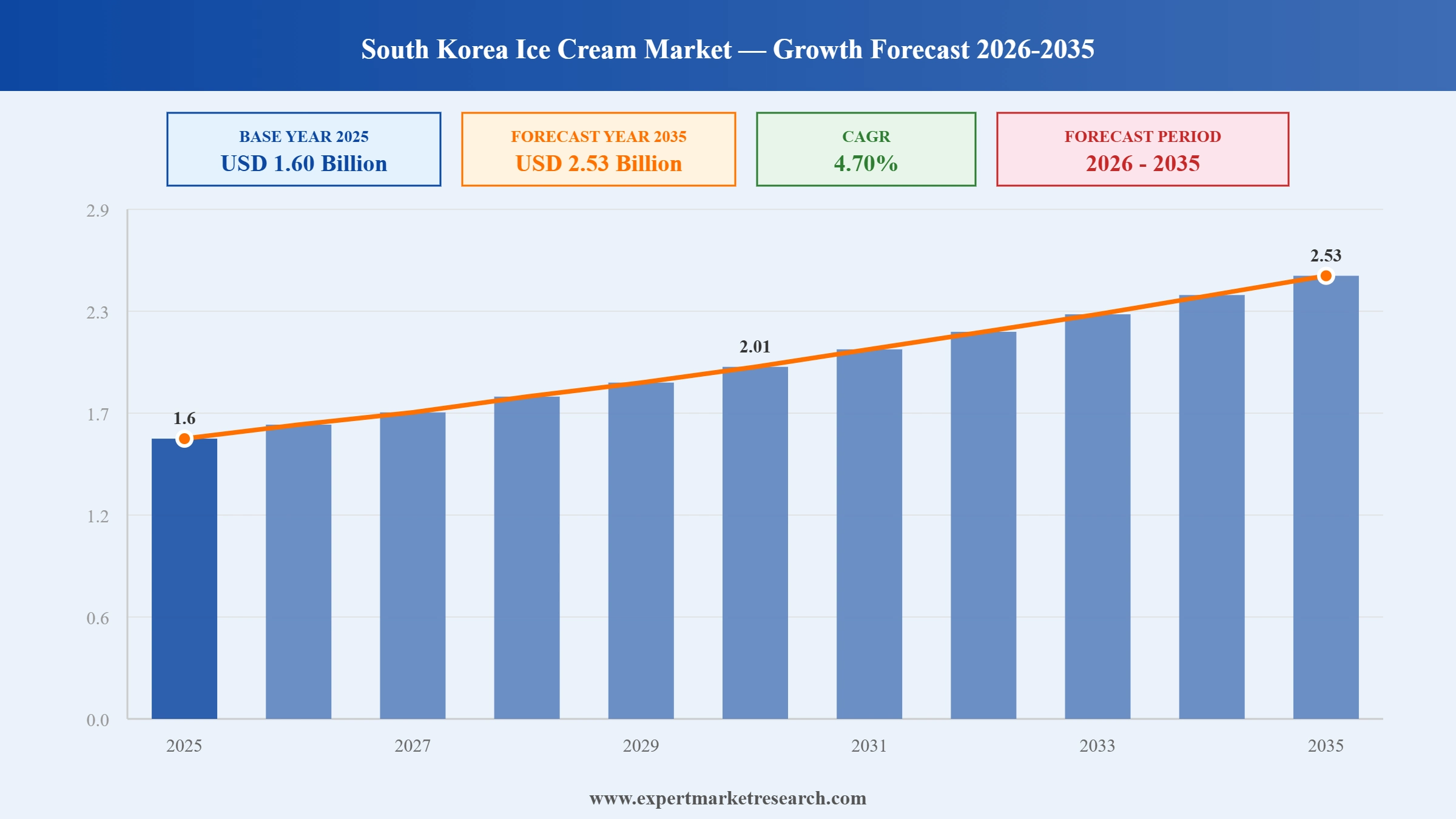

The South Korea ice cream market reached a value of USD 1.60 Billion at 2025 and is projected to expand at a CAGR of around 4.70% during the forecast period of 2026-2035. With robust product innovation by domestic brands, rising consumer demand for premium flavours and health-conscious variants, growing influence of K-pop and digital marketing on purchasing behaviour, and expanding online food delivery services, the market is expected to reach USD 2.53 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

