Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

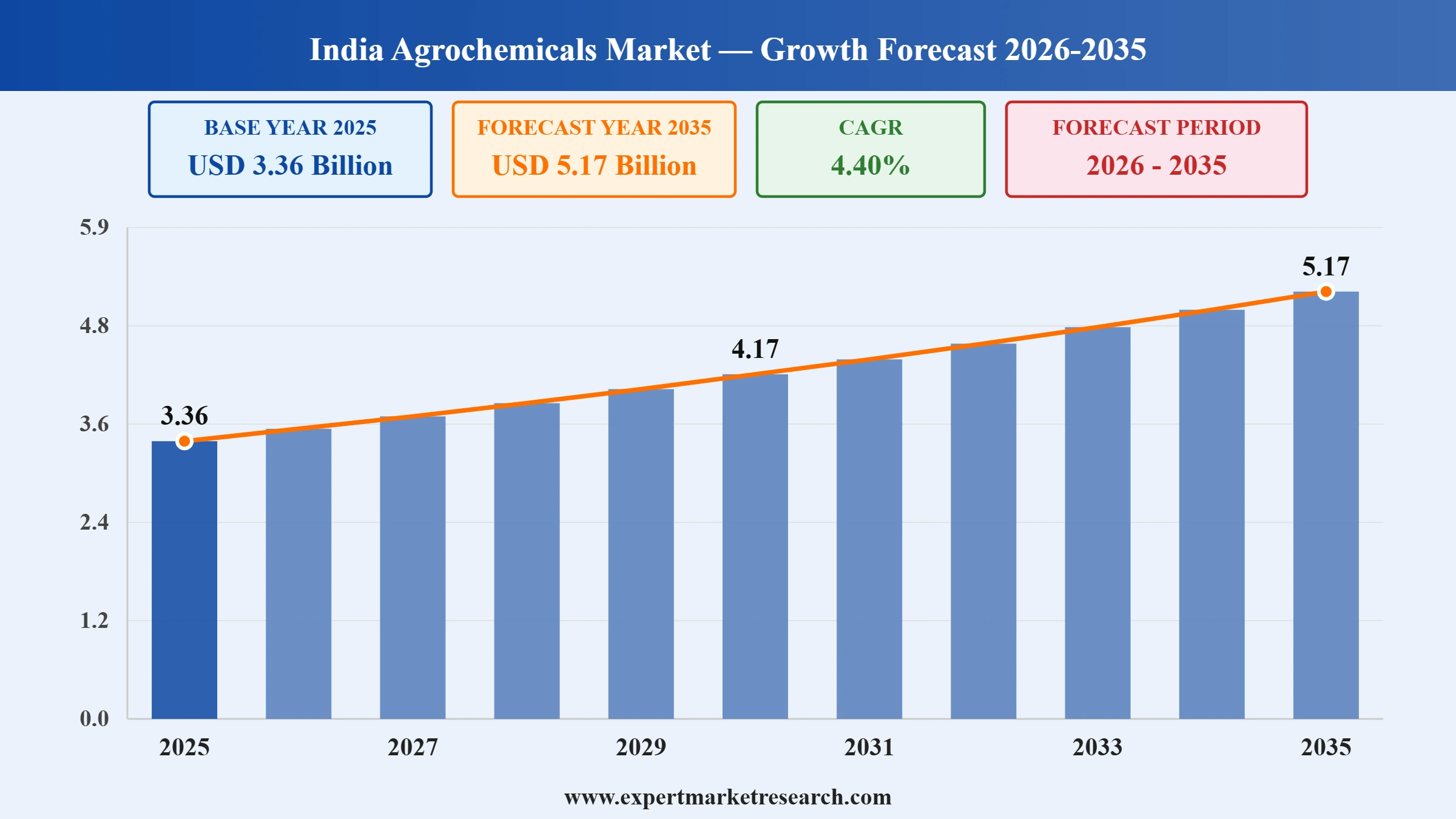

The India agrochemicals market reached a value of USD 3.36 Billion in 2025 and is projected to grow at a compound annual growth rate CAGR of 4.40% during the forecast period of 2026-2035, reaching USD 5.17 Billion by 2035. India occupies a unique position in the global agrochemical industry as the fourth-largest producer globally and the second-largest in Asia Pacific after China, functioning simultaneously as a major domestic consumer and a net exporter of agrochemical products to global markets. This growth is driven by several structurally important factors, including increasing food demand from a population expected to reach 1.5 billion by 2030, government support through favourable policies, production-linked incentive schemes, and direct farmer subsidies, and continuous technological advancements in agrochemical formulations and precision farming techniques that improve application efficiency and crop yields across India's diverse agro-climatic zones.

