Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

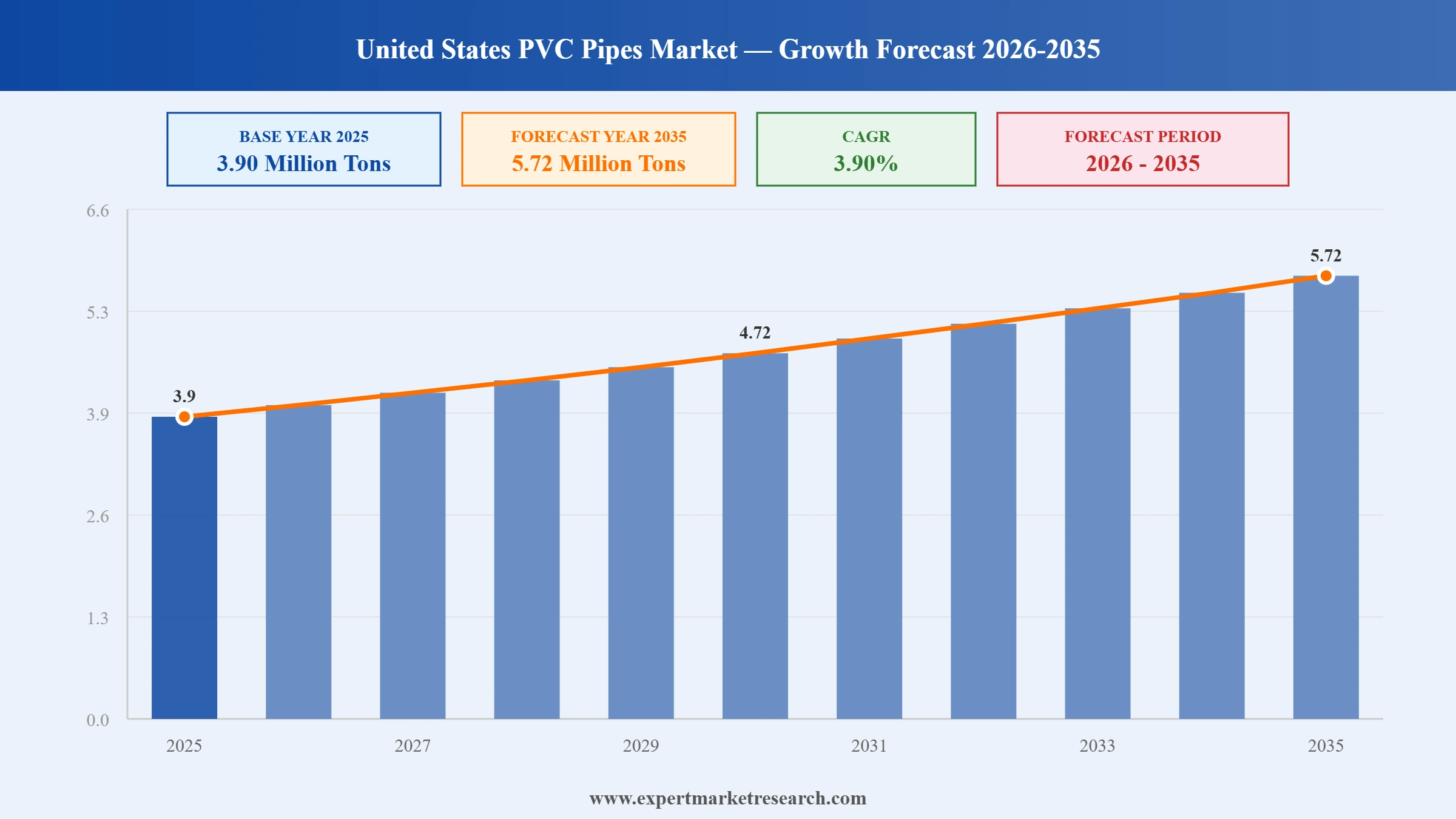

The United States PVC pipes market reached a volume of 3.90 Million Tons at 2025 and is projected to expand at a CAGR of around 3.90% during the forecast period of 2026-2035. With accelerating federal water infrastructure investment under the Bipartisan Infrastructure Law, growing demand from the construction and agricultural irrigation sectors, and rising adoption of advanced PVC pipe technologies for municipal applications, the market is expected to reach 5.72 Million Tons by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The United States PVC pipes market is being shaped by a confluence of sustained federal infrastructure funding, growing construction activity, and advancing product innovation. Manufacturers are investing in higher-performance pipe variants such as molecularly oriented PVC to meet the demands of municipal water projects, while demand from the agricultural, plumbing, and sewage sectors remains structurally robust across both urban and rural markets.

