Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The India automotive HVAC market was valued at USD 1.65 Billion in 2025. The market is expected to grow at a CAGR of 11.20% during the forecast period of 2026-2035 to reach a value of USD 4.77 Billion by 2035. Rising passenger vehicle production, increasing consumer preference for enhanced cabin comfort, and growing adoption of electric vehicles are key factors that are driving the overall growth in the market.

Compound Annual Growth Rate

11.2%

Value in USD Billion

2026-2035

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The India automotive HVAC market is being reshaped by three simultaneous forces: the October 2025 commercial vehicle AC mandate creating structurally new demand in the truck segment, the ongoing cascade of automatic climate control systems into progressively lower vehicle price points, and the EV transition demanding complex heat pump-based thermal management with significantly higher per-vehicle content value. These dynamics are compressing the innovation cycle for domestic and international HVAC suppliers operating in India.

Valeo accelerated its India industrial footprint in February 2026 under the Elevate 2028 strategic plan, operating 6 production sites across Chennai, Pune, Sanand, and Gurgaon. The company entered a 2024 partnership with Atul Greentech and Honda Power Pack to develop EV thermal solutions for Indian three-wheelers.

Subros expanded its HVAC manufacturing footprint in May 2025 with a greenfield plant in Kharkhoda, Haryana, backed by Rs 1.5 billion capex. The company also secured EV HVAC orders from Mahindra BEV and Maruti e-Vitara, targeting new growth segments.

Mahindra launched the XUV 3XO in April 2024, making it the first sub-compact SUV in India to offer dual-zone automatic climate control as standard. The launch demonstrated the accelerating cascade of automatic HVAC systems from premium into mass-market vehicle segments.

Norma Group secured a contract in March 2024 to supply lightweight cooling systems for an Indian electric SUV manufacturer, covering 700,000 EVs through 2030. The deal highlights growing demand for efficient thermal management components in India's expanding electric vehicle segment.

The October 2025 AC mandate for N2 and N3 trucks structurally expanded the India automotive HVAC market by making factory-fitted AC mandatory across all new commercial vehicles. Subros secured Rs 1.5 billion in truck HVAC orders ahead of the mandate.

Automatic climate control is rapidly cascading from premium into mass-market segments across the India automotive HVAC market. In 2018, automatic AC required spending above Rs 20 lakh; by 2024, Mahindra offered dual-zone climate control on the sub-10 lakh XUV 3XO.

EVs are expanding the India automotive HVAC market as heat pump systems replace IC engine compressor-based AC. EV HVAC typically costs 2-3 times more than conventional systems per vehicle, boosting overall supplier revenue per unit as India's EV fleet grows.

India's automotive HVAC market growth is supported by rising vehicle production. According to SIAM, India produced 2.84 crore vehicles in FY2023-24, a 9.62% year-on-year increase, with every passenger car and commercial vehicle built requiring at least one factory-fitted HVAC component.

India's extreme temperatures create structural demand for automotive HVAC systems. Cities like Delhi, Mumbai, and Chennai record temperatures exceeding 40 degrees Celsius for several months annually, making functional HVAC essential rather than optional across India's automotive HVAC market growth trajectory.

The report of Expert Market Research's titled "India Automotive HVAC Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

