Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

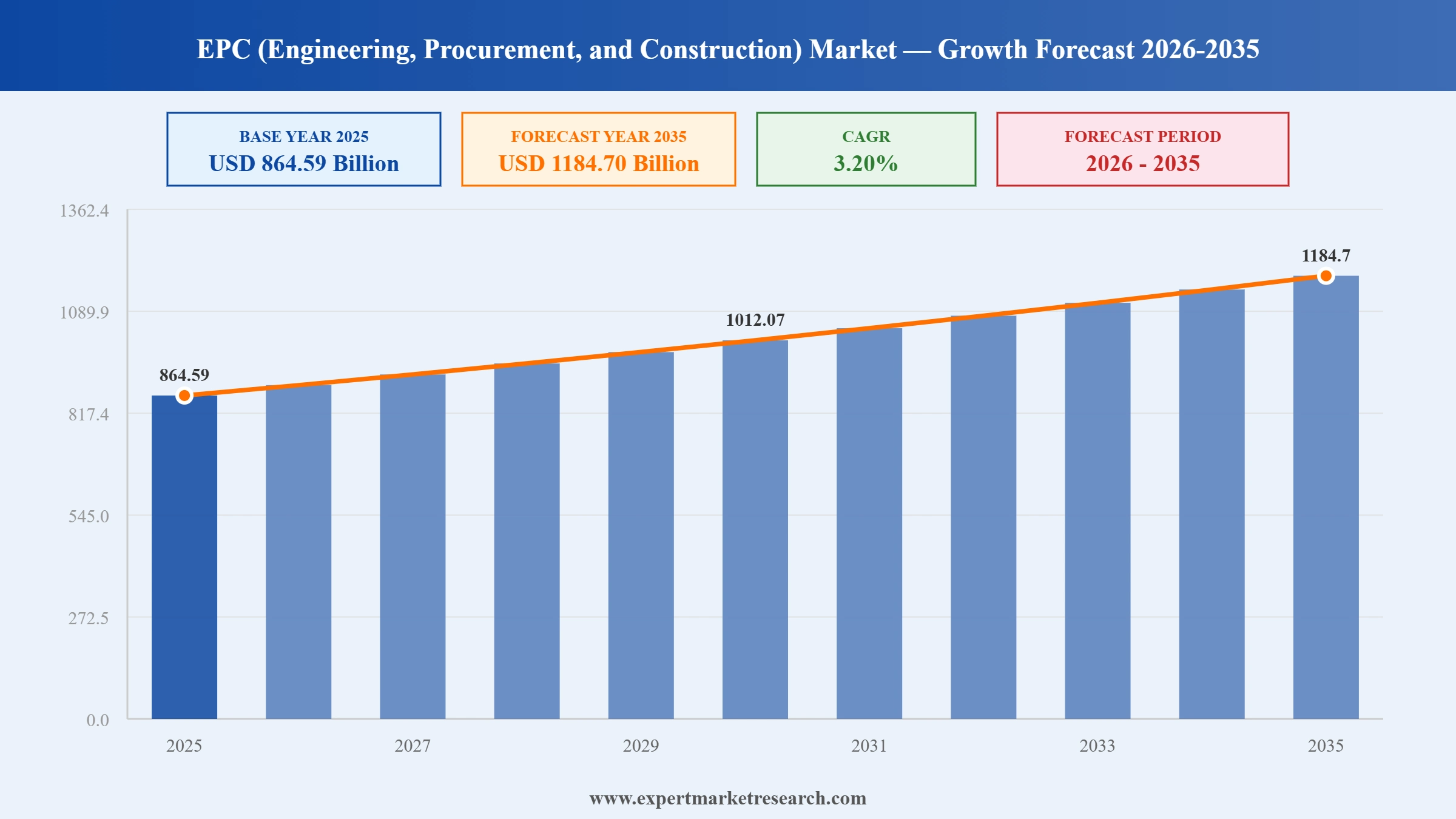

The EPC (engineering, procurement, and construction) market reached a value of USD 864.59 Billion at 2025 and is projected to expand at a CAGR of around 3.20% during the forecast period of 2026-2035. With rising global infrastructure investment, growing demand for integrated turnkey project delivery, accelerating energy transition spending, and expanding industrialisation in emerging economies, the market is expected to reach USD 1184.70 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Global EPC (Engineering, Procurement, and Construction) Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 864.59 |

