Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

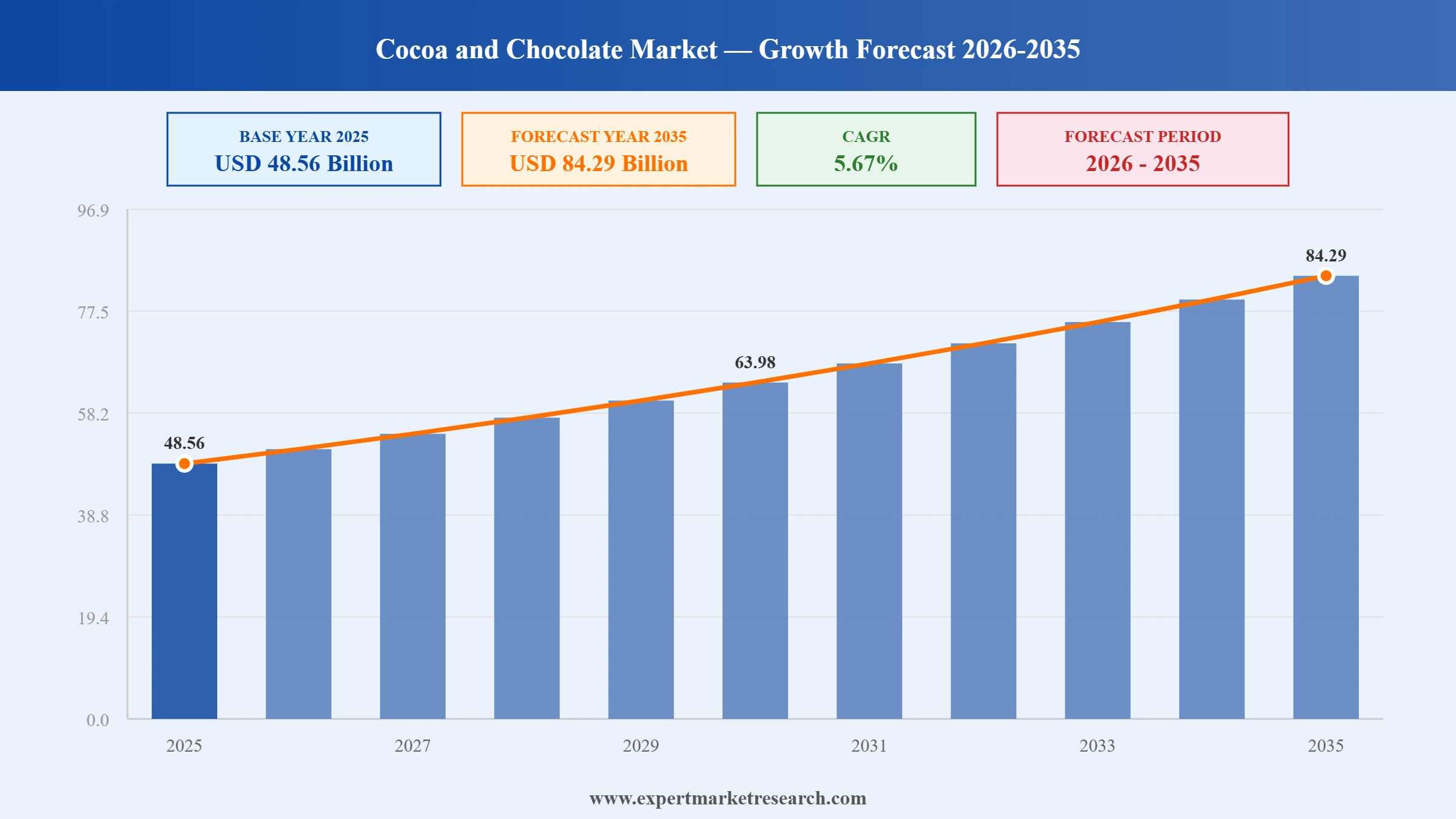

The global cocoa and chocolate market reached a value of USD 48.56 Billion at 2025 and is projected to expand at a CAGR of around 5.67% during the forecast period of 2026-2035. With growing consumer demand for premium and artisanal chocolate products, expanding applications of cocoa derivatives in cosmetics and pharmaceuticals, rising chocolate consumption in emerging economies across Asia Pacific and Latin America, and the shift toward sustainable and traceable cocoa sourcing gaining commercial momentum, the market is expected to reach USD 84.29 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global cocoa and chocolate market is undergoing a period of significant structural adjustment, shaped by cocoa price normalisation following record 2024 highs, leading players exploring portfolio restructuring, and growing Asian market investments. Sustainability pressures, rising consumer preferences for premium dark and functional chocolate, and supply chain resilience are the defining commercial priorities for manufacturers and processors across the value chain.