Westlake Corporation announced in February 2025 its plans to open a new molecularly oriented PVC pipe plant in Wichita Falls, Texas, by 2026, adding four dedicated production lines to support growing municipal demand. The PVCO product offers superior strength, reduced material usage, and improved potable water conveyance compared to standard PVC, aligning directly with rising infrastructure investment in the United States PVC pipes market.

The EPA released FY2025 allocations totalling nearly $3 billion specifically for lead service line identification and replacement, with Illinois, which has the highest number of lead pipes in the nation, receiving the largest share. This funding, channelled through the Drinking Water State Revolving Fund, directly stimulates demand for corrosion-resistant PVC pipe replacements across municipal networks in the United States PVC pipes market.

A federal antitrust lawsuit was filed in Chicago in August 2024, accusing major PVC pipe manufacturers including Westlake, Atkore, Otter Tail, and JM Eagle of conspiring to coordinate price increases. The complaint alleges that these companies artificially raised costs for contractors and municipalities, prompting regulatory scrutiny and encouraging buyers to diversify their supplier base within the United States PVC pipes market.

Westlake Pipe and Fittings announced in May 2024 the addition of a 190,000 square foot facility at its Wichita Falls, Texas, site for the manufacture of PVCO pipes. The expansion, supported by local government incentives, is designed to create new skilled jobs and expand Westlake's product portfolio with advanced molecular-oriented PVC pipe technology targeting the growing municipal infrastructure segment of the United States PVC pipes market.

The Bipartisan Infrastructure Law represents the largest single federal investment in US water infrastructure, committing over $50 billion through EPA programs. This directly fuels United States PVC pipes market demand for durable, corrosion-resistant piping across municipal water supply, sewerage, and lead pipe replacement programs nationwide.

The EPA committed $6.2 billion in FY2025, comprising $3.6 billion in new funds and $2.6 billion previously announced, to upgrade water infrastructure in communities nationwide. This investment accelerates the United States PVC pipes market growth by prioritising PVC-based replacements for failing concrete, clay, and lead systems across urban networks.

PVCO pipes, offering enhanced strength and reduced material usage compared to standard PVC, are gaining measurable traction in US municipal water projects. Westlake's Wichita Falls plant expansion directly responds to this demand, with the United States PVC pipes market increasingly specifying PVCO for high-pressure potable water mains and replacement programs.

Growing adoption of smart and drip irrigation systems in drought-prone states including California, Arizona, and Texas is expanding PVC pipe consumption in the agricultural sector. The United States PVC pipes market is benefitting as farmers invest in efficient, durable irrigation infrastructure to meet crop yield targets and comply with state water conservation regulations.

US construction spending exceeded $1,978 billion in 2023 and continues growing, sustaining consistent demand for PVC pipes in residential plumbing, HVAC, and commercial building applications. This structural tailwind supports the United States PVC pipes market as builders favour PVC for its cost effectiveness, ease of installation, and long service life versus metal alternatives.

The report of Expert Market Research's titled "United States PVC pipes market report and forecast 2026-2035 offers a detailed analysis of the market based on the following segments:

