Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

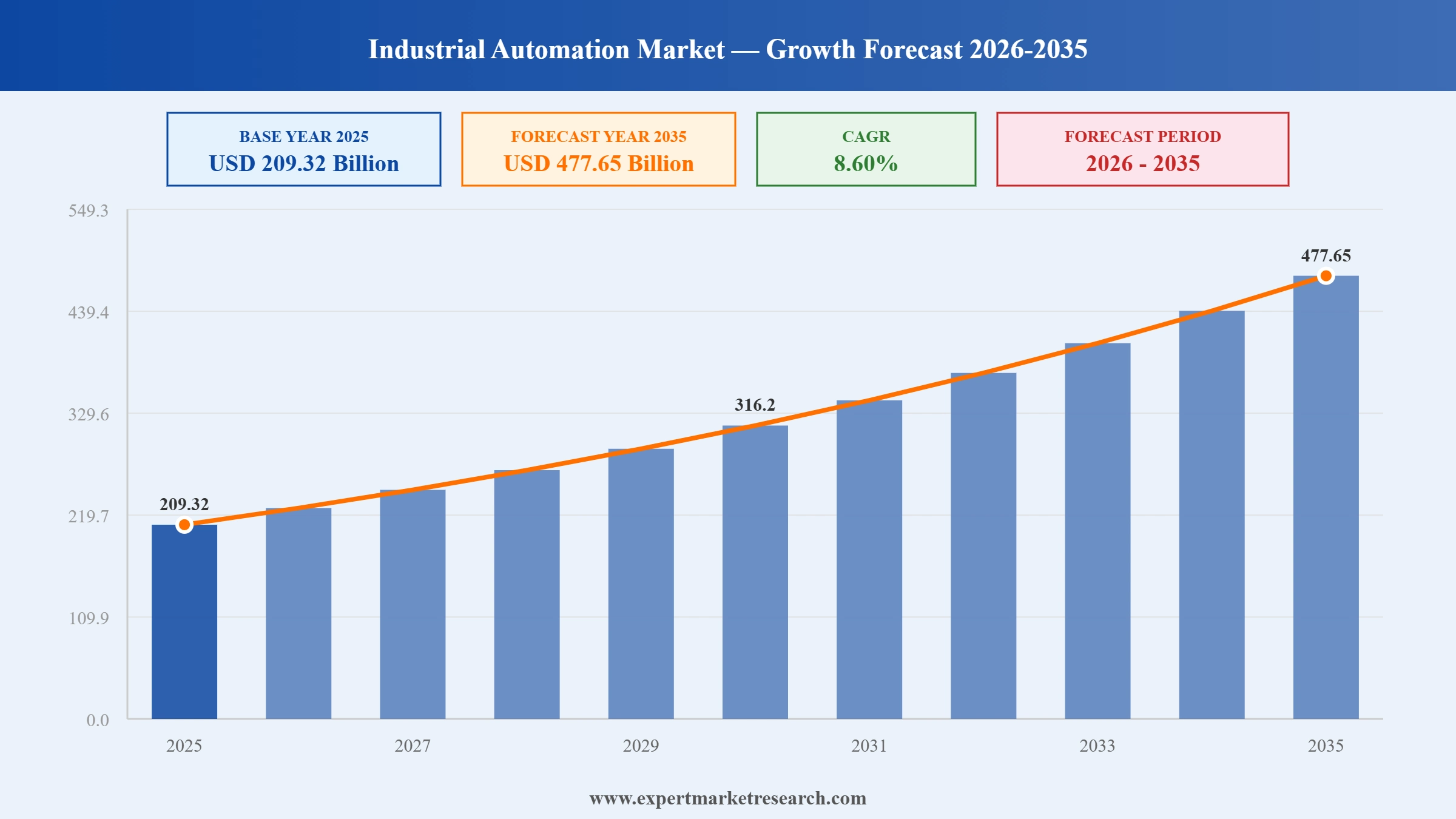

The global industrial automation market attained a value of USD 209.32 Billion in 2025 and is projected to grow at a compound annual growth rate CAGR of 8.60% during the forecast period of 2026-2035, reaching USD 477.65 Billion by 2035. Industrial automation is the usage of control systems including computers, robots, programmable logic controllers, distributed control systems, and information technologies for handling processes and machinery that were previously performed by human operators, delivering greater efficiency, precision, consistency, and cost-effectiveness across manufacturing and industrial operations. The market is being driven by increasing industrialisation, the global adoption of Industry 4.0 frameworks, growing demand for smarter solutions to manage industrial plants, and the accelerating integration of artificial intelligence, machine learning, and the Industrial Internet of Things across production environments.