| Market Size 2035 | USD Billion | 1184.70 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 3.20% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 4.1% |

| CAGR 2026-2035 - Market by Country | India | 6.8% |

| CAGR 2026-2035 - Market by Country | Saudi Arabia | 3.6% |

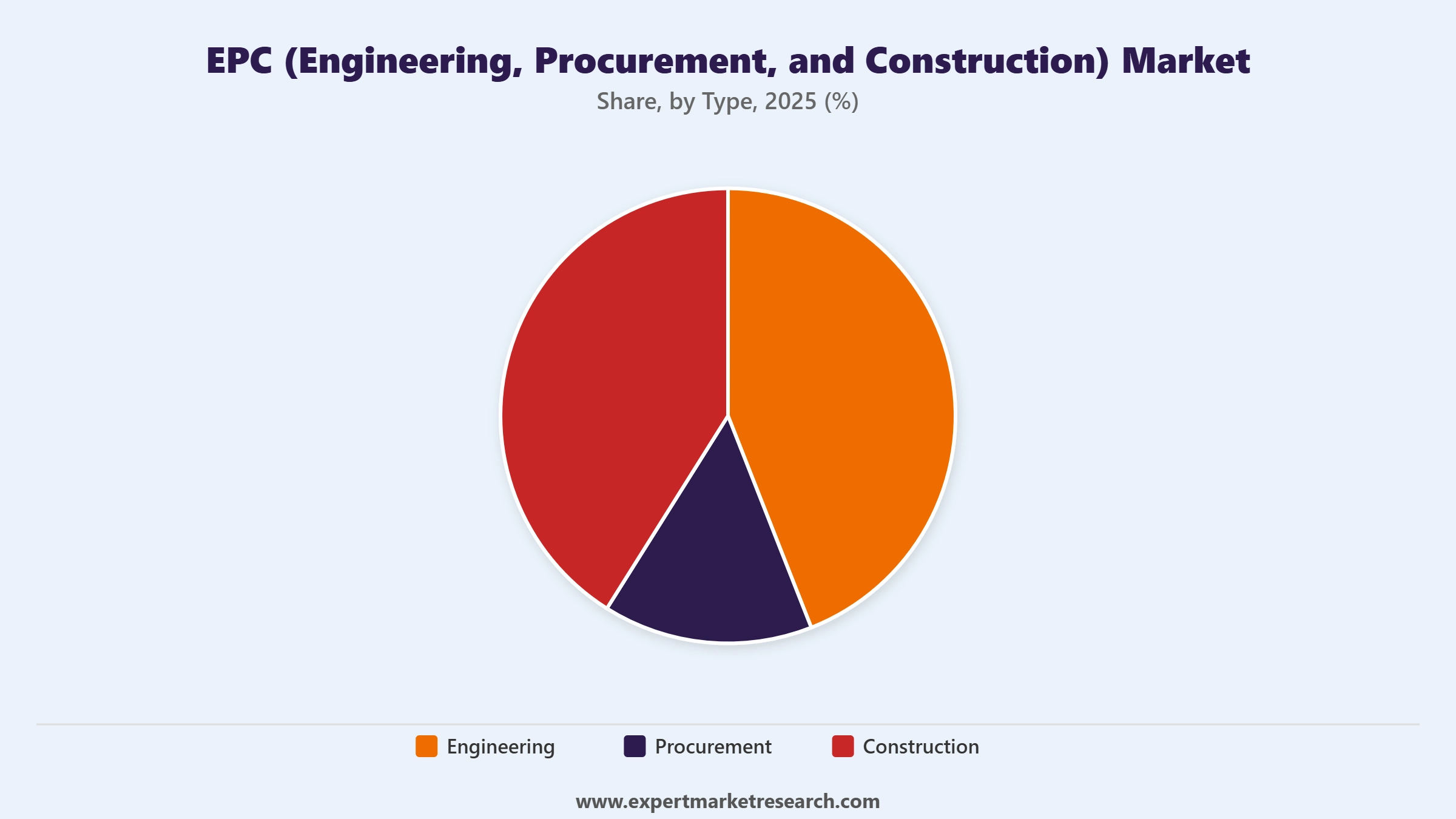

| CAGR 2026-2035 - Market by Type | Construction | 3.6% |

| CAGR 2026-2035 - Market by Drive Type | Power | 3.3% |

| Market Share by Country 2025 | Italy | 2.7% |

The EPC (engineering, procurement, and construction) market is undergoing a significant structural evolution, as energy transition mandates, digital project delivery tools, and large-scale industrial buildouts reshape contract structures and award volumes. Companies are broadening their service scope beyond traditional oil and gas into renewables, pharmaceuticals, and data infrastructure. These shifts are intensifying competition among global EPC contractors while simultaneously creating demand for more integrated, technology-driven project delivery models.

Industry reports in January 2026 confirmed LNG Canada, Fluor's British Columbia development, exceeded 70% completion with first LNG cargo expected mid-2026. The 14 MTPA, two-train project represents one of Canada's largest-ever energy infrastructure builds, delivered under a fully integrated EPC model.

In July 2025, Saipem and Subsea7 signed a binding merger agreement to create Saipem7, a combined global energy services leader. The deal targets annual free cash flow exceeding EUR 800 million and EUR 300 million in projected cost synergies within three years of completion.

Fluor executed an EPCM services contract in April 2025 for a multi-billion-dollar pharmaceutical manufacturing facility in Lebanon, Indiana. The project expands Fluor's presence in the life sciences sector, reflecting the broadening scope of EPC services into advanced manufacturing beyond energy and infrastructure.

Larsen and Toubro announced in February 2025 a major refinery upgrade EPC contract with Indian Oil Corporation, reinforcing India's growing domestic EPC capacity and reflecting the scale of refinery capital expenditure investment across the Asia Pacific region.