The Indian agrochemical industry plays a critical role in national food security, addressing the estimated 15-25% loss of potential crop production to pests and diseases annually a figure cited by leading agricultural institutions that underscores the indispensable commercial and social role of crop protection chemicals. India's total agrochemical production capacity has grown significantly since fiscal year 2019, when it exceeded 1.4 million metric tons, with continued expansion driven by domestic demand growth, export opportunity capture, and the government's Make in India manufacturing promotion initiatives. The country produces all major categories of agrochemicals including insecticides, herbicides, fungicides, fumigants, plant growth regulators, and specialty fertilisers, with domestic manufacturers increasingly focusing on generic molecule formulations that offer cost advantages in both domestic and export markets.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The India agrochemicals market encompasses the production, distribution, and sale of all chemical and bio-based substances used in agriculture to enhance crop productivity, protect crops from pests, diseases, and weeds, and improve the nutritional content of soil. Agrochemicals include two broad primary categories: pesticides comprising insecticides, herbicides, fungicides, fumigants, rodenticides, nematicides, and plant growth regulators and fertilisers, including nitrogenous, phosphatic, potassic (NPK), complex, and specialty fertilisers. Bio-based or organic agrochemicals, including biopesticides, biofertilisers, and plant-derived formulations, represent an emerging and fast-growing segment within the Indian market as farmers, regulators, and export buyers increasingly demand lower chemical residue and more environmentally sustainable crop protection solutions.

The market is regulated at the national level by the Central Insecticides Board and Registration Committee (CIB&RC) under the Insecticides Act, 1968, which governs the registration, manufacture, sale, import, and use of pesticides in India. The Department of Fertilisers under the Ministry of Chemicals and Fertilisers governs the fertiliser sector, including nutrient-based subsidies and maximum retail price controls on key fertiliser grades. This regulatory architecture creates a structured but complex compliance environment that shapes market entry, product launch timelines, and competitive dynamics across both domestic and multinational agrochemical companies operating in India.

| India Agrochemicals Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 3.36 |

| Market Size 2035 | USD Billion | 5.17 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 4.40% |

| CAGR 2026-2035 - Market by Fertilizer Type | Nitrogen Fertilizer | 4.9% |

| CAGR 2026-2035 - Market by Pesticide Type | Herbicides | 4.7% |

| Market Share by Country 2025 | Herbicides | 15.0% |

The agrochemicals market in India is driven by the rising population within the country, which has led to maintaining sufficiency in agricultural practices, further boosting the use of Indian agrochemical products for farming activities. Moreover, as the demand for food products is increasing, the landmass available for agriculture is gradually decreasing due to the heightened effect of urbanisation, which is providing an impetus for the farmers to use different agrochemicals to increase land productivity and maintain soil health. The India agrochemicals market value is also positively influenced by the Indianisation of the agrochemical industry, which has fuelled the sales of agrochemical products.

According to the Agricultural and Processed Food Products Export Development Authority (APEDA), Ministry of Commerce & Industries, Government of India, India produced approximately 2.9 million metric tons (MT) of certified organic products in 2022–2023, including all types of food products such as oil seeds, fiber, sugar cane, cereals & millets, cotton, pulses, aromatic & medicinal plants, tea, coffee, fruits, spices, dry fruits, vegetables, processed foods, etc.

Shift towards bio-based agrochemicals, rise in agrochemical exports, and technological advancements are the key trends propelling the market growth.

FMC Corporation announced on May 7, 2026 a definitive agreement to sell FMC India Private Limited to Crystal Crop Protection Limited for USD 252 million, marking one of the largest agrochemical M&A transactions in India and enabling Crystal to expand its crop protection portfolio and pan-India distribution.

Tagros Chemicals Private Limited acquired German multinational Bayer AG's Flubendiamide insecticide business in India in March 2026, including key brands and formulations used for lepidopteran pest control in rice and cotton crops, marking Tagros' entry into the branded B2C crop protection segment through its newly established entity Arquivo, according to Business Standard reporting dated April 17, 2026.

The Ministry of Agriculture and Farmers Welfare notified the Fertiliser (Inorganic, Organic or Mixed) (Control) Fourth Amendment Order, 2026 on March 30, 2026, significantly expanding India's regulatory framework for biostimulants, introducing detailed scientific specifications for humic acids, seaweed extracts, amino acid formulations, and biochemical biostimulants across crop-specific application protocols.

Nova Agritech Limited received a licence amendment from the Telangana Government in January 2026, permitting the company to manufacture biostimulants at its existing Telangana formulation plant, following commissioning of expanded manufacturing infrastructure funded through INR 24.69 crore in IPO proceeds, increasing total capacity to 14,592 MTPA.

As per the India agrochemicals market dynamics and trends, the increasing adoption of bio-based products, such as biopesticides made with neem is propelling the market growth. This shift is driven by a growing awareness of environmental sustainability and the need to reduce chemical residues in agricultural produce. The Indian government has been increasingly promoting organic farming and the use of bio-based agrochemicals. Farmers are encouraged to switch to organic and bio-based inputs by several programs, such as the Paramparagat Krishi Vikas Yojana (PKVY) and Mission Organic Value Chain Development for Northeastern Region (MOVCDNER). These initiatives try to inform farmers about the advantages of sustainable farming methods in addition to offering financial incentives. Since the pandemic, the organic food business in India has grown exponentially. India is the fifth-largest organic food producer in the world, with 2.6 million hectares under cultivation, according to a 2022 survey of 187 countries that practice organic agriculture by the International Federation of Organic Agriculture Movements (IFOAM) and Research Institute of Organic Agriculture (FiBL). The survey also showed that India has grown its cultivated organic agricultural land by 145.1% over the past ten years, with 1.5% of the country's total agricultural area being used for organic farming. India has the biggest number of organic farmers in the world, at 4.43 million, according to the Economic Survey 2022–2023.