South Korea's ice cream market is evolving beyond basic commodity frozen dessert into a high-engagement consumer category shaped by nostalgia, health trends, and social media culture. Domestic manufacturers are investing in flavour diversification, limited-edition packaging, and celebrity partnerships to sustain consumer excitement, while international brands are competing on premium positioning. The interplay between Newtro cultural nostalgia and contemporary health-conscious demand creates a dynamic innovation environment that sustains category growth.

Binggrae was selected among 145 companies for South Korea's Global Next K-Food programme in April 2026, enabling it to leverage Ministry of Agriculture international marketing infrastructure to expand Melona and other ice cream brands globally across Asia, North America, and Europe.

Binggrae implemented a voluntary retirement programme in February 2026 following a 32.7% operating profit decline in 2025 amid raw material cost pressures. Lotte Wellfood similarly restructured. Both companies are prioritising core brand investment and rationalising product lines around proven high-performing ice cream offerings.

Industry analysis from June 2025 confirmed South Korean ice cream manufacturers actively launching new formats targeting solo consumption and portion control for single-person households. Themed packaging, influencer tie-ups, and QR-code interactive experiences were identified as central brand engagement strategies driving impulse purchase behaviour.

South Korean convenience stores and hypermarkets significantly expanded premium and health-oriented ice cream ranges in August 2024, responding to demand for lactose-free, low-calorie, and low-fat frozen dessert variants. Binggrae and Lotte Confectionery both introduced new health-conscious lines targeting urban consumers.

South Korea's Newtro trend continues to fuel demand for iconic ice cream products with modern reformulations. Melona, introduced in 1992, remains a top-selling product and is gaining international recognition. Binggrae leverages this nostalgia premium through limited-edition flavours supporting South Korea ice cream market growth.

Marketing partnerships between South Korean ice cream brands and K-pop artists are central to brand visibility strategy in South Korea's ice cream market. Digital campaigns, idol-branded packaging, and OTT content integrations are generating strong engagement and sales spikes, boosting Binggrae and Lotte Confectionery's premium product lines.

Rapid expansion of online food delivery platforms in South Korea is creating new purchase occasions for ice cream, with same-day delivery improving cold chain access. This channel growth is especially relevant for premium and artisanal segments in South Korea's ice cream market growth trajectory across urban areas.

South Korea's vast convenience store network of over 50,000 outlets remains the primary impulse channel for the ice cream market. Stores actively expand premium ice cream assortments and imported international brands. Seasonal limited-edition launches generate disproportionate revenue contributions in the South Korea ice cream market.

Health-conscious trends are reshaping South Korea's ice cream market, with manufacturers introducing lactose-free, low-calorie, and plant-based frozen dessert variants. This segment grows faster than the overall market. Unilever has leveraged global R&D capabilities to introduce health-positioned Magnum lines to South Korean convenience stores.

The report of the Expert Market Research's titled "South Korea Ice Cream Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

