Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

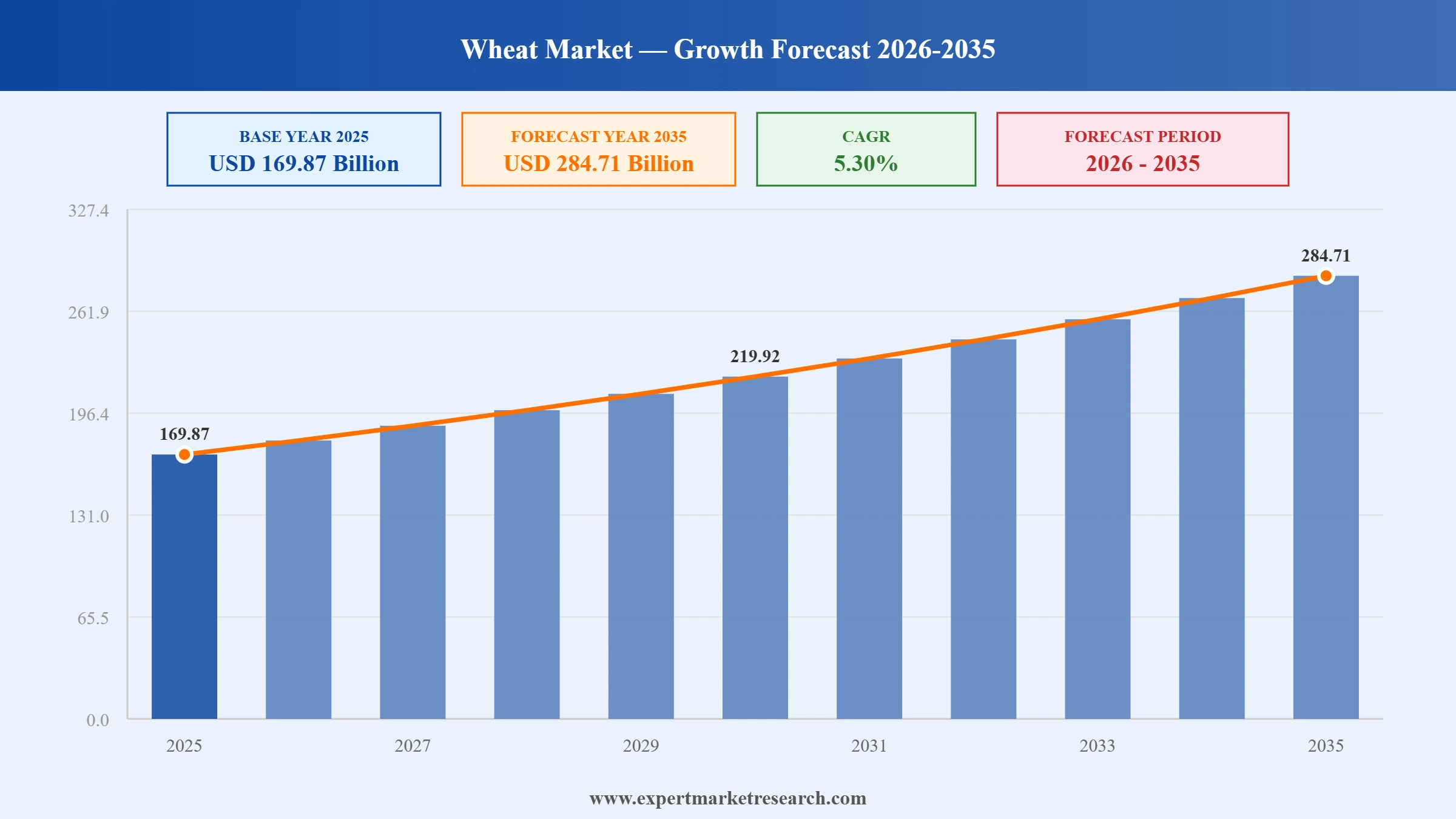

The global wheat market attained a value of USD 169.87 Billion in 2025 and is projected to expand at a CAGR of 5.30% through 2035. The market is further expected to achieve USD 284.71 Billion by 2035. Increasing investments in regenerative wheat farming, digital grain traceability, and premium flour applications ensure that the commercial procurement process remains robust in terms of supply resilience, export performance, and profitability.

