Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The Africa E-Learning Market reached a value of USD 4066.36 Million at 2025 and is projected to expand at a CAGR of around 19.20% during the forecast period of 2026-2035. With surging smartphone adoption, deepening 4G/5G coverage, accelerated post-pandemic digital pedagogy, and rising corporate upskilling demand, the market is expected to reach USD 23548.78 Million by 2035.

Compound Annual Growth Rate

19.2%

Value in USD Million

2026-2035

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Africa E-Learning Market Report Summary | Description | Value |

| Base Year | USD Million | 2025 |

| Historical Period | USD Million | 2019-2025 |

| Forecast Period | USD Million | 2026-2035 |

| Market Size 2025 | USD Million | 4066.36 |

| Market Size 2035 | USD Million | 23548.78 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 19.20% |

| CAGR 2026-2035 - Market by Country | South Africa | 20.5% |

| CAGR 2026-2035 - Market by Country | Morocco | XX% |

| CAGR 2026-2035 - Market by Technology | Mobile Learning | 21.7% |

| CAGR 2026-2035 - Market by Product Type | Services | 21.9% |

| Market Share by Country 2025 | Nigeria | 8.1% |

The Africa e-learning market growth is being shaped by AI-led platform innovation, sweeping government digital schooling rollouts, scaling pan-African EdTech investment, and the mainstreaming of mobile-first vocational learning across formal and informal economies.

At its flagship Inspire 2025 event, Docebo S.p.A. unveiled an AI-first product roadmap featuring AI Creator, AI Video Presenter, AI Virtual Coaching, and the Harmony agentic marketplace. Docebo, an active vendor to South African and pan-African enterprise customers, said the toolset will let L&D teams produce structured courses, simulations, and lifelike video content without external production overhead. The release strengthens its position in Africa's corporate learning segment, where multinational employers increasingly source cloud-based LMS for distributed workforces and franchise networks.

The Mastercard Foundation, in partnership with Co-Creation Hub (CcHUB), opened applications for its 2025 EdTech Fellowship targeting startups operating in South Africa, Nigeria, Kenya, Ghana, and Senegal. The cohort secures business advisory, capital and curriculum-design support, with prior cohorts having held Demo Days across each country. The programme reinforces the funding pipeline for Africa-based platforms such as Eneza Education, Tutor.ng, and Obami, and is widely viewed as catalytic to scaling K-12 and post-secondary digital delivery in low-bandwidth environments.

The African Union Development Agency (AUDA-NEPAD) released a draft African EdTech 2030 Vision and Action Plan, framing Africa's bid to lead global EdTech innovation. The document calls for harmonised standards, regional consortia for content sharing, and incentives for private investment. Stakeholders including ministries from Nigeria, Kenya, and South Africa are expected to align national digital learning roadmaps with the framework, translating into procurement opportunities for content providers, LMS vendors, and connectivity partners.

Industry coverage of the Africa e-learning market formally added Obami (South Africa), Dapt.io, Tutor.ng (Nigeria), and Eneza Education to the active vendor set, alongside long-standing players such as Via Afrika. The expanded vendor map reflects growing investor interest in tutoring marketplaces, LMS platforms, and curriculum-aligned mobile apps across Sub-Saharan Africa, and signals consolidation pressures as larger global LMS providers seek partnerships with locally branded content houses to reach K-12 and university buyers.

The Mastercard Foundation EdTech Fellowship hosted Demo Days in South Africa, Nigeria, Ghana, Kenya, and Senegal in 2024, providing pitch and procurement opportunities for fellowship startups. Several cohort companies have since secured pilots with public-school systems and corporate L&D buyers, validating the commercial pipeline for African EdTech and expanding the addressable base for ancillary providers of payment, analytics, and content-delivery services.

AI-first learning suites are reshaping how African enterprises build and deliver training. Globally listed vendors are moving from content libraries to agentic platforms that auto-generate courses, simulate roleplays, and translate learning into local languages. The shift matters in Africa because employers serve multilingual, distributed workforces and need scalable, low-cost content. Docebo's Inspire 2025 unveiling of AI Creator, AI Video Presenter, and Harmony illustrates the direction. In April 2025, Docebo released its AI-first roadmap, signalling that productivity tools are now table-stakes for corporate buyers across South Africa, Egypt, and Kenya.

