Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

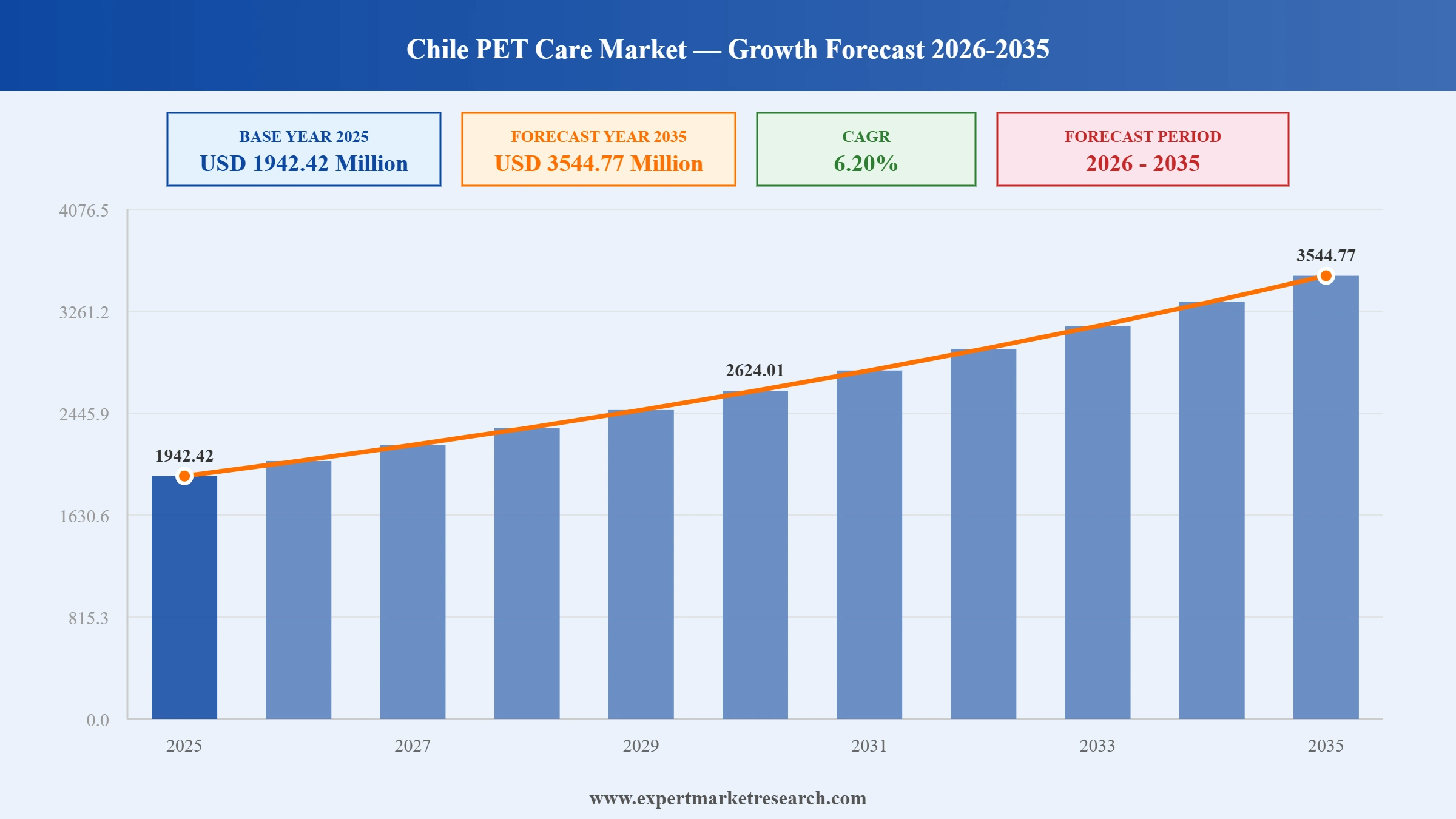

The Chile pet care market reached a value of USD 1942.42 Million at 2025 and is projected to expand at a CAGR of around 6.20% during the forecast period of 2026-2035. With the deepening humanisation of pets driving demand for premium and super-premium food products, Law 21020 on Responsible Pet Ownership increasing pet retention and lifetime spending, accelerating e-commerce adoption expanding accessibility of specialised pet care products, and growing disposable incomes enabling higher per-pet expenditure, the market is expected to reach USD 3544.77 Million by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Chile pet care market is being shaped by a powerful convergence of cultural, regulatory, and commercial forces. Pet humanisation is pushing spending beyond basic nutrition into premium food, functional supplements, and professional grooming, while Law 21020 has structurally anchored pet ownership by making abandonment legally and financially costly. E-commerce platforms and veterinary retail channels are deepening product accessibility across Chilean cities, accelerating premiumisation across all major product categories.

Mars Incorporated expanded its Pedigree and Whiskas premium product ranges available through Chilean retail in 2025, introducing new functional nutrition formulations targeting digestive health and joint care for adult dogs and cats. The expansion reflects growing Chilean consumer willingness to purchase science-backed premium pet food, reinforcing the Chile pet care market's upward premiumisation trajectory.

Nestlé Purina expanded its ProPlan Veterinary Diets range distribution across veterinary clinics in Chile in 2025, responding to growing demand for prescription-grade nutritional management for pets with chronic health conditions. The veterinary channel expansion directly supports the Chile pet care market's growing Pet Nutrition segment as pet owners invest more in clinical-grade dietary management.

Empresas Carozzi, Chile's leading domestic pet food manufacturer, extended its Masterdog line in 2024 with new grain-free and high-protein formulations targeting health-conscious Chilean dog owners. The product development reflects the domestically competitive response to rising imported premium brand presence within the Chile pet care market's dog food segment.

