Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

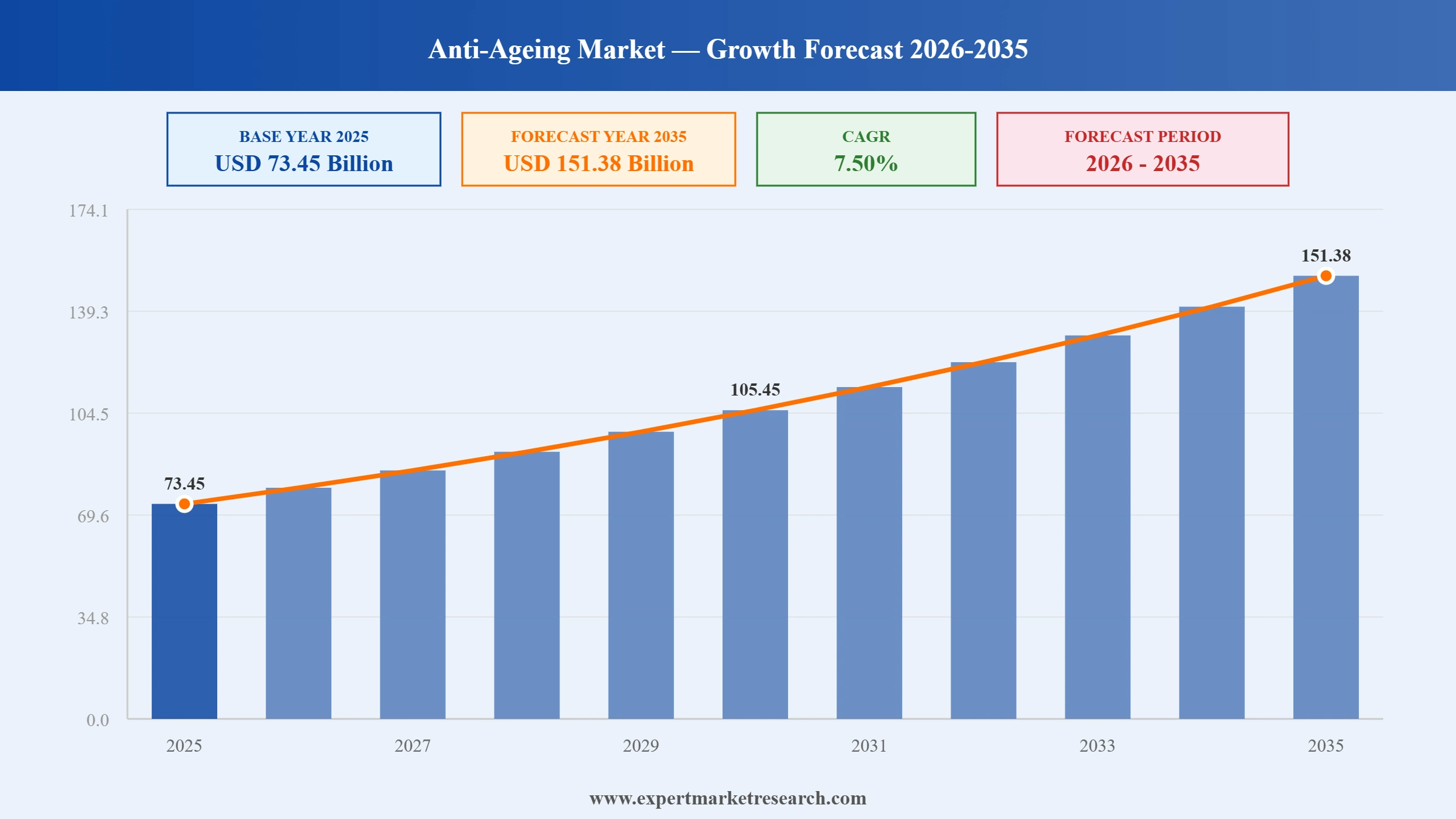

The global anti-ageing market reached a value of USD 73.45 Billion at 2025 and is projected to expand at a CAGR of around 7.50% during the forecast period of 2026-2035. With longevity-led skincare innovation, rapid uptake of injectables and dermal fillers, growing demand for energy-based aesthetic devices, and the rise of personalised regimens, the market is expected to reach USD 151.38 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Global Anti-Ageing Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 73.45 |

