Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

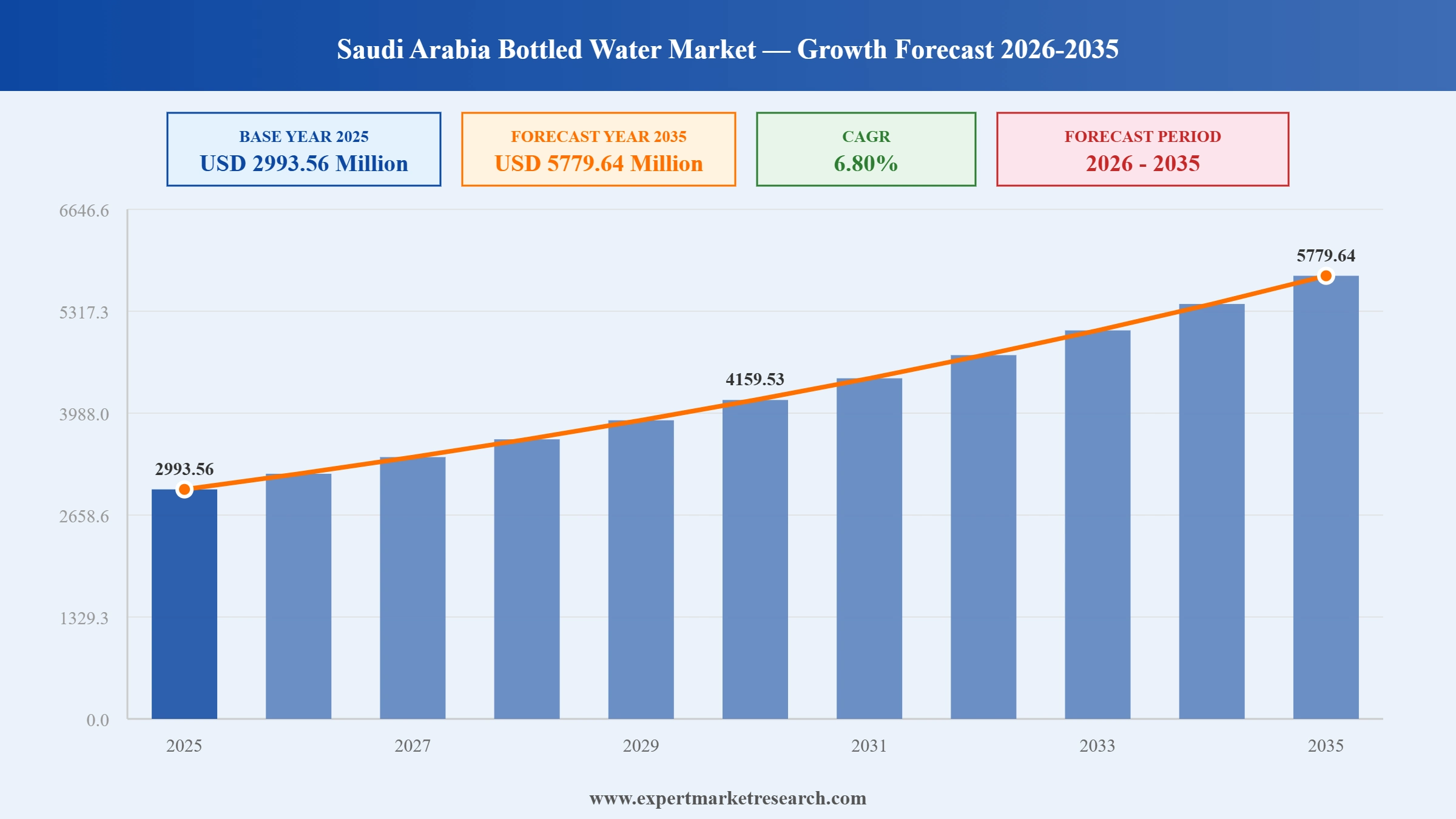

The Saudi Arabia bottled water market reached a value of USD 2993.56 Million at 2025 and is projected to expand at a CAGR of around 6.80% during the forecast period of 2026-2035. With the Kingdom's arid climate and limited freshwater reserves sustaining inescapable hydration demand, rapid growth in HORECA and healthcare sector procurement, rising tourism arrivals driven by Vision 2030 giga-projects and religious pilgrimage, and growing consumer awareness of water quality and safety, the market is expected to reach USD 5779.64 Million by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Saudi Arabia bottled water market rests on a structurally inescapable demand foundation: an arid climate, limited freshwater infrastructure, and a population that relies on bottled water as its safe hydration staple. Vision 2030 is transforming this baseline into a growth opportunity by expanding HORECA capacity, attracting international tourism, and building a domestic hospitality ecosystem that generates consistent incremental demand. Sustainability regulations and packaging innovation are reshaping the supply side as bottlers balance operational compliance with commercial efficiency.

