Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

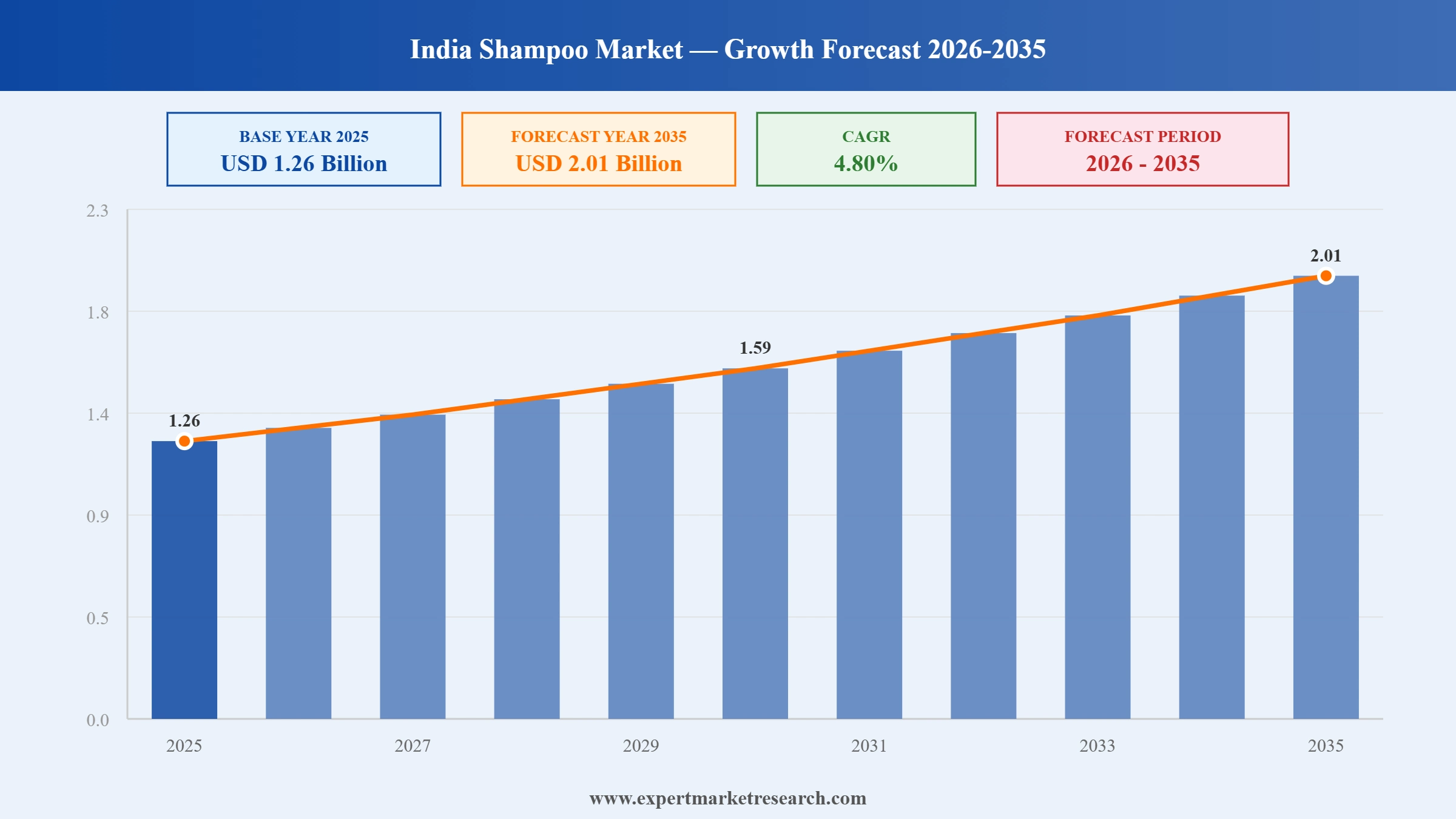

The India shampoo market attained a value of USD 1.26 Billion in 2025 and is projected to expand at a CAGR of 4.80% through 2035. The market is further expected to achieve USD 2.01 Billion by 2035. Two major factors that are changing the India shampoo market are the rapid increase in demand for clean label, sulfate-free, and natural formulations, which is a result of the growing awareness of scalp health and ingredient safety. The second reason is the premiumisation trend which is bolstered as consumers are increasingly looking for specialised products such as anti-hair fall, anti-dandruff, strengthening, or scalp care. This trend is further supported by higher disposable incomes and the strong digital influence of beauty creators and dermatology-led brands.