| Market Size 2035 | USD Billion | 151.38 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 7.50% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 8.6% |

| CAGR 2026-2035 - Market by Country | India | 9.9% |

| CAGR 2026-2035 - Market by Country | China | 8.3% |

| CAGR 2026-2035 - Market by Industry | Dental Care Industry | 9.0% |

| CAGR 2026-2035 - Market by Product Type | Anti-Wrinkle Products | 8.4% |

| Market Share by Country 2025 | France | 3.1% |

The global anti-ageing market is being reshaped by four converging forces - longevity-led product science, rapid scaling of injectable and energy-based aesthetic procedures, the consumerisation of clinical-grade devices, and ingredient personalisation supported by digital skin-analysis tools.

Allergan Aesthetics, an AbbVie company, presented new clinical data across its on-market and emerging facial-injectable portfolio at the IMCAS World Congress 2026 in Paris. The headline asset, TrenibotulinumtoxinE (TrenibotE), is a fast-acting, short-duration neurotoxin under FDA review, designed to deliver visible glabellar-line correction within roughly eight hours and dissipate in two to three weeks - a meaningful shift from longer-acting toxins. Commercial launch is targeted for 2026, expanding consumer entry points into injectable anti-ageing.

At CES 2026 in Las Vegas, L'Oréal Groupe unveiled two breakthrough infrared-light innovations targeting visible signs of ageing across hair and skin. The launches build on the company's longevity-led strategy first disclosed in 2025 and bring near-infrared treatments developed with partner I-Smart Developments closer to mainstream consumer use. The devices reflect the broader pivot of legacy beauty leaders towards clinical, technology-validated rejuvenation tools that move beyond traditional creams and serums, deepening L'Oréal's competitive position in the premium anti-ageing device segment.

L'Oréal disclosed an expansive longevity research programme designed to extend skin healthspan, supported by stabilised vitamin C, PDRN acting at a mitochondrial level, and new Mexoryl actives that address deep cellular changes. The company confirmed a March 2026 Lancôme launch built around Swiss biotech Timeline's Mitopure technology, alongside the Cell Bioprint diagnostic device that began rolling out at Lancôme counters in 2026. The strategy aims to move anti-ageing from cosmetic correction toward measurable biological intervention.

Beiersdorf rolled out NIVEA Cellular Epigenetics Age Rewind Face Serum featuring Epicelline, a proprietary actives platform targeting epigenetic markers of skin ageing. The launch followed Beiersdorf's broader 'longevity bet' strategy and complements its earlier 2024 partnership with Rubedo Life Sciences focused on cellular ageing. The serum positions the mass-prestige NIVEA franchise inside the science-led anti-ageing segment historically dominated by luxury brands and signals a competitive widening of the longevity claim across price tiers.

L'Oréal announced the acquisition of Gowoonsesang Cosmetics and its leading Korean skincare brand Dr.G from Swiss retailer Migros, with Dr.G earmarked for L'Oréal's Consumer Products Division. The deal expands L'Oréal's prestige-adjacent anti-ageing footprint in Korea - a globally significant beauty-innovation hub - and reinforces the group's K-beauty pipeline. Korean skincare's emphasis on early-intervention anti-ageing aligns with the longevity narrative and gives L'Oréal a defensive position against rising independent K-beauty competitors.