In April 2026, Nova Water deployed AI-powered sensors across its Saudi Arabia bottled water production facilities for real-time quality monitoring. The smart factory system achieves zero contamination standards and raises consumer trust in the premium segment, demonstrating how domestic Saudi bottled water producers are leveraging technology to differentiate on product reliability, food safety assurance, and operational efficiency.

In December 2025, Naqi Water Company amended its Riyadh factory production line contract, upgrading the scope from one to two independent production lines at a revised total contract value of SAR 42.32 million. Each line carries a capacity of 60,000 bottles per hour, bringing the facility's total output to 120,000 bottles per hour and adding approximately 700 million bottles of annual capacity to the Saudi Arabia bottled water market.

In July 2025, Naqi Water Company signed a SAR 37.7 million contract with Middle East Factory for Machines Co. to supply a new bottled water production line for its upcoming Riyadh factory. The self-financed facility will add approximately 700 million bottles of annual capacity under normal operating conditions, with financial impact expected from the fourth quarter of 2026, directly addressing rising demand in the Saudi Arabia bottled water market.

In June 2025, Saudi food and beverage giant Almarai agreed to acquire Pure Beverages Industry Co., producer of the Ival and Oska bottled water brands, for USD 277 million. The acquisition expands Almarai's beverage portfolio into bottled water and leverages its extensive domestic distribution network to scale the brands' market reach, reinforcing consolidation among major Saudi Arabia bottled water market players.

Saudi Arabia’s extreme heat and prolonged dry seasons create a non-seasonal, year-round demand floor for bottled water. Average temperatures above 40 degrees Celsius for extended summer periods, combined with an outdoor labour workforce and millions of religious pilgrims, generate inescapable institutional procurement demand that provides stable revenue visibility for producers and distributors throughout the Saudi Arabia bottled water market.

The Vision 2030 programme is fundamentally expanding Saudi Arabia's hospitality, entertainment, and tourism sectors, with giga-projects including NEOM, the Red Sea Project, Diriyah, and Qiddiya collectively representing hundreds of billions of riyals in hotel, restaurant, and entertainment venue development. Each new HORECA property becomes a recurring large-volume bottled water procurement account, making Vision 2030 the single most important structural demand multiplier for the Saudi Arabia bottled water market.

Home and office delivery of 5-litre to 20-litre water dispensers is the fastest-growing distribution channel in the Saudi Arabia bottled water market, driven by increasing household hygiene awareness, convenience preference, and the affordability of subscription delivery models. Digital platforms and mobile apps are enabling same-day delivery scheduling, growing recurring order rates, and supporting the migration of household consumption from retail channels to reliable subscription delivery arrangements.

Bottled water producers in Saudi Arabia are investing in lightweight packaging technologies that reduce plastic weight per bottle by an average of 27%, cutting both material costs and compliance exposure ahead of the 2035 recycling mandate. Innovative formats including biodegradable caps, aluminium cans for premium sparkling water, and refillable carboys for office delivery are diversifying the packaging ecosystem and expanding addressable consumer segments within the Saudi Arabia bottled water market.

The annual Hajj and Umrah pilgrimage seasons create predictable, large-volume bottled water demand surges requiring dedicated supply chain planning from producers. Millions of pilgrims arriving in Makkah and Madinah require safe, accessible hydration, making religious tourism a structurally important demand driver. Producers with established HORECA and institutional distribution networks in the western region are best positioned to capture this recurring revenue opportunity in the Saudi Arabia bottled water market.