Continental policymaking is consolidating around a unified EdTech vision. The release of the AUDA-NEPAD draft African EdTech 2030 Vision in February 2025 sets common targets for digital infrastructure, teacher capacity, and content interoperability. National efforts in Kenya, Nigeria, and South Africa are now aligning curricula, certification, and procurement to this framework. The trend lifts demand for accredited LMS, secure cloud hosting, and regional content marketplaces, while reducing fragmentation that previously held back cross-border scaling for African EdTech vendors.

Funding momentum is broadening the EdTech base. African tech startups raised over USD 1 billion in H1 2025, up roughly 40% on the prior year, with a meaningful share routed to learning platforms via the Mastercard Foundation EdTech Fellowship and similar programmes. Capital is being deployed in K-12 content, micro-credentialing, and AI tutors. The trend matters because it supports vendor longevity, lets startups invest in local-language content, and de-risks the procurement decisions of public buyers in Kenya, Nigeria, and South Africa.

Mobile-first vocational learning is moving from pilot to scale. With smartphone penetration deepening and youth unemployment elevated, governments and donor-backed platforms are pushing app- and SMS-delivered vocational courses to bridge skills gaps. Eneza Education's mobile-tutor model, reaching over 10 million offline learners across Kenya, Ghana, Rwanda, and Côte d'Ivoire, exemplifies the format. The trend is reshaping demand for low-bandwidth content engines, vernacular curricula, and last-mile assessment, and it underpins long-term subscription revenue for both regional and international platform vendors.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Expert Market Research’s report titled “Africa E-Learning Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Sector

Key Insight: K-12 anchors the Africa e-learning market because school-going children represent the continent's largest single learner cohort and the most active focus of public investment. Curriculum-aligned content from Via Afrika, Eneza Education, and Obami is being deployed at district scale, while donor-supported tablet programmes in Kenya, Nigeria, and South Africa drive recurring licence revenue. Corporate and Government Learning is the next-fastest expanding bloc, supported by enterprise digitalisation, financial-services compliance training, and public-sector reskilling tied to industrial-policy goals. Post-secondary momentum reflects rising tertiary enrolment and the shift to blended degrees at universities such as the University of South Africa.

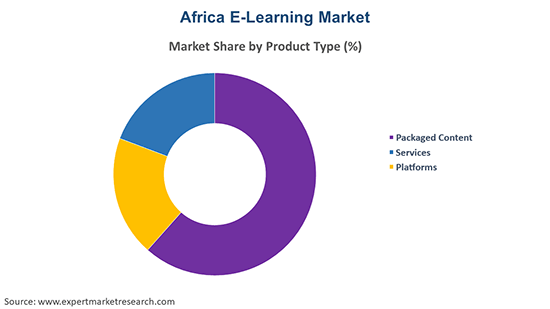

Market Breakup by Product Type

Key Insight: Packaged Content remains the workhorse revenue line because curriculum-aligned digital textbooks, video lessons, and assessment banks are the easiest to procure under existing education-budget rules. Platforms (LMS and learning experience platforms) are the fastest-rising segment, driven by enterprise migrations to cloud LMS such as Docebo and the rollout of national learning portals across South Africa and Morocco. Services—instructional design, content localisation, integration, and analytics—are growing in lockstep, as both ministries of education and corporates need partners to localise English- and French-language content into Arabic, Swahili, Yoruba, and Zulu.

Market Breakup by Technology

Key Insight: Mobile Learning leads adoption because smartphones are the dominant computing device for African learners, supported by sub-USD 100 Android handsets and prepaid mobile-data bundles. LMS is the institutional backbone of the market, with universities and large employers standardising on Docebo, Moodle-based deployments, and African platforms such as Obami. Simulation- and game-based learning are advancing fastest in healthcare, mining, and oil & gas training in countries such as South Africa and Nigeria, where employers need safe, repeatable, scenario-based skill-building. Adoption of immersive AR/VR remains nascent but is rising in private-school and corporate L&D pilots.