In April 2026, Barry Callebaut issued a profit warning as global cocoa bean prices fell sharply, declining over 57% from their December 2024 peak. CEO Peter Schumacher noted that falling cocoa prices supported strong free cash flow but pressured revenue in price-linked B2B contracts, highlighting the ongoing volatility affecting the global cocoa and chocolate market's supply economics.

In February 2026, Barry Callebaut released its 'Top Chocolate Confectionery Trends 2026 and Beyond' report, based on a 24-market, 24,000-person consumer survey conducted in September 2025. The report identified evolving consumer expectations around value, cleaner flavour profiles, and premium sensory experiences as the primary innovation forces reshaping chocolate confectionery globally.

In December 2025, Barry Callebaut announced exploration of separating its cocoa ingredients division from its chocolate manufacturing operations, with reported options including a spin-off, joint venture, or complete sale. The strategic review, triggered by cocoa price volatility and market pressure, represents one of the most significant potential restructurings in the global cocoa and chocolate market's recent history.

In July 2025, Barry Callebaut inaugurated its third chocolate manufacturing facility in India, a 20,000-square-metre greenfield factory in the Ghiloth industrial area of Neemrana, Rajasthan. The plant produces chocolate and compound in various formats, strengthening the company's regional manufacturing footprint and reinforcing India's growing importance as a production and consumption hub within the global cocoa and chocolate market.

After cocoa futures reached record highs of approximately USD 12,931 per metric tonne in December 2024, prices declined over 50% through 2025 as stronger harvests materialised in West Africa. This price normalisation provides relief to cocoa and chocolate manufacturers reliant on B2B ingredient procurement, though supply chain risks linked to climate and crop disease remain a structural concern.

Premium, single-origin, and high-cocoa-content dark chocolate are among the fastest-growing sub-categories in the global cocoa and chocolate market. Health-conscious consumers seeking antioxidant benefits and artisan experiences are driving this shift, prompting manufacturers to expand dark chocolate ranges and invest in bean-to-bar transparency, which is increasingly a purchasing decision factor in mature markets.

Sustainability certification from Fairtrade, Rainforest Alliance, and UTZ is shifting from premium positioning to a baseline requirement across European and North American retail procurement. The EU Deforestation Regulation, coming into effect for cocoa and chocolate products, is accelerating supply chain traceability investments among global players and reshaping sourcing strategies across the cocoa value chain.

Asia Pacific is the fastest-growing region for chocolate consumption, led by China, India, and Southeast Asia where rising incomes and Western dietary influences are driving first-time buyer growth. Barry Callebaut's July 2025 India facility opening illustrates how leading processors are investing ahead of demand in this cocoa and chocolate market growth corridor.

Cocoa butter's use in cosmetics and pharmaceuticals is expanding beyond traditional food applications, driven by consumer interest in natural moisturisers and functional ingredients. This multi-sector demand for cocoa derivatives provides processors with additional revenue streams that buffer against confectionery market cyclicality and support broader cocoa and chocolate market revenue diversification.

The Expert Market Research’s report titled “Global Cocoa and Chocolate Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