The category is shifting from cosmetic correction to measurable biological intervention. Major houses now invest in mitochondrial activators, senolytics, peptides such as PDRN, and epigenetic modulators that claim to extend skin healthspan rather than mask wrinkles. This recasts anti-ageing as a wellness category and supports premium pricing. In January 2025 L'Oréal launched Cell Bioprint at CES - described as a 'skin ageing clock' - diagnosing personal longevity pathways at counter level. The global anti-ageing market growth is therefore tightly linked to ingredient-science credibility.

Lasers, intense pulsed light (IPL), radiofrequency, ultrasound and at-home LED masks are moving from specialist clinics to mass-prestige and direct-to-consumer use. Devices now combine multiple energy modalities and are increasingly marketed for collagen stimulation and pigmentation control. In January 2026, L'Oréal unveiled near-infrared and red-light beauty-tech devices at CES 2026, developed with I-Smart Developments. The launch typifies how legacy beauty groups are entering the device segment historically dominated by medtech firms.

The injectable segment is broadening beyond traditional Botox-style neurotoxins. Allergan's TrenibotulinumtoxinE (TrenibotE), under FDA review and showcased at IMCAS 2026, offers visible results in roughly eight hours with a two-to-three-week effect window - appealing to first-time users and event-driven consumers. Galderma is parallel-developing longer-duration filler platforms. This dual-track innovation broadens the addressable consumer base and supports continued growth in anti-wrinkle injectables.

Longevity claims, once exclusive to luxury and dermo-cosmetic brands, are migrating into mass-prestige lines. NIVEA's Cellular Epigenetics Age Rewind Serum (launched September 2025) places epigenetic actives at accessible price points, broadening category penetration. The trend signals a structural shift: ingredient-science credibility is now table-stakes across price tiers, raising the bar for R&D investment among smaller players and accelerating premiumisation across anti-ageing skincare.

