Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

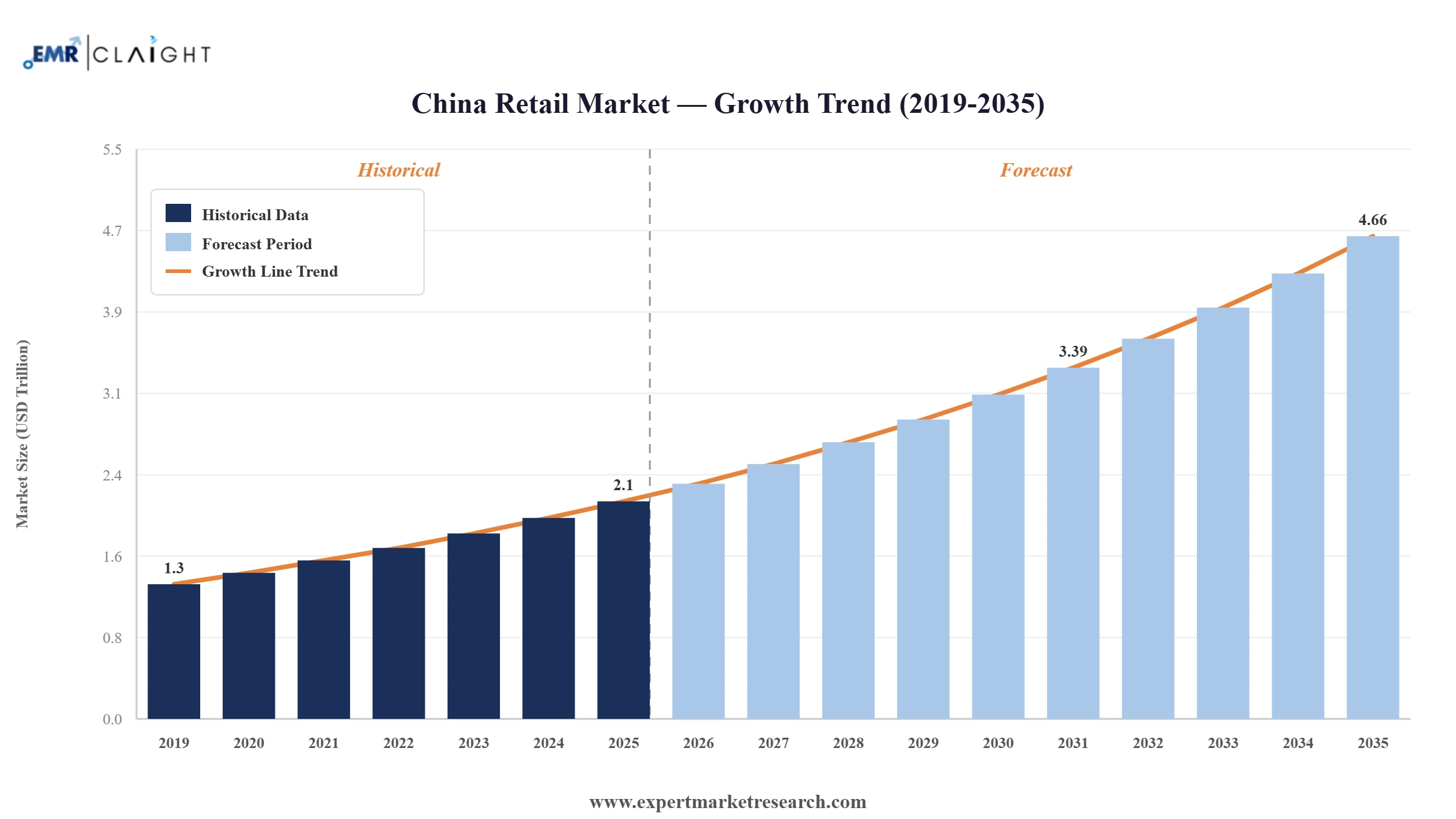

The China Retail Market reached a value of USD 2.10 Trillion at 2025 and is projected to expand at a CAGR of around 8.30% during the forecast period of 2026-2035. With the booming growth of e-commerce and social commerce, an expanding middle-class consumer base, rising demand for luxury and premium goods, and the widespread adoption of artificial intelligence and big data across retail operations, the market is expected to reach USD 4.66 Trillion by 2035.

