Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

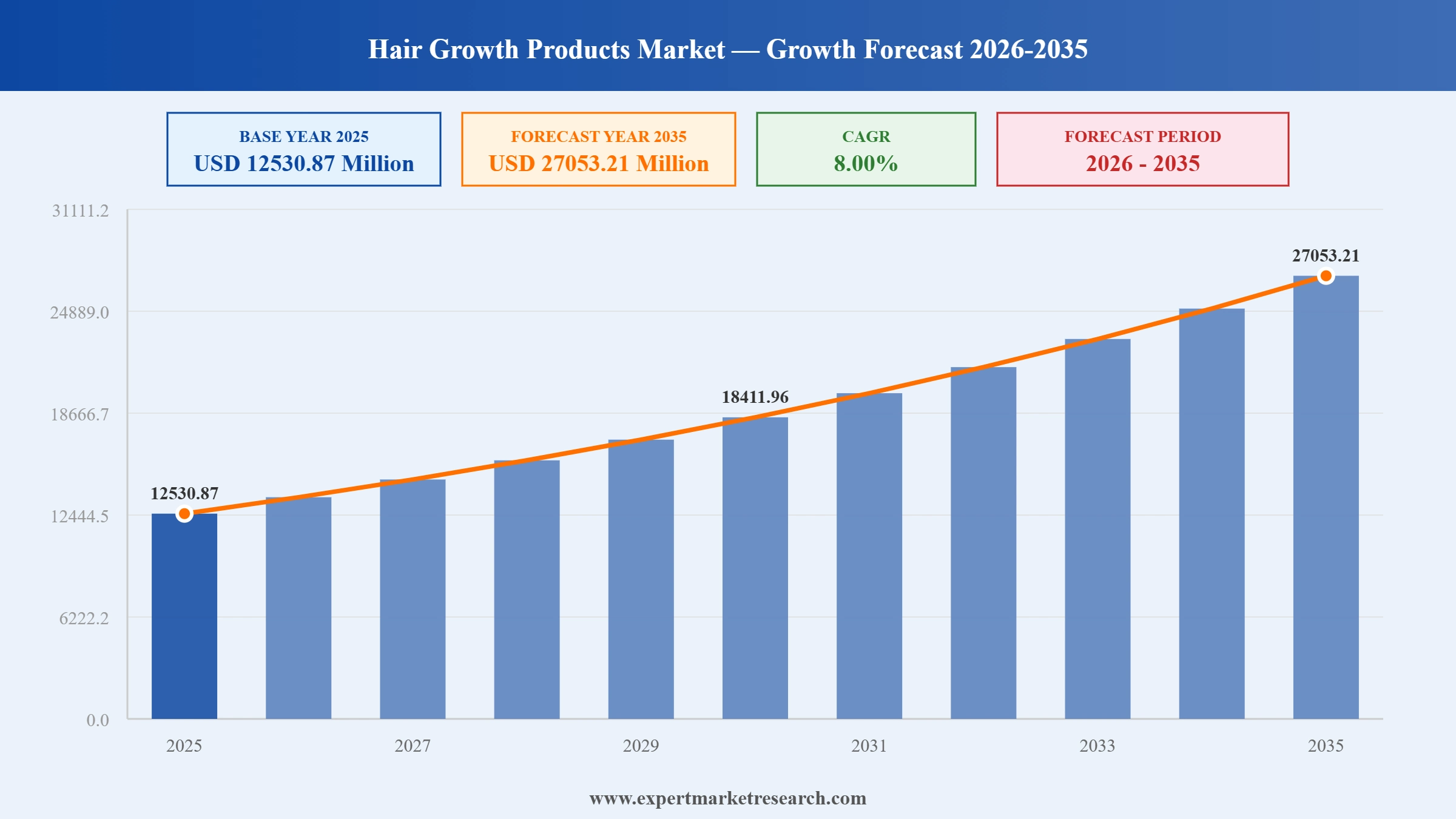

The global hair growth products market reached a value of USD 12530.87 Million at 2025 and is projected to expand at a CAGR of around 8.00% during the forecast period of 2026-2035. With rising global prevalence of androgenetic alopecia and stress-induced hair loss, growing consumer adoption of biotech-powered hair wellness formulations, expanding e-commerce and direct-to-consumer distribution of hair growth treatments, and increasing demand for clinical and device-based hair restoration solutions, the market is expected to reach USD 27053.21 Million by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global hair growth products market is transitioning from a predominantly pharmaceutical category toward a broader hair wellness ecosystem that blends biotech formulations, device-based treatments, and ingestible supplements. Brands are competing on clinical evidence, ingredient transparency, and digital-first community engagement, while the mainstreaming of male grooming and the aging population's demand for regenerative solutions are expanding the addressable consumer base. Platform-based discovery through social media continues to accelerate adoption of premium and science-led brands.

In July 2025, Vegamour launched its GRO+ Advanced Hair Growth and Density Supplements, a dual-pill system formulated by medical doctors and backed by clinical trials. The system targets hair thinning through botanical DHT blockers and a nutrient-rich vitamin soft gel, with full results by day 120. The launch marked Vegamour's entry into ingestible hair wellness, expanding beyond topical products in the global hair growth products market.

In 2025, the rising clinical documentation of telogen effluvium triggered by GLP-1 receptor agonist drugs including semaglutide prompted hair growth brands including Vegamour and Philip Kingsley to develop product ranges specifically addressing drug-induced hair shedding. The trend opened a new product development frontier within the global hair growth products market as prescriptions for GLP-1 drugs accelerated across North America and Europe.

In early 2025, Kenvue, the consumer health company that holds Regaine and Neutrogena, expanded the retail and pharmacy distribution of its minoxidil-based hair growth range across North America and Europe. The expansion reinforced Regaine's position as the leading OTC topical treatment brand in the global hair growth products market.

