Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

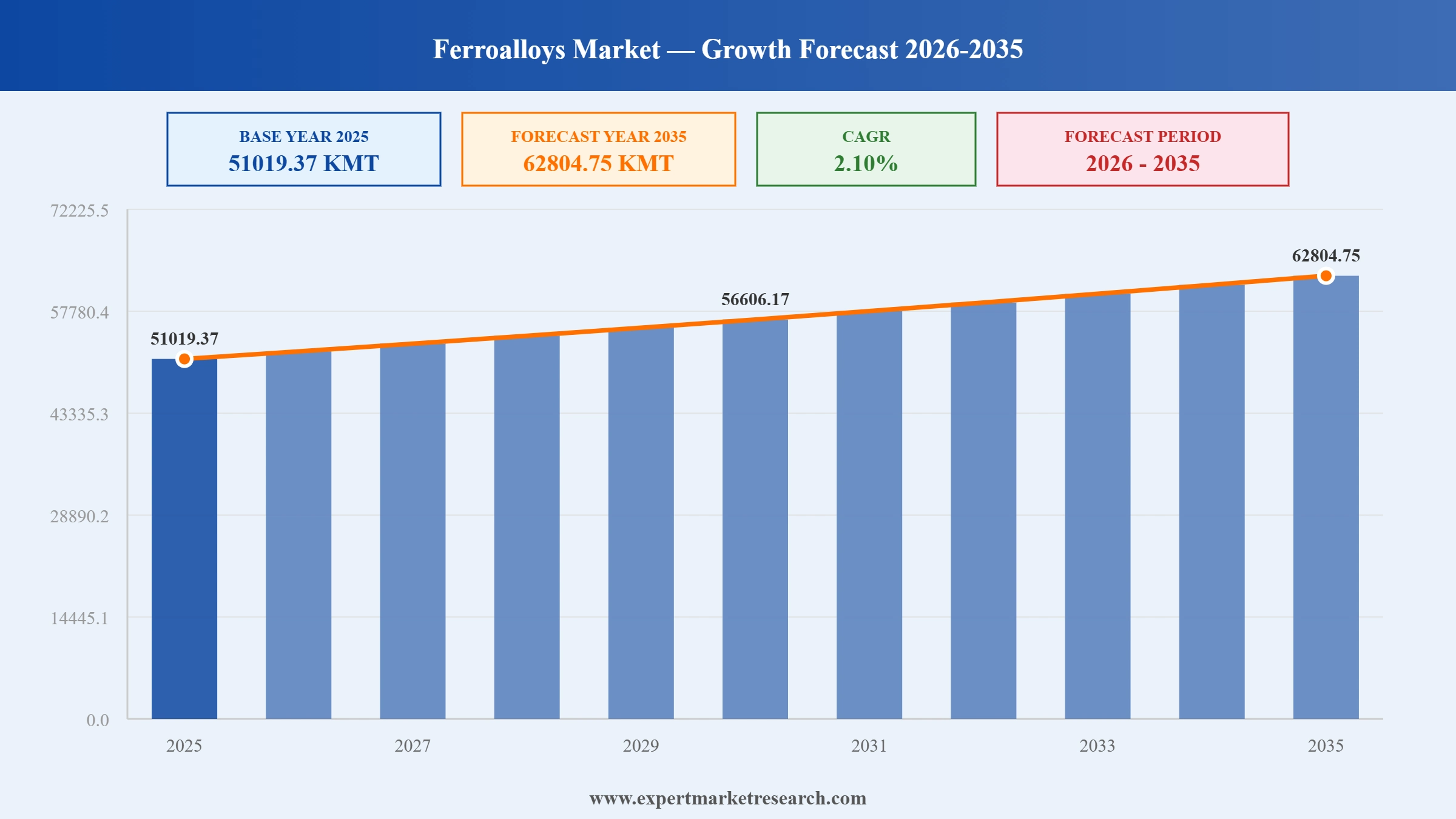

The global ferroalloys market reached a volume of 51019.37 KMT at 2025 and is projected to expand at a CAGR of around 2.10% during the forecast period of 2026-2035. With expanding global steel production sustaining ferroalloy consumption, growing stainless steel demand from construction and automotive sectors, rising superalloy requirements for aerospace and energy applications, and increasing ferrochromium procurement for corrosion-resistant steel, the market is expected to reach 62804.75 KMT by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Global Ferroalloys Market Report Summary | Description | Value |

