Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

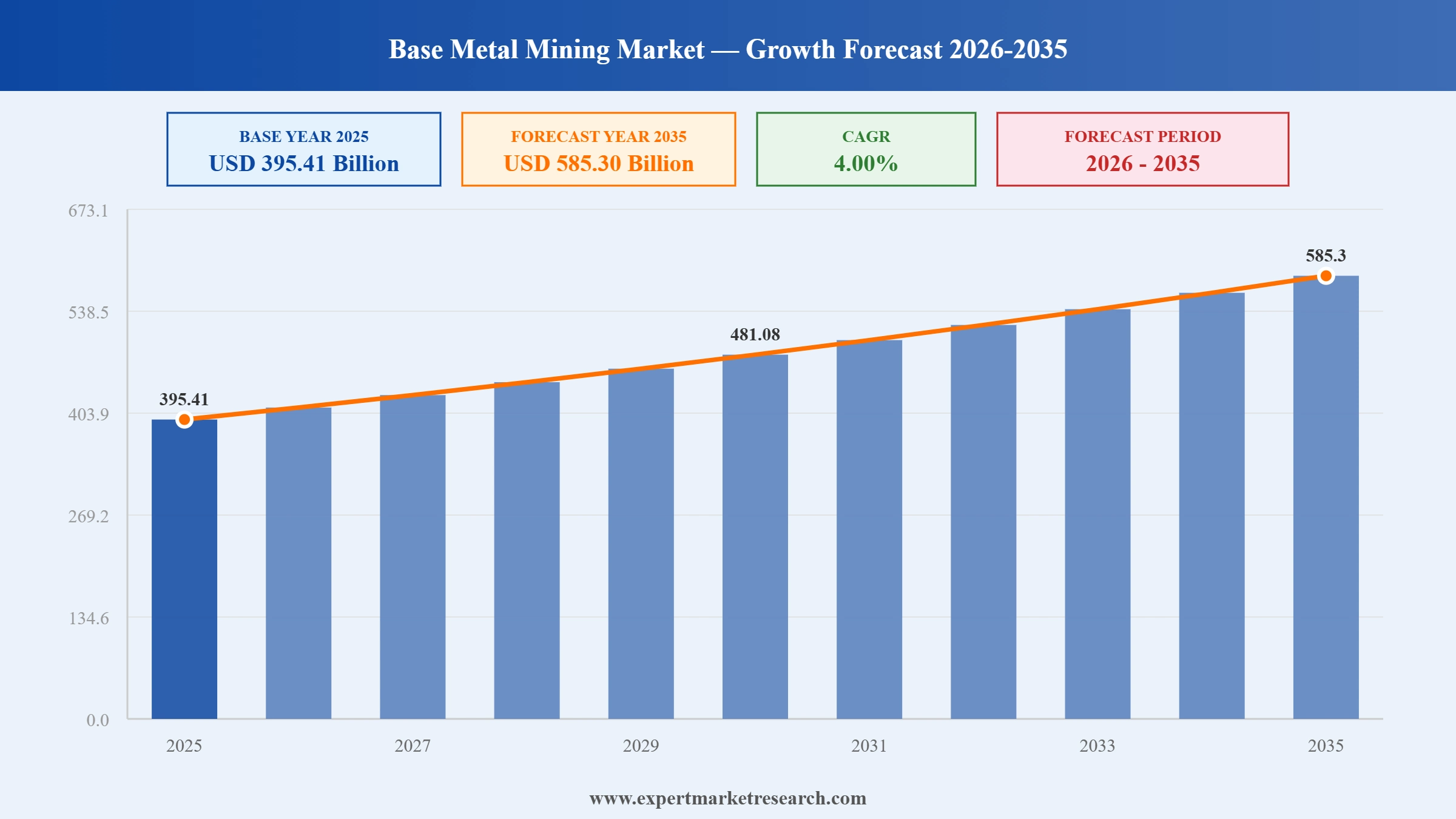

The Global Base Metal Mining Market reached a value of USD 395.41 Billion at 2025 and is projected to expand at a CAGR of around 4.00% during the forecast period of 2026-2035. With record copper prices, EV-led battery metals demand, AI- and grid-driven electrification, and a wave of mega-merger consolidation, the market is expected to reach USD 585.30 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY

