Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

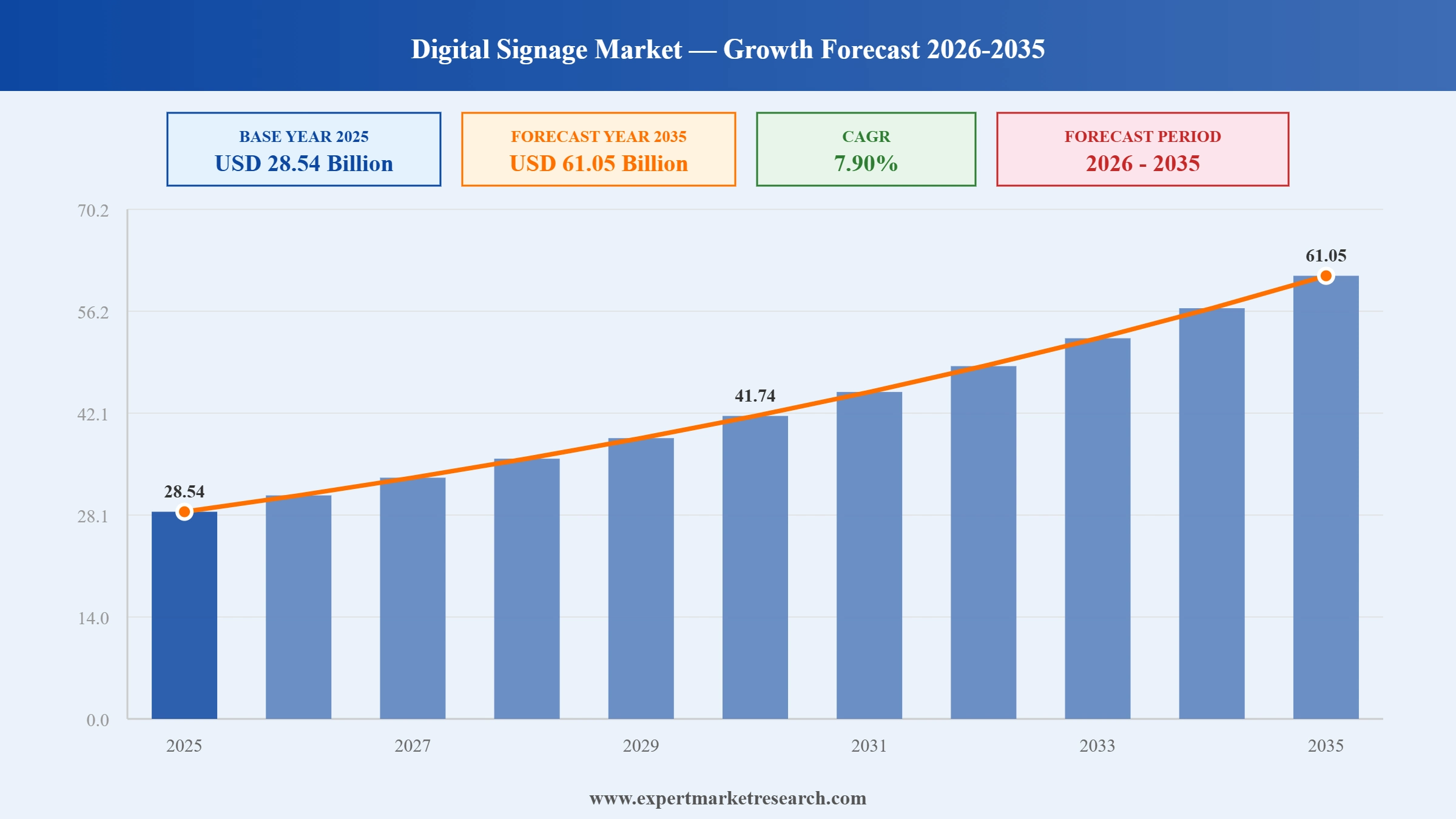

The global digital signage market reached USD 28.54 Billion in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 7.90% during the forecast period of 2026 to 2035, reaching USD 61.05 Billion by 2035, according to Expert Market Research. This sustained growth trajectory reflects the accelerating transition from traditional static signage to intelligent, networked display ecosystems that deliver dynamic, data-driven, and personalised content across retail, transportation, hospitality, healthcare, corporate, and outdoor advertising environments.

The digital signage industry in 2026 is defined by the convergence of AI-powered content generation, cloud-based content management systems, MicroLED and fine-pitch LED display technology advancement, programmatic digital-out-of-home (DOOH) advertising monetisation, and the integration of audience analytics that transform passive display screens into measurable engagement and revenue platforms. Smart city infrastructure investments, expanding retail media network adoption, 5G connectivity enabling real-time dynamic content distribution, and growing computer vision audience analytics are collectively driving the digital signage market's next phase of revenue and margin expansion.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The digital signage market refers to the global commercial ecosystem encompassing networked digital display systems, content management software, media players, installation services, and audience analytics platforms that enable the delivery of dynamic multimedia content including advertisements, informational messaging, wayfinding, entertainment, and real-time data across digital screens in public, commercial, and institutional environments. Digital signage systems are advanced communication solutions that replace traditional printed or static signage with remotely manageable, content-flexible digital displays capable of real-time content updates, targeted messaging, interactive experiences, and audience measurement.