| Base Year | KMT | 2025 |

| Historical Period | KMT | 2019-2025 |

| Forecast Period | KMT | 2026-2035 |

| Market Size 2025 | KMT | 51019.37 |

| Market Size 2035 | KMT | 62804.75 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 2.10% |

| CAGR 2026-2035 - Market by Region | Latin America | 2.4% |

| CAGR 2026-2035 - Market by Country | Brazil | 2.7% |

| CAGR 2026-2035 - Market by Country | Mexico | 2.3% |

| CAGR 2026-2035 - Market by Product | Ferromanganese | 2.4% |

| CAGR 2026-2035 - Market by Application | Superalloys | 2.5% |

| Market Share by Country | USA | 4.4% |

The global ferroalloys market is experiencing significant ownership consolidation and capacity realignment as major steel and mining conglomerates restructure their ferroalloy portfolios in response to changing production economics. Notable transactions involving Tata Steel, IMFA, and Glencore across India and South Africa reflect broader industry adjustments toward optimising geographic production footprints and concentrating operations in cost-competitive regions with abundant raw material access.

Indian Metals and Ferro Alloys (IMFA) completed the acquisition of Tata Steel's ferrochrome plant at Jajpur, Odisha, completing the Rs 610 crore acquisition agreement. The transaction transferred a significant ferrochromium production capacity to IMFA, strengthening its position as a leading ferrochrome producer in India and expanding its total production base within the global ferroalloys market.

Tata Steel presented a comprehensive capacity expansion strategy for its India business, including plans to scale its state-of-the-art facility from 3 million tonnes per annum to 8 million tonnes per annum. This broad-based steel expansion blueprint directly underpins demand for ferroalloy inputs including silicomanganese and ferrochromium, signalling sustained procurement growth from one of the global ferroalloys market's largest integrated steel producers.

IMFA announced a definitive agreement to acquire Tata Steel's Ferro Alloy Plant at Jajpur, Odisha for a base consideration of Rs 610 crore. This strategic acquisition enables IMFA to consolidate ferrochromium production capacity in Odisha, a state with rich chrome ore reserves, positioning the company for expanded output and improved cost efficiency within the global ferroalloys market.

Glencore revealed strategic plans to expand its ferroalloy production capacity in South Africa, targeting increased output of ferrochromium and manganese alloys to serve growing demand from ASIA PACIFIC steel markets. The expansion reflects Glencore's strategy to optimise its geographic production footprint by leveraging South Africa's abundant chrome and manganese ore deposits within the global ferroalloys market.

Global steel production, a primary driver of ferroalloy consumption, continues to grow as construction, automotive, and infrastructure sectors expand in emerging economies. Over 80% of ferroalloys are consumed in steelmaking, creating a structural demand link between global construction activity, vehicle manufacturing output, and ferroalloy procurement volumes across the global ferroalloys market.

Rising demand for stainless steel in construction, consumer appliances, medical equipment, and food processing is driving increased consumption of ferrochromium and ferronickel, the primary alloying elements for stainless grades. The construction sector alone accounts for approximately 50% of total steel consumption globally, creating sustained structural demand for multiple ferroalloy products within the global ferroalloys market.

The aerospace industry's demand for nickel-based superalloys, which rely on ferronickel and other speciality ferroalloy inputs, is growing steadily with aircraft production recovery and next-generation engine development. Growing energy sector investment in gas turbines and industrial equipment further supports premium superalloy procurement, contributing to the higher-value end of the global ferroalloys market.

Steel producers' increasing adoption of electric arc furnace and hydrogen-based steelmaking technologies is gradually shifting the mix of ferroalloy inputs required, favouring high-purity grades and specific alloy compositions compatible with alternative steelmaking routes. This transition creates both challenges and opportunities for ferroalloy producers to develop product specifications aligned with low-carbon steel production within the global ferroalloys market.

Government-led infrastructure investment programmes across India, China, and the Middle East are sustaining steel consumption growth and, by extension, ferroalloy procurement volumes. India's National Infrastructure Pipeline and China's urban infrastructure renewal programmes represent the largest structural demand anchors for ferroalloy producers serving the steel industry within the global ferroalloys market through 2035.

