Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

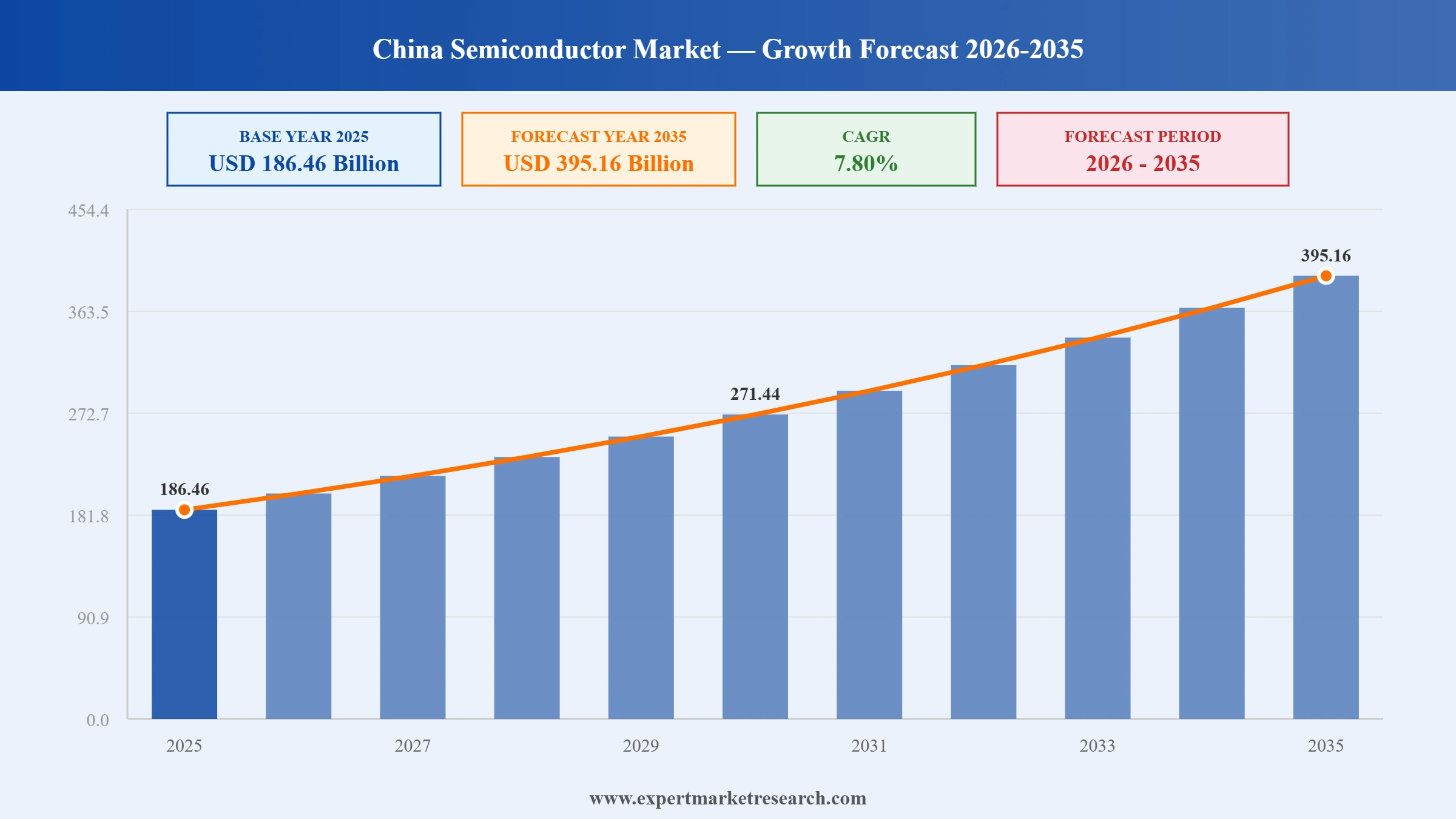

The China Semiconductor Market reached a value of USD 186.46 Billion at 2025 and is projected to expand at a CAGR of around 7.80% during the forecast period of 2026-2035. With rising government investment in domestic chip manufacturing, strong demand growth from AI and automotive applications, accelerating expansion of foundry capacity at mature process nodes, and deepening semiconductor integration across consumer electronics and industrial sectors, the market is expected to reach USD 395.16 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