According to China’s National Bureau of Statistics, total retail sales of consumer goods reached 12.77 trillion yuan in the first quarter of 2026, supported by stronger online shopping activity and rising service consumption. Online retail sales increased 8% year-on-year, while tourism, cultural entertainment, and catering services continued to record stable growth, reflecting improving consumer confidence across the China retail market.

According to South China Morning Post, China's retail sales grew 2.8% year on year in the first two months of 2026, the strongest growth since October 2025, driven by an extended Lunar New Year holiday that boosted spending on food, clothing, and leisure services. The National Bureau of Statistics noted that pro-consumption government policies helped unlock household spending, reinforcing momentum across the China retail market heading into 2026.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| China Retail Market Report Summary | Description | Value |

| Base Year | USD Trillion | 2025 |

| Historical Period | USD Trillion | 2019-2025 |

| Forecast Period | USD Trillion | 2026-2035 |

| Market Size 2025 | USD Trillion | 2.10 |

| Market Size 2035 | USD Trillion | 4.66 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 8.30% |

| CAGR 2026-2035 - Market by Region | Southwestern China | 9.5% |

| CAGR 2026-2035 - Market by Region | Northwestern China | 8.9% |

| CAGR 2026-2035 - Market by Product | Beauty and Personal Care | 9.6% |

| CAGR 2026-2035 - Market by Distribution Channel | Online Stores | 12.4% |

| 2025 Market Share by Region | North China | 13.1% |

The China retail market is dynamic and is powered by rapid urbanization, an expanding middle class population, and technological advancement. The country is experiencing a rapid shift toward online retail, with e-commerce giants such as Alibaba, JD.com, and Pinduoduo having taken a dominant position in the entire space. The market growth is also getting instigated by the growing disposable incomes together with an ever-changing culture of consumer behavior.

The retail demand in China is equally going strong for both local and imported products, as Chinese consumers have grown significantly keen on quality and brand reputation. Within the mega cities, physical retail shopping trend remains strong as some of the shopping malls boast flagship stores. This blended experience of online and offline is quickly becoming the norm known as "omnichannel retail" where consumers appreciate shopping online, going to a brick-and-mortar store to collect their orders, or skimming over products they might want to purchase online. The effects of social commerce and live streaming marketing strategies are further driving increased sales with brands building innovative connections with consumers as they reach them through platforms like WeChat, Douyin, and Taobao Live.

The growing population in China is becoming health-conscious, pushing demand for almost all forms of fitness items such as organic foods, supplements, and skincare products. This health-conscious demographic represents a key niche driving the China retail market. With an ever-increasing disposable income, most consumers are now turning to care for their health. The online health platforms and retail stores that house organic, vegan, and fitness-related products have proliferated with this shift. The domestic and international brands are also cashing in on this growth trend and encouraging healthier lifestyles by advertising and innovating their products and services in this fast-growing niche.

The China retail market is experiencing growth through the rising popularity and adoption of luxury goods from the high-end consumers in the country, especially those in cities such as Beijing, Shanghai, and Guangzhou. High-end fashion, watches, cars, and electronics are in high demand as the middle-class population keeps on stretching. The new wave of consumers, or rather the middle class, are young, tech-savvy. These are consumers who tend to be increasingly enamored of personalized experiences and exclusive products. As a result, retailers in China are widely adopting e-commerce platforms and influencer marketing to incentivize this growing consumer base.

The key trends of the China retail market include e-commerce and online shopping boom, move towards sustainable and ethical consumption, market transformation with Artificial Intelligence and Big Data, and increasing demand for luxury goods.

In February 2025, Alibaba Group Holding Ltd. announced a strategic partnership designed to embed advanced artificial intelligence services into consumer technology products, aimed at enhancing user experience and driving incremental retail sales through intelligent personalisation features. The move was consistent with Alibaba's broader stated strategy of becoming an AI-first technology company, with its retail and e-commerce businesses serving as primary proving grounds for applied AI deployment at scale. By embedding AI-driven product recommendations, dynamic pricing, and intelligent search capabilities directly into consumer technology devices, Alibaba positioned itself to capture purchase intent earlier in the consumer journey, before shoppers even open a dedicated shopping app. This represented a meaningful evolution in the social commerce and retail-tech integration approach that Chinese e-commerce platforms have been pioneering for over a decade, moving from reactive recommendation engines to proactive, ambient retail experiences embedded in everyday consumer devices. The partnership underscored the intensifying race among China's technology and retail giants to leverage AI as a core source of competitive advantage, a trend that is reshaping the structure of China's retail distribution landscape through the forecast period.