The increasing trend in implementing innovative wheat breeding programs is making it easier for farmers to be assured of disease-resistant and reliable yields irrespective of changes in weather conditions. On the other hand, the growing demand for bakery products and high-protein foods is motivating processors to adopt special milling techniques and flour mixes, boosting the wheat market growth. These developments are fostering more stable agreements among growers, processors, and food manufacturers from around the world.

Innovation in the global market is shifting towards value-added processing and robust supply chain operations, not only grain exportations. In January 2024, King Arthur launched Regeneratively-Grown Climate Blend Flour, promoting sustainable wheat cultivation, improved soil health, and resilient farming practices. The move comes at a time when climate-smart wheat is demanded by bakery and food service industries. According to the wheat market analysis, wheat production in the world exceeded 800 million metric tons in the 2024/25 season, despite disruptions caused by climate factors in several exporting countries.

The global wheat market is further experiencing structural changes as companies involved in millings, exports, and manufacturing focus on resilient supply chain operations, wheat quality, and digitization of procurement process. In February 2026, the Indian government set a 303 LMT wheat procurement target for RMS 2026-27, strengthening food security and farmer support. Investments in precise farming, AI-powered grading technology, and storage systems are undertaken to minimize post-harvest losses and provide constant level of protein necessary for industrial users. Prominent producers are also developing a range of specialty wheats used in artisan bakery, high-protein food products, noodles, and vegan products. Such innovations allow food companies to differentiate their products.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Global Wheat Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 169.87 |

| Market Size 2035 | USD Billion | 284.71 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 5.30% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 5.8% |

| CAGR 2026-2035 - Market by Country | India | 6.6% |

| CAGR 2026-2035 - Market by Country | Mexico | 5.8% |

| CAGR 2026-2035 - Market by Type | Flour | 5.6% |

| CAGR 2026-2035 - Market by Application | Biofuel | 5.9% |

| Market Share by Country 2025 | USA | 14.2% |

Brazilian scientists developed the world’s first tropical wheat for biscuits that offer high yields and good heat and disease resistance capabilities. Hence, seed firms can breed new wheat varieties that are able to cope with the changes in weather and climate in new wheat production areas.

Syngenta took steps toward the commercial development of X-Terra hybrid wheat by incorporating hybrid breeding techniques and higher yield and better resource use efficiency. Companies can utilize the hybrid breeding technologies of wheat, leveraging such trends in the wheat market.

Corteva Agriscience launched Pixxaro broadleaf herbicide for wheat with an advantage of good weed management, better crop protection, and higher productivity for farmers. Crop protection companies can therefore offer a wider range of precision herbicides that boost yields and sustainably grow wheat, reshaping the wheat market dynamics.

Indian Institute of Wheat and Barley Research released 13 new wheat varieties with increased productivity, disease tolerance, and climate resilience for farmers. Breeders can therefore work together with research organizations to commercialize improved wheat varieties suitable for different agroclimatic zones.

One of the most prominent trends in the global wheat market is regenerative agriculture as food processors look for low-carbon raw materials for their brands. Prominent milling companies are collaborating with growers for initiatives such as cover cropping, low-till farming, and precision nutrition while maintaining the ability to provide traceable wheat. For instance, in June 2026, Nestlé partnered with Wildfarmed to produce 1.5 billion KitKat bars using regeneratively farmed British wheat annually. At the same time, the United States Department of Agriculture keeps providing its support to climate-smart commodity projects which promote regenerative farming via financial and advisory assistance.

The development of digital technologies helps increase productivity and reduce costs of inputs in wheat farming in leading wheat-producing countries. With the help of AI-based crop monitoring, satellites, drones, and precision application systems, farmers can maximize the effectiveness of fertilizers application, irrigation, and detect diseases at an early stage thus preventing losses in yields. This process is supported by governments through various digital agriculture and smart farming initiatives, accelerating the wheat market value. In June 2026, Sharjah achieved a desert wheat breakthrough, demonstrating climate-resilient cultivation through AI-driven farming, high-protein yields, and water-efficient agriculture.

Breeding of climate-resistant varieties of wheat is becoming an important area for development with adverse weather conditions affecting agricultural output. Significant funds are being invested in breeding programs that make improvements in drought resistance, disease tolerance, and heat resistance without impacting grain quality. The International Maize and Wheat Improvement Center is continuing its collaboration with national agricultural departments to breed new genetics of wheat that are resistant to climate change. In addition, India and Australia are intensifying their efforts in wheat breeding to increase domestic production, boosting the wheat market growth. Similarly, in July 2025, Ghana launched a climate-resilient wheat initiative with India's Arima Farms, promoting local production, food security, and sustainable agriculture.