The digital signage industry spans multiple display technology categories LCD panels, direct-view LED arrays, OLED displays, MicroLED, and projection-based systems across a broad range of deployment contexts: indoor retail environments, outdoor advertising billboards and urban displays, transportation hub wayfinding systems, hospitality and hotel in-room and lobby signage, corporate communication displays, healthcare patient information systems, and educational institution displays. Content management systems (CMS) including cloud-based platforms enabling remote multi-site content scheduling, audience analytics, and programmatic advertising integration represent the fastest-growing value layer in the digital signage stack, as the industry transitions from one-time hardware sales toward recurring software-as-a-service revenue models. Samsung's AI Studio within its VXT platform and the broader shift toward AI-automated content generation exemplify this structural value migration from hardware to intelligent software.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The accelerating transition from traditional printed and static signage to dynamic, remotely managed digital display networks is the fundamental structural driver of global digital signage market revenue growth. Businesses across retail, transportation, hospitality, healthcare, and corporate environments are investing in digital signage to enable real-time content distribution, targeted messaging, and measurable audience engagement capabilities that static printed signage cannot deliver. The emergence of AI-powered content creation tools exemplified by Samsung's AI Studio, which transforms static product images into signage-ready video content within the VXT cloud platform is dramatically lowering the content production barrier for organisations deploying digital signage at scale, enabling marketing teams without professional design expertise to maintain fresh, contextually relevant content across distributed display networks.

Government-led smart city programmes and urban digital infrastructure investments are generating substantial structural demand for outdoor LED digital signage displays across transportation networks, public spaces, and urban mobility corridors. Major broadband and digital infrastructure investment programmes are making outdoor LED digital signage displays a core component of urban mobility and public-safety communication networks. Smart city initiatives across North America, Europe, and Asia Pacific are integrating digital signage with urban management systems for real-time traffic information, emergency communications, public transit updates, and civic engagement applications expanding the addressable market for digital signage solutions well beyond commercial advertising into public sector procurement channels.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The convergence of digital-out-of-home (DOOH) advertising with programmatic buying platforms enabling automated, data-driven ad placement across digital signage networks with audience targeting, real-time bidding, and measurable campaign performance attribution represents one of the most commercially significant growth drivers in the digital signage market. Retailers are channelling capital into interactive touchscreen digital signage that doubles as a retail media revenue stream, turning physical store display infrastructure into a programmatic content platform for brand advertising. The retail media network model where major retailers monetise their store display infrastructure and first-party customer data to offer brands premium advertising inventory is creating a new revenue category that directly incentivises capital investment in in-store digital signage infrastructure.

The widespread deployment of 5G network infrastructure across major metropolitan markets is enabling real-time dynamic content delivery capabilities that were previously constrained by bandwidth and latency limitations of legacy connectivity infrastructure. 5G-connected digital signage displays can receive contextually relevant content updates in near-real-time triggering messaging changes based on live audience demographic data, weather conditions, inventory levels, or breaking news events creating a new category of intelligent reactive signage that moves beyond pre-scheduled content loops. Edge computing integration, where AI inference and content processing are performed locally on the media player or display device rather than centrally in the cloud, further reduces latency and enables uninterrupted operation even in connectivity-constrained environments.

Continuous innovation in display technology particularly the commercial maturation of MicroLED, fine-pitch LED, and high-brightness OLED display formats is expanding the deployment possibilities for digital signage across challenging physical environments and enabling new visual experiences that were previously technically or economically infeasible. Samsung's 130-inch Micro RGB signage unveiled at ISE 2026, combining micro-scale RGB LEDs with the Micro RGB AI Engine Pro, and the 108-inch The Wall All-in-One engineered for installation completable in approximately two hours, illustrate the pace of innovation reducing both the technical complexity and deployment cost of large-format LED signage. Direct-view LED arrays are becoming significantly more energy-efficient, with power consumption per unit of brightness declining materially over recent technology generations improving the total cost of ownership case for LED versus LCD in high-ambient-light and outdoor environments.

Artificial intelligence is transforming every layer of the digital signage value chain from automated content creation to intelligent audience analytics, predictive maintenance, and dynamic content scheduling. Samsung's AI Studio, integrated into the Samsung VXT cloud platform and launched globally in the first half of 2026, represents the commercial vanguard of AI content generation for digital signage: the system transforms static product images into polished, signage-optimised video content automatically, applying refined shadow detailing, adjusted margins, and spatial depth treatments calibrated for Samsung's display portfolio. For enterprise operators managing hundreds or thousands of digital signage displays across distributed retail or corporate networks, AI content generation tools reduce the creative production bottleneck that has historically constrained content freshness and campaign velocity.

The commercial launch of glasses-free 3D digital signage represents the most directionally significant product innovation in the commercial display industry in 2026. Samsung Spatial Signage launched globally in an 85-inch format at ISE 2026 in Barcelona (February 2026) and expanded with a 32-inch compact model for retail shelf and counter deployment (April 2026) delivers three-dimensional content without requiring viewers to wear 3D glasses, enabling immersive product visualisation, brand storytelling, and attention-capturing display experiences in high-traffic retail, hospitality, and corporate environments. Recognised as a CES 2026 Innovation Award Honoree in the Enterprise Tech category, Spatial Signage creates a new premium tier in the commercial display market that enables brands to differentiate physical retail experiences in ways that e-commerce cannot replicate.

The digital signage industry is undergoing a structural shift from hardware-centric one-time transaction business models toward recurring software revenue streams centred on cloud-based content management system (CMS) subscriptions, audience analytics services, and AI content generation tools. Samsung's VXT platform updates including Smart Download, automated screen preset scheduling, and AI Studio represent Samsung's strategic investment in converting commercial display hardware relationships into long-term software subscription engagements. This SaaS model evolution benefits digital signage operators through centralised multi-location management, automatic firmware and content security updates, and data-driven insights into display performance and audience engagement capabilities unavailable on standalone media player configurations.

The integration of computer vision cameras with on-device AI inference chips enables digital signage displays to perform real-time demographic profiling, dwell-time measurement, gaze tracking, and emotional response analysis without transmitting personally identifiable data off-premises. These audience analytics capabilities transform digital signage from a broadcast medium into a measurable engagement platform with documented ROI metrics comparable to digital online advertising channels. Brands deploying AI-triggered programmatic content where the displayed message changes dynamically based on the detected audience demographic profile, time of day, or queue length observe measurably higher engagement rates relative to static content scheduling. This measurement capability is critical to unlocking retailer and brand investment in digital signage as a performance marketing channel.

