Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

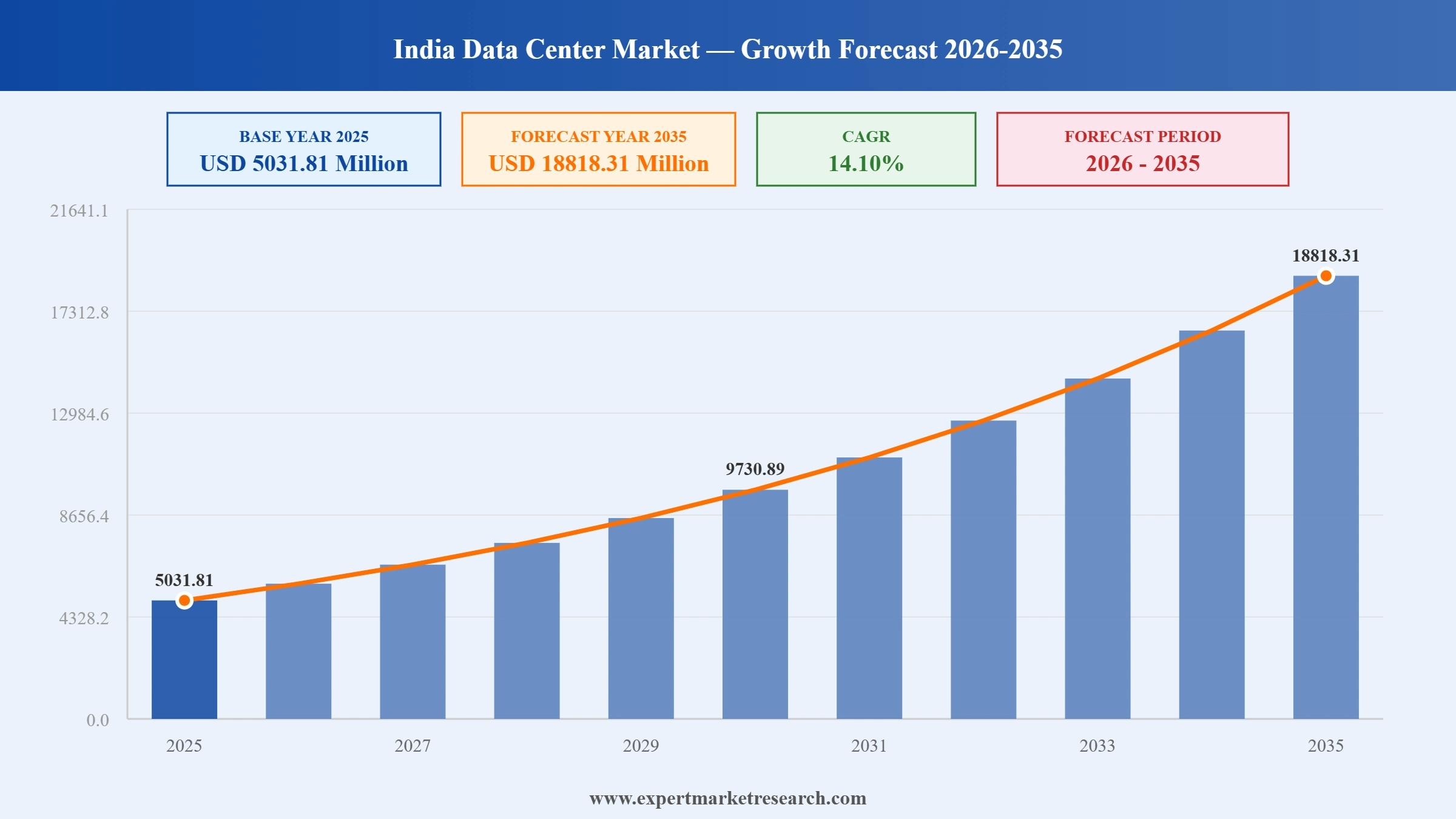

The India data center market reached a value of USD 5031.81 Million at 2025 and is projected to expand at a CAGR of around 14.10% during the forecast period of 2026-2035. With India's rapid digital transformation and exponential rise of AI and cloud workloads driving unprecedented infrastructure demand, government initiatives including Digital India and data localisation regulations mandating domestic data storage, aggressive expansion by both domestic operators and global hyperscalers, and the roll-out of 5G networks creating new low-latency compute requirements, the market is expected to reach USD 18818.31 Million by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

India's data center market is experiencing a fundamental transformation, evolving from a domestic infrastructure play to a global-scale investment destination. AI-driven workload requirements, hyperscaler campus commitments exceeding billions of dollars, and government infrastructure policies are combining to create one of the fastest-growing data center markets in Asia Pacific. West India leads by installed capacity while South India is emerging as an important alternative hub with government-backed incentive programmes.

In February 2026, Larsen and Toubro announced a partnership with NVIDIA to establish a sovereign AI factory in India under the IndiaAI Mission. The initiative includes expanding a 30 MW GPU compute cluster on a 300-acre campus in Chennai and launching a new 40 MW AI-ready data center in Mumbai, reinforcing India's ambition to build domestic AI computing infrastructure.

In August 2025, CtrlS Datacenters announced the launch of the first phase of its Kolkata data center campus, featuring a liquid cooling system to manage thermal loads from high-density AI and cloud workloads. The facility expands CtrlS's national footprint beyond its established Mumbai, Hyderabad, and Chennai campuses, broadening the India data center market's geographic capacity distribution.

By July 2025, NTT Global Data Centers reported 292 MW of live IT load capacity across its India facilities, with plans to expand to 400 MW within 18 to 24 months through new campuses in Noida, Hyderabad, and Bengaluru. NTT's USD 1.2 billion AI cluster investment in Hyderabad reflects the scale of global operator commitments to India's data center market.

In April 2025, CtrlS Datacenters broke ground on a new 12 MW AI-ready data center in Bhopal, Madhya Pradesh, within the Badwai IT Park. Built under Madhya Pradesh's Global Capacity Centers Policy 2025 with an investment of INR 500 crore, the facility is part of CtrlS's broader USD 2 billion green campus development programme across India.

West India, anchored by Mumbai's submarine cable landings and Maharashtra's business-friendly infrastructure policies, accounts for approximately 52% of India's total data center installed capacity. AdaniConnex, Yotta, and STT GDC India have concentrated flagship campuses in Navi Mumbai, positioning the region as the dominant hub of the India data center market.

