Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

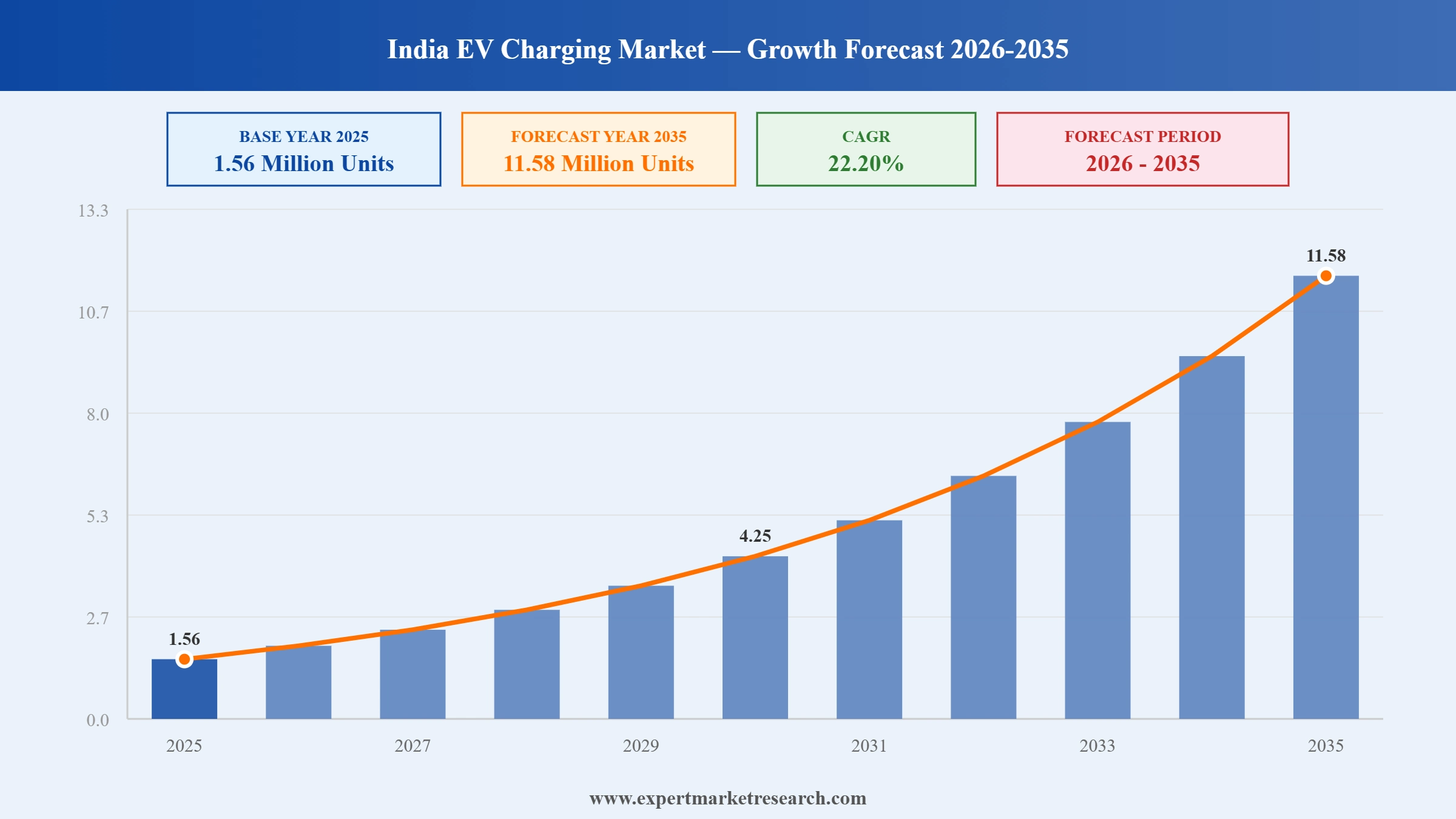

The India EV charging market reached a volume of 1.56 Million Units at 2025 and is projected to expand at a CAGR of around 22.20% during the forecast period of 2026-2035. With the rising popularity of electric vehicles, strong government policy support, rapid expansion of public charging infrastructure, and growing demand for fast and accessible charging solutions, the market is expected to reach 11.58 Million Units by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| India EV Charging Market Report Summary | Description | Value |