Interactive touchscreen digital signage encompassing self-service kiosks, wayfinding terminals, product configurators, and digital menu boards with touch-enabled ordering is one of the fastest-growing product sub-categories within the digital signage market. The post-pandemic acceleration of self-service consumer preferences across retail, food service, banking, healthcare, and transportation has expanded the addressable market for interactive kiosk deployments significantly. Samsung's 2026 partnership expansion with Logitech for Microsoft Teams Rooms certifying Samsung 4K Smart Signage QBC series as part of Microsoft's Express Install for Teams Rooms, enabling meeting room setups completable in under an hour exemplifies the convergence of interactive signage with enterprise collaboration infrastructure.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global digital signage market faces persistent operational and commercial challenges that constrain adoption velocity, particularly among small and medium-sized businesses and in markets with nascent digital infrastructure. High upfront capital costs encompassing display hardware procurement, professional installation, content management software licensing, network infrastructure, and ongoing content production investment represent the most consistently cited barrier to entry for organisations evaluating digital signage deployment for the first time. While display hardware costs have declined substantially over the past decade as LCD and LED manufacturing has matured and commoditised, the total cost of deploying a managed digital signage network including content creation, software subscriptions, and maintenance remains significant for SME operators without dedicated marketing technology budgets. Content creation complexity presents an additional operational challenge: maintaining fresh, contextually relevant, and brand-consistent content across distributed multi-location display networks requires either internal creative resource investment or ongoing agency relationships that add to total programme cost. Cybersecurity vulnerabilities in networked display systems where compromised media players or CMS platforms can enable unauthorised content injection or network intrusion represent a growing challenge as digital signage deployments scale and become more deeply integrated with enterprise IT infrastructure.

Several structural dynamics restrain the pace of digital signage market expansion in specific market segments and geographies. Regulatory restrictions on outdoor digital advertising including brightness limitations, animation frequency caps, and placement restrictions in residential areas and heritage zones constrain the geographic scope and operational parameters of outdoor DOOH deployments across European markets and increasingly in major Asian cities where light pollution regulations are tightening. The proprietary nature of leading digital signage CMS platforms where content management tools are often optimised or exclusively compatible with the hardware ecosystem of a single manufacturer creates switching cost lock-in that limits enterprise customers' ability to diversify hardware vendors or migrate to more cost-effective display alternatives without CMS disruption. Content measurement and attribution standardisation remains limited across the digital signage industry, making it difficult for advertisers to directly compare DOOH audience metrics with digital online advertising performance data a structural barrier to budget allocation from performance-oriented marketing buyers. In developing markets across Sub-Saharan Africa, parts of South Asia, and rural Southeast Asia, inconsistent electrical infrastructure, limited broadband connectivity, and constrained local content production capacity restrain the deployment of networked digital signage solutions beyond major metropolitan areas.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global digital signage market presents substantial and well-documented commercial opportunities across technology, application, and geographic dimensions that support sustained revenue and margin expansion above the 7.90% CAGR baseline through 2035. The programmatic DOOH advertising segment represents one of the most compelling value creation opportunities in the entire digital signage ecosystem: as DOOH inventory becomes tradeable through programmatic platforms with audience-verified targeting and real-time campaign measurement, the digital signage network becomes a competitive channel for performance marketing budgets previously allocated exclusively to online platforms unlocking a materially larger and more recurring advertising revenue stream for DOOH network operators. The convergence of AI content generation, cloud CMS platforms, and audience analytics creates a SaaS layer above commodity display hardware that enables vendors to build high-margin recurring revenue relationships with enterprise customers a structural shift toward subscription economics that significantly improves the lifetime value and revenue visibility of commercial display deployments. Emerging markets across the Gulf Cooperation Council (GCC), India, and Southeast Asia represent the largest geographic expansion opportunity for digital signage, with major smart city infrastructure programmes, rapidly expanding retail modernisation investment, and growing DOOH advertising market development creating simultaneous demand across hardware, software, and services categories. The MicroLED and glasses-free 3D display innovation cycle exemplified by Samsung Spatial Signage is creating a premium product tier with significantly higher average selling prices and gross margins than the maturing LCD commodity tier enabling manufacturers and channel partners to grow revenue and margin simultaneously even in competitive hardware markets. To access the comprehensive opportunity sizing, investment-grade segment and regional forecasts, and technology adoption trajectory analysis, explore Expert Market Research's complete Digital Signage Market report.

Expert Market Research's Digital Signage Market report provides comprehensive segmentation across component, display type, technology, end-use, and location dimensions with market size, share, and CAGR data for each segment over the full 2026 to 2035 forecast period.