The report of the Expert Market Research's titled "Global Ferroalloys Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

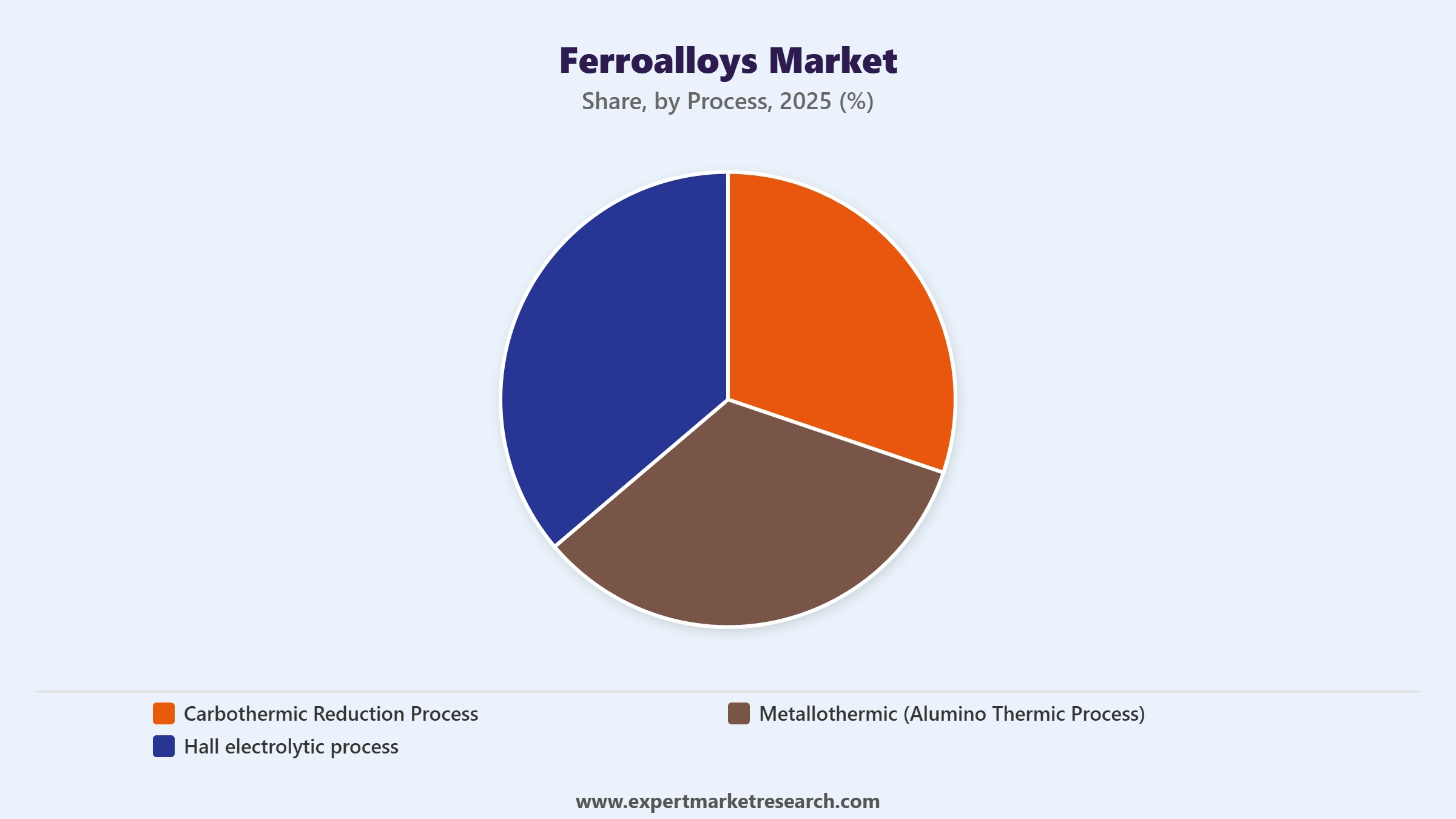

Market Breakup by Process

Key Insight: Carbothermic reduction dominates the global ferroalloys market by process, accounting for over 80% of total ferroalloy production due to its energy efficiency, scalability, and suitability for bulk ferroalloy grades including ferrochromium, silicomanganese, and ferromanganese. Metallothermic processes serve speciality applications requiring high-purity outputs. The Hall electrolytic process is used for specific ferroalloy grades requiring precise control over impurity levels and product composition in speciality steel and superalloy manufacturing.