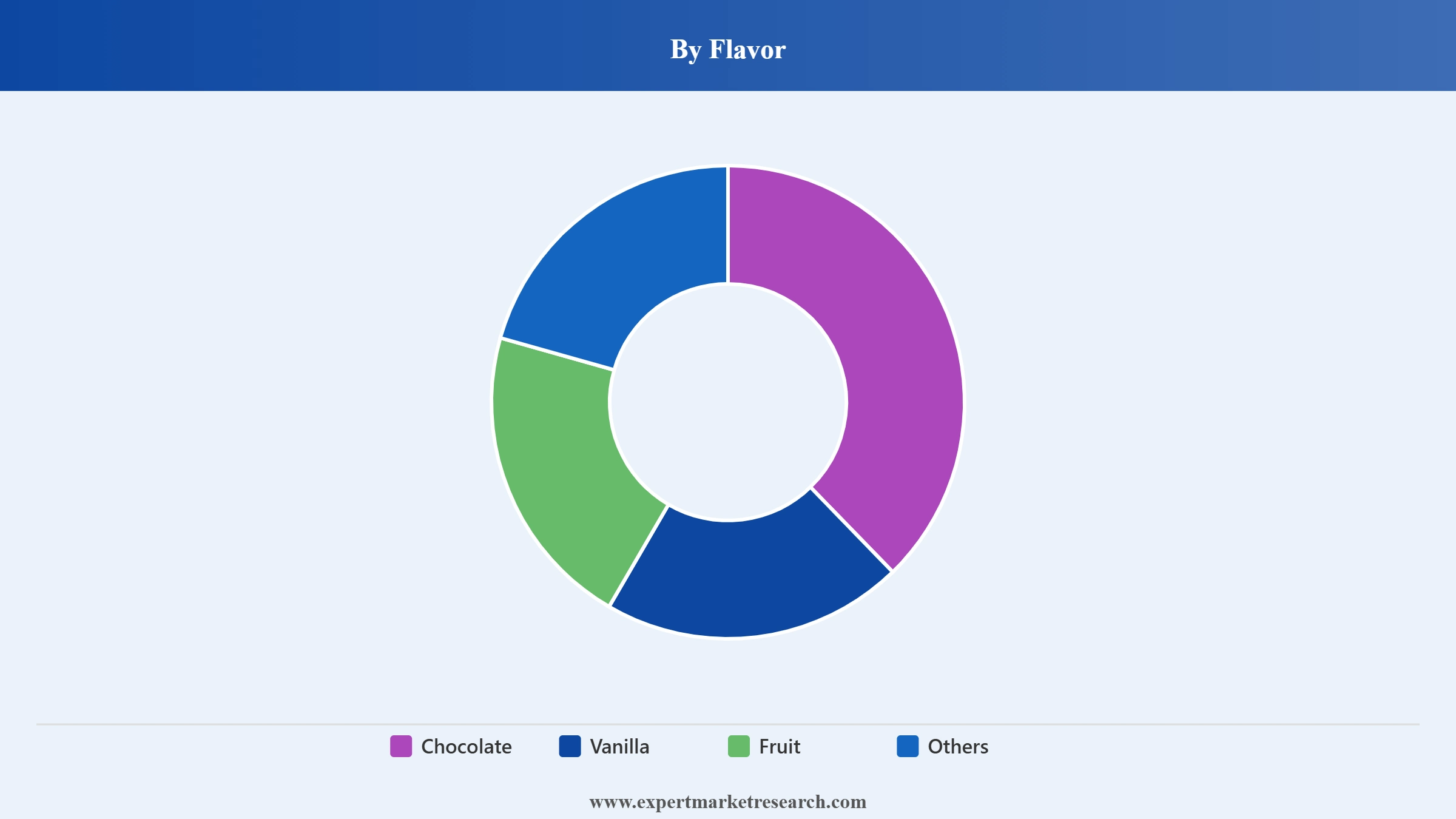

Market Breakup by Flavor

Key Insight: Fruit-flavoured ice cream holds a distinctive position in South Korea's flavour landscape, reflecting the domestic preference for lighter, refreshing profiles suited to the country's humid summers. Iconic products such as Binggrae's Melona exemplify the long-term commercial success of fruit flavours in the South Korean market. Vanilla and chocolate maintain strong positions in premium and take-home categories, while Others captures a rapidly growing segment of novel and seasonal innovations including matcha, red bean, and international fusion profiles.