AI workload requirements are driving a fundamental redesign of India's data center market infrastructure. Operators are adopting liquid cooling, high-density GPU racks, and advanced power distribution to support AI training and inference demands. CtrlS facilities in Chandanvelly handle rack densities up to 135 kW, reflecting the scale of AI-driven architectural changes now reshaping the sector.

India's data localisation requirements mandate that certain categories of sensitive data be processed and stored within national borders, compelling both domestic enterprises and multinational corporations to build or lease India-based data center capacity. This regulatory driver is a structural demand accelerant across BFSI, healthcare, and government verticals in the India data center market.

Hyderabad and Chennai are emerging as significant India data center market hubs, offering disaster-resilient geographies, competitive land pricing, and state government incentive programmes designed to attract hyperscale operators. As Mumbai land constraints and power costs increase, South India's infrastructure investment pipeline is accelerating, with Equinix and NTT expanding Chennai presence.

India's data center operators are accelerating renewable energy adoption in response to sustainability commitments and rising power consumption. CtrlS is constructing a 125 MWp solar farm to power upcoming campuses, while the 2025 CtrlS and NTPC MoU for a 2 GW renewable project demonstrates the strategic scale of clean energy procurement reshaping India data center market operations.

The report by Expert Market Research, titled "India Data Center Market Report and Forecast 2026-2035", offers a detailed analysis of the market based on the following segments:

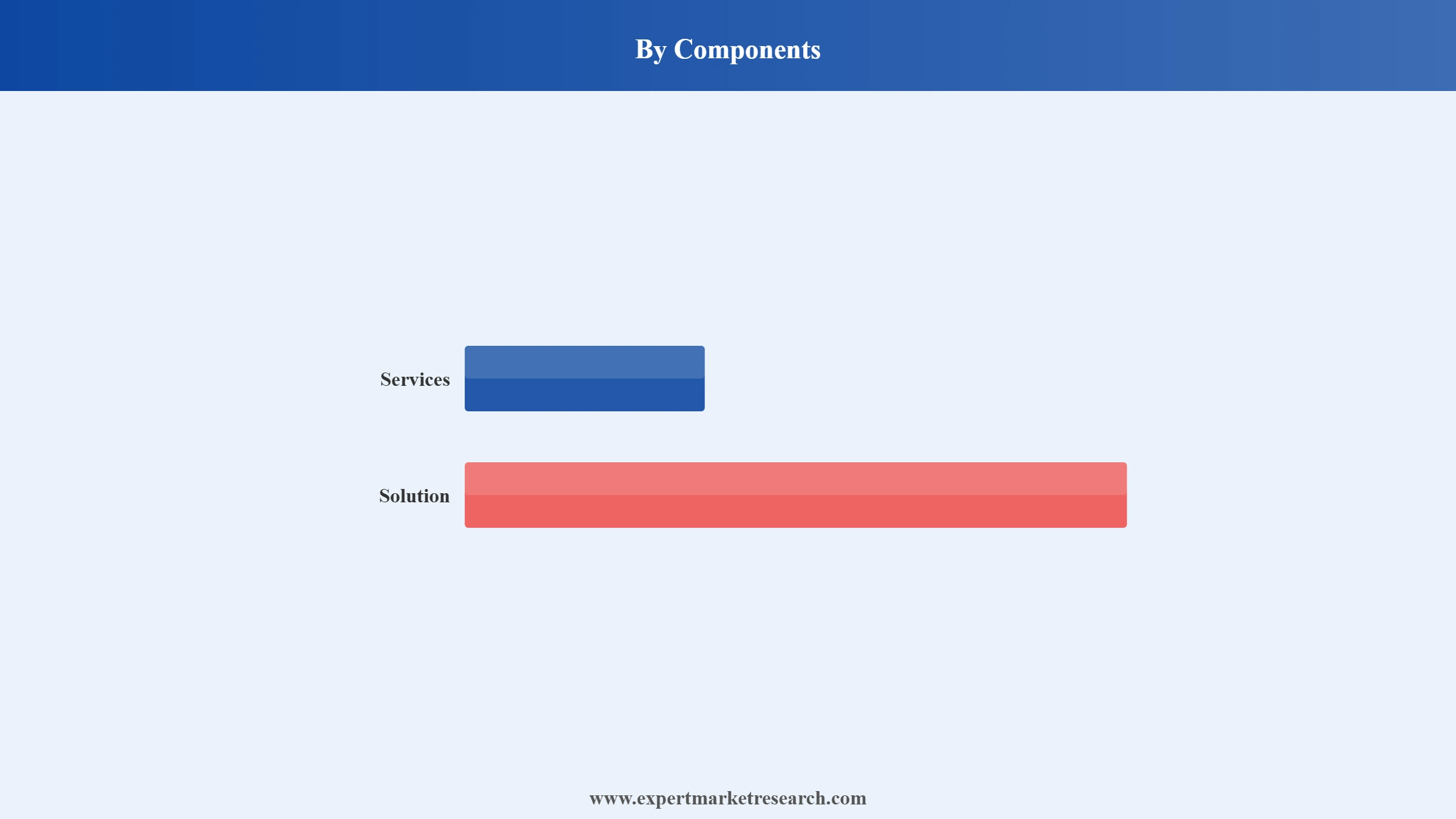

Market Breakup by Components

Key Insight: Solutions encompass hardware, software, and infrastructure installations and represent the largest component by capital expenditure, driven by server, storage, and networking deployments for AI and cloud workloads. The services segment, covering colocation, managed hosting, cloud, and professional services, is the fastest-growing component as enterprises shift from owning infrastructure to leasing scalable managed capacity. Both components are experiencing accelerated investment as India's data center capacity targets surpass 2,000 MW by 2027.

Market Breakup by Infrastructure

Key Insight: IT infrastructure is the dominant and fastest-growing category, encompassing servers, storage, networking, and GPU clusters that form the operational core of every data center. Electrical infrastructure, including UPS systems and generators, is critical for uptime compliance. Mechanical infrastructure investment is surging as liquid cooling solutions are adopted for AI-dense rack deployments. General construction spending is accelerating as operators develop new greenfield campuses across Mumbai, Hyderabad, Chennai, and Bhopal.

