Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The global esports market reached a value of USD 2.43 Billion in 2025 and is projected to expand at a CAGR of around 16.40% during the forecast period of 2026-2035. Supported by escalating global viewership surpassing 640 million, surging sponsorship investments from both endemic and non-endemic brands, the rapid growth of mobile competitive gaming across emerging economies, and the expansion of professionalised league and tournament structures such as the Esports World Cup, the market is expected to reach USD 11.10 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Global Esports Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 2.43 |

| Market Size 2035 | USD Billion | 11.10 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 16.40% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 18.5% |

| CAGR 2026-2035 - Market by Country | India | 19.6% |

| CAGR 2026-2035 - Market by Country | China | 17.7% |

| CAGR 2026-2035 - Market by Revenue Streaming | Sponsorship | 18.4% |

| CAGR 2026-2035 - Market by Streaming Type | Live | 18.0% |

| Market Share by Country 2025 | Saudi Arabia | 2.1% |

The global esports market is undergoing significant transformation as multi-title global championship models attract record-setting investment, sovereign wealth funds reshape industry ownership through landmark acquisitions, and mobile esports drive participation growth across emerging markets. Simultaneously, nation-based competitive formats are being introduced at scale, creating parallels with traditional international sporting frameworks and opening new avenues for government-backed esports development.

The 2026 Esports World Cup, originally scheduled for Riyadh from July 6 to August 23 with a prize pool exceeding USD 75 million across 25 events in 24 game titles, reportedly communicated to stakeholders a relocation to Paris, France, due to regional instability caused by the 2026 Iran conflict. The EWC's Club Partner Program, now a USD 20 million initiative supporting 40 leading esports organisations, has distributed over USD 100 million to clubs globally over the past three years, reinforcing a sustainable financial structure for professional competitive gaming.

A consortium comprising Saudi Arabia's Public Investment Fund, Silver Lake, and Affinity Partners announced a definitive agreement to acquire Electronic Arts Inc. in an all-cash transaction valued at approximately USD 55 billion in September 2025, the largest all-cash sponsor take-private investment in history. PIF rolled over its existing 9.9% stake, positioning the deal to accelerate EA's gaming and esports innovation capabilities across its portfolio of titles including EA Sports FC, Apex Legends, and Madden NFL.

The Esports Foundation formally announced the inaugural Esports Nations Cup at the New Global Sport Conference in Riyadh in August 2025, introducing a nation-versus-nation competitive format featuring 16 game titles from publishers including Electronic Arts, Chess.com, Krafton, MOONTON Games, Tencent, and Ubisoft. Team competitions will involve 24 to 48 national teams per title, with the event scheduled for November 2 to 29, 2026, representing the first time a major esports competition has introduced a structured global national team system at scale.

The International Olympic Committee announced in October 2025 that it would end its partnership with the Saudi Arabian Olympic Committee for organising the Olympic Esports Games, after talks broke down between the IOC, the Saudi committee, and the Esports World Cup Foundation. The IOC intends to pursue an independent approach for the Olympic Esports Games, with potential host countries including Singapore and South Korea, while Saudi Arabia continues its competitive gaming agenda through the EWC and the Esports Nations Cup.

European esports organisation Team Vitality completed the acquisition of Indonesia's Bigetron Esports in May 2025, gaining competitive rosters across Mobile Legends: Bang Bang, PUBG Mobile, Honor of Kings, and Free Fire. The deal, rebranded as 'Bigetron by Vitality', extended Vitality's footprint into Southeast Asia, a region with over 100 million gamers in Indonesia alone and approximately 20% year-over-year mobile gaming revenue growth.

The Esports Foundation selected 40 premier esports organisations from five competitive regions for its 2026 Club Partner Program in March 2026, a USD 20 million initiative providing financial support to professional teams. The programme has cumulatively distributed over USD 100 million to clubs, stabilising the financial infrastructure of the global esports market and enabling teams to invest in player development, content creation, and cross-title competitive participation.

Gameloft launched a new mobile esports platform for Asphalt 9: Legends in March 2025, focusing on community-driven tournaments and competitive play. The initiative expanded the mobile esports ecosystem by offering regular in-app events, live streaming integration, and player rewards, broadening audience engagement across mobile racing enthusiasts worldwide.