In the second half of 2025, German retail company Metro AG planned to open a new store in Haikou, the capital of South China's Hainan province, in a high-profile commercial complex combining duty-free shopping, luxury retail, fast-fashion brands, sports labels, and upscale dining options. The development reflected the growing strategic importance of Hainan as a consumption destination within China's retail geography, following the island province's designation as a free trade port and the Chinese government's continued expansion of duty-free shopping quotas to attract domestic consumption that would otherwise flow to international destinations. Hainan's duty-free retail model has rapidly evolved from a niche sector into a major consumption magnet, with major international luxury brands, global cosmetic companies, and global retail chains increasingly establishing flagship presences on the island to capture the large volumes of premium spending by Chinese consumers seeking international brands at competitive prices. Metro AG's planned Haikou entry illustrated how international retailers are recognising the opportunity created by China's structured effort to build a domestically competitive luxury and premium retail ecosystem through targeted free trade zone policy rather than relying solely on outbound shopping tourism.

In September 2024, Mondelez International announced that it had signed an agreement to acquire a significant majority stake in Evirth, a Shanghai-based manufacturer of frozen-to-chilled cakes and pastry products and one of China's leading companies in this rapidly growing food retail category. Founded in 2013, Evirth specialises in products including mille crepe cakes, Swiss cake rolls, mousse cakes, cheesecakes, snowy mooncakes, and puffs, distributed across club stores, retail chains, catering operations, and new-media commerce channels. The frozen-to-chilled cakes and pastries category in China was estimated at approximately USD 3 billion at the time of the deal and was growing at a CAGR of around 15%, making it one of the most attractive food retail sub-categories in the market. Mondelez had already held a minority stake in Evirth prior to the acquisition, having partnered to develop Oreo and Philadelphia-branded cake and pastry innovations for the Chinese market. The deal strengthens Mondelez's strategic position in China's premiumising food retail landscape, where younger consumers in first and second-tier cities are increasingly seeking fresh, high-quality, and brand-endorsed snacking experiences that go beyond traditional packaged formats.

In October 2024, UNIQLO launched a new sustainable apparel line that directly incorporated traditional Chinese cultural motifs, positioning the collection at the intersection of the dominant Guochao consumer movement and the growing demand for eco-conscious fashion among China's younger consumer base. The Guochao trend, which reflects a surge in national cultural pride and preference for brands that authentically integrate Chinese heritage and aesthetics, has been one of the defining forces reshaping China's apparel and fashion retail segment. By aligning with this movement through a product line that also carried sustainability credentials, UNIQLO demonstrated the increasingly sophisticated requirement for international fashion brands to localise their product narratives to resonate meaningfully with Chinese consumers who are simultaneously drawn to cultural identity and environmental responsibility. The launch represented a significant strategic pivot for the brand in its China retail strategy, moving beyond simple localization into deeper cultural storytelling as a source of competitive differentiation. The initiative also served as a case study for other international fashion and specialty retailers navigating the complex task of competing in China's dynamic and fast-evolving apparel market.

In August 2024, JD.com confirmed a substantial investment to expand its rural supply chain infrastructure, deploying artificial intelligence-powered demand forecasting and advanced logistics technologies to serve consumers in China's lower-tier cities more efficiently and cost-effectively. The investment reflected JD.com's strategic ambition to deepen retail penetration beyond Tier-1 and Tier-2 urban centres, where e-commerce adoption is already mature and competitive intensity is highest, and instead capture the substantial untapped consumption potential of China's rural and lower-tier city population. JD.com's rural supply chain expansion was part of a broader industry-wide push by China's leading e-commerce platforms to extend last-mile delivery capabilities and reduce logistics costs in regions where physical retail infrastructure remains limited. By combining AI-driven inventory management with investments in dedicated rural logistics facilities, JD.com aimed to make the same-day and next-day delivery standards already familiar to urban Chinese consumers achievable in smaller cities and county-level markets. The initiative underscored the critical role that supply chain technology investment plays in the competitive dynamics of China's retail market as growth increasingly shifts from saturated urban markets to the country's vast interior.