Renewable energy is reshaping the engineering, procurement, and construction market, with solar, wind, and green hydrogen projects driving new contract volumes globally. In 2023, renewable EPC contracts represented over 34% of total EPC market value, driven by government clean energy spending mandates.

Digital twin technology and AI are improving project delivery across the EPC market. In February 2024, Fluor Corporation partnered with Microsoft to co-develop AI-based EPC planning tools, now piloted across more than 20 infrastructure projects globally to boost execution efficiency.

Oil and gas holds the largest application share in the engineering, procurement, and construction market. In August 2024, Bechtel signed a fixed-price EPC contract with Sempra Infrastructure for Port Arthur LNG Phase 2, a US Gulf Coast LNG export facility.

Asia Pacific is the fastest-growing EPC market growth region, fuelled by urbanisation and infrastructure investment across China, India, and Southeast Asia. In October 2024, China launched a renewable energy plan targeting 5 billion tons of coal equivalent by 2030, creating new EPC demand.

Modular construction is gaining significant traction in the EPC (engineering, procurement, and construction) sector, reducing on-site time and improving quality control. Adoption has grown by approximately 33% across EPC companies, with oil and gas, power, and industrial facility projects integrating prefabrication to compress schedules and lower overall risk.

The report of Expert Market Research's titled "EPC (Engineering, Procurement, and Construction) Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

Market Breakup by Type

Key Insight: The construction segment holds the dominant share of the EPC (engineering, procurement, and construction) market by type, driven by massive global demand for new infrastructure, industrial plants, power facilities, and transportation networks. As governments and private investors fast-track infrastructure programmes, particularly in energy and transport, construction-phase EPC contracts command the highest spend intensity and longest project durations. The engineering sub-segment is also expanding steadily as the complexity of modern projects, including offshore energy and smart infrastructure, demands sophisticated front-end design and specialist expertise from EPC contractors.