The Esports Foundation revealed National Team Partner selections from over 630 applications across more than 100 countries in March 2026, establishing the first structured global national team system for esports. The inaugural competition is scheduled for November 2026 in Riyadh, featuring 16 titles across team and solo formats.

The Esports World Cup Foundation entered a three-year partnership with Epic Games in December 2025, securing Fortnite and Rocket League as featured EWC titles through 2028. Fortnite's return to the EWC will utilise the Reload game mode, while Rocket League continues as a competitive staple, reinforcing the breadth of genres represented in the global esports championship format.

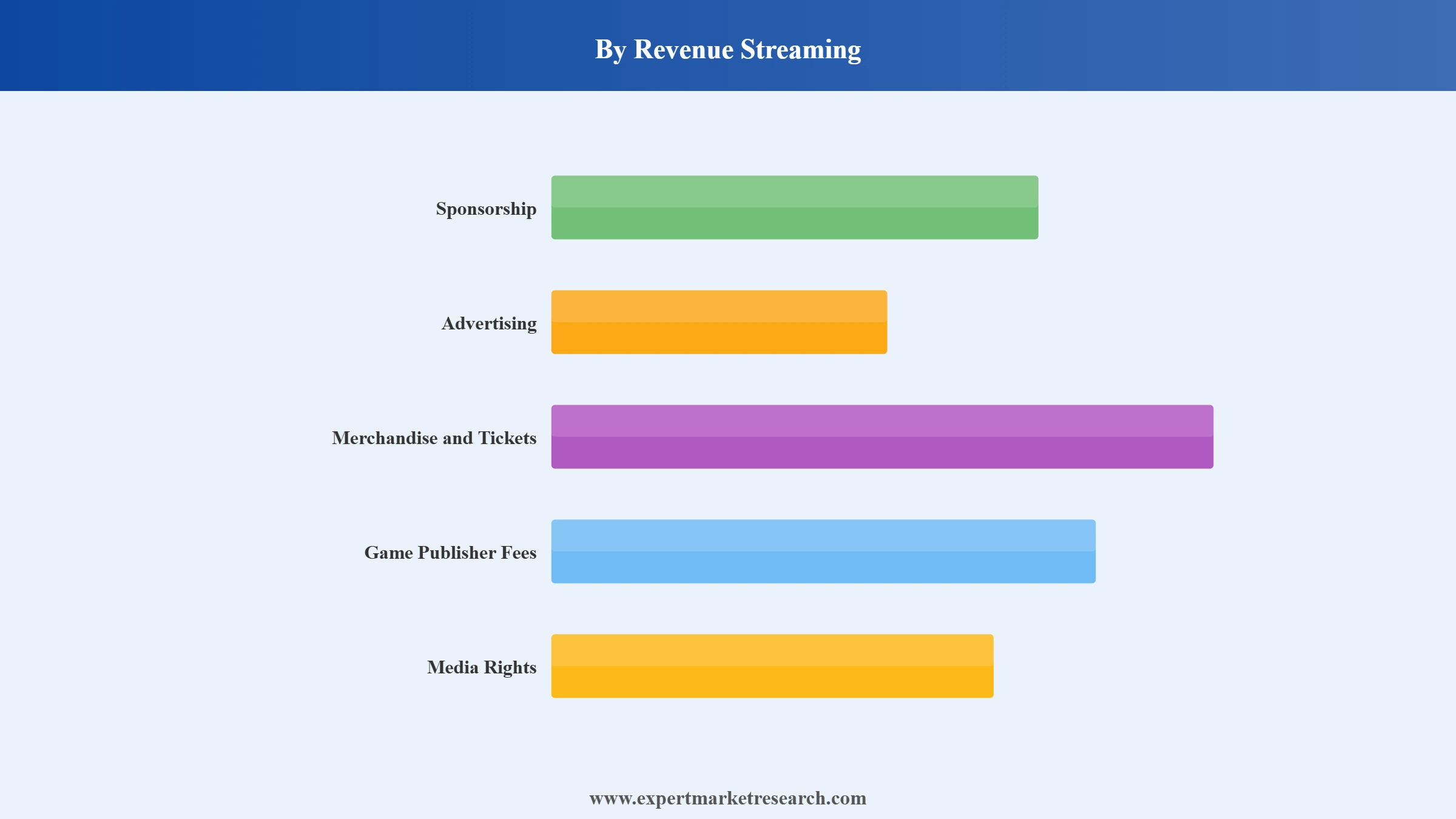

The report of Expert Market Research's titled "Esports Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:Key Insight: The sponsorship segment commands the dominant share of the esports market by revenue streaming, accounting for over 40% of total revenue, anchored by multi-year deals between professional teams, tournament organisers, and brands spanning technology, beverages, automotive, and lifestyle sectors. Major corporations recognise the high levels of viewer engagement and brand recall that esports events offer, with the Esports World Cup's Club Partner Program alone distributing over USD 100 million to participating organisations. Media rights are the fastest-growing revenue stream, as traditional broadcasters and streaming platforms compete for exclusive coverage of major tournament circuits, following the monetisation model of conventional sports broadcasting.

Market Breakup by Revenue Streaming

Key Insight: The sponsorship segment commands the dominant share of the esports market by revenue streaming, accounting for over 40% of total revenue, anchored by multi-year deals between professional teams, tournament organisers, and brands spanning technology, beverages, automotive, and lifestyle sectors. Major corporations recognise the high levels of viewer engagement and brand recall that esports events offer, with the Esports World Cup's Club Partner Program alone distributing over USD 100 million to participating organisations. Media rights are the fastest-growing revenue stream, as traditional broadcasters and streaming platforms compete for exclusive coverage of major tournament circuits, following the monetisation model of conventional sports broadcasting.

