Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

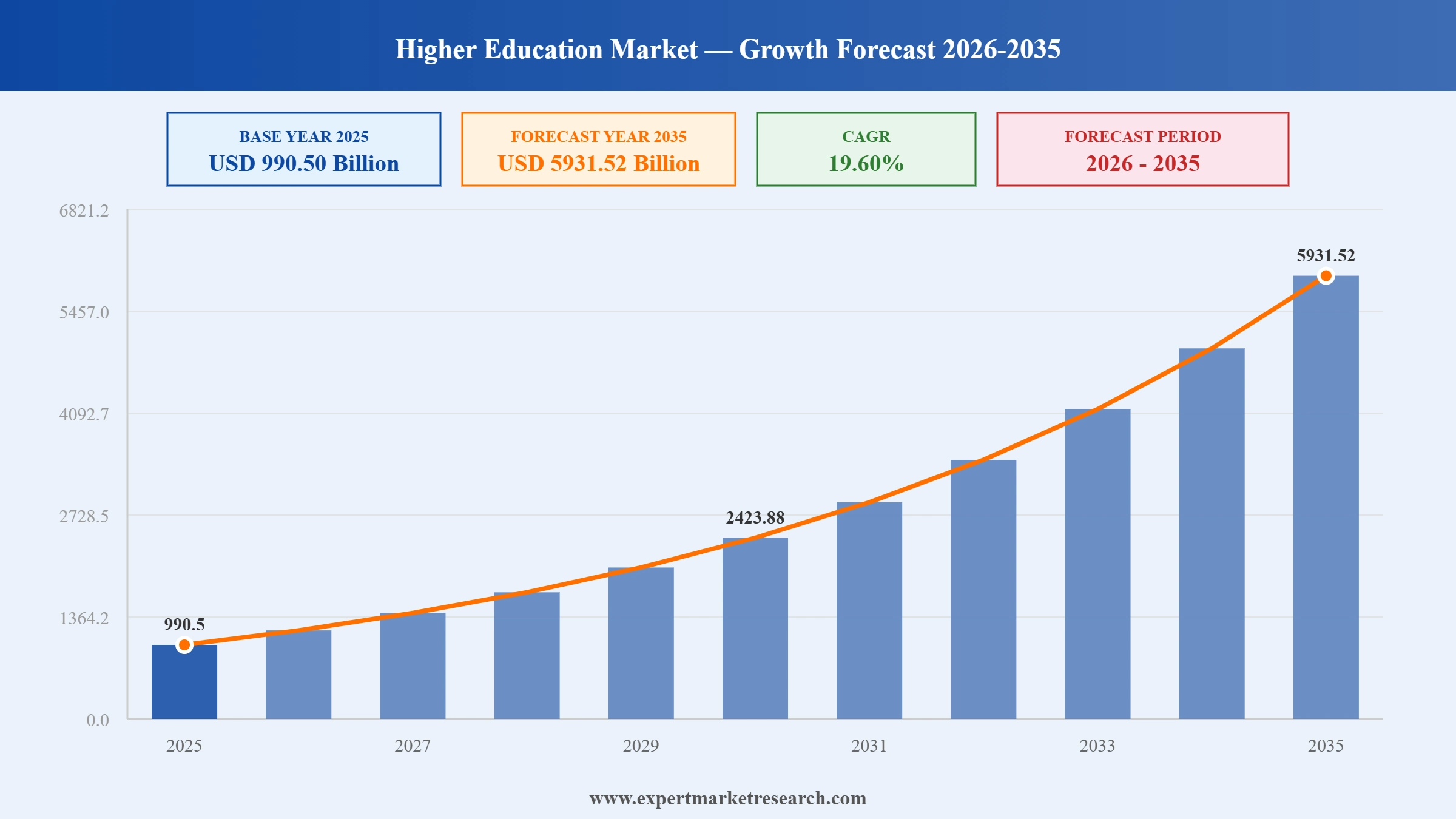

The global higher education market attained a value of USD 990.50 Billion at 2025 and is forecast to grow at a CAGR of around 19.60% from 2026-2035, reaching approximately USD 5931.52 Billion by 2035. This market encompasses all post-secondary education services, encompassing brick-and-mortar universities, private colleges, community colleges, vocational training institutions, and the rapidly expanding universe of online learning platforms and degree-granting digital academies.

