Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

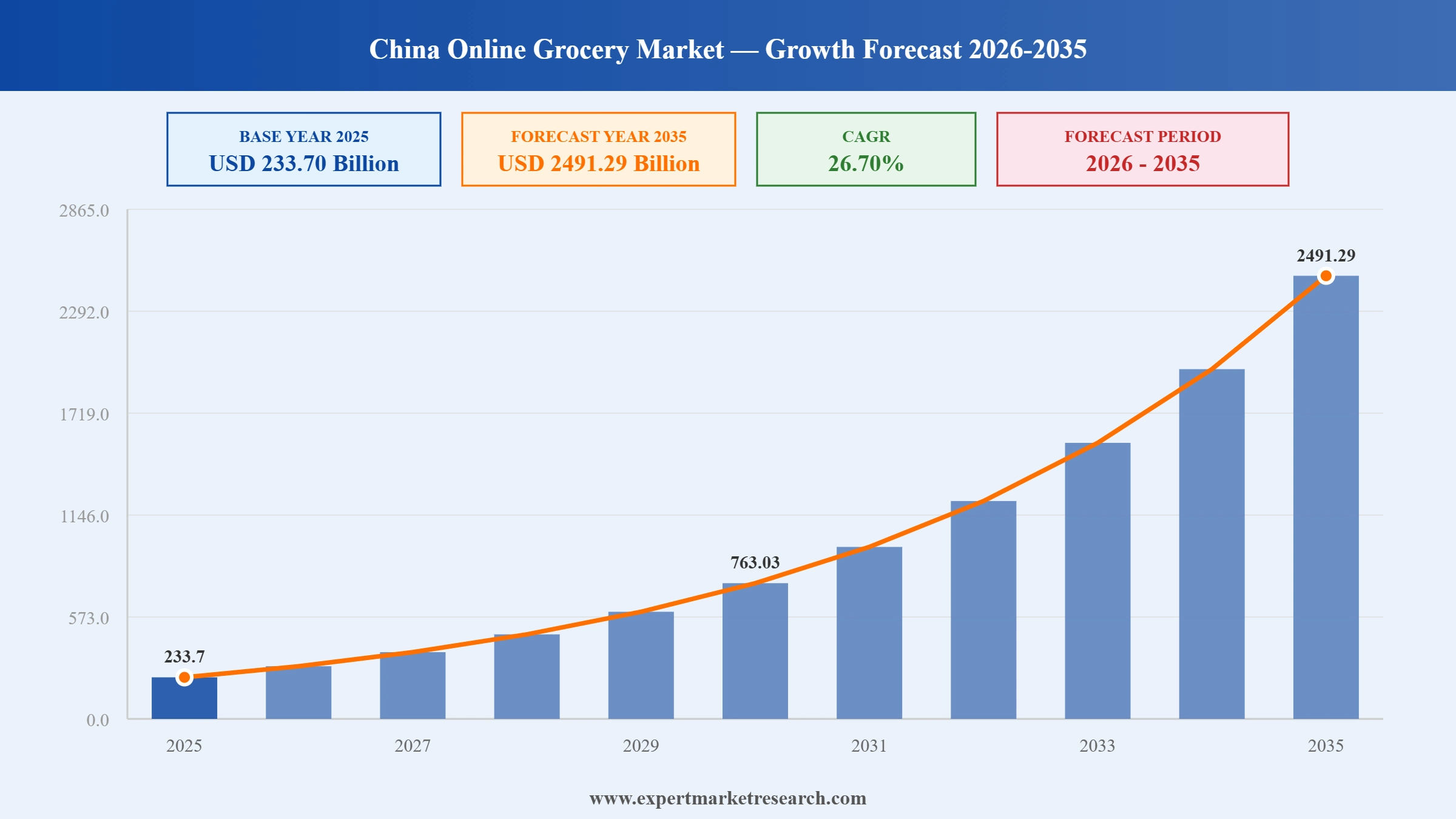

The china online grocery market reached a value of USD 233.70 Billion at 2025 and is projected to expand at a CAGR of around 26.70% during the forecast period of 2026-2035. With surging demand from tier III and IV cities supported by government-backed rural digitisation programmes, rapid scaling of front-end warehouse instant delivery infrastructure by Alibaba's Hema, JD.com's 7Fresh, and Meituan, accelerating mobile app-driven grocery ordering across all urban tiers, and growing consumer preference for fresh produce and grocery staples delivered to the door within 30 minutes, the market is expected to reach USD 2491.29 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The china online grocery market is experiencing a period of rapid structural expansion driven by platform giants' aggressive investment in instant retail infrastructure, the proliferation of front-end warehouse networks, and intensifying competition among Alibaba, JD.com, and Meituan for grocery delivery market share. Government rural digitisation support, AI-driven inventory management, and live commerce integration are collectively transforming online grocery from an urban premium service into a mass-market convenience across all Chinese city tiers.