A major trend that has been gaining a lot of attention in the India shampoo market is the move toward sulfate-free, natural, and "clean-beauty" shampoos, which do not contain harsh synthetic detergents, and this trend is no longer limited to small elite urban pockets but is spreading to more mainstream consumer segments. To support this, in February 2024, Herbal Essences launched its "Pure Plants of Aloe and Camellia Oil" shampoo-and-conditioner line having products with ~ 96% natural-origin ingredients, free from sulfates and parabens, and designed to reduce plastic waste. Another launch that became popular among Indian consumers is TRESemmé Silk Press Sulfate Free Shampoo introduced in 2025, which promotes itself as a mild, amino-peptide source for smooth, frizz-free hair. It is part of a bigger movement toward sulfate-free cleansing in mass-market shampoos. The transition to such products mirrors increased consumer knowledge of scalp/hair-health, product safety, and environmental sustainability, which is quite a different trend from the traditional mass-market shampoos and can be seen very clearly, and therefore boosting the India shampoo market trend.

The India shampoo market is a key segment of the overall hair care and personal hygiene industry, which is a reflection of increased consumer awareness, rising incomes, and changing hair care needs of different demographic groups. The booming demand for herbal shampoos, scalp care, anti-dandruff, and hair-fall management products has been a major driver of the market. In 2025, the market transition to the "skinification" of hair care, i.e., mixing skincare-level nourishment, scalp health, and anti-pollution protection, has, therefore, been a major factor in the continued popularity of the product among Indian consumers who are seeking both effectiveness and styling. The India shampoo market, with its excellent combination of daily necessities and grooming innovations, is thus a vibrant and strategic sector for FMCG and beauty players, thus influencing the shampoo market dynamics in a positive way.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Wella Professionals recently introduced its brand new Ultimate Smooth Range in India. The luxurious line is specifically designed for dry, dull, and frizz-infested hair and it utilizes Squalane and Omega-9 to deeply nourish the hair. Its main attraction, the "Miracle Oil Serum" is the first to show smoothness in 30 seconds and is also the source of the longest frizz control, up to 96 hours. Such a move by Wella can contribute to the India shampoo market expansion as a result of the increased demand for premium anti-frizz and hair care solutions.

Meera by CavinKare introduced Meera Rice Kanji Shampoo that utilizes the traditional rice-kanji (rice congee) and aloe vera to make hair soft, shiny and frizz-free in a natural way. It assures that the first wash will show a result and that smoothness and shine will last for up to three days. This development will accelerate growth in the India shampoo market as it will allow the brand to tap into the increasing consumer demand for natural, heritage-driven haircare solutions that skillfully merge traditional wisdom with the modern formulation, thereby attracting both urban and rural segments.

Himalaya Wellness has launched a new integrated campaign for its anti-hair fall shampoo. The ad campaign focuses on the herb Bhringaraja which is the main cause of hair fall reduction and the slogan “Won’t Let You Fall” is used to depict the fear of hair-fall through a friendship metaphor. Besides the TV spots in southern Indian states, the rollout is also a nationwide digital and influencer push. Such a move will lead to a surge in the India shampoo market as it will create demand for natural hair-care products and also promote the value of herbal, trust-centric shampoos, thus facilitating the India shampoo market development.

Florian Hurel has introduced his first-ever haircare line named fHair in India. The range offers various shampoo and conditioner options including day-to-day care, volume-boosting, colour-protection, and scalp-sensitive formulas, all of which are made using top-notch ingredients like argan oil, macadamia oil, hydrolysed keratin, chamomile, and vitamin E. Such a move might lead to the expansion of the India shampoo market as it will stimulate the demand for salon-quality, premium haircare options that target different hair needs besides cleansing.