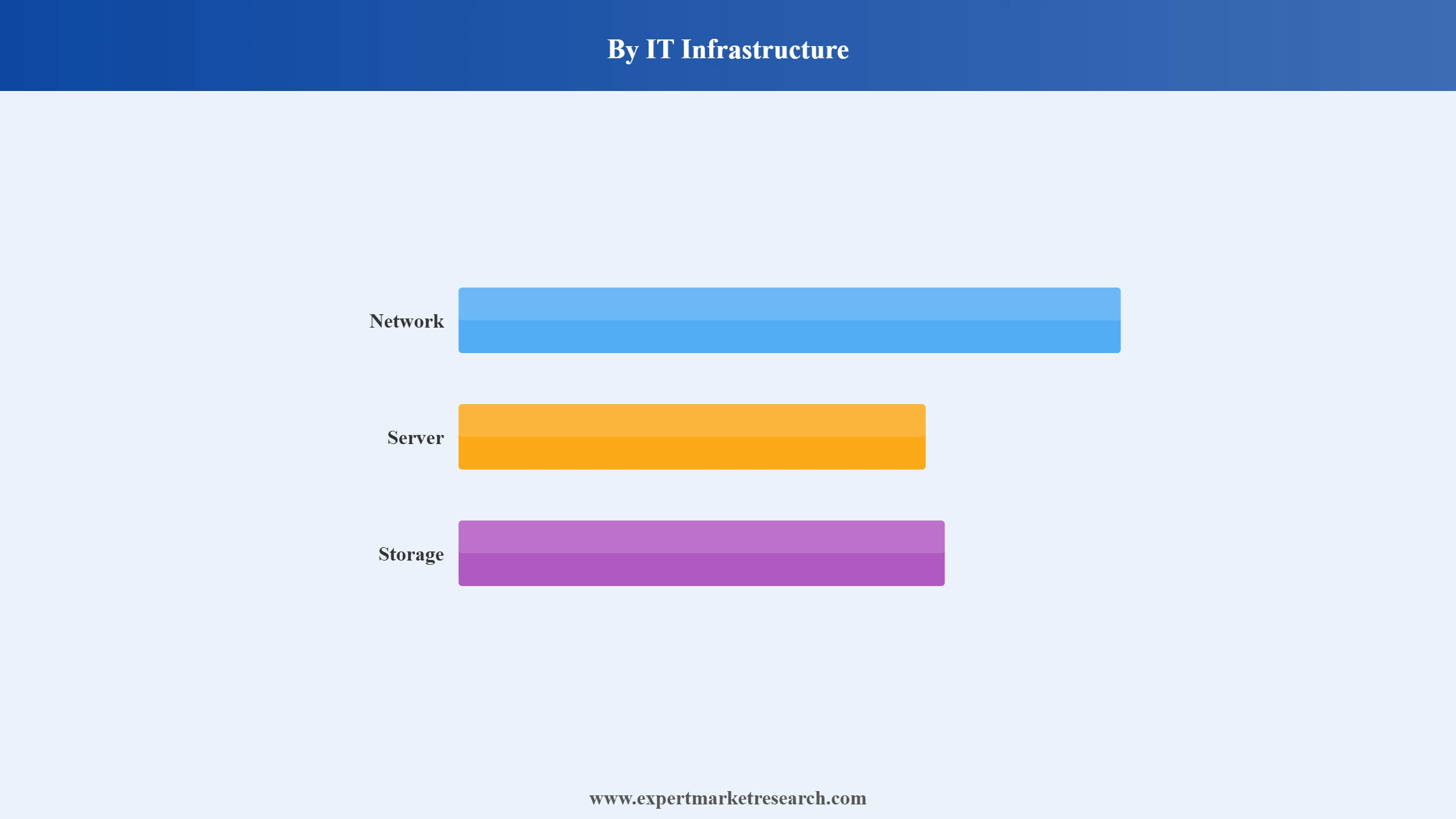

Market Breakup by IT Infrastructure

Key Insight: Servers represent the largest IT infrastructure sub-segment, particularly as AI training and inference workloads require GPU-intensive compute platforms with rack densities up to 135-300 kW per rack. Storage systems are growing rapidly with the surge in unstructured data generated by cloud, AI, and digital services. Networking equipment is expanding to support high-bandwidth interconnects between GPU clusters and storage nodes, with operators investing in next-generation spine-leaf architectures across India's hyperscale campuses.

