Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

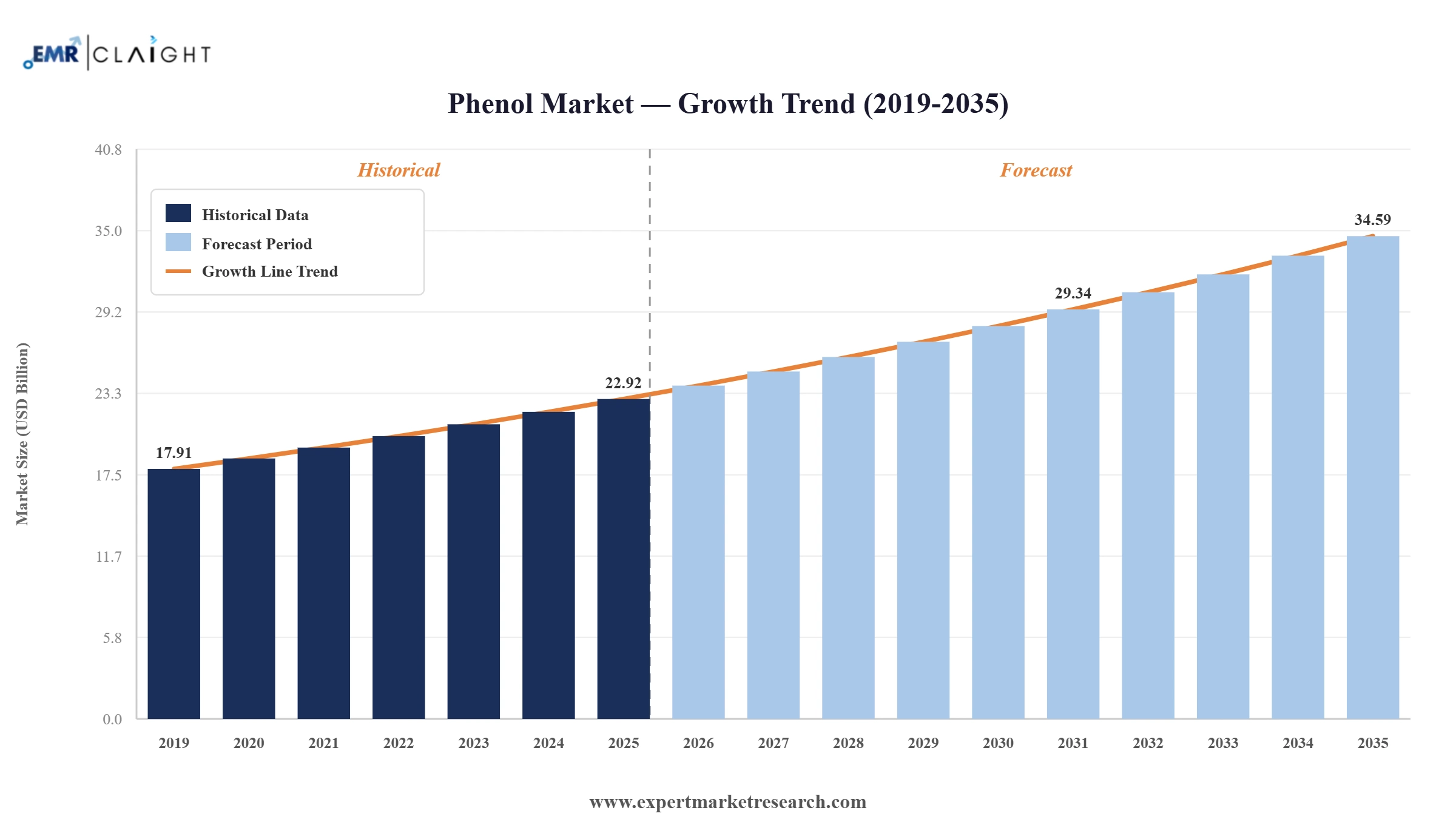

The global phenol market reached a value of USD 22.92 Billion at 2025 and is projected to expand at a CAGR of around 4.20% during the forecast period of 2026-2035. With rising bisphenol A demand for polycarbonate and epoxy resins, growth in phenolic resin specifications for construction and automotive, capacity expansions in Asia and the US, and ongoing rationalisation of European production, the market is expected to reach USD 34.59 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global phenol market is reshaped by Asia capacity build out, US INEOS Mobile growth, European production closures, and continued downstream demand from bisphenol A, phenolic resin, and caprolactam. These shifts are recalibrating regional trade flows and cost curves.