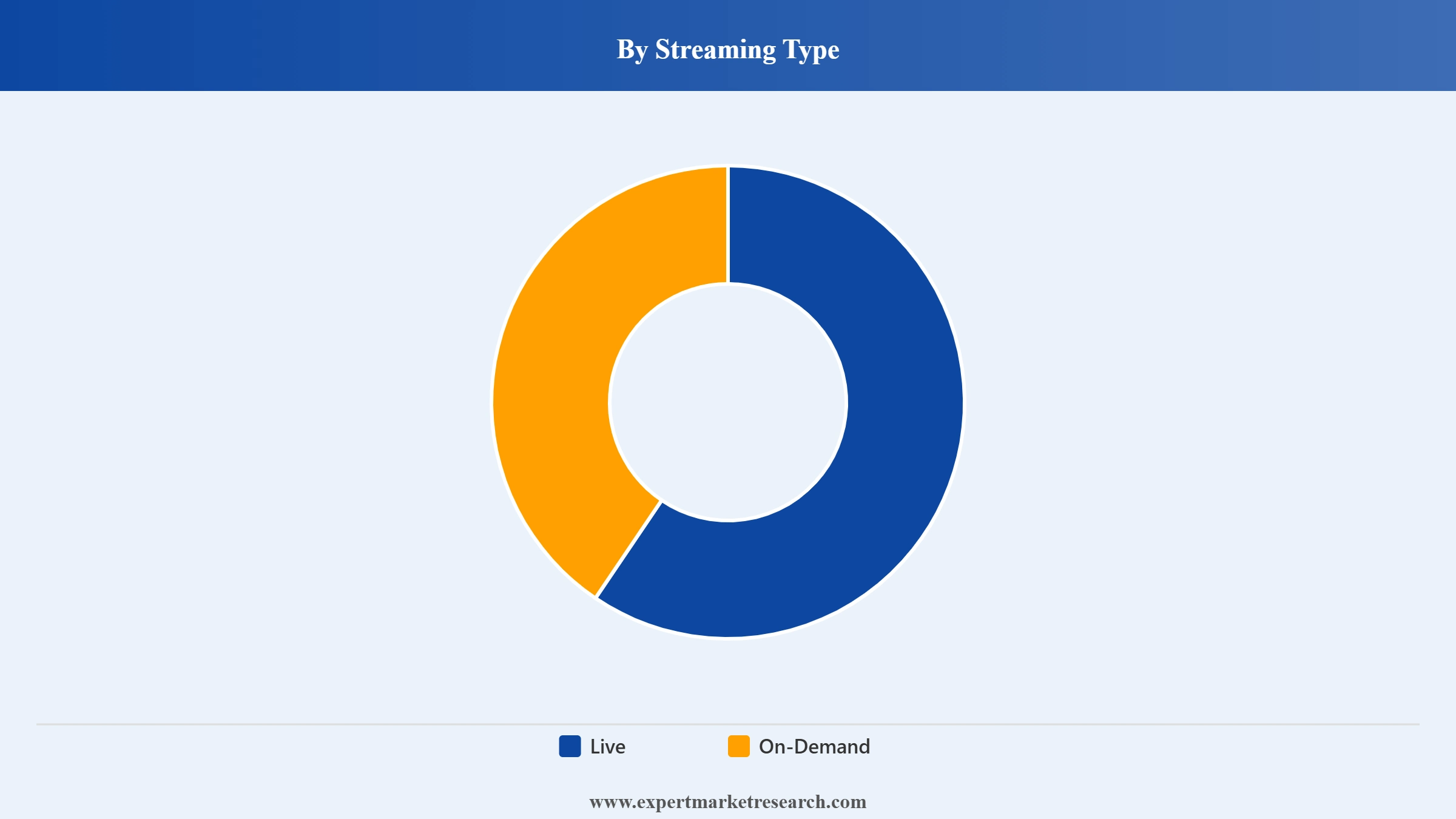

Market Breakup by Streaming Type

Key Insight: Live streaming holds the larger share of the esports market by streaming type, driven by the real-time nature of competitive matches that creates urgency and communal viewing behaviour, commanding higher advertising CPMs and sponsorship value. Platforms such as Twitch, YouTube Gaming, and AfreecaTV serve as primary distribution channels, with concurrent viewership for major tournaments regularly exceeding several million. On-demand content is the fastest-growing format, expanding through highlight reels, coaching content, player vlogs, and tournament replays that attract viewers preferring flexible consumption patterns.

