Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

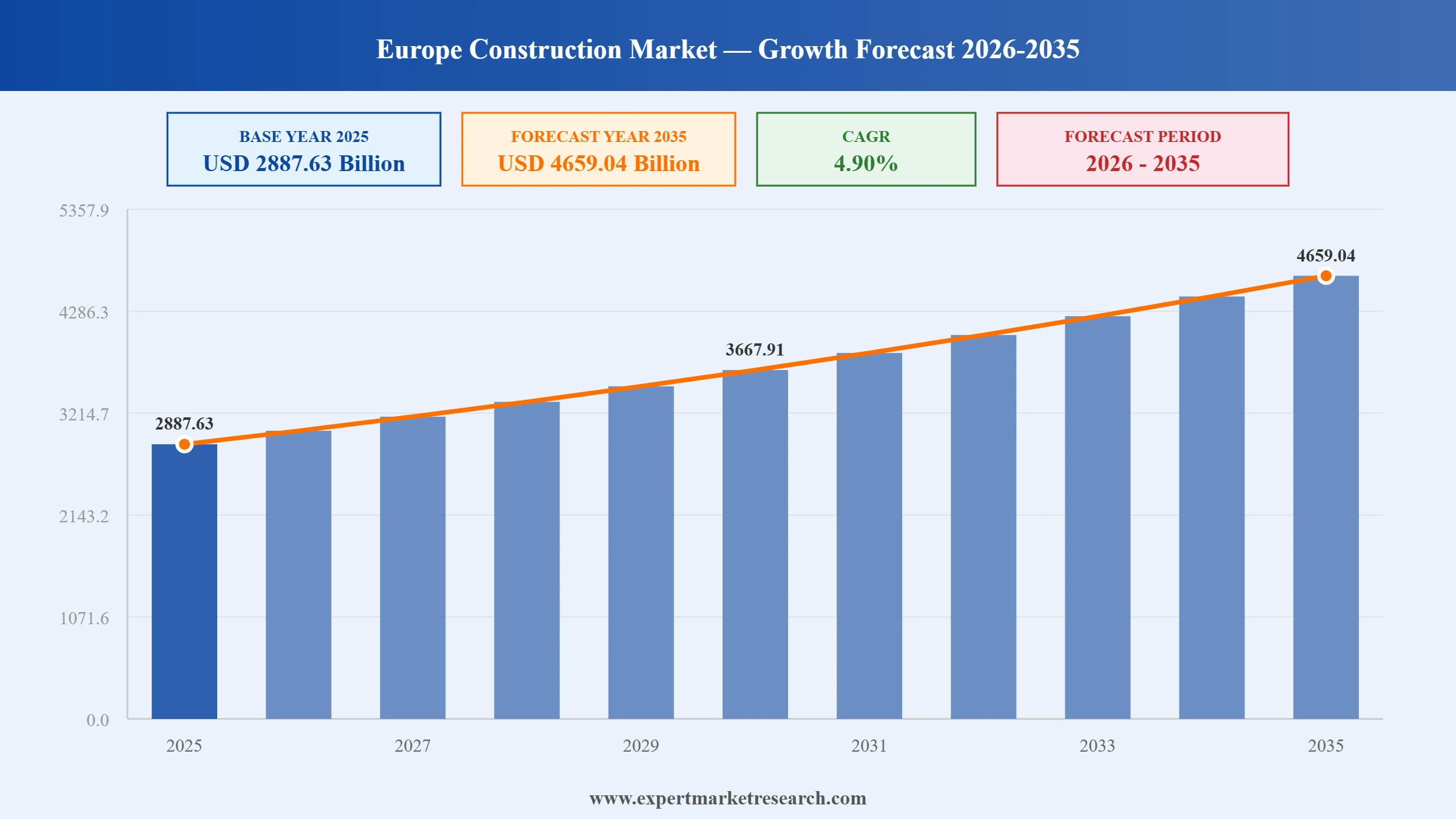

The Europe construction market reached a value of USD 2887.63 Billion at 2025 and is projected to expand at a CAGR of around 4.90% during the forecast period of 2026-2035. With sustained residential housing demand, large-scale healthcare infrastructure investment, EU-backed green building renovation programmes, and growing hospitality sector construction across southern Europe, the market is expected to reach USD 4659.04 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Europe's construction sector is balancing demand for new residential units, healthcare facilities, and hospitality assets against persistent cost inflation and labour shortages. Sustainability mandates under the EU Green Deal and Renovation Wave are reshaping procurement standards, while leading contractors pursue digital construction methods, modular prefabrication, and lower-emission project delivery to retain competitive positions across Germany, the UK, France, and Italy.

In May 2026, Skanska signed a EUR 100 million construction contract with a Nordic public sector client, to be recorded in its second-quarter order bookings. The win reflects Skanska's sustained ability to secure large-scale public infrastructure mandates across the Nordic construction market through its established local delivery network.

In January 2025, VINCI Construction acquired FM Conway, a specialist civil engineering and roadworks company operating primarily in southeast England. The acquisition strengthened VINCI’s UK construction platform, adding civil engineering expertise, BIM-driven workflows, and an established base of public sector road and infrastructure contracts.

In July 2025, Kiloutou, the European equipment rental operator, expanded its heavy earthmoving and aerial lift fleet through acquisitions in Denmark and Italy, boosting its construction support capability across the European market and strengthening its ability to serve civil and residential contractors.