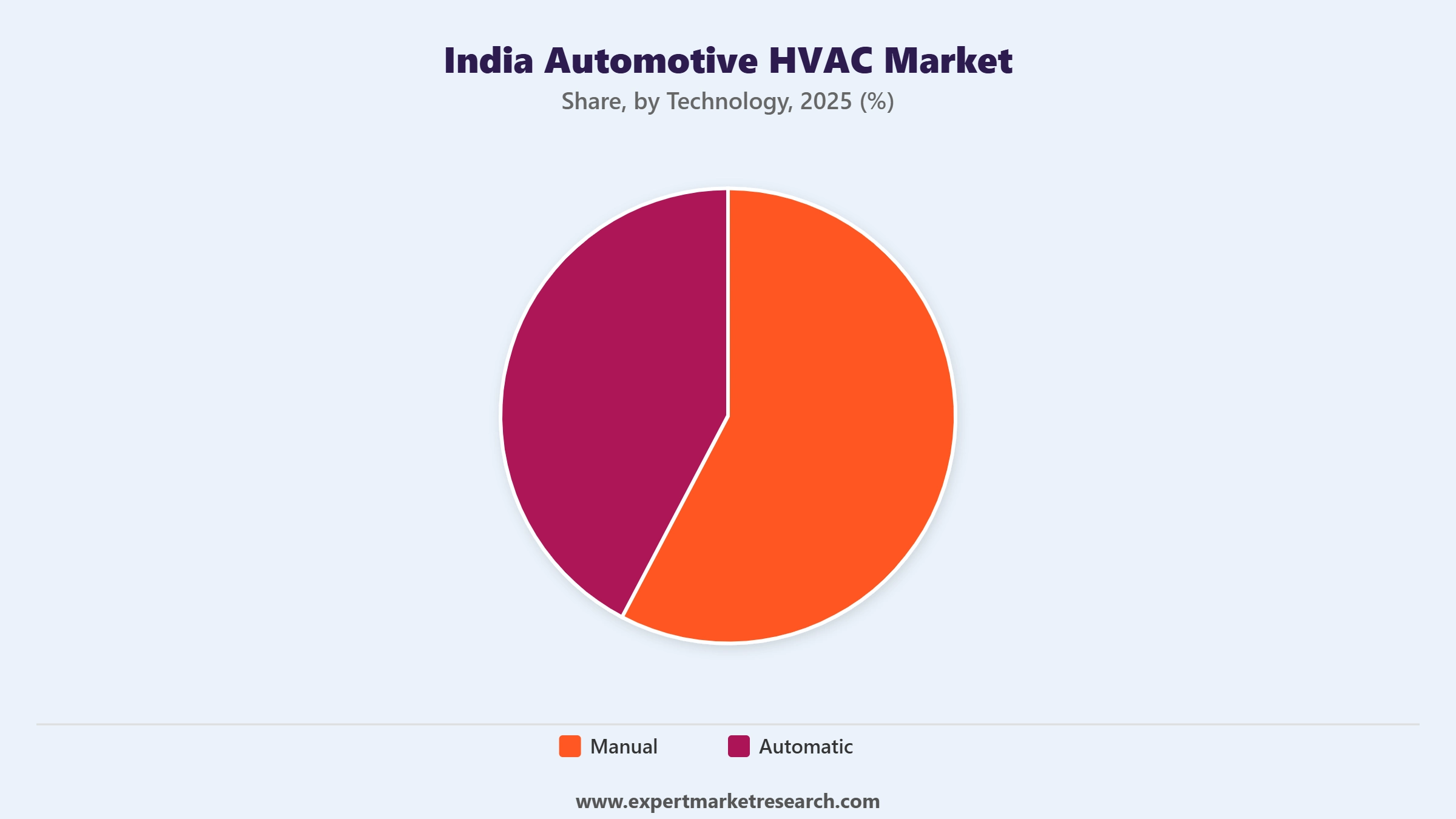

Market Breakup by Technology

Key Insight: Manual HVAC systems hold the dominant volume share in the India automotive HVAC market, as entry-level and lower-mid-range vehicles, which constitute the majority of India's passenger car sales, continue to ship with manual climate control as the standard specification. Manual systems offer cost efficiency and simplicity, making them the default choice for India's price-sensitive mass market. Automatic HVAC systems are the market's primary growth story, expanding at approximately 12.5% CAGR as climate control cascades from luxury vehicles into progressively affordable price segments, driven by OEM competition and rising consumer expectations.