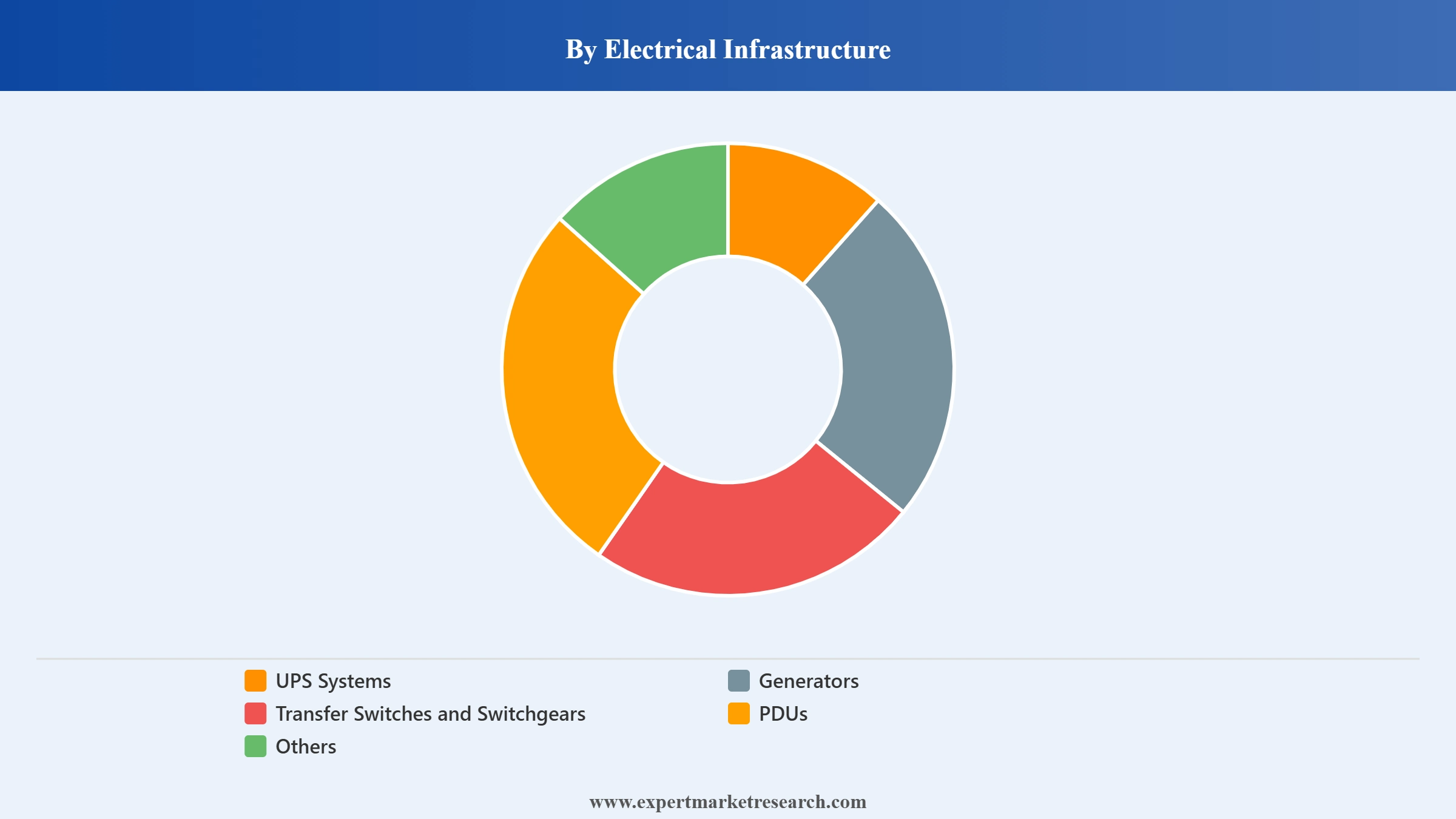

Market Breakup by Electrical Infrastructure

Key Insight: UPS systems are the largest electrical sub-segment, providing the critical bridge power that protects live workloads during grid transitions. Generators serve as the primary backup power source and are mandatory for Tier III and Tier IV certification. Transfer switches and switchgears manage the seamless transition between power sources, while PDUs distribute conditioned power at the rack level. The CtrlS and NTPC 2 GW renewable energy MoU signed in 2025 reflects how electrical infrastructure strategy is shifting toward integrated green power systems in India.

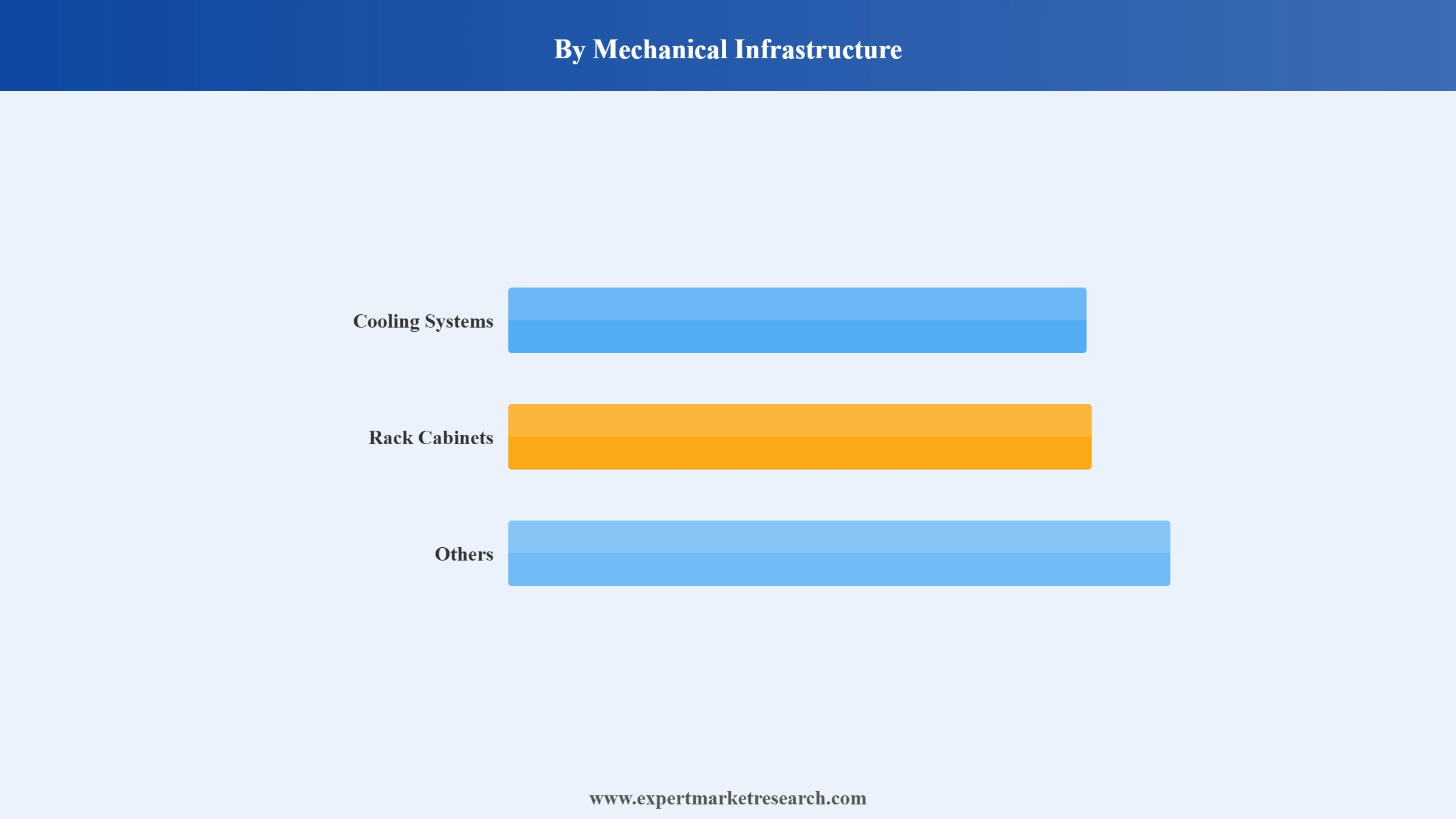

Market Breakup by Mechanical Infrastructure

Key Insight: Cooling systems are the dominant and fastest-growing mechanical sub-segment, driven by the thermal management demands of AI workloads. Operators are transitioning from traditional air cooling to liquid cooling, direct liquid cooling, and immersion cooling systems to handle rack densities that exceed 100 kW. In August 2025, CtrlS inaugurated its Kolkata campus featuring a liquid cooling system specifically designed for AI-dense deployments, demonstrating how mechanical infrastructure modernisation is central to India's data center capacity expansion.