|

China Semiconductor Market Report Summary |

Description |

Value |

|

Base Year |

USD Billion |

2025 |

|

Historical Period |

USD Billion |

2019-2025 |

|

Forecast Period |

USD Billion |

2026-2035 |

|

Market Size 2025 |

USD Billion |

186.46 |

|

Market Size 2035 |

USD Billion |

395.16 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

7.80% |

|

CAGR 2026-2035 - Market by Region |

South Western China |

8.9% |

|

CAGR 2026-2035 - Market by Region |

East China |

8.0% |

|

CAGR 2026-2035 - Market by Type |

Sensors |

8.6% |

|

CAGR 2026-2035 - Market by Tourism Type |

Automotive |

8.6% |

|

Market Share by Country 2025 |

North East China |

9.5% |

China semiconductor market growth can be attributed to rising government policies and initiatives, adoption of technological advancements, and industrial automation and smart manufacturing.

In April 2025, Naura Technology Group, one of China's leading domestic semiconductor equipment manufacturers, projected a 51% year-on-year revenue increase for Q1 2025, reaching approximately CNY 8.98 billion (around USD 1.26 billion). This sharp growth reflected a surge in domestic orders for etching, deposition, and oxidation equipment as Chinese foundries continued to expand capacity at mature nodes. The results underscored the downstream multiplier effect of China's chip localisation drive on its broader semiconductor equipment and materials supply chain.

In April 2025, Semiconductor Manufacturing International Corporation (SMIC), China's largest domestic foundry, reported Q1 2025 revenue of approximately USD 2.247 billion, reflecting a gross margin of 22.5% and a fab utilisation rate of 89.6%. The company attributed this strong performance to robust domestic demand from consumer electronics and automotive clients. Despite ongoing restrictions on advanced lithography equipment, SMIC demonstrated sustained operational output across its mature-node lines, reinforcing its position as the anchor of China's foundry ecosystem and a primary beneficiary of domestic chip localisation policies.

Throughout 2024, Yangtze Memory Technologies Co. (YMTC), China's flagship NAND flash memory producer, scaled up volume manufacturing of its 232-layer 3D NAND technology. Yield improvements achieved by domestic process engineering teams allowed YMTC to meaningfully increase output for consumer storage and mobile device applications. The development marked a significant step in China's memory semiconductor roadmap, closing the gap with established global players and reinforcing domestic supply of NAND flash to consumer electronics manufacturers who had previously depended heavily on imported components.

In 2024, ChangXin Memory Technologies (CXMT), China's primary DRAM manufacturer, reported achieving approximately 80% yield rates on its DDR5 memory production lines. This operational milestone demonstrated CXMT's growing technical maturity and positioned the company as a credible domestic alternative to established global DRAM producers. The achievement was particularly notable given persistent restrictions on certain memory-related equipment exports, and it provided downstream clients with increased confidence in sourcing high-performance DRAM from locally based suppliers.

In May 2024, Chinese chip manufacturers and aerospace companies jointly established the Commercial Space Industry Technology Alliance, led by the Harbin Institute of Technology. With over 100 member organisations, including chip designer Loongson Technology and rocket developer iSpace, the alliance was formed to accelerate the development and domestic supply of high-grade semiconductors for commercial space applications. The initiative reflected China's strategy to build sovereign capability in aerospace-grade components and reduce reliance on imported chips across this high-priority technology domain.

China's third National Integrated Circuit Industry Investment Fund secured approximately USD 47.5 billion in capital commitments from the central government and state-owned financial institutions, making it the largest semiconductor-focused fund in the country's history. Directed at foundry expansion, advanced packaging, and semiconductor materials development, this capital injection directly supports China Semiconductor Market growth by reducing technology gaps and enabling domestic chip companies to scale without depending on foreign capital markets. In May 2024, the fund was formally constituted with contributions from the Industrial and Commercial Bank of China, China Development Bank, and multiple central enterprises, signalling long-term government commitment to achieving semiconductor self-sufficiency across strategic categories.

China's rapid build-out of AI cloud infrastructure is creating sustained, large-scale demand for high-performance semiconductors across memory, processing, and connectivity categories. The shift toward large language models, generative AI, and AI-powered enterprise applications is driving purchases of AI accelerators and high-bandwidth memory at a pace that clearly outstrips conventional computing demand cycles. Domestic cloud operators are committing unprecedented capital to data centre expansion. In early 2025, Alibaba Group pledged CNY 380 billion over three years to AI-ready cloud infrastructure, with Tencent and Baidu making comparable commitments, collectively creating a durable and growing demand base for semiconductor components sourced increasingly from domestic designers.