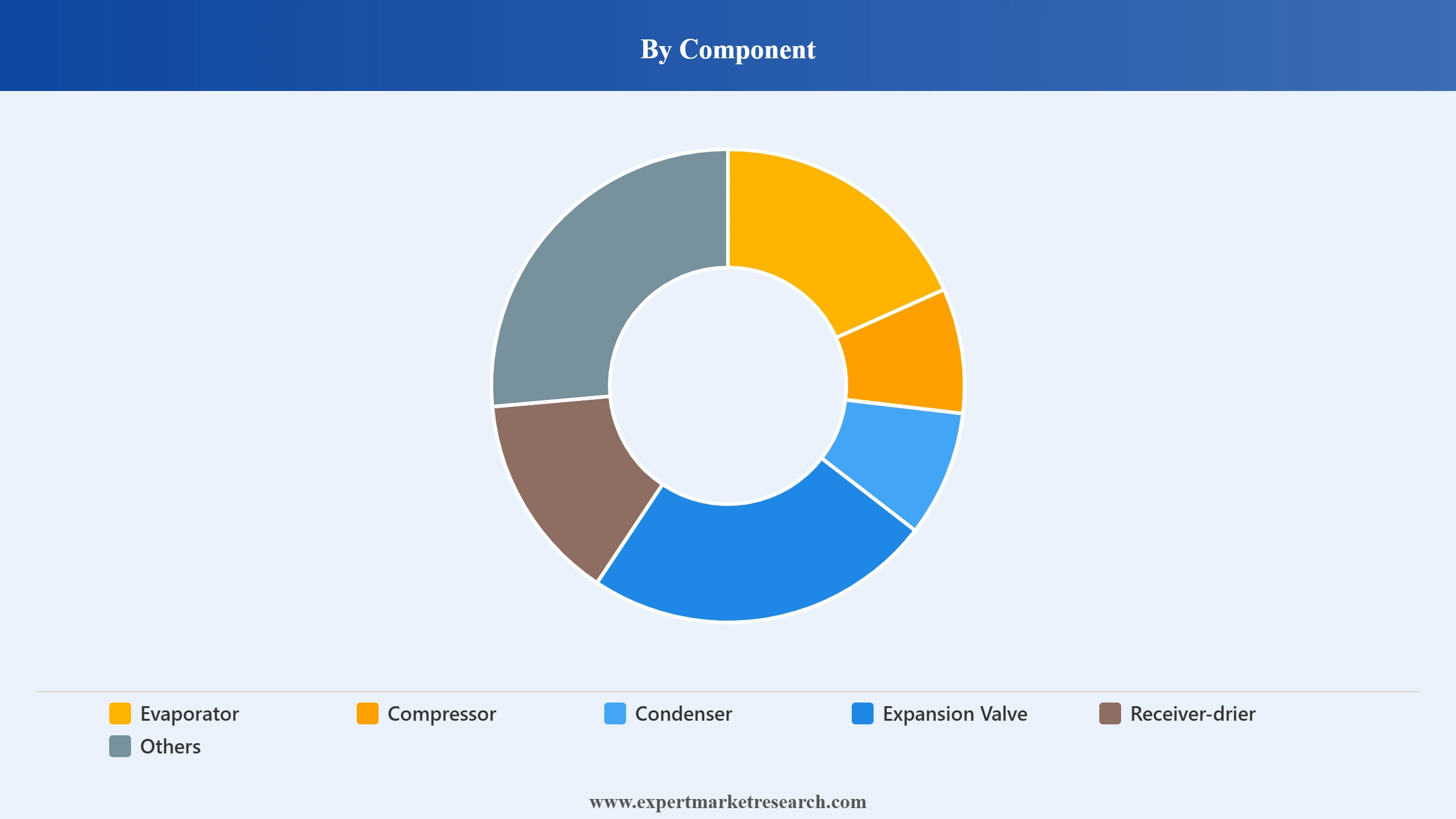

Market Breakup by Component

Key Insight: The condenser holds the leading component share in the India automotive HVAC market, reflecting its critical function in the refrigeration cycle as the component responsible for releasing absorbed heat from the cabin to the atmosphere. Improvements in condenser efficiency, including the adoption of multi-flow and microchannel designs, are enhancing overall HVAC system performance across both passenger and commercial applications. The compressor is the second-highest-value component, with Subros positioning itself as the only domestic compressor manufacturer for passenger cars in India, supplying Maruti Suzuki, Tata Motors, and Mahindra.