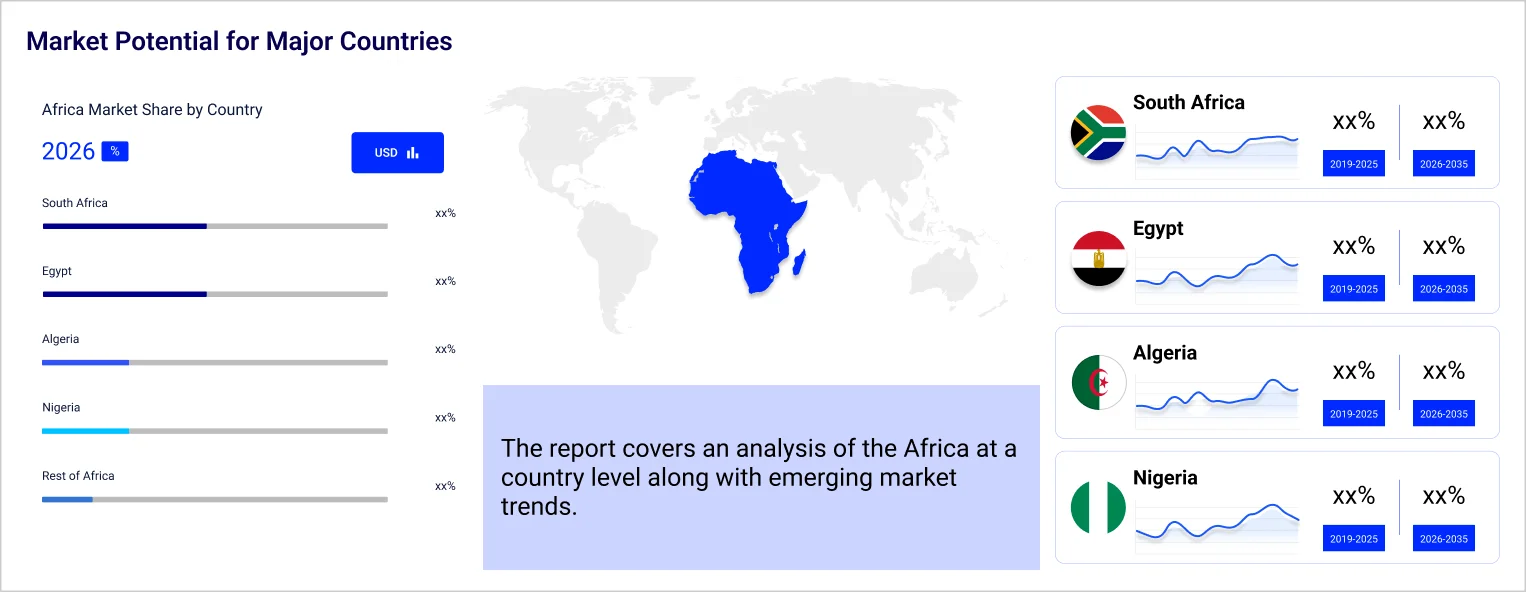

Market Breakup by Country

Key Insight: South Africa leads regional revenue thanks to a mature corporate L&D base, advanced fixed and mobile broadband, and well-funded private-school chains. Nigeria contributes the largest learner pool and an outsized share of public-school digitalisation spending, while Kenya is the most dynamic mobile-learning hub, anchored by Eneza Education's offline-friendly platform. Morocco and Tunisia drive Francophone and Arabic-language content demand, with Morocco's GENIE programme and Tunisia's e-school pilots underpinning curriculum digitalisation. Government-led tablet rollouts, donor co-financing through the World Bank and Mastercard Foundation, and rising private capital flows are the principal demand drivers across all five focus countries.