SABIC Fujian Petrochemical Zhangzhou phenol plant and Shiyou Chemical Yangzhou phenol plant 2 came online in 2026, adding 250,000 and 280,000 tonnes per year of phenol capacity respectively, reshaping Asia Pacific supply and pressuring European producers.

INEOS Group announced plans to boost production of phenol at its Mobile Alabama plant by up to 850,000 tonnes per year, which will make it the largest phenol unit in the world, strengthening US Gulf Coast supply for bisphenol A and phenolic resin customers.

INEOS announced the permanent closure of its Gladbeck Germany 650,000 tonnes per year phenol facility on June 17, 2025, suggesting continued rationalisation of European phenol production amid rising Asian competition and weak European downstream demand.

INEOS confirmed on June 18, 2025 that it will not restart its Antwerp phenol production plant until at least 2027, suggesting further deferral of European capacity restoration and supporting tighter European supply and import dependence in the near term.

Asia Push: The global phenol market is reshaped by Asia capacity additions, with SABIC Fujian Petrochemical Zhangzhou and Shiyou Chemical Yangzhou bringing online roughly half a million tonnes of new capacity in 2026, pressuring European producers and shifting trade flows.

US Push: Global phenol market growth is shaped by US Gulf Coast capacity growth, with INEOS planning to lift Mobile Alabama capacity to make it the largest phenol unit in the world, strengthening Western Hemisphere supply for bisphenol A and phenolic resin customers.

European Push: The global phenol market is reshaped by European rationalisation with the INEOS Gladbeck closure and Antwerp restart deferral, increasing European import dependence and reshaping trade flows from US and Asia into Western Europe.

Demand Push: The global phenol market is lifted by bisphenol A and polycarbonate demand for electronics, EV battery casings, and construction sheet applications, anchoring downstream phenol consumption alongside phenolic resin and caprolactam end uses.

Feedstock Push: Global phenol market growth is aided by cumene benzene and propylene feedstock integration at major producers, with vertically integrated players such as INEOS, Mitsui Chemicals, and Sasol securing cost advantage and supply reliability for downstream markets.

The report of the Expert Market Research's titled "Global Phenol Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

