Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

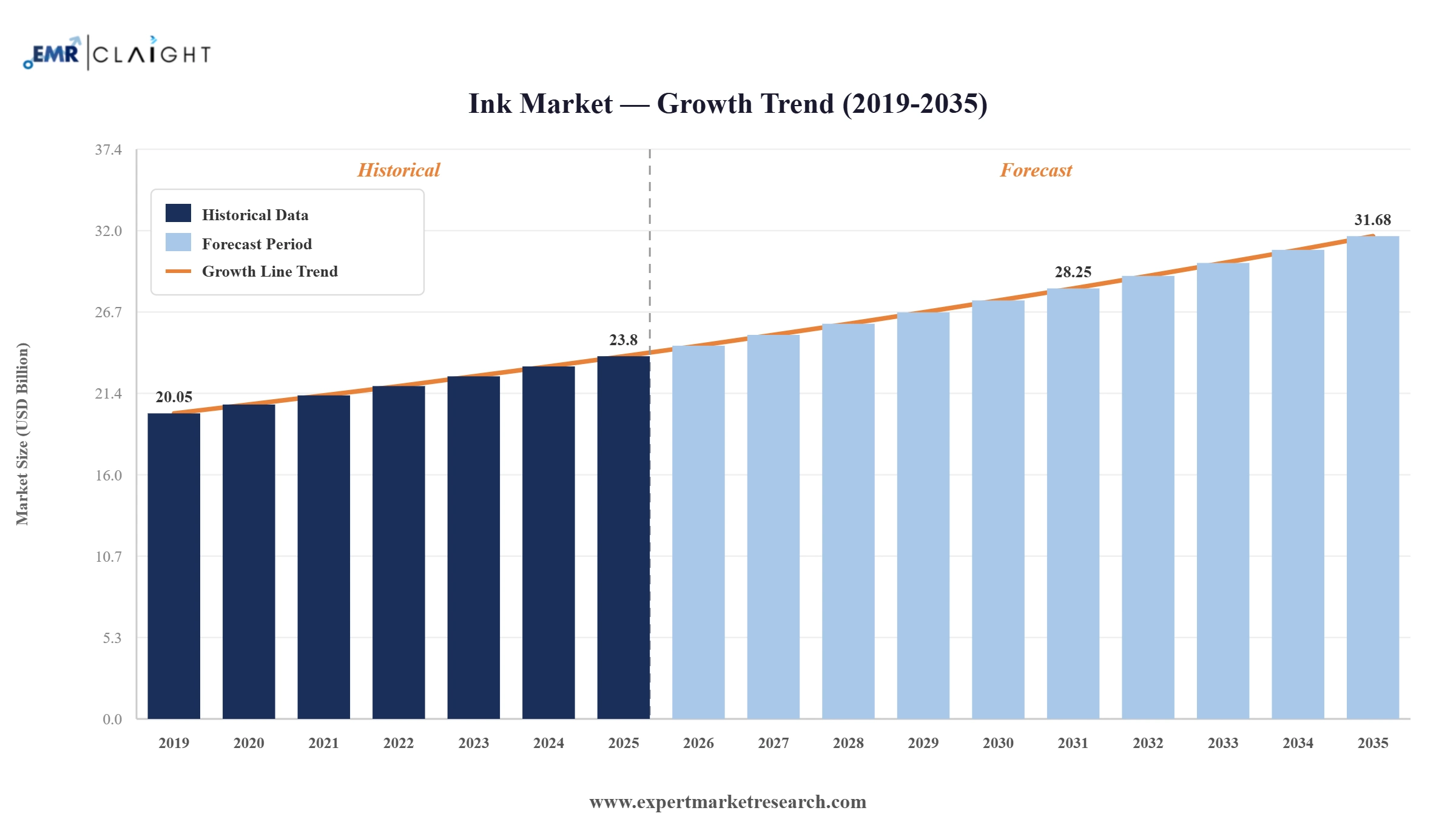

The Global Ink Market was valued at USD 23.80 Billion in 2025 and is set to grow at a CAGR of around 2.90% through 2026-2035. Flexible packaging capacity investments in Asia, alongside sustainability-linked ink innovation, are keeping growth momentum intact. The market is on track to reach USD 31.68 Billion by 2035. Expanding packaging sector demand, rising adoption of eco-friendly ink formulations, accelerating digital printing penetration, and robust e-commerce activity lifting the label and packaging segment are driving the global ink market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global ink market is navigating active consolidation and technology transition. Sustainability-linked formulations are gaining ground across packaging applications, while leading suppliers are investing in regional manufacturing and strategic acquisitions to secure positions in high-growth markets. Regulatory changes around food-contact compliance and recyclable packaging are reshaping product development priorities across Europe, North America, and Asia.