Much of China's semiconductor growth is anchored in mature-node fabrication from 14nm to 65nm, which serves broad demand from automotive, industrial, and consumer electronics segments. China's leading foundries have expanded aggressively at these process nodes, backed by policy support and consistent domestic demand. By 2027, China is projected to hold 31% of global 28nm capacity, reshaping pricing dynamics at mature nodes globally. Through mid-2024, SMIC, Huahong Group, and Nexchip were collectively ramping mature-node lines as part of a coordinated national strategy to establish import-independent semiconductor supply across core electronics manufacturing categories that represent the bulk of China's actual chip consumption.

China's electric vehicle sector, having crossed 50% penetration of new passenger car sales, is generating a structural shift in automotive semiconductor requirements. EV platforms require substantially more chip content per vehicle than conventional cars, spanning power management ICs, motor controllers, battery management systems, and ADAS processing units. Domestic OEMs are deepening semiconductor integration through in-house chip design programs to secure supply and differentiate on technology. In late 2024, Xpeng Motors unveiled a proprietary AI chip delivering 2,200 TOPS for autonomous driving systems, illustrating the depth of chip-OEM collaboration now shaping China's automotive supply chain and the broader market's growth trajectory.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Expert Market Research's report titled “China Semiconductor Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

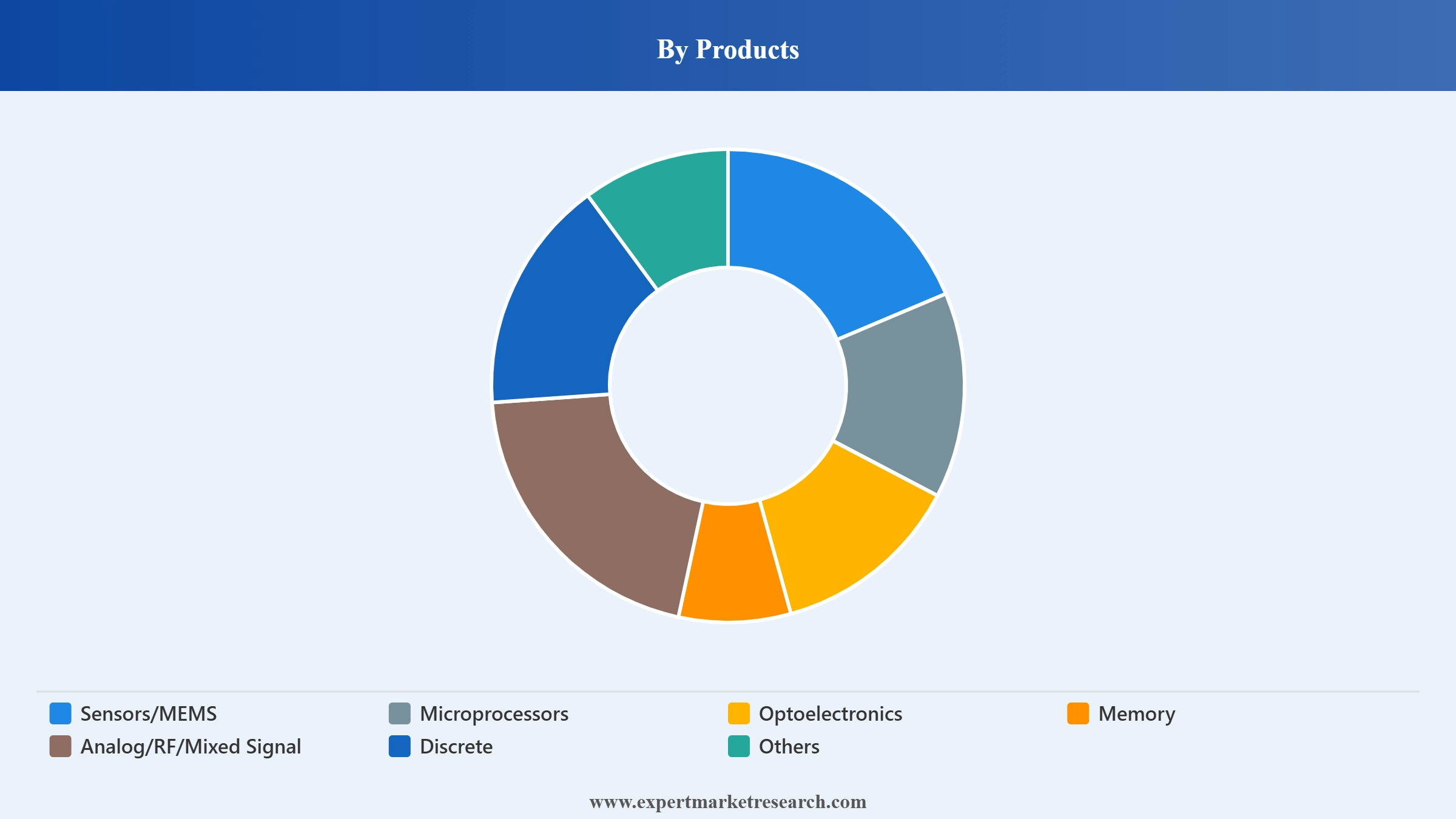

Breakup by Products

Key Insight: Memory chips have emerged as one of the most strategically important product segments within China's semiconductor market, driven by soaring demand from AI data centres, smartphones, and consumer electronics. Domestic producers YMTC and CXMT are scaling up 3D NAND and DDR5 DRAM output, backed by state-directed investment and localisation mandates. Microprocessors and analog chips account for substantial revenue across industrial automation, telecommunications, and automotive applications. The Sensors/MEMS segment is gaining ground in IoT and smart manufacturing use cases, while discrete power devices are benefiting from the rapid adoption of silicon carbide in EV drivetrains, creating a broad and balanced product demand landscape across the forecast horizon.