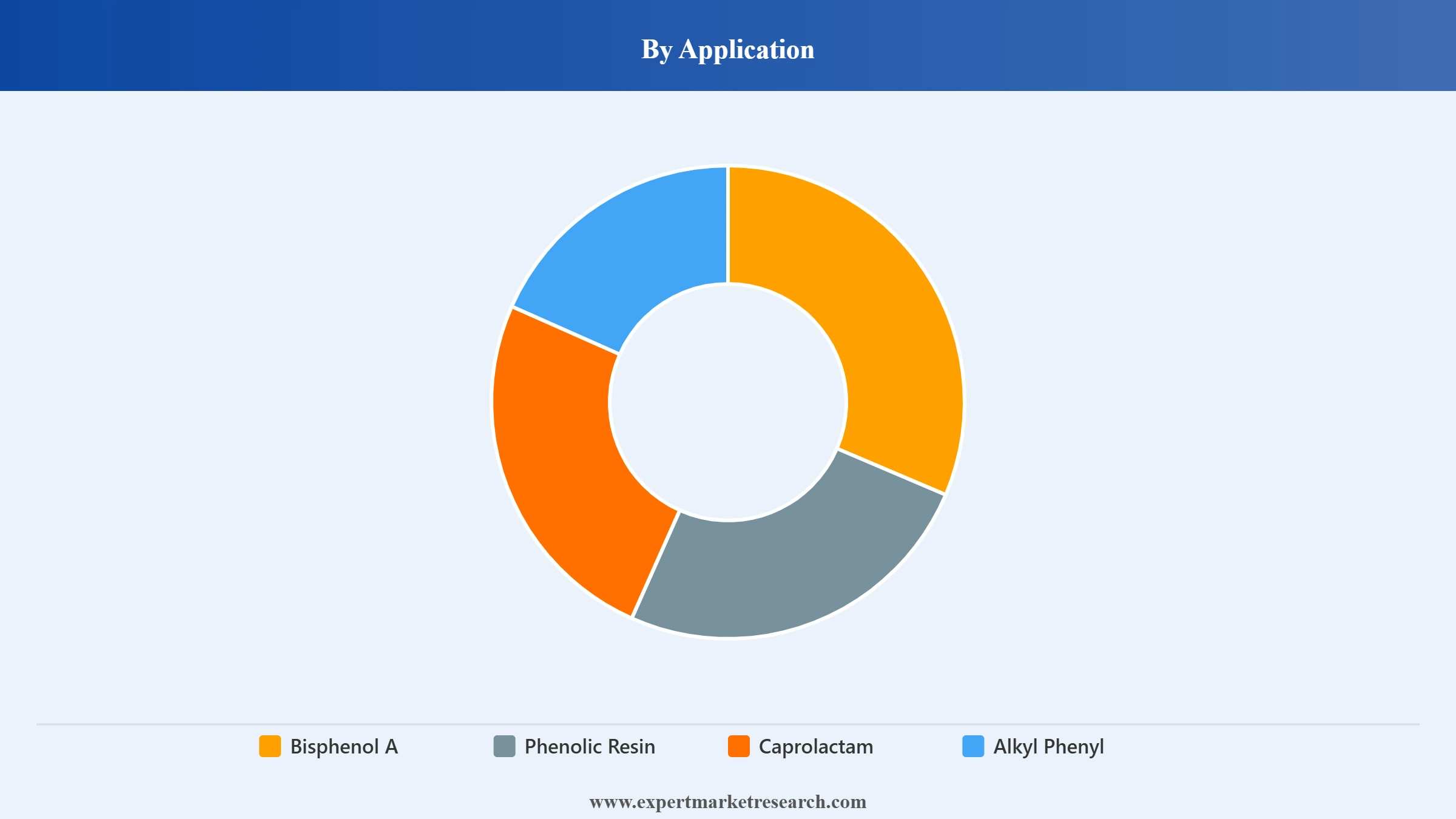

Market Breakup by Application

Key Insight: Bisphenol A leads the application segment with broad demand from polycarbonate plastics, epoxy resins, and EV battery casing applications. Phenolic resin is the next worth noting pool, aided by construction laminates, automotive moulded parts, and abrasives. Caprolactam underpins nylon 6 production, while alkyl phenyl applications serve surfactants, lubricants, and antioxidants. Others including salicylic acid and chlorophenols complete the application pool.