| Base Year | Million Units | 2025 |

| Historical Period | Million Units | 2019-2025 |

| Forecast Period | Million Units | 2026-2035 |

| Market Size 2025 | Million Units | 1.56 |

| Market Size 2035 | Million Units | 11.58 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 22.20% |

| CAGR 2026-2035 - Market by Region | North India | 23.9% |

| CAGR 2026-2035 - Market by Charging Type | AC | 23.2% |

| CAGR 2026-2035 - Market by Power Output | Rapid Chargers | 25.1% |

| Market Share by Region | South India | 31.1% |

The India EV charging market is entering a phase of rapid and transformative expansion, marked by large-scale infrastructure rollouts, policy-backed capital deployment, and growing collaboration between EV manufacturers, charge point operators, and energy companies. Operators are shifting focus from simply adding charger counts toward improving uptime, interoperability, and smart charging capabilities, as reliability becomes the key differentiator for user adoption.

V-GREEN, the global EV charging infrastructure company founded by VinFast's backer Pham Nhat Vuong, signed a strategic partnership with Hindustan Petroleum Corporation Limited in December 2025 to deploy EV charging stations across HPCL's network of over 24,400 retail outlets nationwide. The collaboration significantly accelerates India's public EV charging rollout by leveraging HPCL's existing footprint across urban and highway corridors.

ChargeZone, which operates over 13,500 charging points across India and the UAE, launched Project E-DHARA in November 2025 to transition its entire charging network to 100% renewable energy. The initiative integrates solar power generation, battery energy storage systems, and high-speed charging infrastructure, beginning with a renewable-powered hub at Dahej, Gujarat, representing a major step toward true green mobility in the India EV charging market.

Key Trends Description 3: Tata Power, in collaboration with Tata Passenger Electric Mobility, introduced the TATA.ev MegaCharger concept and inaugurated a large charging hub in Mumbai in September 2025. The company outlined major expansion plans including 30,000 new public chargers and 500 dedicated mega stations, supported by infrastructure investments and state-level projects aimed at scaling EV charging access across India's cities and highways.

The Department for Promotion of Industry and Internal Trade signed a memorandum of understanding with Ather Energy in July 2025 to bolster India's EV and manufacturing startup ecosystem. The partnership provides deep-tech startups with mentorship and infrastructure support across battery technology, vehicle manufacturing, and clean energy, reinforcing Ather's dual role as both an EV maker and a major charge point operator.

India's PM E-DRIVE scheme earmarked Rs. 2,000 crore specifically for deploying public charging infrastructure nationwide, replacing the FAME II programme with stronger funding. Karnataka disbursed Rs. 503 crore to deploy 1,243 new EV chargers, demonstrating the India EV charging market's transition from planning to large-scale execution.

ChargeZone expanded to over 13,500 charging stations through OCPI-based roaming partnerships with Statiq, Bolt, Kazam, Pulse Energy, and others, creating one of India's first large-scale interoperable charging networks. This development directly addresses accessibility fragmentation in the India EV charging market and allows users to access multiple networks through a single application.

India's public EV charging network expanded nearly sixfold between December 2022 and April 2025, reaching 29,277 operational stations. Maharashtra, Karnataka, Uttar Pradesh, and Delhi lead this expansion, with the India EV charging market growth reflecting both government-backed infrastructure programs and private sector investment in urban and highway charging corridors.

EVERTA launched high-performance Made-in-India DC fast chargers in 2025 and commissioned a manufacturing facility in Bengaluru targeting 3,000 chargers annually by 2027. The company aims to capture 15% of India's DC charger market by 2030, reflecting growing localisation momentum within the India EV charging market and government push for indigenous manufacturing.