In June 2025, Fayat Group completed its acquisition of Mecalac, a compact construction equipment specialist, adding 29 production sites and diversifying its portfolio beyond road-building into compact earthmoving equipment. The move reflects continued consolidation among Europe's integrated construction and infrastructure service providers.

The EU Renovation Wave targets doubling Europe's annual building renovation rate, directing capital toward energy-efficient upgrades. This programme creates consistent demand for the Europe construction market through plumbing, insulation, glazing, and structural retrofits across both owner-occupied and social housing stock.

Ageing demographics are driving hospital, clinic, and care facility construction across Europe. The Nantes New CHU Hospital in France and multiple NHS hospital upgrades in the UK exemplify the public investment pipeline sustaining healthcare construction demand and supporting Europe construction market growth in the healthcare vertical.

Germany anchors the Europe construction market by total investment, backed by federally funded affordable housing programmes, energy-efficient building regulations, and large infrastructure renewal. Construction investment in Germany has consistently outpaced the EU average, driven by residential shortage, public transit, and industrial facility demand.

Labour shortages and cost pressures are accelerating adoption of modular and prefabricated construction methods. Skanska, Bouygues, and Balfour Beatty have invested in off-site manufacturing capabilities, reducing project timelines and improving quality control in residential and commercial building programmes across the Europe construction market.

Net Zero and ESG commitments by institutional investors are making BREEAM and LEED certification a baseline requirement for new commercial construction. VINCI, Eiffage, and Acciona are integrating low-carbon materials and circular design into project delivery, raising the sustainability bar across the Europe construction market.

The report by Expert Market Research, titled "Europe Construction Market Report and Forecast 2026-2035", offers a detailed analysis of the market based on the following segments:

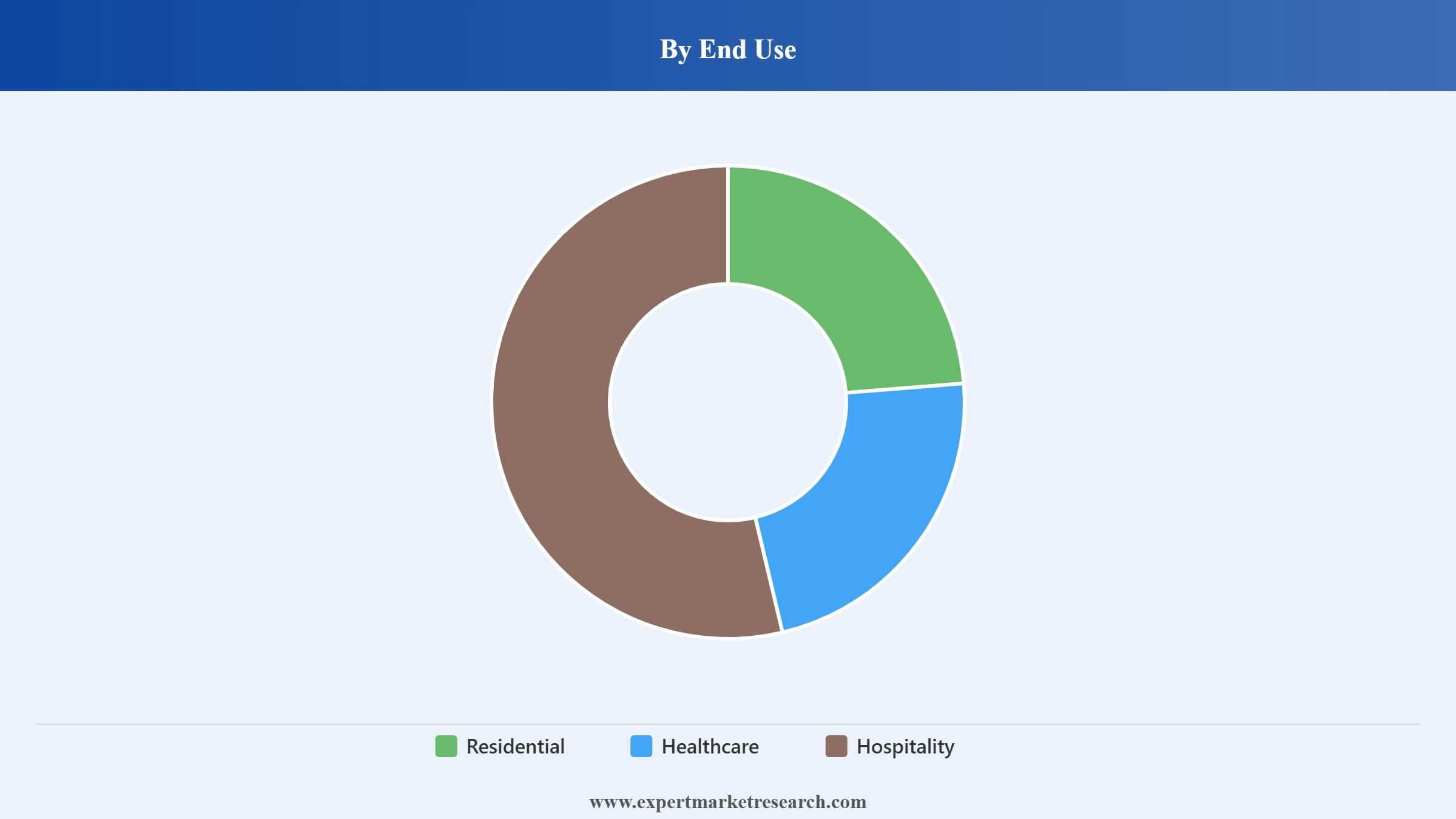

Market Breakup by End Use

Key Insight: Residential construction holds the dominant share because urban housing shortages, EU affordable housing mandates, and energy renovation requirements generate structural, multi-cycle demand across all major European economies. Healthcare is the fastest-growing end use, reflecting public investment in ageing-proof hospitals and primary care networks. Hospitality construction is recovering strongly in southern Europe as international tourism returns, with luxury hotel and resort developments in Spain, Italy, and Greece supporting segment growth in the Europe construction market.