The country's agrochemical exports have been steadily increasing, which not only boosts the Indian economy but also positions the country as a key supplier of agrochemical products worldwide. Latin America, Africa, and the Asia-Pacific region have seen an increase in the global footprint of Indian agrochemical enterprises. As per the India agrochemicals market analysis, one major Indian agrochemical company that is contributing to the increase of exports is UPL Limited, which has distribution networks spanning more than 130 countries. India is a global leader in the export of agricultural products. The total value of agricultural product exports from April to January of 2024 was USD 38.65 billion. India's agricultural exports were valued at USD 52.50 billion in 2022–2023. The nation's overall agricultural exports in 2021–2022 were USD 50.2 billion, a 20% increase from USD 41.3 billion in 2020–21. India's principal export markets for agrochemicals are Brazil, the United States, Japan, Vietnam, and Indonesia. Brazil has emerged as a significant market, with India being one of the top suppliers of crop protection chemicals to support Brazil’s large-scale soybean and corn production.

The Indian government's support and policy reforms play a crucial role in shaping the India agrochemical market outlook. Initiatives like the Make in India Mission and Atmanirbhar Abhiyan aim to boost domestic manufacturing, reduce import dependency, and promote self-sufficiency in agrochemical production, which will likely the India agrochemicals demand forecast. The manufacturing of agrochemicals in India has increased significantly because of the Make in India initiative. To serve both local and international markets, businesses such as UPL Limited, PI Industries, and Rallis India, for instance, have increased the size of their production facilities. India started exporting agrochemicals to more than 100 nations in 2022 after its capacity for producing agrochemicals had grown dramatically. As local production of technical-grade chemicals and raw materials has expanded, India's imports of agrochemicals, particularly from China, have decreased. According to the Ministry of Chemicals and Fertilizers, the Atmanirbhar Bharat program was successful as seen by the 15% decrease in imports in 2022 when compared to 2020 levels.

According to data from the USDA Foreign Agricultural Service (FAS) U.S. Department of Agriculture, rice production in India is projected to increase from the five-year average (2019-2023) of 129,093 thousand tons to 138,000 thousand tons by 2024/25, marking a 7% increase, thus aiding the agrochemicals industry in India. This growth can be attributed to improvements in agricultural practices, government support, and favourable weather conditions. Wheat production is also expected to rise, reaching 114,000 thousand tons in 2024/25, a 6% increase from its five-year average of 107,120 thousand tons. Similarly, corn production is projected to see a significant boost, with an 11% increase, rising from 33,946 thousand tons to 37,500 thousand tons. Soybean production is set to grow by 9%, from an average of 11,186 thousand tons to 12,200 thousand tons in 2024/25.

The Indian government's support for the agrochemical industry is evident through initiatives like the Production Linked Incentive (PLI) scheme for the agrochemical sector. Companies like Rallis India and Insecticides India have benefited from such policies, which incentivise domestic manufacturing and promote self-reliance in agrochemical production.

Additionally, government initiatives focusing on agriculture, such as doubling farmer income by 2022, significant public spending on rural infrastructure, crop insurance coverage, and agricultural credit, are boosting domestic consumption. The rise in disposable income of farmers through schemes like PM-KISAN is increasing the demand of India agrochemicals market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Companies like PI Industries and Dhanuka Agritech Limited are actively investing in research and development to develop innovative agrochemical solutions, precision agriculture technologies, smart formulations, and digital farming tools, aiding the India agrochemicals market growth. This can improve product efficacy and operational efficiency. In January 2021, UPL partnered with TeleSense, a provider of IoT-based grain monitoring solutions, to address post-harvest challenges in the agricultural supply chain. The collaboration aimed to leverage TeleSense's advanced sensors, data analytics, and AI-powered predictive insights to monitor grain quality, storage conditions, and pest infestations in real-time. By integrating TeleSense's technology with UPL's expertise in crop protection and post-harvest management, the partnership sought to optimize storage practices, reduce spoilage, and improve grain quality throughout the storage and transportation phases. According to the Indian Chemical Council, leading companies like UPL and PI Industries are investing over 5-8% of their annual revenue in R&D, with UPL spending approximately INR 1,000 crore annually on innovation. This has led to the development of new eco-friendly products and improved formulations.

Fertilizer production, imports, and sales in India from April to May 2023 exhibit notable trends when compared to the same period in 2022. Urea production increased significantly from 43 lakh tons in 2022 to 50 lakh tons in 2023, representing a 16% growth. Imports of urea also rose by 37%, from 5 lakh tons in 2022 to 7 lakh tons in 2023. This surge in both production and imports contributed to a substantial rise in urea sales, which climbed from 32 lakh tons to 43 lakh tons, marking a 34% increase.