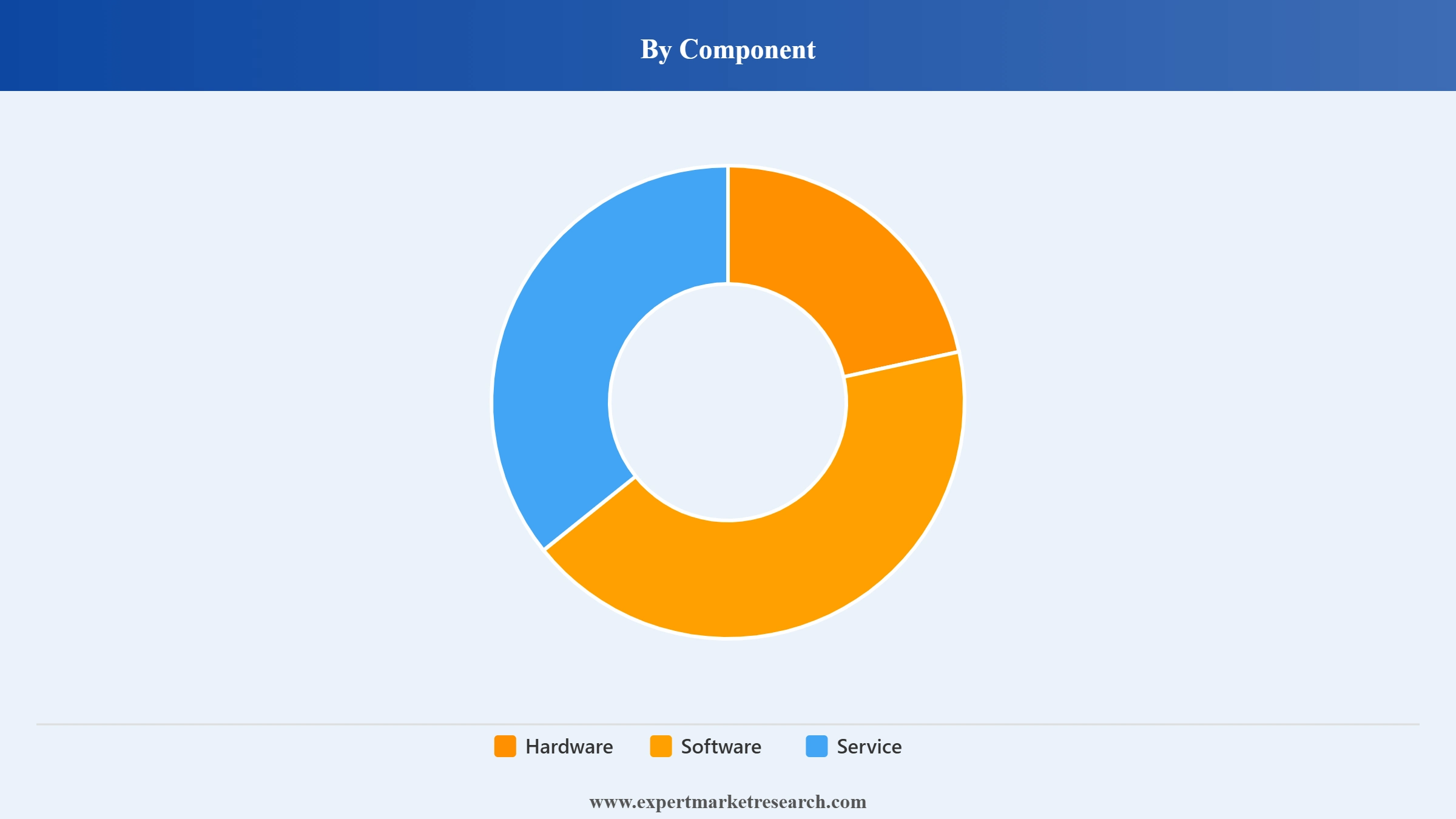

Market Breakup by Component

Hardware is the largest component segment, encompassing LCD and LED display panels, media players, projection systems, mounting hardware, and networking infrastructure. Display hardware spans indoor commercial LCD screens, fine-pitch LED video walls, high-brightness outdoor LED billboards, interactive touchscreen kiosks, and the emerging MicroLED premium tier exemplified by Samsung's Spatial Signage and Micro RGB product lines. Software is the fastest-growing component segment, driven by cloud-based CMS platform adoption, AI content generation tool integration, audience analytics capabilities, and the industry's structural shift toward SaaS recurring revenue models. Services including professional installation, system integration, content management outsourcing, and ongoing maintenance represent a structurally stable segment with growing managed service models where operators pay per-screen monthly fees for fully managed digital signage programmes.