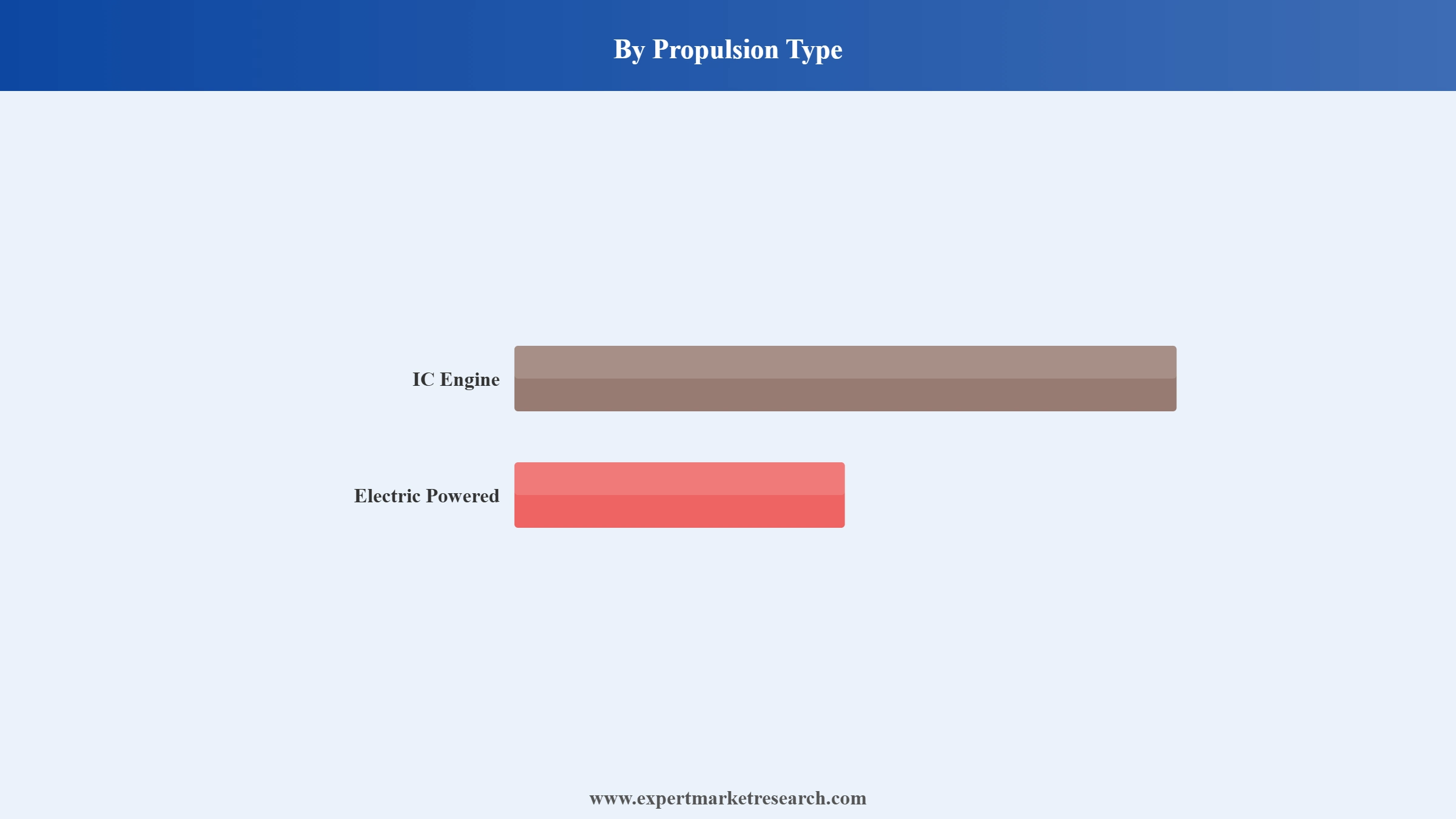

Market Breakup by Propulsion Type

Key Insight: IC engine vehicles dominate the India automotive HVAC market by propulsion type, as the vast majority of India's vehicle fleet runs on petrol or diesel powertrains where conventional compressor-driven AC systems are standard. IC engine HVAC systems benefit from simplicity, cost efficiency, and Subros's well-established local manufacturing capabilities. Electric powered vehicles represent the highest-growth segment, requiring complex heat pump-based thermal systems that manage battery temperature, powertrain heat, and cabin comfort simultaneously, carrying 2-3 times the per-vehicle HVAC revenue of conventional IC engine applications.

