Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The semiconductor market size reached a value of approximately USD 673.18 Billion in 2025. The market is projected to grow at a CAGR of 7.70% between 2026 and 2035, reaching a value of around USD 1413.48 Billion by 2035. The long-term outlook highlights the critical role of advanced chips in data centers, cloud computing, smartphones, renewable energy systems, and intelligent infrastructure. As industries continue to prioritize performance, efficiency, and reliability, semiconductor manufacturers are expected to expand capacity and capabilities to meet rising global demand.

Base Year

Historical Period

Forecast Period

The 2022 U.S. Semiconductor Industry Association report states that U.S. semiconductor exports reached $62 billion in 2021.

The Indian semiconductor market is projected to grow to about $110 billion by 2030, according to the International Trade Administration.

In 2020 China imported $378 billion worth of semiconductors and assembled 35% of global electronic devices, per the Semiconductor Industry Association.

Compound Annual Growth Rate

7.7%

Value in USD Billion

2026-2035

*this image is indicative*

| Global Semiconductor Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 673.18 |

| Market Size 2035 | USD Billion | 1413.48 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 7.70% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 8.9% |

| CAGR 2026-2035 - Market by Country | India | 10.2% |

| CAGR 2026-2035 - Market by Country | China | 8.5% |

| CAGR 2026-2035 - Market by Component | Memory Devices | 8.7% |

| CAGR 2026-2035 - Market by Application | Automotive | 8.8% |

| Market Share by Country 2025 | France | 3.5% |

A semiconductor is a material with conductivity between conductors and insulators, crucial for modern electronic devices. There are intrinsic and extrinsic semiconductors, each with different electrical charge-carrying capabilities. They are used in various industries, including computing, telecommunications, aerospace, medical technology, automotive, defence, and robotics, integral to microprocessors, transistors, diodes, and integrated circuits (ICs).

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The growing demand for advanced smartphones, tablets, laptops, and other electronics drives the semiconductor market. Increased data generation boosts the need for robust data centres, while advancements in electric vehicles (EVs) and autonomous driving also elevate semiconductor requirements.

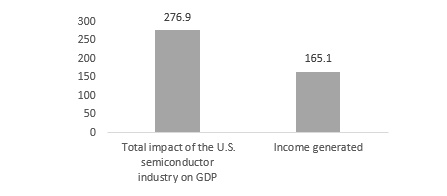

U.S. SEMICONDUCTOR INDUSTRY ON GDP AND INCOME, 2021, IN USD BILLION

According to the 2022 State of the U.S. Semiconductor Industry Association report, U.S. semiconductor exports hit $62 billion in 2021, making them the fourth largest U.S. export. The industry also supported 1.84 million jobs in the U.S. in 2021, significantly boosting the country's semiconductor market growth.

Technological advancements, growing consumer electronics demand, environmental concerns and defence and aerospace are the major trends impacting the semiconductor market trends.

Semiconductor market growth is driven by rising 5G, AI, and ML adoption, crucial for advanced technology manufacturing, enabling faster data processing and low-latency communication.

Semiconductors play a vital role in various digital consumer goods such as smartphones, TVs, and washing machines. They're also utilised in PCs to regulate temperature and vibration, improving device durability and performance.

Rising environmental consciousness is boosting the adoption of hybrid and electric vehicles (EVs), driving demand for semiconductor-dependent products like motor controls, power electronics, battery management systems, communication devices, and infotainment systems.

Semiconductor market growth is fueled by increased production for navigation, communication, and radar systems. Additionally, their expanded use in railway systems, signal processing, control systems, and communication equipment contributes to market expansion.

The semiconductor market undergoes notable changes propelled by diverse technological and market dynamics. The surge in artificial intelligence and machine learning fuels the demand for specialised AI chips, particularly for edge devices such as smartphones and IoT gadgets. 5G technology deployment remains pivotal, while early-stage 6G research influences semiconductor progress.

The increasing use of IoT devices calls for energy-efficient semiconductors with strong security measures. Advancements like smaller process nodes and 3D packaging enhance chip efficiency and durability. Industry practices are shaped by supply chain diversification and environmental considerations, while quantum computing and ongoing mergers and acquisitions drive innovation, especially in meeting consumer electronics demands.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

“Semiconductor Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Component

Market Breakup by Application

Market Breakup by Region

| CAGR 2026-2035 - Market by | Country |

| India | 10.2% |

| China | 8.5% |

| UK | 7.0% |

| USA | 6.9% |

| Italy | 5.4% |

| Canada | XX% |

| Germany | XX% |

| France | XX% |

| Japan | 5.3% |

| Australia | XX% |

| Saudi Arabia | XX% |

| Brazil | XX% |

| Mexico | XX% |

Memory devices, which are crucial for storing data, are vital for the functioning of computers, smartphones, and various other electronic gadgets, thereby driving the growth of the semiconductor market.

