Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

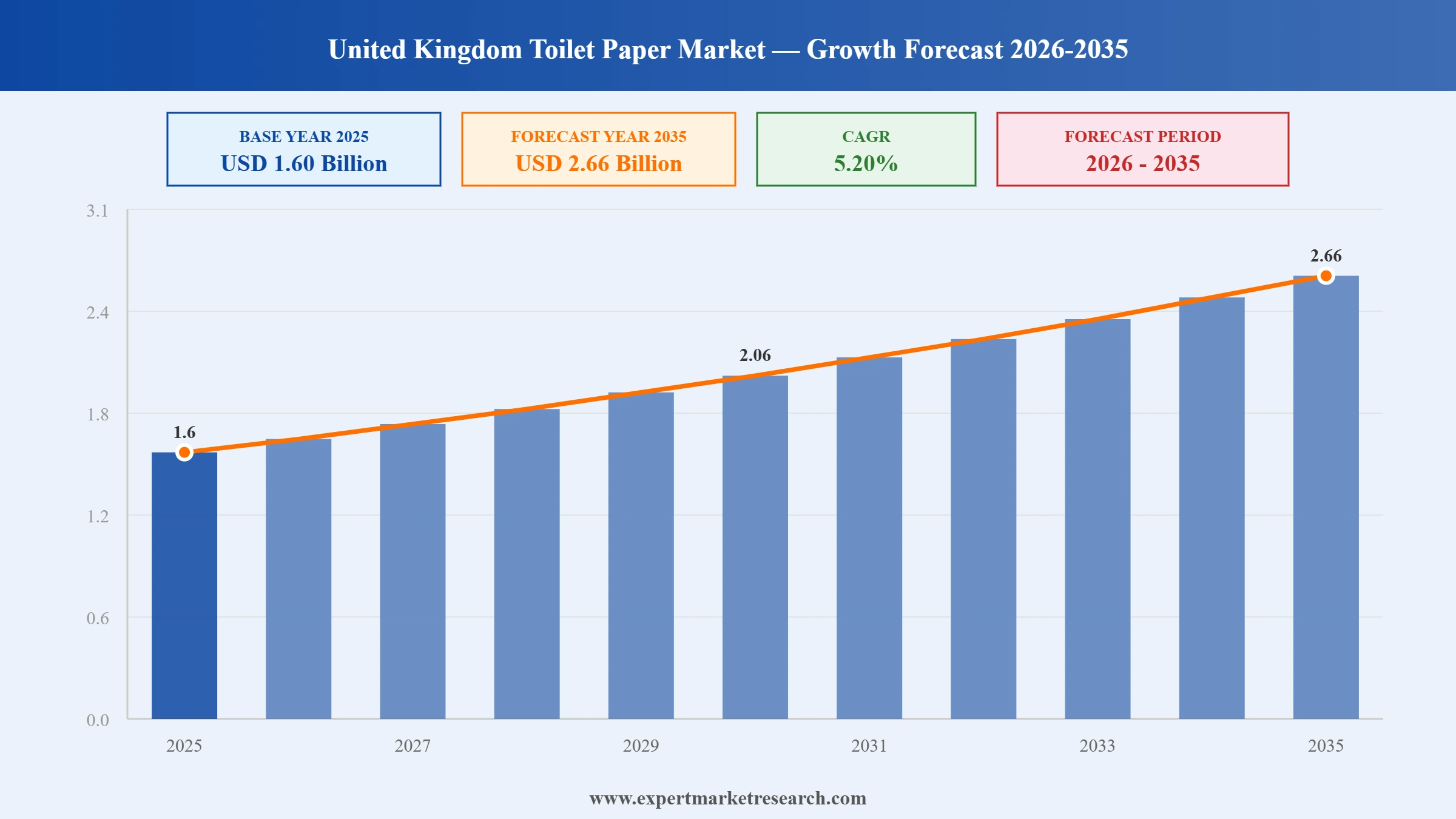

The United Kingdom Toilet Paper Market reached a value of USD 1.60 Billion at 2025 and is projected to expand at a CAGR of around 5.20% during the forecast period of 2026-2035. With a growing preference for eco-friendly and premium tissue products, a steady rise in residential demand driven by population growth, increasing online retail adoption, and strong consumer awareness around personal hygiene, the market is expected to reach USD 2.66 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The United Kingdom toilet paper market is being shaped by four converging forces: a mainstream shift toward eco-friendly and recycled tissue products, the ongoing premiumisation of the tissue category, the rapid growth of e-commerce and subscription-based purchasing, and rising private label adoption driven by cost-conscious consumer behaviour. Each of these trends is rooted in tangible corporate activity and measurable shifts in how UK households and businesses source and consume toilet paper.

In December 2025, The Navigator Company announced a significant restructuring of its UK tissue operations as it progressed the integration of the Accrol business. The plan involves closing the toilet paper and kitchen towel manufacturing facility in Blackburn, Lancashire, and transferring production to a new plant in Leicester and an established site in Leyland. The Leicester facility is expected to grow its capacity by 30 to 50 percent, while Leyland is projected to expand by 15 to 25 percent. The consolidation reduces Navigator's UK manufacturing and logistics footprint from six sites to two, aiming to improve cost efficiency and supply chain reliability.

In May 2024, The Navigator Company finalised its takeover of Accrol Group Holdings Plc, the United Kingdom's leading independent tissue converter, in a deal valued at approximately GBP 127.5 million. Accrol supplies toilet tissues, kitchen rolls, facial tissues, and wet wipes to major UK grocery retailers and discounters. Following the transaction, Navigator anticipated a combined tissue turnover of around GBP 500 million, with the UK market accounting for roughly half of that figure. The deal reinforced Navigator's strategy of consolidating its position across the Western European tissue manufacturing landscape.

