Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

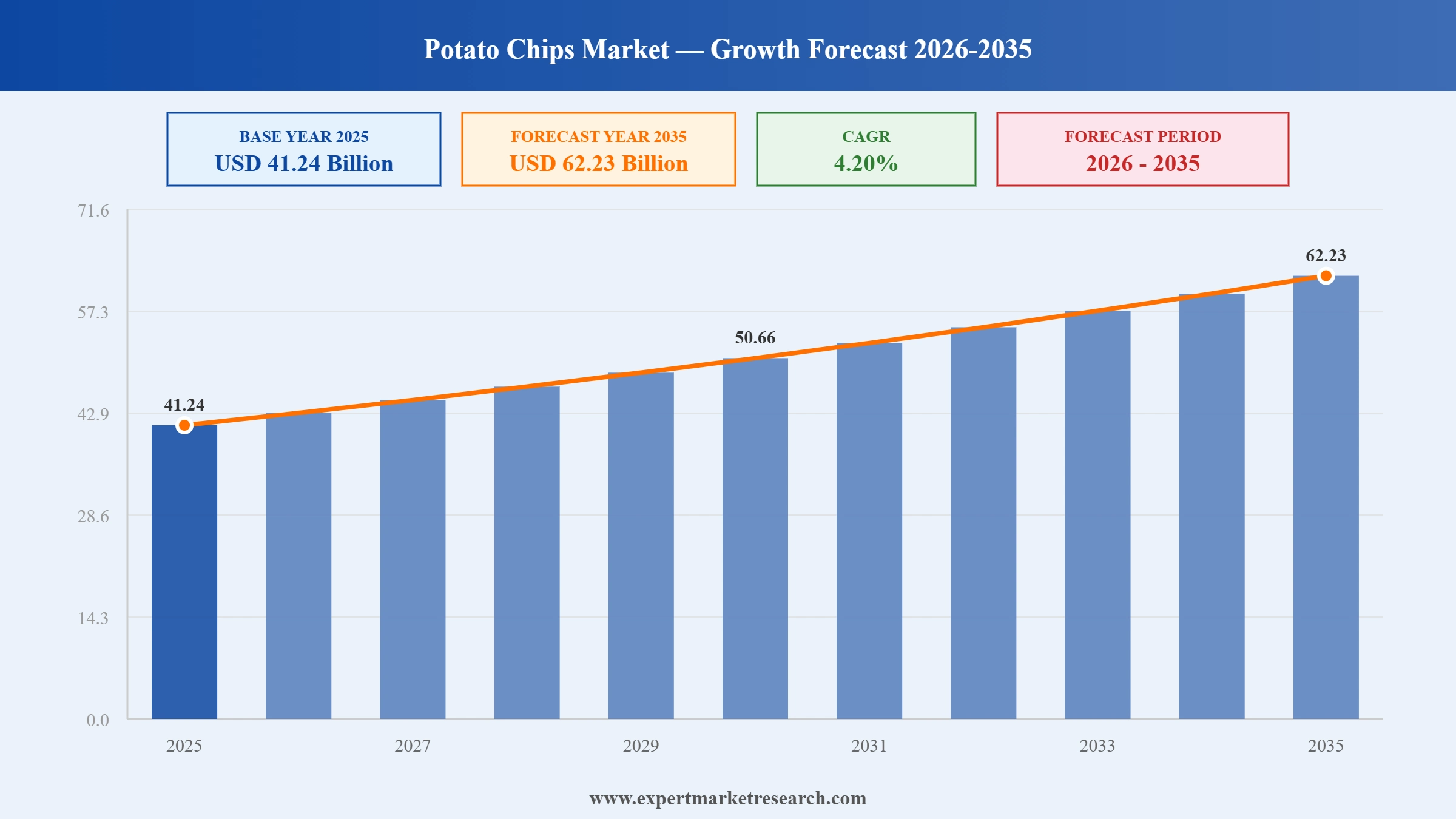

According to Expert Market Research, The global potato chips market was valued at approximately USD 41.24 Billion in 2025 and is projected to reach USD 62.23 Billion by 2035, expanding at a compound annual growth rate (CAGR) of 4.20% over the forecast period. Growth is underpinned by rising snack consumption in emerging economies, ongoing flavour and packaging innovation, and the continued expansion of e-commerce food retail. North America remains the largest regional market by value, while Asia Pacific particularly India and China is expected to record the fastest growth rate through 2035.

Get a sample of the market report in PDF – REQUEST A FREE SAMPLE

The global appetite for convenient, flavourful snacks is not a passing trend it is a structural shift in how people eat. Three macro-level forces are converging to sustain the long-term expansion of the potato chips market:

Urbanisation and Lifestyle Acceleration: The UN estimates that by 2050, nearly 68% of the global population will live in urban areas. Urban lifestyles characterised by longer working hours, reduced home-cooking frequency, and increased reliance on grab-and-go food formats are creating a sustained base of demand for packaged snacks. Potato chips, which require no preparation, refrigeration, or utensils, sit squarely at the centre of this shift.