In November 2024, Philip Kingsley Products Ltd. extended its clinically-backed hair care range with a new Density Stimulating product line targeting thinning-prone hair across the adult and ageing demographics. The launch reinforced the brand's heritage in trichology-led hair wellness and expanded its competitive presence in the global hair growth products segment.

Approximately 40% of global hair loss cases are attributed to androgenetic alopecia, creating a persistent, biology-driven demand base for the global hair growth products market. This clinical foundation differentiates hair growth from discretionary beauty categories and sustains demand through economic cycles, giving pharmaceutical and biotech-backed brands a durable growth runway.

Plant-derived exosome technology, peptide delivery systems, and botanical DHT inhibitors are replacing traditional sulfate-based formulations across premium hair growth products. Vegamour's exosome serum and GRO+ supplement system exemplify how biotech-forward brands are commanding premium pricing and building clinical credibility within the hair growth products market.

Low-level laser therapy devices and AI-guided robotic hair transplant systems from companies such as Venus Concept (ARTAS iX) and REVIAN (REVIAN RED System) are normalising clinical-grade hair restoration outside hospital settings. Accessibility improvements through leasing models and non-surgical alternatives are expanding the hair growth products market addressable base into tier-2 cities.

Approximately 35% of consumers in the hair care and wellness category discover new products through influencers and digital campaigns. In the hair growth products market, TikTok and Instagram have accelerated trial of biotech serums and supplements by enabling brand storytelling around clinical evidence, before-and-after documentation, and community-driven engagement.

Oral supplements and vitamin formulations are growing into a material revenue segment within the global hair growth products market. Consumer interest in addressing hair thinning from the inside out, combined with clean-label and vegan positioning, is driving adoption of biotin, collagen, and adaptogen-based supplements. Vegamour's July 2025 GRO+ supplement launch confirmed ingestibles as the next growth frontier.