Industrial automation encompasses a broad ecosystem of hardware, software, and services that collectively enable manufacturing facilities, process plants, utilities, and logistics operations to automate complex workflows, monitor equipment performance in real time, reduce human error, improve safety, and optimise energy consumption. Key automation technologies include supervisory control and data acquisition (SCADA) systems, programmable logic controllers (PLCs), distributed control systems (DCS), human-machine interfaces (HMI), industrial robots, collaborative robots (cobots), machine vision systems, industrial sensors, and motion control equipment, supported by an expanding portfolio of automation software platforms, analytics tools, and connectivity solutions.

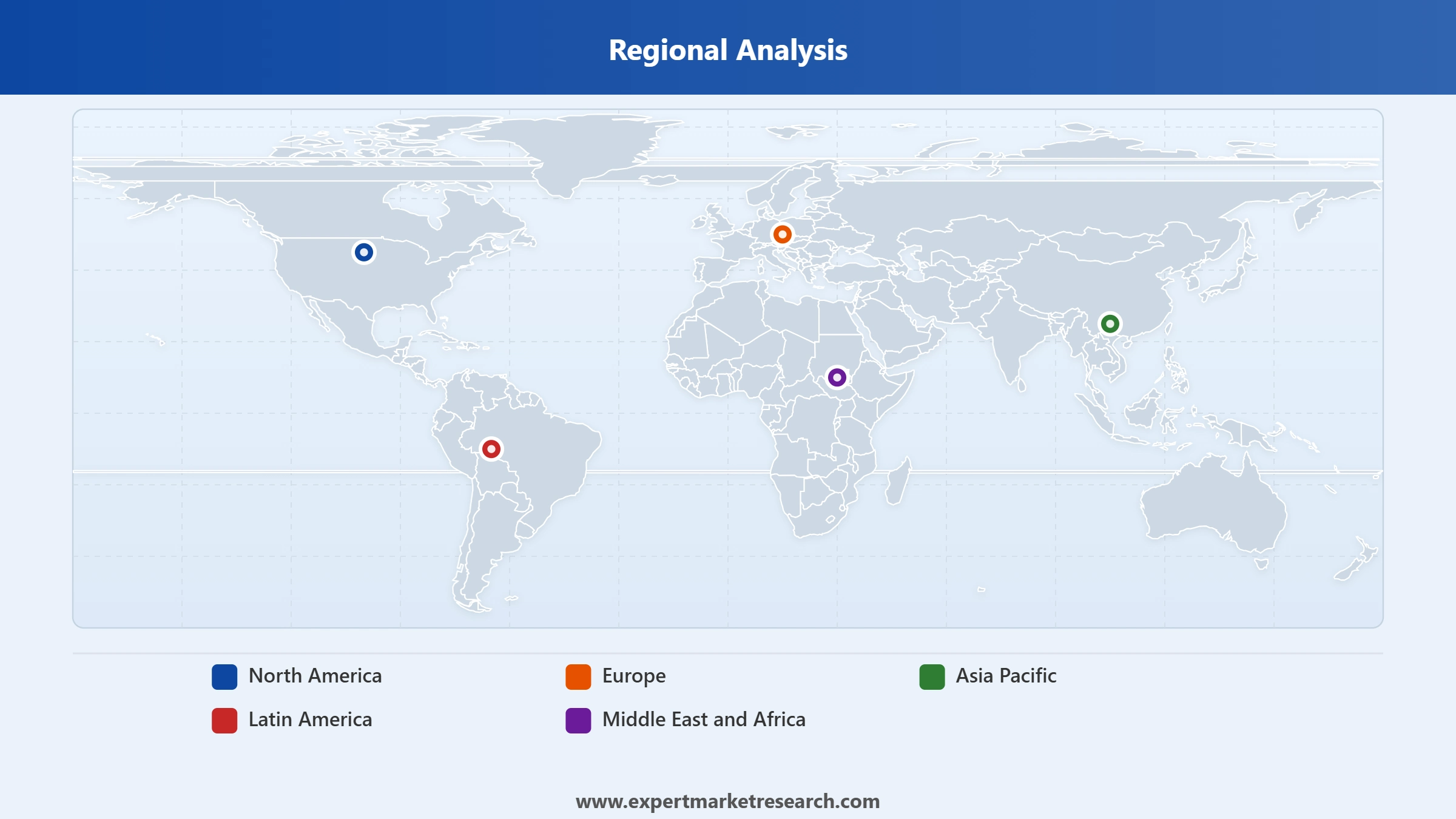

Asia Pacific is the dominant regional market for industrial automation, driven by the presence of large-scale manufacturing operations in China, Japan, South Korea, and India, robust growth of the construction and consumer goods industries, and the production plants of leading automation companies located in the region. North America holds the second-largest regional share, supported by increasing adoption of factory automation systems across US and Canadian manufacturing sectors, significant IoT research and development investment, and government initiatives promoting advanced manufacturing and smart factory development. Europe represents the third-largest market, with Germany, France, and the UK as the leading national markets characterised by sophisticated industrial automation adoption across automotive, aerospace, food and beverage, and pharmaceutical manufacturing.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The industrial automation market encompasses the global commercial ecosystem of manufacturers, technology providers, system integrators, and service companies that design, develop, install, and maintain automation systems for industrial operations. Industrial automation spans two primary operational categories: discrete automation, which involves the production of distinct, countable items such as automobiles, electronics, and packaged goods through assembly-line and machine-tending processes; and process automation, which governs continuous or batch production of products such as chemicals, oil and gas, pharmaceuticals, and food and beverage where materials flow through pipelines, reactors, and vessels under controlled conditions.

Industrial automation is distinguished from other forms of automation by its focus on physical production environments, heavy machinery, and safety-critical operational contexts, requiring ruggedised hardware, real-time control architectures, and industrial-grade cybersecurity frameworks. The market is closely linked to the broader digital transformation of manufacturing under Industry 4.0 and its successors, with automation increasingly integrated with data analytics, cloud computing, artificial intelligence, and edge computing to create intelligent, adaptive, and self-optimising production environments. Key performance metrics for industrial automation systems include production throughput, overall equipment effectiveness (OEE), mean time between failures (MTBF), energy efficiency, yield rate, and total cost of ownership.