The Millennial and Gen Z Snacking Behaviour: Younger consumer cohorts are replacing traditional three-meal-a-day eating patterns with a "grazing" model, eating 4–6 small portions throughout the day. Research consistently shows that millennials and Gen Z consumers are more likely to purchase flavour-forward, limited-edition, and brand-collaborating chip products as seen in launches like Utz x Mike's Hot Honey and Pringles x Miller Lite. This demographic influence is reshaping product development priorities across the market.

Rise of the "Better-for-You" Snack Tier: The clean-label movement has created a profitable middle tier in the potato chips market products that consumers perceive as healthier than conventional chips but still deliver the indulgence they seek. Baked, air-fried, reduced-sodium, and organic variants are capturing premium pricing while broadening the addressable audience for the category.

Consumers are increasingly becoming more health conscious, leading to a surge in the demand for better-for-you snacks, including potato chips. Hence, manufacturers are developing chips with higher protein and fibre content, made from ingredients such as quinoa, chickpeas, and lentils, among others.

The robust growth of the e-commerce sector is driving the potato chips demand growth. E-commerce platforms offer round-the-clock availability of potato chips and boast a wide selection of potato chip flavours and brands, including gourmet, limited-edition, and international varieties. Online platforms also enable brands to customise their offering based on regional preferences as well as provide detailed product descriptions, ingredient transparency, and nutritional information, enabling customers to make informed decisions.

Advancements in packaging technology are increasing the potato chips market value. Key players are developing resealable packs, single-serve packs, and materials engineered to optimise the freshness, convenience, and packaging sustainability of potato chips. In addition, resealable packs assist in retaining the quality of the product, thus appealing to the market segment that appreciates fresh flavours.

Get a sample of the market report in PDF – REQUEST A FREE SAMPLE

Potatoes sit at the heart of the supply chain for this industry, and the health of that supply chain directly dictates production costs, chip quality, and manufacturer margins. While global potato production remains substantial exceeding 375 million metric tonnes annually the industry is not insulated from agricultural risk. Key supply-side variables that market participants monitor closely include:

Potato Variety Selection: Manufacturers specifically source high-solids varieties such as Russet Burbank, Atlantic, and Shepody, which produce crispier, more uniformly sized chips with optimal oil absorption rates. Variety availability fluctuates by growing region and season.

Water Availability: Potato farming is water-intensive. In regions experiencing increasing drought frequency parts of the US Pacific Northwest, Western Europe, and Northern China water-efficient irrigation investment is becoming a competitive necessity rather than an optional sustainability measure.

Price Volatility: Raw potato prices are subject to weather disruptions, energy costs (for storage and processing), and fertiliser price swings. The 2021–2023 global fertiliser cost spike directly impacted the cost-per-bag economics for smaller regional chip manufacturers.

Regenerative and Contracted Farming: Leading brands are increasingly moving toward long-term contracted farming relationships and regenerative agriculture pilots as evidenced by the Ahold Delhaize USA and Campbell's Company initiative for Kettle Brand and Cape Cod chips to stabilise raw material supply and build environmental credibility.

Increasing consumption of snacks; growing trend of health and wellness; rising focus on sustainability; and flavour innovations are favouring the potato chips market expansion.

Ahold Delhaize USA, along with The Campbell’s Company, launched a regenerative agriculture pilot programme to reduce Scope 3 greenhouse gas (GHG) emissions associated with potato farming. The collaboration supports potato farms to implement regenerative farming techniques and create more resilient agricultural systems to carbon emissions through soil health practices. The potatoes harvested from the project will be used in Kettle Brand® chips, Cape Cod® chips, and Campbell’s® soups.

Utz® collaborated with Mike’s Hot Honey® to create Utz Mike’s Hot Honey EXTRA HOT potato chips. The gluten-free and kosher-certified potato chips are available in on-the-go, 2.625-ounce size and a take-home, 7.75-ounce size. The potato chips can be purchased from leading mass, grocery, and convenience stores throughout the United States.

PepsiCo India expanded its potato chips snacks portfolio and launched a heart-shaped potato-based pellet under its flagship brand, Lay’s Shapez. Lay’s Shapez Heartiez portfolio includes masala and caramel flavours to foray into the sweet-flavoured chips. Through this, the company aims to meet the growing demand for crunchy snacks that go beyond traditional offerings in the rapidly expanding potato-based pellet chips market.

Kellogg’s-owned Pringles created a new potato chip range amid the growing demand for lower-salt snacks that include grains. The chips, made from grains and fibre such as barley and wheat, contain a lower amount of salt than conventional chips. The Pringles Multigrain is available in three flavours- Sour Cream & Chilli, BBQ Sauce Flavour and Roast Chicken & Rosemary.

Reportedly, over 90% of Americans eat one to three snacks per day. Potato chips are considered a quintessential snack food due to their convenience, long shelf life, ease of availability in diverse distribution channels, and excellent flavour profiles. The availability of potato chips in different flavours, ranging from classic salt to exotic flavours, also fuels their popularity as a preferred snack food.

The growing focus on health and wellness among consumers is surging the demand for air-popped or baked potato chips made with fewer preservatives, natural ingredients, and no artificial colours or flavours. Brands are also increasingly utilising non-GMO, high-quality, and organic potatoes to appeal to health-conscious consumers.

