Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The China Tire Market reached a value of USD 46.61 Billion at 2025 and is projected to expand at a CAGR of around 7.90% during the forecast period of 2026-2035. With rapid expansion in the electric vehicle fleet driving demand for specialised tires, the dominant shift toward radial construction across passenger and commercial segments, accelerating growth of the aftermarket sales channel on China's enormous installed vehicle parc, and sustained infrastructure investment sustaining commercial and off-road tire volumes, the market is expected to reach USD 99.70 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

|

China Tire Market Report Summary |

Description |

Value |

|

Base Year |

USD Billion |

2025 |

|

Historical Period |

USD Billion |

2019-2025 |

|

Forecast Period |

USD Billion |

2026-2035 |

|

Market Size 2025 |

USD Billion |

46.61 |

|

Market Size 2035 |

USD Billion |

99.70 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

7.90% |

|

CAGR 2026-2035- Market by Region |

Zhejiang |

9.5% |

|

CAGR 2026-2035- Market by Season Type |

All Season Tire |

8.7% |

|

CAGR 2026-2035- Market by Vehicle Type |

Passenger Vehicle |

8.9% |

China's tire industry is being reshaped by four powerful structural forces acting concurrently: an electric vehicle revolution creating new specifications and materials requirements, the commanding dominance of radial technology supported by regulatory mandates, deepening smart tire technology integration, and an aggressive global expansion by domestic manufacturers diversifying beyond traditional export markets.

Following the July 2025 acquisition of the former Bridgestone Shenyang facility, Sailun Group announced a RMB 1.70 billion (approximately USD 237 million) investment programme to upgrade and expand the facility in September 2025. The two-phase project, commenced with a groundbreaking ceremony on 9 September 2025, targets an annual production capacity of 3.3 million all-steel radial truck and bus tires and 20,000 tonnes of off-highway tires. The decision was supported by a confirmed 6.4% increase in domestic demand for medium and heavy-duty commercial tires in China during 2024 and Sailun's assessment of strong demand growth in emerging international markets. The investment underscores the consolidation dynamics reshaping China's commercial tire manufacturing sector.

Sailun Group's wholly owned subsidiary, Sailun (Shenyang) Tire Co., Ltd., completed the acquisition of Bridgestone (Shenyang) Tire Co., Ltd. in July 2025 for RMB 265 million (approximately USD 37 million). The acquired facility, originally founded by Bridgestone in 1996, was one of the earliest foreign-invested tire plants in China and had an annual production capacity of 1.7 million truck and bus radial (TBR) tires. Bridgestone's exit from commercial vehicle tire production in China created a strategic opening for domestic manufacturers, and Sailun's acquisition materially strengthens its TBR portfolio and installed production footprint in northern China, enhancing its ability to supply both domestic fleet customers and international markets including the United States.

Zhongce Rubber Group Co., Ltd., one of China's largest domestic tire manufacturers, officially completed its listing on the main board of the Shanghai Stock Exchange in June 2025. The successful IPO is expected to significantly enhance the company's access to equity capital for funding its ongoing capacity expansion programs at multiple domestic facilities, including plants in Tianjin, Jintan, Dajiangdong, and Fuyang. Zhongce had also launched its first overseas production facility in Indonesia through its MTI subsidiary in December 2024, and the public listing is anticipated to further accelerate its international growth strategy. The event marks a significant milestone for China's domestic tire industry, providing Zhongce with enhanced financial firepower to compete with both domestic rivals and multinational tire groups.

Goodyear Corporation showcased its advanced tire technologies and officially launched the SightLine sub-brand, dedicated to intelligent tire solutions, at the Auto Shanghai 2025 exhibition in April 2025. The SightLine platform integrates embedded sensors capable of real-time monitoring of tire pressure, temperature, and tread wear conditions, enabling fleet operators and passenger vehicle users to access predictive maintenance insights through connected vehicle platforms. The launch reflects the accelerating integration of IoT sensor technology into tire products in China, where the combination of a large commercial fleet market and government emphasis on road safety standards is creating strong demand for technology-enabled tire monitoring solutions. Goodyear's commitment to smart tire technology aligns with the direction taken by Chinese domestic manufacturers who are similarly investing in IoT-enabled product development.

Gubersail Tire rolled off its first green, low-carbon tire at a fully automated facility in Jiangsu Province in February 2025. The facility was purpose-built with state-of-the-art mixing and curing lines designed to reduce the carbon intensity of the production process, and the resulting tire products are formulated to meet the highest environmental performance criteria applicable under China's evolving tire labelling regulations. The development reflects the growing importance of sustainability as a competitive differentiator in China's tire industry, where government pressure to reduce CO2 emissions and the establishment of the China Rubber Industry Association tire labelling system are pushing manufacturers toward low rolling resistance compounds and greener manufacturing operations. Jiangsu Province's subsidy environment for clean manufacturing investments supported the facility's development.