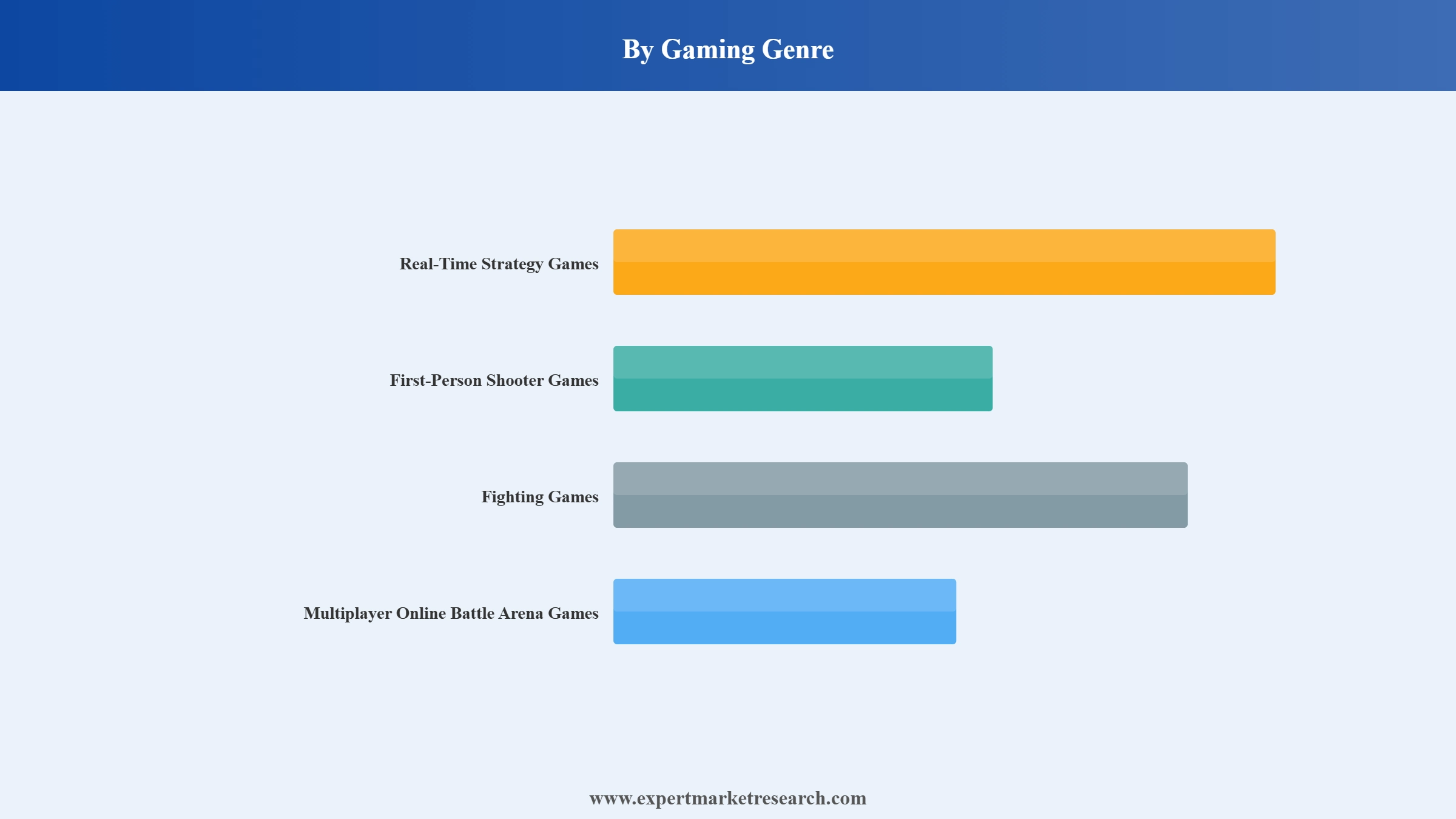

Market Breakup by Gaming Genre

Key Insight: Multiplayer online battle arena (MOBA) games represent the leading genre segment in the esports market, accounting for approximately 28.7% of global revenue, with titles such as League of Legends, Dota 2, and Honor of Kings anchoring the competitive ecosystem through deep strategic gameplay, well-established international tournament circuits, and massive community ecosystems. First-person shooter (FPS) games, including Valorant, Counter-Strike 2, and Call of Duty, are the fastest-growing genre segment, particularly in North America and Europe, driven by franchise league models and the rising popularity of tactical shooter formats in competitive play.