The sector's scale reflects the global imperative for tertiary-level credentials. According to the UNESCO Institute for Statistics, over 235 million students are enrolled in post-secondary institutions worldwide, a figure that continues to expand as developing nations scale higher education access and developed economies intensify upskilling and reskilling initiatives. Revenue is generated across four primary channels: tuition and fee income, government grants and contracts, institutional investment returns, and private endowment income with tuition fees accounting for more than 37% of total market revenue.

From a product architecture perspective, the market includes learning management systems (LMS), student information systems (SIS), campus management platforms, online course delivery infrastructure, and the AI-driven analytics and adaptive learning tools that are increasingly central to modern academic operations. The convergence of these components positions higher education as not just an educational sector, but as a major vertical for enterprise technology investment.

The global higher education market is at an inflection point. The confluence of demographic expansion in emerging markets, digital transformation imperatives, and post-pandemic re-evaluation of learning modalities has produced a structural growth environment unlike any in recent history.

Key market metrics and strategic highlights include:

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Rising Global Enrolment Rates: Post-secondary enrolment continues to grow globally, with the UNESCO Institute for Statistics projecting enrolment surpassing 265 million students by 2030. This growth is particularly pronounced in Sub-Saharan Africa, South Asia, and Southeast Asia, where expanding youth populations and improving secondary completion rates are feeding enrolment pipelines for higher education institutions.

Adoption of Artificial Intelligence and EdTech: The integration of AI across the higher education value chain from admissions processing and personalised learning path generation to administrative automation and predictive analytics is fundamentally altering both institutional cost structures and learner outcomes. AI-powered tutoring systems, adaptive content delivery, and intelligent student support tools are enabling institutions to serve more students at lower marginal cost.

Demand for Digital and Hybrid Learning: Accelerated by the structural changes of the pandemic era, learner preference for flexible, online, and hybrid delivery formats has created a lasting demand shift. Institutions that have invested in robust online infrastructure are capturing enrolment from geographies and demographics previously excluded from campus-based programmes.

Workforce Upskilling and Reskilling Imperatives: The rapid pace of technological change, particularly the impact of generative AI on labour markets, is driving organisations and individuals to invest heavily in continuing education, professional certifications, and advanced degree programmes. This corporate and individual demand for upskilling is expanding the addressable market for higher education institutions.

Government Investment and Policy Support: Public sector investment in higher education remains a powerful growth catalyst. Nations across Asia Pacific, the Middle East, and Africa are directing significant budgetary resources to expanding university capacity and accessibility. India's National Education Policy, China's education infrastructure programmes, and Gulf Cooperation Council countries' education megaprojects are representative of this global trend.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Technology-Driven Transformation of Academic Delivery: The most powerful structural driver of higher education market growth is the deepening integration of advanced technology into academic delivery. Learning management systems have evolved from simple content repositories into sophisticated, data-driven environments capable of tracking individual learner engagement, diagnosing knowledge gaps in real time, and adapting content difficulty and format to optimise retention. Platforms such as Canvas by Instructure, Blackboard by Anthology, and D2L's Brightspace are widely deployed across thousands of institutions globally, creating a technology substrate that enables continuous improvement of teaching quality at scale.

Artificial intelligence amplifies these capabilities substantially: AI-driven tutoring systems, natural language processing for written feedback, automated grading tools, and predictive analytics for student retention enable institutions to address at-risk students proactively. The Center for Democracy and Technology's October 2025 report found that 85% of teachers and 86% of students used AI tools in the preceding academic year a remarkable diffusion signalling a permanent shift in how higher education is delivered.

Rising Demand for Skilled Professionals: Global labour markets are experiencing sustained shortages of professionals in high-value disciplines including data science, artificial intelligence, cybersecurity, biotechnology, and financial engineering. Employers are actively partnering with universities to design curriculum aligned to market needs, and many are funding employee enrolment in higher education programmes directly. This employer-education nexus is creating a dual demand stimulus: institutional enrolment growth driven by individual career aspirations, and corporate-funded educational investment driven by workforce capability gaps.

Expanding Global Middle Class: Rising household incomes across Asia, Africa, and Latin America are enabling a growing proportion of families to invest in higher education. The IMF projects that the global middle class will expand to 5.3 billion people by 2030, with the majority of this growth concentrated in emerging markets precisely the geographies where higher education attainment rates remain below the global average.