The rapid growth of China's electric vehicle fleet is fundamentally changing the technical requirements placed on tire manufacturers, as EV-specific demands for low rolling resistance, noise reduction, high torque capacity, and reinforced load ratings diverge meaningfully from the specifications suited to conventional internal combustion vehicles. Passenger car EV adoption is particularly relevant given that fitments for passenger vehicles led with a 62.55% share of the China tire market in 2024, and EV-specific production lines are expanding at a 10.63% CAGR according to a leading market research firm data. In April 2025, Continental confirmed it would be providing EV tires to 18 of the leading 20 global EV manufacturers, illustrating the intensity of the competitive race to lock in supply relationships with China tire market growth in the EV segment, where design standards are evolving faster than any previous vehicle technology transition.

Radial tire technology now commands 91.26% of the China tire market by volume and continues to expand its dominance across both passenger and commercial segments, driven by government fuel economy regulations that mandate lower rolling resistance, fleet procurement policies favouring extended tread life, and consumer recognition of radial tires' superior ride comfort and handling characteristics. Chinese government regulations through the Ministry of Industry and Information Technology have pushed tire safety standards progressively higher, with research indicating that a significant share of tire-related road accidents are attributable to tire failures, creating additional regulatory momentum favouring premium radial constructions. Giti Tire secured its first OEM winter tire fitment on the BMW 1 Series, reinforcing the readiness of domestic manufacturers to compete in high-specification radial supply for premium vehicle OEMs, further supporting the China tire market outlook for radial category expansion.

The integration of IoT sensors, real-time monitoring platforms, and data analytics capabilities into tire products is accelerating rapidly in China, driven by fleet management companies seeking to reduce maintenance costs, government road safety mandates pushing vehicle operators toward active tire monitoring, and the convergence of connected vehicle platforms that can utilise tire sensor data for autonomous and semi-autonomous driving applications. Goodyear's April 2025 launch of the SightLine brand at Auto Shanghai 2025 formalised the move toward intelligent tires as a discrete product category, while domestic manufacturers including Linglong Tire have established partnerships with technology companies to bring IoT capability to their product ranges. This shift in China tire market trends reflects a broader industry transformation from commodity rubber products toward technology-embedded performance solutions commanding premium pricing, particularly in the commercial fleet and premium passenger car segments.

China's leading tire manufacturers are executing a coordinated global factory expansion strategy, establishing production facilities in Southeast Asia, Europe, the Americas, and Africa to circumvent anti-dumping measures, qualify for preferential trade agreements, and reduce logistics costs for key export markets. Zhongce Rubber's Indonesia MTI facility commenced production in December 2024, Sailun has active manufacturing operations in Cambodia and Mexico, and Linglong Tire operates a plant in Serbia. This internationalisation wave reflects both the commercial maturity of domestic manufacturers and the headwinds from international trade barriers targeting Chinese tire exports. The China tire market forecast benefits from this capacity diversification, as global manufacturing platforms allow domestic producers to serve international OEM customers without the tariff exposure that has constrained pure export strategies from mainland Chinese facilities through 2025.

The Expert Market Research's report titled "China Tire Market Report and Forecast 2026 to 2035" offers a detailed analysis of the market based on the following segments:

Market Breakup by Design

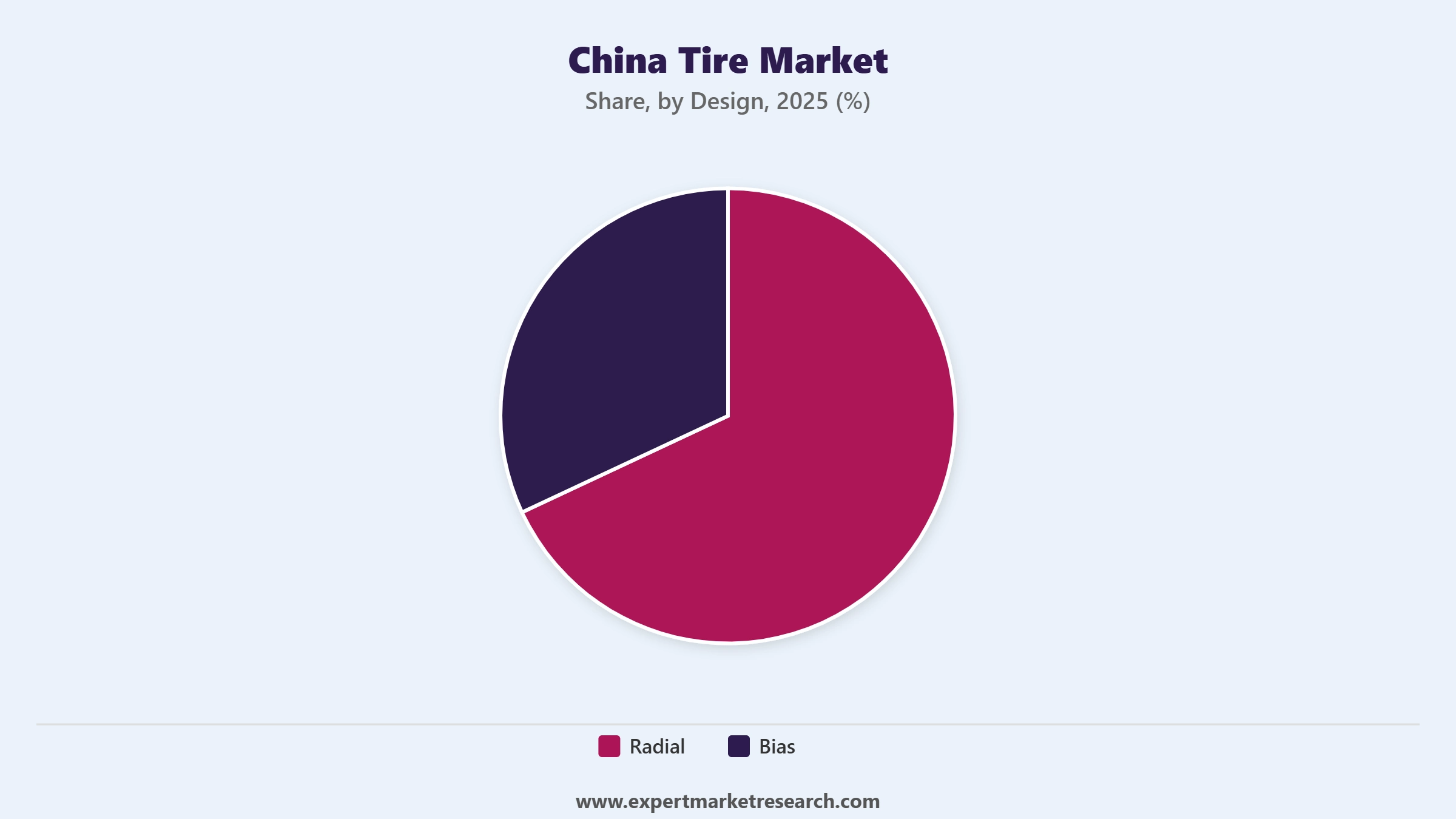

Key Insight: Radial tires hold a commanding position in the China Tire Market, accounting for 91.26% of market volume in 2024, a dominance underpinned by their superior fuel efficiency, durability, heat dissipation, and ride comfort relative to bias alternatives. Government fuel economy and emissions regulations enforced through the China Rubber Industry Association labelling system and Ministry of Industry and Information Technology standards have systematically shifted fleet procurement and consumer preference toward radial constructions. Passenger cars, commercial trucks, and buses are now almost entirely radial-equipped in the OEM channel, with the 6.96% CAGR projected for radial tires through 2030 reflecting continued market share gains as the remaining bias-fitted legacy vehicle parc is gradually replaced. Bias tires retain relevance in niche agricultural, mining, and heavy industrial applications where their thicker sidewalls and cost competitiveness serve specific operational requirements, but their contribution to overall market value is structurally declining.