In February 2024, Tesco, one of the United Kingdom's largest grocery retailers, launched a new range of toilet rolls and kitchen towels manufactured from 100% recycled cardboard and recycled pulp. The move came in direct response to rising consumer demand for sustainable tissue products, particularly among urban households with strong environmental preferences. By offering the recycled range under its own label at an accessible price, Tesco opened the eco-friendly tissue category to a far broader customer base than specialist sustainability brands had previously reached. The launch aligned with wider retailer commitments to reduce plastic use and source more responsibly across the household paper category.

In 2024, Metsa Group, a major European tissue paper producer and distributor, announced plans to establish a new tissue paper manufacturing facility in the East of Yorkshire, United Kingdom. The proposed plant, covering over 200 acres, is designed with a production capacity of 240,000 tons, which would represent a significant addition to UK domestic tissue supply. The investment reflects growing confidence in long-term demand for tissue products in the British market and supports the broader industry trend of manufacturers reducing dependence on imported jumbo rolls by bringing integrated production capacity closer to key consumer markets.

In 2024, WEPA Hygieneprodukte GmbH announced an investment to expand the production capacity of its tissue manufacturing facility in Bridgend, Wales, which produces toilet paper and kitchen towels for the British consumer market. The expansion, supported by the Welsh Government's Environmental Protection scheme, was designed to increase manufacturing throughput while preserving product quality and sustainability standards at the site. The Bridgend plant employs approximately 345 people and has been part of the WEPA Group since 2013. The investment reinforced WEPA's standing as one of Europe's top three hygiene paper manufacturers and strengthened its supply commitments to major UK retail and grocery customers.

Sustainability is no longer a niche concern in the UK toilet paper market; it is a mainstream purchasing driver reshaping product development across the entire category. Shoppers are actively seeking recycled-fibre products and plastic-free packaging, while major retailers are responding with their own eco-branded tissue ranges. This shift is one of the central forces behind United Kingdom toilet paper market growth, as manufacturers retool supply chains to meet both consumer expectations and tightening retailer sustainability requirements. In February 2024, Tesco launched a toilet roll range made from 100% recycled cardboard and recycled pulp, marking mainstream retail's full entry into the sustainable tissue space and validating the commercial scale of this trend.