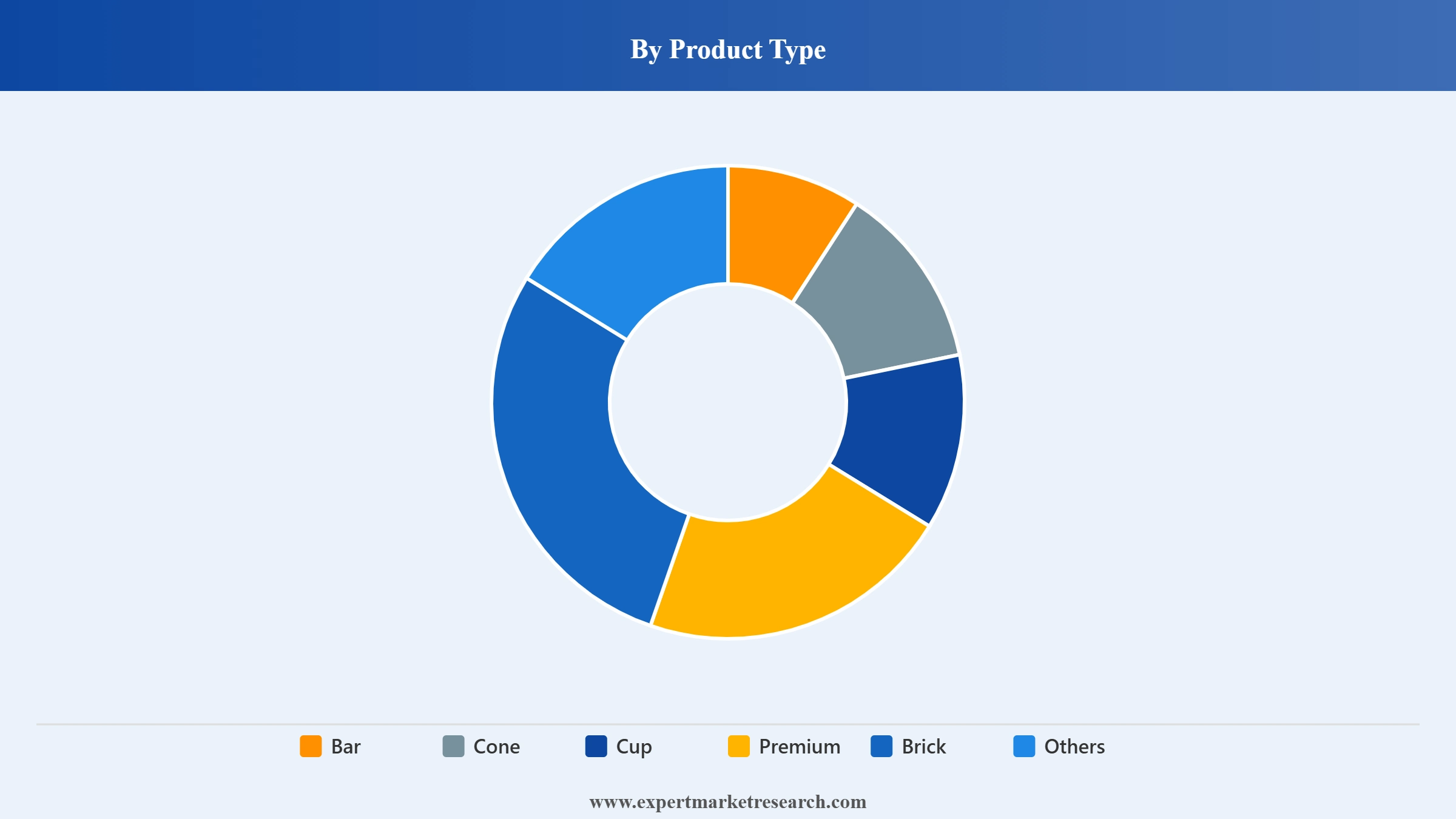

Market Breakup by Product Type

Key Insight: Bar ice cream is the dominant product format in South Korea, representing the most culturally embedded ice cream consumption occasion and the primary impulse purchase format through convenience stores. Bars account for a substantial majority of total ice cream units sold due to their affordability, portability, and the iconic status of products like Melona. Premium formats are the fastest-growing segment as consumers trade up for high-quality, artisanal, and imported ice cream experiences that command higher price points.