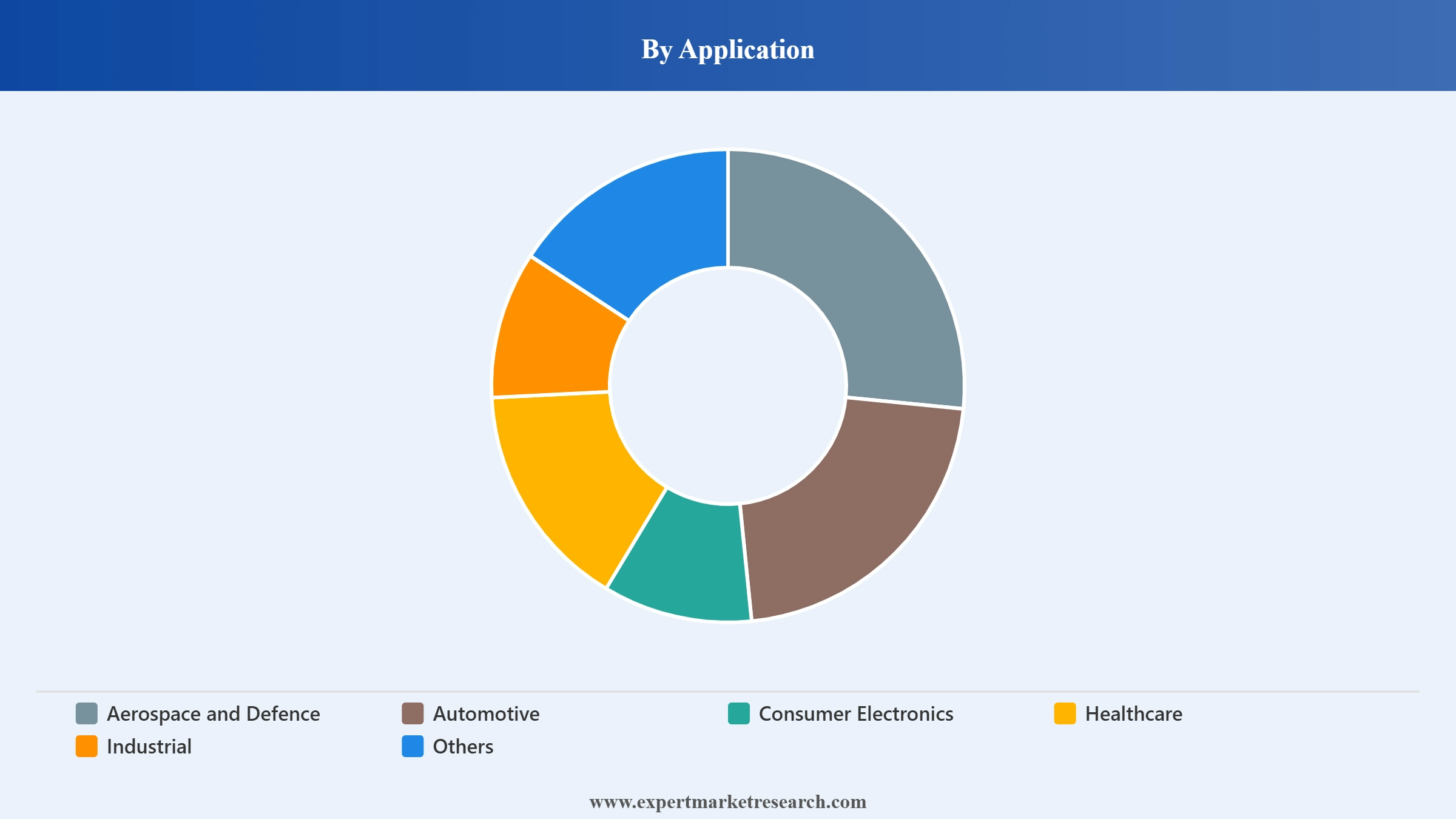

Breakup by Application

Key Insight: Consumer electronics is the single largest end-market for semiconductors in China, with the country's manufacturing base supplying a significant share of global smartphone, personal computing, and smart home device output. Automotive is one of the fastest-growing application segments, fuelled by EV penetration exceeding 50% of new vehicle sales and the associated demand for power management ICs, sensors, and ADAS chips. Aerospace and defence applications are expanding as China's defence budget grows and domestic firms develop high-reliability components for navigation, communication, and surveillance systems. The industrial segment benefits from ongoing factory automation investments across eastern and central provinces, sustaining broad and diversified semiconductor demand.