Alibaba's Hema Freshippo (also known as Hema Xiangsheng) announced plans to reach a total of 500 stores across China in 2026, with 100 new store openings planned across 50 new cities, significantly expanding its omnichannel fresh grocery retail footprint. Each Hema store serves as both a retail destination and a front-end fulfillment hub for 30-minute home delivery within a 3 kilometre radius. The expansion directly reinforces the dominance of organised grocery players in the china online grocery market, shifting consumption from traditional wet markets to technology-enabled fresh grocery platforms.

China's instant retail industry achieved a significant operational milestone with major platforms including Alibaba's Taobao Instant Commerce expanding their front-end warehouse networks to carry up to 15,000 SKUs per location, comparable to a full supermarket product range. These warehouses, stocked close to residential areas and delivering through app-based ordering in under 30 minutes, are becoming the dominant grocery fulfillment model for urban Chinese consumers. The expansion dramatically broadened the china online grocery market's addressable product categories beyond staples into fresh produce, premium foods, and household essentials.

JD.com launched 7Fresh Kitchen, a distinctive new grocery and meal delivery model that develops signature dishes in partnership with food brands and restaurant partners, innovating the supply chain model for fresh food delivery in China. The initiative positioned JD.com's 7Fresh grocery brand as a differentiated competitor to Alibaba's Hema by combining fresh grocery delivery with meal kit and ready-to-eat formats. The launch directly strengthened JD.com's position in the high-frequency fresh produce and grocery segment of the china online grocery market.

JD.com officially launched its food delivery and on-demand retail service nationwide in February 2025, with founder Liu Qiangdong personally participating in a publicity delivery to mark the launch. JD.com pledged RMB 10 billion to support high-quality restaurant partners through its "Double Hundred" initiative. The entry of JD.com into the food and grocery delivery space intensified competition with Meituan and Alibaba's Taobao Flash Sales and Ele.me, creating a three-platform competitive dynamic that is accelerating service quality improvements and consumer subsidy programmes in the china online grocery market.

China's government-backed rural e-commerce and digitisation programmes are systematically expanding online grocery access into tier III and IV cities that previously lacked reliable delivery infrastructure. State subsidies for rural logistics network development, digital payment infrastructure, and cold chain investments are enabling major platforms including JD.com, Alibaba, and Meituan to extend services into hundreds of new cities annually. This rural expansion represents the most significant new growth frontier for the china online grocery market, with tier III and IV city consumers representing an enormous untapped addressable market.

China's leading online grocery platforms are deploying AI-driven inventory forecasting and demand planning systems across their front-end warehouse and dark store networks to minimise fresh produce waste, optimise restocking cycles, and reduce delivery lead times. Alibaba's Hema uses proprietary demand AI models embedded across its 400+ store network, achieving private label sales representing 35% of total revenues. JD.com's Jingdong Metabrain AI platform processes real-time order data across its supply chain, supporting the china online grocery market's expansion into perishable and temperature-sensitive categories.

The integration of livestream commerce into grocery purchasing is a distinctly Chinese phenomenon that is generating significant incremental revenue for online grocery platforms. Taobao Live, JD.com, and Pinduoduo all facilitate grocery purchasing through livestream product demonstrations, flash promotions, and celebrity or KOL-hosted sales events. Producers from major agricultural regions including Guangdong, Jiangsu, and Shanghai use livestreaming to connect directly with urban consumers, bypassing traditional distribution layers and driving premium pricing for local specialty produce in the china online grocery market.

Accelerating cold-chain infrastructure investment by Alibaba, JD.com, SF Express, and Dingdong Maicai is enabling the china online grocery market to expand into premium fresh, chilled, and frozen food categories that were previously limited to offline retail. JD Logistics has built a network of temperature-controlled warehousing facilities across major Chinese cities, supporting same-day fresh produce delivery with minimal quality deterioration. The expansion of reliable cold-chain last-mile delivery is a key structural enabler for the sustained multi-decade growth trajectory of fresh produce categories within the china online grocery market.