China's e-commerce sector continues to expand at a pace that far outstrips most mature markets, with online retail sales surging to approximately 7 trillion yuan, equivalent to roughly USD 981 billion, in the first half of 2024 alone, representing a 9.8% year-on-year increase. Online retail now accounts for approximately 25% of China's total retail sales, and this share continues to rise as infrastructure improves and digital adoption deepens across lower-tier cities. The live-stream commerce format has been a particularly powerful growth engine, with live-stream sales estimated at USD 694.5 billion in 2024 and more than 600 million Chinese consumers engaging with live-stream shopping events daily. Platforms including Alibaba's Taobao Live, Douyin, and JD.com's own live channels have made live commerce a mainstream retail format rather than a novelty, blending entertainment with commerce to drive impulse purchases and build brand discovery in a highly engaging environment. Instant retail, which enables delivery within 30 to 60 minutes for a wide range of products, is further blurring the distinction between online and offline retail, with Alibaba's Hema, JD 7Fresh, and Meituan driving rapid adoption of this model across urban China. Expert Market Research specifically identifies the e-commerce and online shopping boom as one of the four major trends shaping the China Retail Market through the forecast period, reflecting its structural rather than cyclical nature.

The integration of artificial intelligence and big data analytics has moved from a competitive advantage to a baseline operational requirement for China's leading retailers and e-commerce platforms. Alibaba committed to investing CNY 380 billion in AI and cloud computing through 2027, with retail personalisation and supply chain optimisation among the primary stated applications. JD.com has deployed autonomous delivery pods in multiple cities, cutting last-mile delivery costs while expanding service reach. Retailers including Yonghui are leveraging design and data expertise from strategic partners to refresh store layouts and reduce inventory shrinkage. AI-powered demand forecasting is enabling more precise inventory positioning across the country's vast logistics networks, reducing waste and improving availability. For consumers, AI is making its presence felt through increasingly personalised product recommendations, intelligent search, dynamic promotions, and chatbot-assisted shopping journeys that adapt in real time to individual browsing and purchasing patterns. Expert Market Research identifies the market transformation driven by AI and big data as one of the key trends shaping the China Retail Market across the forecast period, a position that is supported by the extraordinary scale and pace of technology investment across the sector.

Consumer preferences in China are shifting meaningfully toward products and brands that demonstrate credible commitments to environmental sustainability, ethical sourcing, and social responsibility, particularly among the younger urban consumers who are reshaping the country's retail demand profile. The Guochao movement, which combines cultural pride with preferences for locally produced and heritage-inspired goods, has intersected with sustainability trends to create a demand for products that feel both authentically Chinese and environmentally responsible. UNIQLO's October 2024 launch of a sustainable apparel line incorporating traditional Chinese cultural motifs was a direct market response to this intersection, reflecting how international retailers are rethinking product development to speak simultaneously to national identity and ecological values. Chinese e-commerce platforms are responding by expanding sustainable product ranges, creating dedicated "green" shopping channels, and implementing carbon tracking features that allow consumers to measure the environmental footprint of their purchases. Government policy is amplifying these trends, with China's national sustainability commitments creating a regulatory and reputational environment in which retailers that fail to credibly address environmental concerns face growing risk of consumer rejection, particularly in premium and luxury segments. Expert Market Research identifies the move toward sustainable and ethical consumption as one of the defining trends shaping the China Retail Market through 2035.

China's appetite for luxury goods is undergoing a structural expansion that goes well beyond cyclical patterns, as the country's growing population of affluent and aspirational consumers drives sustained demand for premium international brands, high-quality domestic labels, and exclusive shopping experiences. Expert Market Research identifies increasing demand for luxury goods as one of the four major trends shaping the China Retail Market through the forecast period, a view consistent with data showing China accounting for a disproportionate share of global luxury consumption growth. The expansion of duty-free retail zones in Hainan under China's free trade port policy has created a domestically competitive luxury purchasing environment, with annual duty-free sales in Hainan exceeding USD 10 billion in recent years and continuing to climb as more brands open flagship stores on the island. Younger Chinese luxury consumers, particularly Gen Z and Millennial shoppers, are pursuing premium experiences both in-store and through digital channels, with luxury brands increasingly investing in live-stream events, personalised digital engagement, and exclusive online product drops to reach this demographic. The premiumisation of everyday categories including food, beverages, skincare, and home furnishings further reflects how the luxury mindset is diffusing beyond traditional high-ticket categories into a broader range of consumer goods, expanding the addressable market for premium retail across China's diverse tier-city landscape.