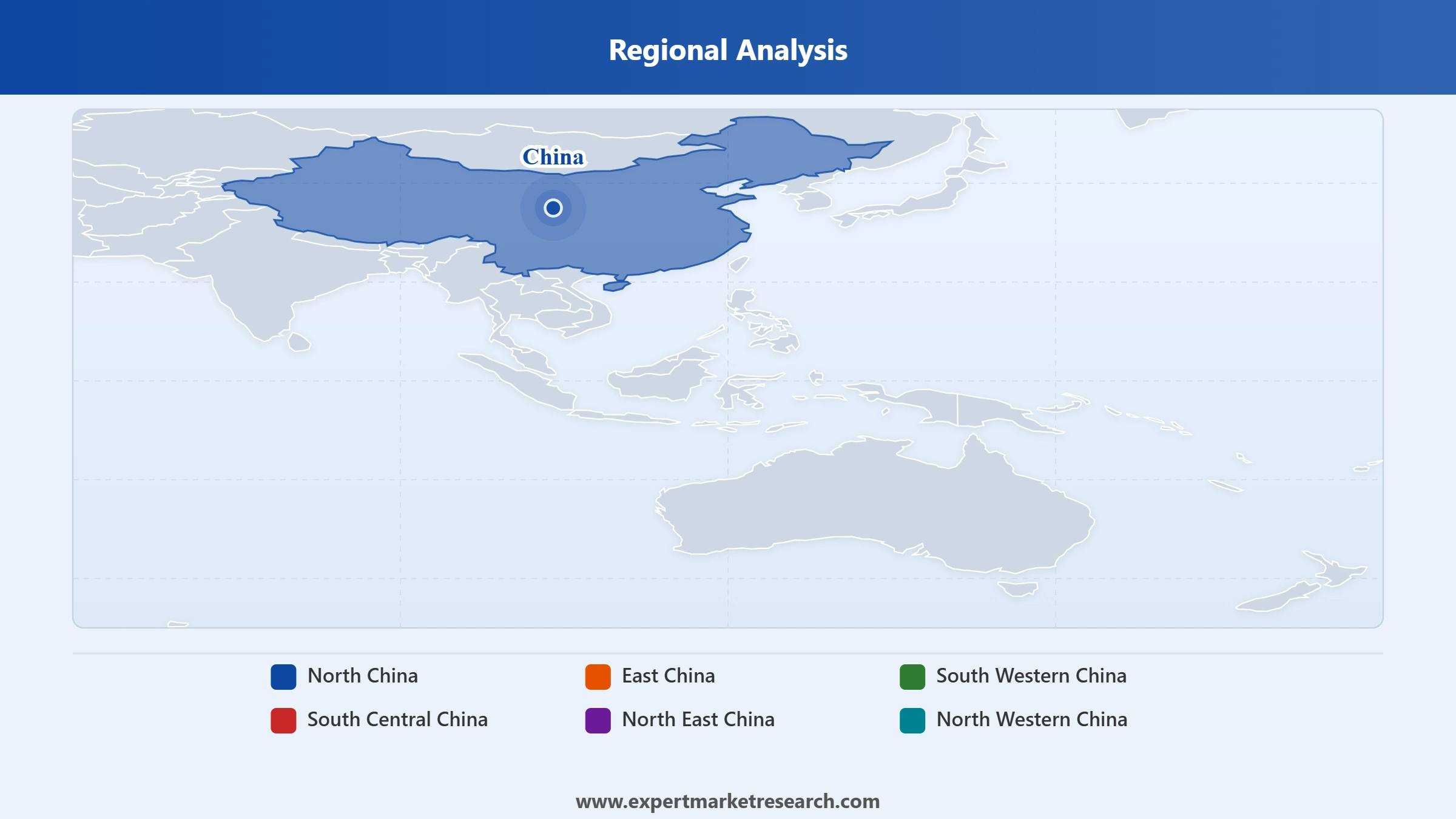

Breakup by Region

Key Insight: East China, anchored by the Yangtze River Delta spanning Shanghai, Jiangsu, and Zhejiang, is the heart of China's semiconductor ecosystem, accounting for a leading share of integrated circuit design, advanced packaging, and assembly operations. Shanghai alone reported IC industry sales exceeding USD 41 billion in recent years. North China, centred on Beijing's Zhongguancun technology hub, is home to state-backed chip design institutes and leading fabless firms. South Central China, particularly Guangdong's Greater Bay Area, attracts foundry and packaging investment on the strength of its proximity to downstream electronics OEMs and established logistics networks.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within China's semiconductor market, Memory commands a prominently growing position, driven by massive domestic consumption of NAND flash and DRAM across smartphones, enterprise storage systems, personal computers, and AI accelerator modules. YMTC has rapidly closed the technical gap with global NAND leaders through its 232-layer technology, while CXMT has achieved meaningful DDR5 yield milestones. Government procurement mandates and technology substitution policies further reinforce memory's share. Microprocessors represent the second-largest revenue category, with firms including Loongson Technology and Phytium serving government computing and defence applications alongside a growing base of industrial and embedded use cases.