The report of the Expert Market Research's titled "China Online Grocery Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

Market Breakup by Type of Category

Key Insight: Grocery and Staples holds the largest category share of the china online grocery market, driven by habitual, high-frequency replenishment of essential household items including cooking oils, rice, noodles, condiments, beverages, and cleaning products through app-based platforms. Fruits and Vegetables is the fastest-growing category, supported by expanding cold-chain infrastructure enabling same-day fresh produce delivery. Alibaba's Hema Freshippo, which sources directly from agricultural suppliers for 30-minute delivery, has driven significant consumer acceptance of online fresh produce purchasing.

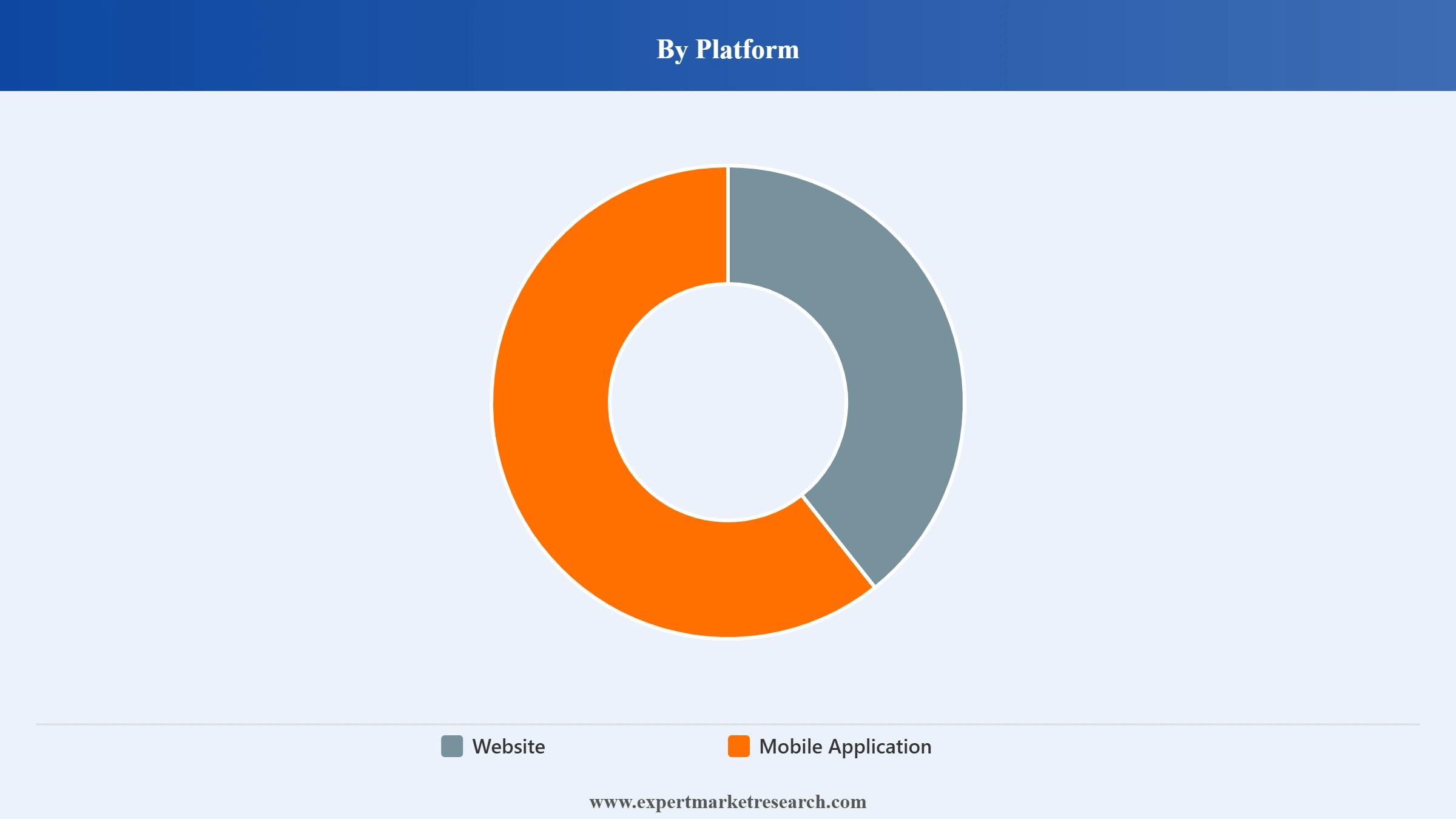

Market Breakup by Platform

Key Insight: Mobile Application dominates the china online grocery market platform segment, reflecting China's mobile-first digital commerce ecosystem where consumers conduct the vast majority of e-commerce activity through smartphone super-apps including Taobao, WeChat, JD.com, and Meituan. The seamless integration of grocery ordering within existing super-app ecosystems removes friction from purchase journeys. Alibaba's October 2025 expansion of front-end warehouses stocking 15,000 SKUs, all accessible via mobile, demonstrates the platform's dependency on mobile application infrastructure.