Modernization of infrastructure is emerging as one of the most promising growth factors as authorities and private sector companies are trying to limit post-harvest waste and increase the efficiency of export activities. Construction of modern grain silos, grain processing and distribution facilities with automation capabilities, and grain management systems is providing more grain storage and retaining its quality during transportation. India is developing its grain storage capacity by increasing scientific grain storage in the Food Corporation of India and other public and private infrastructure facilities, propelling growth in the wheat market. In June 2026, Haryana announced plans to add 20 lakh metric tons of grain storage capacity, reducing post-harvest losses and strengthening wheat supply chains in India.

Growing demand for high-quality and application-oriented wheat products is prompting food processors to venture out of their traditional role of making flour. High protein wheat, organic wheat, and specialized flour mixes are becoming increasingly commercially viable in baking, noodles, snacks, and plant-based foods industries. Specialized equipment and systems for traceability are being developed to help satisfy stringent requirements of quality set forth by international food brands, boosting demand in the wheat market. Value addition in agriculture through food processing and export promotion policies adopted by governments is helping processors earn profits while making strong business ties with commercial food manufacturers. Demonstrating such shifts, in December 2025, Corteva advanced hybrid wheat development for India, targeting higher yields, improved land efficiency, and expanded biofuel crop cultivation.

The Expert Market Research’s report titled “Global Wheat Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