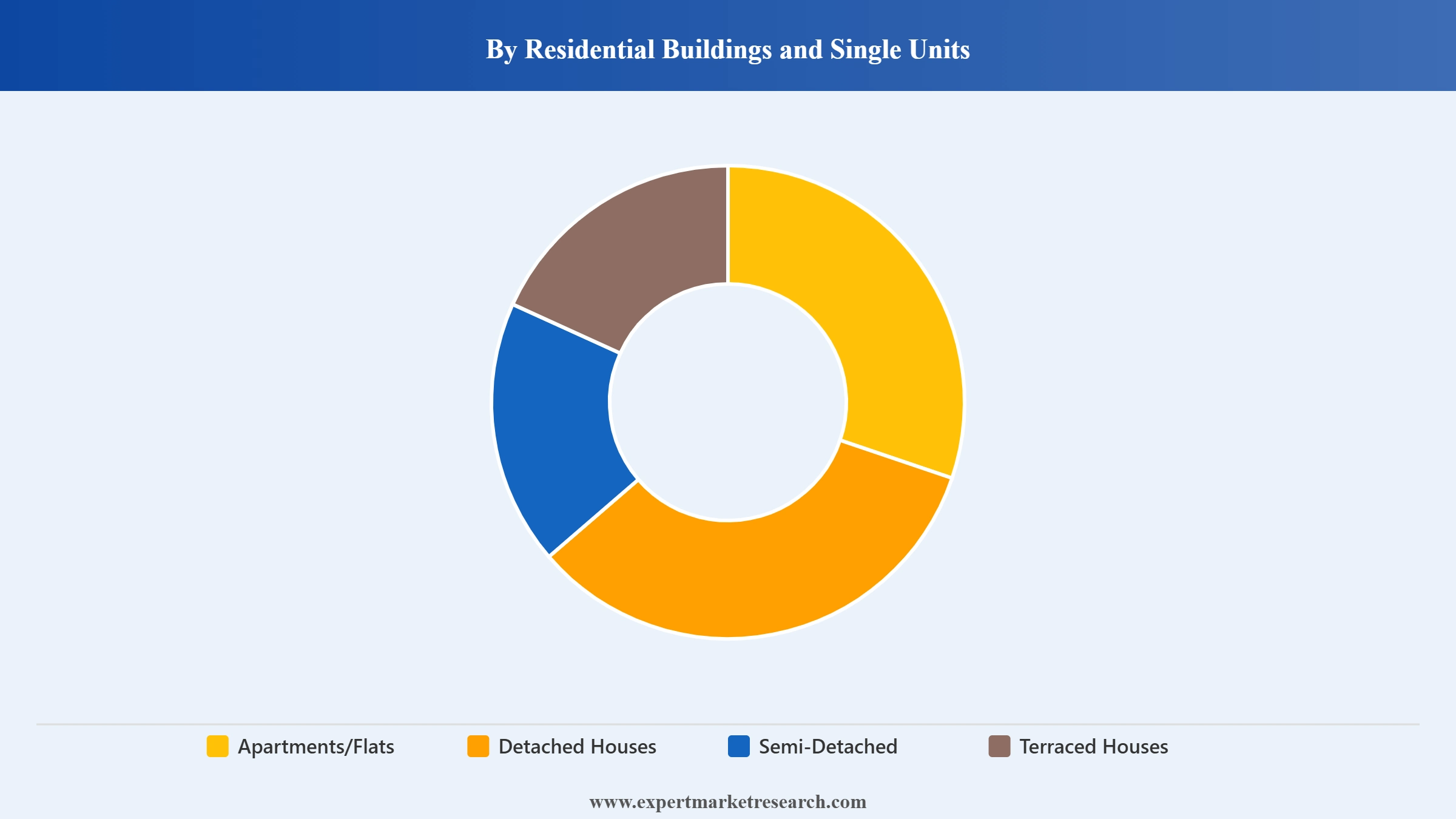

Market Breakup by Residential Buildings and Single Units

Key Insight: Apartments and flats account for the largest share of residential construction by volume across densely populated urban markets including Germany, France, and the Netherlands, where land scarcity and municipal planning favour multi-family formats. Detached houses remain the preferred format in rural and suburban Germany and the Nordic countries. Semi-detached and terraced house construction dominates the UK residential pipeline, where brownfield land reuse policies and affordability constraints drive demand for attached typologies across the Europe construction market.