| Global Base Metal Mining Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 395.41 |

| Market Size 2035 | USD Billion | 585.30 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 4.00% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 5.2% |

| CAGR 2026-2035 - Market by Country | India | 5.9% |

| CAGR 2026-2035 - Market by Country | China | 5.0% |

| CAGR 2026-2035 - Market by Product | Aluminium | 4.6% |

| CAGR 2026-2035 - Market by Application | Construction | 4.5% |

| Market Share by Country 2025 | China | 33.4% |

The Global Base Metal Mining Market is being shaped by an electrification-led copper supercycle, EV battery metals demand, mega-merger consolidation, and Indonesian nickel policy reshaping global supply.

Copper prices broke through USD 11,600 per tonne in early December 2025, setting an all-time high and recording the metal's largest annual gain since 2009 at nearly 40%. The rally was driven by depleted exchange inventories, mine disruptions, accelerated U.S. stockpiling ahead of new tariffs, and structural demand from electrification, AI data centres, and EV adoption. BloombergNEF warned that the copper market may enter structural deficit as early as 2026, underwriting a sustained capex and M&A cycle across base-metal miners.

The Indonesian government announced a ban on new HPAL and NPI processing plants and sharply reduced the national RKAB nickel-ore production quota to 250-260 million wet metric tonnes, down from 379 million wmt in 2025, a cut of roughly 34%. The policy aims to align ore output with domestic smelter capacity, curb oversupply, and support nickel prices. As Indonesia controls about 70% of global mine production, the move has direct implications for global EV battery and stainless-steel supply chains, prompting major miners to reassess sourcing strategies.

Rio Tinto Group and Glencore plc disclosed preliminary discussions about an all-share merger that, if consummated, would create a mining company with an enterprise value of around USD 260 billion, the largest deal in mining history. Copper has been described as the central rationale, with Glencore's Latin American projects, including its 44% stake in Chile's Collahuasi mine, attractive to Rio Tinto. Talks were paused but later restarted under regulatory deadlines, signalling the consolidation pressure facing diversified miners as electrification demand strains supply chains.

Antofagasta plc set out plans to invest approximately USD 3.5 billion in 2025, one of the largest annual capital outlays in its history, to fund expansions across Chile and Peru. The marquee project is a USD 4.4 billion second concentrator at the Centinela copper mine in northern Chile that will add roughly 170,000 tonnes of copper-equivalent output a year, with first copper expected in 2027. The package highlights how leading copper-focused producers are accelerating growth capex to ride the structural electrification-driven demand supercycle.

Anglo American plc moved to divest its Brazilian nickel assets in the first half of 2025 as part of a strategic restructuring triggered by an unsolicited USD 49 billion takeover bid from BHP in 2025. The Barro Alto and Niquelândia operations in Brazil's Midwest attracted interest from a range of bidders. The transaction reflects a broader push by Anglo American to focus on copper, iron ore, and crop nutrients while shedding nickel and other non-core assets to defend its independence.

Copper has emerged as the breakout base metal of 2025, with prices touching record highs above USD 11,600 per tonne and gains of nearly 40% on the year. The Global Base Metal Mining Market market growth is being amplified as electrification, EV manufacturing, AI data-centre power needs, and grid expansion converge on copper-intensive infrastructure. BloombergNEF forecasts copper demand from the energy transition could triple by 2045, with structural deficit as early as 2026. In December 2025, multiple miners reported tightened concentrate availability and elevated treatment-charge negotiations as supply chains adjusted.

A wave of consolidation is sweeping the mining industry, led by Rio Tinto and Glencore's USD 260 billion merger talks in early 2025 and the lingering shadow of BHP's earlier USD 49 billion bid for Anglo American. CNBC and other outlets describe a generational M&A window driven by the need to secure copper, nickel, and other battery metals at scale. In January 2025, market commentary highlighted the strategic premium being placed on copper-heavy portfolios, with Anglo American restructuring and divesting nickel and steelmaking assets to focus on its core base-metal franchise.