The Ministry of Heavy Industries is developing the Unified Bharat e-Charge platform to allow EV users to discover, access, and pay across all charging networks through a single interface. Modelled on UPI's impact on digital payments, UBC addresses the India EV charging market's fragmentation challenge and aims to significantly strengthen network usability and consumer confidence.

The report of Expert Market Research's titled "India EV charging market report and forecast 2026-2035 offers a detailed analysis of the market based on the following segments:

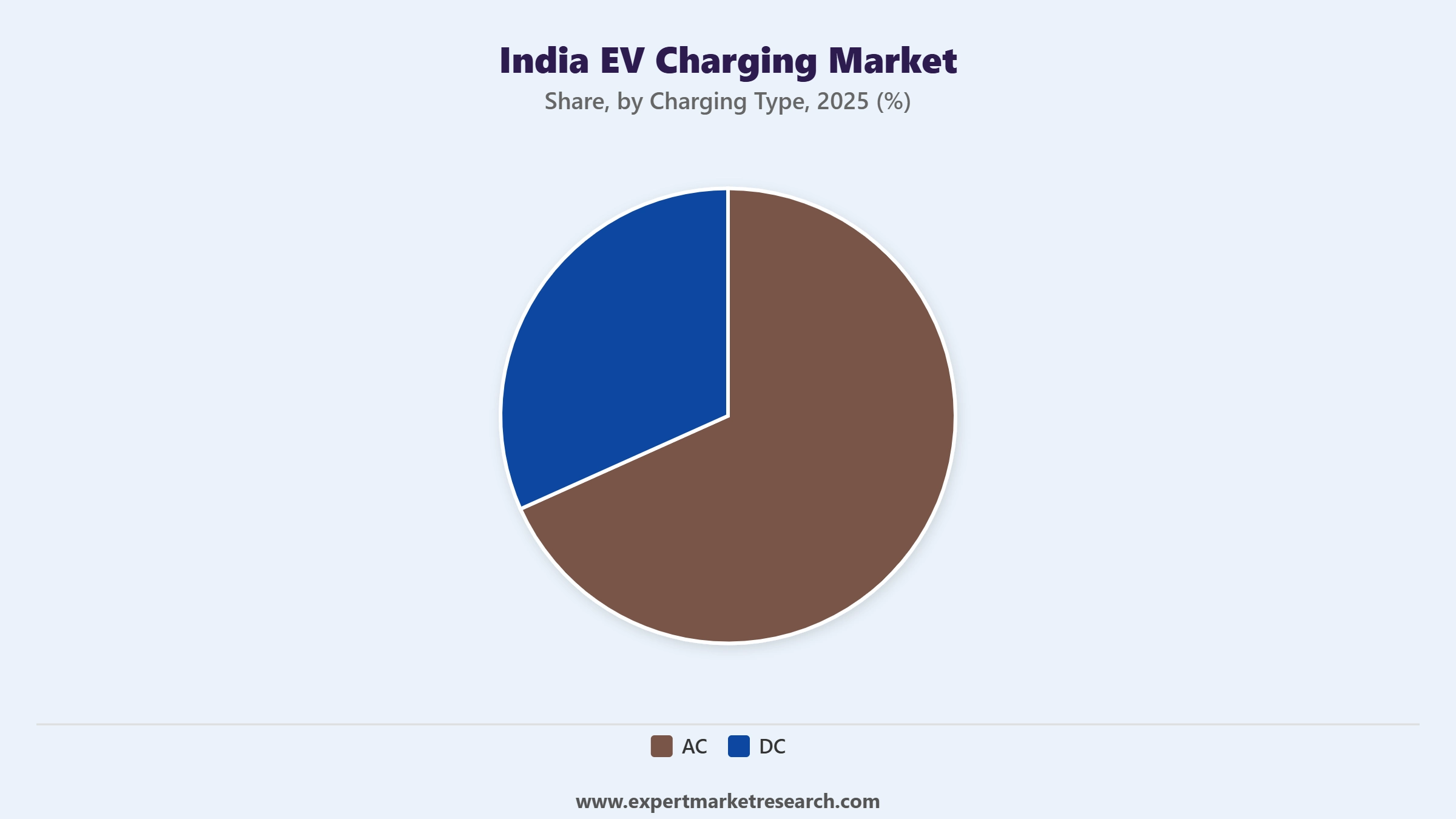

Market Breakup by Charging Type

Key Insight: AC charging holds the dominant share of the India EV charging market by volume, underpinned by its widespread use across India's large base of two-wheeler and three-wheeler electric vehicles, which together account for over 85% of annual EV sales. AC chargers are the primary mode for residential and workplace installations and are deeply embedded in the infrastructure supporting fleet electrification in urban centres. DC fast charging is growing rapidly, driven by public charging network expansion along highways and urban corridors, and is increasingly preferred by passenger car and commercial vehicle operators for its ability to deliver meaningful charge in significantly shorter timeframes.