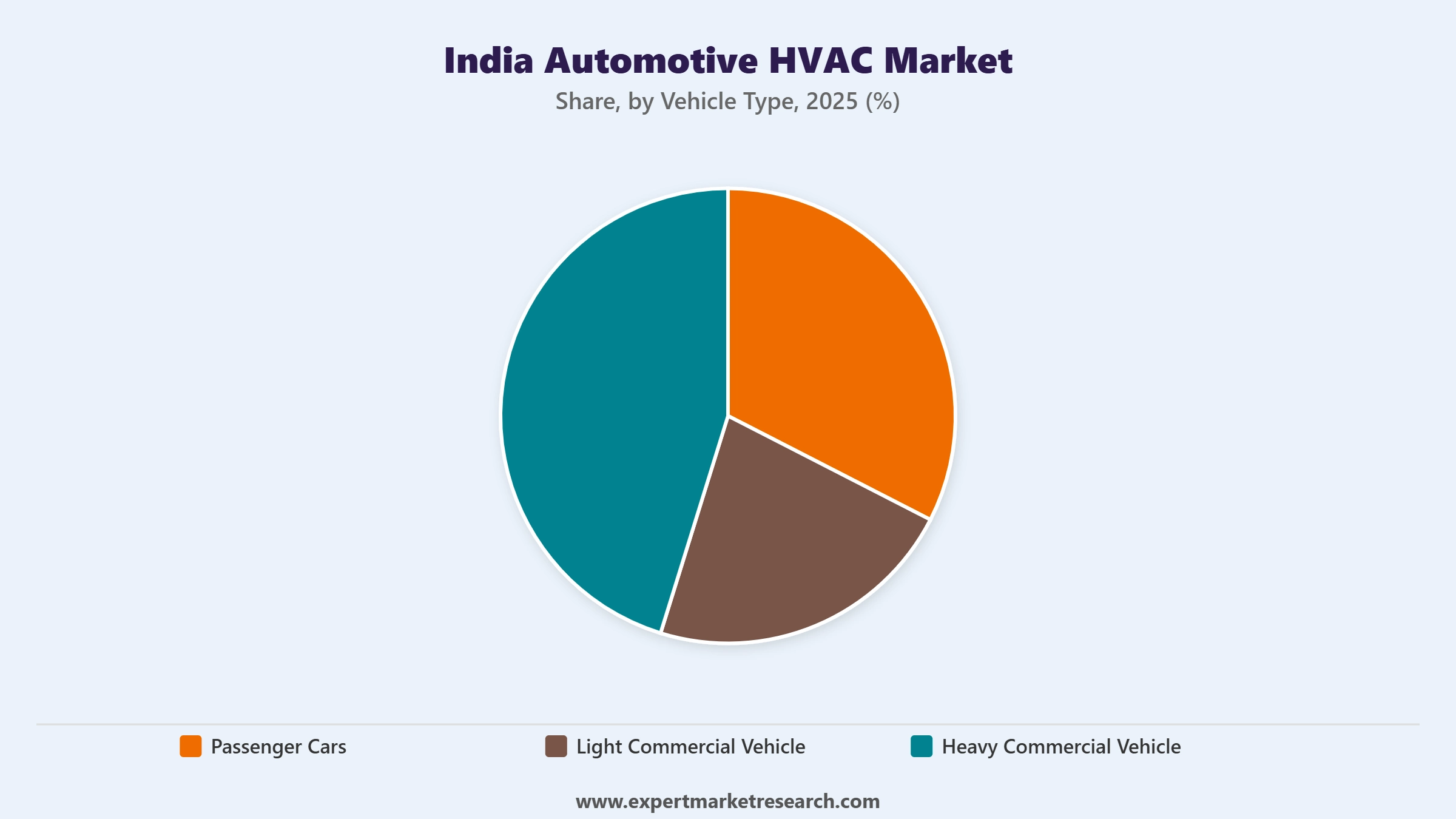

Market Breakup by Vehicle Type

Key Insight: Passenger cars account for the dominant share of the India automotive HVAC market by vehicle type, reflecting the sheer volume of passenger car production in India, which reached 49.01 lakh units in FY2023-24. Every passenger car produced ships with at least a manual HVAC system, making this the most stable and predictable demand base for HVAC suppliers. Heavy commercial vehicles are the fastest-growing segment, driven by the October 2025 AC mandate requiring factory-fitted AC cabins in all new N2 and N3 category trucks, converting AC from an optional to a mandatory fitment across India's entire heavy truck production run.

Market Breakup by Region

Key Insight: North India commands the largest share of the India automotive HVAC market, underpinned by the concentration of India's largest automotive production cluster in the Delhi NCR region, anchored by Maruti Suzuki's Gurgaon and Manesar facilities, and supported by Honda, Hero MotoCorp, and other major OEMs in Haryana and Rajasthan. Subros, the country's largest HVAC supplier, is headquartered in Noida and has major manufacturing plants in the region. South India is growing rapidly, driven by Hyundai and Kia's large-scale production in Chennai. West India is also significant, housing Tata Motors, Mahindra, and Bajaj Auto facilities in Maharashtra.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Technology, manual HVAC systems dominate the market due to their cost efficiency and widespread fitment across India's high-volume entry-level and mid-range passenger vehicles

Manual HVAC systems hold the dominant share of the India automotive HVAC market by technology, reflecting the price sensitivity of India's mass-market passenger car buyers and the prevalence of conventional climate control as the standard specification in vehicles below Rs 10-15 lakh. Maruti Suzuki, India's largest passenger car OEM with over 40% domestic market share, sources manual HVAC components primarily from Subros, whose technology alliance with Denso Japan underpins its product development. The high volume of Maruti's production base in North India makes it the single largest driver of manual HVAC system demand nationally.