Chilean online pet care retailers reported year-on-year sales growth of approximately 35% in 2024, driven by expanding home delivery coverage, subscription-based pet food services, and growing consumer comfort with digital pet product purchasing. The growth demonstrates the accelerating shift in distribution dynamics within the Chile pet care market toward digital channels.

Pet humanisation is the dominant structural demand driver in the Chile pet care market, with approximately 12.5 million dogs and cats in Chilean households being treated as family members. This emotional bond is directly translating into higher spending on premium pet food, functional supplements, and grooming products across urban Chilean households.

Chile's Law 21020 on Responsible Pet and Companion Animal Ownership, in full force since February 2019, has made abandonment legally and financially costly, structurally increasing pet retention rates. Higher retention translates directly into longer lifetime pet care spending relationships, sustaining the Chile pet care market's growth trajectory through the forecast period.

The Agriculture and Livestock Service registered 147 new imported premium pet food products in Chile in 2021 alone, confirming accelerating premiumisation within the Chile pet care market. Chilean pet owners increasingly seek grain-free, high-protein, and breed-specific formulations, with super-premium and veterinary diet categories growing fastest within the Pet Food and Pet Nutrition segments.

Chile imported USD 417 million worth of animal food in 2022, ranking as the 32nd largest importer globally, with Argentina, the United States, China, Brazil, and the Netherlands as primary sourcing origins. Import growth confirms that domestic production capacity in the Chile pet care market is being supplemented by international premium brands to meet rising consumer demand.

E-commerce is rapidly transforming the distribution landscape of the Chile pet care market, with online retailers offering subscription-based pet food delivery, personalised product recommendation tools, and same-day delivery in major cities. Rising smartphone penetration and Chilean consumers' growing digital retail comfort are accelerating online channel share gains across all pet care product categories.