Memory devices, offering significant storage capacity and rapid data access (such as DRAM and SRAM), are versatile and used across a range of applications. They include both volatile RAM and non-volatile flash memory. Technological advancements have improved their density and efficiency, fuelling market growth in response to the demands of IoT, big data, AI, and machine learning.

Logic devices, including CPUs and GPUs, perform complex tasks and enable efficient parallel processing. Adhering to Moore's Law, these devices scale to improve performance and energy efficiency. They are adaptable to various applications, from consumer electronics to specialised machinery, and are driven by advancements in AI, machine learning, and other technologies.

Analogue ICs are adept at processing real-world signals, making them essential for audio equipment, sensors, and communication systems. They manage power effectively for device efficiency and act as key interfaces between digital systems and the analogue world, ensuring precise data conversion.

Optical Storage Devices (OSDs) provide substantial storage capacities, perfect for media storage, backups, and data centres. They offer reliable, long-term data storage and are often a more cost-effective solution for large-scale storage, balancing performance, and affordability.

Micro components, such as microcontrollers and microprocessors, facilitate the development of compact, lightweight, and portable devices. They deliver high processing power and efficiency for complex tasks and are versatile, driving innovation in IoT devices, automotive systems, robotics, and consumer electronics.

Semiconductors facilitate the creation of advanced medical devices like MRI machines, CT scanners, and ultrasound equipment. By enhancing diagnostic accuracy, these technologies contribute to the semiconductor market growth.

Semiconductors drive wearable health monitors, providing real-time health data and facilitating proactive care. They enable remote monitoring, personalized medicine, efficient EHR management, and big data analytics. Additionally, advanced imaging, implantable devices, operational efficiency, and affordable medical devices enhance healthcare outcomes and accessibility.

In aerospace and defence, semiconductors are essential for high-speed, real-time data processing, crucial for advanced avionics and mission-critical tasks. They are durable in harsh environments, have long lifespans, and support compact designs. They improve radar, and sensors, secure communications, reduce costs, and enhance energy efficiency.

Semiconductors facilitate advanced safety features such as collision avoidance and automated braking, play a crucial role in enhancing battery management and power conversion for electric and hybrid vehicles, and drive in-car entertainment and connectivity systems, elevating the overall user experience.

Semiconductors are indispensable for controlling industrial robots and automated machinery, improving productivity and precision. They enable the monitoring of equipment health through sensors and IoT devices, reduce downtime and maintenance costs via predictive analytics, and enhance energy efficiency in industrial power systems, promoting sustainability.

Semiconductors power high-performance processors and memory systems for large-scale data processing, while advancements in technology improve data centre energy efficiency, reducing operational costs and environmental impact. Additionally, they enable scalable storage and networking solutions to meet growing data demands.

Semiconductors are vital for 5G infrastructure, offering faster data speeds, lower latency, and improved connectivity. They support the development of advanced networking equipment, enhancing reliability and efficiency, and facilitate the widespread deployment of IoT, ensuring seamless communication across multiple devices.

Semiconductors drive the performance of smartphones, tablets, and wearables, enhancing their functionality and user experience. They are essential for smart home devices, improving convenience and security, and contribute to superior gaming consoles, smart TVs, and audio systems, enriching entertainment experiences.

According to the semiconductor market analysis, the Asia Pacific region commands a significant market share, with countries like China, South Korea, and Taiwan emerging as major semiconductor manufacturers globally. Moreover, Japan and India are witnessing substantial investments in semiconductor manufacturing due to concerns about semiconductor shortages and geopolitical tensions between China and the United States.

In India, the Ministry of Electronics, and Information Technology (MeitY) aims to boost the country's self-reliance and global stature in Electronics System Design and Manufacturing (ESDM) through the Semicon India Programme. Launched in 2022 with an approved budget of ₹76,000 crore, this initiative is anticipated to bolster semiconductor and display manufacturing infrastructure, thereby stimulating growth in the Indian printed circuit board (PCB) market.

China holds the distinction of being the world's largest manufacturing hub, responsible for producing 36% of the world's electronics, including smartphones, computers, cloud servers, and telecom infrastructure. The Made in China 2025 Plan seeks to achieve 70% self-sufficiency in semiconductors by 2025, as articulated by the Semiconductor Industry Association of China.