Indonesia's late-2025 ban on new HPAL and NPI processing plants and 34% cut to its nickel-ore production quota are tightening battery-grade nickel availability and lifting prices. With Indonesia controlling around 70% of global nickel mine production, the policy is recalibrating EV battery supply chains worldwide and pushing Western miners and OEMs toward 'Green Nickel' offtake agreements, alternative geographies, and recycling. In November 2025, EV battery manufacturers reported renewed urgency in securing long-term nickel supply contracts outside Indonesia.

Demand for copper, nickel, lithium, and other battery-grade base metals is rising in line with global EV adoption, with copper-from-EV consumption growing at roughly 10.5% per year. Major miners including Antofagasta, Freeport-McMoRan, Glencore, and Vale are recalibrating capex toward copper, nickel, and zinc growth projects to capture the demand wave. In 2025, Antofagasta committed USD 3.5 billion in annual capex and approved its USD 4.4 billion Centinela second concentrator, signalling the scale of investment required to meet projected demand.

The Expert Market Research’s report titled “Base Metal Mining Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

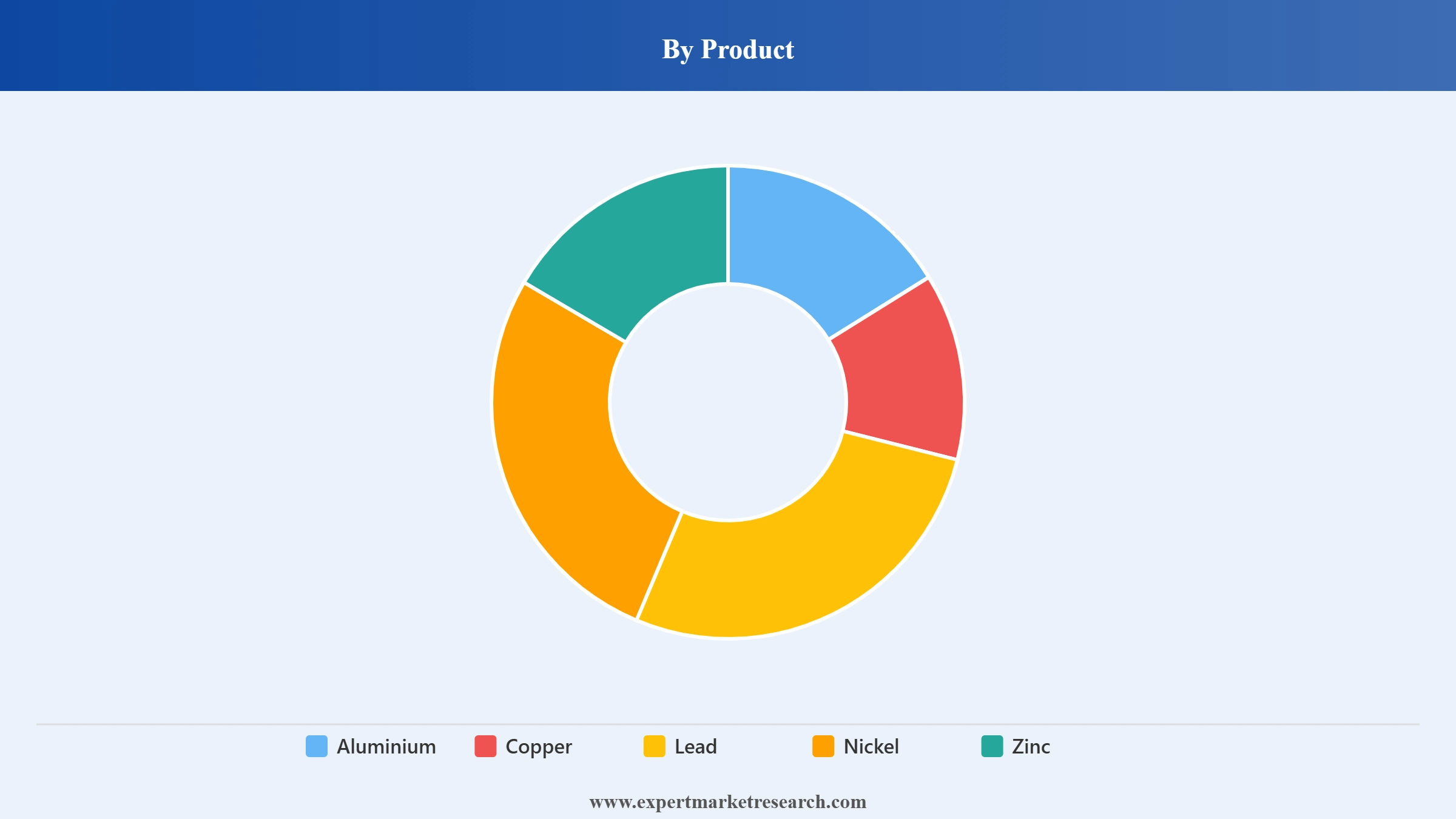

Market Breakup by Products

Key Insight: Copper is emerging as the most strategically important base metal in 2025, with record-high prices, structural deficit forecasts, and rapid demand growth from EVs, grid build-outs, AI data centres, and renewable energy. Aluminium remains the largest by volume, anchored by transport and construction. Nickel is being reshaped by Indonesian policy and the EV battery boom, while zinc and lead continue to support galvanising and battery applications. Major producers including Freeport-McMoRan, Antofagasta, Glencore, BHP, and Rio Tinto are reallocating capex toward copper and battery metals as the energy-transition supercycle intensifies.