“Chile Pet Care Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

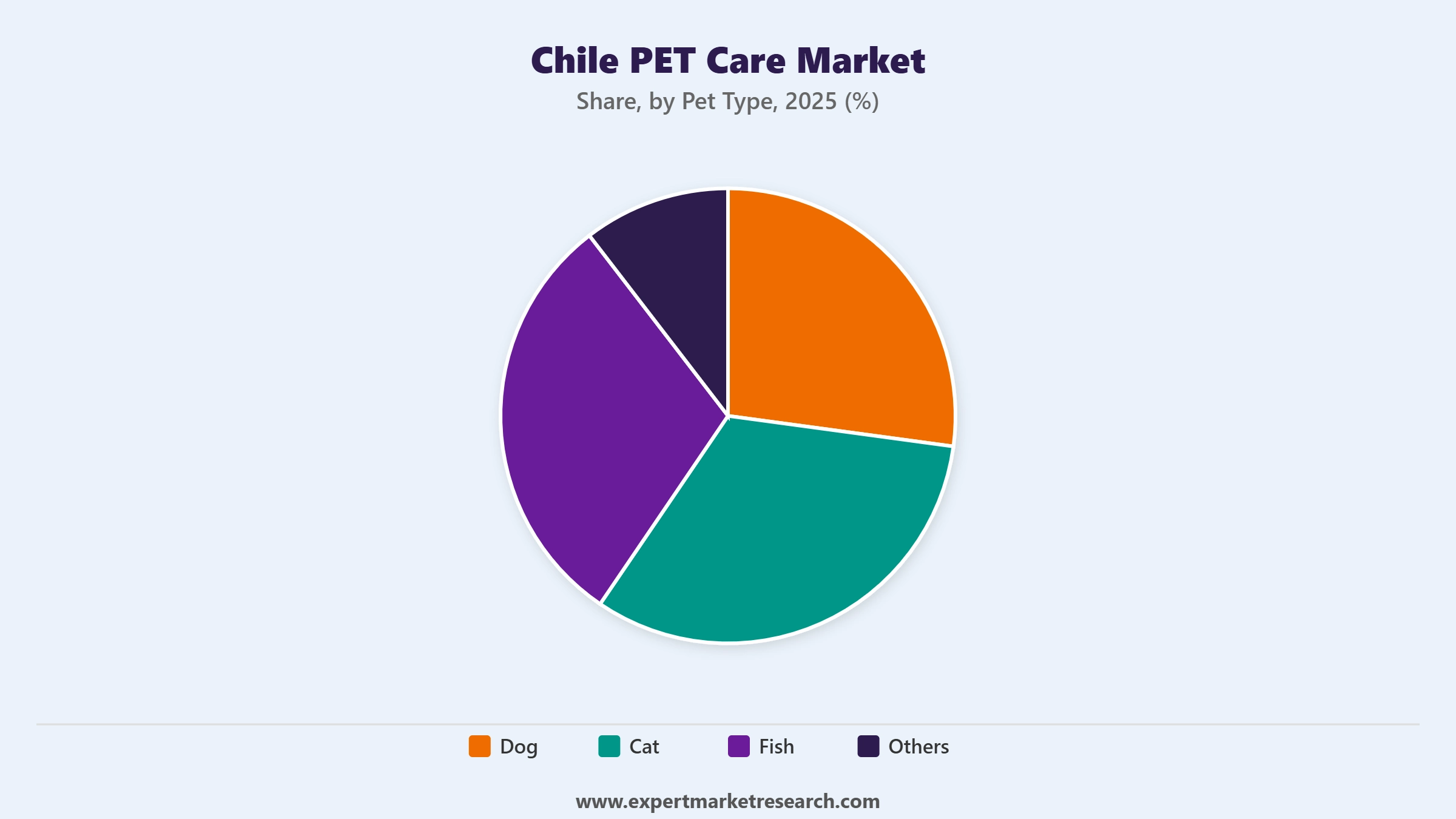

Market Breakup by Pet Type

Key Insight: Dogs hold the dominant share of the Chile pet care market by pet type, underpinned by Chile's deeply embedded dog ownership culture and an estimated population of over 8 million dogs across Chilean households. Dogs generate the highest per-animal spending across food, grooming, and veterinary nutrition categories. Cats represent the fastest-growing pet type segment, driven by urbanisation favouring smaller companion animals and rising awareness of premium cat nutrition and grooming products in Chilean retail and veterinary channels.