Meanwhile, North America is poised for robust growth owing to heightened research and development activities by major players, technological advancements, and the surging demand for consumer electronics. The region boasts a resilient manufacturing sector, encompassing automotive, aerospace, and industrial equipment industries, all of which are increasingly reliant on semiconductors for automation, control systems, and IoT connectivity.

The demand for semiconductors in data centres has surged with the proliferation of cloud computing and the need to process vast amounts of data. North America leads in cloud services, hosting large data centres that require high-performance computing and storage solutions.

In April 2024, the Canadian Prime Minister unveiled a new federal investment of $59.9 million to support projects by IBM Canada and the MiQro Innovation Collaborative Centre (C2MI), aimed at enhancing semiconductor production and fostering economic growth.

In the competitive landscape, these companies are key players in semiconductor manufacturing focused on designing and manufacturing semiconductors and associated products. Their product range spans various applications including automotive, industrial, consumer electronics, and communication infrastructure, offering diverse semiconductor solutions tailored to these sectors.

Intel Corporation (NASDAQ: INTC) founded in 1968 and headquartered in California, is an esteemed American semiconductor and technology company renowned for its production of semiconductor chips and microprocessors that are widely utilized in personal computers globally.

Samsung Electronics Co., Ltd. (KRX: 005930) was established in 1969 and situated in Suwon-si, South Korea, is a prominent South Korean electronics conglomerate engaged in the manufacturing of various products, including consumer electronics, home appliances, semiconductors, and medical equipment.

Texas Instruments was established in 1930 and based in the United States, specializes in the design, manufacturing, testing, and sale of analogue and embedded semiconductors crucial for the development of electronic systems.

Nvidia Corporation; founded in 1993 and headquartered in California, is a pioneer in GPU-accelerated computing, with a focus on creating products and platforms for emerging markets such as gaming, professional visualization, data centres, and the automotive industry.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other semiconductor market key players are Micron Technology, Inc. (NASDAQ: MU), Qualcomm Technologies, Inc. (NASDAQ: QCOM), SK Hynix Inc. (KRX: 000660), Taiwan Semiconductor Manufacturing Company Limited, Broadcom Inc., MediaTek Inc., and NXP Semiconductors N.V. among others.

Europe's automotive and consumer electronics sectors are witnessing robust growth, presenting lucrative opportunities for the semiconductor market. European semiconductor sales surpassed €51.2 billion in 2022, with automotive chips emerging as the largest end-use segment, followed by industrial applications. Europe and China emerged as the largest markets for automotive semiconductors in 2022, accounting for 25.4% and 26.2% of the global automotive market, respectively.

North America Analog Semiconductor Market

Asia Pacific Analog Semiconductor Market

United Kingdom Semiconductor Market

Europe Analog Semiconductor Market

South Korea Semiconductor Market

Upto 15% Off

USD

$4839 $4355

$2999 $2699

$5999 $5099

$7259 $6170

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

Get in touch with us for a customized solution tailored to your unique requirements and save upto 35%!

The market was valued at USD 673.18 Billion in 2025.

The market is projected to grow at a CAGR of 7.70% between 2026 and 2035.

The revenue generated from the semiconductor market is expected to reach USD 1413.48 Billion in 2035.

Technological advancements, growing consumer electronics demand, environmental concerns and defence and aerospace are the major trends impacting the semiconductor market trends.

The semiconductor market is categorised according to the components, which include memory devices, logic devices, analogue IC, OSD and microcomponents.

The key players are Intel Corporation (NASDAQ: INTC), Samsung Electronics Co., Ltd., Texas Instruments, Nvidia Corporation, Micron Technology, Inc. (NASDAQ: MU), Qualcomm Technologies, Inc. (NASDAQ: QCOM), SK Hynix Inc. (KRX: 000660), Taiwan Semiconductor Manufacturing Company Limited, Broadcom Inc., MediaTek Inc., and NXP Semiconductors N.V. among others.

Based on the application, the market is divided into automotive, industrial, data centre, telecommunication, consumer electronics, aerospace and defence, healthcare, and others.

The market is broken down into North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa.

The Asia-Pacific region is the fastest-growing region in the global semiconductor market, driven by technological advancements, and the surging demand for consumer electronics.

The top five companies in the semiconductor market are Intel Corporation (NASDAQ: INTC), Samsung Electronics Co., Ltd., Texas Instruments, Nvidia Corporation, and Micron Technology, Inc. (NASDAQ: MU).

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Component |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Single User License

One User

USD 4,839

USD 4,355

tax inclusive*

Datasheet

One User

USD 2,999

USD 2,699

tax inclusive*

Five User License

Five User

USD 5,999

USD 5,099

tax inclusive*

Corporate License

Unlimited Users

USD 7,259

USD 6,170

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.

Share