With the increasing environmental consciousness, potato chip manufacturers are sourcing potatoes from farms which are adopting organic and sustainable agricultural practices and implementing water-efficient irrigation techniques. They are also utilising sustainable packaging solutions, such as recyclable, compostable, and biodegradable materials, to reduce plastic waste and lower the use of single-use plastics.

The growing consumer demand for bold and innovative flavours is driving the potato chips market development. Manufacturers of potato chips are combining fusion flavours such as sriracha and honey and sweet chilli and lime to create a novel and bold snacking experience. They are also introducing flavours inspired by ethnic and regional cuisines such as wasabi, tandoori masala, and spicy kimchi, among others, to cater to diverse customer tastes.

Modern industrial potato chip lines use continuous fryers and advanced heat-transfer technology to maintain consistent oil temperature, ensuring uniform chip colour and texture. Newer systems reduce energy consumption per kilogram of chips produced by up to 20% compared to batch-frying methods from a decade ago.

Kraft Heinz's 2025 partnership with an AI technology firm to develop machine-learning-based flavour profiles signals a new frontier in product innovation. Rather than relying solely on consumer panels and chef-led R&D, manufacturers are feeding purchase data, social media sentiment, and flavour receptor research into algorithmic tools to predict the next high-demand taste profile before it surfaces organically.

Brands are beginning to explore active packaging formats that include humidity indicators and freshness sensors. These technologies extend effective shelf life communication to consumers a meaningful value-add in markets where crunchiness is a direct proxy for quality perception.

Camera-based optical sorting systems now identify and remove discoloured, undersized, or damaged potato slices before frying, reducing raw material waste and product reject rates at scale. This has particular value in premium and artisan chip manufacturing where visual uniformity commands a price premium.

Get a sample of the market report in PDF – REQUEST A FREE SAMPLE

Rising concerns regarding excessive sodium intake among customers due to the increasing prevalence of cardiovascular issues and hypertension are creating lucrative potato chips market opportunities. Brands are developing potato chips with reduced sodium content and using natural flavouring alternatives such as spices, herbs, and vinegar to enhance their taste. Besides, the growing popularity of gluten-free diets and the increasing prevalence of food allergies among customers are boosting the demand for allergen and gluten-free potato chips.

Key players in the market are investing in energy-efficient production processes, such as the use of renewable energy sources such as wind or solar, to optimise energy consumption. They are also focusing on minimising waste during the manufacturing process by reusing potato skins, peels, and other-by products in animal feed and compost, among others.

The Expert Market Research report titled “Global Potato Chips Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Product Type