A growing share of UK consumers is choosing to trade up from standard toilet paper to multi-ply, ultra-soft, or dermatologically tested variants, particularly in urban households where disposable incomes are higher and comfort is treated as a baseline expectation rather than a luxury. This premiumisation dynamic is encouraging leading brands to expand their upper-tier product lines and invest heavily in quality and skin-friendliness claims. The trend is also prompting private label ranges to improve their tissue quality to retain shoppers who might otherwise gravitate toward premium branded alternatives. In 2024, UK consumer research indicated that 82 percent of Brits regard toilet paper as an essential household item, reinforcing the high perceived value attached to quality tissue products.

Digital retail channels and subscription-based delivery services are steadily capturing market share in the UK toilet paper segment, offering consumers convenience, consistent pricing, and the ability to align purchases with sustainability preferences. Brands offering bamboo, recycled, or FSC-certified tissue on recurring delivery plans have grown their customer bases rapidly, helped by dense urban broadband infrastructure and consumer reluctance to haul bulky household goods from physical stores. The International Trade Administration projected UK e-commerce sector growth at an average annual rate of 12.6 percent through 2025, a figure that directly benefits household paper categories. Manufacturers are responding by developing direct-to-consumer platforms and negotiating higher visibility on leading online marketplaces.

Cost-of-living pressures have accelerated private label toilet paper adoption across the UK, with supermarket own-brand ranges winning shelf prominence and growing consumer acceptance that previously belonged almost exclusively to branded alternatives. Although brand loyalty remains comparatively resilient in the tissue category, household budget constraints in 2024 prompted a wider cross-section of consumers to reassess their default brand choices. Mintel's 2025 analysis of the UK household paper products market noted that own-label product volumes continued to outperform branded alternatives during periods of financial uncertainty. Retailers including Asda, Sainsbury's, and Lidl responded by widening and improving their private label tissue assortments, making quality-competitive options available at accessible price points.

“United Kingdom Toilet Paper Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Type