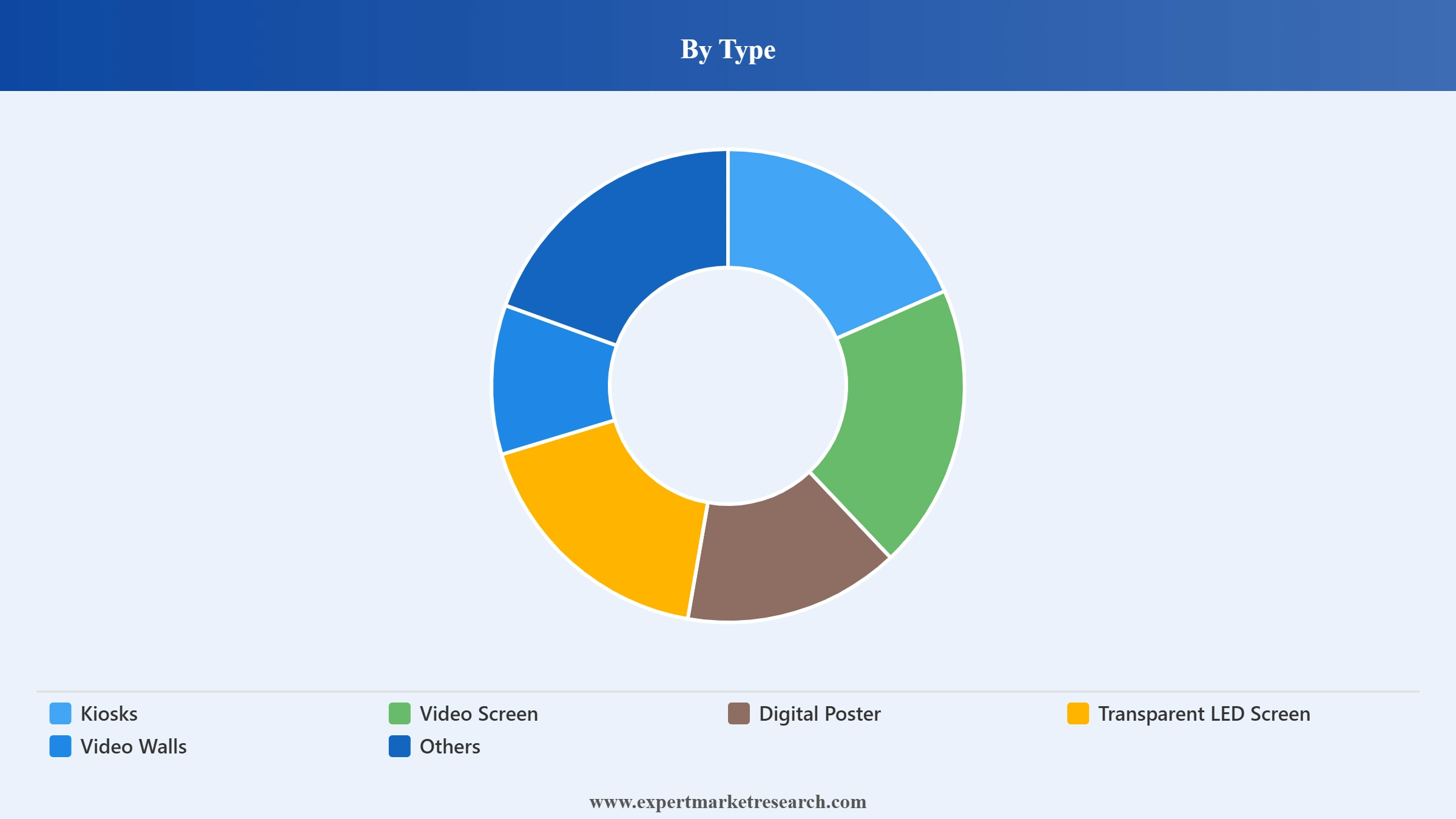

Market Breakup by Type

Kiosks are self-service interactive terminals for ordering, wayfinding, and check-in one of the fastest-growing type segments. Video Screens are the largest segment by unit volume, serving as the foundational display format across all end-use verticals. Digital Posters replicate traditional printed formats digitally, enabling remote content updates in retail storefronts, cinemas, and transit hubs. Transparent LED Screens overlay digital content on glass surfaces storefronts and showroom windows delivering immersive brand experiences while maintaining visibility. Video Walls are multi-panel arrays delivering large-format visuals in flagship retail, control rooms, and corporate environments, commanding the highest average selling prices. Others include digital menu boards, shelf-edge displays, and outdoor billboards.