The Expert Market Research's report titled “Saudi Arabia Bottled Water Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Type

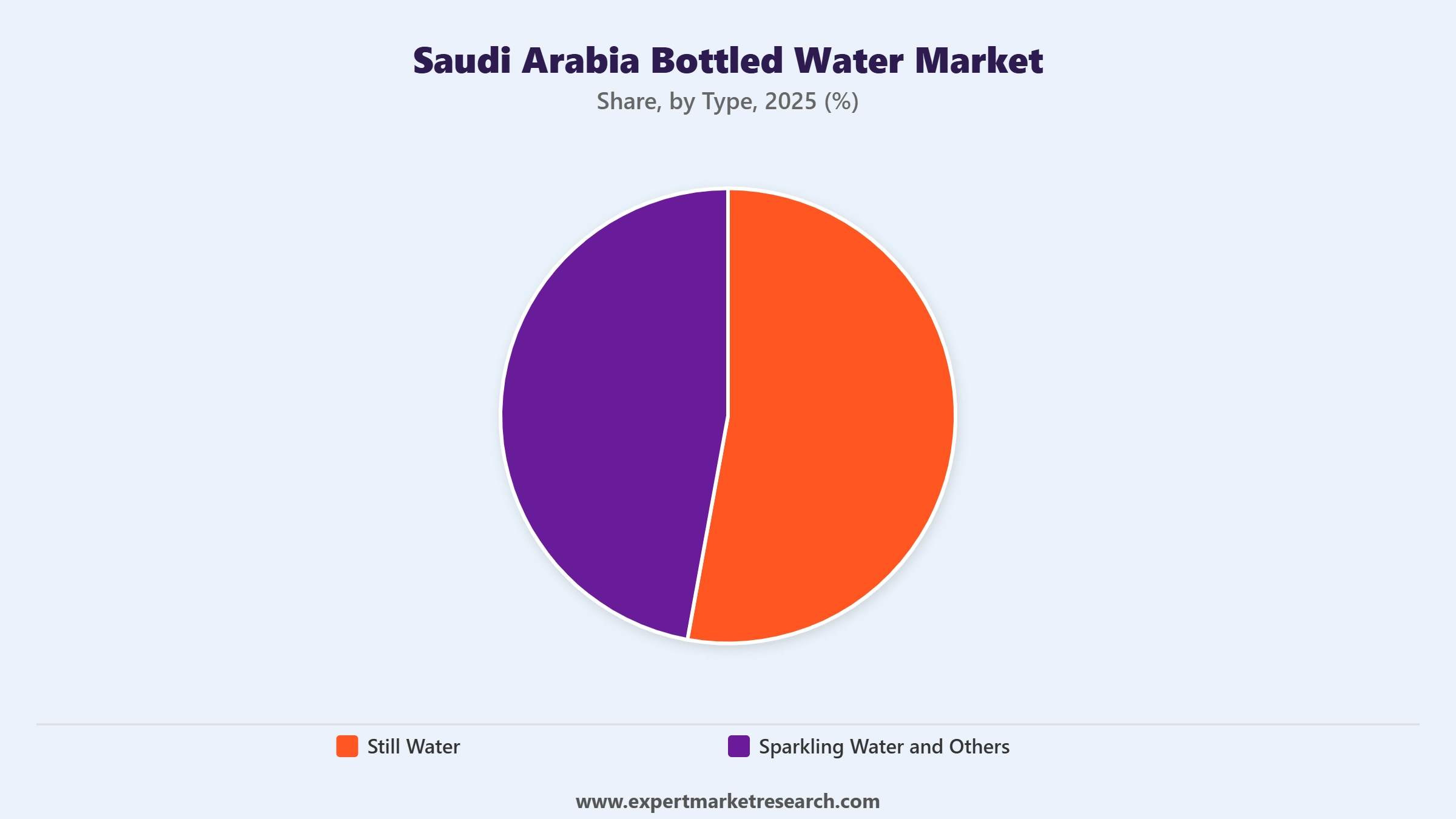

Key Insight: Still water dominates the Saudi Arabia bottled water market by value and volume, serving the everyday hydration needs of households, institutions, and the HORECA sector. Its affordability, broad availability, and neutrality for all age groups make it the default product format. Sparkling water and others represent a growing premium niche, driven by the expansion of international hotel chains and fine dining establishments through Vision 2030 developments. Flavoured and functional water variants are gradually gaining distribution as brands seek to capture higher-value positioning within the Saudi Arabia bottled water market.