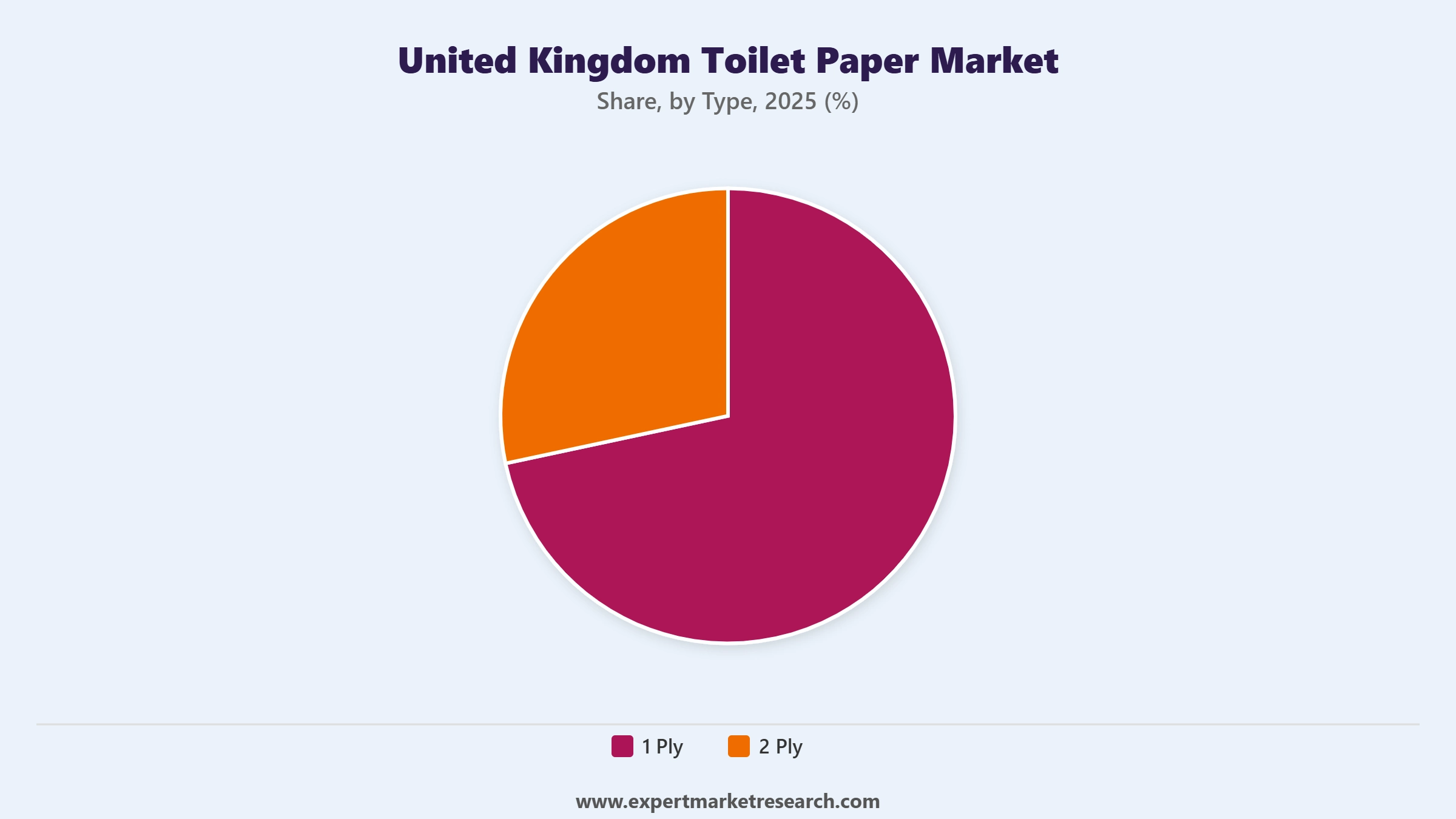

Key Insight: The 2 Ply segment holds the dominant position in the UK toilet paper market by type, reflecting deep consumer familiarity with and preference for the softer, more absorbent format across both residential and commercial settings. Brands such as Andrex, distributed by Kimberly-Clark, and Cushelle, distributed by Essity, have invested consistently in two-ply quality claims, reinforcing category loyalty. The 1 Ply segment retains relevance primarily in institutional and high-traffic commercial environments such as offices, transport hubs, and public facilities, where cost efficiency and high-volume dispensing take precedence over comfort. The Others sub-category captures emerging premium formats including three-ply ultra-soft rolls and recycled-core variants gaining traction among environmentally motivated consumers.