Market Breakup by Flavour

Market Breakup by Distribution Channel

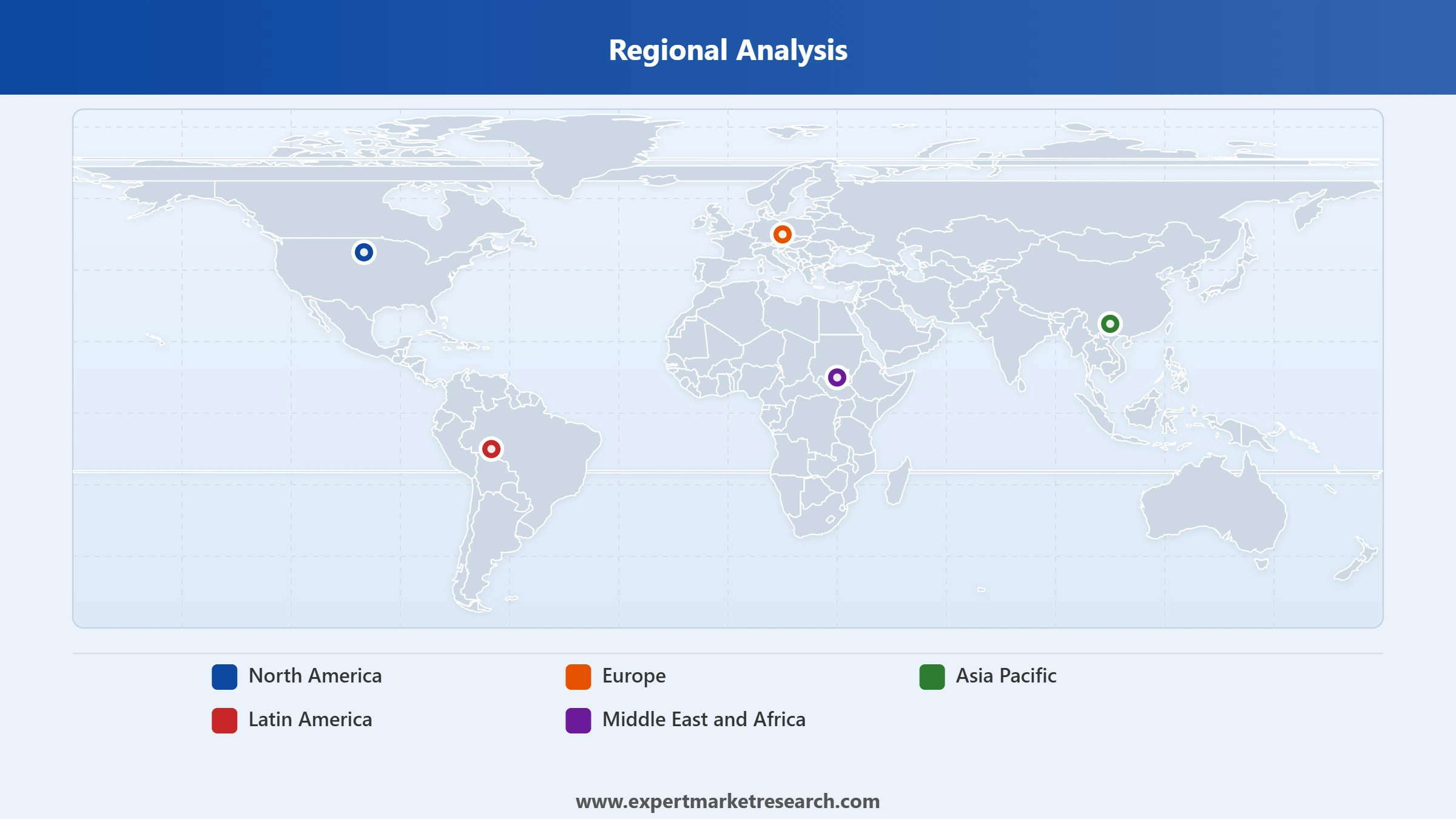

Market Breakup by Region

The potato chips market does not move uniformly across geographies. Understanding regional nuances is critical for market participants making investment, expansion, or procurement decisions.

Get a sample of the market report in PDF – REQUEST A FREE SAMPLE

North America remains the most mature and high-value market for potato chips, driven by deeply ingrained snacking culture, a dense modern retail infrastructure, and the presence of dominant global players including PepsiCo's Frito-Lay division and Utz Brands. The US alone was valued at approximately USD 10 billion in 2022 according to USDA data. The region is witnessing a clear premiumisation trend: consumers are trading up from standard bags to kettle-cooked, artisanal, and functional-ingredient varieties. Private-label chip brands from major grocery chains are also gaining ground, with consumers increasingly perceiving them as quality equivalents at lower price points.

Europe's market is characterised by strong regional flavour preferences and a higher baseline sensitivity to clean-label and sustainable sourcing claims than most other markets. Germany, the United Kingdom, and France are the largest individual country markets. The Lorenz Bahlsen Snack-World and Burts Snacks represent the "local champion" model regionally rooted brands that compete effectively against global giants by emphasising sourcing provenance and authentic recipes. EU-level regulations around food labelling, ingredient transparency, and packaging sustainability are raising compliance costs but are also creating product differentiation opportunities for brands that invest early.

Asia Pacific is the market's primary growth engine, projected to register the highest CAGR through the forecast period. China and India together account for the majority of this regional growth. India's potato chip market is particularly compelling: the country produces over 56 million tonnes of potatoes annually, provides a cost-effective manufacturing base, and hosts a fast-growing middle class with rising disposable income. PepsiCo's Lay's Shapez and ITC's Bingo! brand are actively battling for share in this market. The region's flavour diversity is also unmatched wasabi, nori, spicy miso, masala, pani puri, and chilli-lime variants co-exist with classic salted options across modern trade, kirana stores, and e-commerce platforms.

Latin America presents moderate but consistent growth. Brazil and Mexico are the leading country markets. The dominance of informal retail channels (traditional markets and small neighbourhood stores) means that distribution strategy is more complex here than in developed markets. Affordable single-serve portion formats remain the highest-volume SKU in most countries.

This region's market is still in an early-growth phase but is accelerating rapidly due to young demographics, urbanisation, and growing modern retail penetration. Saudi Arabia, UAE, and South Africa are the primary value contributors. Halal-certified potato chips are a market requirement in GCC countries, and manufacturers entering this market must ensure their entire supply chain including flavourings and additives meets halal standards.