Market Breakup by Packaging Size

Key Insight: The 330 ml to 500 ml packaging size leads the Saudi Arabia bottled water market, serving the most frequent purchase occasion: single-serve on-the-go hydration at retail checkouts, food service outlets, petrol stations, and tourism venues. Sub-330 ml formats serve airline and premium hospitality use. The 501 ml to 1000 ml range serves restaurant table service and commuter carry. Larger 1001-2000 ml sizes serve household retail buyers. The above 5001 ml segment is the fastest-growing, driven by home and office delivery channel growth in the Saudi Arabia bottled water market.

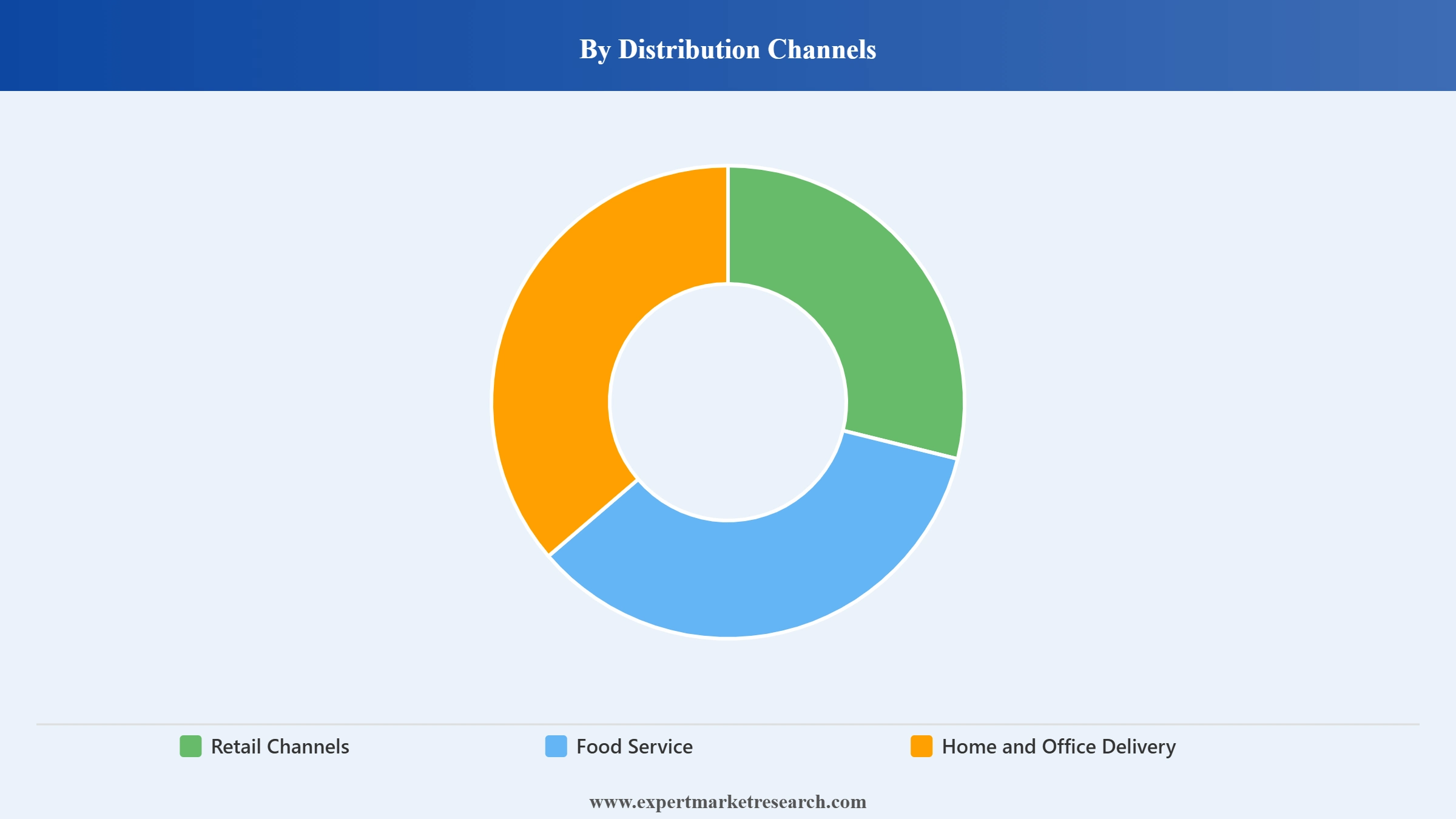

Market Breakup by Distribution Channel

Key Insight: Retail channels hold the largest share of the Saudi Arabia bottled water market, covering supermarkets, hypermarkets, convenience stores, and petrol station forecourts. Food service is a structurally growing channel, driven by Vision 2030's rapid expansion of hotels, restaurants, entertainment venues, and healthcare institutions. Home and office delivery is the fastest-growing channel, supported by rising consumer convenience expectations, digital ordering platform penetration, and the economic advantage of large-format dispenser subscriptions over single-use retail purchases within the Saudi Arabia bottled water market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By type, still water dominates the Saudi Arabia bottled water market due to universal appeal, affordability, and broad distribution across all channels

Still water holds the commanding majority of the Saudi Arabia bottled water market by both volume and value, as it serves the full spectrum of hydration needs from everyday household consumption to institutional and HORECA procurement. Its neutral taste, broad compatibility with all dietary requirements, and cost-effective production make it the default procurement choice for schools, hospitals, construction sites, and pilgrimage facilities. Domestic brands including Maeen Water, Nova Water, and Hana Water Company maintain extensive retail and institutional distribution networks keeping still water consistently accessible across the Kingdom.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Sparkling water and other premium formats are gaining traction within the Saudi Arabia bottled water market, driven by the Vision 2030-led hospitality expansion that has introduced international fine dining and luxury hotel chains requiring sophisticated water service. Almarai’s June 2025 acquisition of Pure Beverages Industry Co. demonstrates how established domestic food and beverage companies are investing in premium and functional water positioning to capture higher-margin growth segments within the Saudi Arabia bottled water market.

By packaging size, the 330 ml to 500 ml format leads due to its single-serve convenience and versatile on-the-go hydration fit