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Automatic HVAC systems are the fastest-growing segment in the India automotive HVAC market, expanding at approximately 12.5% CAGR as OEMs cascade dual-zone climate control and automatic temperature regulation into progressively accessible price points. In April 2024, Mahindra made dual-zone automatic climate control a standard feature option on the XUV 3XO, the first sub-compact SUV in India to do so, illustrating the speed at which this feature is descending from luxury to near-entry-level vehicles. Automatic systems generate higher revenue per unit and higher margins for HVAC suppliers, making this the commercially critical segment for market participants.

By Component, condensers account for the dominant share of the market due to their critical function in HVAC refrigeration cycles and broad fitment across all vehicle segments

Condensers hold the leading component share in the India automotive HVAC market, reflecting their indispensable role in the refrigeration cycle as the component that releases heat from the cabin into the ambient environment. Advances in condenser technology, including multi-flow aluminium designs and microchannel configurations, are improving heat transfer efficiency and supporting vehicle lightweighting objectives. Subros, India's largest automotive condenser manufacturer, produces multi-flow condensers developed in collaboration with Denso, supplying OEMs including Maruti Suzuki, Tata Motors, and Mahindra.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Compressors represent a high-value component segment within the India automotive HVAC market, with Subros holding a unique position as the only domestic manufacturer of passenger car HVAC compressors in India, producing reciprocating and scroll-type compressors through its Denso technology alliance. The expansion of the electric vehicle segment is creating new demand for electric compressors that operate independently of the engine, requiring different manufacturing capabilities and materials. Evaporators are growing steadily, with multi-flow evaporator designs delivering 15% more efficiency at 50% less weight, supporting India's fuel economy and vehicle lightweighting initiatives.