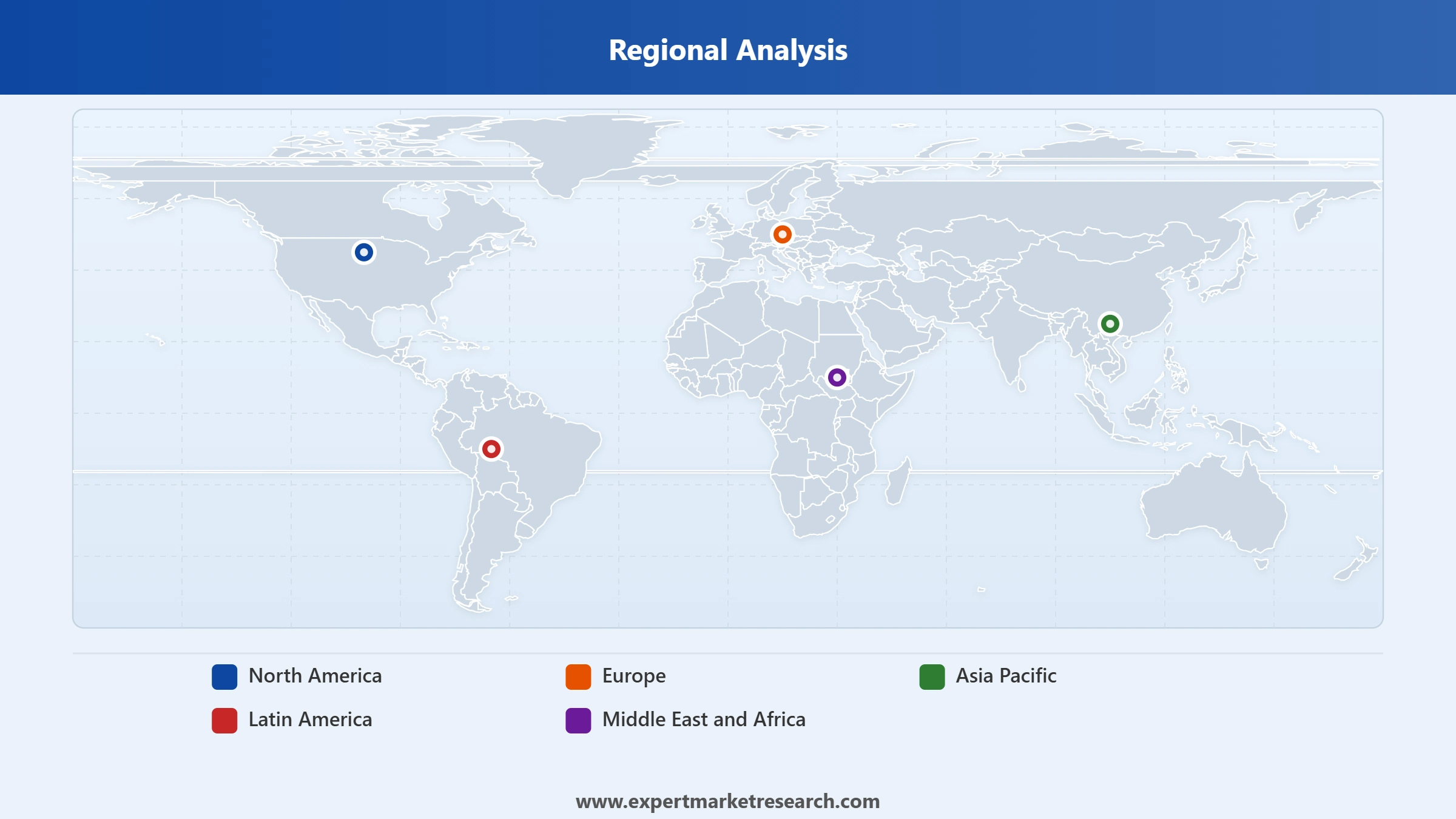

Breakup by Region

Key Insight: North America held the largest share of the esports market in 2025, accounting for approximately 35% of global revenues, driven by a well-developed digital infrastructure, the presence of major game publishers, and a mature sponsorship ecosystem. Asia Pacific is the fastest-growing regional market, propelled by massive gaming populations in China, South Korea, Japan, India, and Southeast Asian nations, combined with the rapid expansion of mobile esports. The Middle East and Africa region is experiencing transformational growth through strategic investments by the Saudi Arabian Public Investment Fund, including the Esports World Cup and the Esports Nations Cup.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Revenue Streaming, sponsorship accounts for the dominant share of the market due to growing brand investment in competitive gaming as a mainstream marketing channel

The sponsorship segment commands the dominant share of the esports market by revenue streaming, underpinned by the growing willingness of global brands to invest in competitive gaming to reach younger, digitally native audiences. Both endemic gaming companies and non-endemic brands across technology, beverages, automotive, and financial services sectors are signing multi-year partnership agreements with professional teams, tournament organisers, and individual content creators. The Esports World Cup's Club Partner Program, which has distributed over USD 100 million to 40 partner organisations over three years, exemplifies the scale of structured sponsorship investment flowing into the industry.

Media rights are emerging as the fastest-growing revenue stream within the esports market, as traditional broadcasters and digital platforms compete for exclusive coverage rights to high-profile tournament circuits. Advertising revenues continue to expand alongside rising viewership on platforms such as Twitch, YouTube Gaming, and regional streaming services in Asia. Merchandise and ticket sales, game publisher fees, and other revenue sources contribute to a diversified monetisation structure that insulates the industry from dependence on any single income stream.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Streaming Type, live streaming accounts for the dominant share of the market due to the real-time engagement dynamics of competitive esports content

Live streaming holds the larger share of the esports market by streaming type, driven by the immediacy and communal nature of watching competitive matches in real time. Live content generates higher advertising CPMs and sponsorship valuations compared to pre-recorded formats, as brands benefit from the unscripted excitement and social interaction that characterises tournament broadcasts. Platforms such as Twitch, YouTube Gaming, AfreecaTV, and Douyu collectively serve as the primary distribution channels, with concurrent viewership for top-tier events such as the League of Legends World Championship and Dota 2's The International regularly surpassing several million viewers.