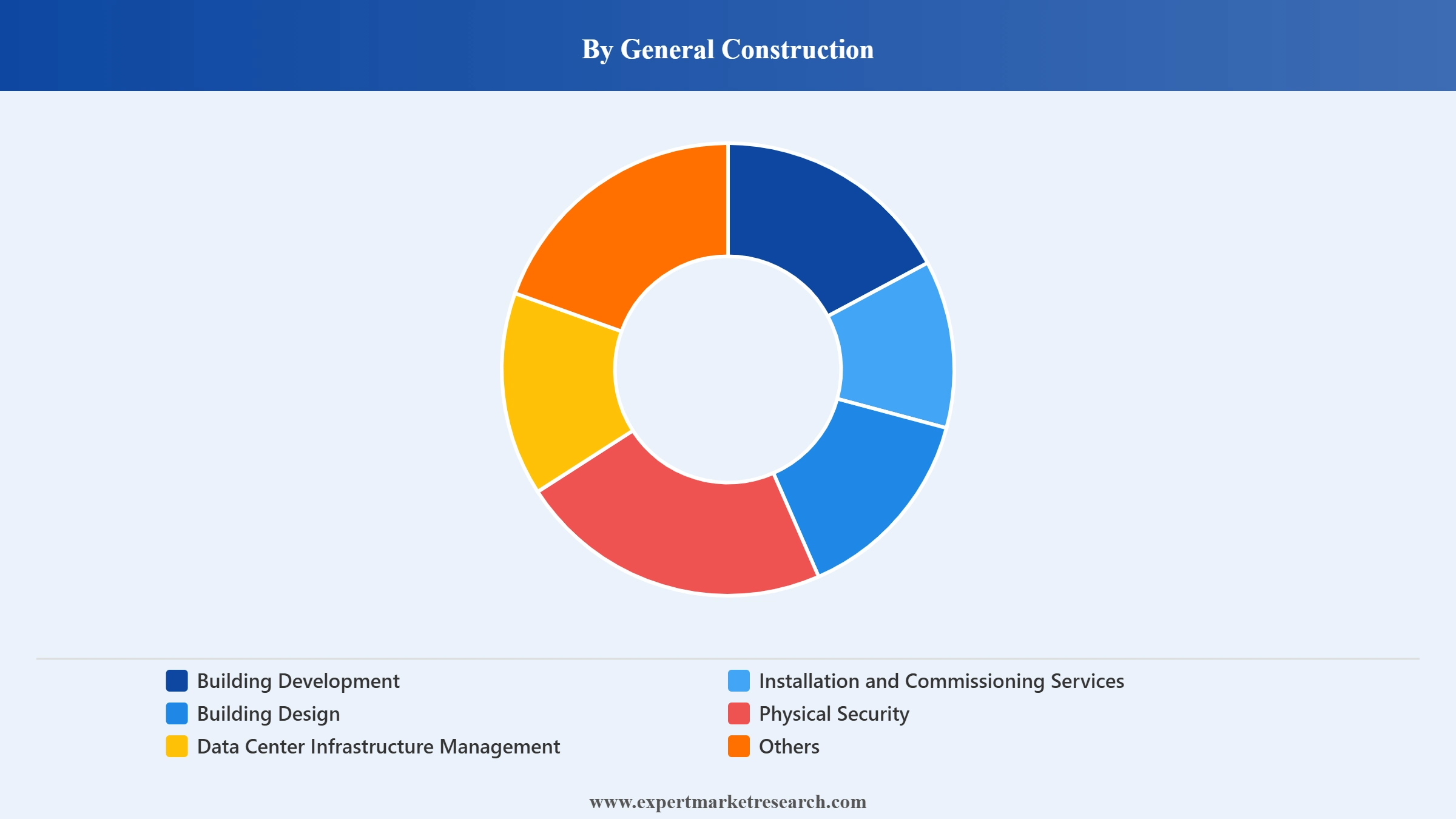

Market Breakup by General Construction

Key Insight: Building development is the largest general construction segment, reflecting the scale of greenfield campus investments across India's key data center hubs. Installation and commissioning services are growing with the rapid pace of capacity additions, requiring specialised MEP and IT fit-out contractors. Data Center Infrastructure Management (DCIM) software is gaining adoption as operators seek real-time visibility into power, cooling, and capacity utilisation. Physical security investment is increasing in line with compliance requirements under India's data localisation regulations.