Cross-border e-commerce has led to huge scope for growth in the China retail market. Consumers are increasingly shifting towards more high-end brands and products with sophisticated tastes and preferences for foreign products such as cosmetics, fashion, and foods. Tmall Global and JD Worldwide offer routes for internationalization to Chinese shoppers much more easily. The opportunity thus brings great chances for foreign investors to access a mature market like China's without a fixed presence.

Heightened environmental consciousness among consumers in China has led to rising demand for environment-friendly products, thereby boosting the growth of the China retail industry. Ethical brands that offer not only green but also recyclable packages and organic or energy-efficient products can capitalize on this opportunity to gain greater market shares. This trend also matches the wider objectives of China in sustainability and gives an edge to retail companies targeting eco-conscious population while contributing to positive environmental wellbeing.

The skyrocketing growth of e-commerce and digital platforms has created a huge impetus to the growth of the China retail market. China boasts of a growing population with good technology literacy and high smartphone penetration, which, in turn, has made online shopping part and parcel of daily lives. The entrance of major e-commerce players such as Alibaba and JD.com, along with the use of AI, big data, and mobile payments, has transformed shopping experiences. Such changes are reshaping the retail landscape and increasing the demand for more innovative digital solutions and omnichannel strategies across the country.

Government policies boosting domestic product consumption are also now serving as catalysts the high retail demand in China. Such measures include tax reductions, consumer subsidies, and urbanization-promoting policies that have hence created the best environment for retail. This initiative also contributes to the consumer economy, even establishing investments and infrastructural developments in retail across most demographics within the country. These policies also stimulate demand while creating new opportunities for retailers, thereby propelling market growth.

The EMR’s report titled “China Retail Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Product

Market Breakup by Distribution Channel

Market Breakup by Region

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Market Insights by Products

The increasing disposable income and the tendency to buy premium and organic food and beverage products for both convenience and healthy living are contributing to boosting growth in the China retail market. Growing awareness about personal well-being and hygiene are also aligning well with the increasing middle-class population, driving the personal and household care sector in China. Consumers are increasingly investing resources to develop skincare, beauty, and hygiene products, thus augmenting innovations and brand loyalty in this sector. Retailers are increasingly penetrating the clothing sector as consumers demand for high-quality trendy clothing, extending their reach into e-commerce and maximizing their digital platforms for fast fashion, footwear, and accessories.

The expanding real estate market in China and rising consumer inclination towards home improvements are also greatly contributing to the growth of the furniture and home décor segment. In addition, the electronics and household appliances sector has made the market reach new heights with rapid technological advancement in smart home devices, personal electronics, and energy-efficient appliances. Increasing adoption of health supplements, over-the-counter medicines, and advancement in healthcare facilities has brought in significant opportunity in the retail sector pharmaceutical trading and drug selling.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