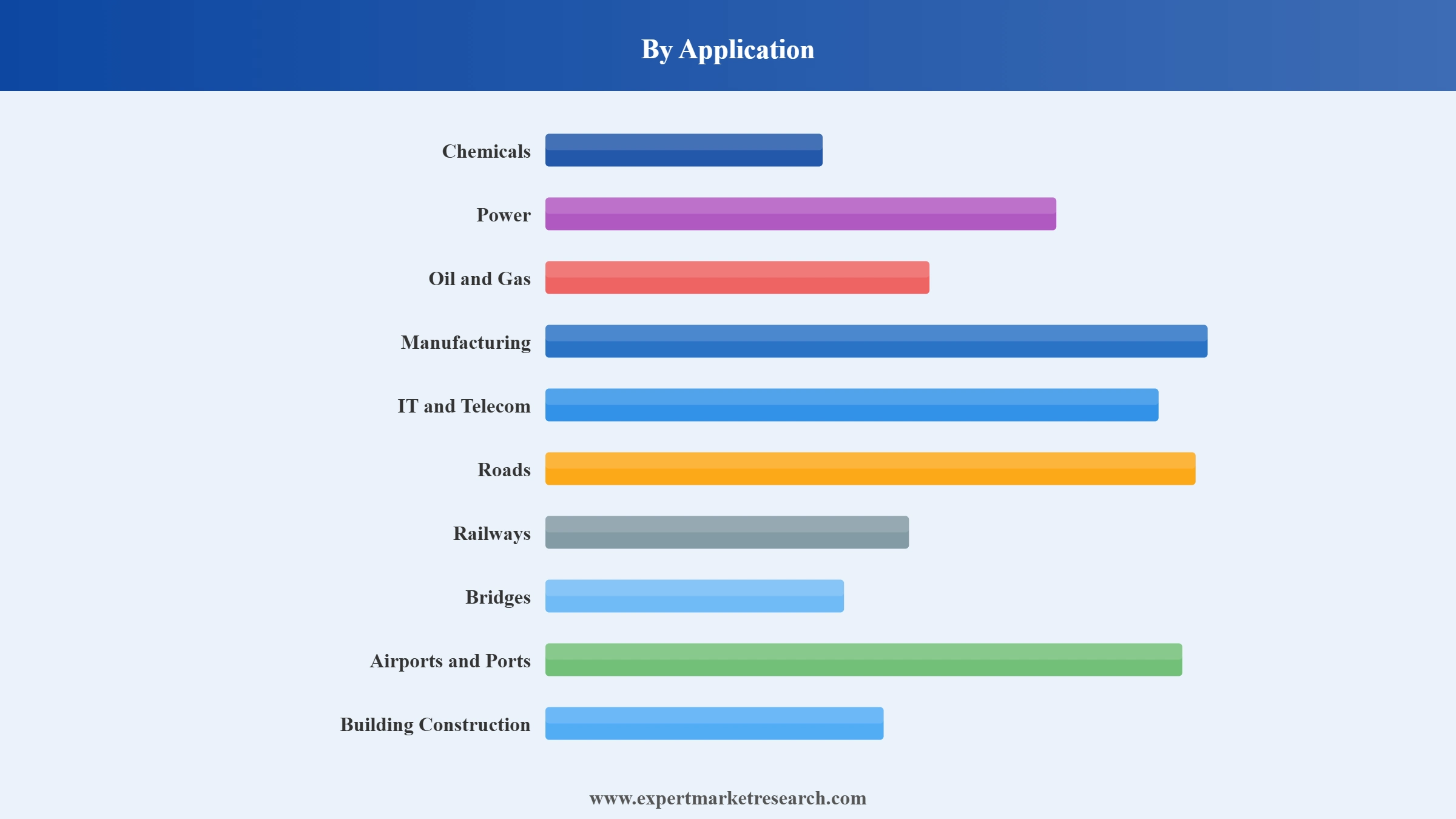

Market Breakup by Application

Key Insight: Oil and gas retains the dominant application share in the EPC market, commanding approximately 36% of global revenues, driven by sustained upstream and downstream investment in production platforms, refineries, LNG terminals, and pipeline infrastructure. Power is the second-largest application, accelerated by the global shift toward renewable energy and the need to modernise ageing grid infrastructure. Roads, railways, and bridges are gaining share as governments prioritise surface transport connectivity. Building construction and IT and telecom are emerging as faster-growing segments, supported by urbanisation trends and expanding digital infrastructure needs globally.