Flint Group Web Offset committed USD 750,000 to transform its Elizabethtown, Kentucky plant into the Americas hub for heatset web offset operations. The investment upgraded varnish manufacturing capabilities and repositioned the facility to serve North America, Latin America, and the Caribbean with the 5600 series ink range.

Sun Chemical announced SunGame, a dedicated product line for the trading card and gaming industry, in May 2026. The range combines high-speed printing inks and durable coatings with brand protection solutions designed to meet international toy safety requirements.

Siegwerk signed a definitive agreement in March 2026 to acquire Hi-Tech Inks, a leading Indian producer of flexographic and gravure printing inks. The combined entity is positioned to become the largest player in India's flexible packaging ink market, holding over 20% share across sites in Bhiwadi and Vapi.

Siegwerk opened a new office and warehouse in Dubai in June 2025, improving service proximity for Middle East packaging customers. The site supports delivery of the company's LED Dual Cure ink technologies, helping regional printers transition to more eco-friendly production processes.

Label and packaging is the dominant application in the global ink market. E-commerce-led demand and rising consumer goods production have sustained flexible packaging and label printing ink volumes. Food, beverage, pharmaceutical, and personal care sectors are the main consumption drivers.

Digital printing is the fastest-growing technology in the global ink market. Inkjet platforms are gaining ground in packaging and commercial print for their short-run flexibility and cost efficiency. Sun Chemical's SunGame launch in 2026 reflects how suppliers are expanding digital ink portfolios.

Water-based and bio-based ink formulations are gaining traction across regulated packaging markets. The German Ink Ordinance, enforceable from January 2027, is driving converter transitions to compliant packaging inks. ALTANA's ACTEGA division and Siegwerk have both expanded their sustainable packaging ink ranges accordingly.

Asia Pacific leads global ink consumption, with China at the centre of flexible packaging ink demand. India's packaging sector growth is drawing fresh investment from global producers. Siegwerk's 2026 acquisition of Hi-Tech Inks positions the combined business as the largest player in India's flexible packaging ink segment.

Commercial printing demand for premium short-run ink formulations continues to rise. UV-curable inks and specialty coatings for brand protection and QR-coded materials are drawing supplier investment. Flint Group's Kentucky plant upgrade and Sun Chemical's SunGame launch both reflect the heightened commercial print focus.

The report of Expert Market Research's titled "Global Ink Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