High Cost of Education and Student Debt Burden: Despite the sector's growth trajectory, the escalating cost of higher education particularly in North America and Western Europe represents a significant structural restraint. In the United States, total outstanding student loan debt has surpassed USD 1.7 trillion, creating a financial overhang that affects graduate consumption patterns and broader economic productivity.

Digital Divide and Infrastructure Inequality: The rapid shift toward online and hybrid learning models has exposed deep inequalities in digital infrastructure access. In many emerging markets, unreliable internet connectivity, limited device penetration, and inadequate digital literacy among both students and faculty constrain the pace at which online higher education can scale.

Regulatory and Accreditation Complexity: The global higher education market operates within a complex web of national accreditation frameworks, licensing requirements, and quality assurance standards that vary significantly across jurisdictions. Cross-border programme delivery, credit transfer agreements, and the recognition of online credentials by employers remain inconsistent globally.

Online and Distance Learning Expansion: The increasing acceptance of online degrees by employers, professional certification bodies, and government agencies has substantially expanded the addressable market for digital higher education. Institutions that invest in high-quality online programme delivery can access learner populations in geographies where campus-based expansion would be cost-prohibitive. Coursera, with approximately 197 million registered learners as of December 2025, demonstrates the commercial viability of this approach at global scale.

Lifelong Learning and Professional Development: The half-life of professional skills is contracting rapidly in the AI era, creating a sustained and growing demand for lifelong learning beyond the traditional 18-22 age cohort. Micro-credential programmes, executive education, and modular certificate courses tailored to working professionals offer institutions significant revenue diversification opportunities.

Emerging Markets Growth: Markets in Sub-Saharan Africa, South and Southeast Asia, and Latin America represent the most substantial long-term growth opportunity in the global higher education landscape. Large youth populations, rising secondary school completion rates, and government commitments to expanding tertiary education access are creating conditions for rapid market development.

AI-Enabled Personalised Learning: Adaptive learning platforms that tailor content, pacing, and assessment to individual learner profiles have demonstrated measurable improvements in learning outcomes and completion rates. The commercial value of demonstrably superior outcomes is a powerful differentiator for institutions competing for enrolment, and for EdTech companies developing B2B solutions for the institutional market.