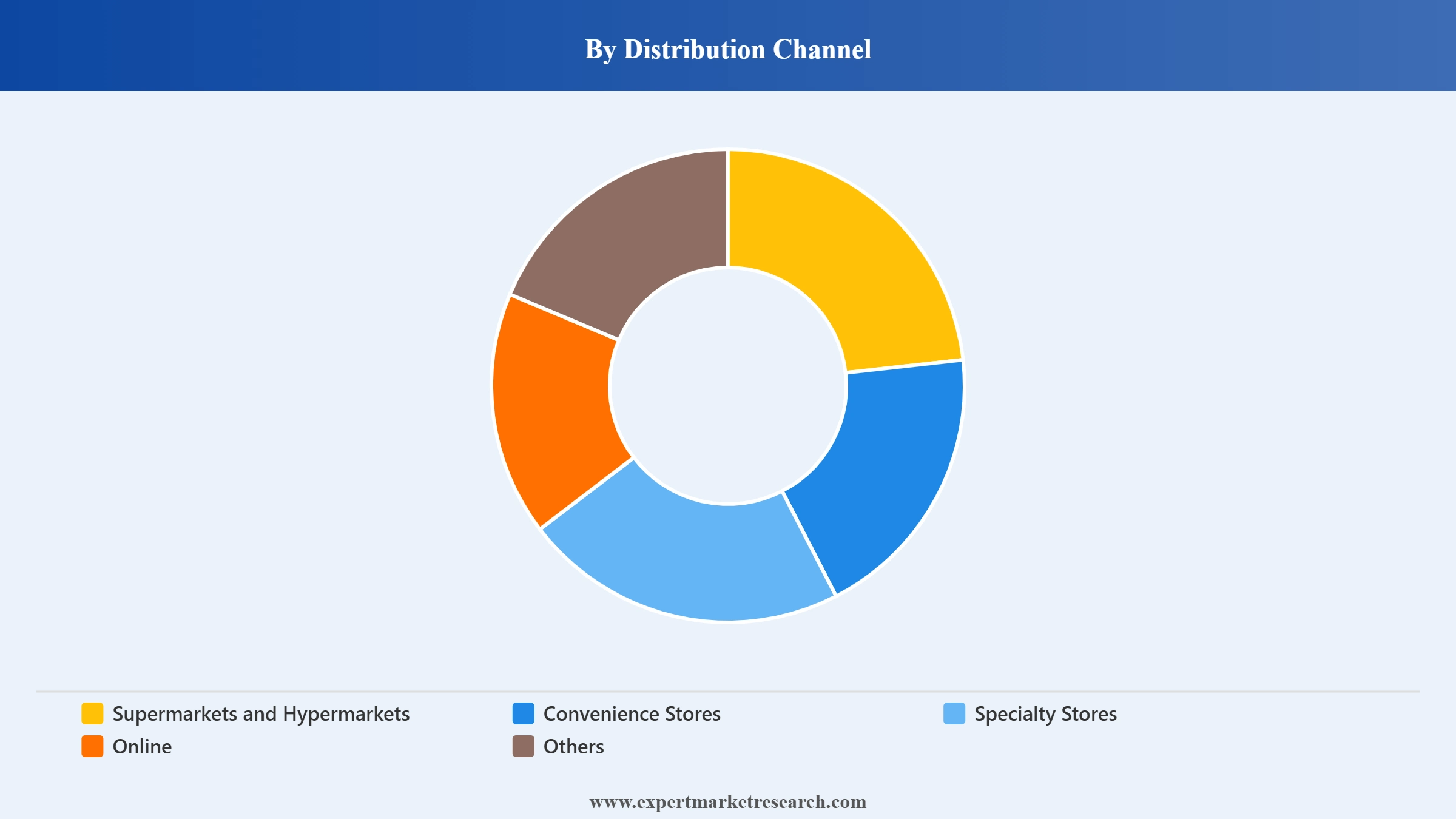

Market Analysis by Distribution Channel

Supermarkets and hypermarkets both as part of the China retail market is growing as consumers increasingly prefer "one stop" shopping experiences. Convenience stores offer viable retail formats, as young consumers opt for fast and better access to various products with extended operating hours in easily accessible locations. Further, the rise in consumer demand for niche product lines has developed growth in specialty stores as they serve specific interests through selective offerings. Online retailing is continuing to take bigger shape with a rapid rise in mobile payments, internet penetration, and an increasing adoption of e-commerce.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Southwestern China Retail Market Insights

The Southwestern China retail market exhibits huge potential for growth due to urbanization and an increase in disposable income. Cities like Chengdu and Chongqing are fast-growing economic centers. These provinces have created a high demand for consumer products ranging from e-commerce, food and beverage, fashion, and electronics. The young, tech-savvy populations in this region tend to be more interested in the digital and online shopping dimensions. Retailers can take advantage of this trend by developing both physical and online locations to capture demand influenced by consumer behavior changes in the rapidly evolving environment.

Northwestern China Retail Market Dynamics

The Northwestern China retail market boasts growth due to newly urbanized centers, such as Xi'an and Lanzhou. The stretching middle-class population with rising disposable incomes have powered this regional market to expand. A major part of the growth is because of the rising demand for consumer goods-electronics, apparel, groceries, etc. The e-commerce dimension in this region is, however, emerging with the developing digital structure. To tap into this market, retailers can tailor their offerings to local tastes, strengthen their product lines, and rely on a combination of traditional and online channels to reach emerging consumers.

North China Retail Market Growth

The retail market in North China is booming, particularly in cities such as Beijing, Tianjin, and Shijiazhuang. The region has a huge population base available, with a growing appetite for luxury and everyday goods. E-commerce continues to thrive in the region, backed by a digitally connected population and the most advanced logistics infrastructures. Despite innovations in retail formats, traditional retail counterparts like supermarkets and shopping malls have not ceased to boost demand, however, online platforms offer better prices with added convenience. Retailers are adapting to these dynamics by integrating omnichannel strategies to cater to both offline and online shoppers effectively.