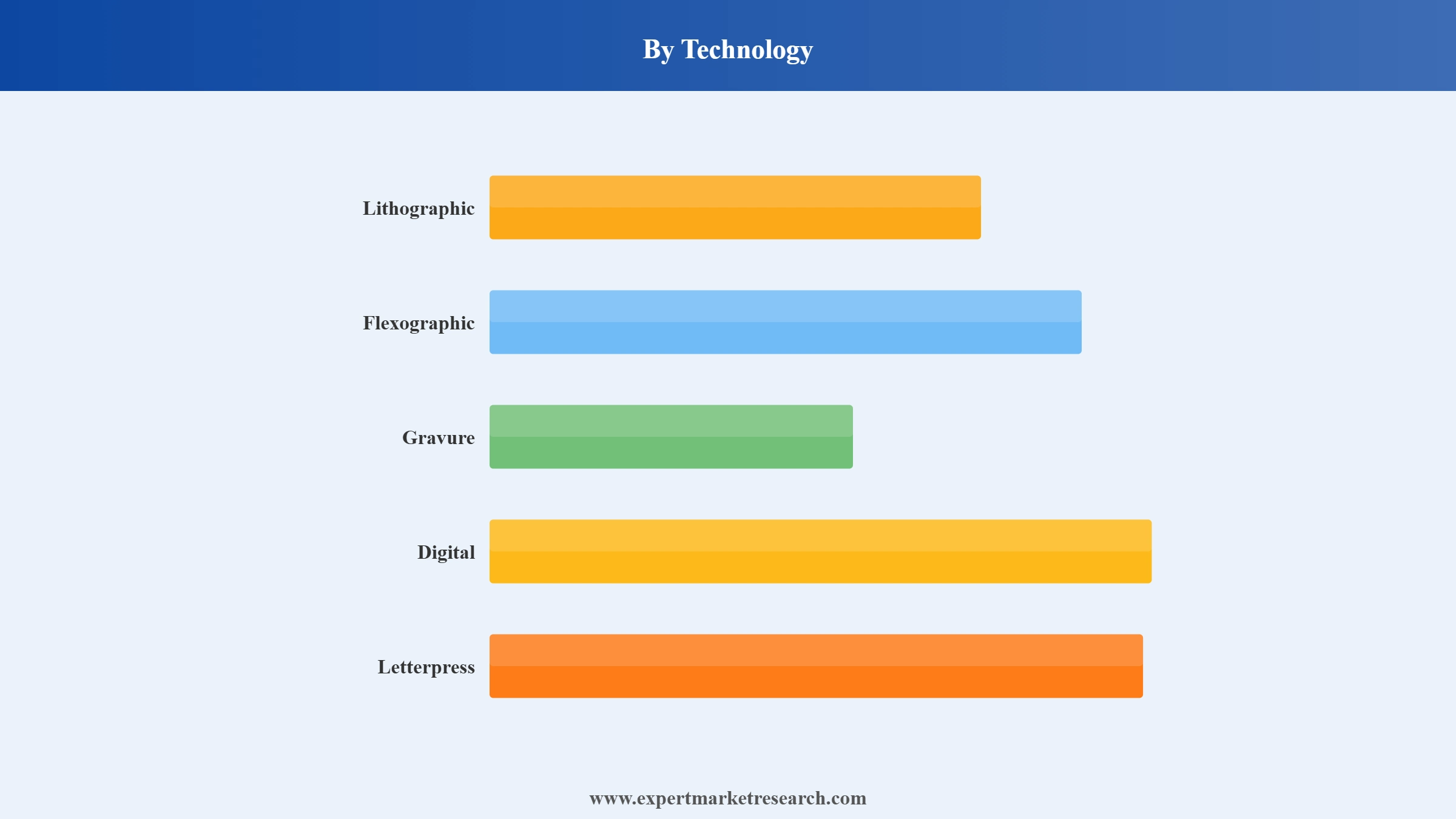

Market Breakup by Technology

Key Insight: Lithographic technology leads the global ink market, supported by its dominant position in commercial printing and carton packaging where offset presses deliver cost-efficient high-volume output. Digital is the fastest-growing segment, driven by inkjet adoption in narrow-web labels and flexible packaging across Asia Pacific and North America.