By Propulsion Type, IC engine vehicles account for the dominant share of the market due to the overwhelming prevalence of petrol and diesel powertrains across India's vehicle fleet

IC engine vehicles account for the dominant share of the India automotive HVAC market, as conventional petrol and diesel powertrains continue to represent the vast majority of new vehicle registrations in India. Conventional HVAC systems in IC engine vehicles rely on the engine-driven compressor, offering a cost-effective and well-understood solution for cabin cooling that India's established supplier base is well positioned to manufacture. The depth of technical knowledge accumulated by domestic suppliers like Subros and Sanden Vikas in IC engine HVAC applications provides a strong competitive foundation for retaining OEM relationships across existing vehicle platforms.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Electric powered vehicles are the highest-growth segment within the India automotive HVAC market, requiring heat pump-based thermal systems that simultaneously manage battery thermal conditioning, cabin comfort, and powertrain heat rejection. EV HVAC systems typically cost 2-3 times more per vehicle than conventional IC engine AC, significantly raising per-unit revenue for capable suppliers. Subros has proactively positioned itself for this transition, securing EV HVAC orders from Mahindra BEV and Maruti Suzuki's e-Vitara programme and announcing the Kharkhoda greenfield plant in May 2025 specifically to support growing EV component demand.

By Vehicle Type, passenger cars account for the dominant share of the market due to high production volumes and near-universal HVAC fitment as a standard feature

Passenger cars command the dominant share of the India automotive HVAC market, driven by the high volume of passenger car production in India, which reached 49.01 lakh units in FY2023-24 per SIAM data. Every passenger car produced ships with at least a manual HVAC system as a standard fitment, providing a consistent and large-scale demand base for component suppliers. The increasing HVAC content per vehicle, as automatic climate control penetrates progressively lower price points, is further expanding the revenue opportunity within the passenger car segment beyond simple volume growth.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Heavy commercial vehicles represent the fastest-growing vehicle type segment in the India automotive HVAC market, propelled by the October 2025 AC mandate requiring all new N2 and N3 category trucks to be fitted with factory-installed AC cabins. This regulation has converted AC from an optional specification in commercial vehicles to a mandatory standard fitment, permanently expanding the addressable market in a segment that previously had minimal factory-fitted HVAC penetration. Light commercial vehicles are also growing, as India's expanding logistics and last-mile delivery fleet increasingly integrates climate-controlled cabins to improve driver conditions and vehicle uptime.

North India dominates the market due to the highest concentration of passenger car OEM production capacity and established HVAC supplier infrastructure in the Delhi NCR and Haryana corridor

North India holds the largest regional share of the India automotive HVAC market, anchored by India's most densely packed automotive production belt spanning Delhi NCR, Gurgaon, Manesar, Neemrana, and Bawal in Haryana and Rajasthan. Maruti Suzuki's Gurgaon and Manesar facilities collectively produce over 20 lakh vehicles annually, driving consistent high-volume HVAC component demand. The concentration of Subros's manufacturing and R&D operations in Noida, combined with the Denso Subros Engineering Centre, creates a technically sophisticated local supply chain that directly supports North India's OEM cluster. The region's extreme summer climate, with temperatures regularly exceeding 45 degrees Celsius, reinforces the critical nature of HVAC performance in vehicles assembled and sold there.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

South India is the fastest-growing regional market in India's automotive HVAC landscape, driven by Hyundai India's 800,000-unit capacity in Sriperumbudur and Kia's growing Anantapur operations, both of which require substantial HVAC content per vehicle. The region's warm and humid climate across Chennai, Bengaluru, and Hyderabad creates natural year-round demand for effective vehicle cooling. In February 2026, Valeo reaffirmed its India strategy by accelerating industrial footprint expansion, with production sites in Chennai and Pune among its key India facilities, reflecting the strategic importance of South and West India to global HVAC suppliers targeting high-volume OEM relationships.

The India automotive HVAC market is moderately concentrated, combining a dominant domestic supplier with a group of global tier-1 companies competing for OEM supply agreements across passenger car, commercial vehicle, and EV segments. Subros, as the only integrated HVAC manufacturer in India with its own compressor production and in-house R&D, holds a structurally advantaged position in the passenger car segment through its deep relationships with Maruti Suzuki and Tata Motors. Global suppliers including Denso, MAHLE, Valeo, and Hanon Systems compete primarily through technical differentiation, particularly in automatic climate control electronics, heat pump technology for EVs, and energy efficiency improvements.