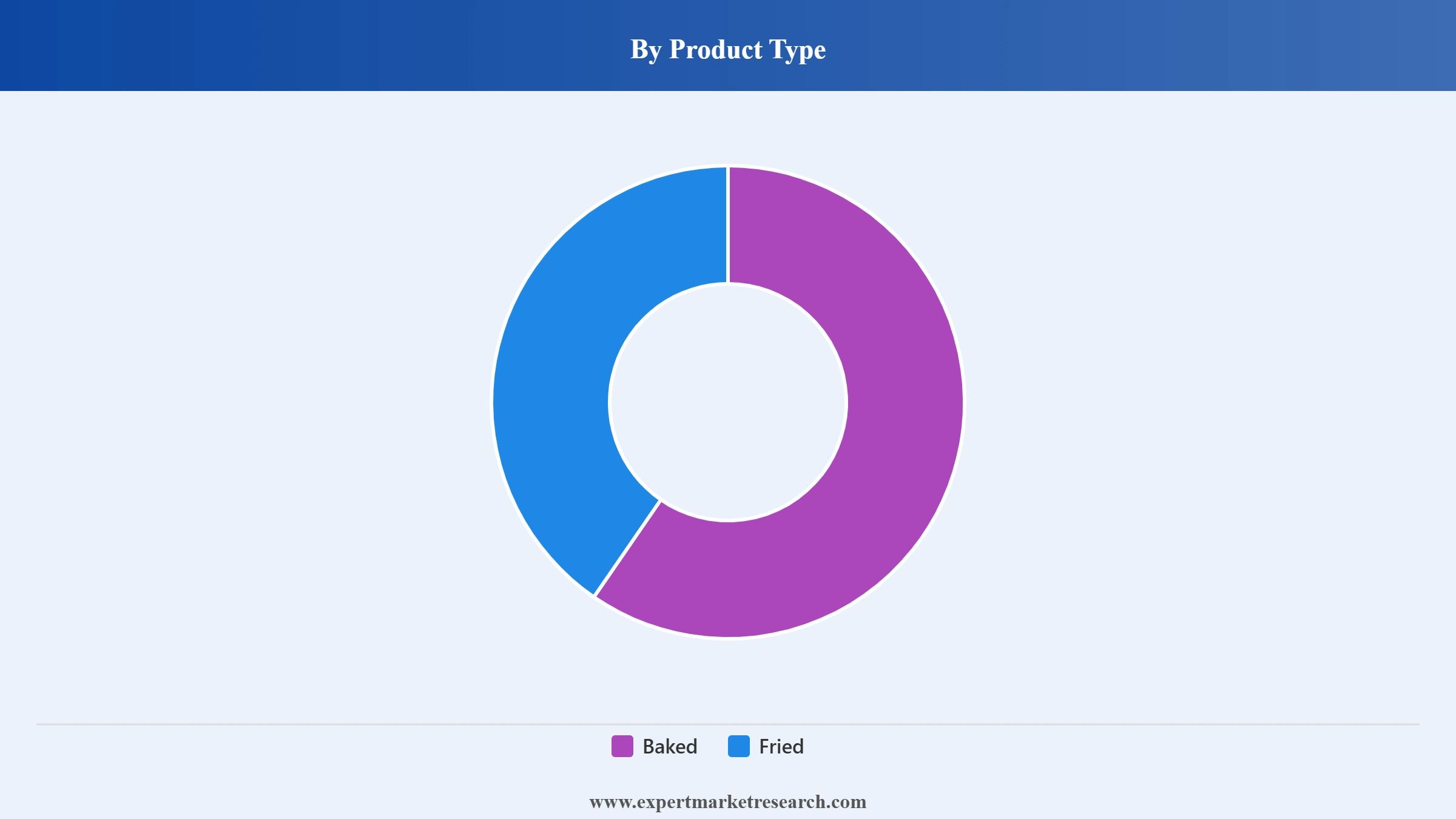

As per the potato chips market analysis, baked potato chips have 14% fewer calories, 50% less fat and 67% less saturated fat than traditional potato chips. Such chips are witnessing high demand in regions such as North America and Europe. Leading market players such as Pepsico, Parle, and Alaska Chip Company, Inc. are capitalising on this trend to gain a competitive edge in the market. Meanwhile, fried potato chips are the widely adopted chips category due to their wide availability and affordability. The rising popularity of snack foods, a rise in population, and improving living standards aid the demand for snacks, including fried potato wafers.