Consumer Electronics secures the largest application-based share within the China Semiconductor Market, driven by the country's role as the world's dominant electronics manufacturer and a major end consumer of smartphones, laptops, tablets, and connected home devices. Automotive represents the fastest-growing application segment, as EV fleet electrification creates unprecedented demand for semiconductor content per vehicle. Major EV manufacturers are deepening chip integration strategies, with several establishing in-house IC design teams.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

East China leads in regional market share, with the Yangtze River Delta accounting for the country's densest concentration of fab capacity, design talent, and assembly infrastructure. South Central China, particularly Guangdong, has attracted foundry and advanced packaging investments at scale due to proximity to downstream OEMs and well-developed logistics networks.

East China is the most consequential semiconductor region in the country, anchoring national production through a dense cluster of fabs, design houses, and packaging and testing firms in the Yangtze River Delta. Shanghai's integrated circuit industry has generated over USD 41 billion in annual sales in recent years, and the Lingang New Area has been designated a semiconductor-focused special economic zone with targeted production output goals. Jiangsu province excels in semiconductor assembly and back-end testing, while Zhejiang is positioning itself as a destination for silicon carbide and gallium nitride device investment. Together, these provinces attract the majority of both domestic and international semiconductor capital, sustaining high foundry utilisation rates and a thriving pipeline of fabless chip design firms serving consumer electronics, telecommunications, and industrial clients.