Market Breakup by Type

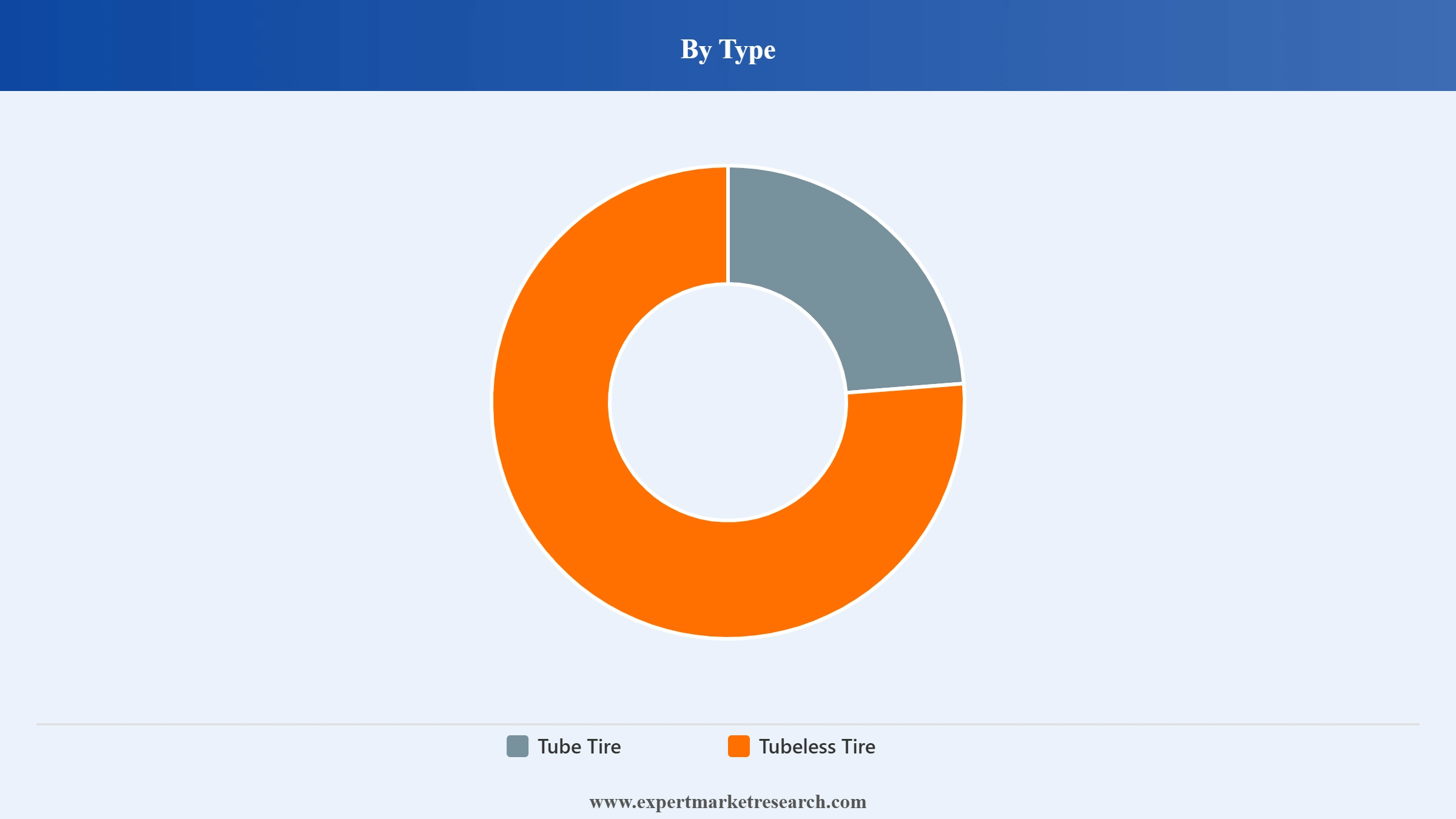

Key Insight: Tubeless tires represent the dominant product type in the China Tire Market, driven by mandatory fitment requirements across all new passenger car OEM channels and rapid penetration across commercial vehicle fleets pursuing reduced maintenance downtime. Tubeless designs eliminate the risk of sudden inner tube failures that cause blowouts, providing measurably better safety outcomes that align with China's regulatory focus on reducing tire-related road incidents. The technology is universally preferred by automotive OEMs for new vehicle platforms and is the standard fitment across the premium passenger and commercial vehicle segments that represent the highest value portions of the market. Tube tires retain a presence in the two-wheeler and three-wheeler segment and in certain agricultural applications, but the sustained shift of the Chinese vehicle fleet toward modern passenger cars and commercial vehicles ensures the long-term structural growth advantage lies firmly with tubeless formats.

Market Breakup by Season Type

Key Insight: All Season tires constitute the largest portion of China's tire market by volume, reflecting the country's diverse climate geography and the preference of urban consumers for year-round fitments that eliminate the logistical requirement of seasonal changeovers. China's northern provinces, including Beijing, Heilongjiang, and Inner Mongolia, represent the primary demand geography for Winter tires, where severe cold and snowfall conditions create genuine safety requirements for cold-weather compound and tread designs. Giti Tire's successful fitment of an OEM winter tire on the BMW 1 Series in 2025 signals that domestic manufacturers are achieving the technical quality thresholds required by European premium OEMs in this segment. Summer tires serve performance-focused consumers and sports vehicle categories. The All Season segment's growth across China's expanding urban middle class reflects the convenience-led preference driving tire purchasing decisions across the growing passenger vehicle parc.