Global Anti-Ageing Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

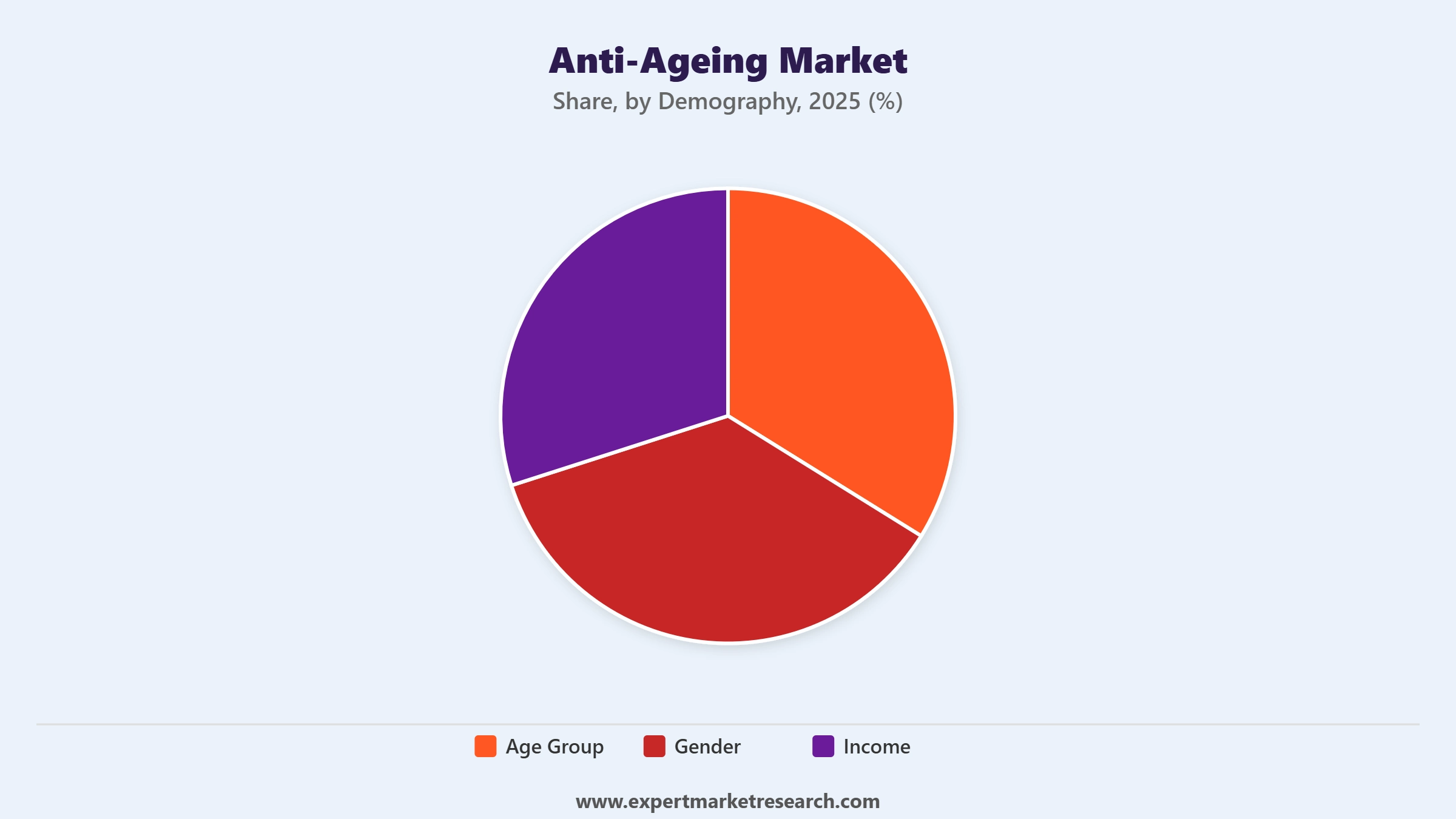

Market Breakup by Demography

Key Insights: Demographics is a foundational lens because purchase behaviour shifts sharply by life stage. Consumers in the 35–54 age band remain the largest absolute spenders on anti-wrinkle and anti-pigmentation products, but the 18–34 cohort drives volume growth as preventive skincare and early-intervention regimens (so-called 'pre-juvenation') become normalised. Income-segmented premiumisation is most visible in dermal fillers and energy-device treatments. Male grooming is the fastest-rising gender sub-segment, supported by widening clinic acceptance and discreet at-home tools.