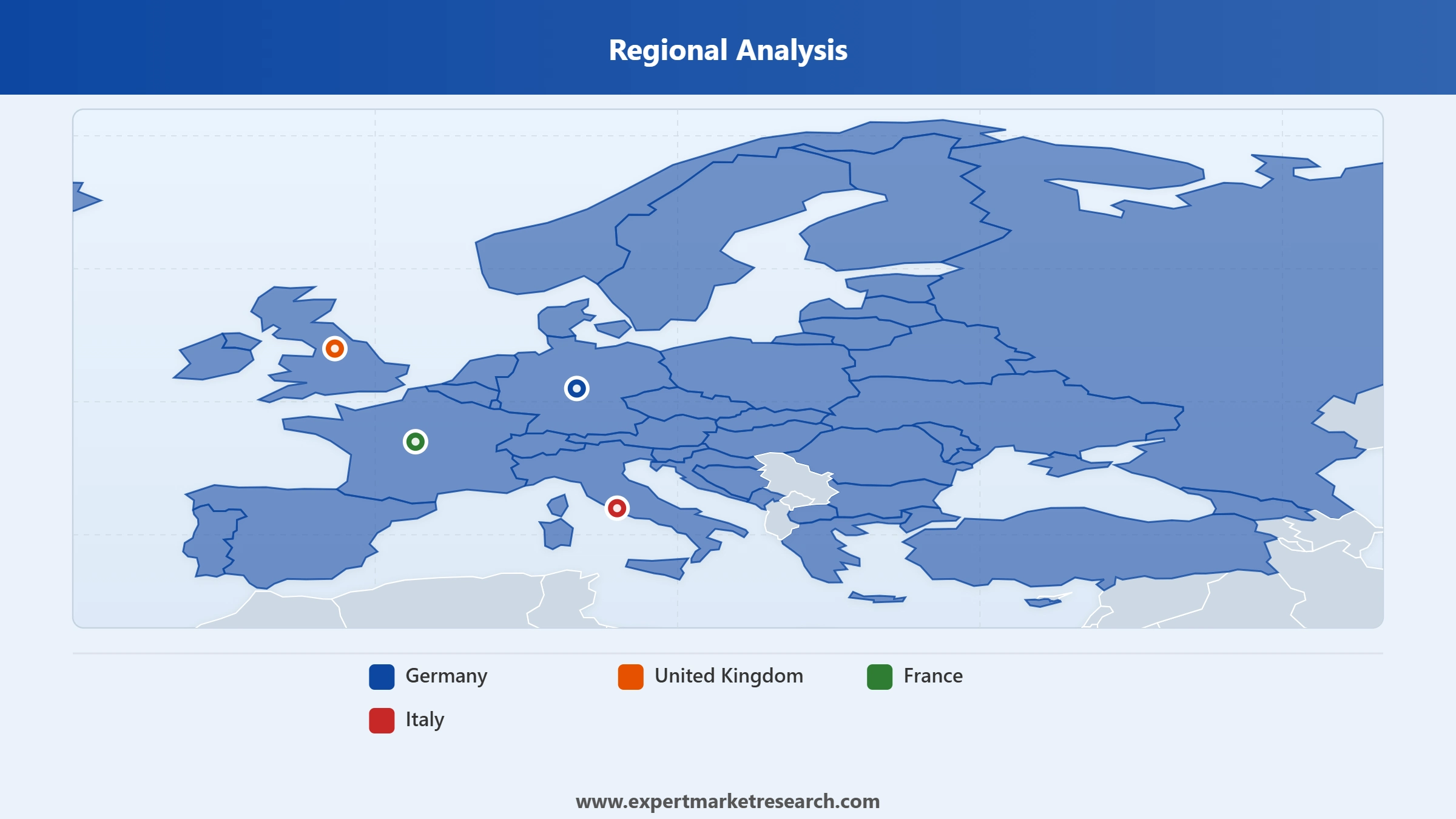

Market Breakup by Region

Key Insight: Germany is the largest national market by construction investment, driven by a federal housing shortage affecting an estimated 700,000 units and sustained public infrastructure spending. The United Kingdom ranks second, anchored by large infrastructure projects including Hinkley Point C and HS2 and NHS hospital renewal. France is a major market through its Grand Paris Express metro expansion and hospital modernisation pipeline. Italy benefits from the Superbonus renovation incentive scheme and public infrastructure investment under the National Recovery and Resilience Plan, reinforcing its position within the Europe construction market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By end use, residential construction dominates the market due to sustained housing shortages and EU renovation mandates

Residential construction holds the largest share of the Europe construction market because demand is structurally underpinned by a growing urban population, an estimated housing deficit of several hundred thousand units in Germany alone, and EU renovation requirements targeting carbon-neutral building stock by 2050. Unlike cyclical commercial or hospitality construction, residential demand is reinforced by policy, demographics, and planning cycles that sustain investment through economic fluctuations.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Healthcare construction represents the next major growth vertical, as governments across Europe allocate capital to replace ageing hospital stock, expand primary care networks, and build resilience into national health infrastructure. In France, the Nantes New CHU Hospital project exemplifies the multi-year procurement cycles supporting healthcare contractors. EU cohesion funds are also directing capital toward healthcare facility upgrades in Eastern and Southern Europe, supporting long-term demand in the Europe construction market.

By residential building type, apartments and flats dominate due to urban land constraints and affordability pressures

Apartments and flats command the largest residential construction share in Europe because urban population density, land cost, and planning regulation in cities across Germany, France, and the Benelux strongly favour multi-family formats. Institutional investors and social housing authorities have also committed capital to large apartment developments, creating a reliable procurement pipeline for contractors specialising in multi-family residential delivery.