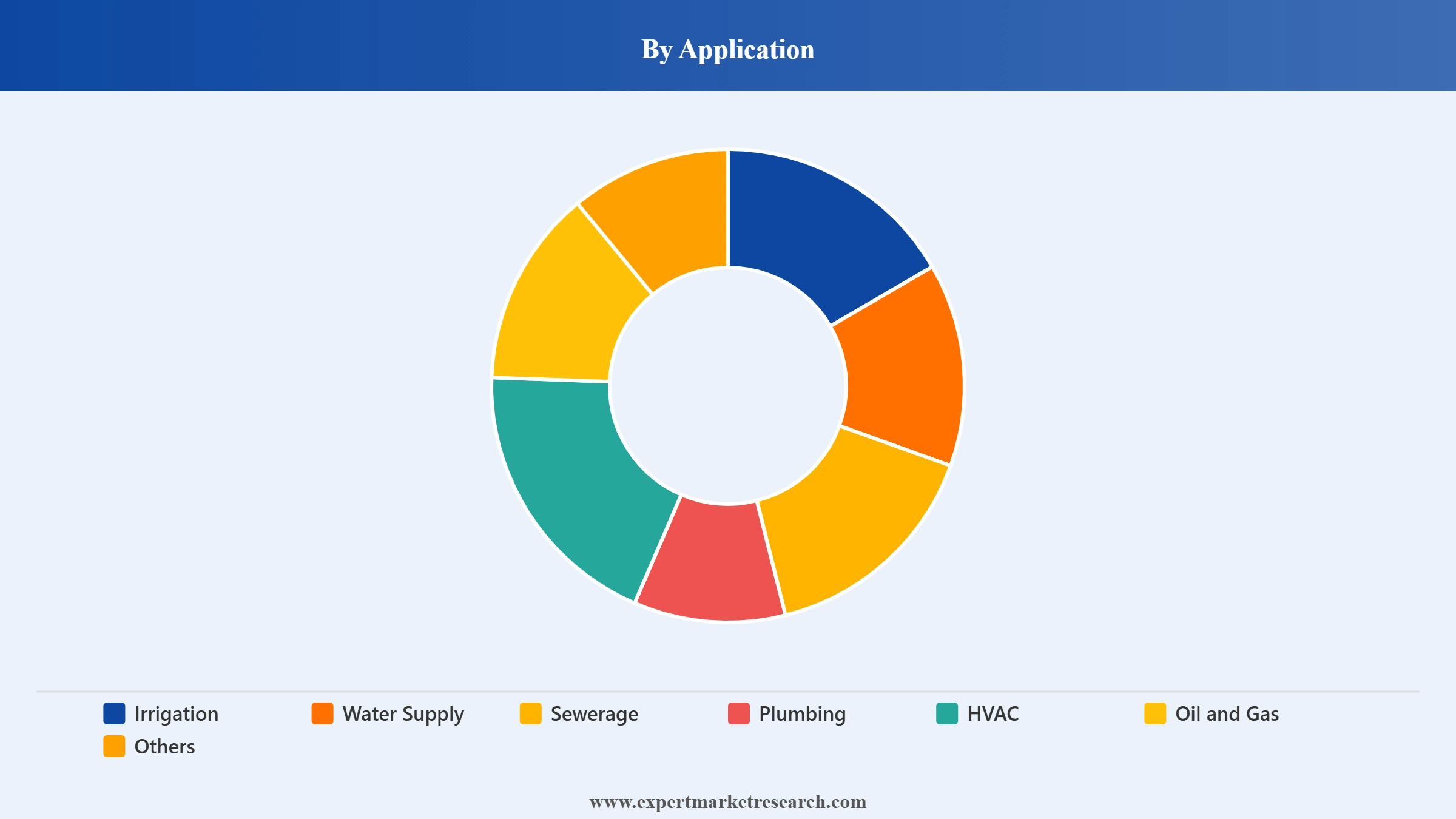

Market Breakup by Application

Key Insight: Irrigation leads the United States PVC pipes market by application volume, driven by widespread use across drip, sprinkler, and surface irrigation systems in the country's large agricultural sector. PVC pipes offer smooth inner walls that minimise friction loss, making them efficient for transporting water over significant distances, and they are well suited to both temporary and permanent irrigation distribution networks. Water supply is the fastest-growing application, as the EPA's Bipartisan Infrastructure Law funding mandates replacement of lead service lines across millions of homes and municipal networks, with PVC emerging as the preferred cost-effective and corrosion-resistant alternative. Sewerage, plumbing, HVAC, and oil and gas applications collectively sustain steady baseline demand, supported by ongoing construction activity, building renovation programs, and regulatory requirements for safe and durable piping solutions.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Application, Irrigation Dominates the Market Due to Extensive Agricultural Water Delivery Requirements and Efficient Pipe Performance

Irrigation holds the dominant share of the United States PVC pipes market, anchored by the country's vast agricultural sector where PVC pipes are widely deployed across drip, sprinkler, and surface irrigation systems. Their smooth inner surface minimises friction losses over long distances, making them the practical default for large-scale water conveyance to farmland. Water-stressed western and southern states drive consistent procurement volumes as farmers upgrade infrastructure to meet efficiency mandates.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Water supply is the fastest-growing application within the United States PVC pipes market, propelled by the federally mandated replacement of an estimated 9 million lead service lines under the Bipartisan Infrastructure Law. With EPA allocating nearly $3 billion in FY2025 specifically for lead pipe replacement, municipalities are procuring PVC pipes at scale as the cost-effective and corrosion-resistant successor material. Sewerage, plumbing, and HVAC applications collectively sustain demand as construction activity and building renovation programs maintain steady consumption across residential and commercial sectors.

The United States PVC pipes market is characterised by a moderately concentrated competitive landscape, with a few dominant domestic manufacturers holding significant market share alongside a broader base of regional and specialty players. JM Eagle, widely regarded as the largest PVC pipe manufacturer in the United States and North America, leads by production capacity and supply contract scale, while Charlotte Pipe and Foundry, Westlake Pipe and Fittings, and North American Pipe Corporation compete on product breadth, geographic reach, and customer relationships across construction, utility, and agricultural channels.