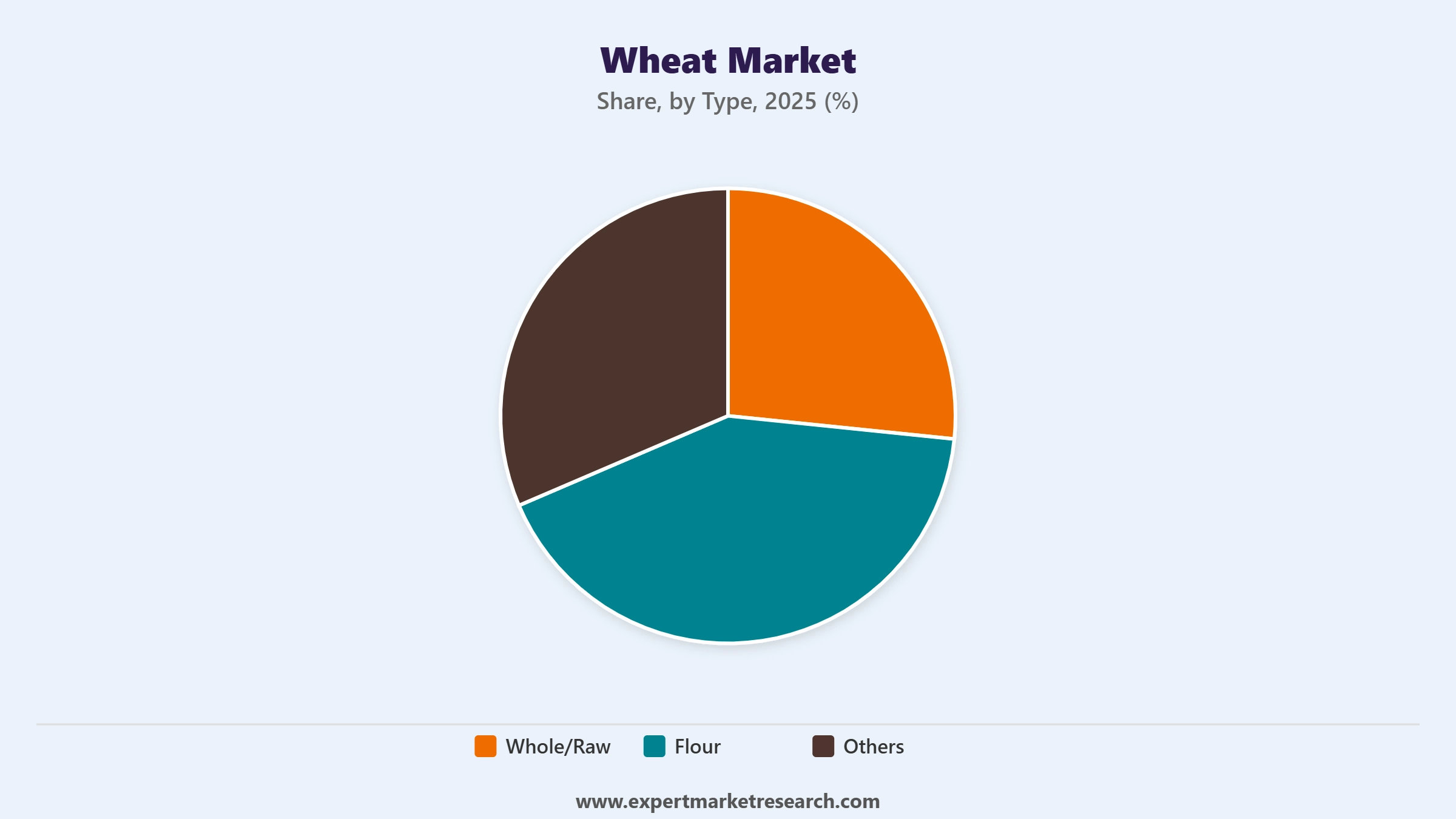

The market for wheat, based on type, is divided into:

Key Insight: As per the wheat market report, whole or raw wheat continues to be the leading segment, as this allows for greater flexibility in procurement by processors, exporters and manufacturers. Flours, on the other hand, are growing at an increasing rate as food manufacturers are seeking ingredients for their use in bakery, snacks and convenience foods. Meanwhile, the others segment that includes wheat bran, semolina, wheat germ and various processed forms of wheat, is receiving more attention in terms of their utilization.