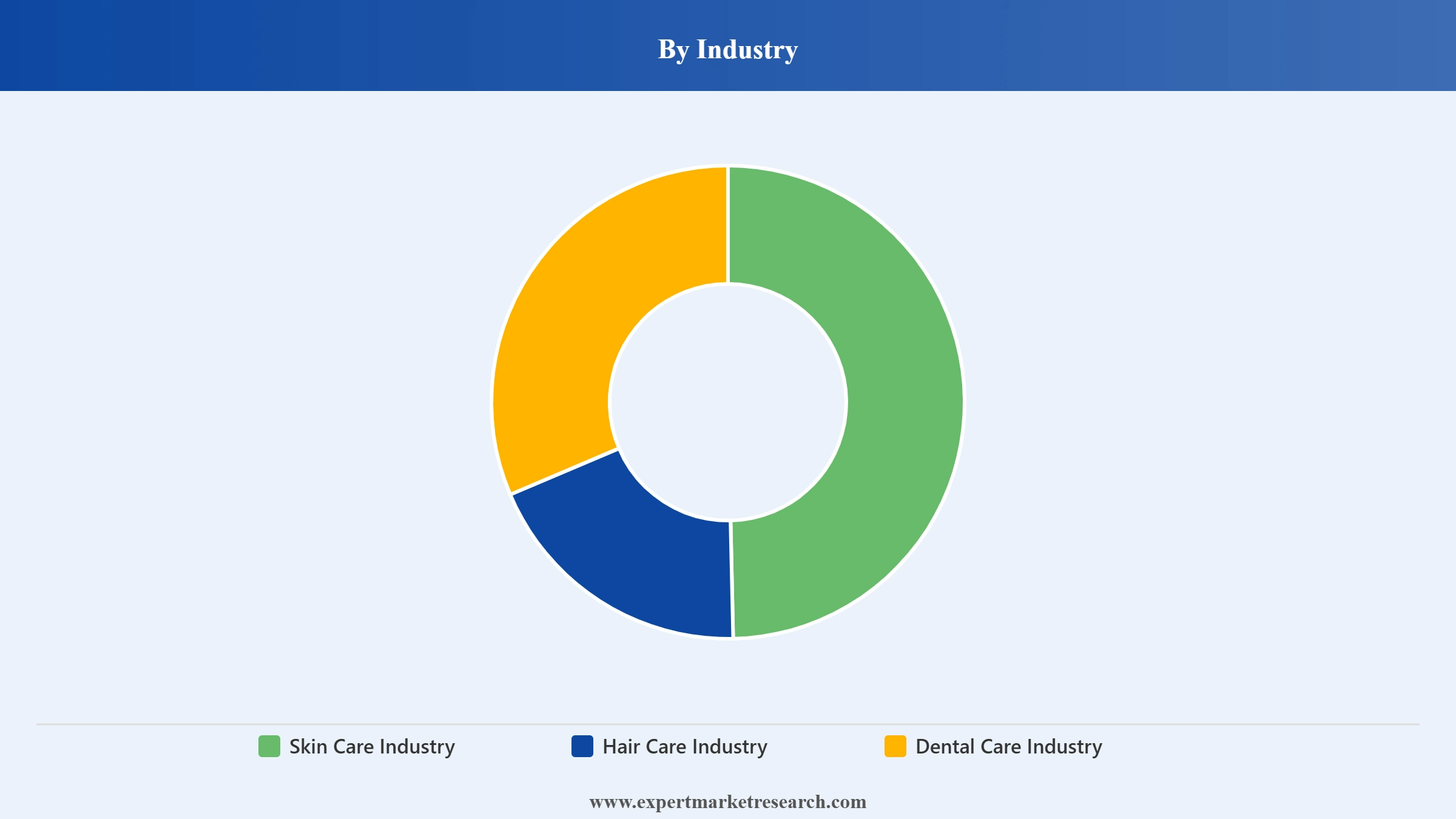

Market Breakup by Industry

Key Insights: Skin care remains the dominant industry vertical, accounting for the bulk of anti-ageing spend through cleansers, serums, creams, and clinical procedures. Hair care is the second-largest band, driven by anti-hair-fall, hair-colour, and hair-gain solutions. Dental care (teeth whitening, restorative aesthetics) is smaller but growing as cosmetic dentistry becomes destigmatised. Crossover formulations - for example scalp-microbiome and follicular-rejuvenation products - blur category lines and create whitespace for innovation-led entrants.