The global adoption of Industry 4.0 frameworks integrating cyber-physical systems, IoT connectivity, big data analytics, and cloud computing into manufacturing operations is the foundational structural driver of industrial automation market growth. Government-backed smart manufacturing programs in Germany, Japan, China, South Korea, and the United States are funding automation adoption across SME and large enterprise manufacturing sectors, with specific incentive programs targeting energy efficiency, productivity enhancement, and carbon reduction through automation investment. The progression toward Industry 5.0, emphasising human-machine collaboration and sustainable production, is further expanding the application of collaborative automation solutions in manufacturing environments.

Structural labour shortages across manufacturing sectors in developed economies and rising labour costs in previously low-cost manufacturing geographies are accelerating the business case for industrial automation investment. According to the International Federation of Robotics, manufacturers with higher robot density consistently demonstrate superior productivity, quality consistency, and export competitiveness. The post-COVID restructuring of global supply chains, with significant reshoring and nearshoring of manufacturing activity to North America and Europe, is creating additional demand for automation as manufacturers seek to maintain cost competitiveness in higher-wage markets through technology substitution.

The integration of Industrial IoT sensor networks, machine learning algorithms, and advanced analytics into automation systems is creating a new generation of intelligent automation that moves beyond pre-programmed rule execution toward adaptive, self-optimising operational behaviour. AI-powered quality inspection systems using machine vision and deep learning are replacing manual inspection in electronics, automotive components, and pharmaceutical manufacturing. Predictive maintenance algorithms trained on equipment sensor data are dramatically reducing unplanned downtime. Generative AI tools for PLC programming and automation system design are reducing engineering time and expanding the pool of engineers capable of deploying sophisticated automation solutions.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

National industrial policies across major economies are creating direct demand pull for industrial automation investment. The US CHIPS and Science Act, Germany's National Industry Strategy 2030, China's Made in China 2025 successor programs, Japan's Society 5.0 initiative, and India's Production Linked Incentive (PLI) scheme across electronics and automotive manufacturing collectively represent trillions of dollars in manufacturing investment over the forecast period, a significant proportion of which will be spent on automation systems, robotics, and digital manufacturing infrastructure.

Escalating quality standards across automotive, aerospace, semiconductor, pharmaceutical, and food and beverage manufacturing driven by tightening regulatory requirements, OEM quality specifications, and consumer expectations are making human-only production processes inadequate for consistent compliance. Automation systems provide the repeatability, precision, and data traceability required to meet these standards at scale. The semiconductor industry's expansion of chip fabrication capacity globally, with cleanroom environments requiring sub-micron precision, is a particular demand catalyst for high-precision industrial automation systems.