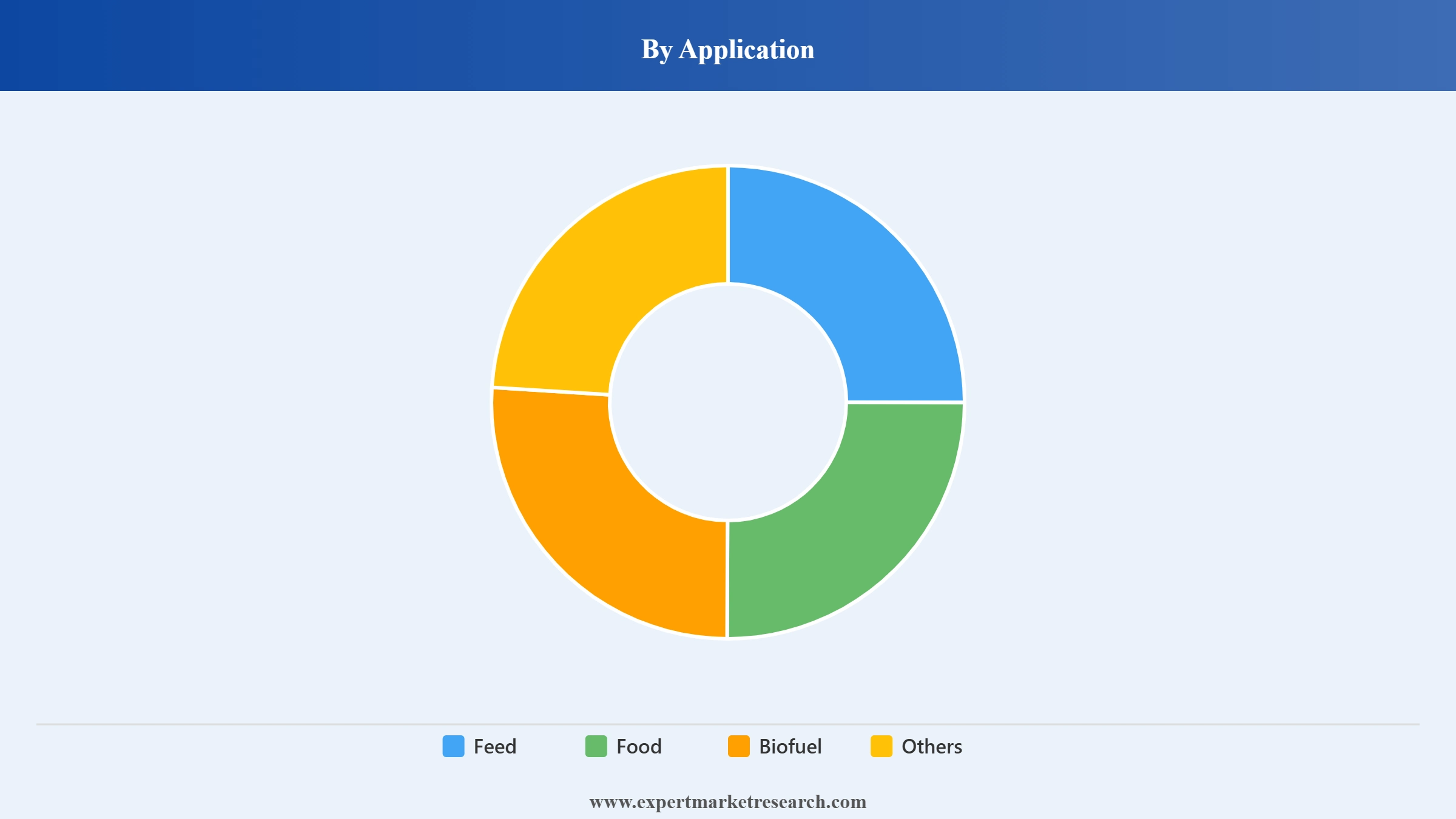

Based on application, the market is segmented into:

Key Insight: Application-based demand highlights the diverse uses of wheat in several industries. Food emerges to be the biggest application across the wheat market scope since it provides the raw material for key staple foods that are consumed around the world and is important for food processing methods. Wheat-based feed will continue being used by livestock farmers to provide nutritious grains for animals whenever the economy supports the use of wheat. Biofuel is gaining popularity owing to the renewable energy goals, encouraging the use of agricultural raw materials to make ethanol. Other applications include starch making, brewing, fermentation, and specialized ingredients manufacturing.