| CAGR 2026-2035 - Market by | Country |

| South Africa | 20.5% |

| Morocco | XX% |

| Nigeria | XX% |

| Tunisia | XX% |

| Kenya | XX% |

By Sector: K-12 holds the largest share of Africa's e-learning market, supported by the continent's youthful demographic and ministry-led digital schooling rollouts. Public-school systems in Nigeria, South Africa, and Kenya are major buyers of curriculum-aligned content and assessment platforms, with Via Afrika supplying digital textbooks across South Africa and Botswana. Corporate and Government Learning is the second-most material block, fuelled by financial services, telecoms, and energy employers shifting to cloud-LMS for distributed workforces. The 2024 Mastercard Foundation Demo Days across five African markets reinforced the buyer pipeline for K-12 and post-secondary platforms, while the AUDA-NEPAD EdTech 2030 Vision is expected to standardise procurement, further entrenching K-12's lead in the medium term.

By Product Type: Packaged Content holds the dominant share of product-type revenue, anchored by the procurement habits of education ministries and the long replacement cycles of digital textbooks and assessment libraries. Platforms are the fastest-rising segment as enterprises and universities migrate to cloud LMS, while Services capture localisation, integration, and analytics work. Docebo's expanding African enterprise pipeline and the launch of AI Creator and AI Video Presenter in April 2025 underline how platform vendors are upselling content-creation tools to existing customers. Via Afrika's Digital Education Academy continues to anchor packaged-content distribution in Southern Africa, supporting the segment's leadership across both K-12 and post-secondary buyers.

By Technology: Mobile Learning commands the largest technology share because smartphones are the dominant access device for African learners and remain affordable relative to laptops. Eneza Education's mobile-tutor platform, which has reached over 10 million offline users across Kenya, Ghana, Rwanda, and Côte d'Ivoire, exemplifies the format's reach into peri-urban and rural communities. LMS sits second in share but leads in revenue per institution, with Docebo, Moodle-based deployments, and African vendors such as Obami serving universities and corporates. Game- and simulation-based formats are growing fastest in healthcare and mining training, supported by employer demand for safer, scenario-based learning.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

South Africa: South Africa anchors the continent's e-learning revenue base, supported by a mature corporate L&D market in financial services, mining, and telecommunications, the deepest fixed and mobile broadband footprint in Sub-Saharan Africa, and a vibrant private-school sector. Via Afrika, established in 1949, dominates digital textbook and teacher-training distribution, while Docebo serves multinational employers headquartered in Johannesburg and Cape Town. The country's National Integrated ICT Policy White Paper and the National e-Learning Strategy provide the public-procurement spine, and provincial education departments are expanding curriculum-aligned content libraries. South Africa also hosts a disproportionate share of the continent's EdTech Demo Days and venture activity.

Nigeria: Nigeria is the continent's fastest-scaling national market, supported by a primary-school cohort exceeding 30 million learners, rapid smartphone adoption, and the National Policy on ICT in Education. Public-private partnerships are equipping classrooms with tablets and digital content, while companies including Tutor.ng, Eneza Education, and global LMS vendors are expanding their footprints. The Mastercard Foundation EdTech Fellowship's 2024 Demo Day in Nigeria deepened the local funding pipeline. Lagos and Abuja host most enterprise L&D spend, and the post-secondary market is being reshaped by digital nano-degrees and certificate programmes positioned to address persistent youth-unemployment challenges in services and ICT.

The Africa e-learning market remains moderately fragmented, with global LMS suppliers, regional content houses, and venture-funded EdTech start-ups competing across distinct buyer cohorts. Global vendors such as Docebo serve large multinational employers and pan-African universities, while regional incumbents such as Via Afrika hold strong franchise positions in school-curriculum content. Mobile-first specialists like Eneza Education compete on offline reach and vernacular content, leveraging USSD and lightweight Android delivery to penetrate rural and peri-urban communities.

Competitive priorities are shifting from coverage to differentiation: AI-driven content authoring, agentic learning assistants, and integrated assessment analytics are reshaping product roadmaps. Strategic partnerships with telecom operators, mobile-money providers, and ministries of education are central to scaling, while donor co-financing through the Mastercard Foundation and AUDA-NEPAD is increasingly decisive in winning public-sector tenders. Consolidation pressures are rising as global vendors seek anchor partnerships with regional content houses to deepen relevance and accelerate go-to-market across the five focus countries.