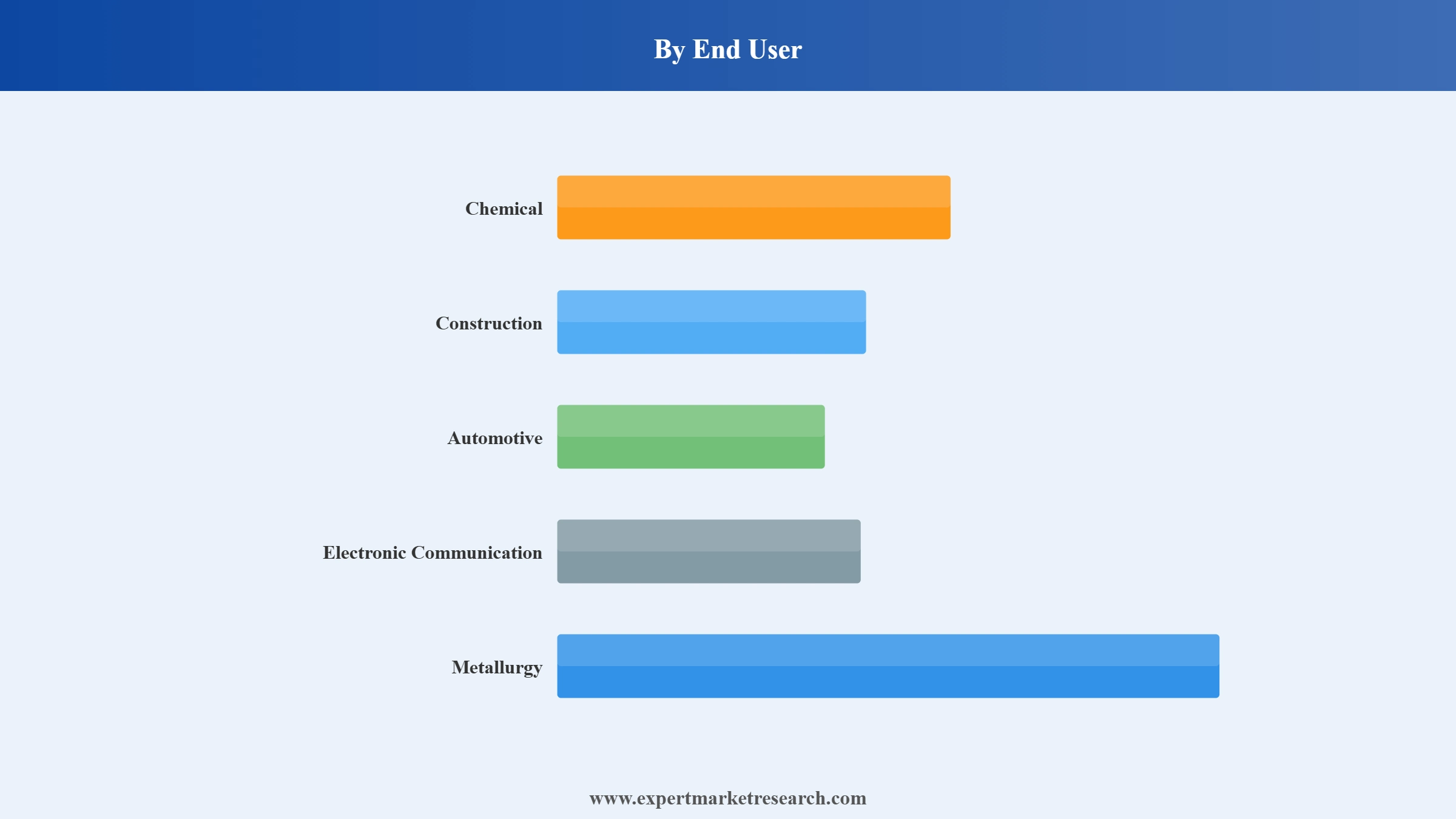

Market Breakup by End User

Key Insight: Chemical end use leads the global phenol market with broad downstream consumption across bisphenol A, phenolic resin, and caprolactam. Construction is the next worth noting pool, aided by phenolic resin moulded parts, laminates, and insulation. Automotive end use is the fastest growing pool on EV battery casing demand and polycarbonate sheet applications. Electronic communication uses polycarbonate housing, while metallurgy uses phenolic binders. Others including textiles and pharmaceuticals complete the end use pool.