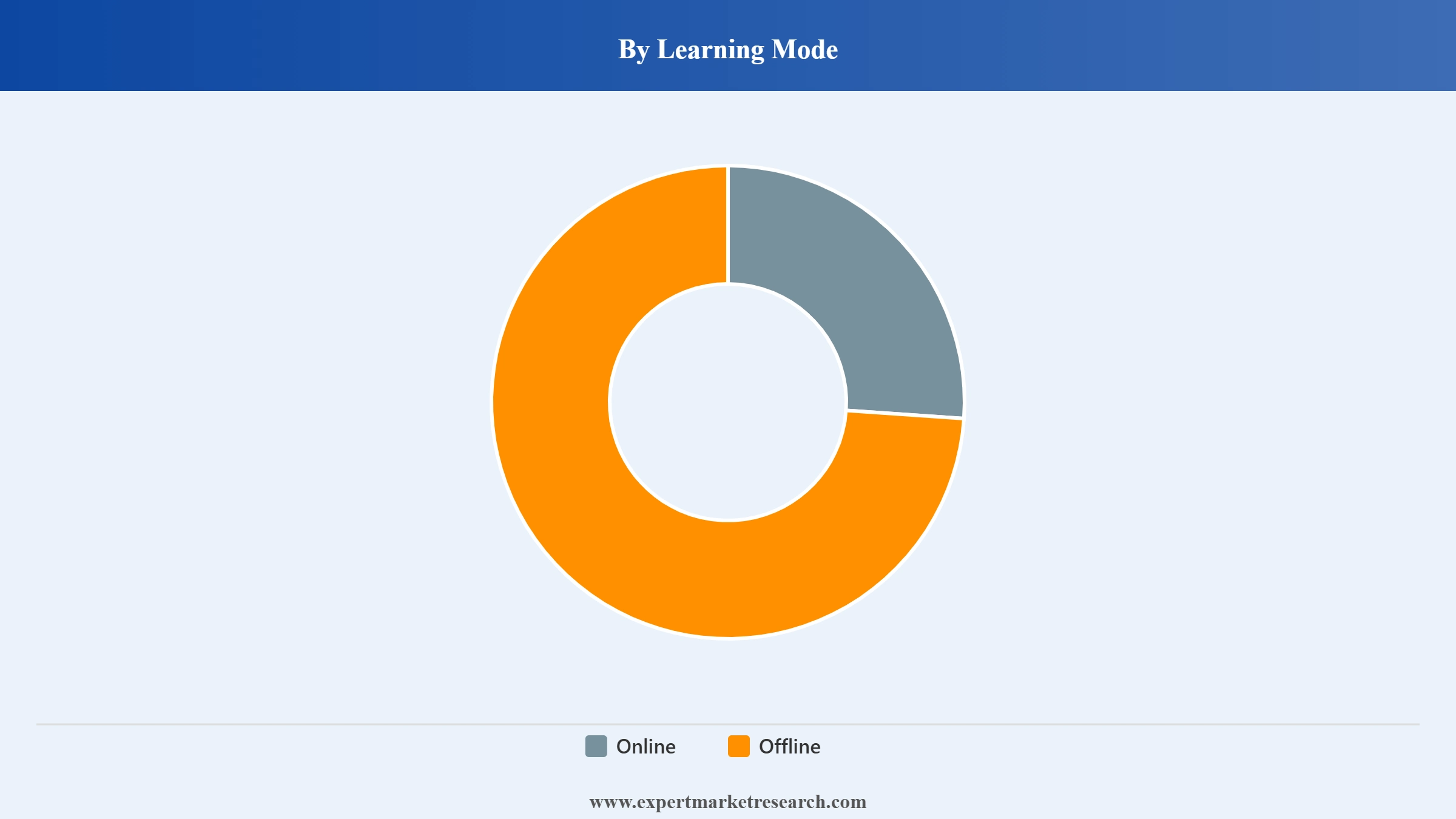

Offline (On-Campus) Learning: The offline segment retains the largest share of total market revenue at more than 71% in 2025, reflecting the continued dominance of campus-based instruction across most geographies. The on-campus experience continues to command a premium, particularly at research-intensive universities and institutions with strong brand equity.

Online Learning: Despite holding a smaller revenue share, the online learning segment is expanding at the fastest CAGR within the higher education market. Fully accredited online degree programmes now span the full spectrum from associate degrees to doctoral qualifications, and the gap in perceived credential value between online and campus-based degrees is narrowing progressively.

Hybrid Learning: The hybrid or blended learning model is gaining traction as institutions seek to balance the flexibility advantages of online delivery with the engagement and retention benefits of face-to-face learning. This modality is particularly valued by working professional students who require scheduling flexibility without forgoing the benefit of campus interaction.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