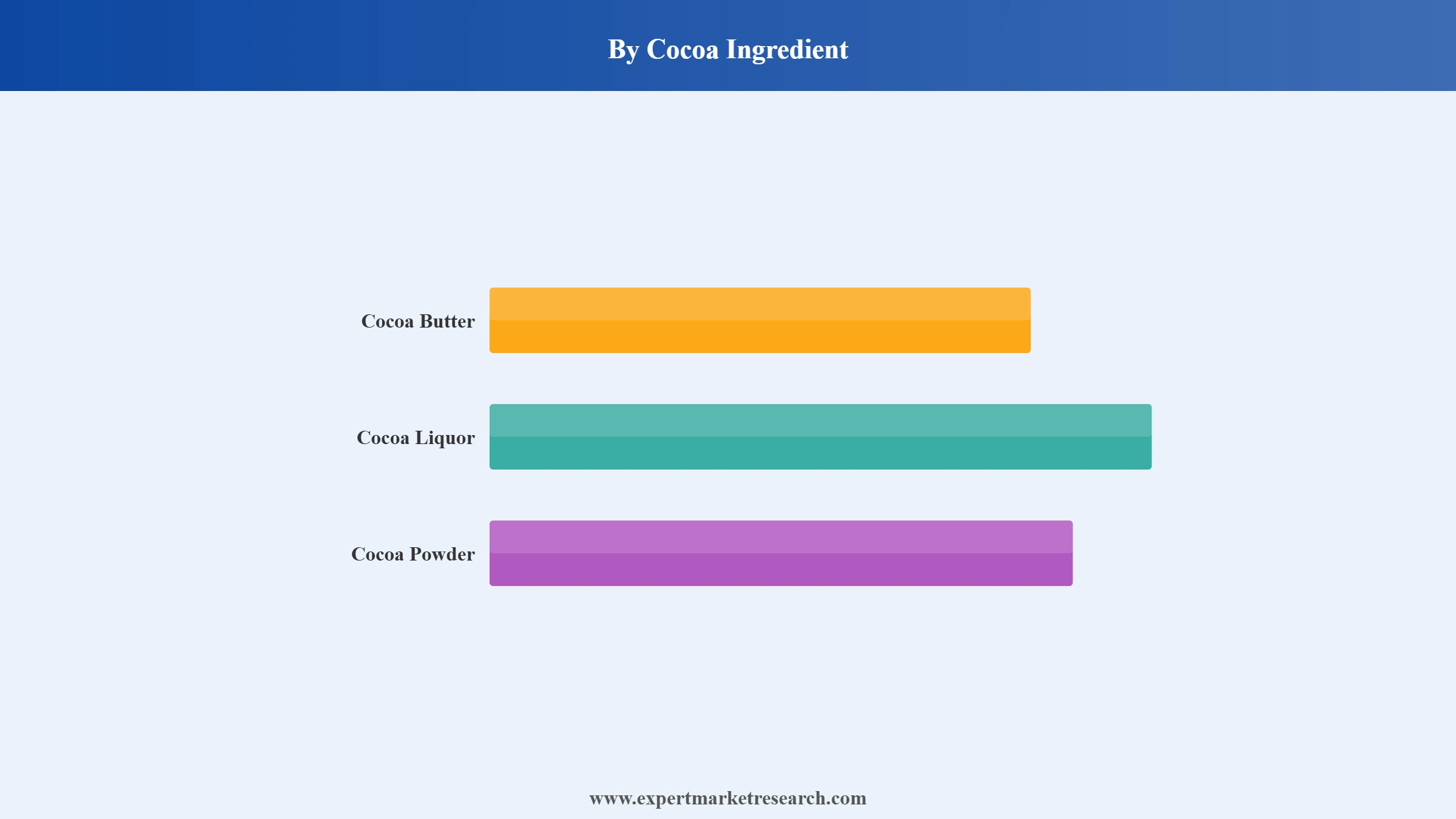

Market Breakup by Cocoa Product Type

Key Insight: Cocoa butter commands the highest value among cocoa derivatives, valued in both premium chocolate manufacturing and cosmetics formulations for its emollient and textural properties. Cocoa liquor serves as the foundational ingredient for all chocolate types. Cocoa powder drives the bakery, beverage, and food manufacturing segments globally. The December 2025 strategic review by Barry Callebaut exploring the potential separation of its cocoa ingredients division from its chocolate manufacturing operations underscores the commercial complexity of managing these three derivatives as distinct product businesses.