Market Breakup by Payment Method

Key Insight: Online payment methods including Alipay, WeChat Pay, and digital banking transfers dominate the china online grocery market, reflecting China's status as one of the world's most cashless consumer economies. Digital payment penetration in Chinese e-commerce exceeds 95%, with QR code-based payment infrastructure ubiquitous across urban and increasingly rural markets. Cash on Delivery maintains relevance in tier IV and rural markets where digital payment infrastructure or consumer confidence in online purchasing may be more limited, but its share is declining steadily.

Market Breakup by Region

Key Insight: Guangdong commands the largest regional share of the china online grocery market, driven by Guangzhou and Shenzhen's status as leading technology and commerce hubs, extremely high smartphone penetration, and dense logistics infrastructure supporting instant retail delivery networks. Shanghai is the second most significant market and the largest single-city online grocery market, benefiting from its affluent consumer base, high disposable income levels, and Alibaba Hema's original and largest concentration of Freshippo stores. Both cities are served by a dense network of front-end warehouses and dark stores.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Type of Category, grocery and staples accounts for the dominant share of the market due to the habitual, high-frequency replenishment needs of Chinese household consumers.

Grocery and staples including rice, cooking oil, condiments, snacks, beverages, and cleaning products generates the highest order volume and repeat purchase frequency in the china online grocery market, anchoring consumer platform loyalty. JD.com's Jingdong Supermarket and Alibaba's Taobao Supermarket both position themselves as the primary destination for household essential restocking. The high frequency of grocery replenishment purchases creates the most valuable consumer engagement loop for platforms, enabling cross-selling into higher-margin categories including fresh produce, premium foods, and personal care.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Fruits and Vegetables is the highest-growth category within the china online grocery market, enabled by cold-chain infrastructure advances and Alibaba Hema's farm-to-table sourcing model that delivers fresh produce within 30 minutes. China's food safety concerns and premium fresh produce demand among urban middle-class consumers are powerful demand drivers. Dingdong Maicai's achievement of small net profitability demonstrates that fresh produce delivery economics are improving, validating the category's long-term commercial viability in the china online grocery market.

By Platform, mobile application accounts for the dominant share of the market due to China's mobile-first digital commerce ecosystem and super-app integration.

Mobile applications dominate the china online grocery market platform segment with approximately 90% or more of grocery orders placed through smartphone interfaces. Alibaba's Taobao, JD.com, Meituan, and Pinduoduo Duo Duo Grocery all embed grocery ordering directly within their mobile super-apps, creating seamless purchase experiences tied to existing payment, loyalty, and social networking behaviours. Alibaba's February 2026 Hema Freshippo expansion plans targeting 500 total stores and 50 new cities are specifically designed to extend the instant delivery coverage area of the mobile ordering platform across China.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Website-based grocery ordering serves primarily business and institutional buyers in the china online grocery market who require procurement interfaces compatible with enterprise purchasing workflows, multi-user account management, and bulk order processing capabilities. JD.com's B2B enterprise grocery procurement offering supports corporate catering, office supplies, and institutional buying through its desktop platform. However, the proportion of total grocery GMV transacted via desktop websites continues to decline as mobile app functionality increasingly surpasses website capabilities for both individual and business consumers.

Guangdong dominates the China online grocery market due to its large affluent urban population, dense instant retail infrastructure, and status as the primary logistics and technology hub of southern China.

Guangdong accounts for the largest provincial share of the china online grocery market, driven by the combined consumer demand of Guangzhou, Shenzhen, Foshan, and Dongguan, encompassing one of the world's largest and most affluent urban agglomerations. Alibaba Hema Freshippo, Meituan Lightning Warehouses, and JD.com 7Fresh operate dense front-end warehouse networks throughout the Pearl River Delta, enabling 30-minute instant grocery delivery. The region's high technology industry employment base and elevated disposable incomes translate into above-average online grocery spending per household.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Shanghai represents the most mature and highest-value city within the china online grocery market, having been the original test bed for Alibaba's Hema Freshippo new retail concept launched there in 2016. Shanghai consumers exhibit the highest online grocery adoption rates in China, with Hema Cloud Supermarket delivering to 90% of cities nationally and achieving a significant proportion of orders from Shanghai's affluent residential neighbourhoods. Beijing is the second-largest city market and the home base for JD.com, whose 7Fresh grocery operations and extensive cold-chain logistics infrastructure give it strong competitive positioning in the capital city segment.