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Terraced houses and semi-detached units hold significant share in the UK and Ireland, where planning policies promote density-sensitive housing in urban extensions and brownfield regeneration. The UK's focus on affordable housing delivery, supported by Homes England grants and local authority land releases, creates sustained demand for attached residential typologies that sit within reach of first-time buyers across the Europe construction market.

| Sector | Data/Statistic |

| Residential | 1.97M dwellings completed in EU-27 in 2020 (-2.9% from 2019) |

| Residential | 63.8% of EU-27 dwellings completed in 2020 by 5 countries |

| Residential | New dwellings price +5.1% and existing dwellings price +7.3% in EU-27 in 2020 |

| Hospitality | Nights spent in tourist accommodation in EU-27 -52.3% in 2020 |

| Hospitality | Hotel occupancy rate 33.8% and average daily rate EUR 86.75 in Europe in 2020 |

| Hospitality | 212,637 rooms in 1,744 hotel projects in Europe as of Jan 2021 (-7.2% in rooms and -6.3% in projects) |

| Healthcare | Health expenditure EUR 1.13T or 9.9% of GDP in EU-27 in 2019 |

| Healthcare | France, Germany, and Sweden had the highest health expenditure shares of GDP in EU-27 in 2019 (11.3%, 11.2%, and 10.9%) |

| Healthcare | EU-27 average of 36.4 hospital beds per 10K inhabitants in 2019 (6.1 in Cyprus to 82.8 in Germany) |

Germany dominates the market due to the largest housing deficit and sustained public and private infrastructure investment

Germany is the anchor of the Europe construction market, with a housing shortfall estimated at 700,000 units driving persistent residential construction demand. Federal and state governments have introduced programmes to accelerate permitting, reduce construction costs, and deliver affordable housing at scale. Industrial building expansion, transport network renewal, and energy infrastructure investments further reinforce Germany's position as the region's largest construction investment market by value.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The United Kingdom is a structurally important growth market, driven by the Hinkley Point C nuclear power station, ongoing HS2 rail network construction, and a multi-year NHS hospital renewal programme. Balfour Beatty, Skanska, and VINCI are actively engaged in UK public infrastructure. The Planning and Infrastructure Bill signals further reform to accelerate housing delivery, and the government's renewed focus on affordable housing is expected to support steady residential construction growth within the Europe construction market through 2035.