The 330 ml to 500 ml packaging format dominates the Saudi Arabia bottled water market by unit volume, ideally suited to the most frequent purchase occasion: single-serve, point-of-sale hydration across retail checkouts, petrol stations, food service outlets, and tourism venues. Its portability, affordability, and compatibility with individual on-the-go consumption make it the highest-velocity SKU category in the market. In a country where outdoor temperatures regularly exceed 40 degrees Celsius, the single-serve format serves both emergency and habitual hydration needs with equal commercial effectiveness.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The above 5001 ml dispenser category is the fastest-growing packaging segment, driven by the accelerating adoption of home and office delivery subscription models. Nova Water's April 2024 launch of Saudi Arabia's first 100% recycled PET bottle demonstrates how domestic producers are innovating across packaging sizes to meet both consumer and regulatory sustainability expectations while sustaining the commercial momentum of the fastest-growing formats in the Saudi Arabia bottled water market.

By distribution channel, retail holds the largest share while home and office delivery is the fastest-growing channel

Retail channels hold the largest share of the Saudi Arabia bottled water market through supermarkets, hypermarkets, convenience stores, and petrol station forecourts that provide high-frequency, impulse-driven single-serve and multi-pack purchases. The food service channel is structurally growing, driven by Vision 2030's rapid expansion of hotels, restaurants, entertainment venues, and healthcare institutions that require consistent, large-volume still and sparkling water procurement as mandatory operating inputs.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Home and office delivery is the fastest-growing distribution channel within the Saudi Arabia bottled water market, supported by rising consumer convenience expectations, digital ordering platform penetration, and the economic advantage of large-format dispenser subscriptions. Nestlé Middle East's 2024 IoT dashboard rollout for office delivery clients demonstrated how leading producers are using digital services to strengthen commercial relationships and reduce churn in the high-value home and office delivery segment of the Saudi Arabia bottled water market.

The Saudi Arabia bottled water market combines large domestic producers with deep local distribution networks alongside multinational companies leveraging global brand equity and premium positioning. Maeen Water, Hana Water Company, and Health Water Bottling Company dominate the domestic mid-market, while Nestlé's Pure Life and Agthia Group's Al Ain Water maintain strong positions through retail distribution scale. Almarai’s June 2025 acquisition of Pure Beverages Industry Co. adds a powerful distribution network to the competitive landscape of the Saudi Arabia bottled water market.