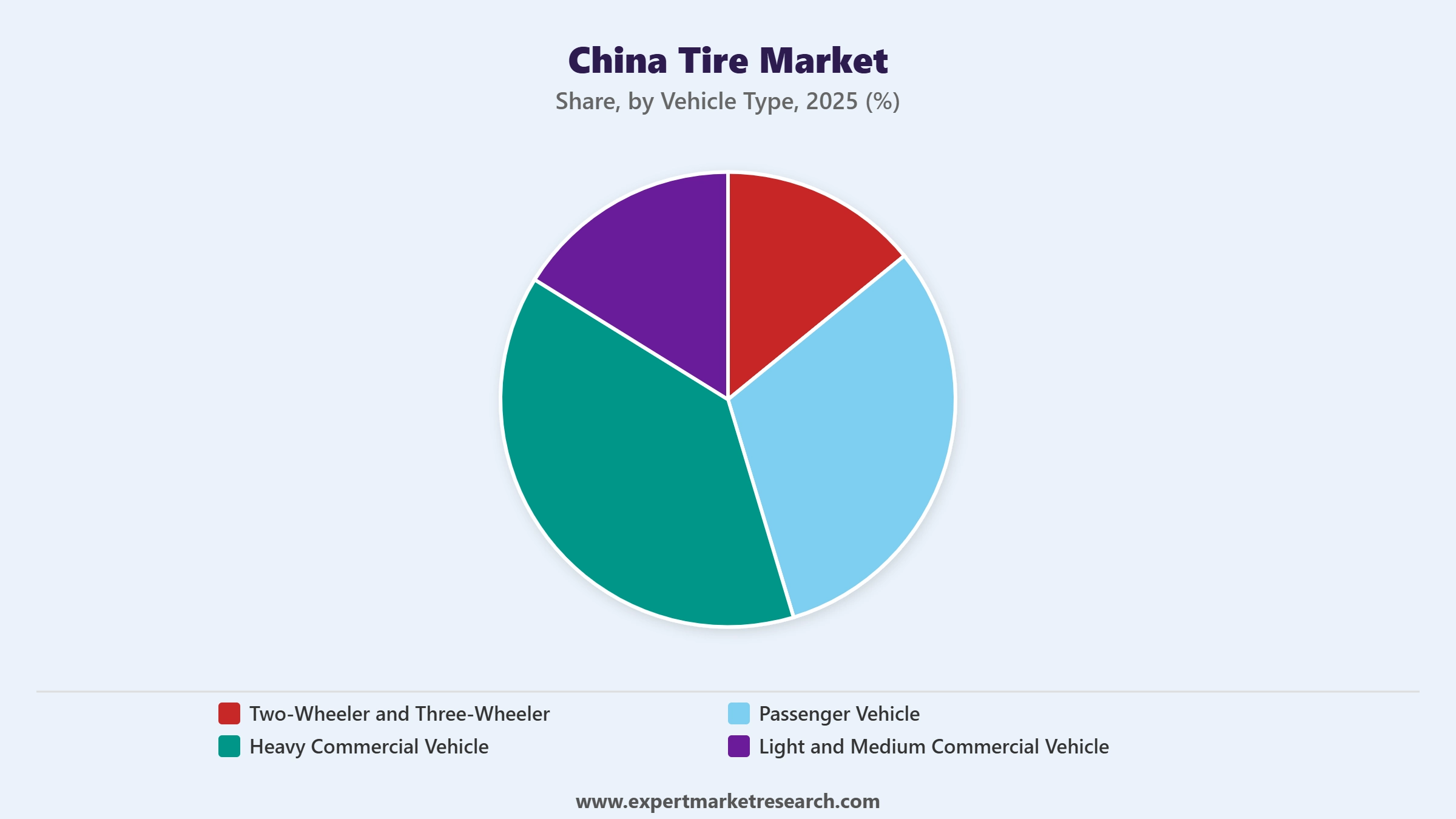

Market Breakup by Vehicle Type

Key Insight: Passenger vehicles represent the largest vehicle type segment in the China Tire Market, holding 62.55% of market share in 2024, supported by China's enormous private car ownership base and the continuing urbanisation and income growth driving new vehicle purchases. China's auto production reached 30.09 million units in 2023, according to Ministry of Industry and Information Technology data, providing a sustained pipeline of OEM tire demand. Heavy Commercial Vehicles constitute the second-largest segment, fuelled by China's Belt and Road infrastructure projects, domestic logistics network expansion, and e-commerce fulfilment fleet growth. Light and Medium Commercial Vehicles are growing on the back of last-mile delivery fleet expansion driven by the e-commerce sector. Two-Wheeler and Three-Wheeler tires serve China's large electric two-wheeler market, which is undergoing its own technology upgrade cycle toward lithium-ion battery systems requiring reconfigured tire specifications.