Indian consumers are increasingly prioritizing their preference for protein-enriched shampoos that support hair strength, repair, and elasticity. Firms are reacting with the products that utilize protein blends to lessen breakage and enhance hair resilience in general. L'Oreal Paris, for example, just launched its Bond Repair Shampoo in India that employs a technology of citric acid complex to both rebuild weak hair bonds and deliver strengthening benefits from the very first few washes. This phenomenon signifies how strengthening performance-driven shampoos are getting popular over not only premium but also mass categories, thus boosting the India shampoo market opportunities.

Consumers have become very attentive to hair fall, dandruff, scalp stress, and pollution-induced hair issues. This has the effect of creating a market for hair cleansers that concentrate on various scalp needs while still providing essential cleansing. Himalaya Wellness has recently introduced a campaign that is spread all over the country for its Anti Hair Fall Shampoo. The main point of the campaign is the usage of Bhringaraja to lower hair-fall and support the scalp's nourishment. The brand communication, therefore, is at the forefront of preventive care and natural efficacy which is in line with the preference of the majority for specialized therapeutic hair care solutions, and hence bolstering the India shampoo consumption.

At present the shampoo market in India is influenced by growing disposable income and the demand for high-end hair care experiences. Customers are paying for premium shampoos that provide the skin of the hair with nourishment, colour protection, smoothness, or advanced repair. So, Wella Professionals introduce their Ultimate Smooth Range with which they not only offer a serum but also the production of visibly smooth hair within seconds. The debut of the product accentuates the move to luxury performance products that the salon and retail chains endorse. This luxurious position of the product encourages customers to upgrade their purchases and contributes to the manufacturer's value growth.

As per the India shampoo market report, the expansion of organised retail and fast growing ecommerce platforms is making a wider variety of shampoos available to consumers across India. Brand manufacturers can now place organic, premium, and specialized shampoos in both modern trade and online marketplaces, which increases the visibility and accessibility of these products. CavinKare is spreading its new Meera Rice Kanji Shampoo in supermarkets, general trade, and through e-commerce to reach urban as well as rural customers. Such an omnichannel presence not only deepens consumption but also accelerates category growth.

The shampoo market in India is seeing a shift towards demand for shampoos that provide sensorial self care benefits rather than just cleansing, where benefits like deep hydration, soft hair texture and a spa-like experience are emphasised. In fact, L’Oréal Paris introduced its Hyaluron Moisture shampoo range in India in August 2022. The range employs hyaluronic acid to provide 72-hour moisture and, as a result, hair is said to be hydrated and bouncy. This evolution of the trend is indicative of millennial consumers' growing preference for hair care products that are not only luxurious but also wellness-oriented.

The EMR’s report titled “India Shampoo Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