South Central China, centred on the Greater Bay Area in Guangdong province, occupies the second-most significant position in China's semiconductor geography. Its strategic advantage rests on physical and commercial proximity to major consumer electronics manufacturers in Shenzhen and Guangzhou, which creates ready-made demand for power devices, optoelectronics, and communication chips. Provincial authorities have committed CNY 500 billion across 40 semiconductor investment projects, including the region's only 300mm fabrication facility capable of producing 80,000 wafers per month. Access to Hong Kong's capital markets provides additional financial flexibility for chip companies seeking to scale operations.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The China Semiconductor Market is characterised by a combination of established multinational chip companies with significant China sales and design operations, and an increasingly assertive cohort of domestic players receiving state support. Competitive intensity is highest in segments adjacent to AI computing, automotive electronics, and consumer devices, where both global leaders and Chinese challengers are investing heavily. Leading international firms retain advantages in process node leadership and design tool capabilities, while domestic players are narrowing the gap at mature nodes and gaining ground in specific high-volume categories through policy-driven substitution.

Competition is intensifying as export restrictions have accelerated domestic substitution across multiple chip categories, spurring the growth of Chinese fabless designers and equipment suppliers. Global semiconductor leaders continue to maintain operations and design centres in China while managing trade compliance requirements. Key competitive dynamics include capital access, engineering talent, process node currency, and the ability to serve China's vertically integrated EV and consumer electronics supply chains at both speed and scale.

Founded in 1999 and headquartered in Neubiberg, Germany, Infineon Technologies AG is a global semiconductor leader in power electronics, microcontrollers, and security chips. The company holds a strong market position in automotive and industrial semiconductors, with a significant commercial presence in China serving EV manufacturers and factory automation clients. Infineon's insulated-gate bipolar transistors and silicon carbide power modules are widely adopted in Chinese EV battery management systems, while its microcontroller platforms address a growing base of industrial IoT applications.

Founded in 1965 and based in Wilmington, Massachusetts, USA, Analog Devices, Inc. (ADI) designs and manufactures precision analogue, mixed-signal, and digital signal processing integrated circuits. The company serves China's market with components for telecommunications infrastructure, industrial automation, healthcare instrumentation, and automotive systems. Its high-speed data converters and operational amplifiers are widely used by Chinese OEMs in radar systems, 5G base station hardware, and battery testing equipment.

Founded in 1989 and headquartered in Chandler, Arizona, USA, Microchip Technology Inc. is a leading supplier of microcontrollers, digital signal controllers, and analogue semiconductors. The company holds a particularly strong position in embedded control applications across automotive, industrial, and consumer electronics markets. In China, Microchip serves a broad base of system manufacturers deploying its PIC and AVR microcontroller families in smart home devices, motor control systems, and building automation products.

Founded in 2006 and headquartered in Eindhoven, Netherlands, NXP Semiconductors NV is a global leader in automotive, industrial, and secure connectivity semiconductors. NXP has a material business presence in China, particularly in automotive chips used in advanced driver assistance systems and vehicle networking. Its S32 automotive processing platforms are integrated into products developed by Chinese EV manufacturers and tier-one suppliers. NXP also serves China's mobile payments and secure identification ecosystem through its NFC and secure element products.

Other key players in the market are Texas Instruments Inc., ON Semiconductor Corp., Skyworks Solutions Inc., Renesas Electronics Corp., Qorvo Inc., MediaTek Inc., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

There is no shortage of semiconductor reports, but few go as deep into China's evolving chip ecosystem as this one. From product-level demand trends and regional investment flows to a rigorous competitive profile of the players setting the pace, our 2026-2035 outlook gives you the intelligence you need to move with confidence. Whether you are evaluating supply chain exposure, exploring partnership opportunities, or monitoring the pace of domestic chip localisation, this report delivers clarity where it counts. Download your free sample today and take your first step into the China semiconductor opportunity.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market attained a value of nearly USD 186.46 Billion.

The market is assessed to grow at a CAGR of 7.80% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach about USD 395.16 Billion by 2035.

The major drivers of the market are rising government policies and initiatives and the adoption of technological advancements.

The key trends aiding the market expansion include the increasing demand for electronics, industrial automation and smart manufacturing and rapid industrial automation.

As per the EMR report, the different applications of semiconductors in the market are aerospace and defence, automotive, consumer electronics, healthcare, and industrial, among others.

The major regions considered in the market are Shanghai, Zhejiang, Guangdong, Jiangsu, and Beijing, among others.

The major players in the market are Infineon Technologies AG, Analog Devices, Inc., Microchip Technology Inc., NXP Semiconductors NV, Texas Instruments Inc., ON Semiconductor Corp., Skyworks Solutions Inc., Renesas Electronics Corp., Qorvo Inc., and MediaTek Inc. among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Products |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.