Artificial intelligence is transitioning from an adjacent technology to a core component of industrial automation systems, embedded in quality inspection, predictive maintenance, production scheduling, energy optimisation, and autonomous material handling. At Hannover Messe 2026, Siemens and NVIDIA jointly demonstrated AI-native automation architectures in which large language models and physics simulation engines collaborate to train autonomous industrial robots without the need for explicit programming. This paradigm shift from deterministic programmed automation to adaptive AI-driven automation represents the most significant technical evolution in the market since the introduction of PLCs in the 1970s.

The deployment of 5G private networks, Wi-Fi 6E, and proprietary industrial wireless protocols across manufacturing facilities is enabling a new generation of wireless automation applications including mobile autonomous guided vehicles (AGVs), wireless sensor networks for real-time equipment monitoring, and flexible automation cells that can be reconfigured without cable infrastructure changes. Private 5G deployment at automotive and electronics manufacturing facilities in Germany, Japan, South Korea, and the United States is enabling ultra-reliable, low-latency wireless automation at the scale required for production-critical applications.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The traditional boundary between discrete and process automation is blurring as unified automation platforms capable of managing both assembly-line and continuous process operations reduce the total cost of automation infrastructure and simplify system integration. Hybrid manufacturing environments combining discrete assembly with process operations such as electric vehicle battery production, which integrates continuous electrode coating processes with discrete cell assembly and pack integration are driving demand for unified automation architectures that span both operational paradigms.

Factory automation and assembly automation are the highest-volume application segments within the market, encompassing robotic assembly, material handling, welding, painting, inspection, and packaging across automotive, electronics, food and beverage, and consumer goods manufacturing. The electrification of the automotive industry is creating a structural shift in factory automation demand, with EV battery manufacturing requiring new automation capabilities including electrode processing, cell formation, and module assembly that are distinct from traditional internal combustion engine powertrain production.

Collaborative robots designed to operate safely alongside human workers without safety caging are the fastest-growing product category within industrial automation, growing at a CAGR of 36.40% through 2035. Cobots are expanding automation access to SME manufacturers and flexible production environments where traditional industrial robots are impractical due to space, cost, or operational flexibility constraints. AI-enhanced cobots with advanced force sensing, vision guidance, and natural language programming interfaces are addressing a wider range of assembly, quality inspection, and material handling tasks than first-generation cobot platforms.

The global industrial automation market faces significant challenges rooted in cybersecurity vulnerabilities, technology complexity, and workforce skills gaps. The convergence of operational technology (OT) and information technology (IT) networks in Industry 4.0 environments creates expanded attack surfaces for industrial cyber threats, with ICS-CERT reporting a sustained increase in cyberattacks targeting industrial control systems across critical infrastructure sectors. High upfront capital investment requirements for automation systems particularly for SME manufacturers in emerging economies create adoption barriers that limit the addressable market in the near term. The shortage of qualified automation engineers, PLC programmers, and systems integrators in many markets creates project execution constraints that delay automation deployment timelines and elevate service costs.

Structural restraints moderate the pace of market expansion. Legacy manufacturing infrastructure in established industrial economies creates integration complexity and retrofit cost barriers that slow automation adoption in existing facilities compared to greenfield installations in emerging markets. Supply chain concentration in automation hardware manufacturing particularly for semiconductors, servo drives, and precision sensors creates lead time and availability risks that complicate large-scale automation project execution. Trade policy uncertainty and semiconductor export controls affecting automation equipment supply chains create business planning complexity for global manufacturers executing multi-year automation investment programs.

Despite these challenges, the industrial automation market presents compelling and expanding growth opportunities. The automation of services, logistics, and retail beyond traditional manufacturing represents a large and partially untapped extension of the addressable market, with warehouse automation, autonomous mobile robots, and automated quality inspection systems expanding industrial automation technology into sectors that have historically operated with minimal automation investment. The energy transition is creating substantial new automation demand across renewable energy manufacturing, hydrogen production, grid management, and battery manufacturing, with these sectors requiring sophisticated automation capabilities for which existing industrial automation technology is well positioned. The full Expert Market Research Industrial Automation Market Report and Forecast 2025-2035 provides granular analysis across automation type, component, industry, and region to support manufacturers, investors, system integrators, and technology vendors in identifying and capitalising on the most valuable growth vectors in this large and rapidly evolving global market.