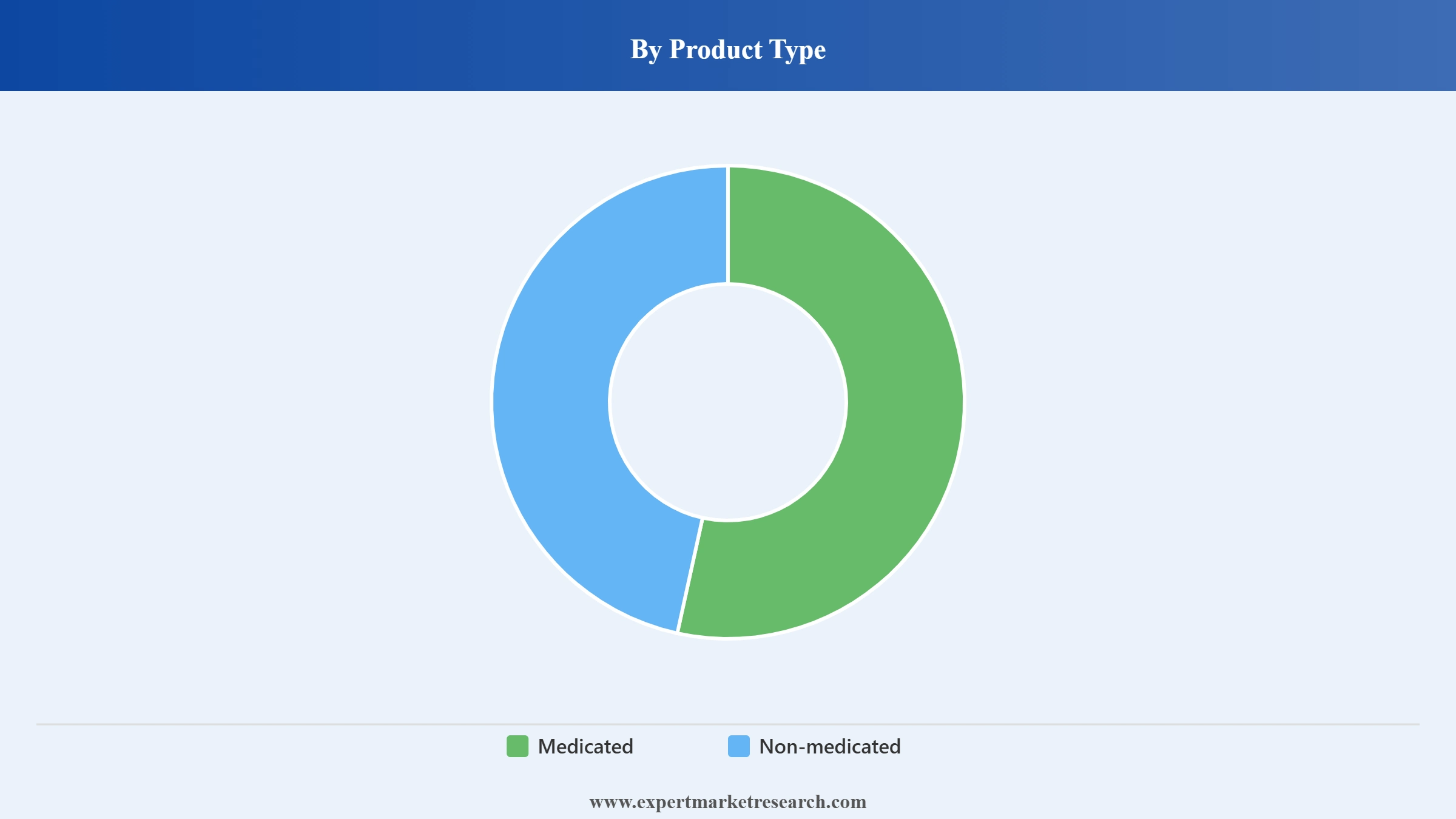

Market Breakup by Product Type

Key Insight: India shampoo industry covers both medicated and non-medicated formats. Non-medicated shampoos continue to lead in the market as they are used for regular cleansing and cosmetic needs in all income groups. Medicated shampoos, however, are rapidly getting more popular as more and more consumers are facing dandruff, hair fall, dryness, and scalp irritation due to changes in weather, pollution, and hard water. Adoption is being facilitated by frequent recommendations from dermatologists on social platforms and by the growing visibility of pharmacies. Consumers do not see medicated offerings as a solution for occasional use but rather as reliable weekly use solutions which lead to repeated purchases and widening category relevance.