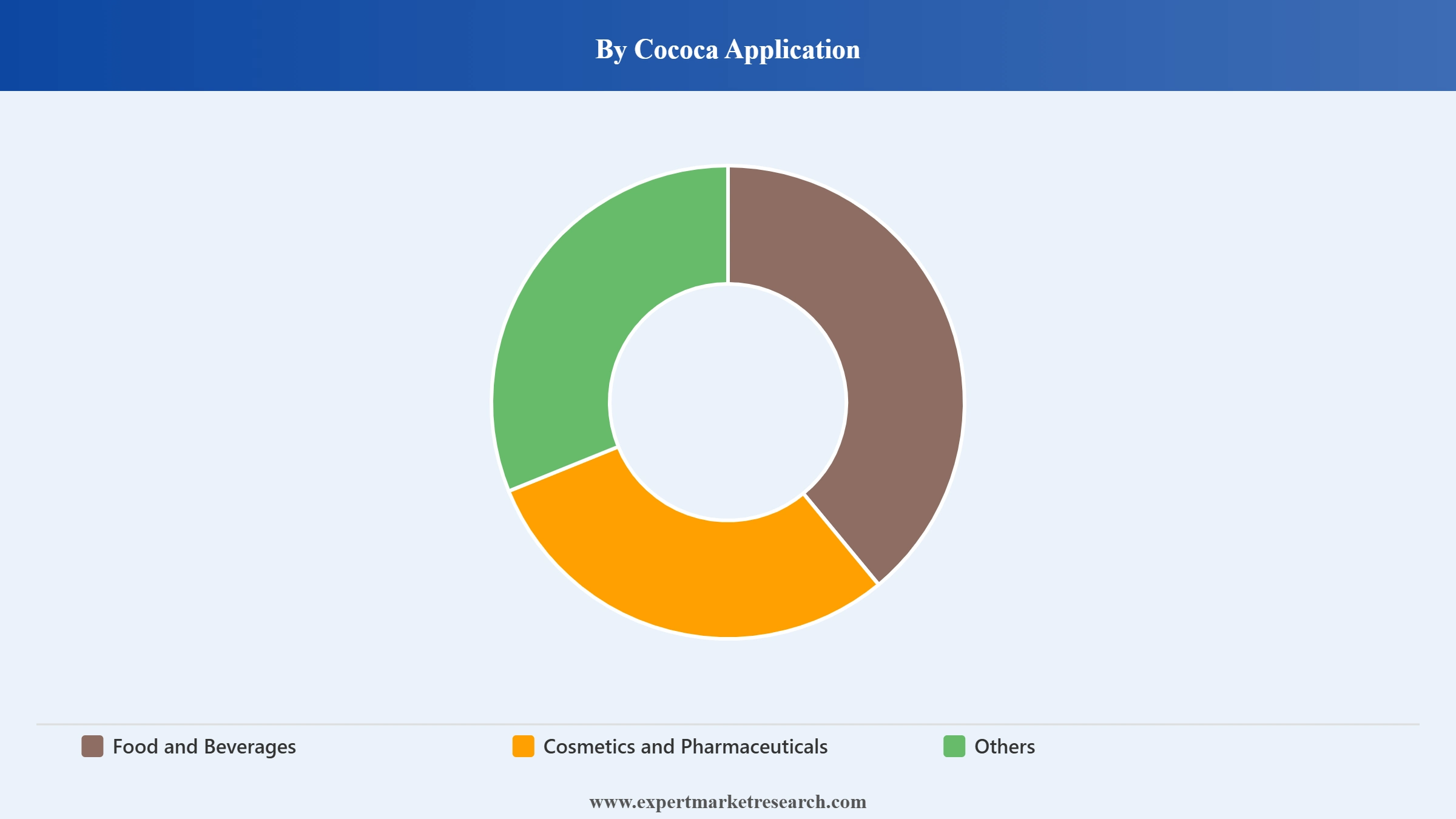

Market Breakup by Application

Key Insight: Food and beverages accounts for the dominant share of global cocoa application, with the confectionery sub-segment generating the largest revenues across everyday chocolate bars, boxed assortments, and premium artisan formats. Dairy applications including chocolate milk, ice cream, and desserts, and bakery applications in cakes and coatings, provide stable industrial volume. Cosmetics and pharmaceuticals represent a growing secondary channel as cocoa butter's natural emollient and antioxidant properties drive adoption in skincare and nutraceutical formulations, particularly as clean-label consumer demand expands.