The report by Expert Market Research's titled "Global Hair Growth Products Market Report and Forecast 2026-2035", offers a detailed analysis of the market based on the following segments:

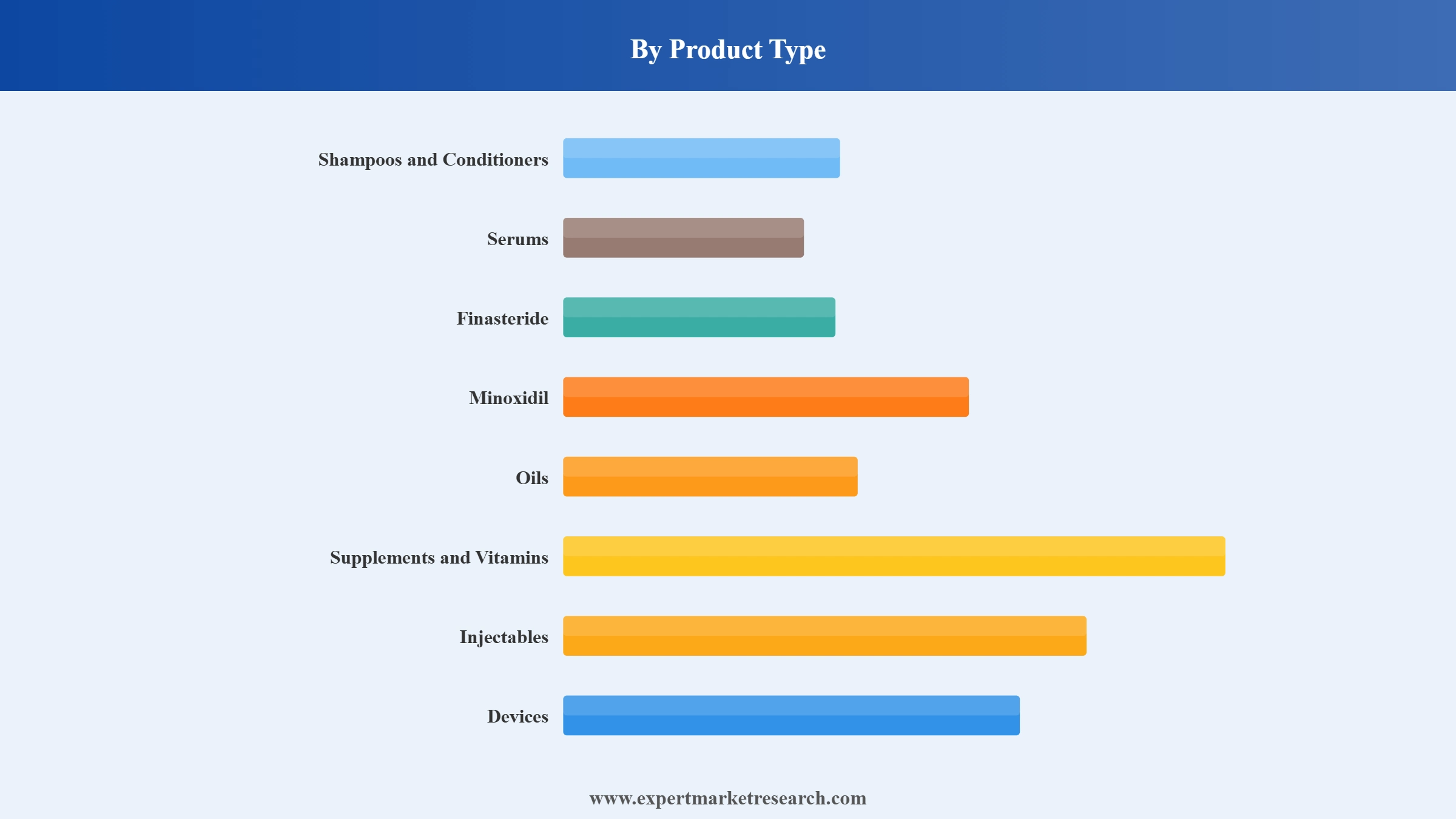

Market Breakup by Product Type

Key Insight: Shampoos and conditioners hold the largest product type share in the global hair growth products market due to daily usage habits, high repurchase frequency, and the broadest consumer familiarity. Minoxidil is the dominant clinically validated topical treatment, while serums and devices are the fastest-growing categories as biotech innovation and device accessibility improve. Injectables and supplements are emerging segments gaining share with premium, clinical-outcome-focused consumers.