The Europe construction market is highly fragmented, with large multinationals including VINCI, ACS, Skanska, and Bouygues competing for major public and private contracts alongside hundreds of national and regional specialists. Competition is intensifying around sustainability credentials, digital construction capability, and ability to deliver complex projects on schedule and within budget. Public procurement increasingly requires contractors to demonstrate carbon reduction plans, BIM proficiency, and supply chain transparency.

Consolidation through acquisition is a recurring competitive strategy, as major contractors seek to build local market depth, acquire specialist capabilities, and expand geographic reach. VINCI's acquisition of FM Conway in January 2025 is illustrative of how Europe's leading contractors strengthen their positions by absorbing established national and regional players.

French multinational founded in 1899 and headquartered in Rueil-Malmaison. VINCI is Europe's largest construction company by revenue, operating across concessions, construction, and energy segments. With more than 30,000 active projects and presence in over 120 countries, VINCI's construction division covers civil engineering, building, and infrastructure development across all major European markets.

Spanish multinational construction and services conglomerate founded in 1997 and headquartered in Madrid. ACS operates globally through its construction, industrial services, and services divisions. It holds controlling stakes in Hochtief AG and is active across transportation infrastructure, energy infrastructure, and industrial construction in Europe, the Americas, and Asia Pacific.

Swedish construction and project development company founded in 1887 and headquartered in Stockholm. Skanska operates in building construction, civil engineering, and residential and commercial property development. It is active in Sweden, Norway, Finland, the UK, and the US, with a strong focus on green building certification and sustainable infrastructure delivery.

French construction subsidiary of Bouygues S.A., founded in 1952 and headquartered in Paris. Bouygues Construction operates across general building, civil works, and energy and services in more than 90 countries. It is known for complex hospital, residential, and public building projects across Europe, supported by its Swiss subsidiary Losinger Marazzi.

Other key players in the market are Hochtief AG, Eiffage S.A., STRABAG International GmbH, Balfour Beatty plc, Ferrovial S.A., Acciona, S.A., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock a comprehensive view of Europe's construction opportunity with our full market report for 2026. Understand where residential housing, healthcare, and infrastructure investment are concentrating, and which countries and contractors are best positioned to capture the next decade's growth. Whether you are a contractor, investor, developer, or material supplier, this report gives you the intelligence to move first. Download your free sample today and identify the key opportunities across European construction.

United Kingdom Construction Market

North America Construction Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the Europe construction market reached an approximate value of USD 2887.63 Billion.

The market is expected to grow at a CAGR of 4.90% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach USD 4659.04 Billion by 2035.

Construction is any project that starts with a design for a structure at a specific location and ends with assembling all the components to build that structure.

Europe market is being aided by the rising demand for affordable housing, the surging construction of commercial buildings, and the growing infrastructural development activities.

The key trends propelling the market expansion include technological advancements, the development of green energy infrastructure, and the adoption of sustainable construction practices that can reduce emissions.

The major countries in the market in Europe are the United Kingdom, Germany, France, and Italy, among others.

The major end uses of construction in the market are residential, commercial, healthcare, and hospitality, among others.

The significant residential buildings and single units segments in the market include apartments/flats, detached houses, semi-detached, and terraced houses, among others.

Key players in the market are VINCI SA, ACS Group, Skanska AB, Bouygues Construction, Hochtief AG, Eiffage S.A., STRABAG International GmbH, Balfour Beatty plc, Ferrovial S.A., and Acciona, S.A, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by End Use |

|

| Breakup by Residential Buildings and Single Units |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.