Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

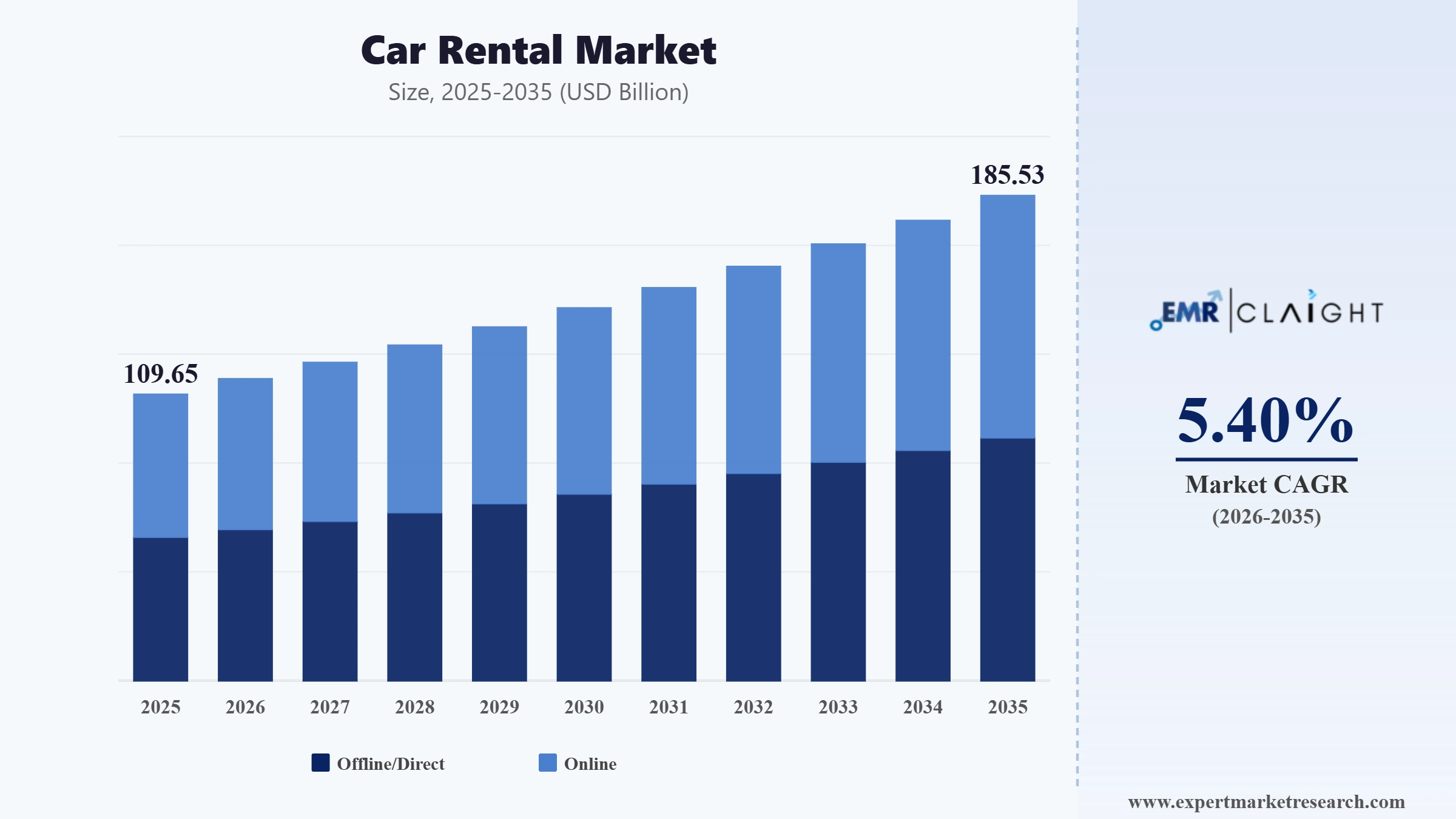

According to Expert Market Research analysis, the global car rental market was valued at approximately USD 109.65 Billion in 2025 and is projected to reach USD 185.53 Billion by 2035, registering a compound annual growth rate CAGR of 5.40% during the forecast period of 2026 to 2035. This sustained growth reflects a powerful convergence of post-pandemic travel recovery, accelerating adoption of digital booking, electric vehicle fleet expansion, and the rise of subscription-based and shared mobility models across both developed and emerging economies.