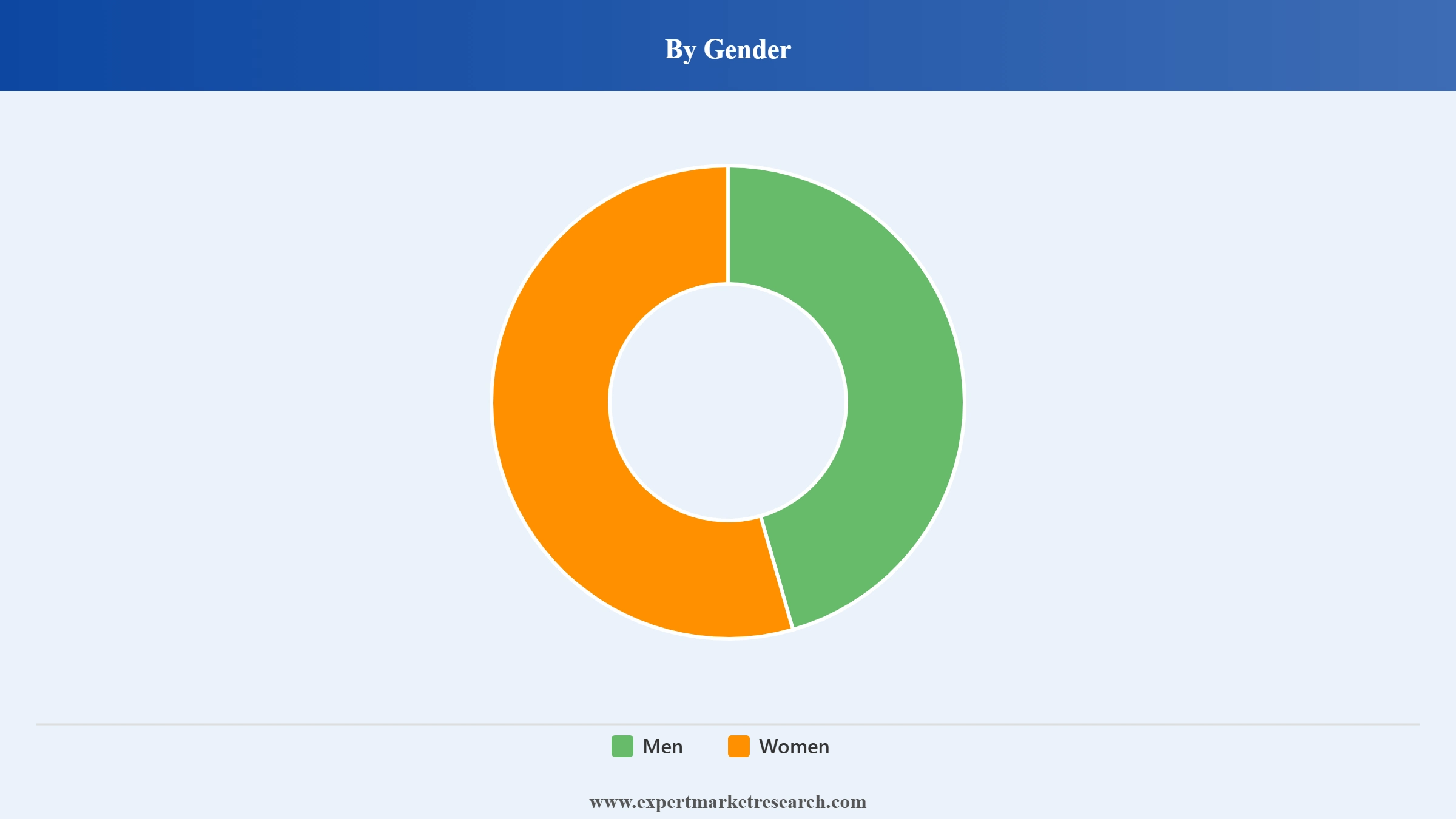

Market Breakup by Gender

Key Insight: Men account for the larger share of the global hair growth products market, driven by the significantly higher clinical incidence of androgenetic alopecia among males. Minoxidil, finasteride, and device-based restoration systems are primarily consumed by the male demographic. However, women represent the faster-growing segment as awareness of female pattern hair loss increases and brands develop dedicated formulations addressing female hormonal and stress-induced hair thinning.