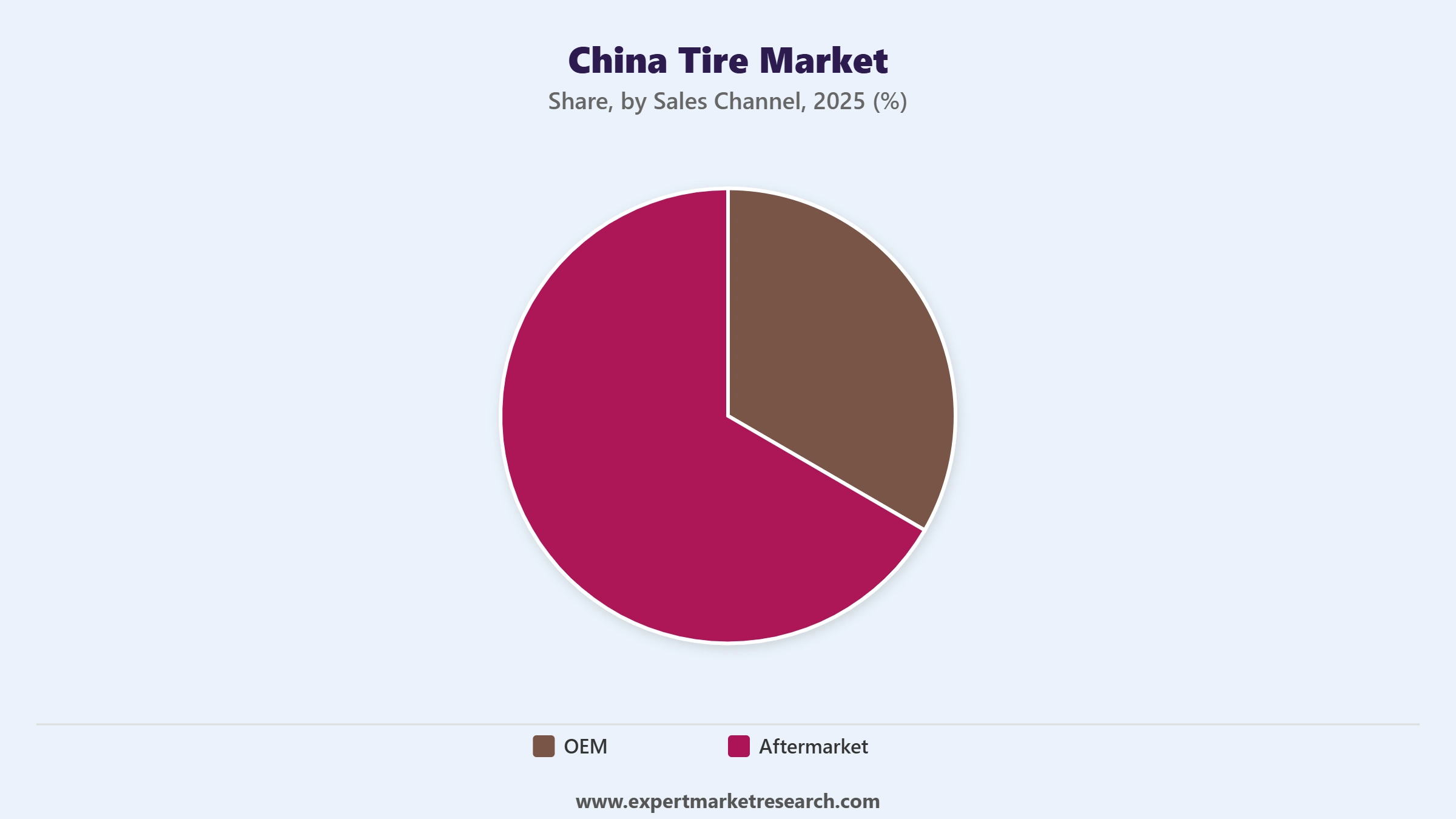

Market Breakup by Sales Channel

Key Insight: The Aftermarket segment holds a substantial share of the China Tire Market at approximately 69.24% of revenue in 2024, according to a leading market research firm data, and is growing at an 8.05% CAGR through 2030, reflecting the replacement cycle dynamics of China's enormous installed vehicle parc. As the vehicle fleet has matured and aged, the frequency of replacement tire purchases has accelerated, creating a high-volume aftermarket that benefits domestic manufacturers with established nationwide distribution networks. The OEM channel, while smaller in volume terms, carries premium pricing characteristics and strategic value for manufacturers as OEM fitment drives brand preference in the replacement purchase cycle. Key domestic players including Zhongce, Sailun, and Giti have all invested in strengthening their OEM relationships with both domestic automakers and international vehicle groups manufacturing in China.