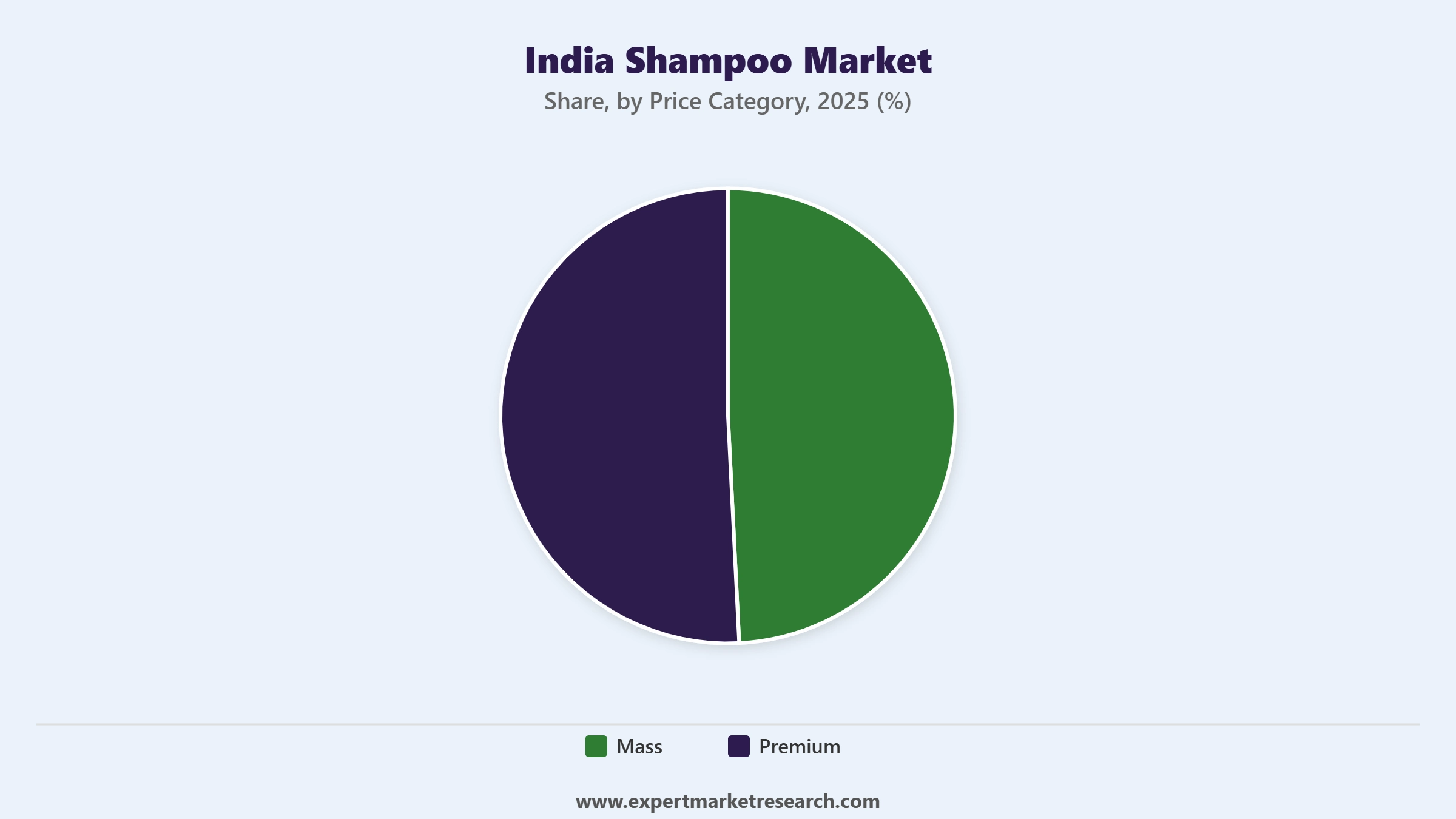

Market Breakup by Price Category

Key Insight: The market is divided into mass and premium shampoos. Mass shampoos still make up the majority base because of their affordability and availability in rural and semi-urban stores. Premium shampoos are becoming popular as the younger and urban consumers are looking for richer textures, high-performance ingredients, and self-care oriented experiences. These consumers do not consider shampoo as a beauty wellness product, but as a basic hygiene item, thus shaping new trends in the India shampoo market. The salon recommendations, video-based product discovery, and rising incomes are helping the premium formats to grow at a faster pace than the overall category and, at the same time, facilitating frequent up-gradings.