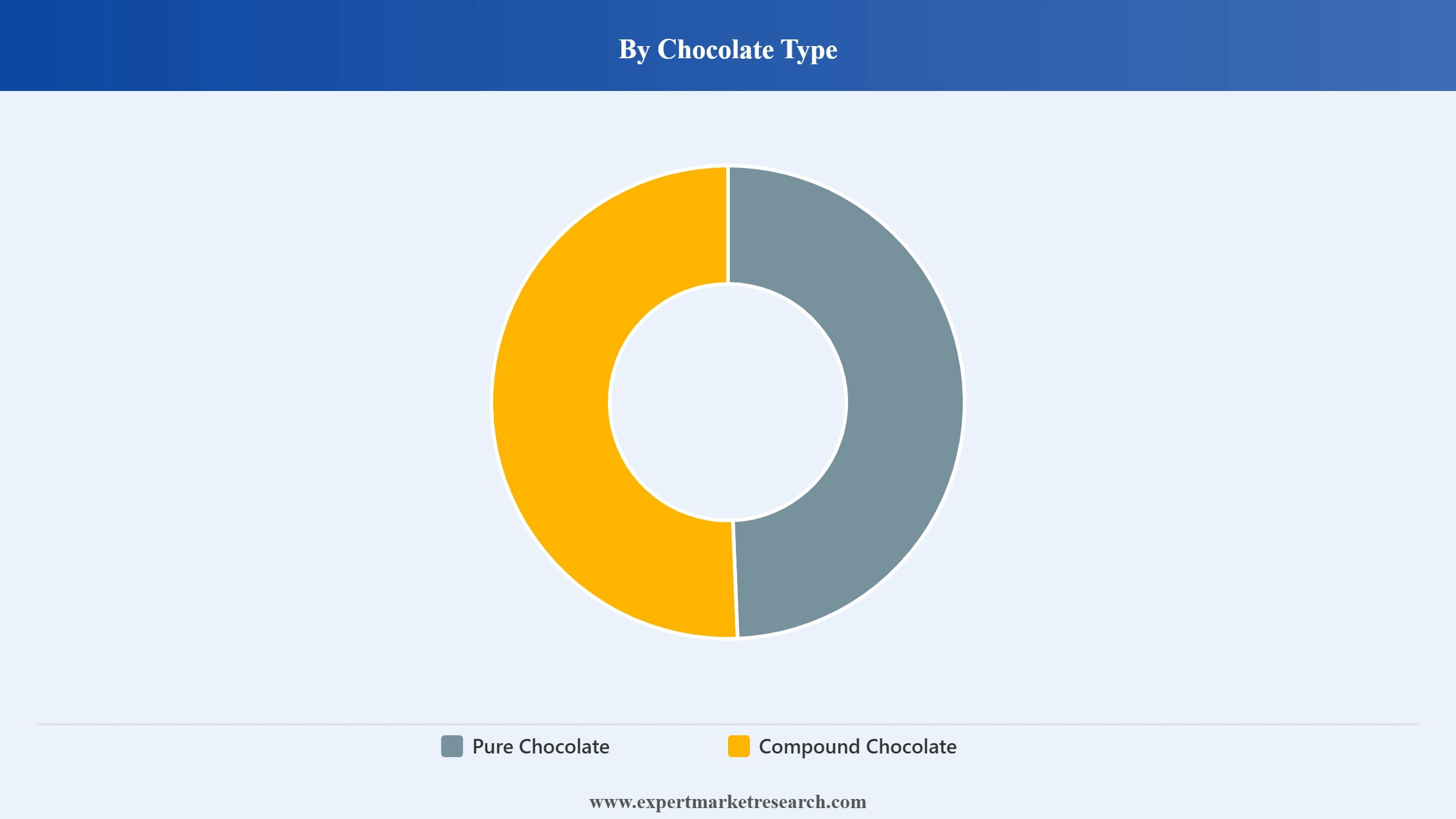

Market Breakup by Chocolate Type

Key Insight: Pure chocolate commands premium pricing and leads B2C and artisan market segments, with its cocoa butter content delivering the superior melting properties and flavour complexity that consumers, baristas, and chefs demand. Compound chocolate, which substitutes cocoa butter with lower-cost vegetable fats, dominates cost-sensitive industrial food manufacturing applications including bakery coatings, confectionery centres, and ice cream products across emerging markets. Barry Callebaut's July 2025 India facility, producing both chocolate and compound formats, reflects the strategic importance of serving both segments from a single manufacturing footprint.