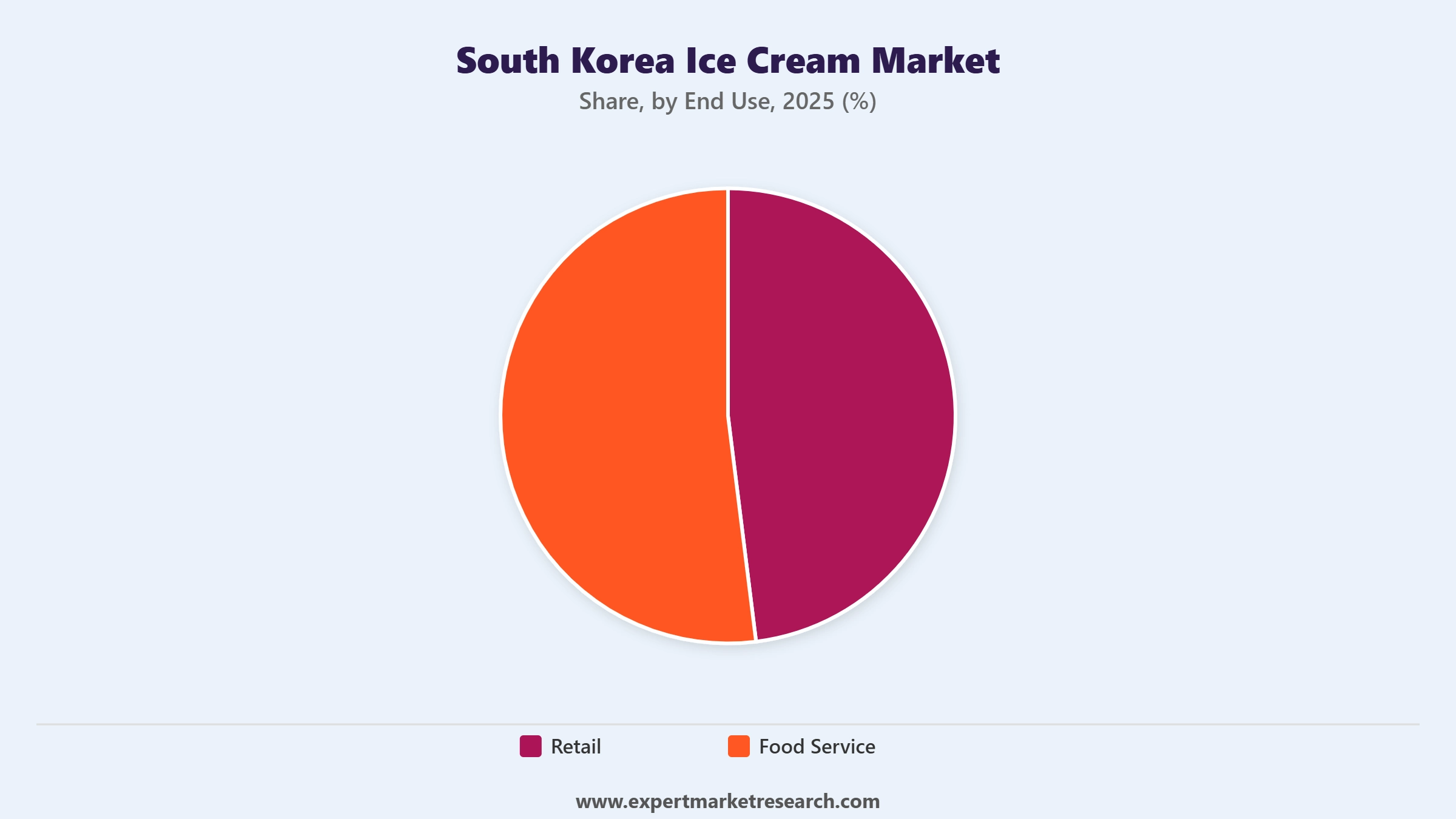

Market Breakup by End Use

Key Insight: Retail accounts for the dominant share of South Korea's ice cream end-use market, driven by the ubiquitous convenience store and supermarket networks that serve as primary ice cream purchase points. Food service is growing steadily as speciality ice cream parlours, cafes, and restaurant dessert menus expand their frozen dessert offerings to capture premiumisation and experiential consumption trends among urban consumers seeking distinctive dessert experiences.