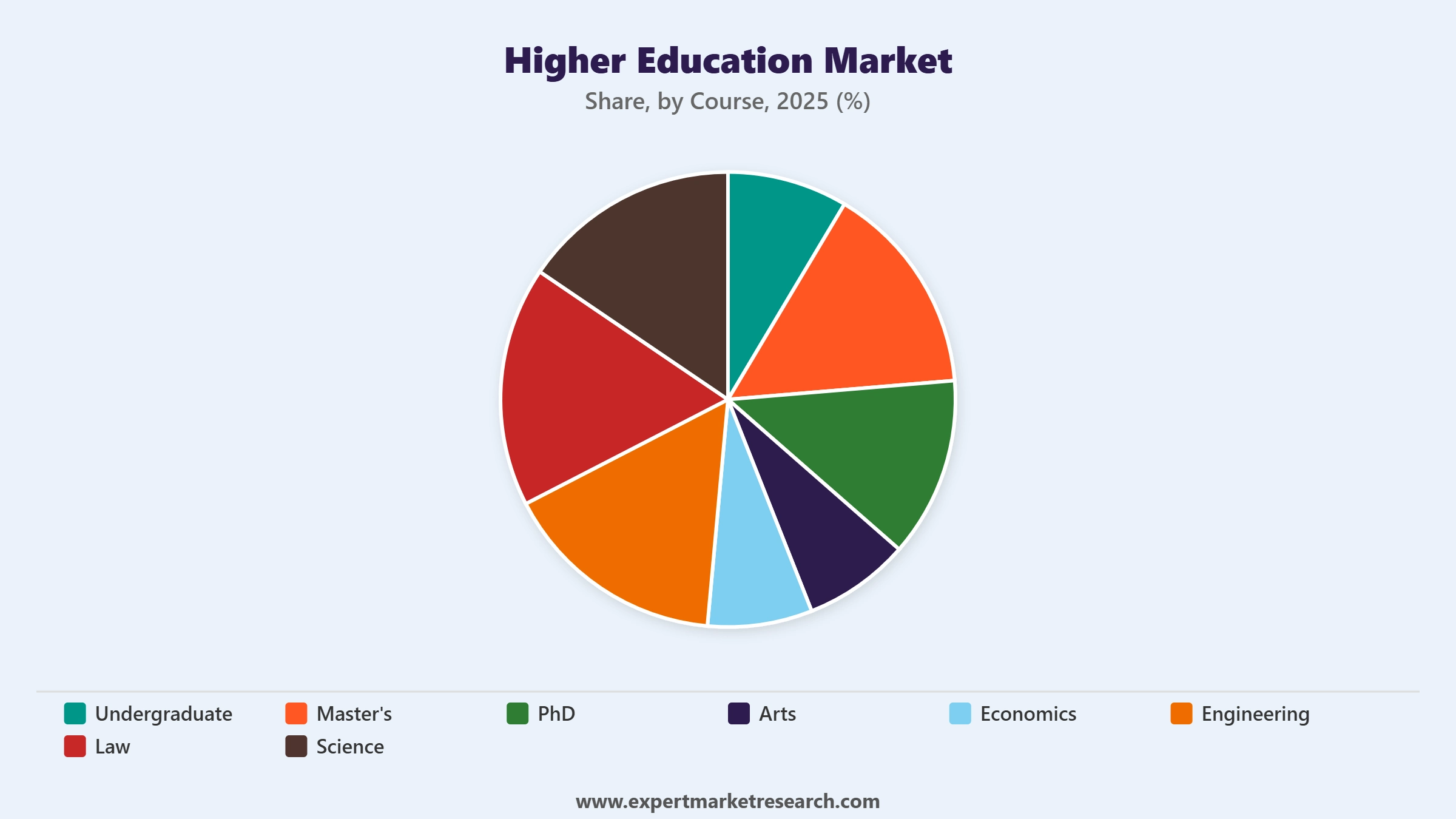

Undergraduate Programmes: The undergraduate segment accounts for more than 80% of total enrolment volume in 2025. Growth in this segment is closely correlated with secondary school completion rates, national enrolment targets, and the affordability of tertiary education.

Master's Degree Programmes: The master's segment is the fastest-growing course category, with a CAGR materially above the overall market average. This reflects employer demands for advanced degrees, the growth of employer-sponsored tuition assistance, and the expansion of professional master's degrees in technology, business, and healthcare.

PhD and Doctoral Programmes: The doctoral segment is strategically significant due to its research output and its role in generating the human capital pipeline for both academic institutions and the innovation economy. Governments and corporations are investing in doctoral training in priority research areas including life sciences, clean energy, and AI.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