Get a sample of the market report in PDF – REQUEST A FREE SAMPLE

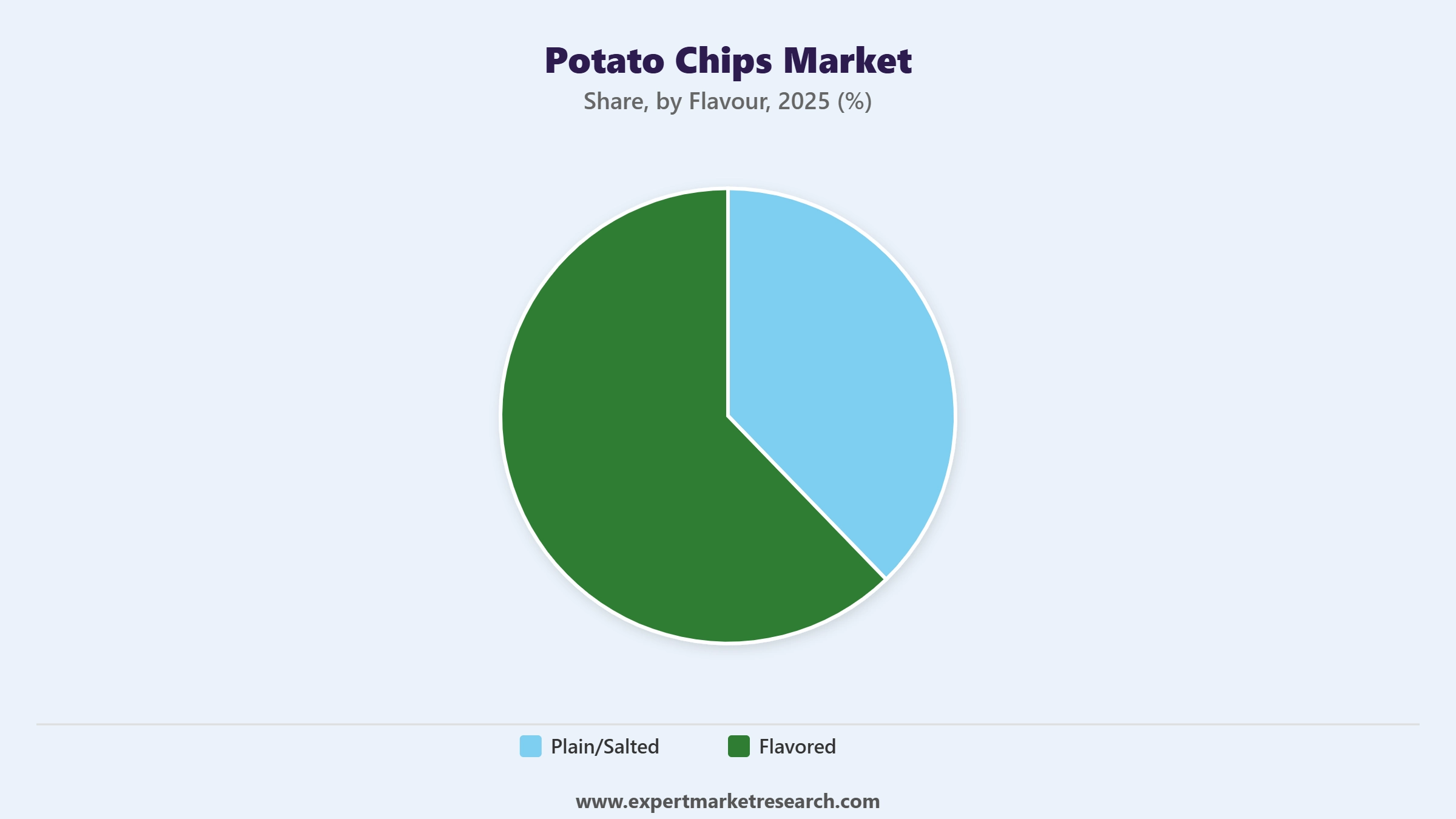

Based on flavour, plain/salted chips dominate the growth of the potato chips market as these are mostly served with fast food items such as burgers and sandwiches. Conversely, flavoured potato chips made from spices and added flavourings are widely popular as an indulgent snack across the globe.

One segment that is frequently underweighted in potato chips market analysis is packaging format. Packaging is not just a vehicle for the product it is increasingly a direct driver of purchase decisions, consumption occasions, and sustainability positioning.

Single-Serve / On-the-Go Formats: These are the fastest-growing packaging segment, driven by commuter culture, convenience retail expansion, and calorie-conscious portion awareness. Single-serve packs under 50g account for a growing share of convenience store and vending channel revenue globally.

Family and Bulk Packs: Still the dominant format by volume in retail grocery, family-size bags benefit from at-home snacking occasions and multi-person consumption events. The growth of hybrid work arrangements post-2020 has sustained elevated household snack purchasing in most developed markets.

Resealable Bags: Premium and artisan chip brands have led adoption of resealable closures, which command a price premium and signal freshness commitment. Mainstream brands are beginning to adopt this format as differentiation migrates down the price ladder.

Sustainable Packaging Materials: The industry is under growing pressure from both consumers and regulators to reduce reliance on multi-layer plastic film. Home-compostable high-barrier films (such as TIPA's 2025 snack packaging product) and recyclable mono-material structures are attracting investment. Frito-Lay's commitment to 100% recyclable or compostable packaging is the most high-profile statement of intent in the industry to date.

Key potato chips market players are focusing on flavour and format innovations to meet evolving customer preferences. Potato chips companies are also adopting sustainable packaging solutions and sourcing potatoes from organic and eco-friendly farms to capitalise on the growing environmental consciousness among customers.

Utz Brands, Inc., headquartered in Pennsylvania, United States, is a leading manufacturer of diverse savoury snacks. Founded in 1921, the company’s popular brands include On The Border® Chips & Dips, Boulder Canyon®, Zapp’s®, and Utz®, among others. Its products are distributed across the US through mass merchandisers, grocery, convenience, club, and drug channels.

The Lorenz Bahlsen Snack-World GmbH & Co KG, headquartered in Neu-Isenburg, Germany, is one of the leading European snack companies. Its product portfolio includes pretzel sticks, chips, flips, and nuts. Some of its leading brands include Curly, Crunchips, Saltletts, NicNac’s or Saltletts.

Campbell Soup Company, headquartered in New Jersey, United States, and founded in 1869, is a leading producer of soups and canned food products. Some of its leading brands include Cape Cod, Campbell’s, Goldfish, Prego, Snyder’s of Hanover, Michael Angelo’s, noosa, Pace, and Pacific Foods. In FY 2024, the company generated net sales of USD 9.6 billion. Calbee, Inc., headquartered in Tokyo, Japan, is one of Asia's most significant potato chip and snack manufacturers. Founded in 1949 and listed on the Tokyo Stock Exchange, Calbee distributes products across Japan, the United States, United Kingdom, and a growing number of European and Asian markets. Its flagship Jagabee and Calbee Potato Farm brands have earned strong brand equity in Japan's premium snack tier. In 2025, Calbee expanded its European footprint through an acquisition of a local snack manufacturer a move that reflects the brand's strategic ambition to become a genuinely global player beyond its home market stronghold.