Market Breakup by Distribution Channels

Key Insight: Convenience stores are the most strategically important distribution channel for South Korea's ice cream market, given their extraordinary density and role as the primary impulse purchase touchpoint for bar and cone formats. With over 50,000 convenience store outlets nationwide, they provide unparalleled reach for new product launches and seasonal limited editions. Hypermarkets and supermarkets are the preferred channel for take-home brick and cup formats. Online channels are growing fastest for premium and imported ice cream products that lack widespread physical distribution.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Flavor, fruit flavours hold a distinctive dominant share due to cultural preference and iconic product heritage

Fruit-flavoured ice cream commands the largest share of South Korea's ice cream market by flavour, driven by deeply embedded consumer preferences for light, refreshing profiles over the heavy sweetness of chocolate or vanilla. The commercial longevity of Melona, Binggrae's iconic melon-flavoured bar introduced in 1992, exemplifies how fruit flavours have achieved cultural institution status in the South Korean market. Manufacturers continuously introduce new fruit flavour variants to capture seasonal demand and drive impulse purchasing through convenience store channels.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Vanilla ice cream holds the second-largest flavour share in South Korea, performing particularly strongly in premium, cone, and cup formats where consumers associate vanilla with quality and versatility. International premium brands have reinforced vanilla's premium positioning through consistent product quality and aspirational branding. The chocolate segment maintains a loyal consumer base particularly in the take-home brick format, while the Others segment is expanding as manufacturers experiment with matcha, red bean, and international fusion flavour profiles.

By Product Type, bars account for the dominant share due to cultural ubiquity and convenience store impulse purchase alignment

Bar ice cream is the most consumed product format in South Korea, capturing the largest share of total ice cream revenue through its dominance in convenience store impulse purchasing. The format's portability, single-serve sizing, and price accessibility make it the default ice cream consumption occasion for a wide demographic range. Binggrae, Lotte, and Haitai all maintain strong bar product portfolios, with iconic lines that sustain consistent year-round demand supplemented by seasonal limited-edition launches generating peak sales spikes.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Premium ice cream is the fastest-growing product type within the South Korea ice cream market, reflecting the broader premiumisation trend across South Korean food and beverage categories. Consumers are increasingly willing to pay significantly higher prices for premium single-serve or small-batch ice cream products offering superior ingredient quality, unique flavour profiles, or association with internationally recognised brands. This has supported both the expansion of imported premium brands and the launch of domestic premium-tier product lines by established manufacturers.

By Distribution Channel, convenience stores hold the dominant share due to exceptional density and impulse ice cream consumption

Convenience stores are the single most commercially important distribution channel for South Korea's ice cream market, leveraging their extraordinary national coverage of over 50,000 outlets to deliver near-universal product accessibility. The channel's alignment with impulse ice cream consumption patterns, supported by prominent refrigerated display units near checkout points, makes it the primary sales driver for bar and cone formats. Manufacturers prioritise convenience store launch strategies for new products, using the channel as a rapid national rollout mechanism.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Hypermarkets and supermarkets represent the second-largest distribution channel, particularly important for take-home formats including brick and larger cup products purchased for family consumption. Online channels are growing rapidly, driven by the expansion of rapid food delivery services that have made ice cream accessible for immediate home delivery. The rise of curated premium ice cream subscription and gifting boxes through online platforms creates new premium consumption occasions that support higher average selling prices in the South Korea ice cream market.

The South Korea ice cream market is moderately consolidated, with domestic giants Binggrae and Lotte Confectionery leading in volume and distribution reach, while international brands including Unilever and Baskin-Robbins (BR IP Holder LLC) compete primarily in the premium and food service segments. Haitai Confectionery and Foods maintains a significant domestic presence. Competition centres on product innovation, brand visibility through K-pop partnerships, and pricing strategy across distribution channels.