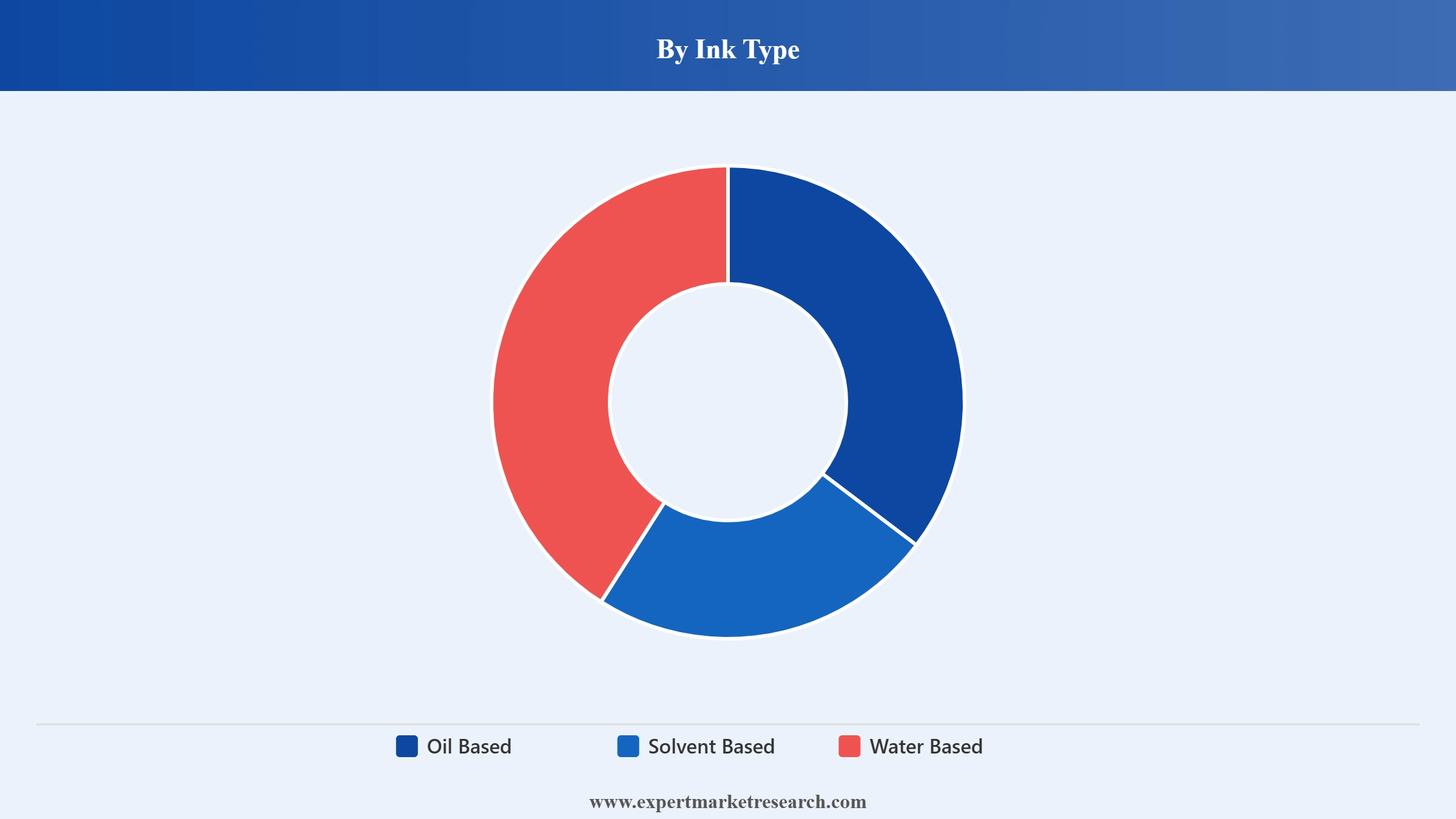

Market Breakup by Ink Type

Key Insight: Oil-based inks hold the largest type-level share, anchored by their use in heatset web offset, newspaper, and commercial offset printing. Water-based inks are the fastest-growing type, driven by VOC reduction mandates in Europe and rising food-contact compliance requirements across the global packaging supply chain.