As per India agrochemicals industry analysis, the production of Di-Ammonium Phosphate (DAP) grew from 7 lakh tons in 2022 to 8 lakh tons in 2023, reflecting a 10% rise. DAP imports saw a remarkable increase of 73%, from 6 lakh tons to 10 lakh tons. Consequently, DAP sales surged by 47%, from 9 lakh tons in 2022 to 14 lakh tons in 2023. On the other hand, Muriate of Potash (MOP) showed a different trend. While imports grew significantly by 85%, from 3 lakh tons in 2022 to 6 lakh tons in 2023, sales declined by 43%. NPK Complex fertilizers also experienced a robust increase in production, import, and sales. Production increased by 31%, from 12 lakh tons to 16 lakh tons, imports rose by 56%, from 4 lakh tons to 6 lakh tons, and sales saw a significant increase of 55%, from 7 lakh tons to 10 lakh tons.

Overall, the total production of fertilizers in India increased by 18%, from 62 lakh tons in April to May 2022 to 73 lakh tons in the same period in 2023. Imports rose sharply by 61%, from 18 lakh tons to 29 lakh tons. The total sales of fertilizers saw a significant increase of 37%, from 50 lakh tons in 2022 to 68 lakh tons in 2023. These trends indicate a strong growth trajectory in the fertilizer sector in India, driven by increased domestic production.

The EMR’s report titled “India Agrochemicals Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Type

Market Breakup by Nature

Market Breakup by Application

Market Breakup by Region

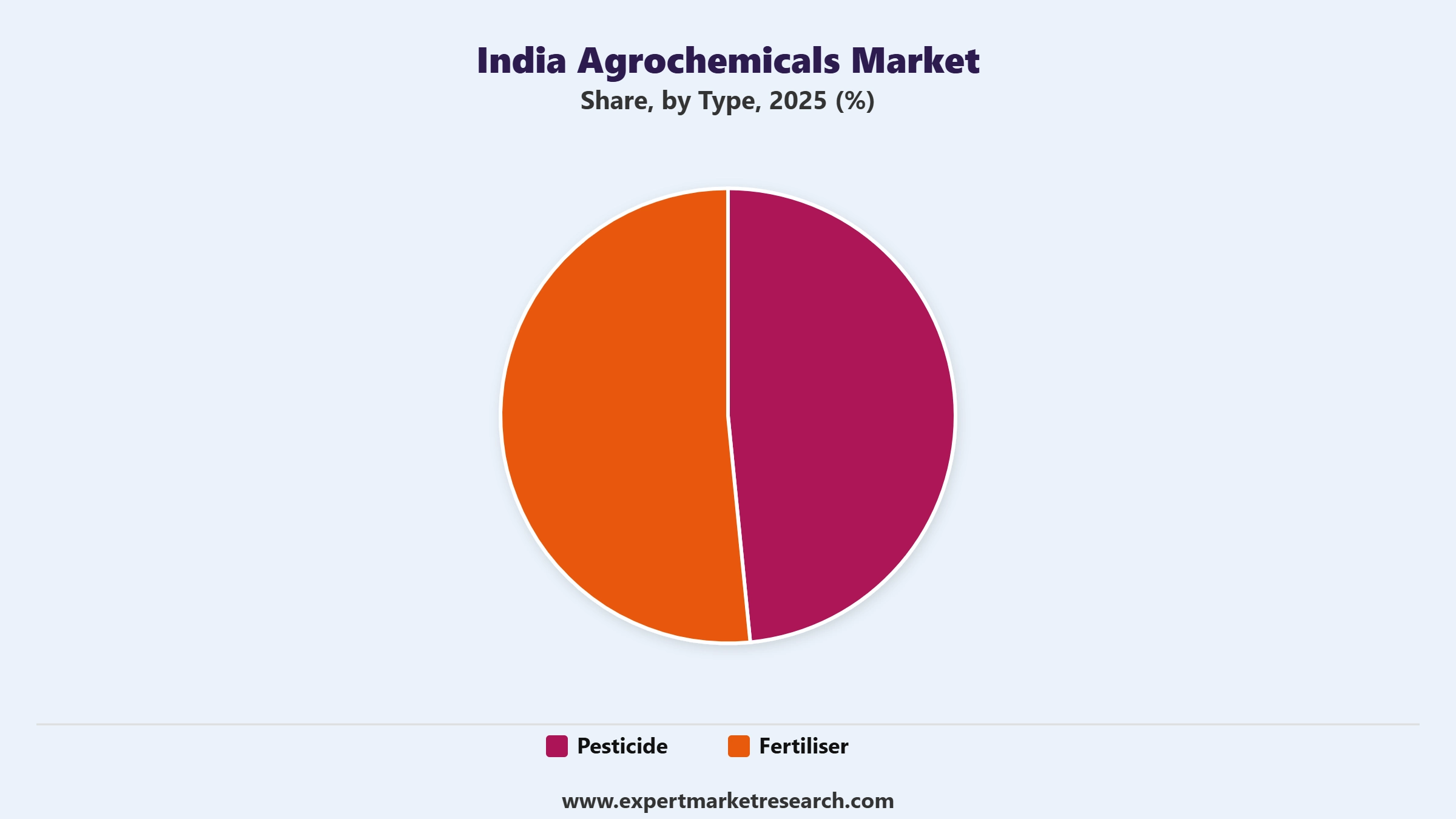

Market Analysis by Type

Fertilisers are used across a wide range of crops, including rice, cereals, grains, and tubers, to meet the growing demand for nutritious food in India. As per India agrochemicals market report, nitrogenous fertilisers are expected to grow at a CAGR of 4.9% between 2026 and 2035 in the fertilisers segment, as nitrogen is a vital macronutrient required for crop growth and development.