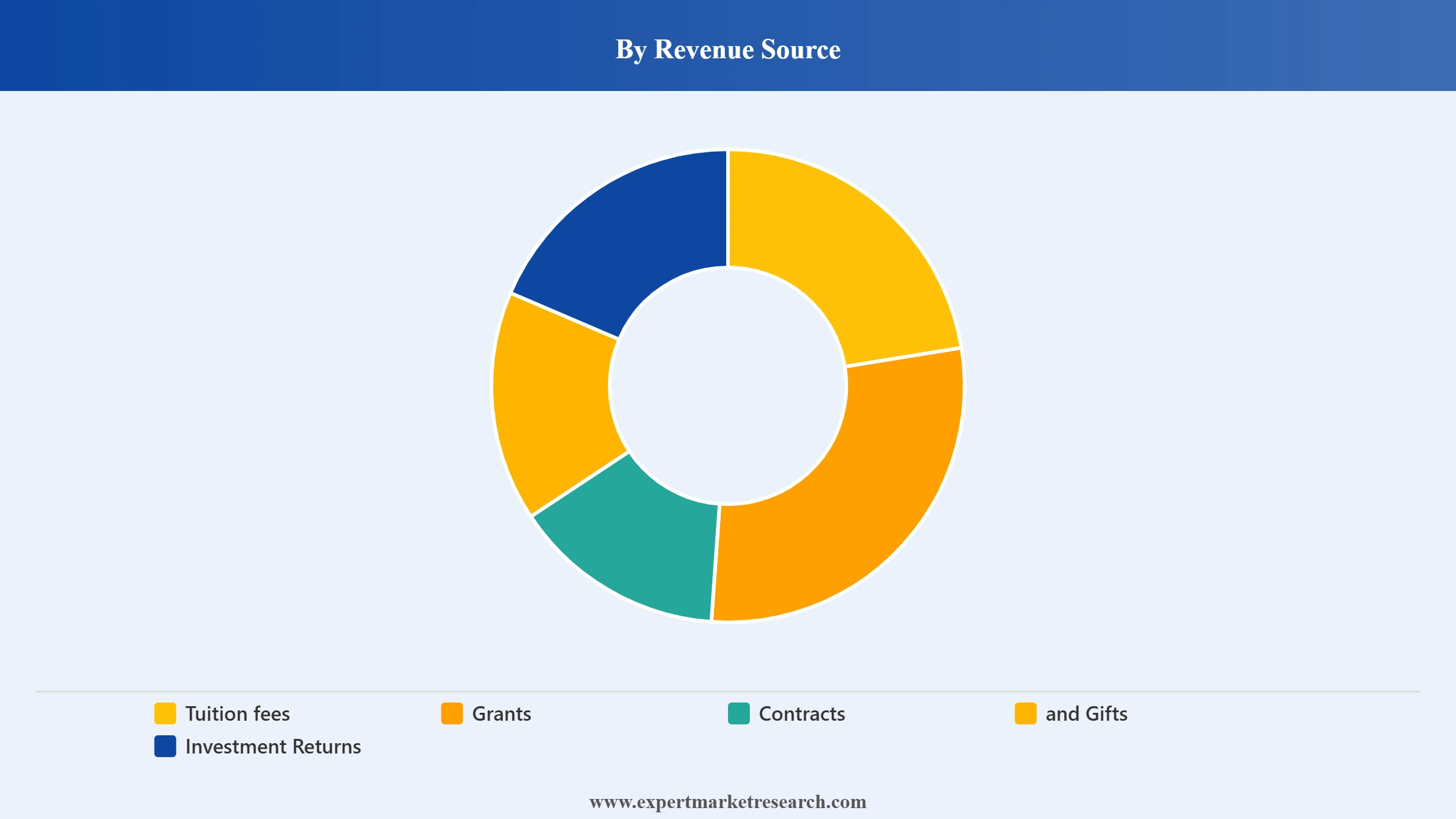

Tuition and Fees: Tuition income is the dominant revenue source, representing more than 37% of total market revenue. The expansion of online programmes is enabling institutions to serve more students without proportional increases in campus infrastructure.

Grants, Contracts, and Research Funding: Government grants and research contracts represent the second-largest revenue source, particularly for public research universities. Areas such as quantum computing, AI safety, and climate technology are currently receiving elevated funding.

Investment Returns: Many leading universities derive significant revenue from endowment investment returns. The largest endowments at Harvard, Yale, Stanford, and MIT provide multi-billion-dollar annual income streams that fund financial aid, research, and faculty recruitment.

Other Revenue: Ancillary revenue sources including conference facilities, executive education, IP licensing, and international partnership fees are growing in strategic importance as institutions diversify away from tuition and government funding dependence.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America is the leading region in the global higher education market by revenue and institutional prestige, anchored by the United States' world-class research universities including Harvard, MIT, Stanford, and Princeton, whose global brand equity attracts international students paying premium tuition. The region's strong private college sector, employer-driven curriculum partnerships, and well-developed EdTech infrastructure supporting online delivery make it the highest-value regional market in terms of per-student revenue generation.

Asia Pacific is the fastest-growing regional market, driven by China's ongoing investment in university capacity, India's large and expanding student-age population, and South Korea and ASEAN governments' digitisation of higher education infrastructure. In June 2025, Coursera reported 20 million new learners in 2024 with content available in 24 additional languages, confirming Asia Pacific's role as the primary engine of global higher education market growth, particularly in online and mobile-first learning modalities.