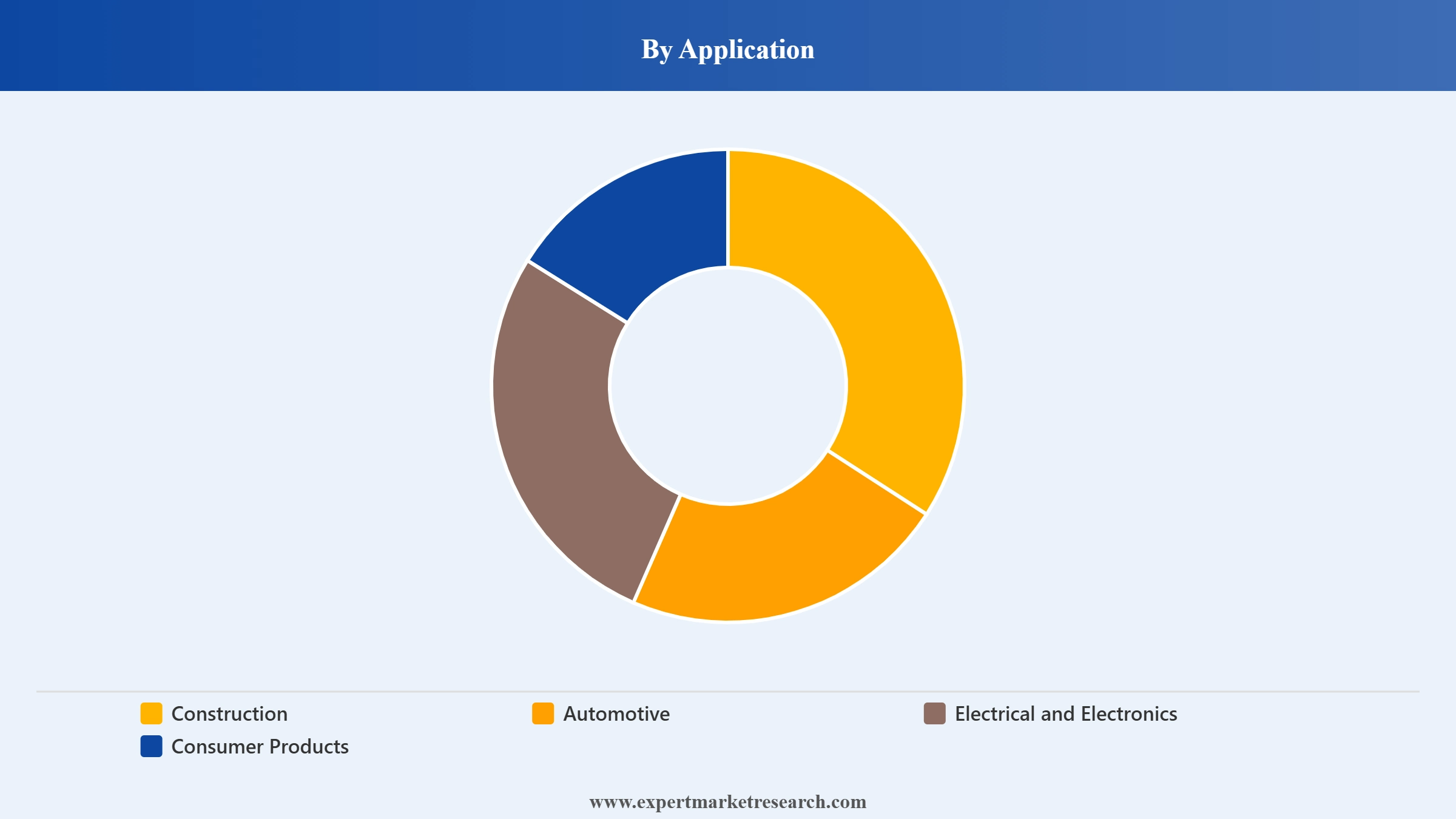

Market Breakup by Application

Key Insight: Construction is the largest application for base metals, consuming aluminium, copper, and zinc across buildings, infrastructure, and urban transport projects, particularly in Asia Pacific and the Middle East. Automotive is the fastest-growing application, with EV adoption lifting copper, nickel, and aluminium intensity per vehicle. Electrical and electronics is benefiting from grid expansion, renewable energy, and AI data-centre build-outs that demand large copper volumes. Consumer products and packaging continue to support base-metal demand, with sustainability and recycled-content programs gaining momentum across major OEM procurement.