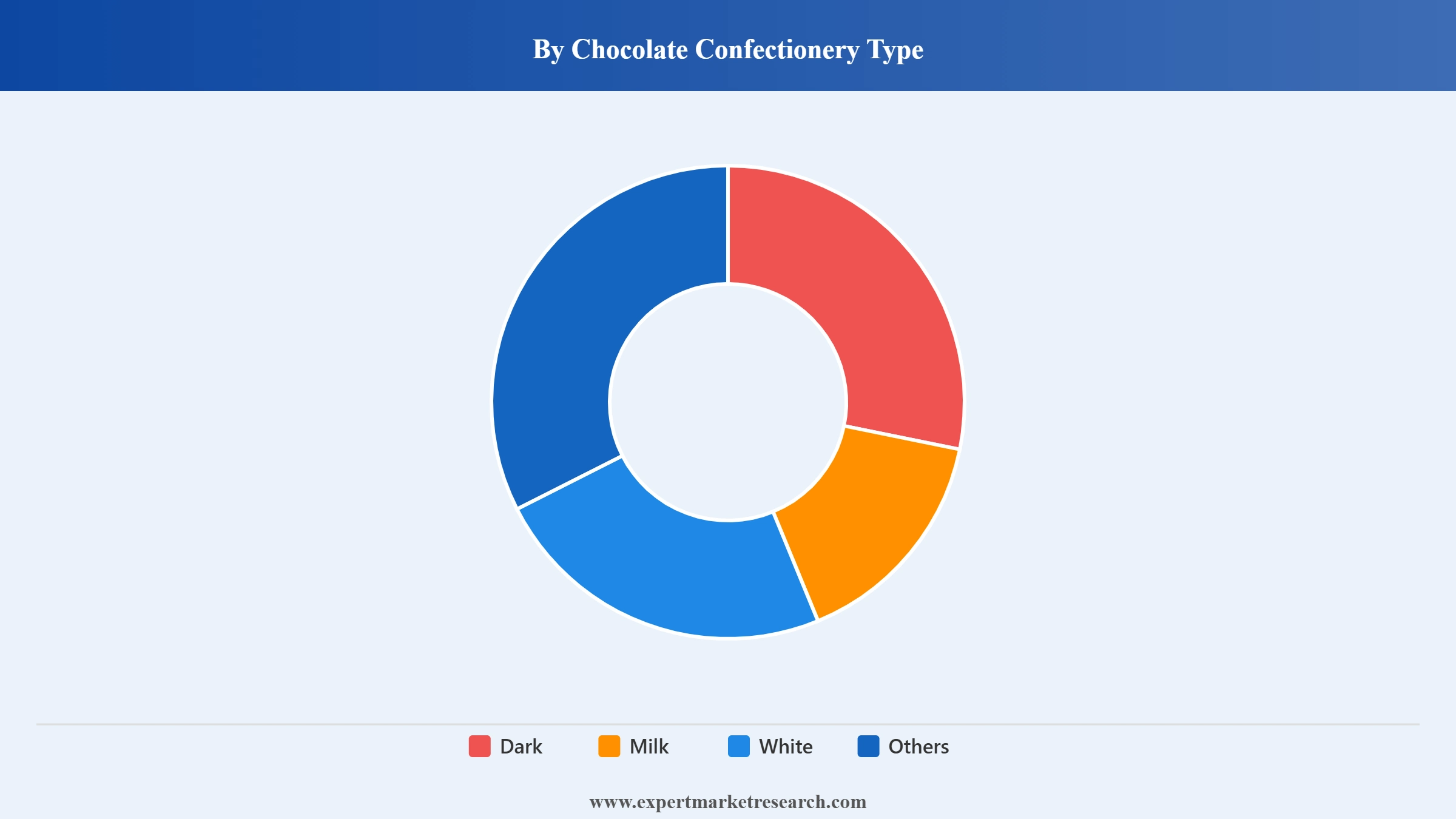

Market Breakup by Chocolate Confectionery Type

Key Insight: Milk chocolate holds the largest volume share of the global chocolate confectionery market, anchored by broad consumer appeal across age groups and well-established brand portfolios from Mars, Mondelez, and Nestle. Dark chocolate is the fastest-growing type, driven by health-conscious consumer demand for antioxidant benefits, premium single-origin formats, and higher cocoa-content positioning. White chocolate serves niche confectionery and bakery applications. Barry Callebaut's February 2026 Trends 2026 report identified premium sensory experiences and clean-label formulation as the primary innovation forces reshaping all confectionery type categories globally.