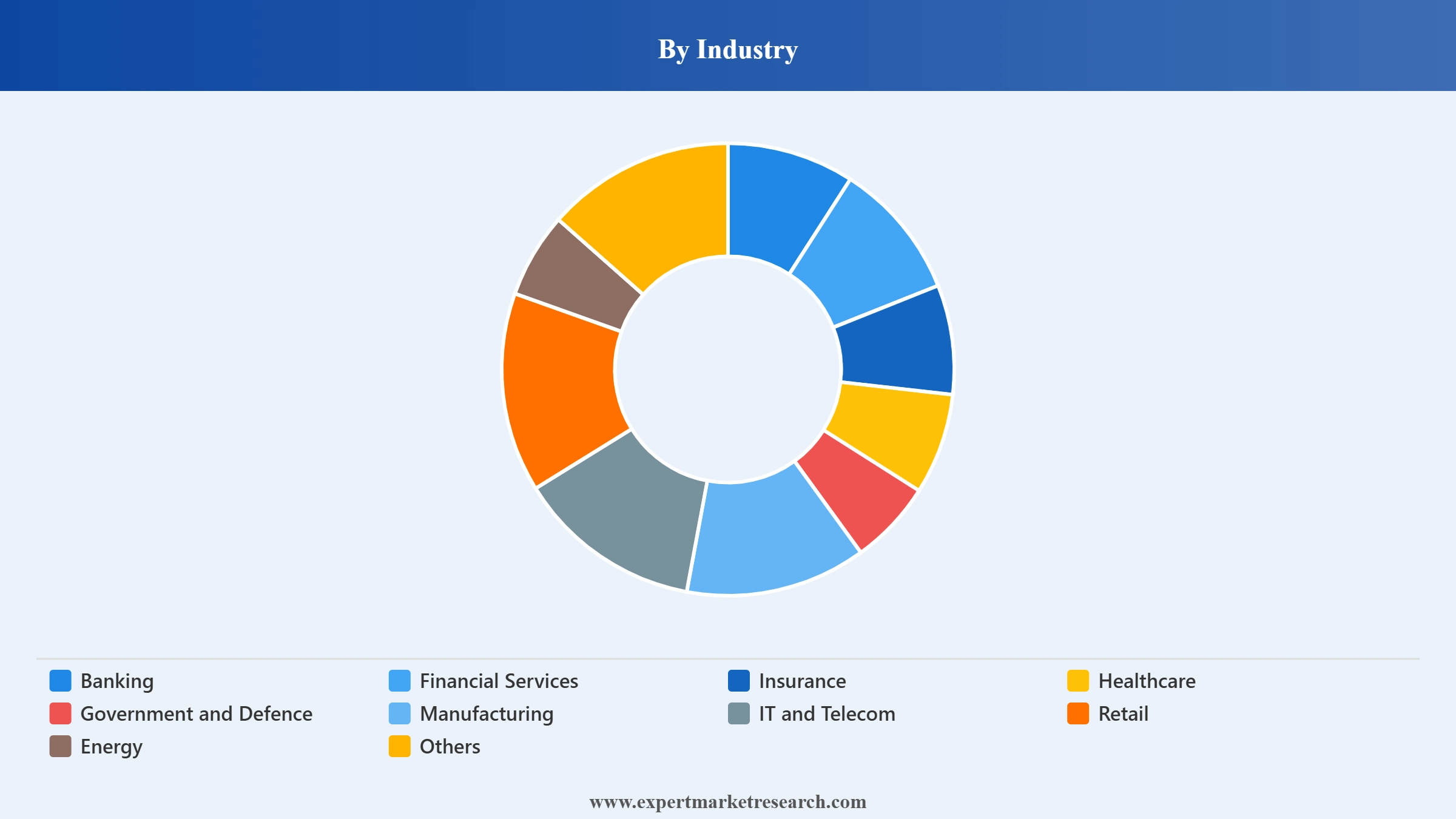

Market Breakup by Industry

Key Insight: IT and telecom is the dominant industry vertical, accounting for approximately 44-47% of market demand, driven by cloud computing deployments, telecom digitalisation, and 5G infrastructure buildout. BFSI is the second-largest vertical, with strict data localisation mandates compelling banks and insurers to maintain robust domestic data center capacity. Healthcare, government, and manufacturing verticals are growing rapidly, supported by electronic health records adoption, e-governance programmes, and smart factory digitalisation across India.

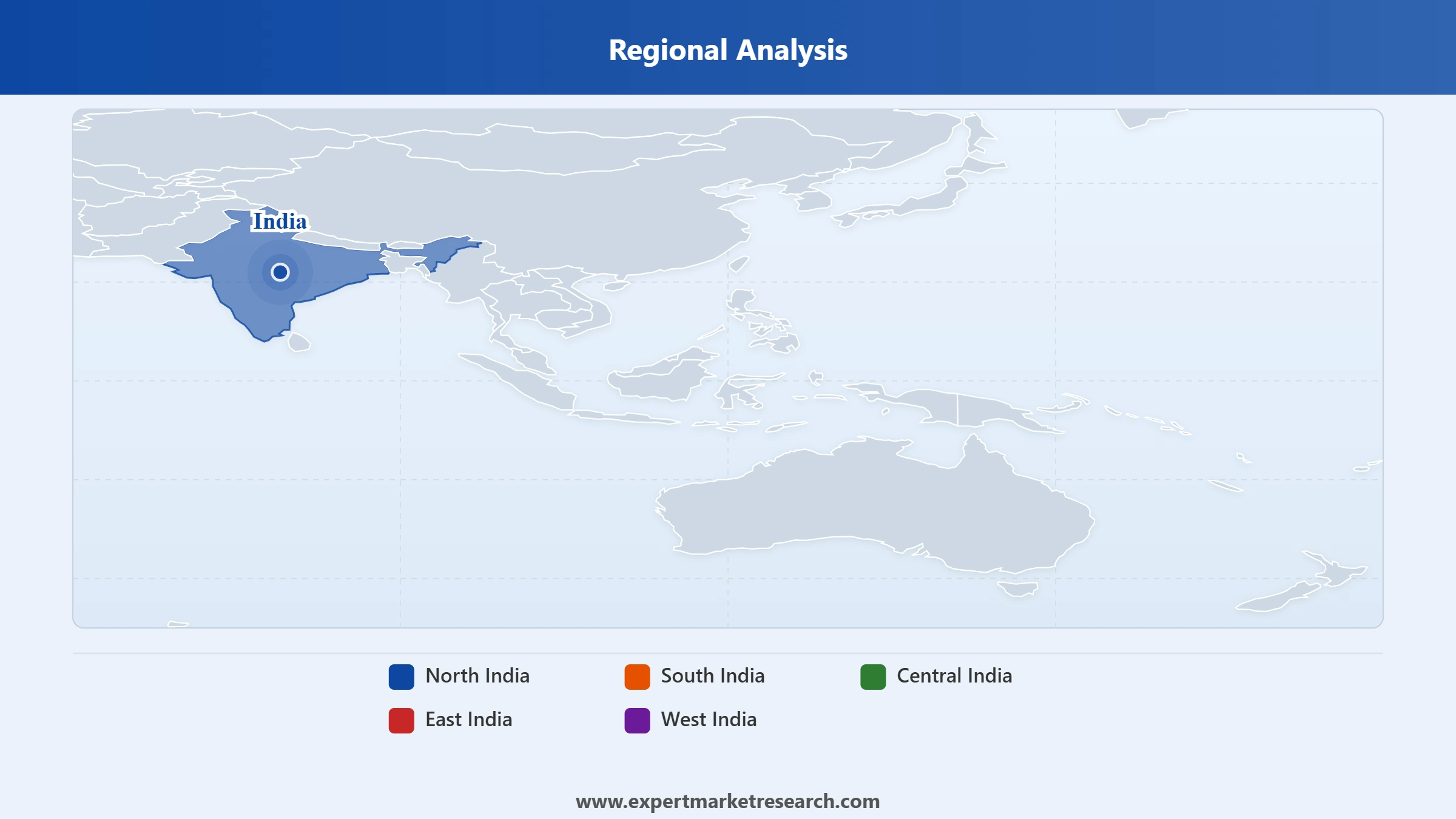

Market Breakup by Region

Key Insight: West India dominates with over 52% of national installed capacity, anchored by Mumbai's submarine cable ecosystem and Maharashtra's concentration of financial services enterprises. South India is the fastest-growing region, with Hyderabad and Chennai attracting hyperscale investment through state incentive programmes. North India is expanding rapidly around the Delhi-NCR corridor, with Noida emerging as a key hub. Central India is gaining traction with CtrlS's April 2025 Bhopal groundbreaking under MP's Global Capacity Centers Policy, while East India is the earliest-stage market with growing investment pipelines.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By components, solution dominates the market due to high capital expenditure on hardware and infrastructure installations