The china online grocery market is dominated by three technology conglomerates: Alibaba Group through Hema Freshippo and Taobao Instant Commerce, JD.com through 7Fresh and Jingdong Supermarket, and Meituan through its instant retail and flash grocery delivery platforms. These three platforms collectively command the majority of the market through substantial infrastructure investments in front-end warehouses, cold-chain logistics, and AI-powered inventory management. Competition is intensifying as JD.com's February 2025 national food delivery launch challenged the Meituan-Alibaba duopoly that had previously dominated on-demand grocery and food delivery.

Founded in 1999 and headquartered in Hangzhou, China, Alibaba Group Holding Ltd. operates China's largest online grocery platform through its Hema Freshippo (Hema Xiangsheng) fresh retail chain and Taobao Instant Commerce platform. In February 2026, Hema announced plans to open 100 new stores in 50 new cities, reaching a 500-store total in 2026. Alibaba's October 2025 expansion of Taobao Instant Commerce front-end warehouses stocking 15,000 SKUs per location further consolidated its dominant position in the china online grocery market.

Founded in 1998 and headquartered in Beijing, China, JD.com Inc. is China's largest retailer by revenue, operating the 7Fresh fresh grocery chain, JINGDONG Supermarket platform, and JD Logistics cold-chain network. In July 2025, JD.com launched 7Fresh Kitchen, a distinctive grocery and meal supply chain innovation model partnering with food brands to develop signature dishes. In February 2025, JD.com launched its nationwide food delivery service in direct competition with Meituan and Alibaba's Taobao Flash Sales, expanding its presence across the china online grocery market.

Founded in 1994 and headquartered in Seattle, Washington, Amazon.com Inc. operates in the China online retail market primarily through its cross-border e-commerce platform Amazon.cn, enabling Chinese consumers to purchase imported food products including premium imported grocery staples, health foods, and specialty international products. Amazon serves the premium imported food segment of the china online grocery market by leveraging its global supply chain to bring international brands to Chinese consumers seeking quality-assured imported grocery products not widely available through domestic platforms.

Miss Fresh is a China-based online fresh grocery delivery company operating a direct-to-consumer model focused on fresh produce, meats, seafood, dairy, and prepared foods delivered directly to consumers within urban Chinese cities. The company operates front-end dark store warehouses in key cities to enable fast, same-day delivery of temperature-sensitive grocery products. Miss Fresh targets the quality-conscious urban consumer segment of the china online grocery market, competing against Alibaba Hema and JD.com 7Fresh on produce freshness and cold-chain delivery reliability.

Other key players in the market are Meituan, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Tap into the extraordinary growth of the china online grocery industry from 2026 with our comprehensive market report. Explore category dynamics, platform competition, city-level growth strategies, instant retail infrastructure expansion, and the competitive battles reshaping China's grocery landscape. Whether you are an investor, platform operator, food manufacturer, or logistics provider, this report provides the intelligence you need. Download your free sample today and discover the key opportunities shaping the china online grocery industry through 2035.

Australia Online Grocery Delivery Market

India Online Grocery Market

Online Grocery Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the China online grocery market reached an approximate value of USD 233.70 Billion.

The market is projected to grow at a CAGR of 26.70% between 2026 and 2035.

Key strategies driving the market include investing in AI-driven stock forecasts, partnering with local farms, developing multi-platform access points, localizing warehousing, and leveraging livestream selling for B2B procurement.

The key challenges are high logistics costs, regulatory inconsistencies, and cold chain gaps in rural zones.

The market is mainly concentrated in Shanghai, Zhejiang, Guangdong, Jiangsu, and Beijing, among others.

The leading type of categories in the market are grocery and staples and fruits and vegetables, among others.

The market segmentations based on platform include website and mobile application.

The leading payment methods in the market are online and cash on delivery.

The key players in the China online grocery market include Alibaba Group Holding Ltd., JD.com Inc., Meituan, Miss Fresh, and Amazon.com Inc., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type of Category |

|

| Breakup by Platform |

|

| Breakup by Payment Method |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.