The EMR’s report titled “Industrial Automation Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

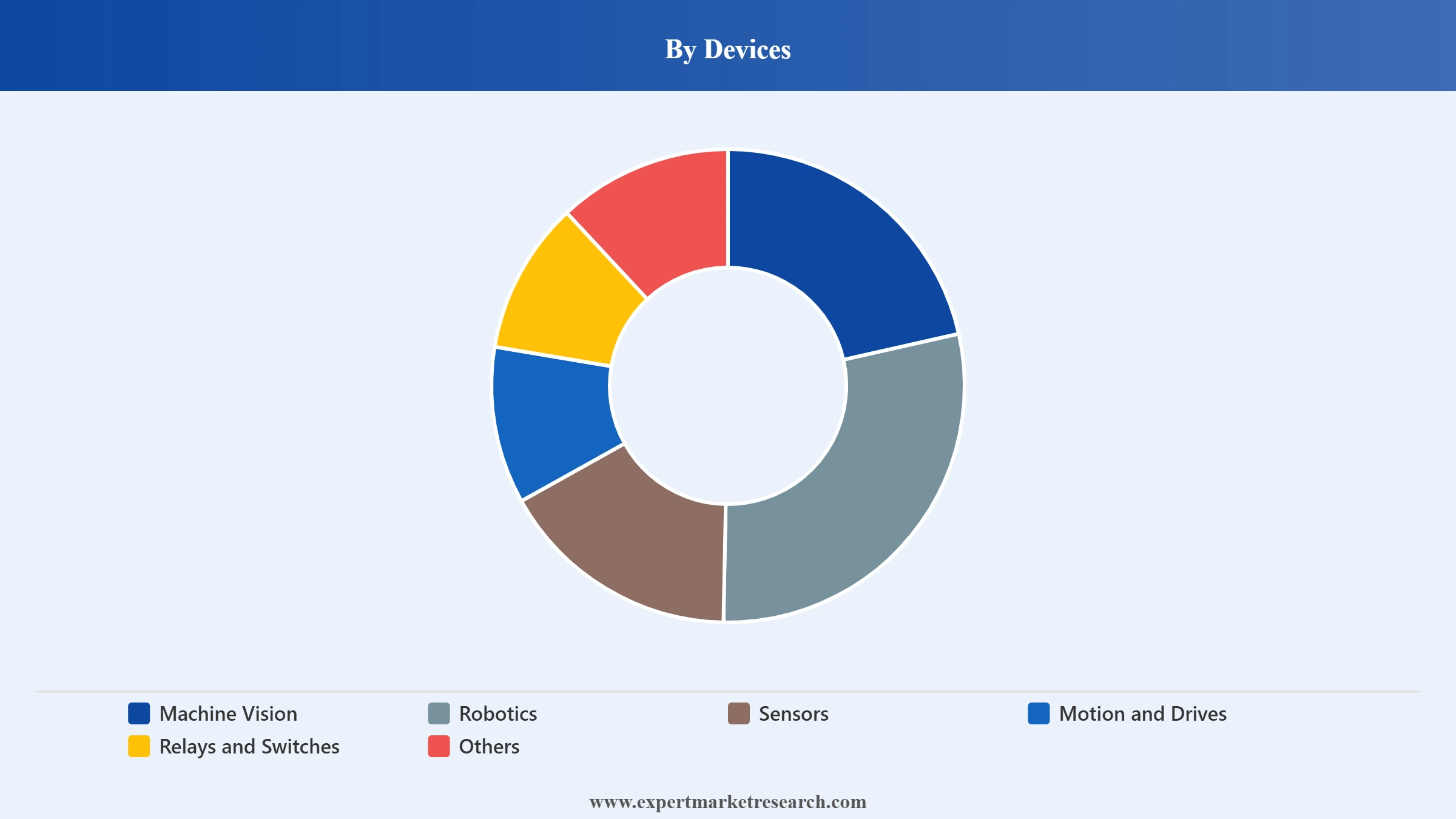

Market Breakup by Devices

Key Insight: The industrial automation market is segmented by devices into machine vision, robotics, sensors, motion and drives, relays and switches, and others. Machine vision systems enable automated quality inspection and defect detection across electronics, automotive, and pharmaceutical manufacturing. Robotics represent the highest-value device segment, encompassing industrial robots, collaborative robots, and autonomous mobile robots across assembly, welding, and material handling. Sensors provide real-time data on temperature, pressure, flow, and vibration enabling intelligent process control and predictive maintenance. Motion and drives govern the precise movement of automated machinery across production lines, while relays and switches provide critical switching and protection functions across electrical automation infrastructure.