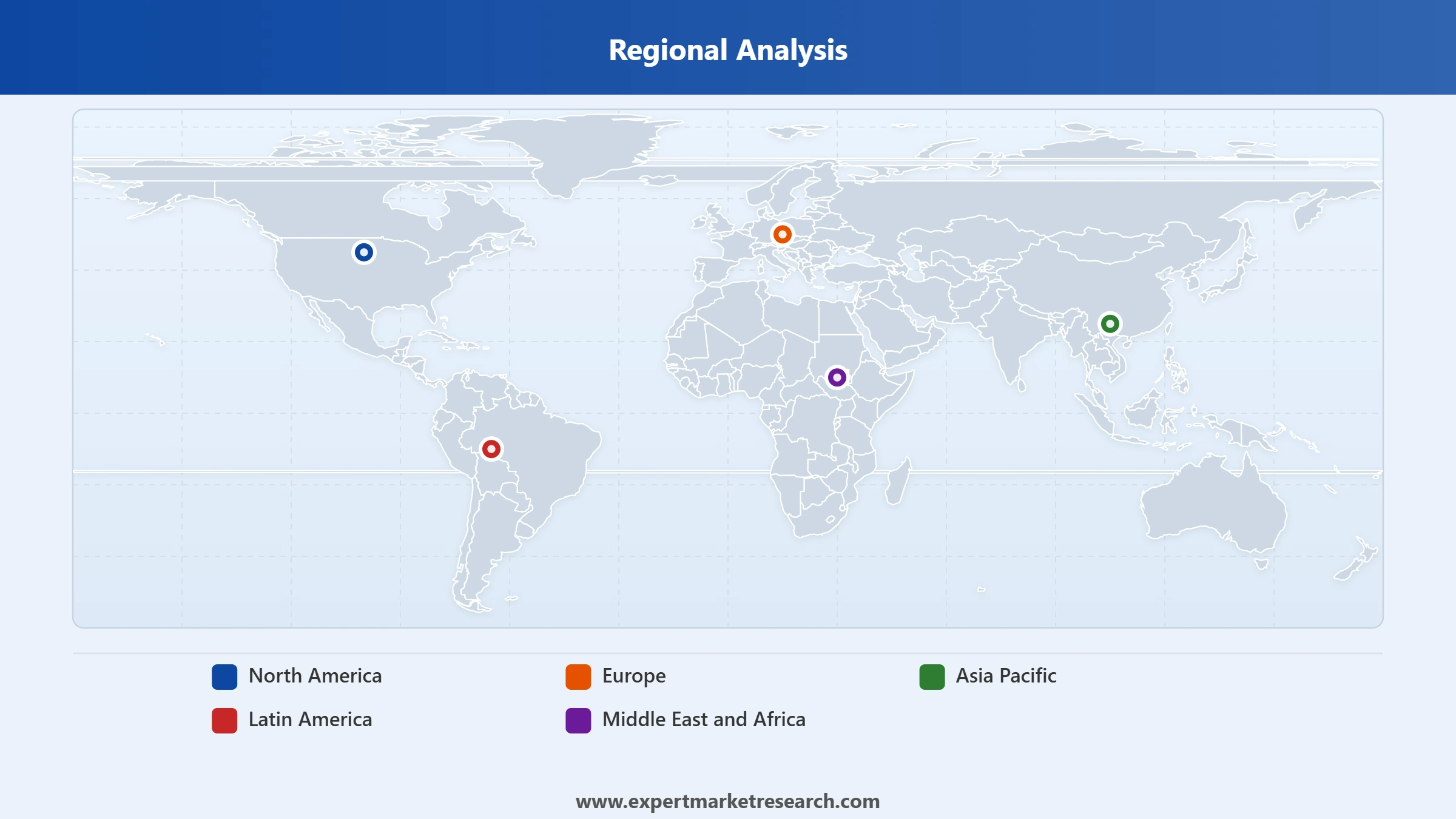

Market Breakup by Region:

Key Insight: Regional dynamics in the wheat market emphasize the existence of different strategies for development within the industry. The Asia Pacific region takes the lead due to its intensive cultivation of wheat, wheat consumption, and integrated food production facilities. Europe occupies a dominant position by producing superior quality wheat with the use of the latest milling technology and exporting facilities. North America gains strength with large-scale mechanization of farming and the best quality of wheat that allows effective exports. Latin America keeps growing because of its agricultural reforms and export orientation. In May 2024, Bioceres commercialized HB4 transgenic wheat in Argentina, introducing drought-tolerant varieties with improved yields and climate resilience.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By type, the whole/raw wheat segment dominates the market owing to expanding industrial grain procurement

The whole/raw wheat dominates the global wheat market as it is the main ingredient used by flour mills, grain traders, feed manufacturers, and food processors. The increasing preference among business users for direct grain purchases enables greater processing and quality options. Development of facilities related to grain storage, transportation, and traceability is also contributing significantly to the growth of the category. International trade of wheat and increased demand for milling wheat motivate farmers to produce more and manage their supply chains efficiently. In August 2025, The Humble Seed launched whole wheat protein crackers, combining super seeds with plant-based protein for healthier snacking options.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Flour is currently the fastest-growing type segment that is boosting demand in the wheat market as its use increases within industrial bakeries, packaged food manufacturers, noodle makers, and food service industry. Flour millers are developing specialized types of flour, with a higher protein content, clean label, and formulations for specific applications, to improve differentiation. Increasing demand for convenient food and premium bakery goods motivates investment in state-of-the-art milling equipment. Flour blending, which is tailored to the needs of food manufacturers for consistency and innovation, is becoming more popular. In June 2025, Jindal Rice launched fortified rice, basmati, and wheat flour, expanding nutritious staple offerings to strengthen India's food security.

By application, the food segment captures the largest market share driven by extensive global wheat consumption

The food segment stands out as the major application area since wheat plays an important part in the making of bread, pasta, noodles, biscuits, breakfast cereals, bakery products, processed foods, and others. The global food industry is investing in better quality formulations, fortified foods, and clean label ingredients in order to meet changing customer needs. Urbanization and need for convenience foods are contributing to an increase in commercial wheat demand. Consistent purchases from international food companies and increasing food processing sectors are also playing a crucial role in maintaining wheat's importance as a key agriculture crop for future industrial use. For instance, in July 2025, pladis Türkiye and Sabancı University developed biofortified wheat, launching nutrient-enriched biscuits with zinc- and selenium-fortified wheat flour.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Biofuel is becoming the fastest-growing segment across the wheat market scope due to renewable fuel feedstock diversification by governments and energy companies. Wheat is increasingly being used in the ethanol production process in which excess or poor-quality wheat can be converted to green transport fuel. Continuous investments in biorefineries and changing energy security policies are prompting commercial use of wheat beyond food applications. In January 2026, bp and Corteva launched Etlas biofuel platform, producing sustainable crop-based feedstocks for aviation fuels and renewable diesel.