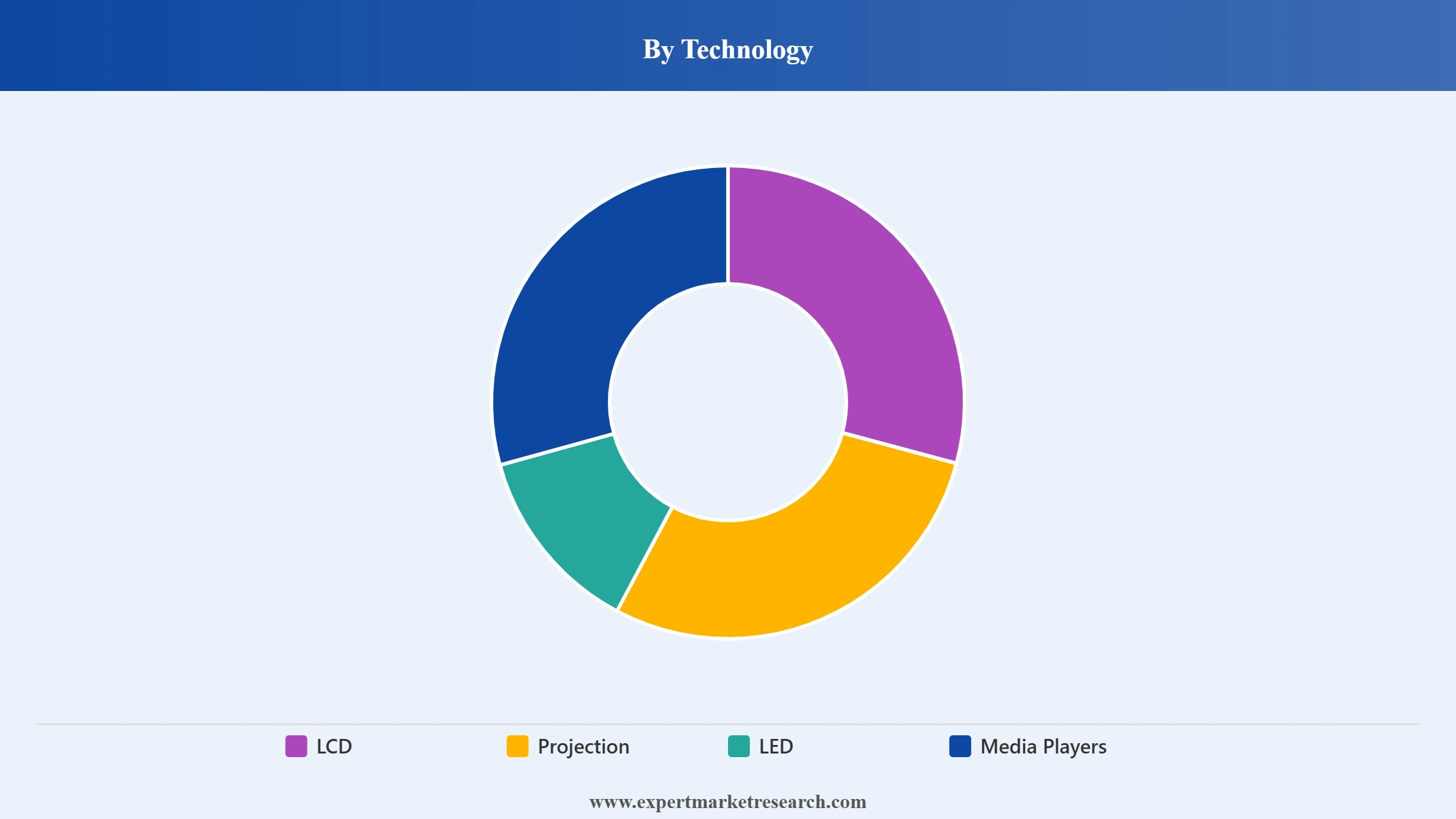

Market Breakup by Technology

LCD technology retains the largest installed base and new deployment share by unit volume, driven by its proven reliability, cost-effectiveness, and comprehensive size range from small shelf-edge screens to large indoor commercial displays. Direct-view LED arrays are displacing LCD video walls in high-ambient-light, outdoor, and premium indoor environments, with energy efficiency, brightness performance, and bezel-free seamless visual quality advantages that justify the premium price positioning. OLED technology serves premium indoor applications where colour accuracy, contrast performance, and ultra-thin form factor commands priority. MicroLED represents the emerging premium frontier illustrated by Samsung's 130-inch Micro RGB signage at ISE 2026 with its Micro RGB AI Engine Pro enabling exceptional brightness, colour volume, and ultra-slim design in flagship retail and premium commercial space deployments.

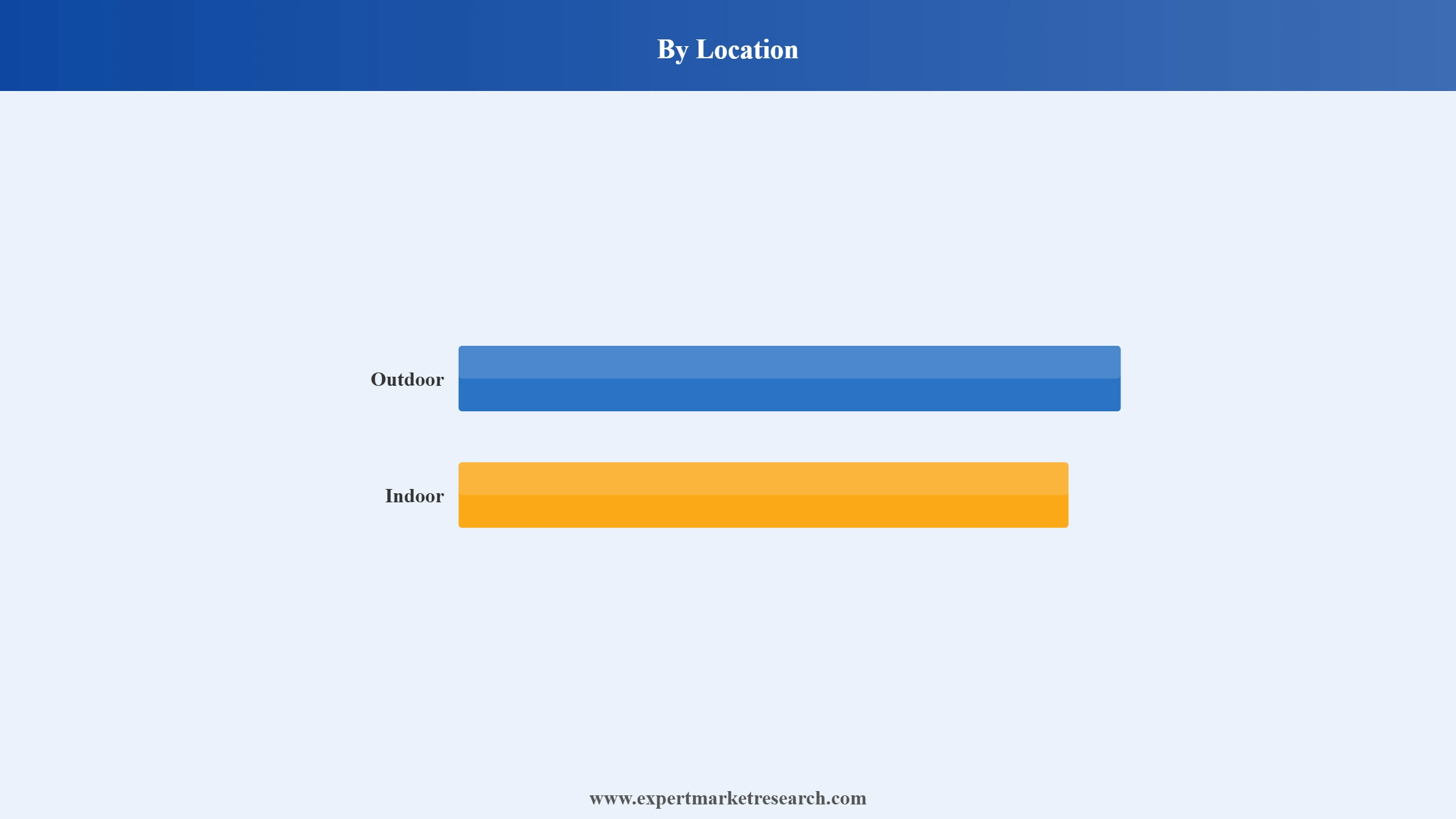

Market Breakup by Location

Indoor digital signage installations dominate by revenue, encompassing the full range of retail, corporate, hospitality, healthcare, and transportation interior deployments. Outdoor digital signage comprising high-brightness LED billboards, roadside digital advertising panels, transit shelter screens, and urban public information displays is growing at a faster CAGR, driven by smart city investment programmes, DOOH advertising market expansion, and the decreasing cost of weatherproof high-brightness LED display technology. LG's range of UL-verified Anti-Discoloration high-brightness outdoor displays, engineered to maintain colour accuracy under prolonged sunlight exposure, exemplifies the technical innovation that is improving outdoor digital signage reliability and reducing lifetime operating costs.