The competitive environment is evolving as manufacturers invest in advanced pipe technologies such as PVCO, expand production capacity to serve federal infrastructure programs, and pursue efficiency improvements to manage PVC resin cost volatility. Antitrust scrutiny following the August 2024 federal lawsuit has added a further dynamic, encouraging buyers to diversify their supplier base and incentivising manufacturers to sharpen their value propositions on quality, delivery, and product innovation rather than price coordination. Domestic resin producers like Shintech supply the raw material backbone that supports the broader manufacturing ecosystem.

Founded in 1982 and headquartered in Los Angeles, California, JM Eagle is the largest PVC pipe manufacturer in the United States and North America. The company operates manufacturing facilities across multiple states and supplies PVC, PE, and HDPE pipes to municipal water and sewage utilities, agricultural irrigation systems, and construction projects nationwide. JM Eagle's multi-million ton supply contracts and extensive distribution network make it the dominant player in the United States PVC pipes market, with a product range covering pressure pipe, sewer pipe, electrical conduit, and irrigation pipe across a wide range of diameters.

Founded in 1974 and headquartered in Houston, Texas, Shintech Inc. is the largest producer of polyvinyl chloride resin in the United States and a key upstream supplier to the domestic PVC pipe manufacturing industry. The company operates integrated production facilities in Louisiana leveraging ethylene chloride feedstocks, producing suspension PVC and specialty resins that serve pipe manufacturers, construction material producers, and industrial chemical users. Shintech's large-scale, cost-efficient production operations provide a stable resin supply foundation that supports the competitive position of domestic PVC pipe manufacturers in the United States market.

Headquartered in Knoxville, Tennessee, Dura-Line LLC is a leading manufacturer of HDPE and PVC conduit and piping systems used in telecommunications, energy, and utilities infrastructure across North America. The company specialises in innerduct, microduct, and protective conduit systems, with PVC products serving electrical and data cable conduit applications in residential, commercial, and industrial construction. Dura-Line's broad manufacturing footprint across the United States and its focus on infrastructure-grade protective conduit solutions position it as a significant participant in the conduit and utility segment of the United States PVC pipes market.

Founded in 1951 and headquartered in Oakville, Ontario, IPEX Inc. is a leading North American manufacturer of thermoplastic piping systems including PVC, CPVC, ABS, and polyethylene products for plumbing, electrical, and industrial applications. The company operates manufacturing facilities across Canada and the United States, supplying residential and commercial plumbing systems, industrial process piping, and electrical conduit through a wide distribution network. IPEX's broad product portfolio, strong relationships with plumbing contractors, and consistent quality standards make it a key competitor in the plumbing and electrical segments of the United States PVC pipes market.

Other key players in the United States PVC pipes market are Charlotte Pipe and Foundry, Silver-Line Plastics LLC, Diamond Plastics Corp., Cantex Inc., Cresline Plastic Pipe Co. Inc., and others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock the full potential of your strategy with the most comprehensive analysis of the United States PVC pipes market 2026. Access detailed data on infrastructure investment trends, application-level demand forecasts, competitive dynamics, and regional growth opportunities across America's evolving piping landscape. Whether you are a manufacturer, distributor, contractor, or investor, this report delivers the clarity and evidence you need. Download your free sample today and explore the growth opportunities shaping the United States PVC pipes sector.

Central America PVC Pipes Market

India Ductile Iron Pipes Market

Latin America PVC Pipes Market

North America PVC Pipes Market

Saudi Arabia PVC Pipes Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

At 2025, the market reached an approximate volume of 3.90 Million Tons.

The market is projected to grow at a CAGR of 3.90% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach 5.72 Million Tons by 2035.

Key strategies driving the market include investing in high-grade materials, partnering with agri-tech firms, targeting smart retrofits, expanding recycling capabilities, and aligning with federal infrastructure schemes to meet evolving B2B and regulatory expectations.

The key trends of the market include the increasing use of new technologies, growth of the construction sector, and rising use in electrical conducting.

Polyvinyl chloride (PVC) pipes are pipes that are made of PVC, synthetic plastic polymers that are the chlorinated form of hydrocarbon polymer and used in a wide variety of applications.

PVC pipes are made of polyvinyl chloride and are considered to be stronger and more suited for trenchless installations while HDPE pipes are made of high density polyethylene and are more suitable for low pressure applications.

The various applications of PVC pipes in the market include irrigation, water supply, sewerage, plumbing, HVAC, and oil and gas, among others.

PVC pipes are important due to their ability to work well with high-pressurised water, and their suitability for drainage systems and underground plumbing.

JM Eagle Inc, Shintech Inc., Dura-Line LLC, IPEX Inc., Charlotte Pipe and Foundry, Silver-Line Plastics LLC, Diamond Plastics Corp., Cantex Inc., Cresline Plastic Pipe Co., Inc., and Others.

The key challenges are volatile resin costs, tightening EPA emission norms, and competition from alternative materials like HDPE and PEX.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Application |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.