The solution component leads the India data center market, reflecting the capital-intensive nature of building and equipping modern facilities. Server, storage, and networking deployments for AI and cloud workloads account for the largest share of capital spending across hyperscale and colocation campuses. As India's installed data center capacity targets surpass 2,000 MW by 2027, sustained capital allocation toward solution components is expected to remain the primary revenue driver throughout the forecast period.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The services component is growing faster than solutions, as enterprises transition from owning infrastructure to leasing scalable managed capacity from colocation operators, cloud providers, and managed service companies. In February 2026, the L&T and NVIDIA sovereign AI factory partnership illustrated how solution hardware deployments and managed AI compute services are converging, creating new hybrid revenue models that are reshaping the services segment of the India data center market.

By infrastructure, IT infrastructure dominates the market due to the foundational role of servers, storage, and networking in every facility

IT infrastructure holds the largest share of the India data center market by infrastructure type, driven by server, storage, and networking investments that are accelerating as AI and cloud workloads expand. GPU-intensive server deployments are the fastest-growing sub-category, with rack densities scaling from conventional 5-10 kW to over 100-300 kW per rack across AI-optimised campuses. This shift is compelling operators to redesign facilities from the ground up to support next-generation compute architectures.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Electrical infrastructure investment is growing rapidly to meet expanding power requirements, with UPS systems and generators essential for Tier III and Tier IV uptime compliance. Mechanical infrastructure is seeing elevated investment as liquid cooling adoption accelerates for AI-dense deployments. General construction spending is at peak levels as greenfield hyperscale campuses are developed across Mumbai, Hyderabad, Chennai, and Bhopal, with CtrlS's April 2025 Bhopal groundbreaking illustrating how general construction activity is spreading into Central India's emerging data center hubs.

By IT infrastructure, servers account for the dominant share of the market due to AI workload-driven compute demand

Servers represent the largest IT infrastructure sub-segment in the India data center market, propelled by the explosive demand for GPU-intensive compute platforms supporting AI training, inference, and large-scale machine learning workloads. Operators including CtrlS and AdaniConnex are investing in high-density server infrastructure capable of handling rack loads up to 135-300 kW, a fundamental departure from traditional compute architectures. Yotta Data Services' order of 16,000 NVIDIA H100 GPUs in 2024, targeting 32,000 by March 2025, illustrates the server demand trajectory.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Storage systems are growing rapidly with the surge in unstructured data generated by cloud services, AI model outputs, and digital platforms. Networking equipment is expanding to support high-bandwidth interconnects between GPU clusters and distributed storage nodes, with operators investing in next-generation spine-leaf and fabric architectures. The activation of the 2Africa Pearls cable system in 2025 has expanded India's international bandwidth and reinforced demand for high-capacity network infrastructure across the India data center market.

By electrical infrastructure, UPS systems dominate the market due to their critical role in protecting live workloads during grid transitions

UPS systems hold the dominant share within the electrical infrastructure segment, providing the essential bridging power that protects active workloads during transitions between grid power and backup generation. For AI and financial services workloads where even milliseconds of downtime carry significant business risk, UPS reliability is a non-negotiable facility specification. The growing density of India's data center deployments and the push for Tier III and Tier IV certification are driving continued investment in modular, scalable UPS architectures across the India data center market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Generators are the primary backup power source and represent the second-largest electrical sub-segment, with diesel and increasingly gas-fuelled systems deployed across all hyperscale and colocation campuses. Transfer switches and switchgears ensure seamless power source transitions, while PDUs distribute conditioned power at the rack level. The 2025 CtrlS and NTPC MoU for a 2 GW renewable energy project signals how India's data center operators are embedding large-scale clean energy procurement directly into their electrical infrastructure strategy.

By mechanical infrastructure, cooling systems dominate the market due to the thermal management demands of high-density AI deployments

Cooling systems represent the dominant and fastest-growing mechanical infrastructure sub-segment in the India data center market, driven by the dramatic increase in thermal load generated by AI workloads. Traditional air cooling is increasingly insufficient for rack densities exceeding 50 kW, prompting operators to adopt liquid cooling, direct liquid cooling, and immersion cooling systems. CtrlS's Chandanvelly facility handles densities up to 135 kW per rack, with immersion cooling solutions capable of scaling to 300 kW, setting industry benchmarks for thermal management in India.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Rack cabinets represent the second mechanical sub-segment, with high-density and open-frame rack designs being adopted to accommodate the physical footprint of GPU clusters and associated networking infrastructure. In August 2025, CtrlS inaugurated the first phase of its Kolkata data center campus with a purpose-built liquid cooling system designed for AI-dense deployments, demonstrating how mechanical infrastructure modernisation is a central investment priority for operators expanding capacity across the India data center market.

By general construction, building development dominates the market due to the scale of greenfield hyperscale campus investment

Building development holds the largest share of the general construction segment in the India data center market, reflecting the scale of greenfield campus construction being undertaken by hyperscale operators and colocation providers across Maharashtra, Telangana, Tamil Nadu, and emerging Tier-2 cities. AdaniConnex's 1 GW pipeline across Navi Mumbai, Hyderabad, Pune, and Chennai, combined with NTT's multi-city campus expansion programme, represents billions of dollars of active building development committed over the forecast period.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Installation and commissioning services are growing with the rapid pace of capacity additions, requiring specialised MEP and IT fit-out contractors. Data Center Infrastructure Management software is gaining adoption as operators seek real-time visibility into power, cooling, and capacity utilisation across distributed multi-site portfolios. Physical security investment is expanding in line with India's data localisation compliance requirements. Building design investment is also rising as AI-ready facilities require fundamentally different floor plate, power, and cooling architecture than conventional data center builds in the India data center market.