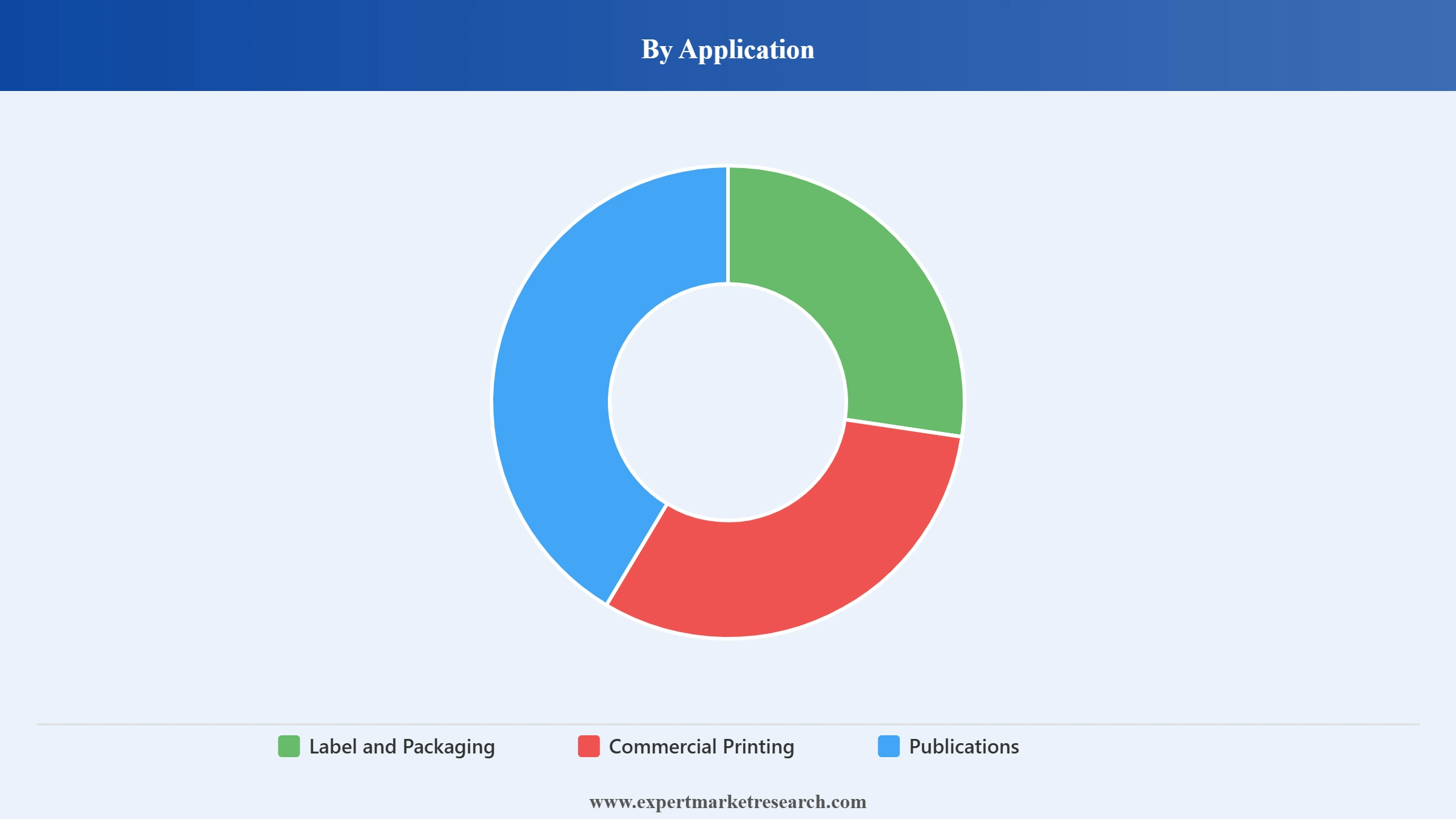

Market Breakup by Application

Key Insight: Label and packaging is the dominant application, accounting for the majority of global ink consumption. Sustained e-commerce growth and the non-discretionary nature of product labelling in food, beverage, pharmaceutical, and consumer goods sectors provide structural demand resilience throughout the forecast period.

Market Breakup by Region

Key Insight: Asia Pacific leads global ink consumption, underpinned by a concentration of flexible packaging converters and a fast-growing e-commerce-driven label segment. China, India, and Southeast Asia form the core demand base, with India and Southeast Asia recording the highest within-region growth rates through the forecast period.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Technology, Lithographic dominates the market due to its established cost efficiency and suitability for large-volume commercial and packaging print runs

Lithographic printing leads the global ink market by volume and value. The segment's strength lies in commercial printing and packaging, where high-speed offset presses deliver consistent color quality at scale. Label and packaging industries rely on lithographic systems for carton printing, folding box board, and food-grade packaging. Sun Chemical and Flint Group maintain broad lithographic ink portfolios serving the global installed base.

Digital technology is gaining ground steadily. Inkjet installations in narrow-web label printing and digital packaging have grown each year through 2025. Sun Chemical's SunGame launch in May 2026 and Kornit Digital's Atlas MATRIX platform reflect how suppliers are responding to the rising demand for short-run and customized digital print workflows.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Ink Type, Oil Based inks account for the dominant share of the market due to their broad compatibility with traditional high-volume printing processes

Oil-based inks hold the highest market share by ink type, anchored by their role in heatset web offset, newspaper, and commercial offset printing. The segment benefits from the large global installed base of compatible equipment and cost-effective formulation economics for high-run applications. Sun Chemical and Flint Group both maintain extensive oil-based ink lines serving this installed base.

Water-based inks are the fastest-growing type, driven by VOC regulation in Europe and tightening food-contact compliance across the packaging supply chain. The German Ink Ordinance, enforceable from January 2027, has accelerated converter transitions to low-migration formulations. ALTANA's ACTEGA unit and Siegwerk have both expanded their water-based packaging ink offerings in response.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Application, Label and Packaging accounts for the dominant share of the market due to the structural growth of e-commerce, food production, and regulated consumer goods sectors

Label and packaging is the global ink market's largest application. Demand is driven by continuous requirements from food and beverage, pharmaceutical, and consumer goods sectors where product labelling is non-discretionary. E-commerce-led packaging volumes have added a further structural demand layer. The segment's resilience across economic cycles makes it the most reliable consumption anchor in the market.