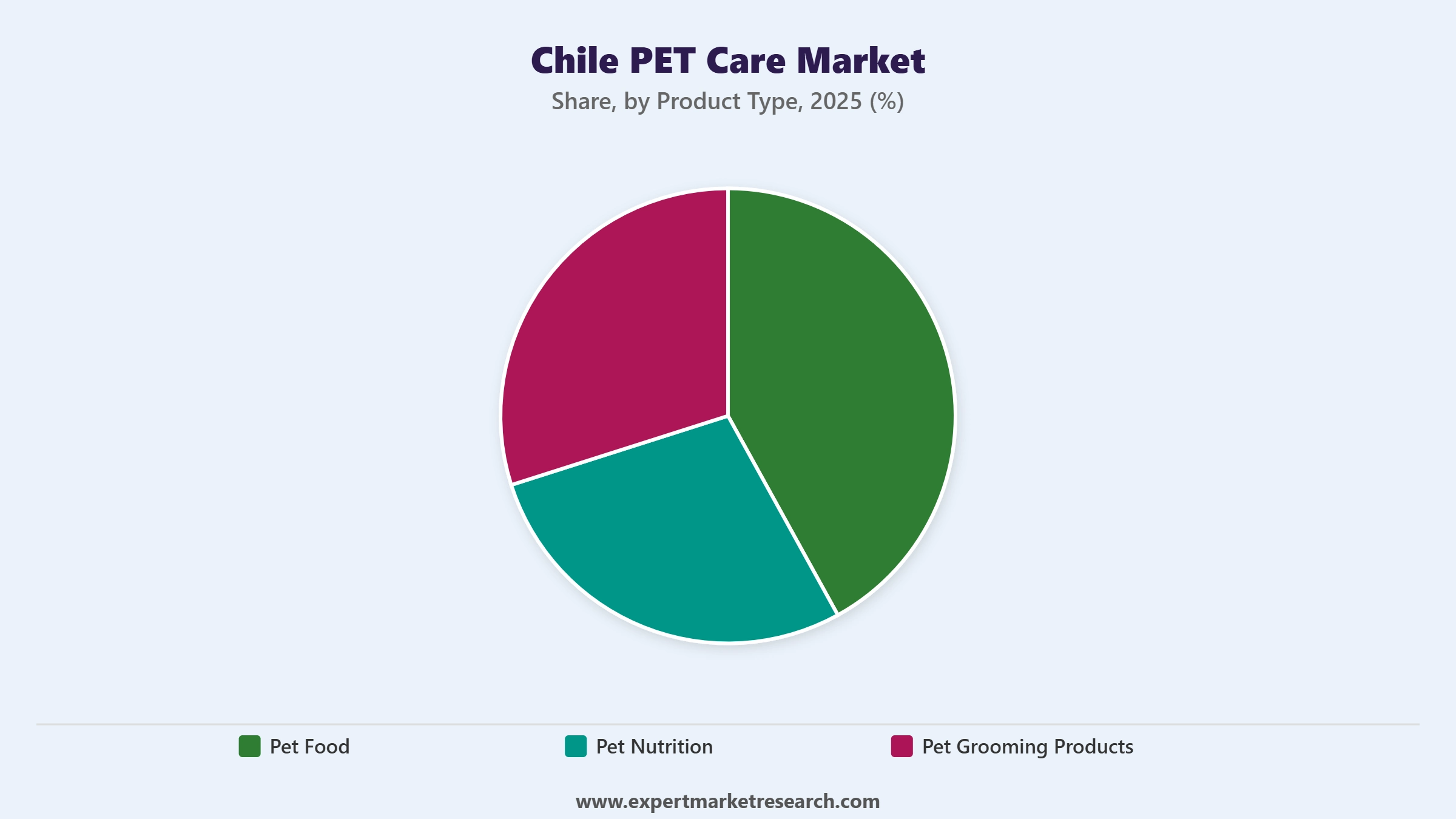

Market Breakup by Product Type

Key Insight: Pet Food holds the dominant share of the Chile pet care market by product type, driven by daily necessity consumption and the ongoing premiumisation from standard to premium and super-premium formulations. Chile imported USD 450 million of animal feed in 2021, representing a 69.9% increase from 2020, confirming strong underlying demand growth. Pet Nutrition is the fastest-growing product type, driven by growing veterinary recommendation of dietary supplements, oral care, and prescription veterinary diets for dogs and cats across Chilean clinical settings.