The global car rental market, encompassing the broader vehicle rental and car rental services markets, is one of the most dynamic and structurally evolving segments of the global mobility ecosystem. Serving leisure travellers, corporate accounts, insurance replacement clients, and urban commuters, the car rental industry operates at the intersection of travel technology, fleet management, and shared mobility, delivering access-over-ownership solutions across more than 100 countries worldwide.

The global car rental market trends reflect a sector undergoing profound structural transformation. The following highlights define the current competitive and operational landscape across the rental car industry:

The car rental market is characterised by a moderately consolidated competitive structure at the premium end, dominated by three major holding groups in North America, alongside strong regional players in Europe, Asia-Pacific, and emerging markets. Key entities in the global car rental market include:

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global car rental market trends are shaped by three interlocking megatrends: the sustainability imperative driving fleet electrification, the digital transformation of booking and operations, and the rise of shared mobility solutions expanding the market's addressable base. These forces are not isolated; they are mutually reinforcing drivers redefining how the car rental services market is designed, delivered, and consumed.

The electric vehicle car rental market segment has become the most transformative emerging sub-category within the global vehicle rental market. Environmental sustainability has evolved from a peripheral ESG consideration into a core strategic priority for the world's largest rental operators. Regulatory mandates across the European Union, United Kingdom, and several US states requiring phase-outs of internal combustion engine (ICE) vehicles by 2030–2035 are compelling fleet operators to accelerate EV adoption at a pace requiring significant capital investment.

Hertz's commitment to purchase up to 100,000 Tesla vehicles later partially scaled back due to depreciation pressures, nonetheless signaled a pivotal shift in fleet electrification strategy across the rental car industry. Sixt SE has committed to 40% EV and hybrid fleet composition by 2026 across its European operations. Europcar, under Volkswagen Group ownership since 2021, holds a structural EV sourcing advantage through preferential access to the VW Group portfolio: Volkswagen ID series, Audi Q4 e-tron, Porsche Taycan, positioning it uniquely for premium EV rental. In October 2025, Europcar reported a 93% year-on-year increase in battery electric vehicle rentals, confirming accelerating enterprise adoption of the electric vehicle car rental market segment.

Beyond fleet electrification, operators are investing in carbon offset programmes, renewable energy at depot facilities, and circular fleet lifecycle management sustainability criteria increasingly required by corporate procurement mandates from multinationals with Scope 3 emissions reduction targets.

The evolution of online vs offline car rental booking patterns has fundamentally restructured the car rental services market's distribution economics. The digitalization of the entire customer journey from search and booking through pick-up, in-rental experience, and return has accelerated dramatically, transforming what was once a largely analog, counter-based transaction into a seamless, mobile-first digital experience.

Online booking now accounts for the substantial majority of global rental transactions, with operator-owned apps, online travel agencies (OTAs) including Expedia, Booking.com, and Priceline, and aggregator platforms including Kayak and Rentalcars.com collectively controlling the dominant share of booking volume. The shift in online vs offline car rental booking market share is particularly pronounced among leisure travellers under 45, the highest-frequency rental demographic in mature markets. Artificial intelligence is deployed across dynamic pricing, predictive fleet maintenance, and customer service automation, enabling real-time rate adjustments based on demand forecasting, competitor pricing, and event calendars. In April 2025, Hertz partnered with UVeye to deploy AI-powered vehicle inspection kiosks nationwide; in July 2025, Hertz further partnered with Palantir Technologies to implement AI-driven fleet and workforce management across its global network.