On the other hand, pesticides segment includes insecticides, herbicides, and fungicides. Herbicides and fungicides are expected to grow at a CAGR of 4.7% and 4.2% between 2026 and 2035. The increasing use of herbicides is a notable driver for the growth of this segment, as farmers seek to manage weeds more effectively. Additionally, there is a growing demand for insecticides, particularly for the cultivation of staple crops like cereals and grains.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Potassium-based fertilisers are also seeing increased demand, as they help increase protein content in plants. The low cost and better efficiency of potassium chloride compared to traditional fertilisers are major factors contributing to the growth of the fertilisers segment, thus contributing to the agrochemicals market share in India.

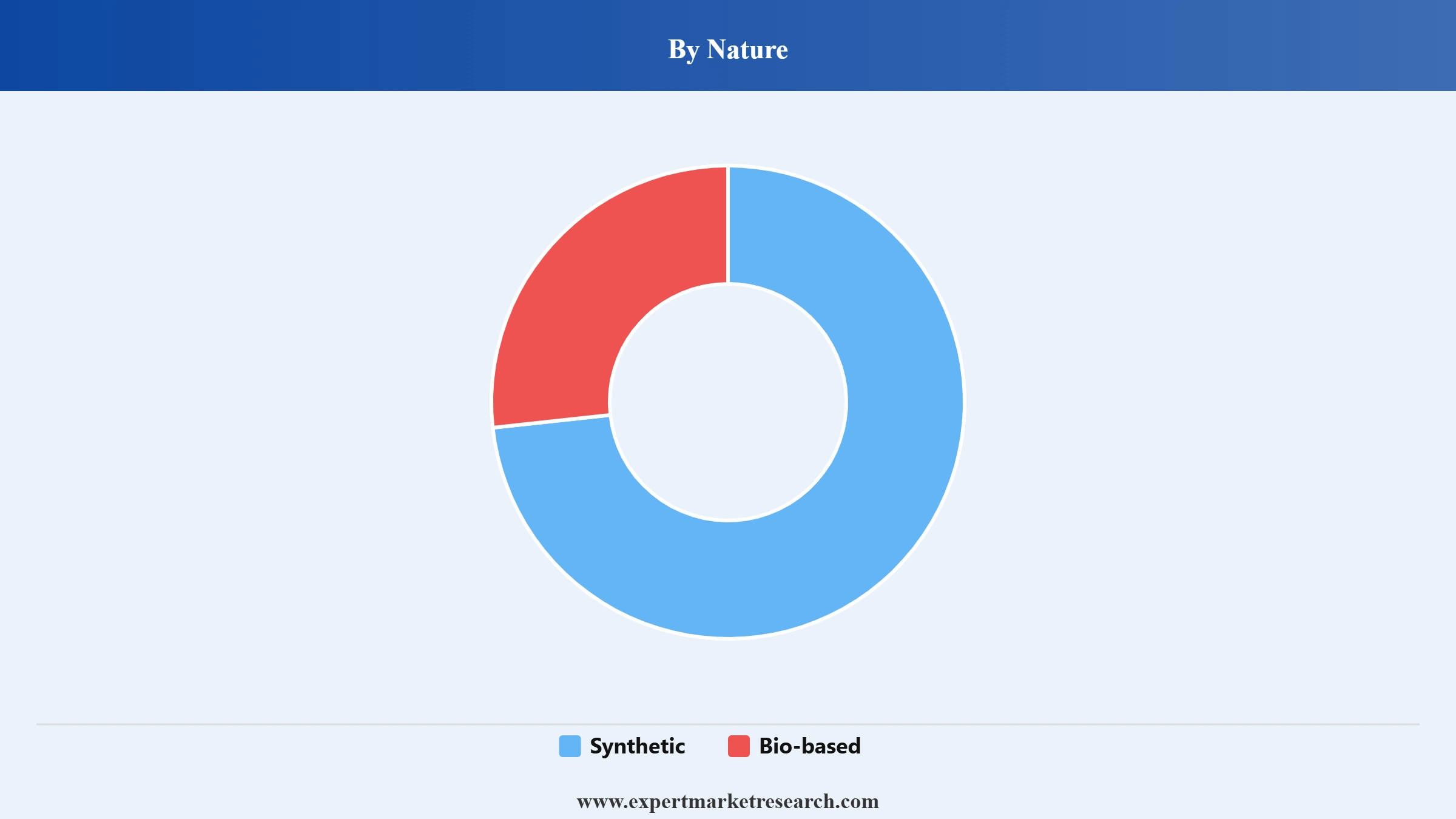

Market Analysis by Nature

Synthetic agrochemicals, including pesticides and fertilisers, continue to dominate the landscape. For instance, the government's recent registration of 335 molecules in the agrochemical sector underscores a strong regulatory framework that supports innovation and this market segment’s expansion. Recent trends show a notable increase in the use of herbicides and fungicides as farmers seek effective solutions to combat pests and diseases, particularly considering rising labour costs.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

On the other hand, biobased agrochemicals are gaining traction as sustainable alternatives to traditional synthetic products. This segment includes bio-pesticides and bio-fertilisers, which are increasingly being adopted due to environmental concerns and regulatory pressures promoting organic farming practices. Initiatives by companies like BASF and Syngenta are focused on developing biobased solutions that align with eco-friendly farming methods. Furthermore, government programs aimed at educating farmers about the benefits of biobased products highlight the shift towards more sustainable agricultural practices.