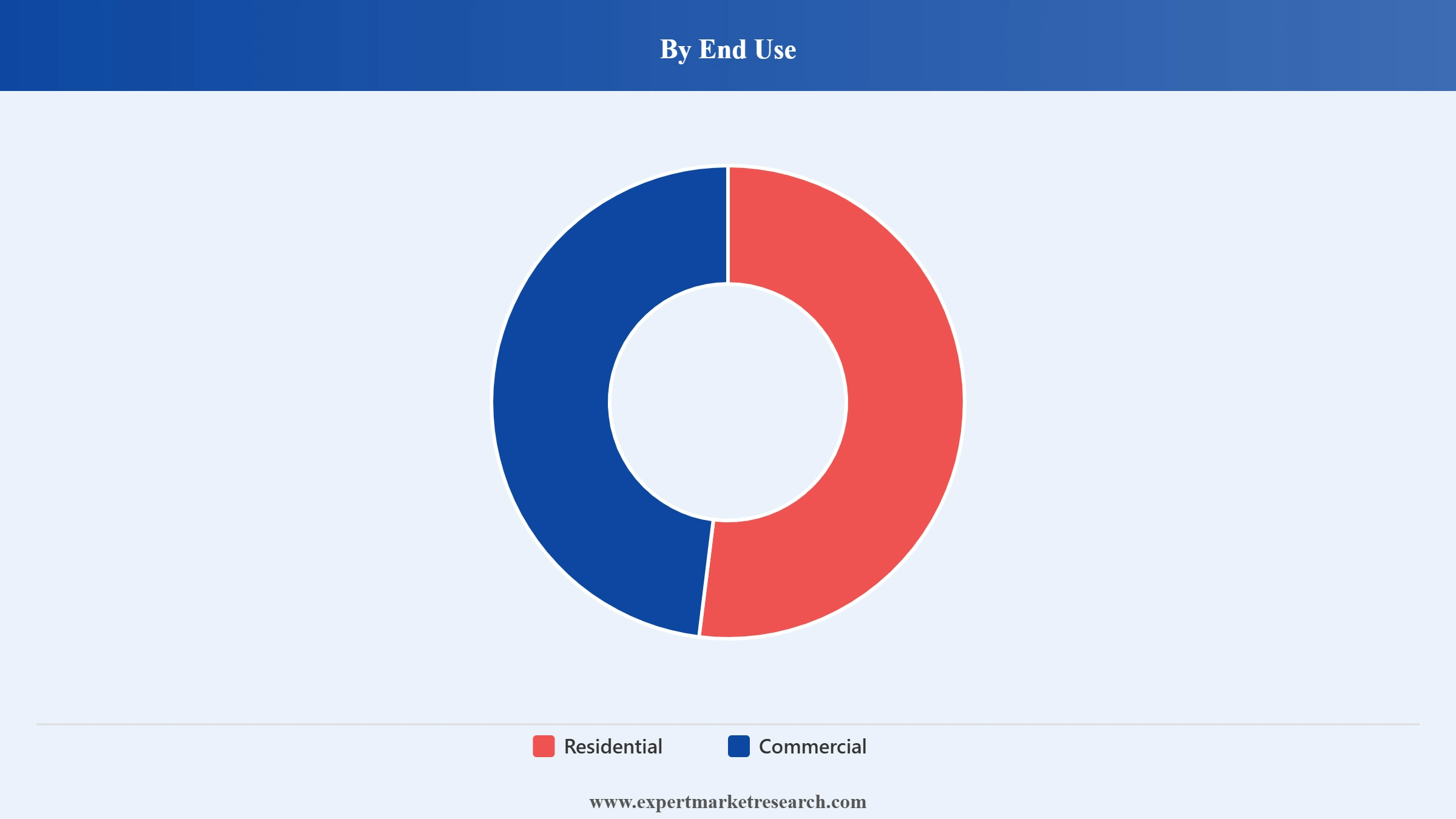

Market Breakup by End Use

Key Insight: Residential end use accounts for the larger share of UK toilet paper consumption, supported by stable household demand across England's densely populated cities and a strong repeat purchase cycle through the grocery retail channel. Population growth averaging 1.0 percent annually as of mid-2023 according to government estimates has added incrementally to the residential consumer base each year. The commercial segment, which includes offices, hospitality venues, healthcare facilities, and educational institutions, contributes meaningful volume through B2B procurement of bulk and jumbo-roll formats. The post-pandemic recovery of the UK hospitality and events sector provided fresh momentum to commercial demand between 2022 and 2025, with major tissue suppliers including WEPA and Essity serving both segments through differentiated product portfolios.

Market Breakup by Distribution Channel

Key Insight: The B2C distribution channel accounts for the majority of UK toilet paper revenues, encompassing supermarkets, hypermarkets, convenience stores, discounters, and the rapidly expanding e-commerce platform segment. Retailers such as Tesco, Sainsbury's, Asda, and Aldi collectively drive the greatest consumer throughput, stocking a broad mix of branded and own-label tissue products across price tiers. B2B distribution serves commercial and institutional buyers, including office facilities managers, hospitality operators, and NHS-contracted healthcare providers, primarily through wholesale and contract supply arrangements. The boundary between B2B and B2C purchasing is blurring gradually as businesses source from the same online platforms and subscription services that were previously associated with household consumers.