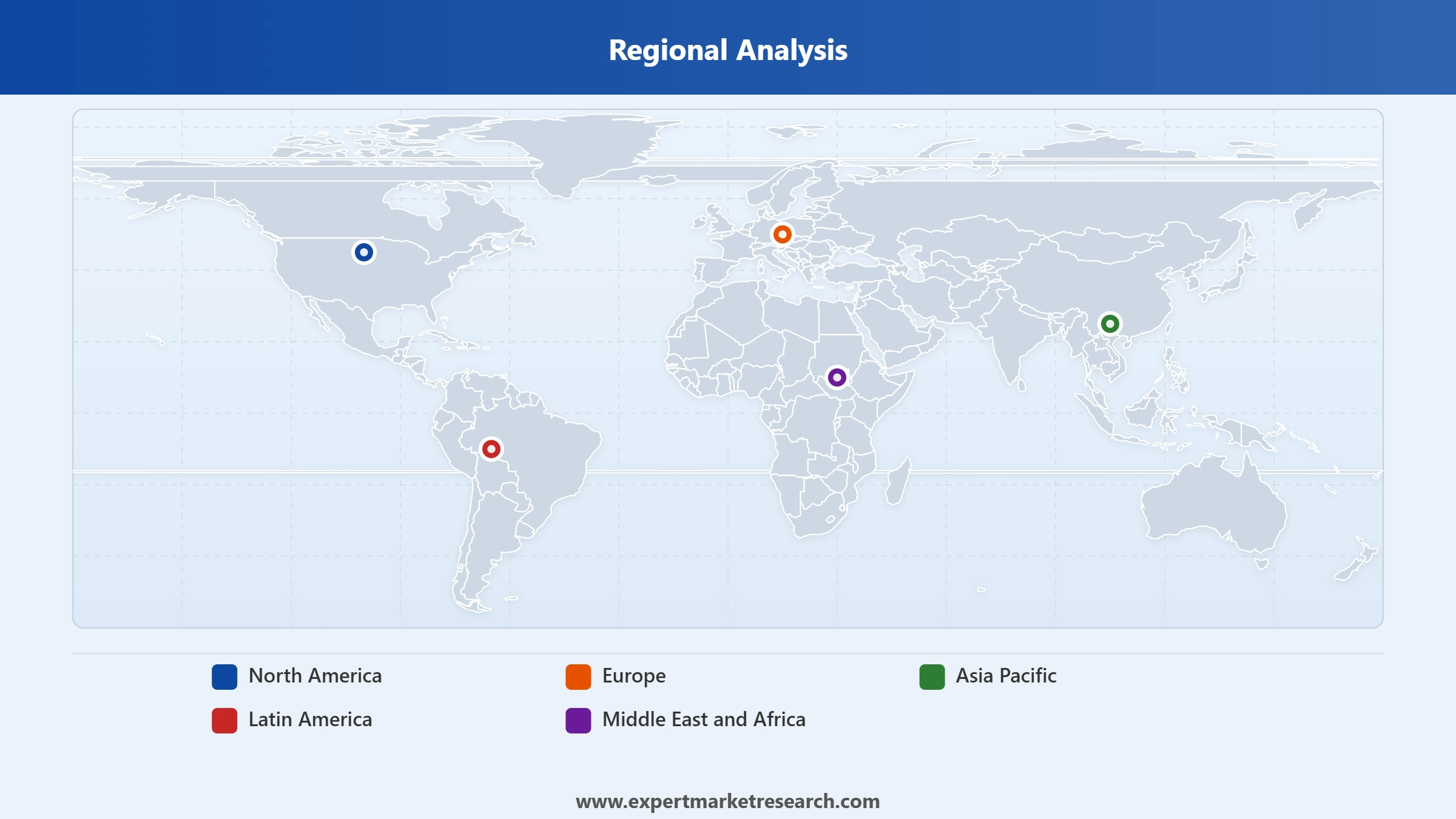

Market Breakup by Region

Key Insight: Asia Pacific dominates base-metal mining and processing, led by China's smelter base, India's downstream demand, and Indonesia's nickel supply. Latin America hosts the world's largest copper reserves, with Chile and Peru as anchor jurisdictions for Antofagasta, Freeport, BHP, and Glencore. North America is responding to U.S. tariff policy and federal incentives by accelerating domestic copper, zinc, and nickel projects. Europe is investing in recycling and refining capacity to support its energy transition, while the Middle East and Africa, led by zinc, copper, and emerging mining hubs, are seeing rising upstream investment from Chinese and Western majors.

Read more about this report - REQUEST FREE SAMPLE COPY

By Product, Aluminium and Copper jointly dominate the global base-metal mining market by value. Aluminium leads on sheer volume across transport, construction, and packaging, while Copper is gaining share rapidly on the back of record prices, electrification demand, and EV adoption. BloombergNEF forecasts copper demand from the energy transition could triple by 2045, and copper prices broke records in late 2025, lifting valuations for pure-play copper miners. Nickel is being reshaped by Indonesia's late-2025 policy shift, with battery-grade nickel commanding premiums and EV manufacturers seeking diversified supply outside the country.

Read more about this report - REQUEST FREE SAMPLE COPY

By Application, Construction remains the largest end use, anchored by infrastructure and urbanisation in Asia Pacific and the Middle East where aluminium, copper, and zinc volumes are heavy. Automotive is the fastest-growing application, with EV adoption lifting per-vehicle copper, nickel, and aluminium demand. Electrical and electronics is also expanding