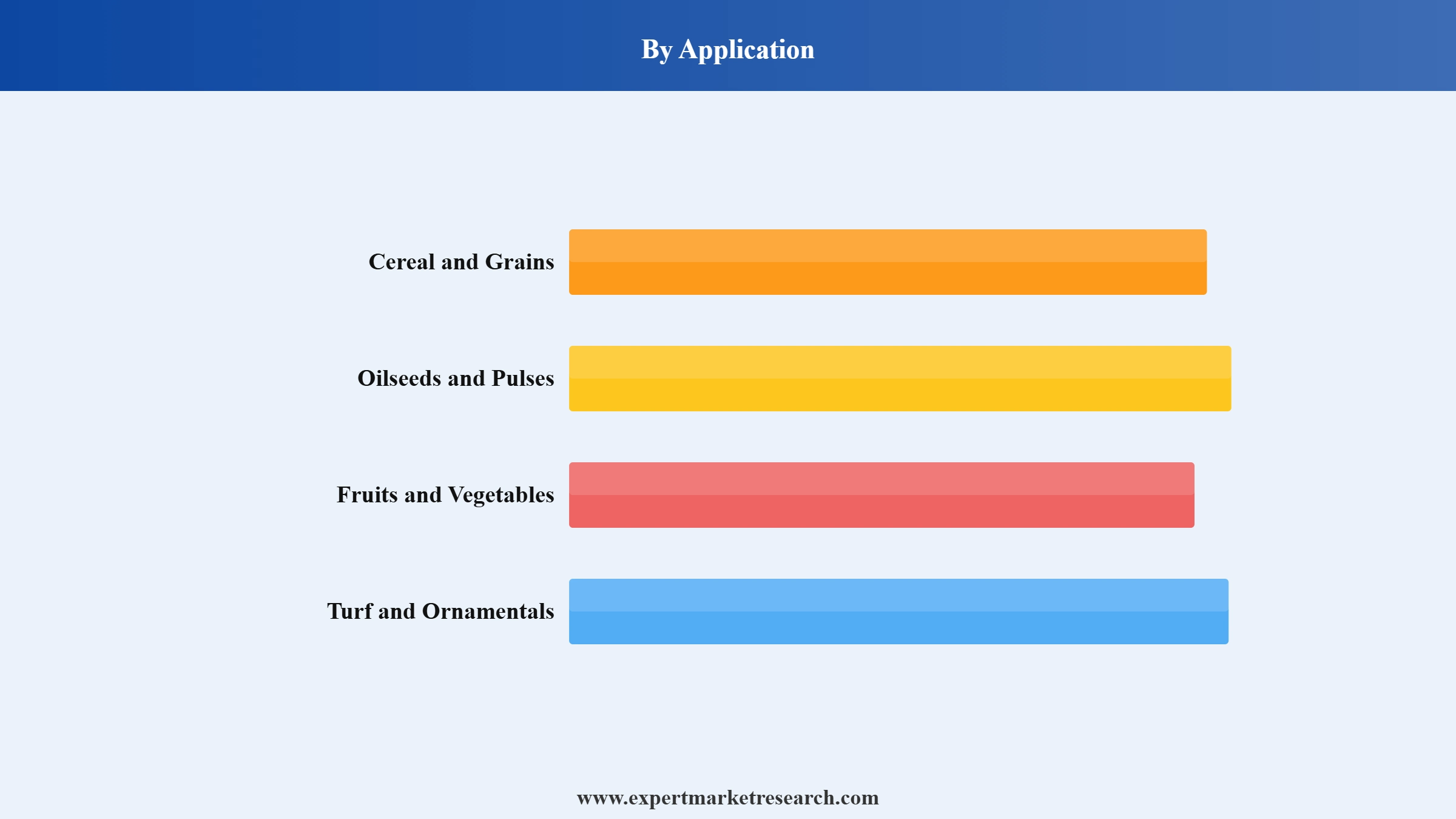

Market Analysis by Application

The Indian agrochemicals market is segmented into various categories, including grains and cereals, pulses and oilseeds, fruits and vegetables, and turfs and ornamentals. In the grains and cereals segment, the demand for agrochemicals is primarily driven by the need to enhance productivity amid increasing food security concerns. For instance, paddy cultivation, which consumes about 26-28% of agrochemicals in India, has seen the introduction of products like Bayer's "Safi" herbicide to combat weeds effectively. The government's initiatives to promote self-sufficiency in food grain production have led to increased use of fertilisers such as Urea and DAP (Diammonium Phosphate) to boost crop yields.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The government has also been promoting the cultivation of oilseeds to reduce import dependency, resulting in a rising demand for herbicides tailoured for these crops. For example, the use of Glyphosate has become essential for managing weeds in soybean cultivation. Additionally, the National Mission on Oilseeds and Oil Palm aims to increase domestic production through improved agricultural practices and inputs, leading to pulses and oilseeds segment’s growth.