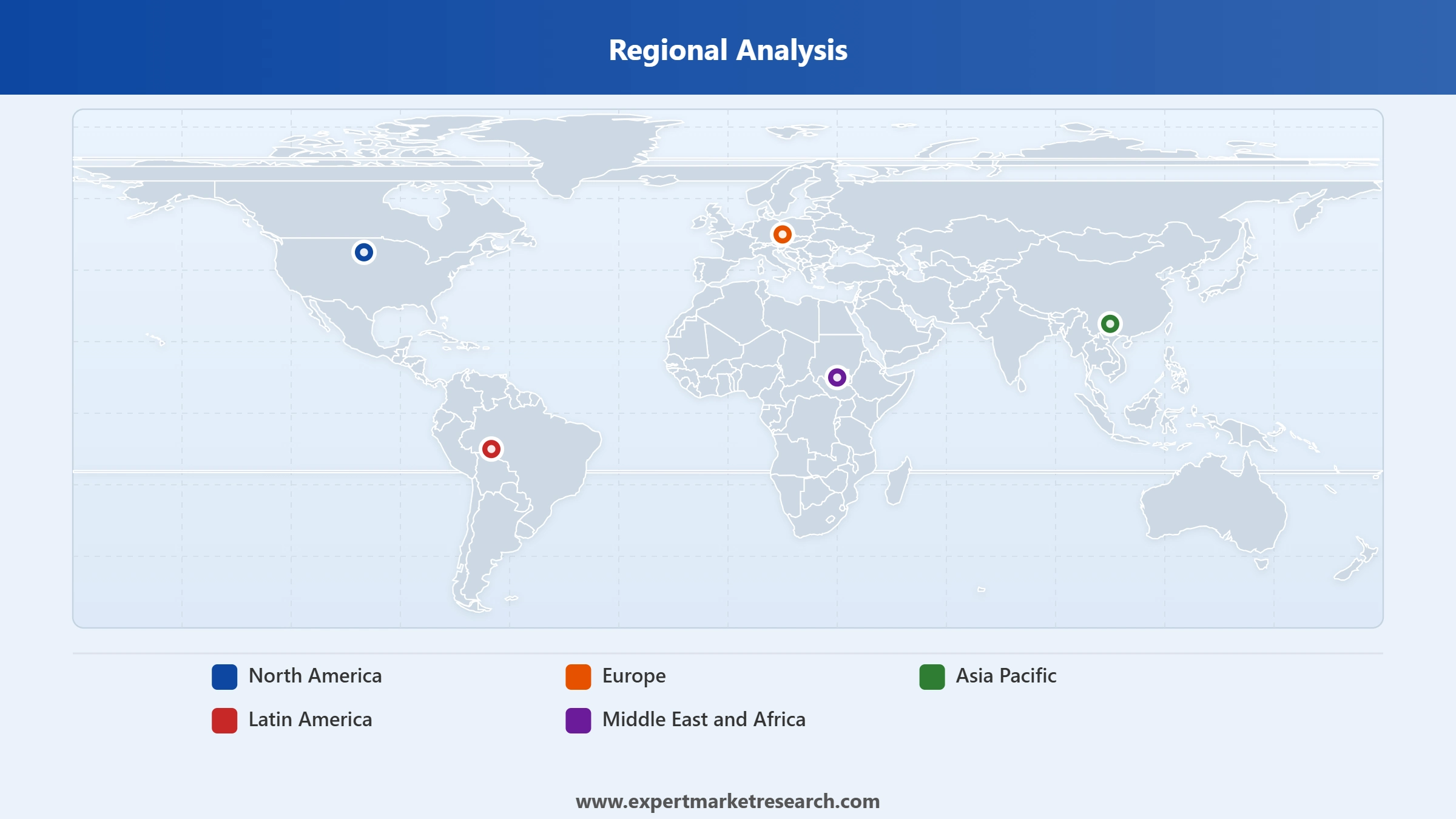

Market Breakup by Region

Key Insight: Asia Pacific dominates global phenol demand on the back of China and India downstream consumption and major capacity additions. On balance, north America anchors integrated cumene phenol production with US Gulf Coast plants. Europe contributes through Solvay, INEOS, and Mitsui assets but is undergoing rationalisation. Middle East and Africa are emerging on Saudi and Egypt downstream chemicals projects. Latin America is led by Brazil and Mexico chemicals demand and limited domestic production.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Application, Bisphenol A dominates the market due to polycarbonate and epoxy resin demand

Bisphenol A leads the global phenol market with broad demand from polycarbonate plastics, epoxy resins, and EV battery casing applications across Asia Pacific, North America, and Europe. February 2026 SABIC and Shiyou Chemical capacity additions illustrate how Asian phenol producers are scaling supply for downstream bisphenol A and polycarbonate manufacturing.

Phenolic resin is the next worth noting pool, aided by construction laminates, automotive moulded parts, and abrasives. Caprolactam underpins nylon 6 production. January 2026 INEOS Mobile Alabama 850 kt growth illustrates how US producers are scaling phenol supply for downstream chemical customers, supporting global phenol market growth across applications.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By End User, Chemical accounts for the dominant share of the market due to broad downstream consumption

Chemical end users dominate the global phenol market with broad downstream consumption across bisphenol A, phenolic resin, and caprolactam producers worldwide. That said, construction is the next worth noting pool, aided by phenolic resin moulded parts and laminates. Automotive end use is gaining share quickly on EV battery casing and polycarbonate sheet demand.

Electronic communication uses polycarbonate housing for devices and equipment. Metallurgy uses phenolic binders for foundry sand, while textiles and pharmaceuticals add incremental demand. June 2025 INEOS Gladbeck closure and Antwerp deferral are reshaping European downstream supply patterns and contributing to broader global phenol market growth dynamics.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific dominates the market due to capacity additions and downstream demand

Asia Pacific leads the global phenol market on the back of China, India, and South Korea downstream consumption and major 2026 capacity additions, including the February 2026 SABIC Fujian Petrochemical Zhangzhou and Shiyou Chemical Yangzhou plants 2. China continues to dominate incremental phenol demand for bisphenol A, polycarbonate, and phenolic resin downstream markets, supporting Asia trade flows and pressuring European supply.