By industry, IT and telecom leads the market due to cloud computing, 5G infrastructure, and enterprise data migration demand

IT and telecom is the dominant industry vertical in the India data center market, accounting for approximately 44-47% of total demand. Cloud service provider deployments by AWS, Microsoft Azure, and Google Cloud, combined with 5G network infrastructure buildouts and enterprise cloud migration programmes, drive sustained high-volume demand for data center capacity. The activation of international subsea cable systems in 2025 has reinforced India's position as a regional internet gateway, further amplifying IT and telecom sector demand for domestic data center infrastructure.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

BFSI is the second-largest vertical at approximately 20-33% market share, driven by stringent data localisation regulations mandating domestic processing of financial transaction and customer data, and the digital banking revolution expanding real-time payment infrastructure. Healthcare, government, and manufacturing verticals are growing rapidly, driven by telemedicine deployments, Digital India e-governance programmes, and smart factory digitalisation. In February 2026, L&T's sovereign AI factory partnership with NVIDIA highlighted the growing importance of India's strategic computing and defence vertical within the India data center market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

West India leads the market due to Mumbai's submarine cable ecosystem and dominant installed capacity position

West India commands over 52% of India's total data center installed capacity, anchored by Mumbai's status as the country's primary submarine cable landing point and its concentration of financial services enterprises. Operators including AdaniConnex, Yotta, and STT GDC have established flagship campuses in Navi Mumbai, drawn by world-class connectivity infrastructure and Maharashtra's supportive data center policies. West India's dominance is expected to be maintained throughout the forecast period given its infrastructure head start.

South India is the fastest-growing data center region in the India data center market, with Hyderabad and Chennai attracting significant hyperscale investment driven by state incentive programmes, reliable power grids, and disaster-resilient geographies. NTT's USD 1.2 billion AI cluster in Hyderabad and Equinix's Chennai expansion illustrate the scale of commitment. CtrlS's April 2025 Bhopal groundbreaking under MP's Global Capacity Centers Policy 2025 indicates that Central India is also entering the investment pipeline.

India's data center market is highly competitive, combining domestic conglomerates such as AdaniConnex and Yotta with global operators including NTT Global Data Centers, Equinix, and STT GDC India. Domestic players benefit from government relationships, local market knowledge, and cost advantages, while global operators bring technical expertise, international customer relationships, and access to capital markets. Competition is intensifying as AI-driven demand attracts new entrants and prompts aggressive capacity expansion by existing operators.

Competitive differentiation is increasingly built around AI-readiness, green energy credentials, and hyperscale campus scale. Liquid cooling capabilities, renewable energy partnerships, and land bank access are becoming critical strategic assets. The 2025 CtrlS and NTPC renewable energy MoU for a 2 GW project, and AdaniConnex's 1 GW capacity target, illustrate the scale of ambition reshaping competition in the India data center market as operators position for the AI infrastructure decade.

Founded in 2009 and headquartered in Mumbai, CtrlS Datacenters is India's largest hyperscale data center operator, with facilities across Mumbai, Hyderabad, Chennai, Bengaluru, and Kolkata. CtrlS has committed USD 2 billion for green, AI-ready campus development, with recent projects including a Bhopal facility under Madhya Pradesh's Global Capacity Centers Policy 2025 and a 125 MWp solar farm.

NTT Global Data Centers, a subsidiary of Nippon Telegraph and Telephone Corporation headquartered in Tokyo, Japan, operates a significant India network with 292 MW of live IT load capacity as of July 2025. NTT is investing USD 1.2 billion in an AI-optimised cluster in Hyderabad and expanding to Noida, Bengaluru, and additional campuses to meet rising cloud and AI demand across the India data center market.

AdaniConnex is a joint venture between Adani Enterprises and EdgeConneX, headquartered in Ahmedabad, India. It is pursuing a 1 GW national capacity target backed by a USD 10 billion investment roadmap. With a flagship Navi Mumbai campus targeting 1,000 MW IT load and campuses under development in Hyderabad, Pune, and Chennai, AdaniConnex represents the most ambitious domestic capacity expansion in India's data center market.

Founded in 1999 and headquartered in Chennai, India, Sify Technologies is a leading domestic data center and managed services provider operating across Chennai, Mumbai, Bengaluru, Hyderabad, and Delhi. Sify's AI-Hub data center development programme and established enterprise customer base across BFSI, government, and IT verticals position it as a key player in India's growing hyperscale and colocation data center sector.

Other key players in the market are Arshiya Limited, YottaData Services Private Limited, Reliance Communications Ltd. (Reliance Datacenter), Pi DATACENTERS Pvt. Ltd., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Access the complete intelligence behind India's data center market opportunity with our latest comprehensive report. From AI infrastructure demand and hyperscale campus expansion to regional capacity distribution and renewable energy integration, this report gives operators, investors, vendors, and cloud providers the clarity to make well-informed decisions in one of the world's fastest-growing digital infrastructure markets. Download your free sample today and explore the full scope of the India data center growth story.

United States Data Center Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 5031.81 Million.

The India data center market is assessed to grow at a CAGR of 14.10% between 2026 and 2035.

The India data center market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 18818.31 Million by 2035.

The market is being aided by the increasing digital transformation, the introduction of various favourable government initiatives to boost investments in data centers, and the expansion of data center solutions.

The market growth can be attributed to the growing demand for high-speed data with low latency, the increasing adoption of data centers in the telecom industry, and the growing usage of data centers in the healthcare industry.

The major regions in the market in India include North India, South India, Central India, East India, and West India.

The various components of data center are services and solution.

The major IT infrastructures of data center in the market are network, server, and storage.

The significant electrical infrastructures in the market are UPS systems, generators, transfer switches and switchgears, and PDUs, among others.

The different mechanical infrastructures of data center are cooling systems and rack cabinets, among others.

The several general construction segments of data center are building development, installation and commissioning services, building design, physical security, and data center infrastructure management, among others.

The major industries of data center are banking, financial services, and insurance, healthcare, government and defence, manufacturing, IT and telecom, retail, and energy, among others.

The major players in the market are CTRLS Datacenters Ltd., Arshiya Limited., NTT Global Data Centers, Sify Technologies Limited., YottaData Services Private Limited, AdaniConnex Private Limited, Reliance Communications Ltd. (Reliance Datacenter), Pi DATACENTERS Pvt.Ltd., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Components |

|

| Breakup by Infrastructure |

|

| Breakup by IT Infrastructure |

|

| Breakup by Electrical Infrastructure |

|

| Breakup by Mechanical Infrastructure |

|

| Breakup by General Construction |

|

| Breakup by Industry |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.