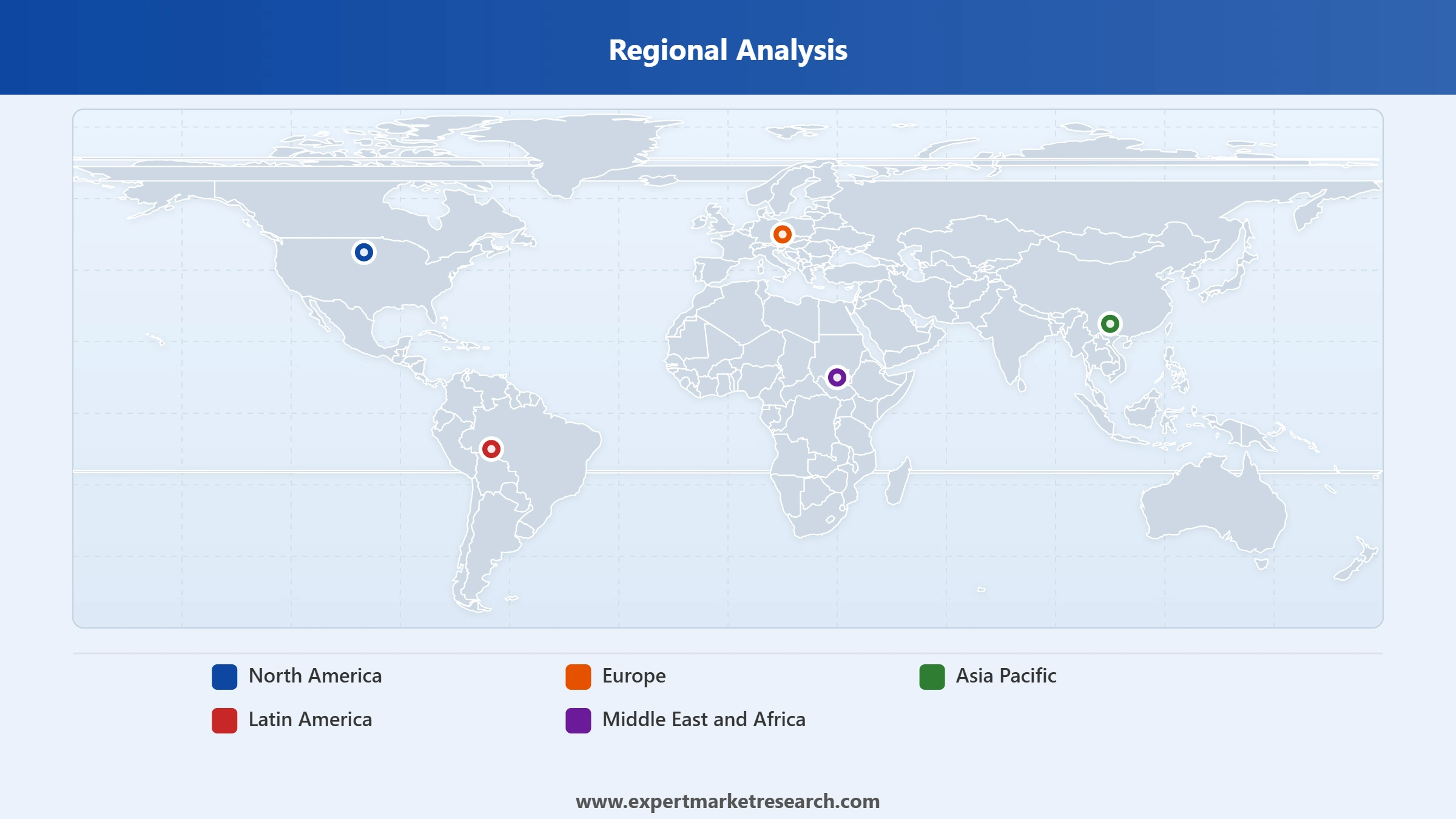

Market Breakup by Region

Key Insight: North America holds the largest regional share of the EPC market, driven by significant investment in energy infrastructure, industrial manufacturing, and technology-led construction under the US Infrastructure Investment and Jobs Act, which allocated USD 1.2 trillion to rebuilding roads, bridges, and energy grids. Asia Pacific is the fastest-growing region, powered by China, India, and Southeast Asia's infrastructure buildouts and renewable energy programmes. Europe is advancing through Green Deal-linked EPC activity, while the Middle East and Africa represent expanding frontiers for large-scale energy and industrial EPC contracts.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Type, construction dominates the market due to high project spend intensity and global infrastructure demand