Burts Snacks Limited, based in London, England, and founded in 1999, is one of the independent premium hand-cooked snacking companies in the United Kingdom. The company uses Red Tractor-approved potatoes from local growers in Cornwall and Denver. Some of its best seller flavours include Sea Salt & Malt Vinegar, Lightly Sea Salted, and Mature Cheddar & Onion potato chips.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other key players in the potato chips market include Kellogg Company, PepsiCo, Inc., Herr Foods Inc., and Calbee, Inc.

The competitive playbook in the potato chips market has grown considerably more sophisticated over the last decade. Five distinct strategic approaches characterise how leading players are currently competing:

Flavour-Led Differentiation: Limited-edition and consumer-co-created flavours (Lay's "Do Us A Flavor", Pringles collaborations) generate social media engagement and trial purchase behaviour beyond what traditional advertising can achieve at equivalent cost.

Health and Functional Positioning: Investing in baked, air-fried, reduced-sodium, and organic product lines allows brands to retain health-conscious consumers who might otherwise exit the category entirely. This strategy also enables higher retail price points than conventional fried chips.

Supply Chain Vertical Integration: Brands that control or closely partner on raw material production through contracted farming or regenerative agriculture programmes gain resilience against commodity price volatility and acquire sustainability narratives that resonate with ESG-oriented retail buyers.

Geographic Expansion into Emerging Markets: Asia Pacific, Latin America, and MEA markets offer significantly higher per-capita consumption growth potential than saturated North American and Western European markets. First-mover brands establishing distribution, manufacturing, and flavour localisation capabilities early are positioned to capture disproportionate share as these markets mature.

E-Commerce and Direct-to-Consumer Optimisation: Online retail now represents the fastest-growing distribution channel for potato chips globally. Leading brands are investing in direct-to-consumer platforms, customised variety packs, and subscription snack box models to capture data-rich consumer relationships beyond the anonymous brick-and-mortar environment.

Get a sample of the market report in PDF – REQUEST A FREE SAMPLE

For investors, brand managers, procurement teams, and market entrants evaluating the potato chips market, several opportunity vectors stand out:

Premium and Artisan Segment Growth: The artisan and premium chip category typically characterised by hand-cooked preparation, single-origin potato sourcing, and craft-style packaging is growing faster than the mainstream segment in developed markets. Brands like Burts Snacks (UK) and Cape Cod (US) demonstrate that consumers will pay a meaningful premium for perceived quality authenticity. Entry into this segment is achievable at smaller production scales than mainstream chip manufacturing, making it accessible to new market participants.

White-Space Geographies: Southeast Asia (Vietnam, Indonesia, Thailand), Sub-Saharan Africa (Nigeria, Kenya), and the Gulf Cooperation Council (GCC) countries represent under-penetrated markets with rapidly expanding modern retail footprints. Distribution partnerships with regional FMCG distributors and co-manufacturing arrangements with local food processors are the most capital-efficient routes to entry.

Private Label Supply Opportunities: The growth of own-brand (private label) potato chips at major global grocery retailers including Walmart, Carrefour, Tesco, and Amazon Fresh is creating significant volume opportunities for contract manufacturers. Retailers are allocating increasing shelf space to private-label snacks as they improve margin economics and respond to consumer price sensitivity in inflationary environments.

Functional and Fortified Chip Innovation: The "better-for-you" snack space is moving beyond merely removing negatives (less fat, less sodium) toward actively adding positives. Protein-fortified chips (using lentil or chickpea flour blends), prebiotic-infused variants, and vitamin-enriched products are small but rapidly growing sub-niches. The intersection of snacking convenience and functional nutrition is where the next generation of value-added potato chip products is being built.

No market analysis is complete without a candid assessment of the headwinds. The potato chips industry faces several structural and emerging challenges that market participants must account for in their strategic planning.

Health and Wellness Headwinds: Despite the growth of better-for-you variants, potato chips as a category remain associated with high calorie density, elevated sodium content, and saturated fat nutritional attributes that are increasingly regulated and stigmatised in public health discourse. Government-led front-of-pack labelling schemes (such as Chile's black octagon warning labels and the UK's traffic light system) are contributing to consumer reconsideration of high-sodium snack purchases. These regulatory trends are most advanced in Latin America and Europe but are spreading to other markets.

Commodity Cost Volatility: Raw potato prices, cooking oil costs (sunflower, palm, canola), and packaging material prices are all subject to supply disruptions, climate variability, and geopolitical shocks. The 2022–2023 sunflower oil supply disruption caused by the Russia-Ukraine conflict is a recent example of how rapidly input cost structures can shift for chip manufacturers with global supply chains.

Sustainability and Plastic Packaging Scrutiny: Multi-layer plastic film the standard packaging material for potato chips due to its superior oxygen and moisture barrier properties is among the most difficult packaging formats to recycle. Extended Producer Responsibility (EPR) regulations now in effect or forthcoming in the EU, UK, and parts of Asia are placing financial obligations on manufacturers for end-of-life packaging management. The transition to sustainable packaging alternatives involves significant capital expenditure and technical risk around maintaining chip freshness.