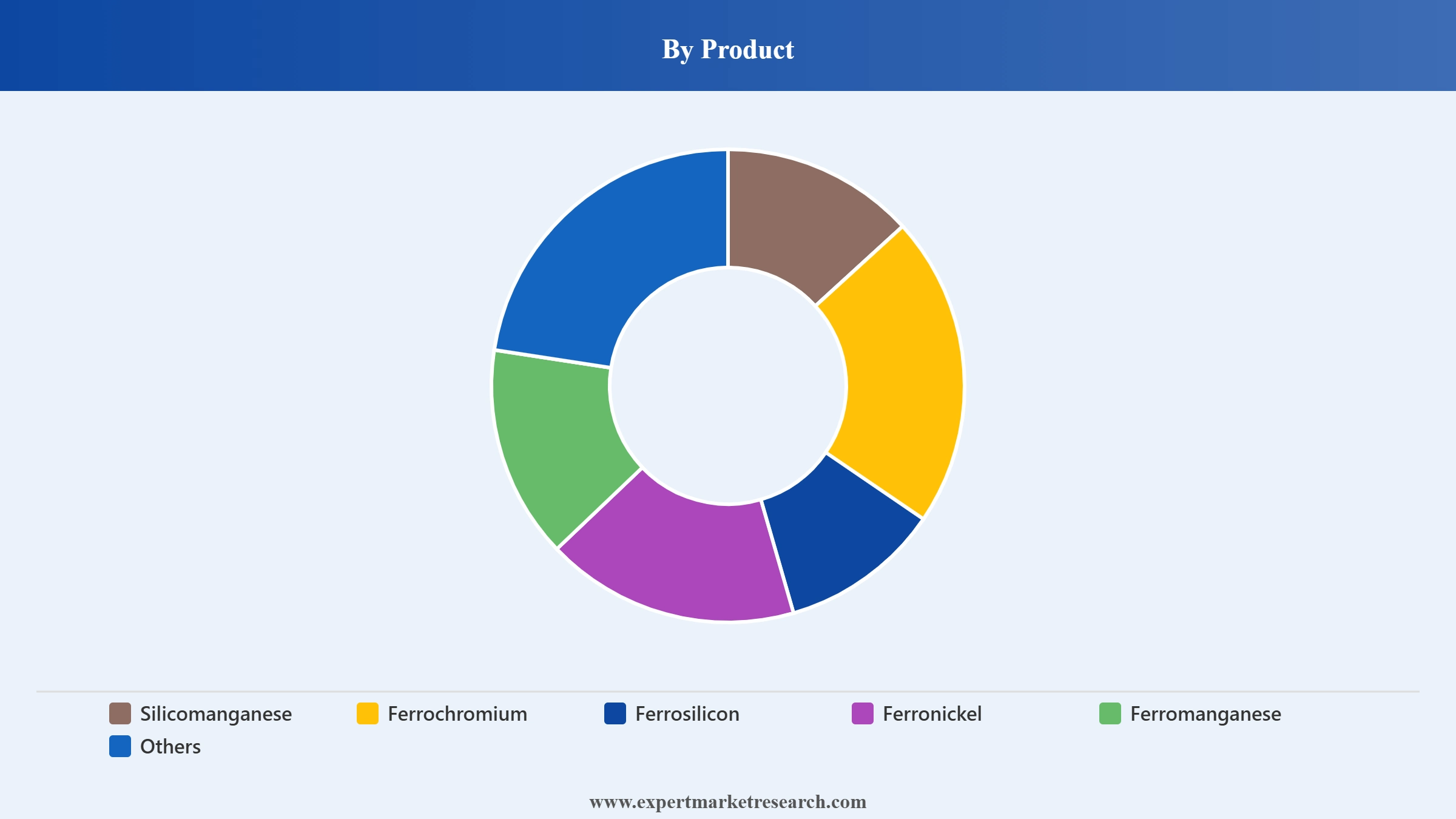

Market Breakup by Product

Key Insight: Ferrochromium and silicomanganese are the two largest volume products in the global ferroalloys market, collectively serving the stainless steel and carbon steel segments which account for over 80% of total ferroalloy consumption. Ferrosilicon serves both steel deoxidation and cast iron applications. Ferronickel is the primary nickel source for austenitic stainless steel production. Ferromanganese is a fundamental deoxidiser and sulphur control agent used across most steel grades globally.