On-demand content is the fastest-growing streaming type segment in the esports market, expanding through highlight compilations, coaching tutorials, player vlogs, post-match analysis, and full tournament replays. This format attracts viewers who prefer flexible consumption schedules and serves as an entry point for new audiences discovering competitive gaming. Content creators and professional players are leveraging on-demand platforms to build personal brands and generate supplementary revenue through subscriptions, donations, and advertising, further broadening the overall esports content ecosystem.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Gaming Genre, multiplayer online battle arena games account for the dominant share of the market due to deep strategic gameplay and massive global tournament ecosystems

MOBA games hold the largest share of the esports market by gaming genre, driven by the global popularity of League of Legends, Dota 2, and Honor of Kings, which collectively sustain the most-watched and highest-prize competitive circuits in esports. The League of Legends World Championship and Dota 2's The International attract millions of viewers annually, generating substantial sponsorship, media rights, and advertising revenue. Mobile MOBAs, particularly Honor of Kings and Mobile Legends: Bang Bang, are expanding the genre's reach across Asia Pacific and Latin America, where mobile-first gaming populations represent the primary growth demographic.

First-person shooter games are the fastest-growing genre segment in the esports market, led by Valorant, Counter-Strike 2, and Call of Duty, which have built structured franchise league models that provide year-round competitive programming. Fighting games, anchored by Street Fighter 6 and Tekken 8, maintain a loyal competitive community with strong representation at multi-title events including the Esports World Cup. Real-time strategy games continue to serve as foundational esports titles, particularly in South Korea, where StarCraft's legacy has shaped competitive gaming culture for over two decades.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Region, North America accounts for the dominant share of the market due to advanced digital infrastructure, established professional leagues, and strong corporate sponsorship ecosystems

North America continues to lead the global esports market, accounting for approximately 35% of global revenues in 2025. The region benefits from an advanced broadband infrastructure, the presence of major game publishers such as Riot Games, Activision, and Electronic Arts, and a mature sponsorship ecosystem. Professional leagues including the League of Legends Championship Series (LCS) and the Call of Duty League have established year-round competitive schedules that sustain viewer engagement and advertising revenues. Collegiate esports programmes are expanding rapidly across American universities, building a talent pipeline for the professional circuit.

Asia Pacific represents the fastest-growing regional market for esports, driven by massive gaming populations in China, South Korea, Japan, India, and Southeast Asian nations. China's esports ecosystem is bolstered by government support for digital entertainment and the growing popularity of mobile esports titles. India's esports market is witnessing rapid expansion, valued at approximately USD 248 million in 2025, with a projected CAGR of 18.80% driven by rising smartphone adoption and brand investment in gaming tournaments. Europe, Latin America, and the Middle East and Africa are each contributing to expansion, with Saudi Arabia's strategic investments through the Esports World Cup and the Esports Nations Cup positioning the Gulf region as a global esports hub.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global esports market features a diverse competitive landscape comprising game publishers, tournament organisers, streaming platforms, and professional team operators. Leading players are focused on expanding their intellectual property portfolios, securing multi-year broadcasting and sponsorship agreements, investing in mobile gaming to capture emerging market demographics, and building cross-platform competitive ecosystems. The sector is undergoing a structural shift as sovereign wealth fund-backed consortia reshape ownership dynamics through landmark acquisitions, while indigenous esports organisations in regions such as Southeast Asia, the Middle East, and Latin America are scaling through strategic partnerships and club programme participation.

Competitive priorities in the market include multi-title tournament development, mobile esports infrastructure investment, national team competition frameworks, and digital fan engagement innovation. The Esports World Cup's multi-game championship model and the incoming Esports Nations Cup are redefining how competitive gaming is organised at the international level, creating new revenue pools and audience acquisition channels for both publishers and team operators.