Private Label Margin Pressure

The growth of retailer private-label chip products exerts downward pressure on branded player margins in mature markets. As private-label quality improves and consumer price sensitivity rises, branded manufacturers face the dual challenge of justifying premium pricing while maintaining distribution relationships with retailers who directly compete with their products.

More Insights On

Upto 15% Off

USD

$2999 $2699

$4399 $3959

$5599 $4759

$6659 $5660

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 41.24 Billion.

The market is assessed to grow at a CAGR of 4.20% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 62.23 Billion by 2035.

The major drivers include Increasing demand for healthy snack options and innovation in flavours of potato chips.

The key trends include technological advancement in processing equipment and the rising popularity of vegan or plant-based snacks.

By product type, the market is divided into baked and fried.

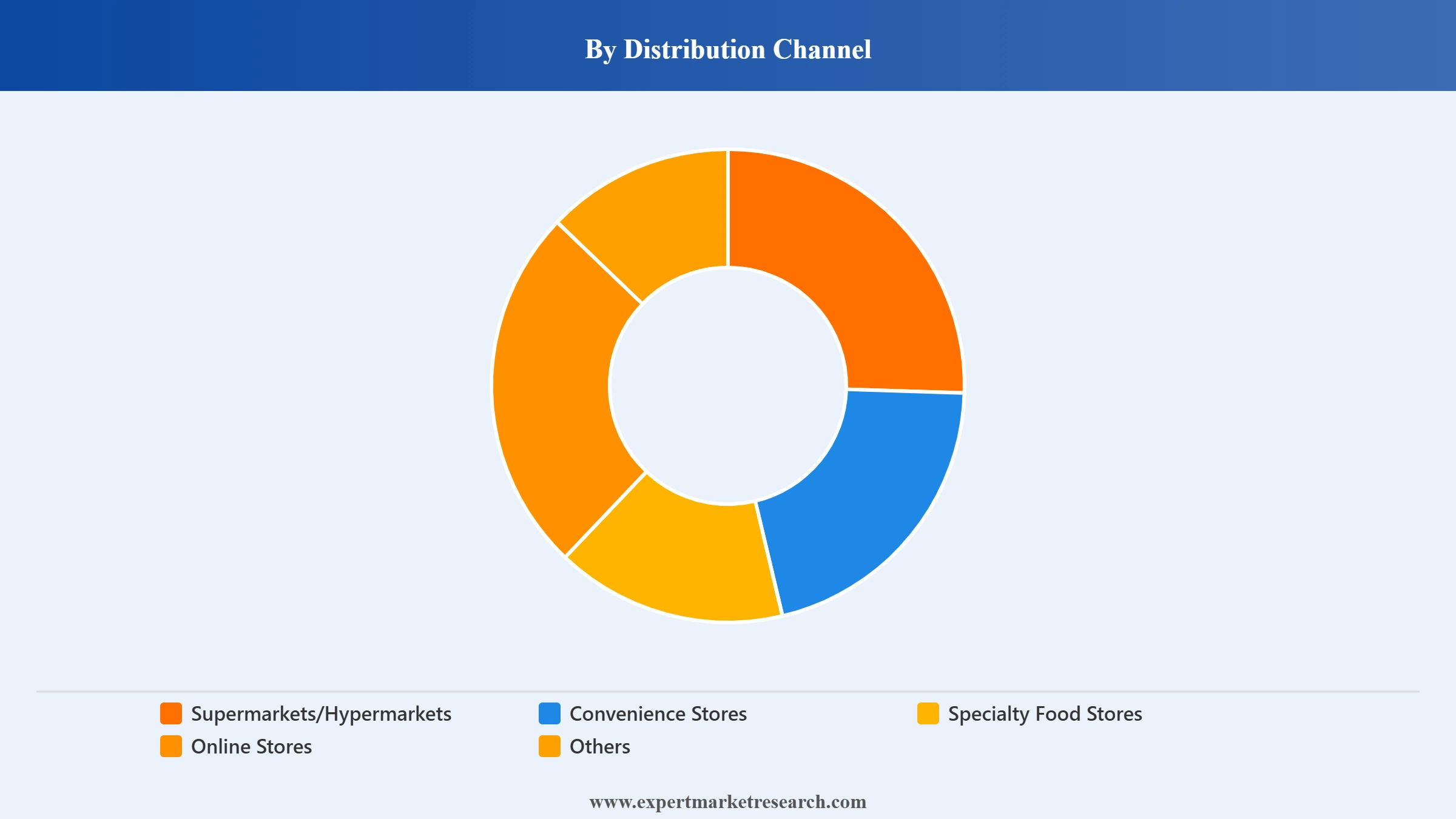

Based on distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, speciality food stores, online stores, and others.

The competitive landscape consists of Kellogg Company, PepsiCo, Inc., Utz Brands, Inc., The Lorenz Bahlsen Snack-World GmbH & Co KG, Campbell Soup Company, Burts Snacks Limited, Herr Foods Inc., and Calbee, Inc., among others.

The market is broken down into North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Flavour |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,999

USD 2,699

tax inclusive*

Single User License

One User

USD 4,399

USD 3,959

tax inclusive*

Five User License

Five User

USD 5,599

USD 4,759

tax inclusive*

Corporate License

Unlimited Users

USD 6,659

USD 5,660

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.