The integration of car rental services into broader digital travel ecosystems airline booking platforms, hotel reservation systems, and corporate travel management tools (SAP Concur, Egencia, American Express GBT) is deepening the entrenchment of rental services in end-to-end travel workflows and creating durable new distribution channels.

The shared mobility revolution represents the most significant competitive threat and the most important market expansion opportunity in the contemporary car rental industry. Peer-to-peer (P2P) car-sharing platforms led by Turo in North America and Getaround in Europe have created a new vehicle rental model that bypasses traditional fleet operators, leveraging private vehicle owners as distributed rental assets. Turo reported over 350,000 active vehicle listings as of 2025, representing substantial shadow inventory competing directly with traditional daily rental in leisure and urban markets.

In response, major operators are developing competitive P2P and subscription offerings. Zipcar (Avis Budget Group) operates one of the world's largest one-way car-sharing networks. In November 2025, Sixt SE launched its SIXT+ subscription service across five additional European markets: Italy, Spain, the Netherlands, Belgium, and Austria, offering flexible monthly vehicle subscriptions with insurance coverage and vehicle-switching options. Hertz and Enterprise have similarly piloted subscription and corporate car-sharing platforms. These strategic responses reflect a recognition that the mobility market is evolving toward on-demand, asset-light access models that require rental operators to expand their service architecture beyond the traditional airport rental transaction.

The sustained growth trajectory of the car rental market is supported by a robust convergence of structural and cyclical demand drivers that operate across geographies and customer segments, underpinning the market's resilience across economic cycles.

Global urbanization, with over 56% of the world's population now in urban areas, projected to reach 68% by 2050 (United Nations), is creating structural demand for rental and shared mobility as an alternative to private vehicle ownership. In dense urban environments, the prohibitive costs of parking, insurance, depreciation, and maintenance are accelerating adoption of on-demand rental, car-sharing, and subscription mobility among younger, urban-centric demographics across North America, Europe, and Asia-Pacific.

Simultaneously, urbanization in emerging markets in South and Southeast Asia, Sub-Saharan Africa, and Latin America is driving car rental demand as a professional transportation solution in cities where public transit is inadequate, and private ownership rates remain low. In India, Indonesia, and Nigeria, the vehicle rental market serves as a primary mobility solution for an expanding middle class engaging in business travel and consumer leisure.

Regulations mandating ICE vehicle phase-outs are creating a structural tailwind: rather than requiring consumers to navigate EV ownership complexities, rental companies serve as a 'try before you buy' gateway for EV adoption, expanding the electric vehicle car rental market while fulfilling regulatory compliance requirements. Corporate sustainability mandates are equally powerful drivers: multinational corporations with net-zero Paris Agreement commitments are requiring travel management programmes to prioritise low-emission rental options, generating a structural demand shift in the high-value corporate rental segment.

Technological innovation is expanding both supply-side efficiency and demand-side convenience across the rental car industry. AI-driven fleet management systems optimize asset utilisation, predict maintenance needs, and automate pricing, dramatically improving large-scale fleet economics. Telematics integration provides real-time vehicle performance data and enables usage-based insurance (UBI) models. On the demand side, mobile app experiences, digital key technologies enabling contactless vehicle access, and integration with Google Travel and airline apps have reduced booking friction and increased impulse rental behaviour across all major markets.

The tourism vehicle rental market, the single largest application segment by revenue, has been the primary beneficiary of international travel's robust recovery from the COVID-19 trough. International tourist arrivals globally reached record levels in 2025, driven by pent-up leisure demand, strong outbound tourism from India, China, Southeast Asia, and the GCC, and sustained US and European leisure travel. International travellers are disproportionately high-frequency rental users in drive-holiday destinations including US national parks, European coastal regions, Australian outback, and Caribbean islands.