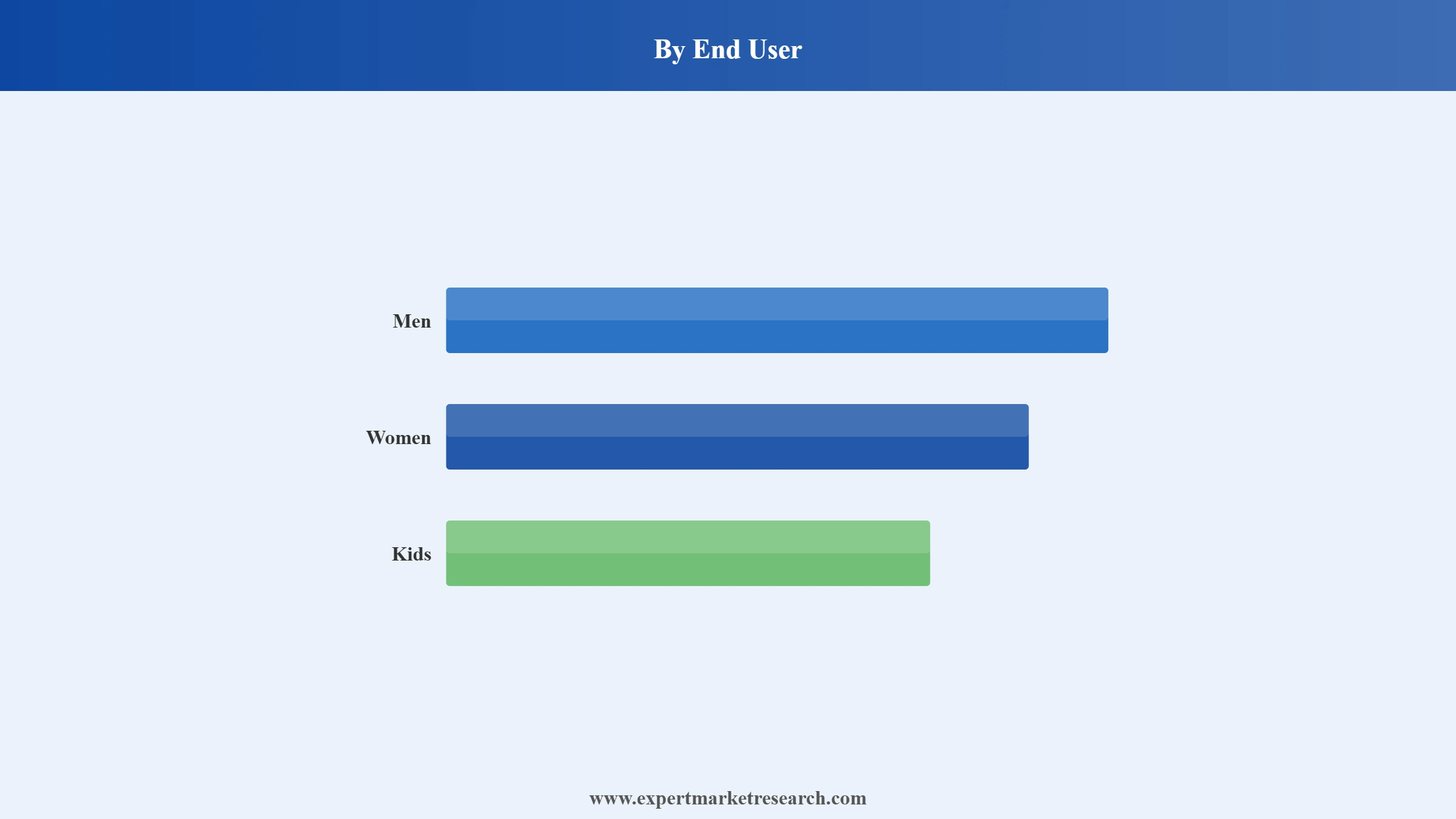

Market Breakup by End User

Key Insight: Shampoo consumption spans men women and kids. Women continue to be the biggest user group as they demonstrate higher involvement in hair fall control, scalp care, shine building, and styling needs. Besides, they also try out several formats and switch more frequently. Men's usage is getting more and more popular due to the increasing interest in grooming, fresh feel, cleansing, and early signs of hair thinning. Purpose-driven male variants are gaining steady growth especially through online shopping. Kids shampoos are a small niche of the market but still, they keep a stable demand for gentle tear-free and mild fragrance solutions from young families.

Market Breakup by Distribution Channel

Key Insight: The majority of India's shampoo sales are handled through supermarkets, hypermarkets, convenience stores, drug stores and pharmacies, online channels, and other formats like beauty stores and salons. Modern retail is still catering to urban consumers who require organised shelves and easy-to-understand comparisons and pushing the growth of the India shampoo market. Convenience stores are still very significant for impulse and refill purchases in local neighbourhoods. Drug stores and pharmacies are the main contributors to the growth of medicated shampoo. Online channels are increasing their customer base at the fastest rate due to a wide assortment, authenticity, and ease of access to smaller towns. Quick commerce and influencer-driven discovery are two of the main reasons why online conversion for premium and specialised shampoos is getting accelerated at a faster rate.