Cost pressures from raw material volatility and 2025 domestic demand softness have prompted the leading Korean players to restructure while continuing to invest in brand-building activities. International players are selectively targeting premium growth segments while domestic manufacturers defend volume positions across mainstream categories. The ability to execute compelling seasonal limited-edition launches through convenience store channels is an increasingly important competitive capability.

Binggrae was founded in 1967 and is headquartered in Seoul, South Korea. The company is one of the country's most iconic domestic food brands, best known for its Melona melon ice cream bar introduced in 1992 and still one of South Korea's best-selling ice cream products. Binggrae has successfully expanded internationally, with Melona available across North American, Southeast Asian, and European markets. The company was selected for the South Korean government's Global Next K-Food initiative in April 2026 to accelerate its international brand expansion.

Lotte Confectionery, established in 1967 and headquartered in Seoul, South Korea, is a leading confectionery and ice cream manufacturer under the Lotte Group conglomerate. The company produces a wide range of ice cream products across bar, cone, cup, and take-home formats, maintaining strong distribution across convenience stores and supermarkets nationwide. Lotte Confectionery has been investing in premium product development and international market expansion, though it faced operating profit headwinds in 2025 due to raw material cost increases.

Haitai Confectionery and Foods was founded in 1945 and is headquartered in Seoul, South Korea. It is one of the oldest confectionery companies in Korea with a diversified portfolio that includes ice cream, snacks, and beverages. Haitai's ice cream brands have maintained a loyal consumer base through consistent product quality and competitive pricing. The company operates an established domestic distribution network and has been selectively expanding its international product portfolio to capitalise on growing global interest in Korean food products.

Unilever plc was founded in 1929 and is headquartered in London, United Kingdom. Through its Wall's and Magnum ice cream brands, Unilever competes in South Korea's premium ice cream segment, targeting consumers seeking international brand quality and premium product experiences. Unilever's ice cream business benefits from the company's global R&D capabilities and established cold chain logistics. In the South Korean market, Magnum is well positioned in the premium impulse segment across convenience stores and supermarkets.

Other key players in the market are BR IP Holder LLC, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Discover the latest insights on the South Korea ice cream market 2026 with our comprehensive report. Stay ahead with valuable data on flavour innovation, distribution channel dynamics, and the competitive positioning of leading brands. Whether you're a food manufacturer assessing premium product opportunities or an investor evaluating sector growth, this report gives you the clarity you need. Download your free sample now and discover key opportunities in South Korea's thriving ice cream industry.

South Korea Plant-Based Dessert Innovations

South Korea Confectionery Developments

South Korea Premium & Artisanal Desserts Innovation

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the South Korea ice cream market reached an approximate value of USD 1.60 Billion.

The major drivers of the ice-cream industry are product innovation, online food delivery services, rising disposable income, digital marketing and celebrity influence, and flavour variants.

The key market trends in the Ice cream industry of South Korea are the popularity of health consciousness among costumers and ‘Newtro’ culture.

The dominant flavours of ice cream in the South Korea ice-cream market are chocolate, vanilla, and fruit, among others.

Retail stores like hypermarkets, supermarkets and convenience stores are the leading distribution channels. However, speciality stores like cafes and ice cream parlours have the most variety in flavours.

The key players in the South Korea ice-cream industry are Lotte Confectionery Co., Ltd., Binggrae Co. Ltd., BR IP Holder LLC, Unilever plc, Haitai Confectionery and Foods Co., Ltd., among others.

The market is projected to grow at a CAGR of 4.70% between 2026 and 2035.

The market is expected to witness a healthy growth rate during the forecast period of 2026-2035 to reach a value of USD 2.53 Billion by 2035.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Flavor |

|

| Breakup by Product Type |

|

| Breakup by End Use |

|

| Breakup by Distribution Channels |

|

| Market Dynamics |

|

| Trade Data Analysis |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.