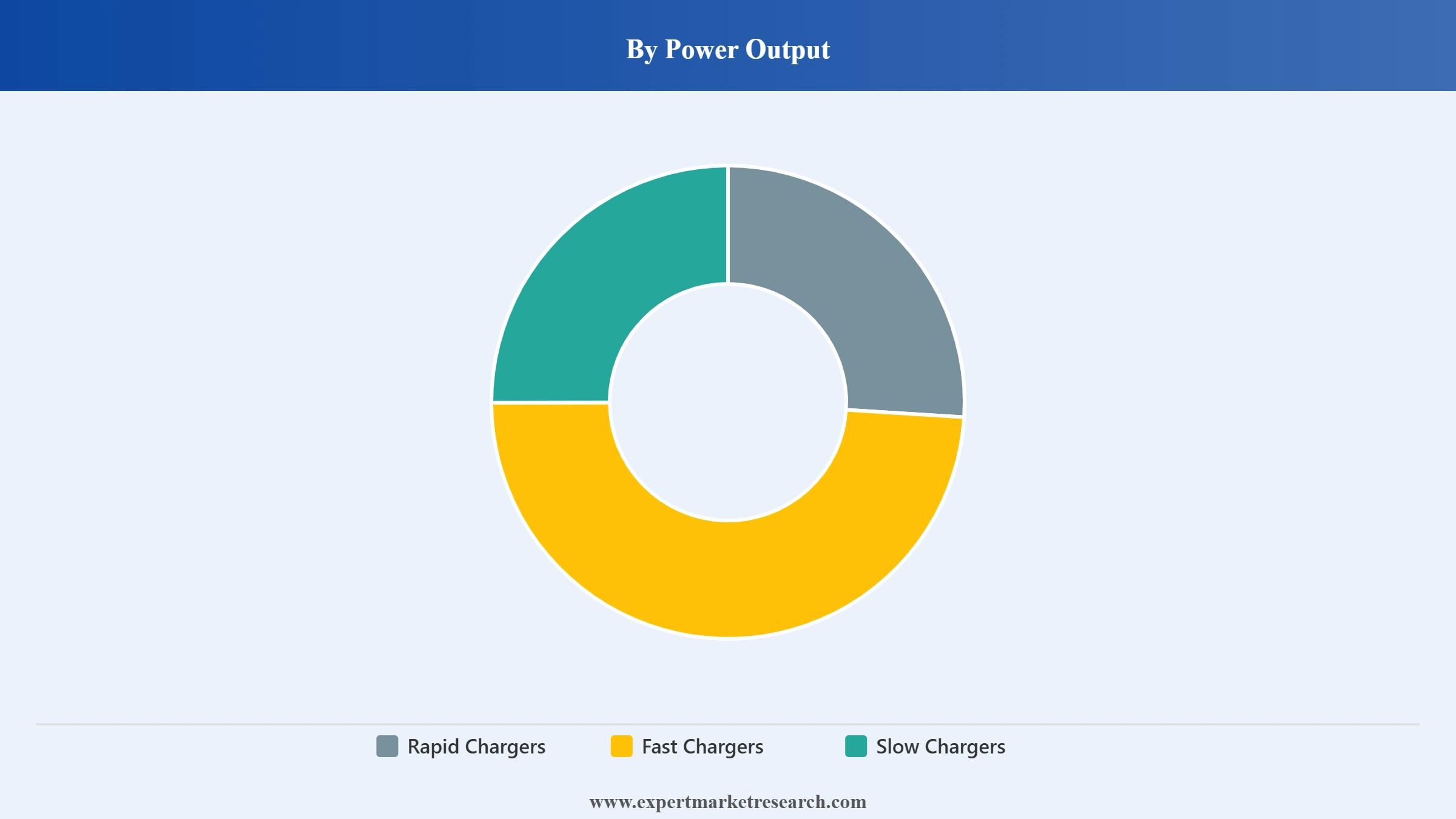

Market Breakup by Power Output

Key Insight: Slow chargers dominate the India EV charging market by volume, primarily due to the enormous scale of India's two-wheeler and three-wheeler EV segment, where overnight or extended-duration charging at 8 to 12 hours is standard practice across private and semi-public settings. Fast chargers represent the largest revenue-generating segment, driven by growing passenger car EV adoption and the expanding public charging network across metropolitan cities and national highways. Rapid chargers are the fastest-growing category, with companies like Tata Power, Statiq, and EVERTA deploying high-power DC units along key corridors to eliminate range anxiety for long-distance EV travel.