In the fruits and vegetables category, India ranks as the second-largest producer globally, accounting for nearly 90% of total horticulture production. This segment is witnessing a surge in demand for fungicides such as Tricyclazole, commonly used in rice cultivation to control blast disease. Notably, India leads in producing several horticultural crops like mangoes, bananas, and potatoes, which also drives the need for effective crop protection solutions. Additionally, the government's commitment to enhancing agricultural productivity through initiatives like Krishi Vigyan Kendras supports the adoption of advanced agrochemical solutions across all segments.

The India agrochemicals market faces significant operational and structural challenges that moderate the pace of market expansion despite strong underlying agricultural demand fundamentals. Regulatory complexity under the Insecticides Act, 1968 currently under revision creates lengthy and unpredictable product registration timelines, with new molecule registrations often requiring 5-10 years from data submission to commercial approval, creating a substantial competitive disadvantage relative to agricultural economies with more streamlined agrochemical registration frameworks. Pesticide adulteration and counterfeiting represent persistent challenges that undermine farmer confidence, compress margins for legitimate manufacturers, and create safety and efficacy concerns across informal distribution channels in smaller states. Climate variability including erratic monsoon patterns, unseasonal rainfall, and drought stress creates demand volatility that complicates production planning and inventory management for agrochemical distributors and retailers across India's geographically diverse agricultural landscape.

Structural restraints moderate the commercialisation and adoption pace in several important market dimensions. India's vast smallholder farming population with the average farm holding below 1.5 hectares limits the per-farm purchasing volumes that individually justify agrochemical dealer investment in quality products, creates challenges in reaching farmers with accurate usage guidance, and sustains a fragmented informal distribution infrastructure that is difficult for regulated manufacturers to serve cost-effectively. The fertiliser subsidy regime, while beneficial for farmer affordability, creates price signal distortions that can encourage excessive or imbalanced nutrient application, contributing to soil health degradation and long-term productivity challenges. Resistance development in key pest and pathogen populations to established active ingredient classes including resistance to pyrethroid insecticides, triazole fungicides, and glyphosate herbicide in multiple weed species is shortening the commercial lifecycle of established products and requiring continuous innovation investment that creates scale challenges for smaller domestic manufacturers with limited R&D budgets.

Despite these structural headwinds, the India agrochemicals market presents compelling and multi-dimensional growth opportunities throughout the forecast period. The PLI scheme for agrochemicals is creating a structured investment incentive that is attracting both domestic and international capital into new manufacturing capacity, with targeted outcomes including doubling India's agrochemical export value and expanding domestic production of import-dependent specialty active ingredients. India's growing role as a global generic agrochemical manufacturer and CRAM partner for multinational originator companies creates a revenue diversification opportunity beyond domestic consumption, with export revenues providing higher-margin growth beyond the regulated domestic pricing environment. The transition toward bio-based agrochemicals, precision agriculture, and integrated pest management creates structural demand for a new generation of agrochemical products and services that domestic innovators are well-positioned to develop and commercialise, particularly in biopesticide formulations where India's biodiversity and traditional agricultural knowledge provide unique raw material and product development advantages. The full Expert Market Research India Agrochemicals Market Report and Forecast 2026-2035 provides granular analysis across agrochemical type, nature, crop application, and regional market dimensions to support manufacturers, distributors, investors, policymakers, and global agrochemical companies in navigating and capitalising on India's large, complex, and rapidly evolving agrochemical market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North India

North India is one of the largest regional markets for agrochemicals in the country, anchored by the agricultural powerhouses of Punjab, Haryana, and Uttar Pradesh states that collectively account for a dominant share of India's wheat and rice production under the Green Revolution agricultural model. Punjab and Haryana have among the highest pesticide application rates per hectare in India, driven by intensive commercial farming, high cropping intensity (two to three crops per year on irrigated land), and well-developed agricultural input supply chains. The region represents a mature agrochemical market characterised by high-volume commodity pesticide and fertiliser consumption, growing emphasis on integrated pest management driven by pesticide resistance concerns, and increasing adoption of specialty nutrients and precision agriculture technologies.

East and Central India

The East and Central India region spanning Odisha, Bihar, Jharkhand, Chhattisgarh, and Madhya Pradesh represents a significant and growing agrochemical market with substantially lower per-hectare input use than North and West India, reflecting a combination of smaller farm holdings, lower irrigation coverage, and less developed agricultural input supply chains in tribal and remote farming districts. This lower base of agrochemical penetration creates a structural growth opportunity as infrastructure development, extension services, and formal credit availability progressively improve across the region. Madhya Pradesh, with its large soybean and wheat production base, is the most commercially active state for agrochemical distribution within the region.