rapidly, lifted by grid build-outs, renewable installations, and AI data-centre power infrastructure. Consumer products and other applications, including packaging, appliances, and industrial machinery, contribute steady demand. ESG-linked offtake and recycled-content specifications are increasingly defining how miners and OEMs structure long-term contracts.

Read more about this report - REQUEST FREE SAMPLE COPY

Asia Pacific dominates the global base-metal mining and processing landscape, anchored by China's smelter and refining capacity, India's rapidly expanding downstream demand, and Indonesia's pivotal role in nickel mine supply. Indonesia accounts for roughly 70% of global nickel production, and its late-2025 policy shift to ban new HPAL and NPI plants and cut RKAB production quotas by around 34% is reshaping global EV battery supply chains. China's electrification, EV manufacturing, and infrastructure investment continue to support copper, aluminium, and zinc volumes. Indian miners are scaling base-metal production in line with national infrastructure ambitions and growing automotive output.

Read more about this report - REQUEST FREE SAMPLE COPY

Latin America is the heart of global copper supply, hosting Antofagasta, BHP, Freeport-McMoRan, Glencore, and Southern Copper assets across Chile and Peru. Antofagasta's USD 3.5 billion 2025 capex and USD 4.4 billion Centinela expansion underscore the region's strategic importance. Chile remains the world's largest copper producer, while Peru ranks among the top globally. Brazilian operations span iron ore, nickel, and zinc, with Anglo American divesting its Barro Alto and Niquelândia nickel assets in 2025. Regional miners are also navigating evolving royalty regimes, community engagement, and water-stewardship standards as ESG diligence intensifies among offtake buyers and lenders.