The competitive dynamics are shifting as EV adoption forces traditional suppliers to invest in heat pump design, electric compressor manufacturing, and battery thermal management capabilities. Companies building localised EV HVAC engineering expertise are gaining first-mover advantage in securing long-term supply agreements with India's EV OEMs. The October 2025 truck AC mandate is also creating a new competitive front in commercial vehicle HVAC, where players like Subros and Denso are investing in high-capacity, energy-efficient truck AC systems.

Subros Limited, founded in 1985 and headquartered in Noida, Uttar Pradesh, is India's leading manufacturer of thermal products for automotive applications, operating in technical collaboration with Denso Corporation, Japan, and Suzuki Motor Corporation. The company holds approximately 40% market share in automotive air conditioning systems and is the only domestic compressor manufacturer for passenger cars in India. Subros operates 7 manufacturing plants across Noida, Manesar, Pune, Chennai, Nalagarh, and Karsanpura, serving OEMs including Maruti Suzuki, Tata Motors, Mahindra, Force Motors, and Nissan.

Denso Corporation, founded in 1949 and headquartered in Kariya, Aichi, Japan, is a global leader in automotive thermal, powertrain, electrification, and electronic systems, supplying OEMs worldwide. In India, Denso operates as the primary technology partner of Subros through the Denso Subros Engineering Centre in Noida, providing application design, quality improvement, and component technology for car air conditioning systems. Denso's Everycool commercial vehicle cooling system launched in September 2023 targets truck cabin comfort without engine operation, directly addressing India's commercial vehicle market.

MAHLE GmbH, founded in 1920 and headquartered in Stuttgart, Germany, is a leading global automotive parts manufacturer specialising in thermal management, filtration, and powertrain systems for combustion engines and electric vehicles. In India, MAHLE operates through MAHLE Anand Thermal Systems, a joint venture producing HVAC components for passenger cars and commercial vehicles. MAHLE's corporate strategy, Mahle 2030+, places electrification and thermal management at its core, with the company investing in heat pump and battery thermal management solutions relevant to India's growing EV market.

Valeo, founded in 1923 and headquartered in Paris, France, is a global automotive technology company with a strong focus on electrification, thermal management, and driver assistance systems. In India, Valeo operates 6 production sites across Chennai, Pune, Sanand, and Gurgaon, employing over 7,500 people. Under its Elevate 2028 strategic plan, Valeo is accelerating its India industrial footprint and has entered EV thermal partnerships with Indian three-wheeler manufacturers. Its heat pump technology for electric vehicles, commercialised in European EV programmes, is increasingly relevant to India's EV OEM supply chain.

Other key players in the market are Sanden Vikas (India) Ltd., Hanon Systems, Delphi Technologies, Samvardhana Motherson Group, Air International Thermal Systems, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Gain a decisive advantage in the India automotive HVAC market 2026 with our comprehensive research report. From the truck AC mandate's structural impact and automatic climate control feature cascade to EV thermal management transitions and regional production dynamics, this report delivers the clarity you need. Whether you are planning a supply agreement, evaluating manufacturing investment, or assessing competitive positioning, download your free sample today and explore the key opportunities shaping the future of automotive HVAC in India.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market is projected to grow at a CAGR of 11.20% between 2026 and 2035.

The market is categorised according to the technology, which includes manual and automatic.

The market is categorised according to the vehicle type, which includes passenger cars, light commercial vehicle, and heavy commercial vehicle.

The key players in the market include Subros Limited, Denso Corporation, Sanden Vikas (India) Ltd., MAHLE GmbH, Valeo, Hanon Systems, Delphi Technologies, Samvardhana Motherson Group, Air International Thermal Systems, and Others.

Based on the component, the market is divided into evaporator, compressor, condenser, expansion valve, receiver-drier, and others.

Based on the propulsion type, the market is divided into IC engine and electric powered.

The market is broken down into north India, east and central India, west India, and south India.

In 2025, the India automotive HVAC market reached an approximate value of USD 1.65 Billion.

The market is anticipated to witness robust expansion and attain a value of USD 4.77 Billion by 2035.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Technology |

|

| Breakup by Component |

|

| Breakup by Propulsion Type |

|

| Breakup by Vehicle Type |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.