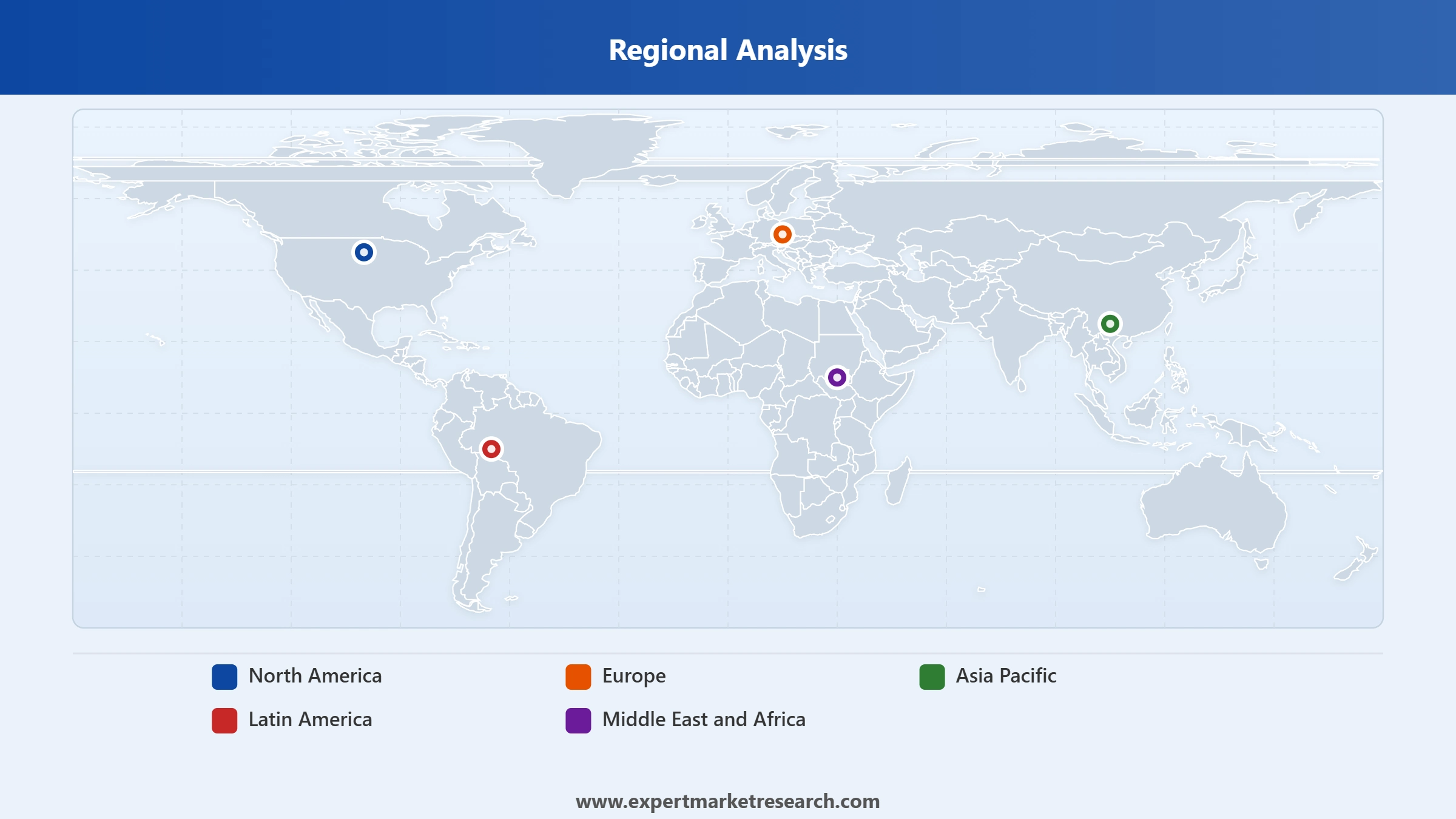

Market Breakup by Region

Key Insights: Europe leads the global cocoa and chocolate market with the highest per-capita consumption, concentrated in Switzerland, Germany, and the United Kingdom where premium and gifting chocolate demand is deeply embedded in consumer culture. North America follows, anchored by strong confectionery and food manufacturing demand. Asia Pacific is the fastest-growing region, with first-time chocolate consumer acquisition accelerating in China and India. West Africa, anchored by Cote d'Ivoire and Ghana, dominates global cocoa bean production at approximately 70% of supply, making the Middle East and Africa region pivotal to the upstream raw material supply chain.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By cocoa product type, cocoa butter dominates the market due to its dual role in premium chocolate manufacturing and cosmetics applications

Cocoa butter commands the highest value among cocoa derivatives, essential for delivering the smooth melt, texture, and sheen that define premium chocolate. Its application extends beyond confectionery into cosmetics, where it is a sought-after ingredient in moisturisers, lip balms, and skincare products. Rising demand for natural, plant-derived ingredients in beauty formulations is reinforcing cocoa butter's cross-sector value, providing processors with revenue diversification that buffers against cocoa bean price volatility.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Cocoa liquor serves as the primary building block for dark and milk chocolate production, with demand closely tracking confectionery manufacturing volumes. Cocoa powder is a versatile derivative widely used across bakery, beverage, and food manufacturing applications, from chocolate cakes and biscuits to drinking cocoa and flavoured dairy products. The December 2025 strategic review by Barry Callebaut exploring the potential separation of its cocoa ingredients division reflects the increasing commercial complexity of managing these cocoa product types within a single integrated value chain.

By application, food and beverages dominates the market due to sustained global demand across confectionery, dairy, and bakery sectors

Food and beverages holds the dominant share of global cocoa and chocolate application, driven by universal consumer demand for chocolate-based confectionery, dairy, and bakery products. The confectionery sub-segment generates the largest revenues, encompassing everyday chocolate bars, seasonal gifting products, and the fast-growing premium artisan chocolate category. Dairy applications including chocolate milk, ice cream, and chocolate desserts, alongside bakery uses in cakes, biscuits, and pastries, provide stable industrial volume demand that anchors the food and beverages application across both mature and emerging markets.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Cosmetics and pharmaceuticals represent a growing secondary application as cocoa butter's natural emollient, antioxidant, and skin-nourishing properties gain wider recognition in the beauty and health industries. The EU Deforestation Regulation, which came into effect for cocoa and chocolate products, is driving sustainable sourcing practices across all food and beverages applications, reshaping procurement strategies and creating differentiation opportunities for certified supply chain participants in the global cocoa and chocolate market.

By chocolate type, compound chocolate accounts for the larger volume share of the market due to its cost advantage in industrial food manufacturing

Compound chocolate holds the larger volume share of the global chocolate market, particularly across industrial food manufacturing applications in emerging economies. By replacing cocoa butter with lower-cost vegetable fats, compound chocolate delivers a cost-efficient solution for bakery coatings, confectionery centres, ice cream bars, and biscuit applications where price sensitivity is high and cocoa butter's premium melting properties are less critical. Across Asia Pacific, Latin America, and the Middle East, compound chocolate is the default choice for the high-volume food processing sector.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Pure chocolate, however, commands premium pricing and leads the B2C, gifting, and artisan market segments, where cocoa butter content is a key quality marker for consumers and food service operators. Barry Callebaut's July 2025 India facility was designed to produce both pure chocolate and compound formats, reflecting the strategic necessity of serving both segments from a single integrated manufacturing hub. The growing premiumisation trend across mature markets and an emerging aspirational consumer class in Asia Pacific are steadily expanding pure chocolate's volume share within the global cocoa and chocolate market.

By chocolate confectionery type, milk chocolate leads the market due to mass consumer appeal and established global brand portfolios

Milk chocolate holds the largest share of the global chocolate confectionery market by volume, driven by its broad appeal across all consumer age groups and its dominant position within the product portfolios of leading brands including Mars, Mondelez (Cadbury and Milka), and Nestle. Its creamy sweetness, familiar flavour profile, and strong retail visibility in hypermarkets, convenience stores, and food service channels ensure consistent high-volume turnover across both premium and value tiers in mature and emerging markets worldwide.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Dark chocolate is the fastest-growing confectionery type, propelled by health-conscious consumer demand for antioxidant benefits, premiumisation, and expanding single-origin and high-percentage-cocoa formats. Barry Callebaut's February 2026 Chocolate Confectionery Trends 2026 report, based on a 24-market consumer survey, identified premium sensory experiences and cleaner flavour profiles as the dominant forces reshaping consumer expectations, directly benefiting dark chocolate's market share. White chocolate and other specialty types serve niche bakery, confectionery, and gifting applications, completing the range available across the global cocoa and chocolate market.