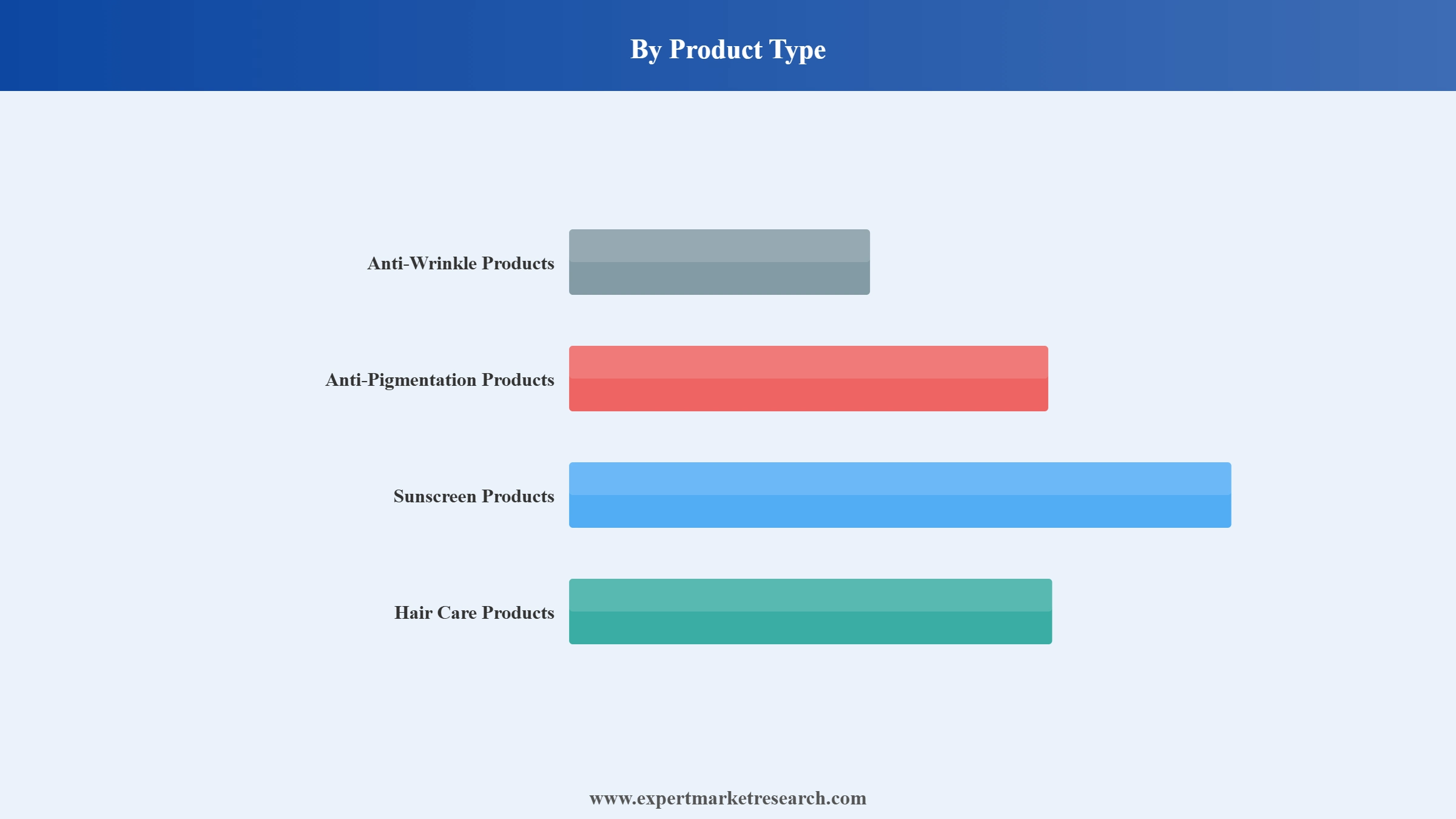

Market Breakup by Product Type

Key Insights: Anti-wrinkle products lead by revenue, with botulinum toxin A injections (Botox, Dysport, Xeomin, Daxxify) and hyaluronic-acid dermal fillers driving clinic traffic. Sunscreen has the broadest demographic reach because it functions as both protection and prevention, while anti-pigmentation creams and chemical peels are growing fastest in Asia Pacific. Hair-care anti-ageing - particularly minoxidil-alternatives, peptide serums, and at-home red-light devices - is a key whitespace category.

Market Breakup by device and technology

Key Insights: Aesthetic energy devices are the fastest-growing segment due to rising demand for non-invasive cosmetic treatments. Laser and IPL devices lead in skin rejuvenation and hair removal applications, while radio frequency and ultrasound devices are gaining popularity for skin tightening and body contouring procedures. Microdermabrasion devices continue to see steady demand for exfoliation and anti-aging treatments across clinics and beauty centers.