East China Retail Market Growth

Innovations in the East China retail market tend to be present in provinces like Shanghai, Hangzhou, and Nanjing as they lead this country in consumer spending. The region boasts of an increasingly tech-savvy population; hence, market growth has taken up its maximum pace between e-commerce and mobile payments. High-end lifestyle products, along with electronics and fashion have driven the market with improved brand propositions. Consumers have also shown gradual preferences for sustainable and eco-friendly products, thereby accelerating the retail market trends and dynamics.

Northeast China Retail Market Insights

The retail market in Northeast China promises growth through rising urbanization, disposable income, and changing consumer psychology. Steadily developing cities like Harbin and Shenyang generate high demand for most products in the retail range, including day-to-day goods and premium items, boosting huge potential for the retail industry. The booming e-commerce sector has also stimulated market growth with improved internet infrastructures including 5G technologies, while more people enjoy the convenience of shopping through digital platforms. Retail companies in this region are improvising their strategies by combining traditional retail formats with online channels for a more personalized, localized shopping ecosystem.

Southcentral China Retail Market Trends

The up-and-coming retail market in Southcentral China is growing due to increasing disposable incomes and urbanization in cities such as Wuhan, Changsha, and Guangzhou. These provinces serve as major growth drivers. Major trends also include a shift towards e-commerce, as consumers here now prefer to shop online for convenience and variety. Further, the market growth is fueled by an increasing number of health-conscious consumers in the area, particularly demanding organic foods, wellness items, and fitness products. The area is changing from shopping for concrete products to experiential retailing that combines an offline store with an interactive experience.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The China retail market features one of the world's most intensely competitive and technologically sophisticated competitive landscapes, combining domestic e-commerce giants, traditional hypermarket operators, international retailers, and a rapidly expanding ecosystem of social commerce and instant retail platforms. Key competitive strategies revolve around logistics excellence, AI-powered personalisation, supply chain expansion into lower-tier cities, live-stream and social commerce integration, and the development of premium and sustainable product ranges that speak to China's evolving consumer values. The market is characterised by rapid strategic pivots and heavy technology investment as players compete for share across both digital and physical retail channels.

Alibaba Group Holding Ltd. is a Chinese multinational technology and commerce company headquartered in Hangzhou, Zhejiang Province, and the operator of China's largest e-commerce ecosystem, including Taobao, Tmall, Hema, and Alibaba International. Through its platforms, Alibaba reaches hundreds of millions of active consumers across China and is a foundational player in shaping the competitive dynamics of the country's retail market. The company has committed to investing CNY 380 billion in artificial intelligence and cloud infrastructure through 2027, with retail personalisation, supply chain optimisation, and smart logistics identified as primary application areas. In February 2025, Alibaba announced a strategic partnership to embed advanced AI services into consumer technology products, enabling ambient and proactive retail experiences beyond traditional app-based shopping. In May 2025, Alibaba's fresh food retail arm Freshippo recorded its first annual profit and announced plans to open nearly 100 new stores in lower-tier cities, reflecting the brand's expansion strategy beyond the saturated Tier-1 urban market. Alibaba also announced it would divest its Chinese department store unit to sharpen its focus on core e-commerce and technology-driven retail operations, a strategic consolidation consistent with its long-term ambition to be the world's most advanced AI-powered commerce platform.

JD.com Inc. is a Chinese e-commerce company headquartered in Beijing and the operator of one of China's largest direct-sales and third-party marketplace retail platforms, with particular dominance in consumer electronics, home appliances, and fresh food. The company is widely regarded as China's most logistics-advanced e-commerce operator, running one of the country's most extensive self-operated delivery networks spanning over 2,700 counties. In August 2024, JD.com confirmed a major investment to expand its rural supply chain infrastructure, using AI-powered demand forecasting and advanced logistics to serve consumers in lower-tier cities more effectively. JD.com has also been expanding aggressively into food delivery and instant retail through its JD Daojia and 7Fresh platforms, entering into competition with Meituan and Alibaba's Hema in the fast-growing on-demand delivery market. The company has been deploying autonomous delivery pods to cut last-mile costs and invested in embodied-AI robotics to automate warehouse and customer service operations. These investments position JD.com as both a retail operator and a technology platform business, with its logistics and AI capabilities serving as structural competitive advantages that are increasingly difficult for smaller competitors to replicate at scale.