Europe leads the global cocoa and chocolate market due to the highest per-capita chocolate consumption and a deeply embedded confectionery culture

Europe holds the largest regional share of the global cocoa and chocolate market, driven by centuries-old confectionery traditions and the highest per-capita chocolate consumption in countries including Switzerland, Germany, and the United Kingdom. European consumers lead demand for premium, sustainably certified, and dark chocolate formats, making the region the most commercially significant revenue contributor for processors and branded manufacturers. The EU Deforestation Regulation is reshaping sourcing practices across the cocoa value chain, compelling all operators supplying European retail markets to demonstrate deforestation-free supply chains.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific is the fastest-growing region in the global cocoa and chocolate market, with China and India representing the most dynamic consumer acquisition opportunities. Rising disposable incomes, urbanisation, and the adoption of Western confectionery habits are expanding the first-time chocolate buyer pool at scale. Barry Callebaut's July 2025 inauguration of its third India manufacturing facility in Neemrana, Rajasthan, producing both chocolate and compound in various formats, underscores the scale of investment flowing into Asia Pacific to serve this fast-developing growth corridor.

The global cocoa and chocolate market is led by a small number of vertically integrated global processors and a larger group of branded chocolate manufacturers. Barry Callebaut and Cargill dominate upstream cocoa processing and B2B chocolate supply, while Mars, Mondelez, and Nestle lead consumer-facing chocolate brands. The market is highly concentrated at the processor level but more fragmented at retail, where premium artisan brands compete alongside mass-market incumbents.

Competition is intensifying around sustainable sourcing credentials, product innovation, and supply chain resilience. Players are investing in AI-driven flavour development, cocoa genomics, and vertical integration to manage commodity risk. The EU Deforestation Regulation and rising consumer scrutiny of social conditions in cocoa-growing regions are adding compliance costs but also creating differentiation opportunities for companies with transparent and certified supply chains.

Founded in 1996 and headquartered in Zurich, Switzerland, Barry Callebaut is the world's largest chocolate and cocoa products manufacturer, with annual sales of approximately CHF 14.8 billion in fiscal year 2024/25. In July 2025, it opened its third India facility in Neemrana, Rajasthan. In December 2025, the company announced a strategic review exploring the separation of its cocoa and chocolate divisions.

Founded in 1911 and headquartered in McLean, Virginia, Mars is one of the world's largest privately held food companies, with confectionery brands including Snickers, M&M's, Twix, and Maltesers. Mars held over 12% of global chocolate market share in 2025, operating across confectionery, petcare, and food manufacturing with a deep presence in both mature and emerging markets globally.

Founded in 2012 and headquartered in Chicago, Illinois, Mondelez International owns the Cadbury chocolate brand globally, along with Milka, Toblerone, and Cote d'Or. As one of the five leading global chocolate companies, Mondelez invests extensively in sustainable cocoa sourcing through its Cocoa Life programme, covering over 200,000 farmers across Cote d'Ivoire, Ghana, and India.

Founded in 1866 and headquartered in Vevey, Switzerland, Nestle is one of the world's largest food and beverage companies, with chocolate brands including KitKat, Aero, and After Eight sold in over 180 countries. Nestle's cocoa sourcing is governed by its Responsible Sourcing Standard, with active programmes supporting farmer livelihoods and deforestation-free supply chains across key production regions.

Other key players in the market are Olam Food Ingredients (OFI), Cargill Incorporated, Meiji Holdings Co. Ltd., Cocoa Processing Company Limited (CPC), and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Gain the full picture of global cocoa and chocolate market dynamics with our latest comprehensive report. From cocoa bean supply and pricing trends to premium chocolate innovation and Asia Pacific consumer growth, this report provides the data-driven intelligence that processors, manufacturers, retailers, and investors need. Understand where the market is heading and identify the sub-segments and regions offering the strongest growth potential. Download your free sample today.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 48.56 Billion.

The market is projected to grow at a CAGR of 5.67% between 2026 and 2035.

The major players in the market are Barry Callebaut AG, Cargill Incorporated, Nestlé S.A., Olam Food Ingredients (ofi), Cocoa Processing Company Limited (CPC), Mondelez International, Inc., and Meiji Holdings Co., Ltd., among others.

Cocoa butter holds a leading share in the market due to its increasing use in the pharmaceutical and cosmetic sector.

Companies are prioritising sustainable cocoa sourcing to address environmental concerns and social issues such as child labor and deforestation. Programs like Nestlé’s Cocoa Plan and Barry Callebaut’s Forever Chocolate initiative emphasize traceability, farmer training, and community development. Moreover, chocolate producers are increasingly focussing on products innovation in terms or infusion of organic ingredients and new flavours.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Cocoa Ingredient |

|

| Breakup by Cococa Application |

|

| Breakup by Chocolate Type |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.