Market Breakup by Application

Retail is the largest application segment, covering in-store promotional displays, interactive kiosks, queue management, and self-checkout across fashion, F&B, electronics, and pharmacy environments. Entertainment venues deploy large-format LED video walls for ticketing, event promotion, and audience engagement. Transport airports, metro systems, bus terminals, and highways is the second-largest segment with the highest uptime and brightness requirements. Healthcare facilities use digital signage for patient queue management, wayfinding, and health education. Hospitality covers hotel lobby signage, in-room entertainment, and restaurant menu boards. Education institutions deploy displays for campus wayfinding, announcements, and collaborative classrooms. BFSI institutions use digital signage for branch communication, queue management, and self-service banking kiosks. Others include government offices and smart city public infrastructure deployments.

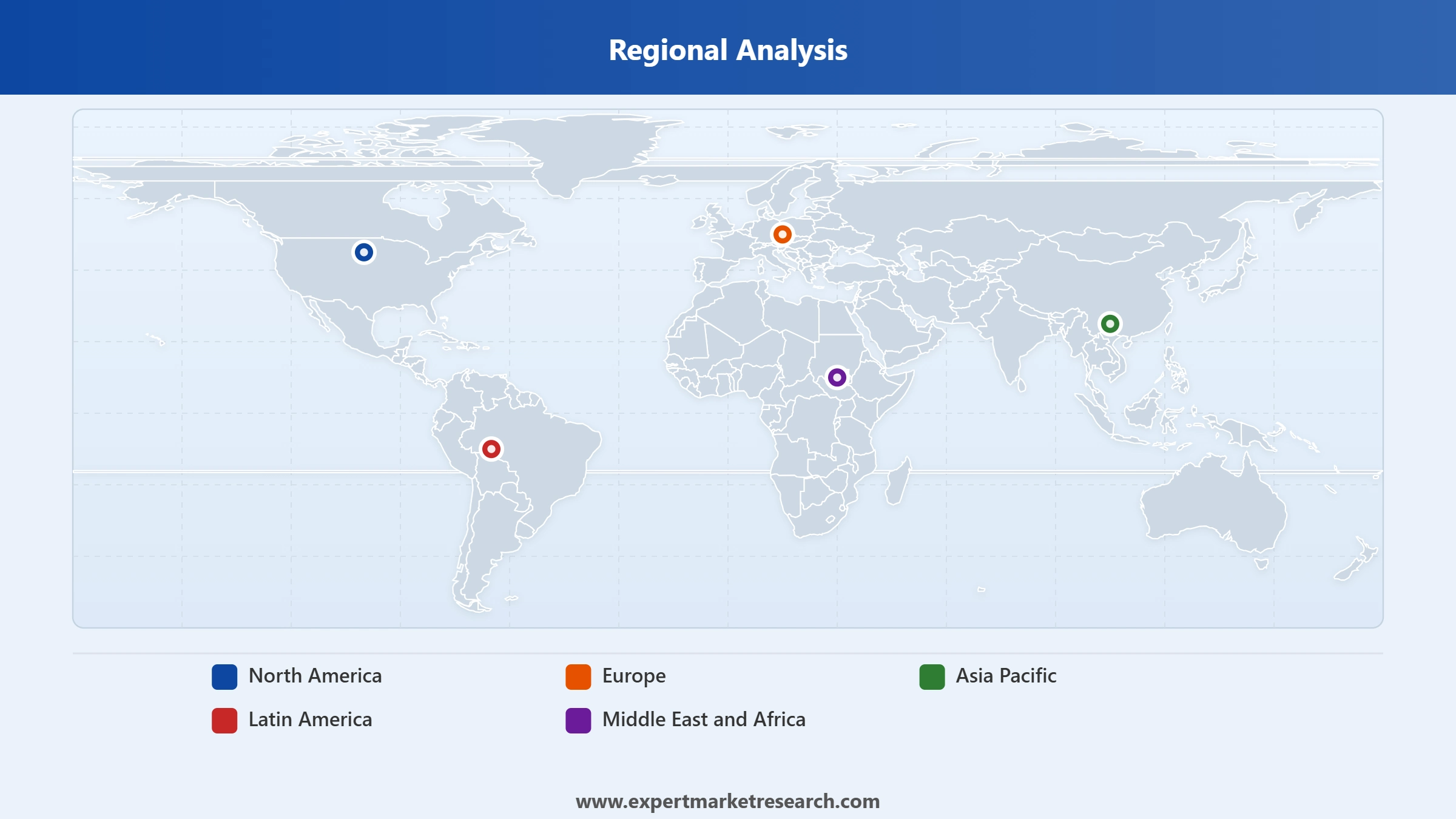

Market Breakup by Region

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America is the world's largest digital signage market by revenue, led by the United States which commands the dominant regional share driven by the maturity of the US retail and DOOH advertising ecosystem, technology adoption leadership, and major smart city and digital infrastructure investment programmes. The US retail industry is a primary growth driver, with major retailers deploying advanced AI-enabled digital signage with audience analytics to maximise customer data utilisation and advertising revenue generation. The US market has seen Apple and Samsung make substantial investments in digital signage infrastructure, leveraging the country's strong technology penetration and enterprise IT adoption base. Canada is a significant secondary market with growing DOOH network expansion and corporate digital communication investment. High upfront costs continue to limit adoption among small and medium-sized US businesses, creating a commercial opportunity for managed service providers offering per-screen monthly pricing models that eliminate capital expenditure barriers.

Europe holds a substantial position in the global digital signage market, characterised by advanced retail digitisation in Western European markets, strong transportation and transit signage investment, and regulatory-driven energy efficiency standards that are accelerating the transition from LCD to LED technology across the continent. The United Kingdom, Germany, France, Italy, and Spain are the primary revenue-generating markets all significant and commercially mature European digital signage markets with deep enterprise deployment and growing investment community engagement. The EU's sustainability regulations encourage energy-efficient LED display adoption, while urban heritage zone regulations constrain outdoor DOOH expansion in certain historical city centres. Europe leads globally in GDPR-compliant audience analytics deployment, where on-device AI processing without cloud data transmission has become the regulatory-required standard for digital signage audience measurement.