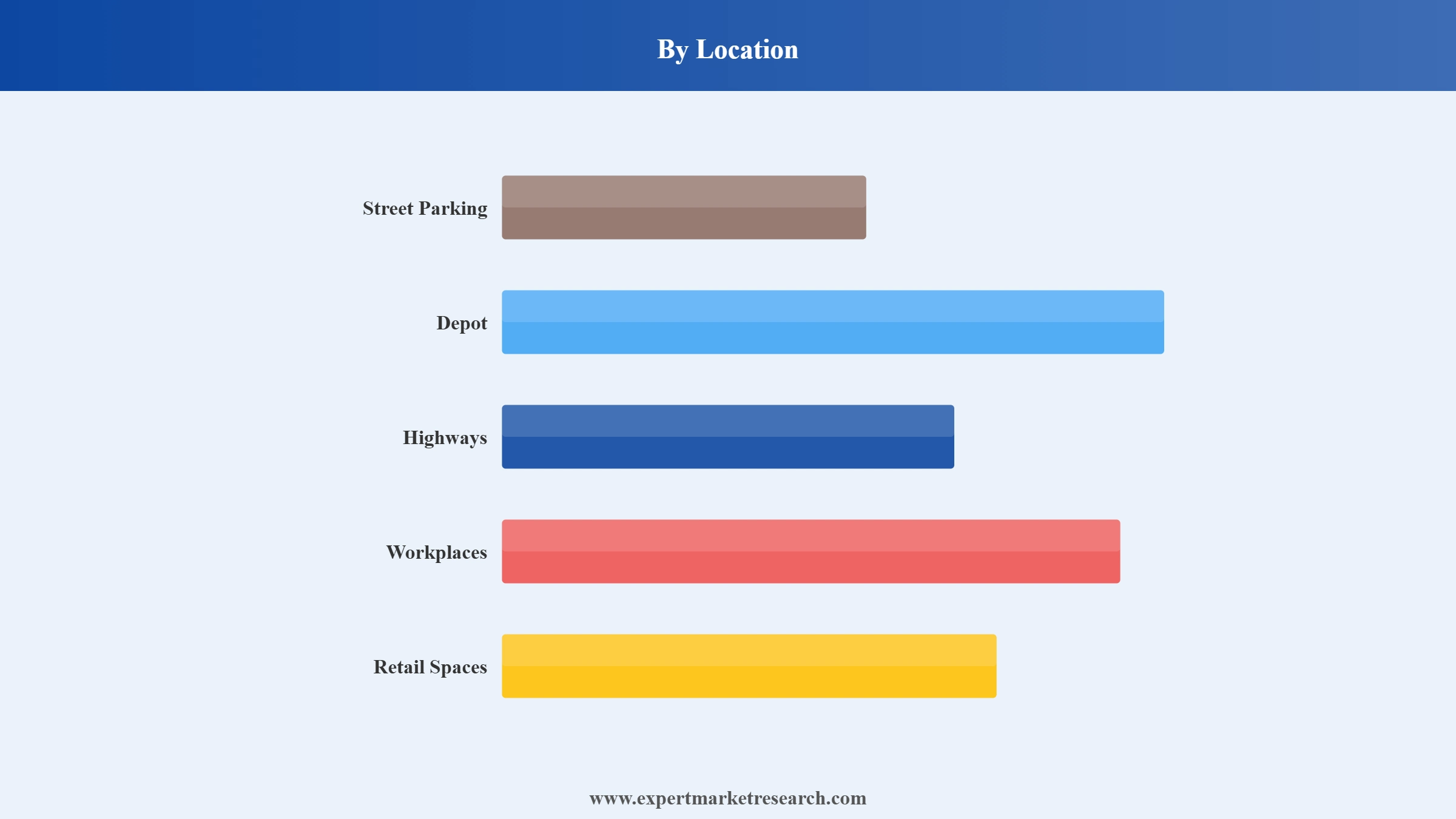

Market Breakup by Location

Key Insight: Street parking locations account for a significant share of public EV charging deployments in India, particularly across metro cities where on-street charger rollouts are driven by municipal authorities and charge point operators. Highway charging is the fastest-growing location segment as automakers and energy companies race to eliminate intercity range anxiety, with India targeting one charging station every 25 kilometres along national highways. Workplace and retail space charging are gaining momentum as corporations embed EV charging into ESG commitments and shopping centres use charging availability as a footfall driver, creating diversified demand across the India EV charging market.

Market Breakup by Phase

Key Insight: Single-phase charging dominates India's residential and small-scale commercial EV charging landscape, meeting the needs of two-wheeler and three-wheeler owners who rely on standard household electricity connections for overnight charging. Three-phase charging is growing strongly across commercial, industrial, and public fast-charging applications, where higher power outputs are required for passenger car and fleet vehicle charging. The shift toward faster on-board charger capacities from 3.3 kW to 7.2 kW and beyond is progressively driving adoption of three-phase infrastructure among passenger vehicle owners seeking shorter charging cycles.

Market Breakup by Region

Key Insight: South India leads the India EV charging market in penetration rate, with Karnataka hosting over 6,097 public charging stations and Kerala recording the highest EV penetration at 7.9%, driven by strong state-level EV policies, progressive consumer adoption, and active charge point operator expansion. West India, led by Maharashtra with 3,746 stations across Mumbai, Pune, and Nagpur, commands significant market share through urban density and strong OEM and CPO investment. North India is anchored by Delhi's aggressive charging expansion plans and Uttar Pradesh's rapidly growing EV market, supported by government incentives and fleet electrification programs.