Market Breakup by Region

Key Insights: North America remains the largest regional market by spend, anchored by the United States' large injectable and clinical-aesthetics base, FDA-cleared device pipeline, and dense medspa network. Europe leads in dermo-cosmetic and luxury skincare exports, with France, Germany, Italy and the UK as anchor markets. Asia Pacific is the fastest-growing region, propelled by China, Japan, Korea, and India through K-beauty innovation, rising disposable income, and local aesthetic-clinic chains. Latin America (Brazil, Mexico) is gaining ground via cosmetic-tourism and Middle East and Africa is seeing rapid adoption in GCC capitals.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Demography: The 35–54 age band remains the dominant share holder in the demography segment, broadly accounting for over a third of category revenue, because this cohort actively addresses wrinkles, pigmentation, and volume loss while having peak purchasing power. The supporting evidence is the rapid scale-up of clinic-based procedures aimed at this age band: Allergan's IMCAS 2026 presentation reaffirmed that women aged 35–55 account for the majority of US neurotoxin and filler volumes, and the company's pipeline is calibrated to retention in this band.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Industry: Skin care holds the dominant industry share, reflecting daily-use frequency, broad demographic reach, and the bulk of innovation pipelines. Major groups disclose the highest R&D intensity inside skincare. The supporting evidence is L'Oréal's December 2025 commitment to longevity science - including the March 2026 Lancôme x Timeline Mitopure launch - and the 2024–2026 wave of mass-prestige longevity launches such as NIVEA's Epicelline serum, both of which sit squarely inside skincare and reinforce that vertical's dominance.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Product Type: Anti-wrinkle products dominate by revenue, led by botulinum toxin A injections and hyaluronic-acid dermal fillers. The supporting evidence is the steady commercial pipeline at the leading aesthetics firms: Allergan's TrenibotE, Galderma's longer-duration filler platforms, and Merz's AI-guided injection trials all centre on the anti-wrinkle segment, confirming category leadership and the willingness of incumbents to invest most heavily here.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America: The region remains the anchor of global anti-ageing demand because of its mature medspa network, dense aesthetics-clinic footprint, and a regulator (FDA) actively clearing new neurotoxins, fillers, and energy-based devices. Demand is supported by rising acceptance of preventive injectables among younger consumers and steady product innovation from Allergan Aesthetics, Galderma and Merz. M&A and pipeline activity continue to concentrate here; AbbVie's January 2026 IMCAS data drop on TrenibotE - targeted for 2026 US launch - illustrates how the region absorbs first-in-class assets first. Companies are also expanding consumer-direct device channels, supporting category premiumisation in the United States and Canada.

Asia Pacific: The fastest-growing regional market, supported by rising disposable incomes, the global influence of K-beauty, expanding aesthetics-clinic chains in China, Japan, Korea, and India, and proactive cross-border e-commerce. Korean innovation continues to set ingredient and format benchmarks; L'Oréal's December 2024 acquisition of Dr.G from Migros' Gowoonsesang business exemplifies how multinationals are using M&A to access the K-beauty pipeline. Japanese consumers favour high-tech device-led regimens, while India and Southeast Asia drive volume growth through mass-prestige skincare and growing male-grooming uptake. Investment is flowing into local clinic chains and contract-manufacturing capacity across the region.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global anti-ageing market is moderately consolidated at the top, with the top five beauty groups capturing a meaningful share of branded skincare revenues, while the injectable and device segments are concentrated among a few specialist majors. Competitive priorities have shifted from category extension toward longevity claims, ingredient differentiation, M&A in K-beauty, and direct-to-consumer device launches.

The next layer is dynamic: regional players, indie K-beauty brands, and medtech start-ups continue to take share through ingredient transparency, social-media reach, and physician-distributed channels. Multinationals respond with venture funds (Beiersdorf's €100M skincare VC fund), bolt-on M&A, and co-development deals with biotech partners - making the second tier a meaningful innovation engine rather than a fringe.