Asia Pacific is the fastest-growing regional digital signage market, driven by China's massive domestic retail and outdoor advertising market, India's accelerating retail modernisation and smart city investment, Japan and South Korea's technology-advanced commercial display ecosystems, and Southeast Asia's expanding mall, transportation, and hospitality digital signage deployment. China and India are the key growth enablers in the region, with both markets combining large-scale smart city programmes, rapidly expanding retail real estate infrastructure, and growing DOOH advertising market development. Japan and South Korea are mature, technology-advanced markets where precision fine-pitch LED, OLED, and emerging MicroLED technologies achieve their highest commercial penetration rates. Samsung's investment in display manufacturing capacity expansion including a reported USD 1.7 billion display fabrication expansion in Vietnam highlighting the supply-side commitment to next-generation panel capacity reinforces Asia Pacific's position as the global centre of digital signage hardware production and innovation.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Middle East and Africa region, with particular strength concentrated in the Gulf Cooperation Council (GCC) states UAE, Saudi Arabia, Qatar, Kuwait, Bahrain, and Oman represents one of the most commercially dynamic digital signage markets globally. GCC markets are characterised by exceptionally ambitious smart city programmes including Saudi Arabia's NEOM, UAE Smart Dubai, and Qatar's urban digitalisation initiatives, combined with premium retail environments, world-class transportation hubs, and major hospitality infrastructure that collectively create sustained demand for high-specification digital signage solutions. The region's large-scale construction of new retail, hospitality, and commercial real estate during this period of economic diversification programmes creates significant greenfield digital signage deployment opportunities where digital infrastructure is installed from inception rather than replacing legacy analogue systems. Sub-Saharan Africa remains an early-stage market for formal digital signage deployment, with South Africa and Nigeria as the primary development markets, while North Africa's major urban centres are expanding outdoor LED advertising network investment.

Latin America's digital signage market is anchored by Brazil and Mexico, with growing secondary market development in Colombia, Argentina, and Chile. Brazil's large retail sector, expanding DOOH advertising market, and growing corporate digital communication investment drive the region's largest national digital signage revenue contribution. Mexico's proximity to the US market and the presence of major international retailers, quick-service restaurant chains, and transportation infrastructure operators create consistent demand for digital signage solutions across the retail, food service, and transit segments. The Latin American market faces structural headwinds from economic volatility, import tariffs on display hardware, and inconsistent broadband infrastructure in secondary cities but the combination of a young consumer population, urbanisation-driven retail expansion, and growing DOOH advertising investment supports above-average digital signage market growth relative to the global average over the forecast period.

The global digital signage market is served by a competitive ecosystem spanning display hardware manufacturers, content management software providers, systems integrators, and managed service operators.

| Company | Headquarter | Key Product / 2026 Initiative |

| Samsung Electronics | South Korea | Spatial Signage (glasses-free 3D, CES 2026 Award), AI Studio in VXT CMS, 130-inch Micro RGB, 35.2% global market share (#1 for 17 years) |

| LG Electronics | South Korea | High-brightness UL-verified outdoor displays (Anti-Discoloration), OLED commercial displays, webOS signage platform |

| Sharp NEC Display Solutions | Japan / USA | NEC-branded professional LCD and LED displays, NaViSet Administrator CMS, large-format public display installations |

| Leyard Optoelectronic (Planar) | China / USA | Leyard Planar Simplicity E Series (Jan 2026 launch); fine-pitch LED video walls; Planar Mosaic mosaic display system |

| Daktronics | USA | Large-format LED billboards, sports venue scoreboards and video boards, outdoor LED digital advertising displays |

| Panasonic Connect | Japan | Commercial LCD displays, professional projectors, integrated AV systems for corporate and public sector |

| Sony Professional | Japan | BRAVIA Professional displays, Crystal LED (MicroLED) video walls, enterprise AV solutions |

| BrightSign | USA | Digital signage media players (global market leader in standalone media player segment), BrightAuthor CMS |

| Scala (STRATACACHE) | USA | Enterprise digital signage CMS software, retail media network platform, audience analytics integration |

| Broadsign | Canada | Cloud-based digital signage software for DOOH network operators, programmatic DOOH platform |

| Visix | USA | Digital signage software for corporate communications, meeting room management, campus wayfinding |

| Raydiant | USA | Retail-focused digital signage platform targeting SME operators; emerging market leader in specialised retail signage |

| Others | Various | Delta Electronics, Christie Digital, Omnivex, Deepsky, Intuiface, Winmate, Exceptional 3D, Barco, Broadsign |

Other major players in the digital signage market include NEC Corporation and Planar Systems, Inc., among others. These market players are harnessing advanced technologies such as AI, virtual reality, and 3D ads to stay ahead of the competition.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the global digital signage market attained a value of nearly USD 28.54 Billion.

The market is projected to grow at a CAGR of 7.90% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach USD 61.05 Billion by 2035.

The market is being driven by the growing developments in infrastructure, increasing commercial usage of digital signage, rising technological advancements, surge in commercial demand for advertisements and content creation, and rapid urbanisation.

The demand for 4K and 8K displays and increasing space in retail are the key trends propelling the market's growth.

The major regions in the market are North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa.

The various components in the market are hardware, software, and service.

Kiosks, video screen, digital poster, transparent LED screen, and video walls, among others are the types of digital signages in the market.

The various technologies in the market include LCD, projection, LED, and media players.

The major locations in the market are outdoor and indoor.

The different applications include entertainment, education, healthcare, transport, hospitality, retail, and BFSI, among others.

The major players in the market are NEC Corporation, LG Electronics, Inc., Samsung Electronics Co. Ltd, Panasonic Corporation, Sony Corporation, and Planar Systems, Inc., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Component |

|

| Breakup by Type |

|

| Breakup by Technology |

|

| Breakup by Location |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.