Market Breakup by Region

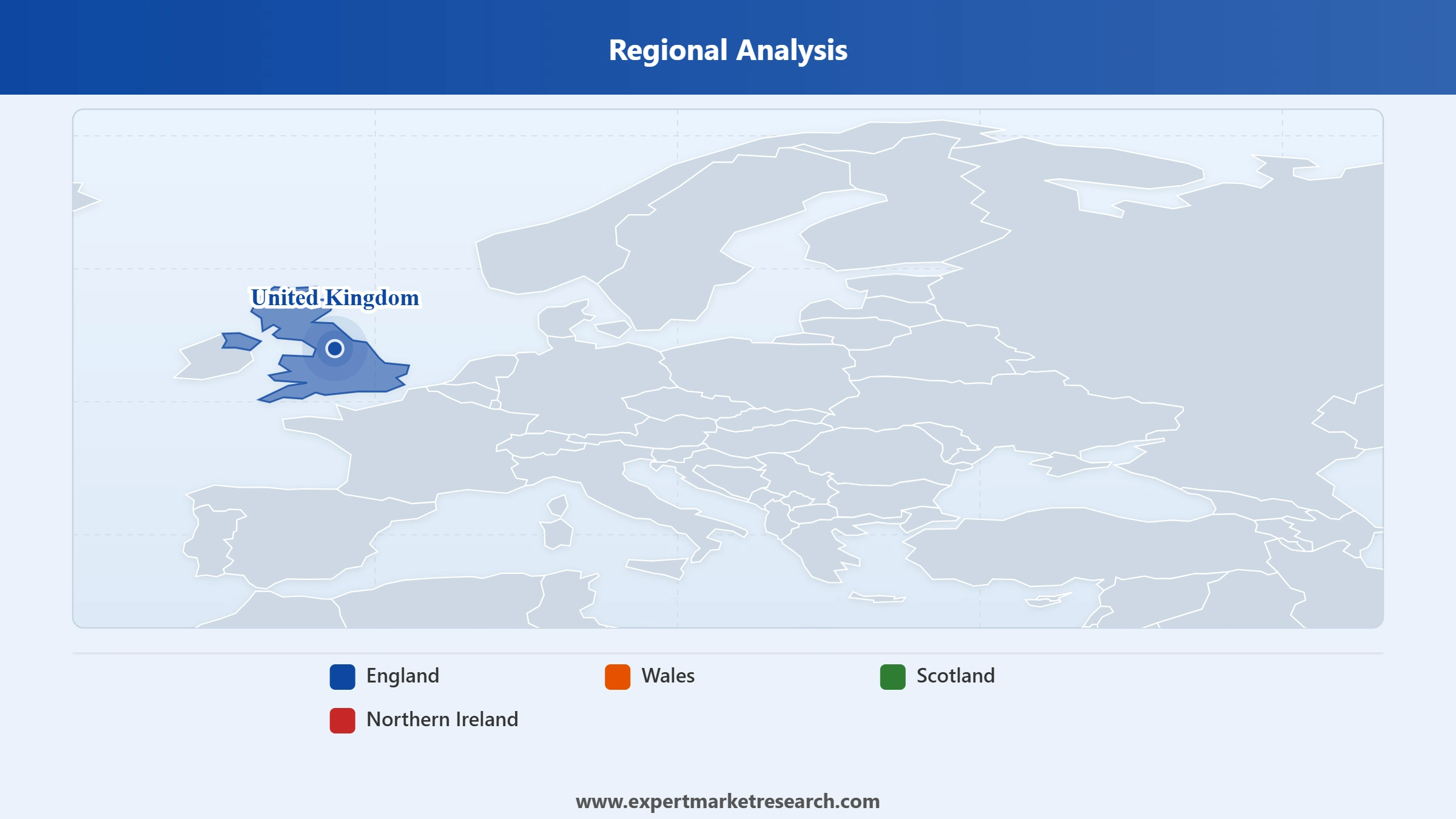

Key Insight: England accounts for the vast majority of UK toilet paper consumption, reflecting its population of approximately 56 million people and its dense concentration of urban retail and commercial infrastructure. Major tissue manufacturing and logistics hubs in Lancashire, Leyland, and Leicester reinforce England's central role in the UK tissue supply chain. Wales hosts a strategically significant production site operated by WEPA in Bridgend, which supplies the broader British market and underwent a funded capacity expansion in 2024. Scotland and Northern Ireland represent smaller but structurally stable demand bases, with consumption driven by household density in Edinburgh, Glasgow, Belfast, and their surrounding communities.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The 2 Ply segment commands the largest share of the UK toilet paper market by type in terms of both value and volume sold through retail channels. Sustained brand investment from Kimberly-Clark in Andrex and from Essity in Cushelle has cemented two-ply as the default household purchase across virtually every income bracket. The cost differential between 1 Ply and 2 Ply products has narrowed materially in recent years, particularly across own-label ranges, which has tilted purchase decisions further in favour of the superior-comfort format. Continued product innovation in recycled-fibre two-ply variants is expected to sustain this segment's lead through the forecast period, as sustainability-conscious consumers increasingly substitute recycled two-ply for standard virgin-fibre alternatives without sacrificing comfort.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The residential end use segment holds the larger share of the UK toilet paper market by end use, underpinned by consistent household demand and a strong repeat purchase cycle operating through established grocery retail formats. UK households replenish toilet paper on predictable schedules, making the residential channel relatively resilient through economic cycles. The commercial segment, while smaller in absolute value, has recovered strongly since pandemic restrictions were lifted, as office occupancy, hotel stays, and restaurant covers returned to near pre-2020 levels. Companies including WEPA Hygieneprodukte and Essity AB serve both segments through clearly differentiated product ranges, capturing share across supermarket retail shelves and institutional procurement contracts simultaneously.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