Asia Pacific secures the dominant share of the market through extensive production and consumption networks

The Asia Pacific region leads the global wheat market owing to its huge production capabilities, high consumption levels, and rising processed food industry. Nations such as China, India, and Australia have considerable impact on supply, trade, and prices of global wheat through their large-scale production and export activities. Programs led by governments for improving varieties of seeds, irrigation systems, and agricultural mechanization are consistently making the region more productive. In April 2026, India approved an additional 2.5 million metric tons of wheat exports, strengthening global supply and supporting farmer incomes.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Latin America is the fastest growing wheat market that is driven by agricultural advancements, better farming techniques, and rising opportunities for exporting wheat to international markets. Nations in Latin America are making considerable investments in precision agriculture, logistics, and storage to make themselves competitive in international grain markets. An increase in the capability of the domestic food processing industry is also helping boost wheat production and motivating processors to procure regional supplies.

The competition in the global market continues to evolve from one related to grain trade into another that is more focused on the utilization of technologies, sustainable sources, and development of premium ingredients. Prominent wheat market players are working on regenerative wheat sourcing, artificial intelligence solutions for assessing grain quality, automation of milling process and digitalization of traceability for consistent quality of ingredients for food manufacturers. The development of direct partnerships with farmers for the purpose of sourcing of identity preserved wheat and specialty grain with high protein and better performance in baking applications is also becoming more popular among the companies.

Another important direction in which wheat companies are evolving is the reduction of emissions in their operations by means of energy efficient milling plants and logistics optimization. There are new opportunities emerging in specialty flours, clean label bakery ingredients, wheat protein concentrates, and export-oriented value-added products.

Nisshin Flour Milling Inc., founded in 1900 and located in Tokyo, Japan, is one of the major producers of flour globally. The firm specializes in developing high-quality wheat flour, functional food components, and specialized grains for bakeries, confectioneries, and processed foods. Its continuous efforts in the development of milling technology, quality management systems, and sustainable supplier relations make it possible to expand its global commercial customer base.

Siemer Milling Company was founded in 1882 in Illinois, United States, and is engaged in providing premium wheat flour to commercial bakeries, food producers, and industrial processing firms. The firm focuses on identity-preserved wheat supply, reliable performance of flour, and customized milling solutions. Due to the company’s ongoing investments in advanced milling technology and food safety programs, it provides application-specific food ingredients.

Founded in 1985, with its headquarters in Minnesota, United States, Miller Milling Company is involved in the production of various lines of flour products using wheat for use by bakeries, food service companies, and packaged food manufacturers. The company concentrates on efficient operations, quality grain testing, and reliable sourcing channels. Its mills located in strategic locations aid in ensuring continuous supply to its customers in the domestic as well as the export markets.

Founded in 2014, with its headquarters in Chattanooga, Tennessee, United States, Grain Craft has become one of the biggest independent flour milling companies in the nation. The company produces various types of specialty and conventional flour products for use by industrial bakeries, pizza makers, snack producers, and food service providers.

Other key players in the market include General Mills, ITC Limited, Ardent Mills, Farm Fresh Wheat, Sunnyland Mills, and Bay State Milling Company, among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock the latest insights with our wheat market trends 2026 report. Discover regional growth patterns, consumer preferences, and key industry players. Stay ahead of competition with trusted data and expert analysis. Download your free sample report today and drive informed decisions in the market.

Food Fortification and Nutrient Enrichment

Grain Storage and Post Harvest Infrastructure

Bakery Ingredients Formulation Innovation

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the wheat market reached a value of USD 169.87 Billion.

The market for wheat is expected to grow at a CAGR of 5.30% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach USD 284.71 Billion by 2035.

The major drivers of the market include the rising disposable incomes, increasing population, and rising demand for low-calorie sweeteners and gluten-free food.

Key trends aiding the market expansion include the increasing focus on sustainable farming methods and the development and adoption of genetically modified wheat varieties.

North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa are the significant markets for wheat.

The major types of the product include whole/raw and flour, among others.

The major applications include feed, food, and biofuel, among others.

Key players in the market are Nisshin Flour Milling INC., Siemer Milling Company, Miller Milling Company, Grain Craft, General Mills, ITC Limited, Ardent Mills, Farm Fresh Wheat, Sunnyland Mills, Bay State Milling Company, and Others.

The wheat market demand is being driven by the demand from the food sector, especially in developing nations like India and China.

Unpredictable weather patterns and extreme conditions, increased incidence of pests and diseases, and geopolitical tensions are the key challenges in the market.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| Report Features | Details |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Trade Data Analysis |

|

| Competitive Landscape |

|

| Competitive Landscape |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.