Tencent Holdings Ltd, founded in 1998 and headquartered in Shenzhen, China, is a global technology conglomerate and the world's largest gaming company by revenue. Through its full ownership of Riot Games, developer of League of Legends and Valorant, and stakes in numerous gaming studios worldwide, Tencent plays a central role in the global esports market. The company's games, including Honor of Kings and PUBG Mobile through its subsidiary Proxima Beta, anchor competitive gaming circuits across Asia, while Riot Games operates the League of Legends World Championship and the Valorant Champions Tour, two of the most prominent esports tournament circuits globally.

Electronic Arts Inc., founded in 1982 and headquartered in Redwood City, California, United States, is a leading publisher of sports and entertainment titles that support major esports competitions. EA Sports FC, Apex Legends, and Madden NFL form the backbone of its competitive gaming portfolio. In September 2025, EA entered into a definitive acquisition agreement with a consortium of Saudi Arabia's Public Investment Fund, Silver Lake, and Affinity Partners valued at approximately USD 55 billion, the largest all-cash sponsor take-private investment in history, expected to accelerate its esports and gaming innovation capabilities.

Riot Games, Inc., founded in 2006 and headquartered in Los Angeles, California, United States, is a subsidiary of Tencent Holdings and one of the most influential players in the global esports market. The company operates the League of Legends World Championship and the Valorant Champions Tour, two of the highest-profile competitive circuits. Valorant registered approximately 15% player growth in 2024-2025, and Riot's sustained investment in regional leagues across North America, Europe, and Asia has made it a defining force in professionalising competitive gaming.

CAPCOM Co., Ltd., founded in 1979 and headquartered in Osaka, Japan, is a leading game publisher renowned for its fighting game franchise Street Fighter. Street Fighter 6 has become a cornerstone title in the fighting game esports community, featured prominently in tournaments including the Esports World Cup and the Capcom Pro Tour. The company's focus on maintaining competitive integrity, regular gameplay updates, and organised tournament structures sustains its relevance across the global competitive gaming landscape.

Other key players in the market are Activision Publishing, Inc., Gameloft SE, Skillz Inc., Motorsport Games Inc., Gfinity PLC, HTC Corporation, and FACE IT LIMITED, among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock strategic clarity in the global esports market 2026 with our comprehensive research report. From sovereign wealth fund acquisitions reshaping industry ownership and the Esports World Cup's multi-title championship model to mobile esports growth across emerging economies and the Esports Nations Cup introducing national team competition at scale, this report delivers the intelligence you need to act with confidence. Whether you are evaluating esports sponsorship opportunities, planning competitive gaming investments, tracking industry consolidation, or benchmarking against leading publishers and tournament organisers, download your free sample today and discover the forces shaping the world's fastest-growing entertainment market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The global market for esports reached a value of USD 2.43 Billion in 2025.

The market is estimated to grow at a CAGR of 16.40% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035, to reach a value of USD 11.10 Billion by 2035.

The rising awareness about esports, increasing number of professional sports clubs penetrating the esports arena, and rising accessibility of smartphones are the major drivers of the market.

The key trends in the market include the emergence of cloud gaming, growing adoption of smartphones, and availability of high-speed internet networks.

Sponsorship, advertising, merchandise and tickets, game publisher fees, and media rights, among others, are the different revenue streaming of esports.

Live and on-demand are the different streaming types in the market.

Real-time strategy games, first-person shooter games, fighting games, and multiplayer online battle arena games, among others, are the various gaming genres in the market for esports.

Yes, esports are considered to be sports with scheduled games/matches, spectators from around the world, and sponsors, with the primary difference being that the sports are played in a video game format.

Tencent Holdings Ltd, Activision Publishing, Inc, Electronic Arts Inc., Gameloft SE, Skillz Inc., Motorsport Games Inc., Gfinity PLC, HTC Corporation, FACE IT LIMITED, Riot Games, Inc., and CAPCOM Co., Ltd., among others, are the key players covered in the global esports market report.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Revenue Streaming |

|

| Breakup by Streaming Type |

|

| Breakup by Gaming Genre |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.