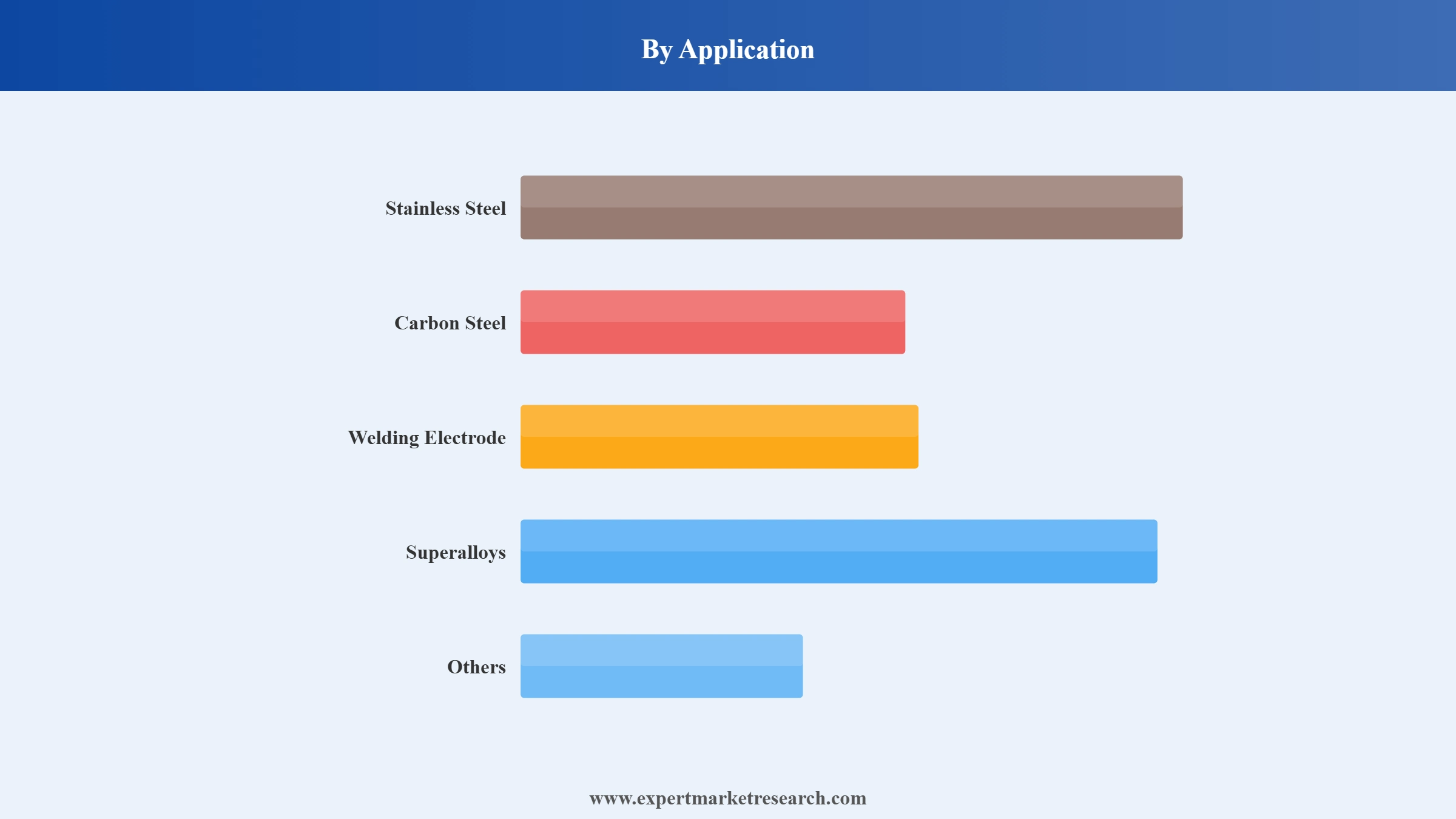

Market Breakup by Application

Key Insight: Stainless steel is the dominant application for the global ferroalloys market, consuming primarily ferrochromium and ferronickel as essential alloying elements that provide corrosion resistance and heat resistance. Carbon steel is the largest volume application overall, consuming silicomanganese and ferrosilicon as deoxidisers and strength enhancers. Superalloys represent a smaller but high-value application segment, requiring specialised ferroalloy grades for aerospace, power generation, and advanced manufacturing.