Walmart Inc. is an American multinational retail corporation headquartered in Bentonville, Arkansas, and among the most strategically significant international retailers operating in China through its Sam's Club and Walmart-branded store formats. Sam's Club has been a standout performer in China's retail market, surpassing CNY 80 billion, approximately USD 11 billion, in annual sales in 2024 and announcing plans for six additional new store openings, including its largest location in northern China, which broke ground in May 2025. Walmart's success with Sam's Club in China reflects the growing appetite among Chinese middle-class consumers for the warehouse club model, which offers curated premium and imported products at competitive membership-based pricing. The company has invested heavily in integrating digital and physical retail in China, including a partnership with Meituan announced in December 2024 to expand its reach through digital commerce channels. Walmart China has also been a pioneer in retail technology deployment, integrating AI-driven inventory management, smart checkout systems, and data analytics capabilities across its store network to enhance operational efficiency and customer experience. The company's deep commitment to the China market through sustained investment in both physical and digital retail infrastructure makes it one of the most formidable international players in China's competitive retail landscape.

Yonghui Superstores Co., Ltd. is a Chinese retail company headquartered in Fuzhou, Fujian Province, and one of China's largest supermarket chains, operating hundreds of stores across the country with particular strength in fresh food and grocery retail. The company has been undergoing a significant strategic transformation in recent years, seeking to leverage design and operational expertise from strategic partners to modernise its store formats, improve product curation, and enhance the in-store consumer experience. In August 2025, Meituan invested CNY 3.5 billion, approximately USD 487 million, for a 20% stake in Yonghui Superstores, an investment that is expected to enable same-day grocery delivery from Yonghui stores to extend to more than 200 additional cities by the end of 2026. This strategic investment reflects the accelerating convergence of China's offline supermarket sector and the instant retail and on-demand delivery platforms that are reshaping consumer expectations around grocery shopping. Yonghui's partnership with Meituan positions it to compete more effectively in the rapidly evolving online-to-offline grocery landscape, combining its well-established fresh food supply chains and store network with Meituan's massive delivery infrastructure and consumer reach. The company continues to invest in store renovation and product range modernisation as it navigates the highly competitive grocery retail environment against both e-commerce giants and international hypermarket operators.

Other Key Players China Resources Ng Fung Co. Limited, GOME Retail Holdings Ltd., Sun Art Retail Group Ltd., Suning Holdings Group Co. Ltd., Wumart Group, Vipshop Holdings Ltd.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Startups in the China retail market are mainly focusing on AI, big data, and automation to enhance customer experience and internal operational efficiency. They are trying to develop personalized shopping experiences, pave logistics systems, and sustainability. Moreover, many startups are using mobile apps and relying on social commerce to provide service to the younger generation of technology-savvy consumers.

Xiaohongshu (Little Red Book)

Founded in 2013, Xiaohongshu (Little Red Book) is a popular Chinese social media and e-commerce platform that mixes lifestyle content, user reviews, and shopping. Users benefit from a unique blend of shopping inspiration and community-driven recommendations.

Klook

Klook, created in 2014, is an innovative retail platform that enables travelers to effortlessly find and book activities and services in a variety of destinations across the world. Klook allows people to discover and schedule unique experiences to enrich their travel vacations.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the China retail market reached an approximate value of USD 2.10 Trillion.

The market is projected to grow at a CAGR of 8.30% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 4.66 Trillion by 2035.

The major drivers of the market are the fast-growing middle-class population, skyrocketing growth of e-commerce and digital platforms, and government policies boosting domestic product consumption.

The key trends of the market include e-commerce and online shopping boom, move towards sustainable and ethical consumption, market transformation with Artificial Intelligence and Big Data, and increasing demand for luxury goods.

The major regions in the market are Southwestern China, Northwestern China, Southcentral China, North China, East China, and Northeast China.

The various products considered in the market report are food, beverage, and grocery, personal and household care, apparel, footwear, and accessories, furniture and home décor, electronic and household appliances, pharmaceuticals, and others.

The various distribution channels considered in the market report are supermarkets and hypermarkets, Convenience Stores, specialty stores, online, and others.

The major players in the market are Alibaba Group Holding Ltd., China Resources Ng Fung Co. Limited, GOME Retail Holdings Ltd., JD.com Inc., Sun Art Retail Group Ltd., Suning Holdings Group Co., Ltd., Walmart Inc., Yonghui Superstores Co., Ltd., Wumart Group, Vipshop Holdings Ltd., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.