Market Breakup by Region

Key Insight: Guangdong leads the China Tire Market among the regional segments, anchored by its role as the country's foremost automotive and electronics manufacturing hub and a major export gateway. The province's enormous EV production ecosystem, centred on Shenzhen, Guangzhou, and Dongguan, is generating concentrated demand for specialised EV tires. Shanghai is the country's premier premium automotive market, hosting major international OEM operations from Volkswagen, General Motors, and Tesla, all of which generate high-specification tire demand across both passenger and commercial segments. Jiangsu has established itself as a significant tire manufacturing province with strong commercial vehicle fleet demand from its logistics sector, and Nanjing's growing EV adoption is creating an emerging demand base for EV-specific tire formats. Zhejiang contributes through its concentration of commercial and industrial vehicle manufacturers, while Beijing drives premium passenger car and SUV tire demand as the country's capital and a high-income consumer centre.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Radial design holds an overwhelming leadership position within the Design segmentation, accounting for 91.26% of China's tire market by volume in 2024. Government fuel economy regulations, safety-driven fleet procurement policies, and the universal adoption of radial construction by automotive OEMs have created a near-total transition away from bias alternatives in passenger and commercial vehicle segments. Bias tires retain a niche position in agricultural and heavy industrial applications where sidewall ruggedness and upfront cost-effectiveness take precedence over rolling resistance and ride quality.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within the Type segmentation, Tubeless tires are the clear market leader, reflecting their mandatory fitment across all modern passenger vehicle platforms and their proven safety advantages eliminating sudden inner tube blowout risk.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Aftermarket sales channel commands approximately 69.24% of China Tire Market revenue, substantially larger than the OEM channel, driven by the replacement cycle needs of China's mature and growing vehicle parc.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within the Vehicle Type segmentation, Passenger Vehicles represent 62.55% of market share, anchored by China's enormous private car ownership base and continued urbanisation. The Passenger Vehicle segment's overlap with the rapidly expanding EV fleet is generating increasing demand for specialised low rolling resistance and noise-optimised tire formats that command premium unit prices relative to conventional fitments. Guangdong is the leading regional market, supported by its concentrated EV manufacturing ecosystem and major export port infrastructure that serves both domestic distribution and international tire trade flows.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Guangdong Province is the most commercially dynamic regional market in China's tire industry, driven by the convergence of three powerful demand forces: the country's largest concentration of electric vehicle manufacturers, a robust automotive and electronics industrial base spanning Shenzhen, Guangzhou, and Dongguan, and major port infrastructure at Guangzhou and Shenzhen that makes the province a critical gateway for both domestic distribution and export of tire products. Guangdong's government has introduced subsidy programmes of up to RMB 1 million per foreign investor to attract international brands into manufacturing joint ventures, directly importing advanced automation standards and production technology into domestic facilities. The provincial EV sector's growth is generating concentrated demand for specialised tires with low rolling resistance compounds and reinforced load ratings calibrated for electric powertrains, creating a premium tire demand pool that rewards manufacturers with EV-specific product development capabilities. As China's EV production continues to scale, Guangdong's position as the epicentre of that growth ensures its leading regional market status through the forecast period.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Jiangsu Province is one of China's most industrially significant tire demand markets, supported by its dual role as both a major tire manufacturing hub and a province with strong commercial vehicle and passenger car markets. Jiangsu hosts tire manufacturing facilities for multiple domestic producers, and the province's Nanjing city is a significant EV adoption centre generating growing demand for electric vehicle-specific tire specifications. The province's logistics sector, one of China's most active in terms of freight volumes, generates robust demand for heavy and light commercial vehicle tires, while infrastructure investment in transportation networks continues to expand the commercial vehicle fleet operated within the province. Gubersail Tire's launch of its first green, low-carbon tire at a fully automated Jiangsu plant in February 2025 illustrates the province's role in pioneering sustainable tire manufacturing, aligning with China's regulatory direction on emissions and the tire labelling framework that rewards low rolling resistance performance.

The China Tire Market features a highly competitive landscape where domestic manufacturers have achieved global scale and are increasingly challenging international incumbents across all product segments and price tiers. The market is led by Chinese domestic players including Zhongce Rubber, Sailun, Giti Tire, and Triangle Tyre, who have built formidable advantages through production scale, cost efficiency, strong OEM relationships with domestic automakers, and progressively improving technology capabilities. International brands including Michelin, Bridgestone, and Continental maintain premium positioning, particularly in high-specification passenger car and commercial vehicle OEM channels, but have faced margin pressure from intensifying domestic competition.

The competitive environment is undergoing structural consolidation, as demonstrated by Sailun's acquisition of Bridgestone's Shenyang commercial tire operations in July 2025, and the listing of Zhongce Rubber on the Shanghai Stock Exchange's main board in June 2025. Chinese manufacturers are simultaneously executing global factory expansion strategies in Southeast Asia, the Americas, and Europe to serve export markets while circumventing anti-dumping measures. The shift toward EV-specific tires and smart tire technology is creating a new competitive dimension where technology investment is becoming as important as production scale in determining market share trajectory.