North America is anchored by integrated US Gulf Coast cumene phenol production, with the January 2026 INEOS Mobile Alabama 850 kt growth strengthening Western Hemisphere supply. That said, europe is undergoing rationalisation following the June 2025 INEOS Gladbeck closure and Antwerp restart deferral. Middle East and Africa are emerging on Saudi and Egypt downstream chemicals projects, supporting global phenol market growth across regions.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global phenol market is moderately consolidated with global cumene phenol majors, Asian state owned integrated chemicals firms, and specialised regional producers competing across bisphenol A, phenolic resin, caprolactam, and alkyl phenyl downstream markets. Competitive priorities revolve around feedstock integration, scale, decarbonisation, and downstream end user partnerships.

Companies are differentiating through capacity growth, feedstock integration, decarbonisation, and rationalisation of high cost European assets. Strategic moves include the January 2026 INEOS Mobile Alabama 850 kt spread, the June 2025 INEOS Gladbeck closure and Antwerp deferral, and February 2026 SABIC Fujian Petrochemical Zhangzhou and Shiyou Chemical Yangzhou plant additions.

Founded in 1998 and headquartered in London, UK, the company is a leading global chemicals firm with major phenol and acetone production at Mobile Alabama and historical European assets. Its phenol business serves bisphenol A, phenolic resin, and caprolactam customers globally through integrated cumene phenol production and an expanding US footprint.

Founded in 1997 and headquartered in Tokyo, Japan, the company is a Japanese chemicals firm with major phenol and downstream bisphenol A production. Its operations supply Asia Pacific and global polycarbonate, epoxy resin, and phenolic resin customers, with vertically integrated cumene phenol bisphenol A operations supporting cost leadership.

Founded in 1929 and headquartered in Houston, Texas as part of Shell plc, the company is a major US Gulf Coast chemicals producer with integrated cumene phenol acetone production. Its phenol output supports downstream bisphenol A, phenolic resin, and caprolactam customers across North America and global export markets.

Founded in 1863 and headquartered in Brussels, Belgium, the company is a leading global chemicals and advanced materials supplier with selected phenol related downstream activities. Its operations support specialty chemicals and polymer customers globally, with European assets contributing to regional production alongside major US and Asia Pacific players.

Other leading companies in the market are Honeywell International Inc., Royal Dutch Shell, Deepak Nitrite Limited, ALTIVIA Chemicals, Sasol Chemicals, Mitsubishi Corporation, Domo Chemicals, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Discover the latest insights on the global phenol market 2026 with our comprehensive report. Stay ahead of the curve with valuable data on product innovations, consumer demand, and top growth regions. Whether you are launching a new product or expanding your brand, this report gives you the clarity you need. Download your free sample now and discover the key opportunities in the thriving Global Phenol.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market size of phenol was approximately USD 22.92 Billion.

The phenol market is assessed to grow at a CAGR of 4.20% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 34.59 Billion by 2035.

The major drivers of the industry such as rising urbanisation, increasing disposable incomes, strong demand from emerging economies, technological advancements, and growing demand for alkyl phenyl are expected to aid the market growth.

Improvements in the phenol production technology, focussed on enhancing output, lowering process costs and improving safety, is expected to be a major trend informing the industry growth.

The major regions in the industry are North America, the Asia Pacific, Europe, Latin America, and the Middle East and Africa, with the Asia Pacific accounting for the largest market share of 52.5%.

The leading end use segment in the industry is bisphenol A, accounting for 47% of market share.

The major players in the industry are INEOS Group, Mitsui Chemicals, Inc., Shell Chemical Co., Solvay SA, Honeywell International Inc., Royal Dutch Shell, Deepak Nitrite Limited, ALTIVIA Chemicals, Sasol Chemicals, Mitsubishi Corporation, and Domo Chemicals, among others.

The Asia Pacific region held the largest market share in 2025.

Bisphenol A accounted for the biggest share in the market as an application.

The construction segment held the largest market share in 2025.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Application |

|

| Breakup by End User |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.