Business travel has also recovered substantially, with shorter, higher-frequency corporate trips commanding a premium for flexible, app-booked, contactless rental options. The GCC's tourism investment strategy Saudi Vision 2030's target of 150 million annual tourist visits by 2030, the UAE's expansion of Dubai and Abu Dhabi as global travel hubs, and Qatar's post-FIFA legacy infrastructure is generating particularly high-growth demand in the GCC car rental market.

A fundamental shift from ownership aspiration to access optimisation is expanding the car rental market's total addressable market. Millennials and Generation Z show a statistically lower propensity for vehicle ownership than prior generations at comparable life stages. This preference shift is reshaping short-term vs long-term car rental market dynamics: monthly subscription services providing all-inclusive mobility without purchase commitment are growing at above-market rates, while 'rental-native' consumers use rental services as a default mobility solution, not merely a vacation travel add-on.

The global car rental market is segmented across five key dimensions booking mode, application type, and vehicle type each offering distinct growth profiles, competitive dynamics, and strategic implications for market participants and investors.

By Booking Mode: Online Booking (Largest) vs. Offline Booking (Fastest-Growing)

Key Information: The online vs offline car rental booking market landscape has shifted decisively toward digital channels. Online booking encompassing operator apps (Hertz, Enterprise, Sixt), OTA platforms (Booking.com, Expedia, Priceline), and aggregators (Kayak, Rentalcars.com, Skyscanner) accounts for over 65% of global rental transactions by volume as of 2025. This channel dominance is most pronounced among leisure travellers under 45 in North America, Western Europe, and urban Asia-Pacific markets.

Offline booking walk-in counter rentals, telephone reservations, and travel agent bookings is demonstrating a paradoxical growth trend particularly in developing markets and the ultra-premium segment. Across Sub-Saharan Africa, South and Southeast Asia, and parts of Latin America, offline booking remains the dominant car rental services market channel due to lower smartphone penetration and preference for in-person service. In the ultra-high-net-worth segment, concierge-driven offline bookings represent a high-value niche maintaining above-average growth as personalised travel services expand.

By Application: Leisure/Tourism (Largest) vs. Business (Fastest-Growing)

Key Information: The leisure/tourism car rental market share makes leisure and tourism the single largest application segment globally by volume. Vacation travellers, international tourists, and domestic road trippers collectively constitute the primary demand driver at airport pick-up locations and popular destination cities. The tourism vehicle rental market generates disproportionate demand during summer peak season in Europe and North America with seaside, mountainous, and national park destinations showing the highest rental incidence and during global holiday travel periods.

The business car rental market segment is the fastest-growing application category, driven by robust corporate travel recovery, business activity expansion in emerging markets, and the increasing corporatisation of formerly informal business travel in India, Southeast Asia, and Africa. Business rentals command higher average daily rates, benefit from negotiated corporate account pricing guaranteeing volume and loyalty, and exhibit lower price elasticity than leisure demand making this segment disproportionately attractive for operators with strong corporate sales infrastructure.

By Vehicle Type: Luxury (Largest) vs. Economy (Fastest-Growing)

Key Information: In the luxury car rental market segment, premium sedans, high-end SUVs, sports cars, and executive class vehicles constitute the largest vehicle category by revenue value reflecting significantly higher achievable daily rates. Luxury car rental market demand is driven by destination wedding travel, premium leisure tourism (European Riviera, US mountain resorts, UAE), senior executive corporate travel, and event-based demand peaks (Formula 1 grands prix, major business conferences). Operator premium sub-brands Hertz Dream Cars, Sixt Excellence, Europcar Prestige have built dedicated service architectures serving this high-margin category.