England is the dominant regional market within the United Kingdom toilet paper industry. Its population of approximately 56 million, concentrated in major urban centres including London, Manchester, Birmingham, and Leeds, generates the largest consumer demand base in the country. The national tissue supply chain is anchored in England, with the Navigator-operated Leicester and Leyland facilities serving as major converting hubs following the restructuring of the former Accrol network in 2025 and 2026. England also serves as the primary demand centre for premium and eco-friendly toilet paper, with urban consumers among the earliest and most consistent adopters of recycled-fibre and plastic-free packaged tissue. The recovery of the commercial hospitality sector across England's major cities has provided renewed volume momentum, with hotels, restaurants, and event venues restocking aggressively as tourism and domestic travel normalised.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Wales contributes a structurally significant manufacturing presence to the UK toilet paper supply chain through the WEPA Hygieneprodukte facility in Bridgend, one of the country's key tissue converting sites. The plant employs approximately 345 people and received a funded capacity expansion in 2024, supported by the Welsh Government's Environmental Protection scheme, increasing its ability to supply toilet paper and kitchen towels across the broader British retail market. Scotland and Northern Ireland represent smaller but stable regional demand bases, with consumption closely tied to household income levels and population density in Edinburgh, Glasgow, Belfast, and surrounding areas. Scotland benefits from its status as the third most populous of the four UK nations and is serviced through the same national grocery distribution networks operating across England, ensuring consistent product availability in both urban supermarkets and rural convenience stores.

The United Kingdom toilet paper market features a moderately consolidated competitive landscape in which global consumer goods giants compete alongside a growing group of domestic private label specialists and regional converters. International players such as Essity AB, Kimberly-Clark Corp., and Procter and Gamble Co. command strong brand equity through household names like Cushelle, Andrex, and Charmin, while independent converters led by Accrol Group (now part of Navigator) and WEPA's UK operation hold substantial positions in the private label and own-brand segments. Price competition is intense within the grocery retail channel, where supermarket own-brands exert consistent downward pressure on branded margins across both 1 Ply and 2 Ply categories.

Market consolidation has gained momentum in recent years, most visibly through Navigator's acquisition of Accrol Group in 2024 and the subsequent restructuring of UK tissue operations that followed into 2025 and 2026. Smaller domestic players including International Tissue Company, Fourstones Paper Mill, Splesh, and Bazoo serve niche and regional demand without the manufacturing scale needed to compete across all retail channels. Companies with FSC-certified supply chains, sustainable product portfolios, and established retailer relationships are increasingly advantaged as major UK supermarkets raise sustainability thresholds for supplier qualification.