Market Breakup by Region

Key Insight: ASIA PACIFIC accounts for the dominant share of the global ferroalloys market, led by China's position as the world's largest steel producer and India's rapidly growing steel industry. China produced approximately 36,000 thousand tonnes of ferroalloys in 2020, reflecting its central role in global supply. MIDDLE EAST AND AFRICA is an important production hub particularly for ferrochromium from South Africa and manganese alloys from various producers serving global markets.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Process, carbothermic reduction accounts for the dominant share of the market due to its scalability and energy efficiency in producing the most widely consumed bulk ferroalloy grades.

Carbothermic reduction dominates global ferroalloy production, processing ores with carbon reductants in electric arc furnaces to produce the key bulk ferroalloy grades that steel mills consume at large scale. This process accounts for over 80% of total ferroalloy output and serves as the primary production route for ferrochromium at Glencore's South African operations and IMFA's expanded Odisha facilities. The process' economic scale advantages and compatibility with most commercially available ore grades ensure its continued dominance in the global ferroalloys market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Metallothermic processes serve specialised segments requiring higher purity outputs than carbothermic reduction can efficiently achieve, including specific ferroalloy grades for superalloy manufacturing and high-specification stainless steel production. The Hall electrolytic process addresses precision applications where trace impurity control is critical. DS Alloyd Pvt. Ltd. and LekonGermess Ltd serve niche segments where product purity specifications exceed what conventional carbothermic processes can deliver at commercially viable costs within the global ferroalloys market.

By Product, ferrochromium accounts for the dominant share of the market due to its essential role as the primary chromium source for stainless steel manufacturing globally.

Ferrochromium is the single largest ferroalloy product by value in the global ferroalloys market, driven by its indispensable role in stainless steel production where a minimum of approximately 10.5% chromium content is required by definition. South Africa, Kazakhstan, and India are the leading ferrochromium producing nations. IMFA's acquisition of Tata Steel's Jajpur plant strengthens India's domestic ferrochromium capacity, while Glencore's South Africa expansion plans reflect the strategic importance of this product globally.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Silicomanganese represents the second largest product in the global ferroalloys market, valued for its role as both a manganese and silicon source in carbon and alloy steel production. Global ferrochrome production exceeded 13 million metric tonnes in 2023, with China and South Africa contributing over 70% of supply. Ferromanganese production reached 6.2 million metric tonnes in 2023, while ferrosilicon output stood at approximately 7.5 million metric tonnes, representing over 18% of total ferroalloy market volume.

By Application, stainless steel accounts for the dominant share of the market due to the high ferrochromium and ferronickel content required in all stainless steel grades.

Stainless steel is the highest-value application in the global ferroalloys market, requiring substantial quantities of ferrochromium (10.5-30%), ferronickel, and ferromanganese per tonne of finished product. Growing demand for stainless steel in food processing equipment, medical devices, construction facades, and automotive exhaust systems is driving consistent procurement growth. Tata Steel Limited supplies premium steel grades incorporating specialised ferroalloy inputs to multiple industrial sectors globally, reflecting the application's commercial significance.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Carbon steel is the largest volume application in the global ferroalloys market, consuming silicomanganese and ferrosilicon as primary deoxidisers and strengthening agents in structural and engineering steel production. The construction sector accounts for approximately 50% of total steel consumption globally, making carbon steel ferroalloy demand highly responsive to infrastructure investment cycles. Ferro Alloys Corporation Limited and Essel Mining and Industries Limited serve the domestic Indian carbon steel market with silicomanganese and ferrosilicon supply.

ASIA PACIFIC dominates the global ferroalloys market due to the region's position as the world's largest steel producer and the scale of its industrial and infrastructure investment.