Sustainability compliance, packaging innovation, and institutional procurement capability are emerging as primary competitive differentiators as the Saudi Food and Drug Authority tightens mineral content standards and the 2035 recycling mandate drives investment in lighter, recyclable packaging formats across the Saudi Arabia bottled water market.

Founded in 1985 and headquartered in Riyadh, Health Water Bottling Company is one of Saudi Arabia's largest domestic bottled water producers, operating the Nova Water brand. The company produces still, sparkling, and flavoured water in a range of packaging formats, serving both retail and institutional channels. Its April 2024 launch of Saudi Arabia's first 100% recycled PET bottle positioned Nova Water as a sustainability pioneer, demonstrating proactive regulatory compliance within the Saudi Arabia bottled water market.

Maeen Water, headquartered in Jeddah, Saudi Arabia, is a leading domestic bottled water brand launched in 2015 and known for tech-forward bottled water systems. The company offers premium alkaline water in glass bottles and holds major contracts with Saudi hospitals and event organisers. Its 2024 launch of magnesium-rich functional water for fitness centres demonstrates Maeen's strategy of moving into higher-margin premium and functional segments within the Saudi Arabia bottled water market.

Founded in 2004 and headquartered in Abu Dhabi, UAE, Agthia Group operates the Al Ain Water brand, one of the Gulf's best-known bottled water names. The company distributes Al Ain Water across Saudi Arabia and the wider GCC through modern trade, food service, and route-to-market direct delivery. Agthia's scale in GCC water production and its strong retailer relationships provide competitive advantages in retail channel visibility and institutional procurement tenders within the Saudi Arabia bottled water market.

Part of Nestlé S.A., founded in 1866 and headquartered in Vevey, Switzerland, Nestlé Middle East FZE distributes the Pure Life brand across Saudi Arabia through established modern trade relationships. Pure Life's global brand equity, consistent quality standards, and multi-size packaging range make it a strong performer in both household retail and premium HORECA channels. Its 2024 IoT dashboard rollout for office delivery clients demonstrates Nestlé's strategy of using digital services to build recurring commercial relationships in the Saudi Arabia bottled water market.

Other key players in the market are Hana Water Company, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Get the complete picture of the Saudi Arabia bottled water market with our latest research report. Discover how Vision 2030, pilgrimage tourism, HORECA expansion, and sustainability mandates are reshaping demand, packaging, and distribution dynamics, and find where your next growth opportunity sits across type, size, and channel. Whether you produce bottled water, manage retail or food service distribution, develop packaging solutions, or invest in consumer staples, this report gives you the clarity to act decisively. Download your free sample today and explore the key opportunities in the Saudi Arabian bottled water space.

North America Bottled Water Market

Argentina Bottled Water Market

Europe Bottled Water Market

Mexico Bottled Water Market

GCC Bottled Water Market

Bottled Water Market

Upto 15% Off

USD

$3999 $3599

$2499 $2249

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the Saudi Arabia bottled water market reached an approximate value of USD 2993.56 Million.

The market is projected to grow at a CAGR of 6.80% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach USD 5779.64 Million by 2035.

Key strategies driving the market include optimizing localized production, investing in AI-based monitoring, expanding B2B subscription models, and launching segment-specific packaging.

Key trends aiding Saudi Arabia bottled water market expansion include the growing demand for bottled water as a substitute for carbonated beverages, the increasing development of innovative bottled water with diverse flavours, and the surging investments in new technologies by the leading companies to boost output.

The major types of bottled water in the market are still water and sparkling water.

The various packaging sizes of bottled water are ≤330 ml, 331 – 500 ml, 501 ml - 1000 ml, 1001 ml – 2000 ml, 2001 - 5000 ml, and ≥ 5001 ml.

The significant distribution channels in the market are retail channels, food service, and home and office delivery.

Currently, there are over seventy bottled water factories in Saudi Arabia, with fourteen of them located in Al-Riyadh City. These factories collectively produce around 5 billion litres of bottled water annually.

The key players in the market include Nestlé Middle East FZE, Agthia Group PJSC, Health Water Bottling Co. Ltd. (Nova Water), Maeen Water, and Hana Water Company, among others.

The key challenges are sourcing sustainable materials, high logistics cost, and seasonal demand spikes.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Packaging Size |

|

| Breakup by Distribution Channels |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.