Europe's higher education market is characterised by the quality and international reputation of its university systems, particularly in the UK, Germany, France, the Netherlands, and the Nordic countries. The EU's Digital Education Action Plan and the Erasmus+ programme are accelerating digital transformation and cross-border academic collaboration.

The Gulf Cooperation Council (GCC) states are directing substantial sovereign wealth investment into education infrastructure under Vision 2030 national development plans. Africa represents the highest long-term growth potential, driven by a large and rapidly growing youth population and improving mobile internet infrastructure enabling affordable online higher education.

Latin America's higher education market is expanding through improved secondary school completion rates, growing middle-class demand for tertiary credentials, and active government investment. Brazil, Mexico, Colombia, and Argentina are the region's largest markets, with strong adoption of MOOC and online learning platforms.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

May 2026 - Coursera formally completed its combination with Udemy following stockholder approval on April 9, 2026. Former Coursera stockholders own approximately 59% and former Udemy stockholders approximately 41% of the combined company on a fully diluted basis. The combined platform positions itself as the world's most comprehensive skills and online learning destination, serving learners across 230+ countries and territories with AI-powered personalised learning at its core.

May 2026 - UNESCO published its first Higher Education Global Trends Report, delivering the most comprehensive global analysis of tertiary education ever produced. The report confirms that higher education enrolment reached 269 million students in 2024 more than double the 100 million enrolled in 2000 while international student mobility tripled to nearly 7 million. The report highlights persistent geographic inequalities, with Sub-Saharan Africa recording a gross enrolment ratio of just 9% against a global average of 43%, and identifies AI policy, quality assurance reform, and inclusive financing models as the highest-priority areas for action by member states.

April 2026 - The University of New Haven received formal approval from the New England Commission of Higher Education (NECHE) to establish its international branch campus in Riyadh, Saudi Arabia the same accreditation standard applied to its domestic US programmes. The campus is scheduled to open in Fall 2026 and represents the first fully accredited US international branch campus in the Kingdom. The development is directly supported by Saudi Arabia's Vision 2030 strategy to diversify the economy through education and attract international academic institutions.

March 2026 - UNESCO published its landmark report "Transforming Higher Education: Global Collaboration on Visioning and Action", establishing a global roadmap for the sector's future. The report highlights that global higher education enrolment has more than doubled over two decades, reaching 269 million students in 2024 with 43% of the higher education-age population now participating in tertiary education, the highest proportion ever recorded. The publication also notes that nearly 7 million students now study internationally, triple the figure from 2000, and identifies AI governance, digital equity, and quality assurance as the sector's most critical strategic imperatives.

February 2026 - The University of Washington and Microsoft announced the expansion of their long-standing partnership to accelerate AI research, broaden student and community AI literacy programmes, and prepare Washington State's workforce for an AI-driven economy. The initiative is underpinned by a forecast of 1.5 million job vacancies in the state by 2032, with over 75% expected to require post-secondary credentials highlighting the direct link between higher education capacity and regional economic competitiveness.

January 2026 - Microsoft announced the Microsoft Elevate for Educators programme, providing educators globally with free professional development resources, AI literacy credentials, and Copilot-powered teaching tools. Concurrently, Microsoft made Microsoft 365 Personal and LinkedIn Premium Career subscriptions available free for 12 months to eligible college students in the United States, directly integrating AI productivity and professional networking into the higher education experience at scale.

The global higher education market features a dual competitive landscape: traditional elite universities competing for international student enrolment, research grants, and institutional rankings, alongside technology platform companies and corporate education providers competing for the growing skills-and-credentials market. EdTech platforms including Coursera and Udemy command scale advantages in online credential delivery, while enterprise software companies like Oracle, SAP, and Microsoft provide the administrative and learning management infrastructure universities depend on.

Competition for research funding, faculty talent, and international students is intensifying among top-tier institutions, while the growing employer-led skills agenda is creating new competitive pressure from corporate learning providers and government-backed reskilling platforms. Institutions that successfully combine research prestige, flexible online delivery, and employer partnership networks hold the strongest competitive positions in the global higher education market.

Founded in 1975 and headquartered in Redmond, Washington, Microsoft is a global technology leader whose Azure cloud infrastructure, Microsoft 365 productivity suite, and LinkedIn Learning platform make it a central technology partner for higher education institutions worldwide. In April 2026, Microsoft joined the Khan TED Institute project alongside Google and McKinsey to co-develop an applied AI bachelor's degree, reinforcing its curriculum co-design role in the higher education market.