Founded 1909 and headquartered in Clichy, France, L'Oréal is the world's largest pure-play beauty group with operations across mass, prestige, professional and active-cosmetics divisions in 150+ countries. Its anti-ageing strength sits in Lancôme, La Roche-Posay, Vichy, Kiehl's and the Aesop and Dr.G additions, plus the L'Oréal Research & Innovation pipeline investing in longevity actives, beauty-tech devices, and AI-led personalisation.

Founded 1882 and headquartered in Hamburg, Germany, Beiersdorf operates Eucerin, NIVEA, La Prairie, Aquaphor and Chantecaille. Its anti-ageing footprint spans mass-prestige to luxury and is supported by a €100M skincare venture fund and a Rubedo Life Sciences cellular-ageing partnership. The September 2025 launch of NIVEA Cellular Epigenetics Age Rewind Serum signals a deliberate move into longevity claims at accessible price points across European, Asian and Latin American markets.

Founded 1946 and headquartered in New York, USA, Estée Lauder Companies operates Estée Lauder, Clinique, La Mer, Bobbi Brown, MAC, Aveda, Origins and a luxury-led prestige portfolio. Its 2025 collaboration with Serpin Pharma to explore SERPIN-protein technologies for inflammation and skin longevity reflects the group's strategy of integrating biotech partnerships into anti-ageing portfolios. Strong department-store and travel-retail distribution underpins global reach.

Founded 1837 and headquartered in Cincinnati, USA, P&G operates the Olay, SK-II, Pantene Pro-V, and Native franchises with deep penetration across mass and masstige anti-ageing skincare. Olay's Retinol24 and Regenerist Collagen Peptide ranges anchor the group's anti-ageing claim, while SK-II maintains a dominant position in Asia Pacific premium anti-ageing through Pitera essence and ritual-based regimens.

Other key players in the market are Unilever, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Discover the latest insights on the global anti-ageing market 2026 with our comprehensive report. Stay ahead of the curve with verified data on longevity-led product launches, injectable and device pipelines, regional growth dynamics, and the strategies of L'Oréal, Beiersdorf, Estée Lauder, P&G and Unilever. Whether you are launching a longevity skincare line, expanding aesthetics-clinic operations, or evaluating an acquisition target, this report delivers the clarity required. Download your free sample now and unlock the most material opportunities in the thriving global anti-ageing space.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

At 2025, the market reached an approximate value of USD 73.45 Billion.

The market is projected to grow at a CAGR of 7.50% between 2026 and 2035.

The market is projected to grow significantly during the forecast period 2026-2035 to reach USD 151.38 Billion by 2035.

Growth is driven by the mainstreaming of longevity-led skincare science (e.g., mitochondrial and epigenetic actives), the broad consumerisation of injectables and energy-based devices, rising preventive-skincare adoption among under-35s, expanding aesthetics-clinic networks in Asia Pacific, K-beauty-led ingredient innovation, and continuous M&A and biotech partnerships among incumbents such as L'Oréal, Beiersdorf and Estée Lauder.

The market is segmented by Age Group, Gender and Income. The 35–54 age band remains the largest spender; the 18–34 cohort is the fastest-growing through preventive 'pre-juvenation' regimens; and male grooming is rising sharply across both clinic and at-home formats.

Longevity science reframing the anti-ageing claim; mainstreaming of energy-based aesthetic devices in clinics and at home; faster, shorter-duration neurotoxins entering the pipeline; and longevity claims migrating from luxury into mass-prestige skincare.

The key players in the market include L'Oréal S.A., Beiersdorf AG, The Estée Lauder Companies Inc., Procter & Gamble, and Unilever.

North America, Europe, Asia-Pacific, Latin America, the Middle East, and Africa are the major regions covered in the market report.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Demography |

|

| Breakup by Industry |

|

| Breakup by Product Type |

|

| Breakup by Devices and Technology |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.