Market Breakup by Control System

Key Insight: The market is categorised by control system into SCADA, DCS, PLC, MES, PLM, ERP, HMI, and others. SCADA systems provide real-time supervisory monitoring across distributed industrial assets including pipelines, utilities, and energy infrastructure. Distributed control systems govern continuous process operations in oil and gas, chemicals, and power generation. PLCs are the most widely deployed control platform across discrete and hybrid manufacturing environments. MES bridges shop floor automation with enterprise planning through real-time production tracking and quality management. PLM and ERP platforms integrate automation data with broader business processes, while HMI systems provide the operator interaction layer across all automation architectures.

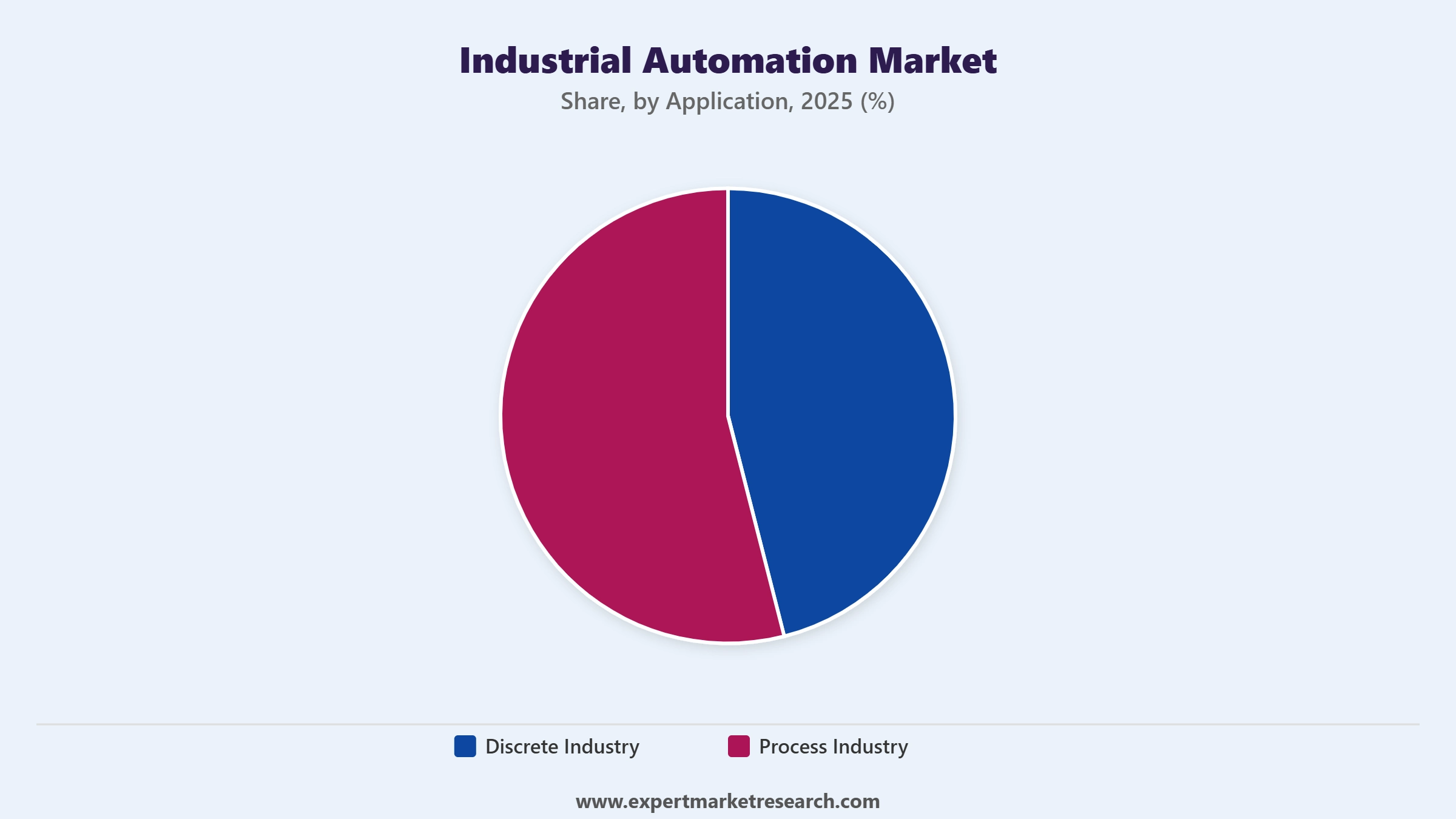

Market Breakup by Application

Key Insight: The industrial automation market is segmented by application into discrete industry and process industry. The discrete industry segment covers automation of manufacturing operations producing distinct, countable items including automotive components, electronics, aerospace structures, and consumer goods through assembly lines, robotic work cells, and machine-tending processes. The process industry segment encompasses automation of continuous or batch production across oil and gas, chemicals, pharmaceuticals, food and beverage, and power generation, where precise control of flow, temperature, pressure, and composition is critical to product quality, safety, and regulatory compliance.