Founded in 1958 and headquartered in Hangzhou, Zhejiang Province, Zhongce Rubber is one of China's largest and most diversified tire manufacturers, producing products across passenger car, truck and bus, agricultural, and industrial tire categories. The company operates an extensive domestic manufacturing network supplemented by its first overseas facility in Indonesia launched in December 2024. Zhongce completed its main board listing on the Shanghai Stock Exchange in June 2025, enhancing its capital access for ongoing expansion at domestic plants in Tianjin, Jintan, Dajiangdong, and Fuyang. Zhongce's dual domestic and international capacity strategy, combined with its diversified product portfolio, positions it as one of the most resilient competitors in China's evolving tire market.

Founded in 1993 and headquartered in Singapore with primary manufacturing and commercial operations in China, Giti Tire is a prominent international tire group with major production facilities across multiple Chinese provinces. Giti serves both OEM and aftermarket channels and has invested consistently in product development for premium fitment applications. In 2025, Giti Tire secured its first OEM winter tire fitment contract with BMW for the BMW 1 Series, marking a significant quality validation milestone for the brand in the premium passenger car segment. Giti's combination of international brand governance, strong domestic manufacturing infrastructure, and growing OEM credentials across both domestic and European automakers gives it a distinctive competitive positioning in China's tire market.

Founded in 2002 and headquartered in Qingdao, Shandong Province, Sailun Group is one of China's most rapidly expanding tire manufacturers, having achieved double-digit revenue and volume growth in 2024 with production of 74.81 million tires representing a 27.59% year-on-year increase. Sailun's strategy combines aggressive domestic capacity investment with international manufacturing diversification through facilities in Cambodia, Indonesia, and Mexico. The July 2025 acquisition of Bridgestone's Shenyang commercial vehicle tire plant for RMB 265 million, followed by a RMB 1.70 billion expansion commitment announced in August 2025, demonstrates the company's ambition to lead the consolidation of China's commercial tire segment. Sailun's strong balance sheet performance and manufacturing scale make it one of the most consequential competitive forces in the current market.

Founded in 1960 and headquartered in Seoul, South Korea, Kumho Tire is an established international tire brand with a significant presence in the China market through dedicated manufacturing facilities and extensive distribution. Kumho serves passenger car, SUV, and light commercial vehicle segments, competing in the mid-to-premium price tier against both domestic Chinese brands and other international manufacturers. The company's Chinese operations supply both domestic OEM customers and aftermarket distribution channels, leveraging its Korean-origin brand reputation for product quality in a market where consumer preferences are bifurcating between value-focused domestic brands and internationally recognised quality-positioned alternatives.

Other key players in the market are Hankook Tire & Technology Co., Ltd., Triangle Tyre Co., Ltd., Double Coin Tyre Group Ltd., AEOLUS TYRE Co. Ltd., Cheng Shin Rubber (Xiamen) Ind., Ltd., and Prinx Chengshan Holdings Ltd., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

The China Tire Market is at an inflection point, shaped by the world's largest EV revolution, relentless domestic manufacturer consolidation, and a global expansion wave by Chinese tire groups rewriting the competitive map of the international industry. Our comprehensive analysis of the China Tire Market 2026 gives you the data-driven clarity to navigate design technology shifts, identify the fastest-growing regional demand centres, assess the EV-specific tire opportunity, and benchmark the competitive strategies of Zhongce, Sailun, Giti, and their key rivals. Download your free sample now and explore the opportunities in China's expanding tire market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the China tire market reached an approximate value of USD 46.61 Billion.

The market is projected to grow at a CAGR of 7.90% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 99.70 Billion by 2035.

The major drivers of the market are increased consumer demand for high-performance and premium tires, e-commerce logistics industry and government investment in infrastructure.

The key trends of the market include growing integration of smart technology, eco-friendly innovation, radialization in transport, and global expansion of domestic brands.

The major regions in the market are Shanghai, Zhejiang, Guangdong, Jiangsu, Beijing, and others.

The various designs considered in the market report are radial and bias.

The various types considered in the market report are tube tire and tubeless tire.

The sales channels considered in the China tire market report are OEM and aftermarket.

The major players in the market are Zhongce Rubber Group Co., Ltd., Giti Tire, Sailun Group Co., Ltd., Kumho Tire Co., Inc., Hankook Tire & Technology Co., Ltd., Triangle Tyre Co., Ltd., Double Coin Tyre Group Ltd., AEOLUS TYRE Co. Ltd., Cheng Shin Rubber (Xiamen) Ind., Ltd., and Prinx Chengshan Holdings Ltd., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Design |

|

| Breakup by Type |

|

| Breakup by Season Type |

|

| Breakup by Vehicle Type |

|

| Breakup by Sales Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.