Economy car rental market growth is outpacing all other vehicle type segments, driven by the expanding middle class in Asia-Pacific and Africa, budget-conscious traveller growth in backpacker tourism destinations, and cost optimisation in corporate travel programmes. The economy car rental market additionally benefits from the most favourable EV transition economics small-format EVs (BYD Seagull, Nissan Leaf, Renault Zoe) have reached purchase price parity with equivalent ICE economy models in several European and Asian markets, enabling simultaneous fleet electrification and volume growth without premium rate requirements.

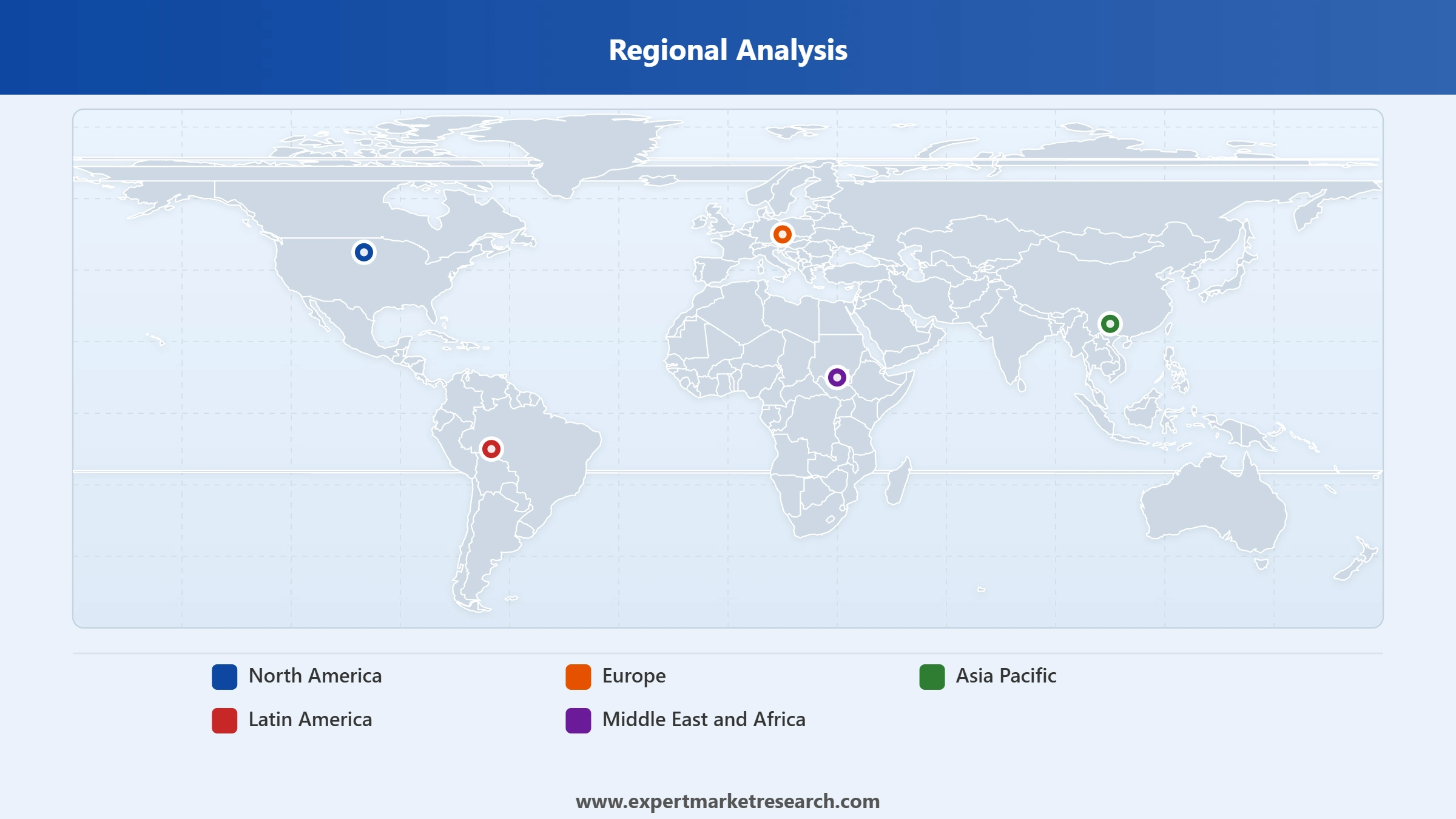

Region Outlook (Revenue, Billion, 2026-2035)