Market Breakup by Region

Key Insight: Asia Pacific is leading the industrial automation market, driven by rapid industrialization, urbanization, and strong manufacturing hubs. China is aggressively investing in smart factories, robotics, and AI-integrated systems. As of February 2025, China established more than 30,000 basic-level smart factories as part of a nationwide initiative to fast-track industrial digitalization and intelligent transformation. Japan’s leadership in robotics and South Korea’s automation in electronics manufacturing further boost the region. India's push for digital manufacturing is also transforming its industrial base. This growing demand for automation makes Asia Pacific the fastest-growing regional segment.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America is the second-largest regional market for industrial automation, with the United States accounting for the dominant share of regional revenue. The United States industrial automation market benefits from a large and technology-forward manufacturing base across automotive, aerospace, electronics, pharmaceuticals, and food and beverage sectors, combined with significant government investment in advanced manufacturing through the CHIPS and Science Act, Manufacturing USA institutes, and the USMCA trade framework creating integrated North American supply chain automation investment. US industrial automation services encompassing system integration, MRO, and software support are the largest and fastest-growing services category in the North American market. Canada is the second-largest national market, with automation adoption growing in automotive assembly, resource extraction, and food processing. Mexico is the third-largest national market in the Americas and a significant automation market in its own right, driven by its role as a nearshoring destination for automotive, electronics, and aerospace manufacturing from the United States and Asia.

Europe is the third-largest regional market globally for industrial automation, with Germany as the dominant national market and home to some of the world's most sophisticated industrial automation deployments across automotive OEMs, machine tool manufacturers, and chemical industry operators. Siemens, Bosch, Festo, and Beckhoff all German companies are among the world's leading automation technology providers, supporting a deep and technologically advanced domestic automation ecosystem. The United Kingdom and France are the second and third-largest European markets, with the UK facing post-Brexit supply chain realignment creating new automation investment demand, and France benefiting from government-backed reindustrialisation programs across aerospace, defence, and energy sectors. The EU Taxonomy for Sustainable Finance and Carbon Border Adjustment Mechanism are creating regulatory pull for energy-efficient automation investment across European manufacturing.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific is the largest and fastest-growing regional market for industrial automation, accounting for the majority of global market revenue and the bulk of new robot installations annually. China is the dominant national market, with a massive and rapidly automating manufacturing sector, government-backed industrial automation investment programs, and growing domestic automation technology vendors competing with international suppliers. Japan is the world leader in industrial robot manufacturing producing approximately 46% of global robot output and maintains one of the highest robot density rates per manufacturing worker globally. South Korea has the world's highest robot density per 10,000 manufacturing workers, driven by its electronics and semiconductor manufacturing clusters. India is the fastest-growing major economy in the Asia Pacific automation market, with PLI schemes across electronics, pharmaceuticals, automotive, and food processing creating new automation demand from both domestic manufacturers and international companies establishing Indian production operations.

Latin America is a growing and increasingly significant market for industrial automation, with Mexico as the dominant national market driven by its position as a major nearshoring destination for automotive, aerospace, and electronics manufacturing. Mexico's industrial automation services market is particularly active, with significant system integration and MRO demand from foreign-owned manufacturing facilities in automotive clusters in Monterrey, Puebla, and Guanajuato. Argentina is an emerging automation market with growing adoption in food processing, petrochemicals, and agricultural equipment manufacturing. Brazil is the largest domestic consumer market in Latin America, with automation demand driven by its automotive manufacturing sector, expanding food and beverage industry, and government policies promoting industrial modernisation.

The Middle East and Africa represent a developing but fast-accelerating market for industrial automation, with GCC countries particularly Saudi Arabia and UAE driving demand through Vision 2030, Vision 2071, and comparable industrial diversification programs that are investing heavily in oil and gas automation, petrochemical plant upgrades, smart city manufacturing zones, and renewable energy infrastructure. Saudi Arabia's industrial automation sensors and control systems market is a particular growth area, supported by ARAMCO's downstream diversification and NEOM's automated manufacturing facility development. Africa remains at an early adoption stage for advanced industrial automation, with South Africa, Egypt, and Morocco representing the most developed national markets.