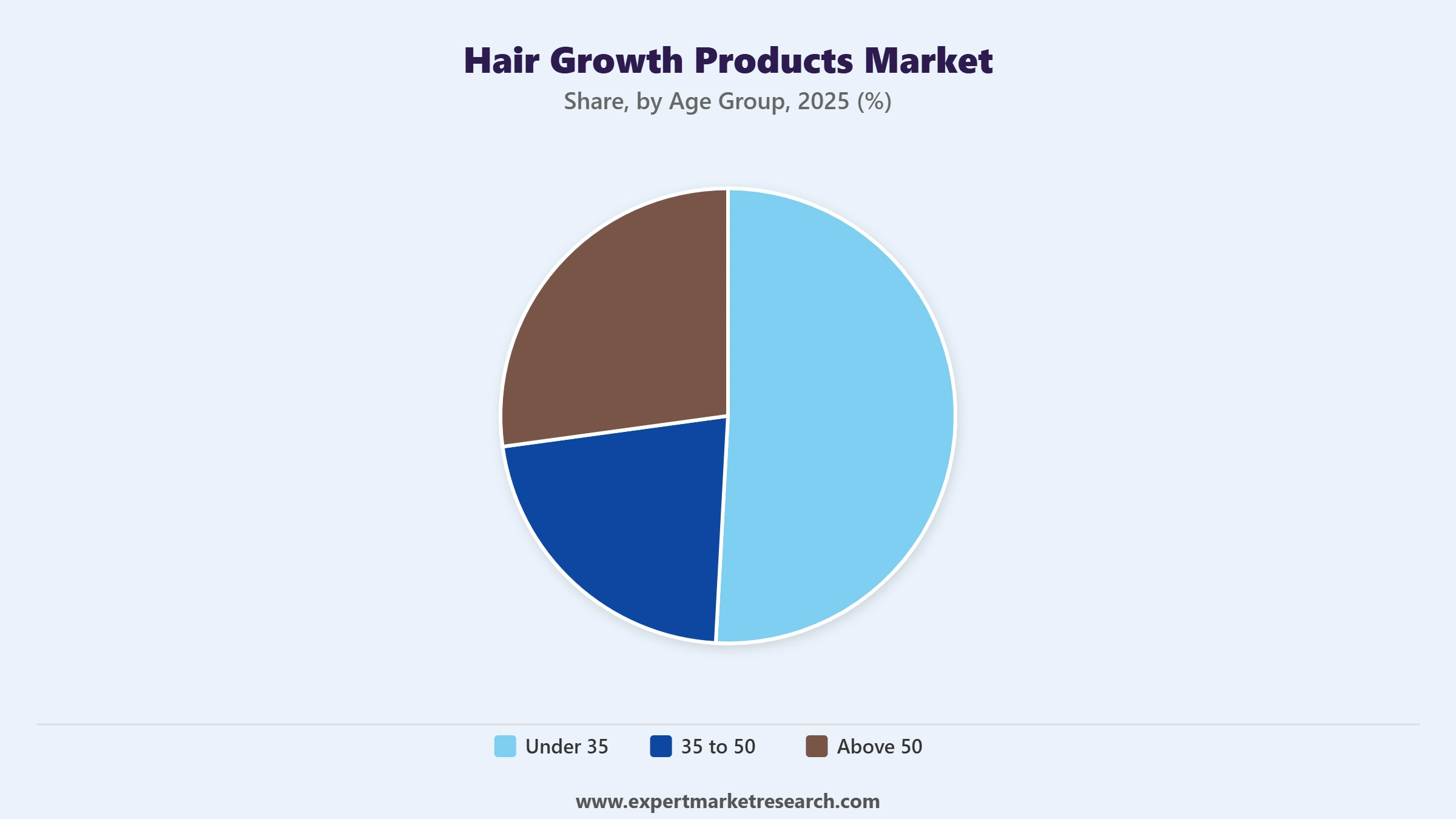

Market Breakup by Age Group

Key Insight: The 35 to 50 age cohort represents the dominant demand group, as this segment experiences peak onset of androgenetic alopecia and has both the income and motivation to invest in effective treatments. The above 50 segment is the fastest-growing age group, driven by ageing population demographics and growing interest in regenerative and restorative hair solutions. The under-35 segment is expanding through preventive wellness adoption, fuelled by social media awareness of scalp health.