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Charging Type, AC Dominates the Market Due to Widespread Use Across India's Two-Wheeler and Three-Wheeler EV Base

AC charging accounts for the dominant share of the India EV charging market by volume, driven by the massive installed base of two-wheeler and three-wheeler electric vehicles that depend on standard AC chargers for residential and semi-public charging. With two-wheelers making up over 50% of annual EV sales and three-wheelers at 36%, AC infrastructure remains the backbone of India's EV charging ecosystem.

DC fast charging is the faster-growing sub-segment within the India EV charging market, gaining rapid traction along public charging corridors, highways, and fleet depots. Operators including Tata Power, ChargeZone, and Statiq are prioritising DC deployment to address range anxiety for passenger car users. The government's PM E-DRIVE scheme includes dedicated funding to expand public DC infrastructure, with targets to scale from 12,000 public chargers in 2025 to an estimated 80,000 to 120,000 by 2030.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Power Output, Slow Chargers Account for the Dominant Share of the Market Due to India's Large Two-Wheeler and Three-Wheeler EV Fleet

Slow chargers hold the commanding volume share of the India EV charging market, anchored by the country's enormous two-wheeler and three-wheeler EV segment, where extended overnight charging at residential and depot locations is the standard operating model. Their low cost, ease of installation, and compatibility with standard electrical connections make them the practical default for the majority of Indian EV users.