West India

West India led by Maharashtra and Gujarat is the most agriculturally and industrially diverse agrochemical market region in the country. Maharashtra is the country's largest producer of horticultural crops including grapes, oranges, sugarcane, and cotton, which are all high-value, high-intensity agrochemical consumers particularly fungicides for grape and citrus disease management. Gujarat is the primary manufacturing hub for India's agrochemical industry, hosting the majority of large-scale technical grade and formulation plants, including facilities operated by Dhanuka, Meghmani Organics, Astec LifeSciences, and multiple multinational contract manufacturing facilities.

South India

South India comprising Andhra Pradesh, Telangana, Karnataka, Tamil Nadu, and Kerala is a significant agrochemical consuming region characterised by a diverse crop portfolio including rice, cotton, chilli, tobacco, coffee, tea, rubber, coconut, and banana. The region has a highly commercial approach to agricultural input use, with well-developed agri-input dealer networks, strong extension service infrastructure in states including Andhra Pradesh and Telangana, and high adoption rates for newer fungicide and insecticide products among commercial farmers. Coromandel International, one of India's largest agrochemical companies, is headquartered in Hyderabad and has its strongest distribution presence across Andhra Pradesh, Telangana, and Karnataka.

The Indian agrochemicals market is experiencing significant growth, driven by increased investments in research and development (R&D) focused on innovative products and sustainable practices. Major players like Bayer AG, Syngenta, and UPL are developing new agrochemical molecules to combat emerging pests while adhering to environmental regulations. This shift includes a strong emphasis on green chemistry and promoting eco-friendly products that reduce toxicity and reduce application rates. Technological advancements, such as digital agriculture tools, enhance R&D efficiency by streamlining the discovery of effective compounds. Additionally, government initiatives like "Make in India" support domestic manufacturing and innovation in the sector. As global demand for sustainable agricultural solutions rises, India's commitment to R&D and green practices positions it as a key player in the global agrochemicals market.

Sumitomo Chemical Co., Ltd. is a Japanese multinational chemical company founded in 1913. Its headquarters are in Tokyo, Japan. The company provides a diverse range of products including agrochemicals, petrochemicals, pharmaceuticals, and speciality chemicals.

Dhanuka Agritech Limited is an Indian agrochemicals company founded in 1985. Its headquarters are based in Gurgaon, India. The company manufactures a wide range of pesticides, insecticides, herbicides, and other crop protection products for crops such as rice, cotton, and vegetables to support the growth of the agrochemicals industry in India.

Meghmani Organics Ltd. was founded in 1989 and its headquarters are in Ahmedabad, India. It is a leading manufacturer of pesticides, insecticides, and other crop protection chemicals in India. The company's products are designed for use on crops such as sugarcane and cotton.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other India agrochemicals market key players include Corteva Agriscience AG, Tata Chemicals Ltd., UPL Limited, Bayer AG, Syngenta Crop Protection AG, BASF SE, Rallis India Limited, and PI Industries Limited, among others.

UPL Limited

Syngenta India Limited

Rallis India Limited

Dhanuka Agritech Limited

Various startups are playing a crucial role in revolutionizing the India agrochemicals market by introducing advanced technology solutions such as precision farming, AI-based quality control, and IoT-driven crop monitoring. They are contributing to reducing the overuse of agrochemicals while ensuring sustainable agriculture, helping farmers achieve better yields with fewer chemical inputs.

Fasal

Founded in 2018 and located in Bengaluru, Fasal is an agri-tech startup that provides AI-powered, IoT-based precision farming solutions. The startup uses climate-based data to help farmers make informed decisions regarding the application of agrochemicals, water, and other inputs. Fasal's technology ensures that agrochemicals are used only when necessary, reducing over-application and optimizing resource usage. In 2022, Fasal raised significant funding to expand its operations across India. The company is now working with farmers to reduce agrochemical usage by providing real-time data about crop health, weather patterns, and pest threats.

Arya Collateral

Founded in 2013 and located in New Delhi, Arya is a post-harvest agritech company that provides warehousing, storage, and financial solutions to farmers and agri-businesses. Arya helps farmers reduce losses due to pests and diseases by providing storage solutions that minimize the need for chemical inputs. Their services help in optimizing agrochemical usage in post-harvest management. Arya recently raised funding to scale up its operations and digital platform, providing farmers with better post-harvest storage solutions and minimizing the need for chemical preservatives.

Australia Agrochemicals Market

Colombia Agrochemicals Market

Agrochemicals Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 3.36 Billion.

The market is assessed to grow at a CAGR of 4.40% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 5.17 Billion by 2035.

The major drivers of the market include, growing population, regional economic growth, increased government initiatives to assist farmers, and create awareness among them regarding modern agricultural practices, and rapid technological advancements.

The key guiding the growth of the market in India include increasing investment in the protection of crops, and the development of integrated farming practices and their growing acceptance among the farmers in the region.

Regions considered in the market are north region, east and central region, west region, and south region.

Based on crop application, the market is divided into grains and cereals, pulses and oilseeds, fruits and vegetables, and turf and ornamentals, among others.

Key players in the market are Corteva Agriscience AG, UPL Limited, Bayer AG, Syngenta Crop Protection AG, BASF SE, PI Industries Limited, Sumitomo Chemical Co., Ltd, Dhanuka Agritech Limited, Meghmani Organics Ltd, Tata Chemicals Ltd, and Coromandel International Limited, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Nature |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.