Key Information: North America dominates the global car rental market with approximately 38% revenue share in 2024, supported by strong leisure and business travel demand and the presence of major operators including Enterprise, Hertz, and Avis Budget. Europe is the second-largest market, driven by robust inbound tourism across Western Europe and fleet electrification initiatives. Asia Pacific is the fastest-growing region, projected to expand at a CAGR of 11.3% from 2025 to 2030, led by rising disposable incomes, urbanization, and app-based rental platform adoption across China, India, and Southeast Asia. Latin America shows steady growth driven by expanding tourism infrastructure in Brazil and Mexico, while the Middle East and Africa is an emerging high-potential market backed by large-scale hospitality investments in GCC countries aligned with Vision 2030.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America maintains its position as the world's largest car rental market, accounting for approximately 38% of global market value in 2025. The United States is the undisputed epicenter of the industry, home to the three largest car rental holding groups globally Enterprise Holdings, Hertz Global Holdings, and Avis Budget Group and the world's most extensively developed airport rental infrastructure. US airports including Hartsfield-Jackson Atlanta, Los Angeles International, Dallas/Fort Worth, and Chicago O'Hare serve as the highest-volume car rental pick-up locations globally, with consolidated rental facility (CONRAC) buildings processing millions of transactions annually.

The US market is characterised by high penetration of digital booking channels, strong corporate accounts infrastructure, and intensifying competition from ridesharing platforms (Uber, Lyft) in urban markets. Canada represents a significant and growing sub-market, with major operators maintaining strong presence at Toronto Pearson, Vancouver International, and Montreal-Trudeau airports. The Canadian market benefits from strong US-cross-border leisure travel, a resilient domestic business travel segment, and relatively limited ridesharing penetration in non-metropolitan areas conditions that sustain healthy rental utilization rates across the national network.

Europe represents the second-largest car rental market globally and the epicenter of the industry's EV and shared mobility transformation. The European market is structurally distinct from North America in several important respects: higher urban density creates stronger demand for car-sharing and short-duration rentals; inter-city rail connectivity (particularly in Western Europe) competes with rental for business travel; and the EU's aggressive EV transition regulatory framework is forcing fleet electrification at a pace and scale unmatched in other global markets.

Key European markets include Germany (the continent's largest economy and home to Sixt SE's headquarters), France (Europcar's home market), the United Kingdom (recovering strongly post-Brexit with inbound tourism driving airport rental demand), Spain (one of Europe's highest-volume summer tourist rental markets), and Italy. The Volkswagen Group's acquisition of Europcar and subsequent integration with VW's own mobility services business creates a vertically integrated auto-to-rental ecosystem in Europe that could reshape competitive dynamics over the medium term.

Asia-Pacific is the world's fastest-growing car rental market, driven by the demographic and economic momentum of its two largest markets, India and China, alongside rapid development in Southeast Asian markets including Indonesia, Vietnam, Thailand, and the Philippines. The region's growth is underpinned by rising middle-class incomes, accelerating airport infrastructure development, expanding inbound international tourism, and, in markets like India, a structurally distinctive rental model built around chauffeur-driven services that address urban traffic complexity and navigational challenges for domestic and international business travelers.

India deserves particular strategic attention in the context of this report's GSC data: India ranks as the second-largest country by impressions (542), behind only the United States (1,881). Key Indian operators including Carzonrent, Myles (part of Mahindra Finance), Zoomcar (peer-to-peer), and Savaari have built technology-enabled platforms serving both business and leisure segments. Japan, South Korea, and Singapore represent mature APAC rental markets with high service quality standards, strong airport rental infrastructure, and growing inbound tourism demand, particularly from China following the lifting of COVID-era travel restrictions.