The construction segment leads the EPC (engineering, procurement, and construction) market by type, reflecting the capital-intensive nature of physical project execution across energy, transport, and industrial applications. Construction accounts for the highest cost share of any EPC contract, covering civil works, structural fabrication, equipment installation, and commissioning. Governments across Asia Pacific, the Middle East, and North America have significantly expanded public infrastructure budgets, generating a robust pipeline of EPC construction contracts in roads, energy facilities, and industrial plants.

The engineering sub-segment is expanding steadily within the EPC market as project complexity increases. Front-end engineering design, technical feasibility studies, and detailed engineering are critical enablers of successful project execution, particularly for offshore energy, chemical plants, and advanced manufacturing facilities. In June 2024, Fluor secured an engineering services contract for Phase One of Northvolt's EUR 4.5 billion lithium-ion battery facility in Heide, Germany, illustrating the growing demand for specialist engineering capabilities within large-scale industrial EPC programmes.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Application, oil and gas accounts for the dominant share of the market due to sustained upstream and downstream capital investment

Oil and gas commands the largest application segment of the engineering, procurement, and construction market, driven by continuous capital investment in production facilities, LNG terminals, refineries, and pipeline infrastructure across the Middle East, North America, and Asia Pacific. Offshore oil and gas EPC contract awards are anticipated to reach USD 54 billion in 2025, reflecting sustained demand for energy infrastructure despite the growing energy transition. EPC contractors serving this sector benefit from long contract durations, large ticket sizes, and complex, multi-disciplinary project scopes.

The power application segment is growing rapidly within the EPC market, fuelled by global investment in renewable energy infrastructure including solar, wind, hydropower, and green hydrogen. Governments and private investors are channelling capital into large-scale power EPC contracts to meet net-zero commitments and address energy demand growth. Building construction and IT and telecom are also gaining momentum as urbanisation and digital infrastructure expansion drive demand for integrated project delivery models. In October 2024, China launched a comprehensive renewable energy plan targeting consumption of 5 billion tons of coal equivalent by 2030, generating a vast new EPC pipeline.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America dominates the market due to large-scale energy, industrial, and infrastructure investment

North America holds the largest share of the EPC (engineering, procurement, and construction) market, underpinned by substantial public and private investment in energy, transport, and industrial infrastructure. The US Infrastructure Investment and Jobs Act, which directed USD 1.2 trillion toward roads, bridges, and energy grid modernisation, has generated a sustained pipeline of EPC opportunities. The United States accounts for the largest national share, with Bechtel, Fluor, and Quanta Services among the region's most active contractors. Canada is also a significant contributor, anchored by major LNG and hydrocarbon infrastructure programmes in British Columbia and Alberta.

Asia Pacific is the fastest-growing regional market for engineering, procurement, and construction services, driven by rapid urbanisation, expanding middle-class populations, and large-scale government infrastructure investment across China, India, and Southeast Asia. China's focus on renewable energy and high-speed rail projects, alongside India's highway expansion and power sector investment, are generating consistent EPC award volumes. In October 2024, China launched a renewable energy plan targeting 5 billion tons of coal equivalent by 2030, while India added 24 GW of new renewable capacity in 2024, both fuelling strong EPC demand across the region.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The EPC (engineering, procurement, and construction) market is moderately fragmented, with a mix of large global contractors and regional specialists competing across energy, infrastructure, and industrial sectors. The top ten EPC players collectively dominate around 46% of global contract value, with competitive advantage driven by technical expertise, financial strength, geographic presence, and the ability to manage complex multi-disciplinary projects at scale. Mergers, acquisitions, and strategic partnerships are increasingly being used to build broader capabilities and expand into new geographies.