Market Breakup by Region

Key Insight: The market spans North India East and Central India West India and South India. All regions maintain steady demand due to varied climate and cultural routines. While South India and West India are getting considerable momentum as consumers in these regions opt for nourishing herbal and moisturizing shampoos that are suitable for humid coastal weather which mostly results in frizz and scalp buildup. These regions reflect high awareness, strong digital adoption, and greater willingness to buy premium or specialised formats. North India retains strong winter-linked demand while East and Central markets expand through rising distribution access.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Non medicated shampoos lead due to affordability, routine use and strong brand familiarity

The dominant product type in India is non medicated shampoo, which is dominantly propelling the India shampoo market revenue. This category performs well as the majority of households focus on daily cleansing which is supported by nice fragrances, creamy textures and the trust of known brands. Non medicated variants also receive strong support from kirana stores in where families are buying single use sachets most frequently. Consumers are comfortable with the haircare routine without resorting to problem specific products. For example, shampoos from brands like Sunsilk, Dove and Clinic Plus maintain their leadership in the Indian market by offering variants for softness, volume, shine and general nourishment all created for regular use. These shampoos appeal to a wide range of ages and income levels which, in turn, consolidates their scale. The celebrity led campaigns and their strong advertising investment help them to be equally recalled in urban and rural markets.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Mass priced shampoos dominate with sachet driven affordability and widespread rural urban acceptance

The mass price segment is still the major one due to its general affordability which is the key factor in a price sensitive market. Mass shampoos do well as they provide reliable performance at a low price together with small sachets that are suitable for daily or weekly budgets. This category is mostly consumed by the rural population where buyers are choosing brands that they know and that are accessible in the nearby stores rather than pricey ones, further boosting the India shampoo industry revenue. Products like Clinic Plus and Head & Shoulders in small packs are the most common in the households as they are the easiest ways to provide regular cleansing and basic problem relief. Family-sized bottles in the mass tier are also trendy among urban middle-income groups who are looking for the grocery planning that will give them the best value for a month. This demand driven by scale is what keeps mass pricing as the mainstay of the Indian shampoo category.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Women lead usage through frequent routines, strong influence and broader household purchase decisions

Women continue to be the leading end-user segment as they follow a more detailed hair care routine and are faster to adopt products that focus on shine, smoothness, nourishment, and scalp comfort. Moreover, women are the ones who mainly drive the experimentation with formats such as serums, cleansers and weekly treatments which in turn increases the overall usage frequency. Their engagement is largely dependent on beauty content, product reviews, and hair styling that is related to work, outings, and social occasions, thereby propelling the India shampoo market growth. Brands like Dove and L'Oreal Paris are able to retain loyalty particularly among women by providing ranges that are concentrated on softness, hydration, and damage repair. Women in the family, often, are the ones deciding which shampoo to use for all members thus not only making their decision-making role more powerful but also confirming their dominance in the total consumption.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North India leads with a large population, varied climate, strong retail reach, and consistent demand

North India, with its large and varied population, is still the major area that contributes to the volume of the national shampoo market. This is made possible by the region's diverse and well-developed retail networks which extend not only to cities but also to rural areas. The region goes through different weather conditions such as cold and dry winters as well as hot and dusty summers which in turn raise the need for cleansing and moisturizing shampoos that are used more frequently. Moreover, bigger family sizes and the strong preference for value packs are some of the reasons that further drive volume growth of the India shampoo industry.

There are a number of popular brands like Dove Clinic Plus and Pantene that have a strong presence in provinces such as Uttar Pradesh, Punjab, Haryana and Rajasthan. This is achieved through the numerous kirana stores spread across these states and the promotional activities being carried out. On one hand, deeply rooted grooming habits like regular oiling on the other hand, frequent washing have resulted in steady shampoo consumption. All these factors combined have made North India the volume powerhouse of the national shampoo market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Leading India shampoo market players are leaning towards making their products more powerful, more personalized and with a cleaner ingredient list to meet the changing consumer expectations. Their goal is to make products that, besides being effective in solving the mentioned hair care issues, will be safe and use natural ingredients. As a matter of fact, Himalaya Wellness launched an Anti-Hair Fall Shampoo campaign in July 2025, which is basically the herb Bhringaraja. The campaign is designed to provide the consumers with a natural, highly reliable way to solve hair fall and improve scalp health, thus making the customers who want herbal care and efficacy happy.