Market Breakup by Region

Key Insight: North America holds approximately 30% of the global hair growth products market, anchored by high consumer spending on premium personal care, a mature clinical ecosystem, and strong DTC brand penetration. Asia Pacific dominates by volume with over 46% share in 2025, led by China and India's large populations and rising awareness of hair health solutions. Latin America and the Middle East and Africa are growing markets as e-commerce access improves and international brands enter through distribution partnerships.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By product type, shampoos and conditioners dominate the market due to daily usage frequency and universal consumer familiarity

Shampoos and conditioners lead the global hair growth products market by volume and revenue, serving as the entry point for most consumers beginning a hair growth regimen. Their daily use creates high repurchase cycles, and the integration of growth-promoting actives such as biotin, caffeine, and niacinamide into mainstream shampoo formulations has expanded the category beyond specialist treatments into everyday personal care. Major brands including Kenvue's Neutrogena and Philip Kingsley have developed clinically positioned shampoo and conditioner lines.

Minoxidil holds the dominant position among clinically active topical treatments and is the best-recognised ingredient in hair growth medicine, approved by the FDA for both men and women. The OTC availability of minoxidil under brands such as Regaine and Rogaine ensures wide accessibility. In early 2025, Kenvue expanded Regaine's distribution across North America and Europe, reinforcing the category's reach. Devices are the fastest-growing product type as REVIAN's red-light and Venus Concept's ARTAS iX robotic restoration systems gain commercial traction.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By gender, men account for the dominant share of the market due to higher clinical prevalence of androgenetic alopecia

Men generate the larger share of revenue in the global hair growth products market, as androgenetic alopecia affects up to 50% of men by age 50. Pharmaceutical treatments such as finasteride and minoxidil were originally developed and marketed predominantly to males, and the male segment continues to drive the highest spending on clinical treatments and device-based restoration. Cultural normalisation of men investing in appearance and hair health is sustaining demand growth beyond those already experiencing significant hair loss.

Women represent a structurally underpenetrated and fast-growing segment as awareness of female pattern hair loss and postpartum hair thinning increases. Brands are developing dedicated female formulations that avoid hormonal actives and leverage botanical DHT inhibitors and exosome technology. In July 2025, Vegamour's GRO+ Advanced Supplement system was explicitly positioned for female consumers experiencing hormonal and stress-related hair thinning, demonstrating the commercial priority brands are placing on the female segment within the hair growth products market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By age group, the 35 to 50 cohort accounts for the dominant share of the market due to peak androgenetic alopecia onset and high disposable income

The 35 to 50 age group commands the largest share of the global hair growth products market, as this demographic is both most affected by clinically significant hair thinning and best positioned financially to invest in effective treatments. Prescription treatments, premium serums, and device-based restoration systems see their highest adoption rates in this cohort, and the group's digital savviness makes them accessible through direct-to-consumer brand channels and dermatologist-recommended products.

The above-50 segment is growing fastest, supported by ageing population demographics across North America, Europe, and East Asia. This group is increasingly seeking regenerative hair solutions rather than just preventive products, driving demand for injectables, growth factor serums, and robotic transplant systems. The under-35 cohort is entering the market earlier through preventive scalp care and supplement adoption, with social media content around hair wellness establishing hair growth products as a mainstream wellness category.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America dominates the market due to high clinical awareness, strong DTC brand presence, and premium consumer spending on hair wellness

North America leads the global hair growth products market by revenue, accounting for approximately 30% of global sales, driven by the highest per-capita spending on personal care, a mature dermatology and trichology infrastructure, and a well-developed direct-to-consumer digital commerce ecosystem. The United States is the primary market, where brands like Vegamour, Kenvue's Regaine, and Venus Concept operate established clinical and retail channels. The region's regulatory clarity around OTC minoxidil and device clearances further facilitates commercialisation.