Founded in 1998 and headquartered in Mountain View, California, Google delivers higher education technology through Google Workspace for Education, Google Career Certificates, and its Coursera partnership for cloud and AI curriculum content. In June 2025, Coursera's TIME100 recognition highlighted Google's role as a key curriculum partner whose professional certificates are directly integrated into accredited programmes serving millions of learners globally.

Founded in 1977 and headquartered in Austin, Texas, Oracle is a global enterprise software provider whose Student Information System, learning management, and cloud ERP solutions are deployed across hundreds of universities globally. Oracle's higher education suite helps institutions manage enrolment, financial aid, research contracts, and online learning infrastructure, making it a critical operational partner in the global higher education technology market.

Founded in 1636 and based in Cambridge, Massachusetts, Harvard University is the world's oldest and most recognised higher education institution with an endowment exceeding USD 50 billion. Harvard's global alumni network, HBX online programmes, and cross-disciplinary research institutes position it as both a traditional credential leader and an expanding online and executive education provider in the global higher education market.

Other key players in the market are Anthology Inc., Blackbaud Inc., Ellucian Company L.P., IBM Corporation, SAP SE, Pearson plc, Dell Inc., VMware Inc., Xerox Holdings Corporation, ServiceNow Inc., Unifyed, Hyland Software, California Institute of Technology, Columbia University, Imperial College London, Massachusetts Institute of Technology, Peking University, Stanford University, Tsinghua University, The Trustees of Princeton University, The University of Tokyo, University of Cape Town, University College London, University of Oxford, University of the Andes, University of Pennsylvania, Yale University, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Access the full intelligence on the global higher education market with our comprehensive research report. Understand how AI integration, online learning expansion, employer-driven curriculum, and platform consolidation are reshaping competitive dynamics across institutions, technology providers, and credential platforms. Whether you are a university administrator, EdTech operator, technology vendor, investor, or policymaker, this report delivers the data and strategic clarity to stay ahead. Download your free sample today and explore the key growth opportunities across higher education.

Upto 15% Off

USD

$2999 $2699

$4839 $4355

$5999 $5099

$7259 $6170

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market is projected to grow at a CAGR of 19.60% between 2026 and 2035.

The key strategies driving the market include digital transformation through online learning platforms, international student recruitment, partnerships with edtech firms, personalized learning experiences, and emphasis on career-oriented programs. Institutions also focus on data-driven decision-making, hybrid learning models, alumni engagement, and expanding access to underserved populations for sustainable growth.

Key trends aiding market expansion include the advancements in technology, emergence of distance learning, increasing demand for online classes, and changing student and industry expectations.

Regions considered in the market are North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa.

The major institutions are public, and private.

The key players in the market report include Anthology Inc., Blackbaud, Inc., Google LLC, Microsoft Corporation, Ellucian Company L.P, Oracle Corporation, IBM Corporation, SAP SE, Pearson plc, Dell, Inc, VMware, Inc, Xerox Holdings Corporation, ServiceNow, Inc, Unifyed, Hyland Software, California Institute of Technology, Columbia University, Imperial College London, Massachusetts Institute of Technology, Peking University, Stanford University, Tsinghua University, The President and Fellows of Harvard College, The Trustees of Princeton University, The University of Tokyo, University of Cape Town, University College London, UCL, University of Oxford, University of the Andes, University of Pennsylvania, and Yale University, among others.

North America led the higher education market, largely due to its advanced research, technological advancements, and scientific innovations, which make it increasingly attractive to both domestic and international students.

In 2025, the market reached an approximate value of USD 990.50 Billion.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 5931.52 Billion by 2035.

The undergraduate segment is the most dominant in the market, accounting for the highest enrolment globally.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Institution |

|

| Breakup by Learning Mode |

|

| Breakup by Course |

|

| Breakup by Revenue Source |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,999

USD 2,699

tax inclusive*

Single User License

One User

USD 4,839

USD 4,355

tax inclusive*

Five User License

Five User

USD 5,999

USD 5,099

tax inclusive*

Corporate License

Unlimited Users

USD 7,259

USD 6,170

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.