The Global Base Metal Mining Market is moderately consolidated at the top, dominated by diversified mining majors including BHP, Rio Tinto Group, Glencore, Vale, and Anglo American, copper specialists Freeport-McMoRan, Antofagasta, and Southern Copper, and Chinese champion Zijin Mining. Russian nickel and copper player Nornickel remains a key supplier despite geopolitical headwinds.

Competitive priorities centre on securing long-life copper, nickel, and zinc resources, scaling exposure to battery metals, deploying ESG-credentialed production, and pursuing mega-merger and tuck-in M&A. Leaders are committing record capex to brownfield expansions, particularly in Chile and Peru, while restructuring portfolios to focus on the highest-margin energy-transition metals.

Founded in 1981 and headquartered in Phoenix, Arizona, Freeport-McMoRan is one of the world's largest publicly traded copper producers, with a portfolio anchored by the Grasberg mine in Indonesia and major U.S. and South American operations. Capabilities span open-pit and underground mining, smelting, and refining of copper, gold, and molybdenum. Notable strengths include scale, low-cost production, and exposure to the electrification-driven copper supercycle.

Founded in 1888 and headquartered in London, UK, Antofagasta plc is a Chilean copper-focused mining major with operations including Centinela, Los Pelambres, and Antucoya. The company is investing approximately USD 3.5 billion in 2025 across Chile and Peru and has approved a USD 4.4 billion second concentrator at Centinela. Notable strengths include long-life Chilean copper assets, water-stewardship leadership, and a disciplined capital allocation track record.

Founded in 1974 and headquartered in Baar, Switzerland, Glencore plc is a diversified mining and trading group with leading positions in copper, nickel, zinc, and cobalt. The company holds a 44% stake in Chile's Collahuasi copper mine and is pivoting nickel output toward 'Green Nickel' certification to capture premiums from European automakers. Glencore is also at the centre of the 2025 USD 260 billion merger discussions with Rio Tinto Group.

Founded in 1885 and headquartered in Melbourne, Australia, BHP Group is the world's largest mining company by market capitalisation, with a diversified portfolio spanning iron ore, copper, nickel, and metallurgical coal. Key copper assets include Escondida in Chile and Olympic Dam in Australia. BHP's 2024 unsolicited USD 49 billion bid for Anglo American highlighted its strategic intent to scale copper exposure, although Rule 2.8 of the UK Takeover Code has paused further moves through early 2026.

Other key players in the market are Zijin Mining Group Co., Ltd., Nornickel, Rio Tinto Group, Vale, Southern Copper Corporation, and Anglo American plc, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Discover the latest insights on the Global Base Metal Mining Market 2026 with our comprehensive report. Stay ahead of the curve with valuable data on the copper supercycle, EV battery metals, mega-merger M&A, and top growth regions. Whether you are launching a new project or expanding your metals portfolio, this report gives you the clarity you need. Download your free sample now and discover the key opportunities in the thriving Global Base Metal Mining.

Refining And Metallurgy In Base Metal Mining

Sustainability Advances In Base Metal Mining

Beneficiation And Processing Technology Trends

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the base metal mining market reached an approximate value of USD 395.41 Billion.

The market is assessed to grow at a CAGR of 4.00% between 2026 and 2035.

The major drivers of the market include the expansion of various end user verticals, surge in industrialisation, rising urbanisation, infrastructural development, increasing demand for copper, rising focus of the government on pro-mining policies and an increase in disposable income.

Key trends aiding the market expansion include the growing technological improvements including the use of robotic and remote technologies, and the growing focus on recycling and sustainable mining practices.

North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa are the significant markets for base metal mining.

The products include copper, silver, zinc, lead, nickel, and aluminium, tin, among others.

Key players in the market are Freeport-McMoRan, Inc., Antofagasta plc, Zijin Mining Group Co., Ltd., Nornickel, Glencore plc, BHP Group Limited, Rio Tinto Group, Vale, Southern Copper Corporation, Anglo American plc, Others.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 585.30 Billion by 2035.

The strict government policies related to mining, including its negative environmental impact, and high-risk nature of mining operations are the key challenges in the industry.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.