The global industrial automation market is served by a concentrated group of large multinational technology conglomerates, specialist automation vendors, and a growing tier of software-focused and AI-native companies. The competitive landscape is shaped by portfolio breadth across hardware, software, and services, strength of channel and system integrator networks, industrial domain expertise across key end-use industries, and investment in AI, cloud connectivity, and digital twin capabilities.

Founded in 1847, Siemens AG is headquartered in Munich, Germany and is a global leader in industrial automation and digitalization. Siemens has pioneered technologies like the Digital Twin and MindSphere, its cloud-based IoT platform. The firm’s innovations drive smart manufacturing, energy efficiency, and seamless integration of hardware and software solutions.

Established in 1890 and based in St. Louis, the United States, Emerson Electric Co. excels in automation solutions and commercial technologies. Emerson is recognized for its Plantweb digital ecosystem and DeltaV distributed control systems, enabling real-time analytics, process optimization, and enhanced operational reliability in industries worldwide.

ABB Ltd., formed in 1988 via the merger of ASEA and BBC, is headquartered in Zurich, Switzerland and is renowned for its advances in robotics, electrification, and industrial automation. ABB's innovative offerings include ABB Ability™, a suite of digital solutions supporting predictive maintenance, energy monitoring, and performance improvement.

Rockwell Automation, Inc., founded in 1903 and based in Milwaukee, the United States, is a prominent player in industrial automation and information technology. Known for its Allen-Bradley and FactoryTalk brands, Rockwell delivers smart manufacturing systems, IIoT solutions, and integrated control systems to drive industrial productivity and digital transformation.

The global industrial automation market features a competitive landscape of multinational technology conglomerates, specialist automation vendors, and semiconductor providers, shaped by product breadth, system integration capability, and investment in AI and digital connectivity.

Mitsubishi Electric Corporation is a leading provider of factory automation systems, PLCs, servo systems, and industrial robots, with a dominant position across Asia Pacific through its widely deployed MELSEC PLC platform and MELFA robot series. Schneider Electric SE offers its EcoStruxure architecture spanning process control, SCADA, MES, and energy optimisation, with its Modicon PLC range and Aveva software portfolio positioning the company as a comprehensive automation and industrial software provider across manufacturing and process industries. Texas Instruments Incorporated supplies the critical semiconductor components including microcontrollers, motor drivers, and industrial communication chips that underpin PLCs, servo drives, and factory automation equipment manufactured by leading automation vendors globally.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Discover the latest industrial automation market trends 2026 with our comprehensive report. Download your free sample now to access detailed forecasts, competitive analysis, and emerging technology insights. Stay ahead in the rapidly evolving automation landscape by leveraging trusted data and expert perspectives. Don’t miss out on crucial market opportunities—get your report today!

Upto 15% Off

USD

$3999 $3599

$2499 $2249

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 209.32 Billion.

The market is projected to grow at a CAGR of 8.60% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach USD 477.65 Billion by 2035.

The key strategies driving the market include investing in AI and IoT innovations, forming strategic partnerships, and pursuing mergers to expand capabilities. Companies focus on customizable, energy-efficient solutions, digital transformation with cloud and analytics, and strong after-sales services. Geographic expansion into emerging markets also drives growth and competitiveness.

The trends in the market include the rising demand for precise production and high-quality automation control system and the emerging technologies like AR and VR.

The major regions in the market are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific.

Machine vision, robotics, sensors, motion and drives, and relays and switches, among others are the leading devices in the market.

Supervisory Control and Data Acquisition (SCADA), Distributed Control System (DCS), Programmable Logic Controller (PLC), Manufacturing Execution System (MES), Product Lifecycle Management (PLM), Enterprise Resource Planning (ERP), and Human Machine Interface (HMI), among others are the significant control systems in the market.

Discrete industry and process industry are the two major applications. Discrete industry can be further divided into automotive, packaging, food processing, and textile, among others. Process industry is further categorised into chemical, power, oil and gas, healthcare and pharma, and plastic, among others.

The key players in the market report include Siemens AG, Emerson Electric Co., ABB Ltd., Rockwell Automation, Inc., Mitsubishi Electric Corporation, Schneider Electric, and Texas Instruments Incorporated, among others.

Robotics is the most dominant segment in the market, revolutionizing manufacturing processes across sectors.

The industrial automation services market encompasses system integration, engineering design, MRO services, software subscription, field maintenance, and managed automation services. It is the fastest-growing and highest-margin segment within industrial automation, driven by growing manufacturer reliance on specialised service providers for the design, deployment, and management of complex automation systems.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Devices |

|

| Breakup by Control System |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.