Founded in 2005 and headquartered in Toronto, Canada (with a strong Italian heritage), Docebo S.p.A. is a leading provider of AI-driven cloud-based learning platforms for enterprises. With a workforce of more than 800 employees, the company supports global and pan-African multinational customers across financial services, telecoms, and retail, and unveiled an AI-first roadmap (AI Creator, AI Video Presenter, Harmony) at Docebo Inspire 2025.

Established in 1949 and headquartered in South Africa, Via Afrika is a long-standing publisher and digital-learning provider serving South African and Botswanan schools and colleges. Its Via Afrika Digital Education Academy delivers approved teacher-training programmes alongside CAPS-aligned digital textbooks, study guides, and classroom resources, anchoring the company's leadership across Southern Africa's K-12 and post-secondary segments.

Founded in 2011 in Kenya by Chris Asego, Kago Kagichiri, and Toni Maraviglia, Eneza Education is a mobile-first EdTech firm focused on primary and secondary learners. Operating across Kenya, Ghana, Rwanda, and Côte d'Ivoire, the platform connects students, parents, and teachers through curriculum-aligned content delivered via SMS, USSD, and Android, and has reached over 10 million offline users.

Founded in 2008 and headquartered in Cape Town, South Africa, Obami is a social learning platform designed for schools, universities, and corporate clients. Featured in pan-African vendor mappings released in February 2025, the company's collaborative LMS, content marketplace, and analytics tools support blended-learning models across South Africa and broader Sub-Saharan Africa.

Other key players in the market are Tutor.ng, Dapt.io, Coursera Inc., edX (2U Inc.), Udemy Inc., Moodle Pty Ltd., Snapplify, GetSmarter (a 2U company), Cypher Learning, Instructure (Canvas), and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Discover the latest insights on the Africa E-Learning Market 2026 with our comprehensive report. Stay ahead of the curve with valuable data on platform innovations, technology adoption, and top growth countries. Whether you are launching a new learning platform or expanding into Sub-Saharan Africa, this report gives you the clarity you need. Download your free sample now and discover the key opportunities in the thriving Africa E-Learning industry.

Smart Education and Learning Market

Managed Learning Services Market

United States E-Learning Market

Europe Mobile E-learning Market

Self-Paced E-Learning Market

Asia E-Learning Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

At 2025, the market reached an approximate value of USD 4066.36 Million.

The market is projected to grow at a CAGR of 19.20% between 2026 and 2035.

The market is projected to grow significantly during the forecast period 2026 - 2035 to reach USD 23548.78 Million by 2035.

Growth is driven by surging smartphone and mobile-data adoption, ministry-led digital schooling programmes in South Africa, Nigeria, and Kenya, expanding corporate L&D budgets, donor co-financing via the Mastercard Foundation, the consolidation of continental policy under the AUDA-NEPAD EdTech 2030 Vision, and the integration of AI, simulation, and game-based formats into K-12 and post-secondary delivery.

K-12 holds the largest share of demand, supported by Africa's youthful demographic and ministry-led digital schooling rollouts. Corporate and Government Learning is the next-most material category and is expanding rapidly as enterprises shift to cloud LMS, while post-secondary growth is anchored by tertiary enrolment expansion and the rise of blended degrees and certificate programmes.

Key trends include the rapid roll-out of AI-first learning platforms (e.g., Docebo's April 2025 unveiling), the codification of a continental EdTech policy framework via the AUDA-NEPAD EdTech 2030 Vision, accelerating capital inflows that exceeded USD 1 billion to African tech startups in H1 2025, and the mainstreaming of mobile-first vocational learning across Kenya, Nigeria, and South Africa.

The key players in the market include Docebo S.p.A., Via Afrika, Eneza Education LTD., Obami, Tutor.ng, Dapt.io, and other global LMS vendors such as Coursera, edX, Udemy, and Moodle.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Sector |

|

| Breakup by Product Type |

|

| Breakup by Technology |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.