ASIA PACIFIC commands the dominant share of the global ferroalloys market, anchored by China's steel industry producing approximately 1 billion tonnes annually and India's rapidly expanding steel capacity. The construction sector in Asia Pacific accounts for approximately 50% of total steel consumption, creating structural demand for silicomanganese, ferrosilicon, and ferrochromium. Tata Steel Limited, DS Alloyd Pvt. Ltd., and Ferro Alloys Corporation Limited are among the significant ferroalloy producers serving the Indian market's growing steel output.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Middle East and Africa is a strategically important production hub for the global ferroalloys market, particularly for ferrochromium and manganese alloys. South Africa's abundant chrome ore reserves make it the world's leading ferrochromium exporter, with Glencore's expanded production plans reinforcing the region's long-term supply significance. EUROPE also maintains important ferroalloy production capacity particularly in Russia and Poland, serving regional steel mills with ferrochromium and ferrosilicon while managing energy cost pressures affecting electric arc furnace operations.

The global ferroalloys market is moderately concentrated at the large-scale production end, with vertically integrated mining and metallurgical companies including Glencore Plc. and Tata Steel Limited commanding significant market positions through resource ownership and production scale. The Indian market features a cluster of domestically focused producers including IMFA, Ferro Alloys Corporation Limited, and Essel Mining and Industries Limited serving the growing domestic steel industry, while speciality producers like AMG Vanadium LLC and Metraco NV serve specific niche alloy segments.

Founded in 1907 and headquartered in Mumbai, India, Tata Steel Limited is one of the world's most geographically diversified steel producers, with operations in India, Europe, and other markets. The company's Ferro Alloys and Minerals Division has historically been a significant ferrochromium producer in Odisha, India. In November 2025, Tata Steel announced the sale of its Ferro Alloy Plant at Jajpur for Rs 610 crore to IMFA, reflecting a strategic portfolio rationalisation within the global ferroalloys market.

AMG Vanadium LLC is a United States-based producer of ferrovanadium and specialty alloys, operating within the AMG Advanced Metallurgical Group. The company produces ferrovanadium for high-strength low-alloy steel applications, serving steel mills, aerospace alloy producers, and specialty chemical manufacturers. AMG Vanadium leverages spent catalyst recycling and primary vanadium extraction to supply a specialised but high-value product segment within the global ferroalloys market, particularly in the North American and European regions.

Metraco NV is a Belgian-based ferroalloy trading and distribution company specialising in the procurement and supply of ferrochromium, silicomanganese, ferrosilicon, and other ferroalloy grades to European steel producers and specialty metal users. The company serves as an intermediary in the global ferroalloys market, sourcing material from major producing countries including South Africa, China, and India, and supplying European customers seeking reliable supply chain management and logistics services for ferroalloy raw materials.

DS Alloyd Pvt. Ltd. is an Indian ferroalloy producer and trader engaged in the manufacture and supply of ferrosilicon, silicomanganese, and other ferroalloy products to the domestic steel industry. The company serves Indian steel mills requiring consistent ferroalloy supply for deoxidation and alloying processes in carbon and alloy steel production. DS Alloyd operates within the rapidly growing Indian ferroalloys segment of the global ferroalloys market, benefiting from proximity to domestic steel producers and growing local demand.

Other key players in the market are LekonGermess Ltd., Glencore Plc., Ferro Alloys Corporation Limited, Essel Mining and Industries Limited, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Gain in-depth intelligence on the global ferroalloys industry from 2026 with our comprehensive market report. Explore product demand dynamics, regional production shifts, competitive strategies, and application sector growth trends shaping the market. Whether you are a ferroalloy producer, steel mill procurement manager, or resource investor, this report provides the clarity you need. Download your free sample today and discover the key opportunities in the thriving global ferroalloys industry through 2035.

High Performance Alloys Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market attained a volume of 51019.37 KMT in 2025.

The market is estimated to grow at a CAGR of 2.10% during 2026-2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach a volume of 62804.75 KMT by 2035.

The major drivers of the market include the availability of iron ore in abundance and the various advantages offered by ferroalloys.

The expansion of the construction sector, increasing demand for steel, and the growing demand from end-use sectors are the key trends propelling the growth of the market.

The key regional markets for ferroalloys are North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa.

The key applications of the product are stainless steel, carbon steel, welding electrode, superalloys, others.

The key players in the market include Tata Steel Limited, AMG Vanadium LLC, Metraco NV, DS Alloyd Pvt. Ltd., LekonGermess Ltd., Glencore Plc., Ferro Alloys Corporation Limited, and Essel Mining & Industries Limited, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Process |

|

| Breakup by Product |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.