Fast chargers are the highest revenue-generating segment in the India EV charging market, reflecting the premium commanded by faster turnaround times for passenger car users and fleet operators. Rapid chargers are the fastest-growing category, with EVERTA, Tata Power, and ChargeZone deploying high-output DC units along national highway corridors. The government's highway charging target of one station every 25 kilometres is directly stimulating rapid charger deployment at scale.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Location, Street Parking Dominates the Market Due to High Urban EV Density and Government-Led Public Infrastructure Rollouts

Street parking locations account for the largest share of public EV charging deployment in the India EV charging market, driven by municipal government programs in cities like Delhi, Mumbai, and Bengaluru that have prioritised on-street charger installation to serve dense urban EV populations. Delhi alone planned approximately 18,000 public and semi-public charging points, reflecting the scale of urban street-based infrastructure investment.

Highway charging is the fastest-growing location segment within the India EV charging market, supported by the government's target of one charging station every 25 kilometres along national highways and private investments from HPCL, IOCL, and charge point operators including ChargeZone and V-GREEN. Workplace and retail space charging are expanding steadily as corporations embed EV charging into ESG strategies and shopping centres leverage charging amenities to drive footfall.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

South India Dominates the Market Due to Leading EV Penetration, Strong State Policy Support, and Extensive Charging Infrastructure

South India leads the India EV charging market in terms of EV penetration and charging network density, with Karnataka hosting over 6,097 public charging stations as of July 2025 and Kerala recording the highest EV adoption rate of 7.9% among all Indian states. Tamil Nadu, a major electric two-wheeler manufacturing hub, adds further depth to the region's EV ecosystem, with 1,524 charging stations supporting strong retail and fleet adoption. State-level policies across Karnataka, Kerala, and Tamil Nadu have been among India's most proactive, offering purchase subsidies, road tax waivers, and dedicated charging infrastructure development programs that have created a self-reinforcing cycle of EV adoption and charging network expansion.

West India is the second-largest region in the India EV charging market, anchored by Maharashtra, which hosts 3,746 public charging stations across Mumbai, Pune, and Nagpur and has attracted significant investments from both domestic charge point operators and oil marketing companies. Maharashtra's urban density, strong OEM presence, and municipal government support for EV charging have positioned it as a key market for fast charger deployment along urban corridors and residential complexes. North India, led by Delhi and Uttar Pradesh, is growing rapidly with Delhi's expansive public charging plans and UP's fast-emerging EV market supported by state incentives, while East and Central India represents the highest growth potential as infrastructure investment begins penetrating smaller cities and highway corridors in these underpenetrated regions.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The India EV charging market features a dynamic mix of established power utilities, EV manufacturers with proprietary charging networks, global technology companies, and technology-driven domestic startups competing across hardware, software, and network operation. Leading players such as Tata Power, Ather Energy, ChargeZone, and Reliance BP Mobility are expanding fast-charging corridors, forging strategic partnerships with automakers and fuel retailers, and deploying smart digital platforms to differentiate their offerings and capture growing market share.

Multinational players including ABB and Delta Electronics are leveraging global hardware expertise and compliance capabilities to serve the premium public and commercial charging segments, while domestic innovators like Charzera Tech and BPM Power are competing on product agility, localisation, and cost competitiveness. The market is witnessing a clear trend toward interoperability, with the ChargeZone-led coalition working toward unified payment and access systems, and the government's Unified Bharat e-Charge platform aiming to consolidate the fragmented network landscape into a single accessible interface.