Founded in 1929 and headquartered in Stockholm, Sweden, Essity AB is a leading global hygiene and health company active in over 150 countries. In the United Kingdom, Essity markets its consumer tissue products under the Cushelle and Tork brands, with Cushelle holding strong brand recognition across supermarket tissue aisles. The company is committed to 100% recyclable plastic packaging across its portfolio and has invested consistently in sustainable fibre sourcing. Its deep retail relationships, widespread distribution network, and strong consumer marketing investment underpin its resilient competitive position in the UK tissue market.

Founded in 1872 and headquartered in Dallas, Texas, Kimberly-Clark Corp. is one of the world's largest producers of paper-based consumer goods. In the United Kingdom, the company markets Andrex, which remains among the country's most recognised and recalled toilet paper brands. Kimberly-Clark has sustained investment in FSC-certified sourcing and recycled-fibre product development, and Andrex commands premium shelf space across all major UK grocery formats. Its combination of brand equity, product quality signalling, and advertising consistency gives it a durable competitive advantage in the premium and mid-tier tissue segments.

Founded in 1837 and headquartered in Cincinnati, Ohio, Procter and Gamble Co. is a global consumer goods leader active across personal care, health, and household product categories. In the United Kingdom, the company has a presence in the tissue market and has been at the forefront of sustainable packaging innovation, introducing a zero-plastic paper-based wrapper across multiple global markets in April 2024. Its extensive retail distribution reach and commitment to reducing plastic in consumer packaging by 50 percent by 2030 position it as an active participant in the sustainability transformation of the UK tissue category.

Nova Tissue Co. Ltd. is a UK-based tissue paper manufacturer producing a range of toilet rolls, kitchen towels, and facial tissues for the domestic market. The company operates primarily within the private label and value segment, supplying retailers and wholesale distributors with competitively priced tissue products. Its UK manufacturing base and operationally lean structure allow it to respond with agility to shifts in retailer sourcing preferences, making it a practical supplier option for major supermarkets seeking to diversify their private label tissue supplier portfolios as sustainability and cost pressures mount.

Other key players in the market are Accrol Group Holdings Plc, WEPA Hygieneprodukte GmbH, International Tissue Company Ltd., Fourstones Paper Mill Co. Ltd., Splesh, Bazoo, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Understand where the United Kingdom toilet paper market is heading from 2026 to 2035 with our comprehensive research report. From sustainable product innovation and premiumisation trends to private label dynamics and regional growth patterns, this report gives you the full picture. Whether you are a tissue manufacturer refining your product strategy, a retailer reviewing your own-label supply chain, or an investor evaluating the household paper sector, our analysis provides the evidence base you need. Download your free sample today and begin exploring the opportunities shaping the UK tissue and hygiene industry.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the United Kingdom toilet paper market attained a value of nearly USD 1.60 Billion.

The market is projected to grow at a CAGR of 5.20% between 2026 and 2035.

The market is expected to attain a value of USD 2.66 Billion by 2035.

The major drivers of the market are the rising population, growth in disposable income, and increasing health awareness.

The key trends of the market include the manufacturing of sustainable products, innovations by major brands, and the increasing use of recyclable packaging.

The major regions in the market are England, Wales, Scotland, and Northern Ireland.

The various types of toilet paper considered in the market report are 1 Ply and 2 Ply, among others.

The significant segments based on end-use considered in the market report are residential and commercial.

The various distribution channels in the market are B2B and B2C.

The major players in the market are Essity AB, Kimberly-Clark Corp., Procter & Gamble Co., Nova Tissue Co. Ltd., Accrol Group Holdings Plc, WEPA Hygieneprodukte GmbH, International Tissue Company Ltd., Fourstones Paper Mill Co. Ltd., Splesh, and Bazoo, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by End Use |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.