Market Breakup by Distribution Channel

Key Insight: Supermarkets and Hypermarkets hold the largest distribution channel share of the Chile pet care market, serving as the primary purchase point for mainstream pet food brands and grooming products due to high consumer footfall and competitive pricing. Online Retailers represent the fastest-growing channel, with year-on-year sales growth of approximately 35% reported in 2024. Veterinary Clinic and Pet Medical Shops are gaining share as pet owners seek professional guidance on premium nutrition and health supplement purchasing decisions.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Pet Type, Dog dominates the market due to Chile's deeply embedded dog ownership culture and high per-animal spending

Dogs hold the dominant share of the Chile pet care market because dog ownership is deeply embedded in Chilean household culture, with an estimated population exceeding 8 million dogs nationally. Dogs generate disproportionately high per-animal spending across food, grooming, and veterinary nutrition categories relative to other pet types. The combination of Law 21020's pet retention effect and the emotional intensification of the human-dog bond is sustaining above-average lifetime spending growth within the segment through the forecast period.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Cats represent the fastest-growing pet type segment in the Chile pet care market, driven by urbanisation creating practical preference for smaller companion animals in apartments and urban residences. Rising awareness of premium cat-specific nutrition, cat litter quality, and feline dental health products is translating into elevated per-cat spending among younger urban Chilean pet owners. The cat segment is experiencing particularly strong growth in treats, wet food, and specialised dietary supplement categories, with premium cat food showing some of the highest value growth rates within the overall market.

By Product Type, Pet Food accounts for the dominant share of the market due to daily necessity consumption and accelerating premiumisation

Pet Food holds the dominant share of the Chile pet care market because it is a daily necessity generating consistent, recurring purchase behaviour across all pet types. The structural growth driver beyond baseline volume consumption is premiumisation: Chilean pet owners are progressively upgrading from standard to premium and super-premium formulations as disposable income rises and pet humanisation deepens. The Agriculture and Livestock Service's registration of 147 new imported premium products in 2021 alone confirms the pace of supply-side response to this premium demand shift.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Pet Nutrition is the fastest-growing product type in the Chile pet care market, driven by veterinary recommendation of dietary supplements, oral care products, and prescription veterinary diets as part of comprehensive pet health management programmes. Growing awareness of pet-specific health conditions including dental disease, joint deterioration, and digestive disorders is creating new consumer demand for functional nutrition products beyond standard food categories. Pet Grooming Products are growing steadily as professional grooming culture expands among urban Chilean dog and cat owners investing in home grooming equipment.

By Distribution Channel, Supermarkets and Hypermarkets account for the dominant share of the market due to high consumer footfall and mainstream product accessibility

Supermarkets and Hypermarkets retain the dominant distribution channel share of the Chile pet care market by virtue of their role as the primary weekly shopping destination for mainstream Chilean households. The channel's breadth of coverage across Chilean cities and its competitive pricing on standard and mainstream premium pet food brands make it the default purchase point for the majority of pet owners. Major national supermarket chains stock a comprehensive range of domestic and imported pet food brands, providing reliable distribution coverage for both leading domestic brands and international labels.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Online Retailers represent the fastest-growing distribution channel in the Chile pet care market, with year-on-year sales growth of approximately 35% in 2024 driven by subscription-based pet food delivery services, expanding home delivery logistics coverage, and increasing Chilean consumer comfort with digital purchasing. The online channel is particularly strong for premium and super-premium products that are not always available in nearby physical retail, as well as for veterinary diet products requiring professional guidance integrated into digital shopping platforms. Pet Stores are growing their share as curated specialty retail destinations offering premium brands and personalised pet owner advisory services.