Several India shampoo companies are placing their money in luxurious product lines that bring salon level results, smooth and shiny hair and long lasting nourishment. Some of them are also fortifying their science based or dermatology inspired brand portfolio to gain the trust of consumers who are looking for visible hair and scalp health improvement. Meanwhile, companies are widening their digital presence, getting ready for the next wave of ecommerce, and crafting the right message through social media to engage and interact with the younger generation who value authenticity, are looking for convenient solutions and want to see proven results.

L’Oréal S.A. is a French beauty major and its Indian subsidiary L'Oréal India was established in 1994 with the head office in Mumbai. In India, it sells shampoos through its worldwide brands like L'Oréal Paris and Garnier. The shampoo assortment consists of hydrating and scalp-care shampoos for example L’Oréal Paris Hyaluron Pure 72H Purifying Shampoo which not only cleanses the scalp but also hydrates the hair.

Hindustan Unilever Limited (a subsidiary of Unilever plc) is located in Mumbai and has roots going back to 1931 in India. It provides hair care through brand names such as Sunsilk, Clinic Plus and Dove. The mentioned shampoos are aimed at the mass and mid-market consumers who are offered nourishing, softening, and smoothing variants that are appropriate for the Indian hair types.

Procter & Gamble (P&G) opened its doors in India in 1985 and its regional business is run from Mumbai. The most famous shampoo brands of P&G in India are Pantene, which is popular for its Pro-Vitamin B5 hair repair and strength-boosting formulas, and Head & Shoulders for the anti-dandruff scalp care. The product range of these brands covers anti-dandruff, hair-fall control, moisturizing, and damage-repair solutions for various hair needs.

Johnson & Johnson Consumer Inc. came to India in 1957 and so far has been offering baby and child-care shampoos through brands such as Johnson's Baby. The company's shampoo products were mainly for the infants and young children, featuring gentle, tear-free cleansing formulas, and mild fragrance, thus, addressing safety and mildness requirements for baby hair and scalp care.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other prominent players in the market include Colgate-Palmolive Company, Dabur India Limited, Kao Corporation, Beiersdorf AG, Oriflame Holding AG, and Marico Limited, among others.

To explore the comprehensive India Shampoo Market 2026-2035 report with full data tables, segmentation and region-wise breakdown, download a sample or contact our team for a consultation call. Unlock actionable insights now to shape your hair-care strategy for India’s rapidly evolving shampoo market.

India Scalp Treatment And Dermatology Hair Care Trends

India Bath Care Innovation Landscape

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 1.26 Billion.

The market is projected to grow at a CAGR of 4.80% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach USD 2.01 Billion by 2035.

Some of the pivotal strategies that sustain the India shampoo market are the premium innovations, the use of natural and herbal ingredients, and the extension of the scalp-focused and problem-solving formulations.

Key trends aiding the market expansion include a shift towards waterless and low-water shampoos, as well as the popularity of dry shampoos, shampoo bars, and powder-based shampoos.

Regions considered in the market are North India, East and Central India, West India, and South India.

Different price categories in the market are mass and premium.

Based on distribution channel, the market segmentations include supermarkets and hypermarkets, convenience stores, drug stores and pharmacies, and online, among others.

The key players in the market include L'Oréal SA, Unilever Plc, Johnson & Johnson Consumer Inc., Procter & Gamble Company, Colgate-Palmolive Company, Dabur India Limited, Kao Corporation, Beiersdorf AG, Oriflame Holding AG, and Marico Limited, among others.

Major challenges for the shampoo market in India are severe price competition, increasing prices of raw materials, and the need for constant innovation to satisfy the diverse hair types. Besides that, companies are confronted with the shift in demand for products with clean and natural ingredients, while there are some distribution gaps in rural areas and the market is getting more fragmented due to the emergence of new digital-first brands.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Price Category |

|

| Breakup by End User |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.