The Middle East and specifically the GCC countries of the UAE, Saudi Arabia, Qatar, Kuwait, Bahrain, and Oman represent one of the most strategically compelling emerging opportunities in the global car rental market. Saudi Vision 2030's ambitious tourism diversification strategy, targeting 150 million tourist visits annually by 2030 (versus approximately 18 million in 2019), is creating massive demand for infrastructure for rental services. The UAE, anchored by Dubai's world-class aviation hub and Abu Dhabi's MICE tourism ecosystem, maintains the most developed GCC rental market, with operators including SIXT, Budget, Hertz, and regional champions Udrive and ekar competing across the value spectrum.

Africa presents the market's most significant long-term untapped growth opportunity, with Sub-Saharan economies showing rising corporate travel activity, expanding middle-class leisure travel, and tourism infrastructure development. Ghana, which appears in EMR's GSC data ranking position 7–8 for CAGR-specific queries, exemplifies this opportunity: West Africa's growing business hub is attracting investment from operators building chauffeur and self-drive platforms for the region's business travel demand. Kenya (safari tourism), Nigeria (West Africa's largest economy), and South Africa (the continent's most developed rental market) represent the core Africa opportunity set for operators and investors.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global car rental market operates within a competitive structure that combines large, vertically integrated holding groups with strong global airport networks at the premium end, alongside agile regional operators and technology-driven disruptors competing across niche segments and emerging markets. The industry exhibits moderate concentration at the global level but significant fragmentation at the regional and local market level, particularly in Asia-Pacific, Africa, and Latin America.

Founded in 1918 and headquartered in Estero, Florida, the Hertz Corporation is one of the world's oldest and most recognized car rental brands. Hertz operates under the Hertz, Dollar, and Thrifty brands across over 5,500 locations globally, including approximately 1,900 airport locations. In 2024, Hertz undertook a major fleet restructuring program, divesting approximately 30,000 electric vehicles and implementing its "Buy Right, Hold Right, Sell Right" fleet strategy, achieving a fleet composition where over 60% of vehicles were less than one year old by year-end 2024.

Founded in 1946 and headquartered in Parsippany, New Jersey, Avis Budget Group operates the Avis, Budget, and Zipcar brands across more than 180 countries and territories. The company manages a fleet of nearly 500,000 vehicles and holds approximately 12% of the global market. Avis Budget posted revenues of USD 2.7 billion in Q4 2024, driven by sustained leisure travel demand, and completed a multi-year fleet supply agreement with Stellantis in February 2024 to ensure consistent fleet renewal access.

Enterprise Holdings, founded in 1957 and headquartered in St. Louis, Missouri, is the world's largest car rental company by fleet size and revenue, managing over 1.2 million vehicles across its Enterprise Rent-A-Car, National Car Rental, and Alamo brands in over 90 countries. The company reported revenue of approximately USD 38 billion in 2024, reflecting its dominant position across both the corporate and leisure segments.

Founded in 1912 and headquartered in Pullach, Germany, Sixt SE is a leading premium mobility services provider operating across more than 110 countries. The company offers a range of services including car rental, car sharing, ride-hailing, and fleet management solutions under a unified digital platform. Sixt secured a multi-year supply agreement with Stellantis in January 2024 for up to 250,000 vehicles, ensuring fleet diversification and electrification capacity. In November 2025, Sixt signed an MoU with Al-Futtaim BYD Saudi Arabia to integrate BYD new-energy vehicles into its Gulf rental fleet.