Founded in 1919 and headquartered in Mumbai, Tata Power is one of India's largest integrated power companies and a leading player in the EV charging market through its EZ Charge network. The company operates over 86,000 home chargers and 5,300 public charging points, and in September 2025 launched the TATA.ev MegaCharger concept alongside a large charging hub in Mumbai. Tata Power has outlined plans to deploy 30,000 new public chargers and 500 dedicated mega stations, positioning itself as the dominant infrastructure provider in India's EV charging ecosystem.

Founded in 2013 and headquartered in Bengaluru, Ather Energy is a leading electric scooter manufacturer and one of India's largest charge point operators, with over 1,000 public Ather Grid charging stations deployed nationwide. The company generated USD 16.1 million in revenue from its charging operations in 2024. In July 2025, Ather signed an MoU with DPIIT to support India's EV and manufacturing startup ecosystem, reinforcing its dual role as an EV product innovator and a charging infrastructure enabler.

Headquartered in India, Charzera Tech Private Limited is a domestic EV charging solution provider focused on delivering affordable and scalable charging hardware for public, commercial, and residential applications. The company competes on product agility and cost competitiveness, targeting the growing mid-market segment of charge point operators and fleet managers deploying EV charging infrastructure across Tier-1 and Tier-2 cities. Its localisation capabilities and compliance with Bharat AC-001 and DC-001 standards position it as a relevant partner for government-backed infrastructure programs.

Founded in 1971 and headquartered in Taiwan, Delta Electronics operates through Delta Electronics India Private Limited and is a prominent player in power electronics, automation, and EV charging infrastructure. The company offers a broad range of AC and DC charging solutions from 7 kW to 360 kW, serving residential, commercial, and public charging segments across India. Delta's global manufacturing scale, certification expertise, and integration of energy management software make it a preferred technology supplier for large-scale public charging deployments and OEM charging partnerships.

Other key players in the India EV charging market are ABB Ltd., Sharify Services Pvt. Ltd., TecSo ChargeZone Ltd., Reliance BP Mobility Limited, Brightblu Holding B.V, BPM Power Private Limited (chargeMOD), and others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Gain a decisive edge with the most comprehensive analysis of the India EV charging market 2026. Access data-driven insights on infrastructure expansion trends, fast-charger deployment, policy developments, and regional growth opportunities across India's rapidly evolving EV charging landscape. Whether you are entering the market, scaling operations, or making strategic investment decisions, this report gives you the clarity and evidence you need. Download your free sample today and explore the high-growth opportunities driving India's clean mobility future.

United States Electric Vehicle Charging Systems and Equipment Market

United States Electric Vehicle Charging Infrastructure (EVCI) Market

Japan Electric Vehicle Charging Equipment Market

Electric Vehicle Charging Infrastructure Market

Electric Bus Charging Infrastructure Market

Smart EV Charging Market in India

EV Battery Recycling Market in India

India Solar-Powered EV Charging Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

At 2025, the market reached an approximate volume of 1.56 Million Units.

The market is projected to grow at a CAGR of 22.20% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach 11.58 Million Units by 2035.

The major market drivers include the increasing sales of electric vehicles, introduction of favourable government policies, and improvement of charging infrastructure in commercial spaces.

The key trends fuelling the growth of the market include technological advancements in EV charging, popularity of portable EV charging, and reducing costs of electric vehicles.

EV cars or electric cars refer to cars that operate on electricity rather than traditional fuels.

Regions considered in the market are North India, East and Central India, West India, and South India.

The various locations of EV charging in the market include retail spaces, workplaces, street parking, highways, and depot, among others.

The key players in the market include Tata Power Company Ltd., Ather Energy Private Limited, Charzera Tech Private Limited, Delta Electronics, Inc., ABB Ltd., Sharify Services Pvt. Ltd., TecSo ChargeZone Ltd., Reliance BP Mobility Limited, Brightblu Holding B.V, BPM Power Private Limited (chargeMOD), and Others.

High initial investment, technological challenges, and supply chain disruptions are hampering the market growth.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Charging Type |

|

| Breakup by Power Output |

|

| Breakup by Location |

|

| Breakup by Phase |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.