Commercial printing is the second-ranked application. While publication volumes have declined, commercial print for direct mail, point-of-sale, and branded packaging inserts has held relatively steady. Digital technology adoption within the segment is adding a growth dimension, particularly for short-run and personalized applications in North America and Europe.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific dominates the global ink market due to a concentrated flexible packaging manufacturing base, large-scale label printing capacity, and sustained downstream consumer goods demand

Asia Pacific leads the global ink market, accounting for more than 40% of total consumption. China is the primary driver, home to the largest concentration of flexible packaging converters and publication ink consumers globally. India's packaging sector, supported by government industrial policy and consumer goods growth, is adding fresh capacity and drawing direct investment from global suppliers. Siegwerk's March 2026 acquisition of Hi-Tech Inks is the clearest signal of this priority.

North America holds a structurally important position, with a large installed base of commercial and heatset web offset presses and growing digital printing adoption. Europe benefits from strict sustainability regulation driving premiumization of ink formulations. Latin America and the Middle East and Africa are smaller markets growing steadily, supported by packaged goods sector expansion and rising print infrastructure investment.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global ink market is led by a concentrated group of large international suppliers with broad technology portfolios spanning packaging, commercial print, and specialty applications. Sun Chemical and Flint Group hold the largest positions globally, followed by regional and specialty players across Asia and Europe. Sustainability capabilities, food-contact compliance certifications, and digital print compatibility are the primary competitive differentiators heading into the forecast period.

Mergers, acquisitions, and geographic expansion are actively reshaping the competitive structure. Siegwerk's acquisition of Hi-Tech Inks in India, Flint Group's investment in its Kentucky hub, and Sun Chemical's SunGame launch all signal active repositioning among the leading players.

Founded in 1977 and headquartered in Wesel, Germany, ALTANA AG operates through BYK, ECKART, ELANTAS, and ACTEGA divisions. The ACTEGA unit serves printing inks and coatings directly, providing water-based, UV, and energy-curable ink systems for packaging converters. ALTANA's focus centres on recyclable packaging compliance and low-migration ink technologies for food-contact applications globally.

Founded in 1897 and headquartered in Midland, Michigan, Dow is one of the world's largest diversified materials science companies. Core resins and specialty materials from Dow are key inputs to printing ink formulations globally, supplying binders, rheology modifiers, and functional additives to the ink industry across oil-based, water-based, and UV-curable chemistries.

Founded in 1818 and headquartered in Parsippany, New Jersey, Sun Chemical is a member of the DIC Group and one of the world's largest printing ink producers. The company serves packaging, commercial print, and specialty applications with flexographic, gravure, offset, and digital ink portfolios. Recent launches include SunGame for the trading card industry and TINKREDIBLE MGA for metal decoration.

Founded in 1920 and headquartered in Luxembourg, Flint Group is a leading global supplier of printing inks, coatings, and consumables. It operates across five segments including Flexible Packaging, Narrow Web, Sheetfed Offset, and Digital Xeikon. A USD 750,000 investment in its Elizabethtown, Kentucky facility in 2026 reinforced the company's Americas manufacturing and commercial operations hub.

Other key players in the market are Akzo Nobel N.V., Central Ink Corporation, DIC Corporation, Siegwerk Druckfarben AG, Toyo Ink Group, Sakata INX Corporation, hubergroup, INX International Ink Co., Wikoff Color Corporation, and others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Our full report for 2026-2035 provides the production data, application demand analysis, price trends, and competitive intelligence to navigate the global ink market with confidence. Reach out to our team to access the complete report or request a customised version.

Non-Conductive Inks Market

Conductive Inks Market

Mexico Ink Market

Regulatory Compliant Colorant Materials

Digital Printing Workflow Consumables

Industrial Coating Colorant Systems

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 23.80 Billion.

The market is assessed to grow at a CAGR of 2.90% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 31.68 Billion by 2035.

The major drivers of the market include the increasing applications of ink in the packaging and labelling sector, growth of the commercial printing sector, rising demand from the developing regions, rising disposable incomes, and the growing technological advancements.

The key trend guiding the growth of the ink market is the development and launch of environment-friendly, vegetable-oil based inks.

The major regions in the market are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific, with the Asia Pacific accounting for the largest market share.

Lithographic ink is the leading technology in the market.

Oil based inks represent the leading ink type in the market.

The application segment is led by the label and packaging sector.

The leading key players in the market are ALTANA, Dow, Sun Chemical, Central Ink Corporation, Flint Group, and Akzo Nobel N.V., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Technology |

|

| Breakup by Ink Type |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.