Asia Pacific is the fastest-growing region, holding over 46% of global share in 2025 and projected to expand at the highest CAGR through the forecast period. China and India are the dominant volume markets, driven by large populations, rising awareness of hair health through social media, and increasing disposable incomes enabling trade-up from home remedies to clinically validated products. India and China are both seeing rapid entry of international hair growth brands and domestic innovation in ayurvedic and herbal-based hair growth formulations.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global hair growth products market is fragmented across pharmaceutical companies, medical device manufacturers, and direct-to-consumer hair wellness brands. Clinical credibility, ingredient innovation, and consumer trust are the primary competitive differentiators. The market is bifurcating between prescription-strength medical treatments and premium consumer wellness brands, with each segment requiring distinct go-to-market capabilities.

Competition intensifies across digital channels where DTC brands leverage social commerce, influencer marketing, and subscription models to build loyal customer bases. Clinical brands compete on FDA approval credentials, dermatologist endorsements, and efficacy data, while wellness brands compete on ingredient transparency, clean labelling, and brand community. Strategic investment and product innovation remain the key growth levers for all market participants.

Founded in 2002 and headquartered in Ontario, Canada, Venus Concept is a global medical aesthetics technology company offering AI-powered hair restoration systems. Its NeoGraft automated follicular unit extraction system and ARTAS iX robotic hair transplant platform serve dermatology clinics, plastic surgery centres, and medical spas across over 60 countries in the hair growth products market.

Founded in 2016 and headquartered in California, United States, REVIAN is a medical technology company specialising in multi-wavelength LED light therapy. Its REVIAN RED System delivers dual-wavelength red and amber light to treat androgenetic alopecia and promote hair growth without pharmacological side effects, offering a differentiated non-drug solution in the hair growth products segment.

Founded in 2016 and headquartered in California, United States, Vegamour is a biotech-powered hair longevity brand offering premium vegan hair wellness products. Its GRO Hair Serum and the expanded GRO+ Advanced system, including topical and ingestible components using plant-derived exosome technology, position it as a leading DTC innovator in the clean and science-backed hair growth products market.

Founded in 1886 and headquartered in New Jersey, United States, Johnson and Johnson's consumer health division, now operated under Kenvue, owns Neutrogena and Regaine, two of the most recognised hair growth brands globally. Regaine's FDA-approved minoxidil formulations anchor the OTC hair loss treatment category, and its expanded 2025 distribution reinforced the brand's commercial leadership in the global hair growth products market.

Other key players in the market are Philip Kingsley Products Ltd., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Stay ahead in the global hair growth products market with our latest comprehensive report. Whether you are a hair wellness brand, pharmaceutical company, clinical device manufacturer, dermatologist network, or investor tracking this fast-growing category, our report delivers the market intelligence and strategic clarity to support your decisions. Download your free sample today and explore the key opportunities across hair growth products.

Latin America Hair Care Market

South Korea Hair Care Market

Indonesia Hair Care Market

Australia Hair Care Market

Mexico Hair Care Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 12530.87 Million.

The market is assessed to grow at a CAGR of 8.00% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 27053.21 Million by 2035.

The market is categorised according to the product type, which includes shampoos and conditioners, serums, finasteride, minoxidil, oils, supplements and vitamins, injectables, and devices.

The market key players are Venus Concept, REVIAN, Inc., Vegamour Inc., Johnson & Johnson Consumer Inc., and Philip Kingsley Products Ltd., among others.

Based on the gender, the market is divided into men and women.

Based on the age group, the market is divided into under 35, 35 to 50, and above 50.

The market is broken down into North America, Europe, Asia Pacific, Latin America, and Middle East and Africa.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Gender |

|

| Breakup by Age Group |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.