The Chile pet care market's competitive landscape is defined by a mix of domestically rooted Chilean food conglomerates with dedicated pet food divisions, specialised local pet nutrition and veterinary retail operators, and leading global pet care multinationals distributing their international premium brands through Chilean retail and veterinary channels. Domestic players hold strong positions in standard and accessible premium segments through established distribution networks and brand recognition built over decades, while international brands compete in the premium and super-premium tiers.

Key players are differentiating through product premiumisation, veterinary channel partnerships, and e-commerce capability development to capture the growing segment of health-conscious Chilean pet owners. The competitive intensity is increasing as both domestic manufacturers and international importers target the premiumisation opportunity created by rising disposable incomes and deepening pet humanisation. Import volumes and the registration of new premium products confirm a sustained influx of international competition that domestic players are actively responding to with their own product development programmes.

Empresas Carozzi SA is one of Chile's leading food conglomerates and a dominant domestic force in the Chile pet care market through its Masterdog and Mastercat pet food brands, which hold strong market recognition among Chilean pet owners across standard and accessible premium tiers. The company extended its Masterdog range with new grain-free and high-protein formulations in 2024, responding to growing consumer health consciousness. Carozzi's established distribution network across Chilean supermarkets, hypermarkets, and independent retailers provides significant commercial reach.

Empresas Iansa S.A. is a major Chilean agri-food company with a significant presence in the domestic pet food segment, producing and distributing pet nutrition products targeted at the mass market across Chile. The company leverages its established agricultural supply chain and domestic raw material relationships to maintain competitive cost positions in the Chile pet care market's standard food tier. Iansa's distribution network across Chilean retail formats provides consistent accessibility for its pet food portfolio across urban and rural consumer segments.

Proa Sociedad Anónima is a Chilean company operating in the pet care sector with a focused portfolio of pet nutrition and pet food products distributed across domestic retail and veterinary channels. The company serves the growing segment of Chilean pet owners seeking domestically produced alternatives to imported brands, positioning its products on quality and local production credentials within the Chile pet care market. Proa's operations reflect the expanding domestic manufacturing base developing to meet rising Chilean pet care product demand.

Centro Veterinario Y Agrícola Limitada is a Chilean company operating at the intersection of veterinary services and agricultural supply, providing veterinary care products, dietary supplements, and professional pet care supplies to veterinary clinics and agricultural clients across Chile. The company's positioning in the Veterinary Clinic and Pet Medical Shops distribution channel makes it a relevant participant in the Chile pet care market's growing Pet Nutrition segment, where veterinary recommendation increasingly drives purchasing decisions.

Other key players in the market are Nestlé S.A., Mars, Incorporated, and others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock the full potential of the Chile pet care market with our comprehensive 2026 market report. Whether you are an international pet food manufacturer evaluating Chilean market entry, a domestic producer benchmarking competitive positioning, or an investor assessing Latin American pet care sector exposure, this report delivers the intelligence you need. Download your free sample today and explore the growth opportunities shaping Chile's dynamic and fast-evolving pet care landscape.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The Chile pet care market attained a value of USD 1942.42 Million in 2025.

The market is estimated to grow at a CAGR of 6.20% during 2026-2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach a value of USD 3544.77 Million by 2035.

The different pet types include dogs, cats, fish, and others.

The major distribution channels include supermarkets and hypermarkets, pet stores, veterinary clinic and pet medical shops, online retailers, and others.

The key market drivers include the increasing trend of pet humanization, the rising availability of pet care products through e-commerce channels, and the increasing adoption of pets in Chilean households.

The key players in the market include Empresas Carozzi SA, Empresas Iansa S.A., Proa Sociedad Anónima, Centro Veterinario Y Agrícola Limitada, Nestlé S.A., and Mars, Incorporated, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Pet Type |

|

| Breakup by Product Type |

|

| Breakup by Distribution Channels |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.