Other key players in the market are Europcar Mobility Group, Localiza, ANI Technologies Private Limited (Ola Cabs), Carzonrent, Bettercar Rental LLC, Shenzhen Zhizun Car Rental Co. Ltd., Ace Rent A Car Reservations Inc., Budget Rent A Car System Inc., Midway Auto Group, EMMANKO AG, ALD Automotive, Movida, Al-Futtaim Vehicle Rentals (AVR), and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock the full potential of the global car rental opportunity with our comprehensive 2026 market intelligence report. Whether you are a fleet operator exploring strategic expansion, an investor evaluating market entry positions, or a technology provider assessing partnership opportunities, this report delivers the data clarity and analytical depth you need. From detailed segment-level forecasts and regional growth roadmaps to competitive benchmarking and emerging trend analysis, everything you need to navigate this dynamic industry is in one place. Download your complimentary sample now and begin exploring the opportunities shaping the future of global vehicle rental.

South Korea Car Rental Market

Germany Car Rental Market

Vietnam Car Rental Market

India Car Rental Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the global market for car rentals attained a value of approximately USD 109.65 Billion.

The market is projected to grow at a CAGR of 5.40% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035, reaching a value of USD 185.53 Billion by 2035.

The market's growth is primarily driven by the sustained recovery and expansion of international and domestic leisure and business travel, the rapid proliferation of digital and mobile booking platforms that have lowered the friction of vehicle access, the growing preference among millennials and urban consumers for on-demand mobility over vehicle ownership, increasing airport infrastructure development across emerging markets that expands rental service catchment areas, fleet electrification and sustainability initiatives that align car rental services with evolving corporate and government environmental mandates, and the strategic convergence of traditional rental operators with ride-hailing and peer-to-peer platforms that broadens distribution reach and customer acquisition.

Key trends shaping the global car rental market include the accelerating convergence of traditional rental platforms with ride-hailing and peer-to-peer car sharing ecosystems, exemplified by the Turo and Uber integration launched in 2025. AI-powered fleet management, dynamic pricing algorithms, and contactless customer workflows are becoming standard operational investments. The EV integration trend, despite short-term adoption headwinds demonstrated by Hertz's 2024 fleet restructuring, remains a long-term strategic priority driven by regulatory mandates and corporate sustainability commitments. Asia Pacific's emergence as the fastest-growing region is creating significant expansion opportunities for both global majors and local digital-first operators. Finally, the shift toward flexible, subscription-based rental models is gaining traction among urban consumers and corporate clients seeking predictable mobility budgeting over traditional per-day transactional pricing.

North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa are the major regions covered in the Global Car Rental Market report.

The global car rental market is segmented by booking mode into offline/direct and online channels. Online booking is the dominant segment, accounting for over 71% of global revenue in 2024, driven by mobile app adoption, real-time price comparison capabilities, and the growing use of travel aggregator platforms. Offline bookings, while declining proportionally, remain important for corporate negotiated accounts, insurance replacement rentals, and markets with lower internet penetration. Both channels are expected to register growth in absolute terms through 2035, with online maintaining an accelerating share advantage.

Leisure/tourism, business, local usage, airport transport, outstation, and others are the significant application types of car rental.

The different vehicle types considered in the market report are luxury/premium cars, economy/budget cars, executive cars, SUVs, and MUVs.

The key players in the market include The Hertz Corporation, Avis Budget Group, Enterprise Holdings Inc., Sixt SE, Europcar Mobility Group, Uber Technologies Inc., Localiza, ANI Technologies Private Limited (Ola Cabs), Carzonrent, Bettercar Rental LLC, Shenzhen Zhizun Car Rental Co. Ltd., Ace Rent A Car Reservations Inc., Budget Rent A Car System Inc., Midway Auto Group, EMMANKO AG, ALD Automotive, Movida, and Al-Futtaim Vehicle Rentals (AVR).

The car rental market in North America is expected to experience significant growth opportunities due to the presence of major car rental operators in the region, such as Avis Budget Group and Enterprise Rent-a-Car.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Booking Mode |

|

| Breakup by Application |

|

| Breakup by Vehicle |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.