EPC contractors are increasingly investing in digital project delivery tools, AI-based engineering design, and modular construction techniques to differentiate themselves and improve margins in a market where cost overruns and schedule delays remain persistent challenges. Sustainability and decarbonisation capabilities are also becoming key differentiators as clients accelerate clean energy infrastructure buildouts and demand EPC partners with proven experience in renewable energy, green hydrogen, and carbon-capture projects.

Bechtel Corporation, founded in 1898 and headquartered in Reston, Virginia, United States, is one of the world's most influential EPC contractors with a presence across more than 40 countries. The company delivers large-scale projects in energy, infrastructure, mining, and nuclear sectors, leveraging deep engineering expertise and a track record spanning over a century of complex project execution. Bechtel's recent portfolio includes the Port Arthur LNG Phase 2 contract with Sempra Infrastructure and multiple renewable energy developments.

Fluor Corporation, founded in 1912 and headquartered in Irving, Texas, United States, is a global EPC and project management company serving energy, chemicals, mining, infrastructure, and government sectors. The company is known for managing complex, large-scale projects worldwide through integrated engineering, procurement, and construction capabilities. Fluor's active project portfolio includes the LNG Canada development in British Columbia and pharmaceutical manufacturing facilities in the United States, reflecting its growing sector diversification.

Larsen and Toubro Limited, founded in 1938 and headquartered in Mumbai, India, is a leading multinational EPC conglomerate with operations spanning construction, engineering, manufacturing, technology, and financial services. L&T's engineering and construction division is among the largest in India, delivering end-to-end EPC solutions in infrastructure, power, oil and gas, and defence. The company has been selected as EPC contractor for a gigascale solar project in Abu Dhabi, underscoring its international EPC capabilities.

Mitsubishi Heavy Industries, founded in 1884 and headquartered in Tokyo, Japan, is a global industrial manufacturer and EPC contractor operating across energy, defence, transportation, and infrastructure sectors. The company delivers complex EPC projects in power generation, LNG, offshore energy, and industrial plant construction, combining advanced engineering with manufacturing integration. MHI has a strong Asia Pacific presence and is actively investing in decarbonisation technologies including carbon capture, hydrogen, and ammonia-fuelled power generation projects.

Other key players in the market are McDermott International Ltd., Saipem S.p.A., DEPCOM Power Inc., Petrofac Limited, Blue Ridge Power, Blattner Energy Inc., John Wood Group PLC, Quanta Services Inc., The Shaw Group Inc., Sentry Electrical Group Inc., Sinopec Engineering (Group) Co. Ltd., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Stay ahead in the EPC (engineering, procurement, and construction) market 2026 with our comprehensive research report. From the latest contract awards and technology adoption trends to regional growth hotspots and competitive dynamics, this report equips you with the clarity to make decisive strategic moves. Whether you are entering a new market, evaluating a partnership, or benchmarking against top global EPC contractors, download your free sample today and unlock the opportunities shaping the future of engineering and construction.

Australia Power EPC Market

North America Power EPC Market

United States Power EPC Market

Vietnam Power EPC Market

Philippines Power EPC Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The EPC (engineering, procurement, and construction) market was valued at USD 864.59 Billion in 2025.

The market is projected to grow at a CAGR of 3.20% between 2026 and 2035.

The revenue generated from the EPC (engineering, procurement, and construction) market is expected to reach USD 1184.70 Billion in 2035.

The market is categorised according to the type, which includes engineering, procurement, and construction.

The market key players are Fluor Corporation, Larsen & Toubro Limited, Saipem SpA, Mitsubishi Heavy Industries, Ltd., John Wood Group plc, McDermott International Ltd., Bechtel Corporation, DEPCOM Power, Inc., Petrofac Limited, Blue Ridge Power, Blattner Energy Inc., Quanta Services, Inc., The Shaw Group Inc., Sentry Electrical Group, Inc., and Sinopec Engineering (Group) Co., Ltd., among others.

Based on the application, the market is divided into chemicals, power, oil and gas, manufacturing, it and telecom, roads, railways, and bridges, airports, and ports, building construction, and others.

The market is broken down into North America, Europe, Asia Pacific, Latin America Middle East, and Africa.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.